Financial Planning Case Study: Analyzing the Smith Family's Finances

VerifiedAdded on 2023/05/29

|9

|1425

|498

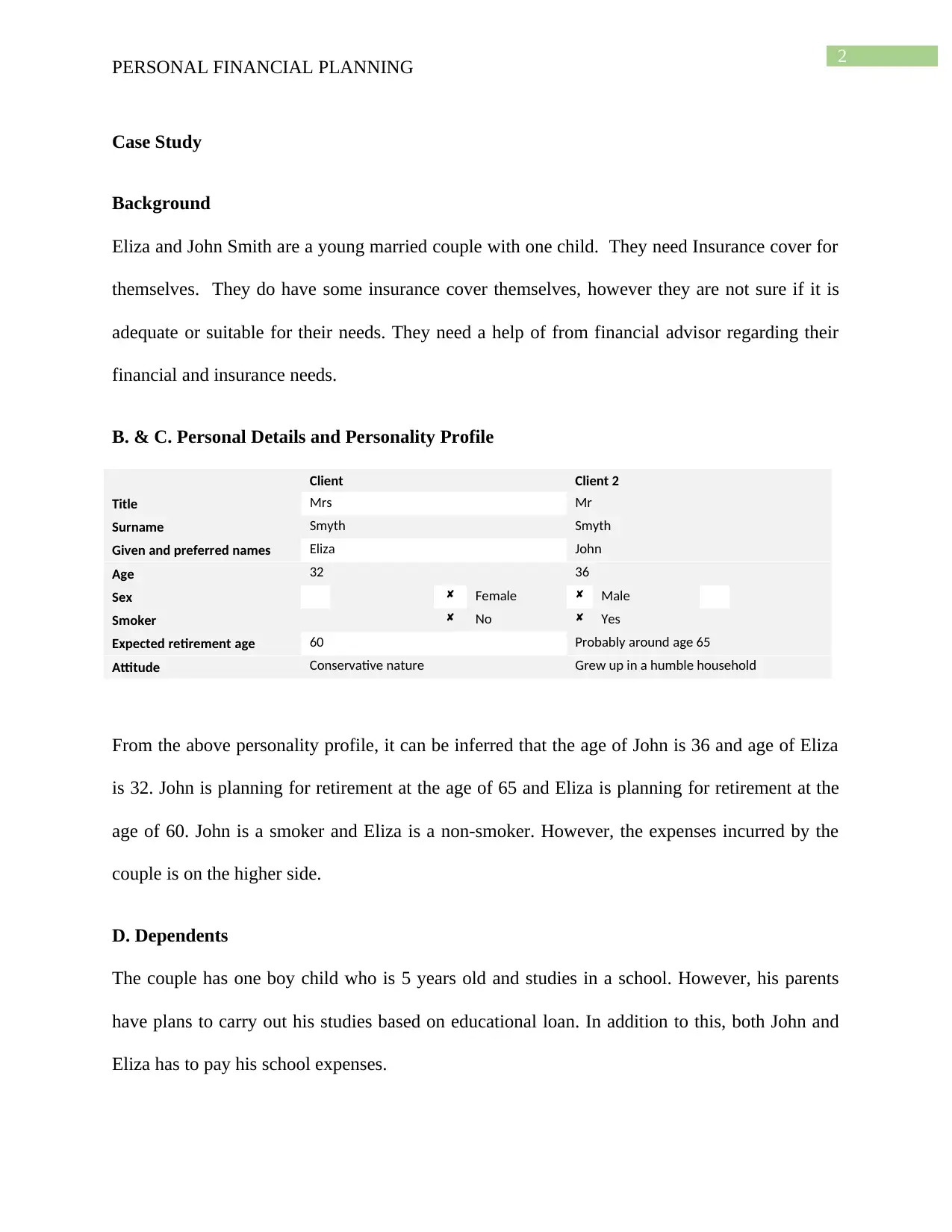

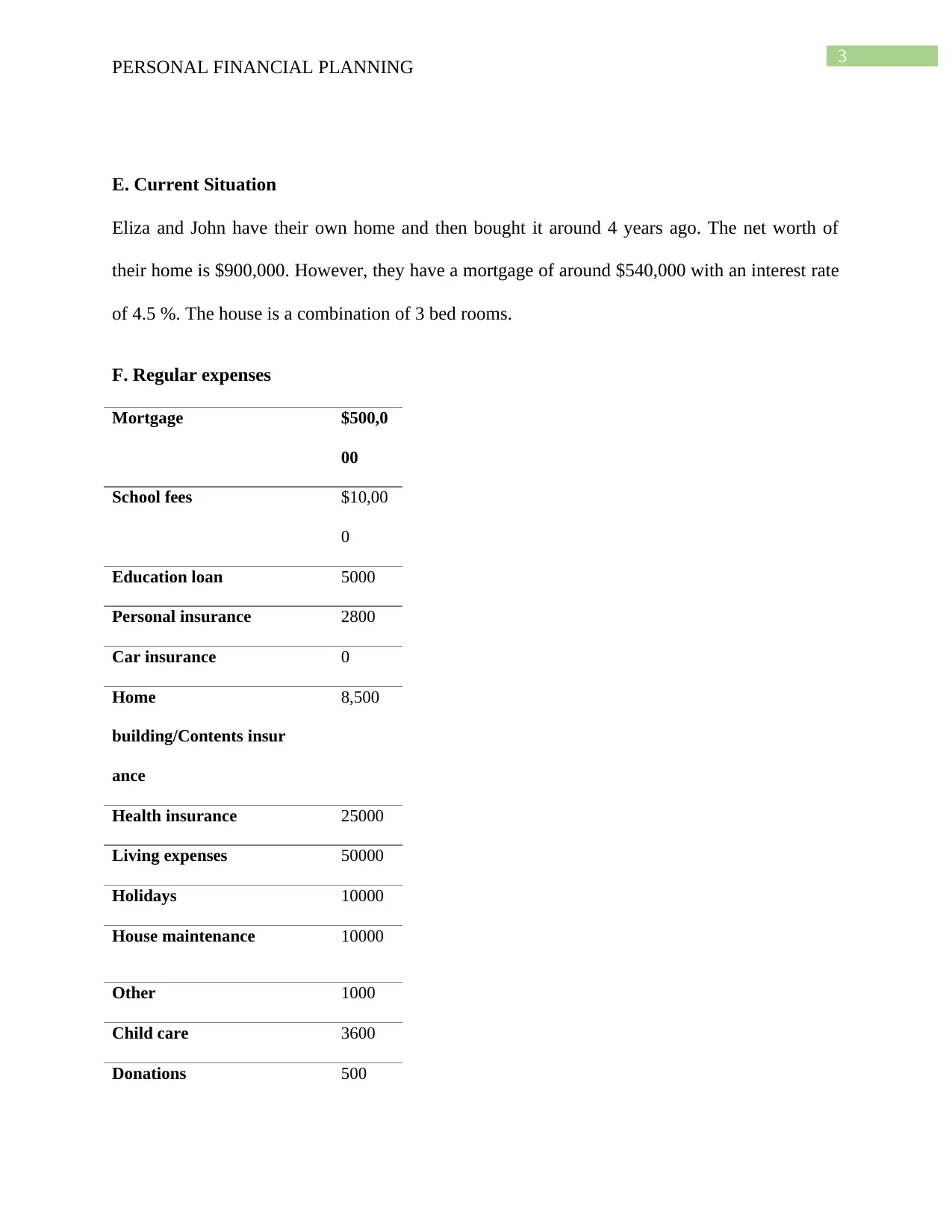

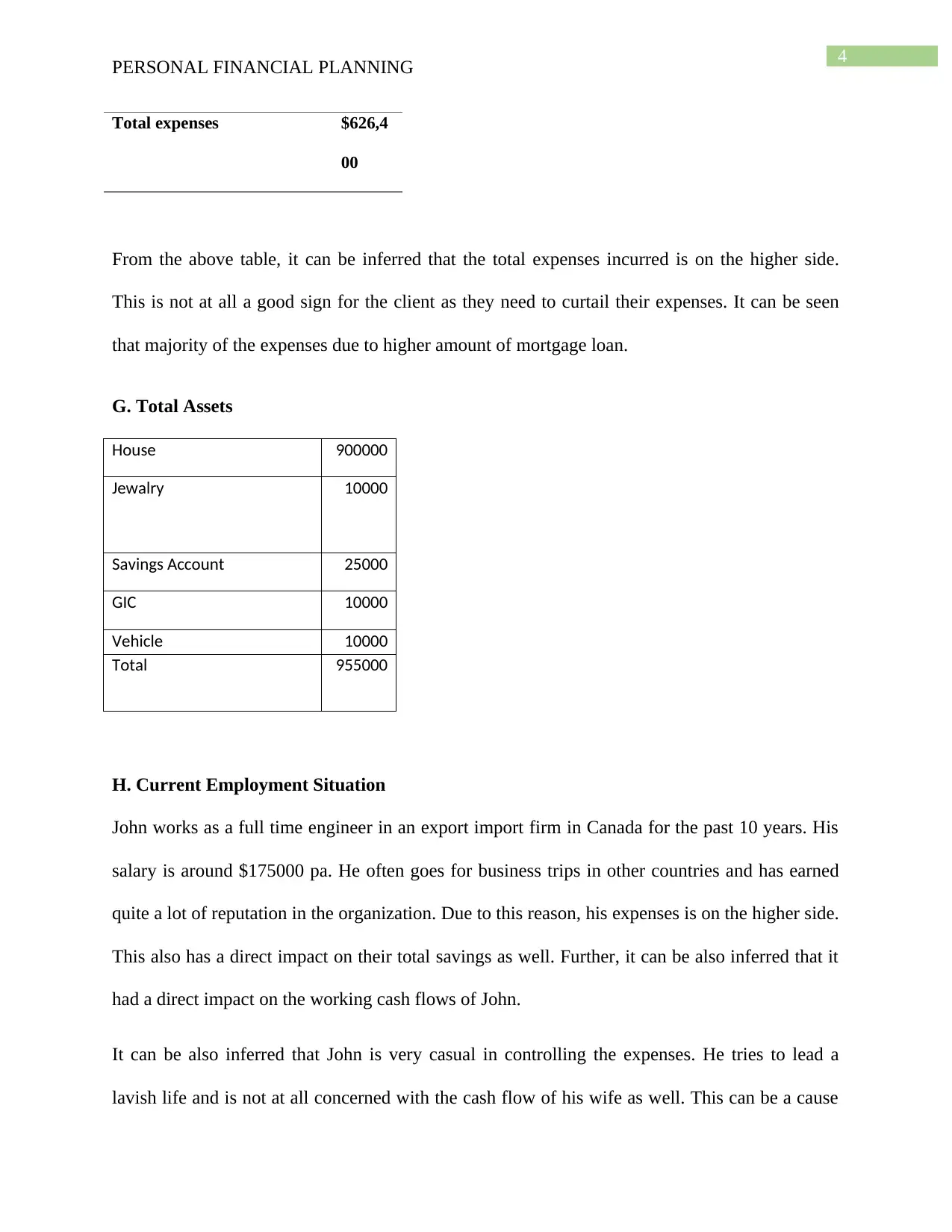

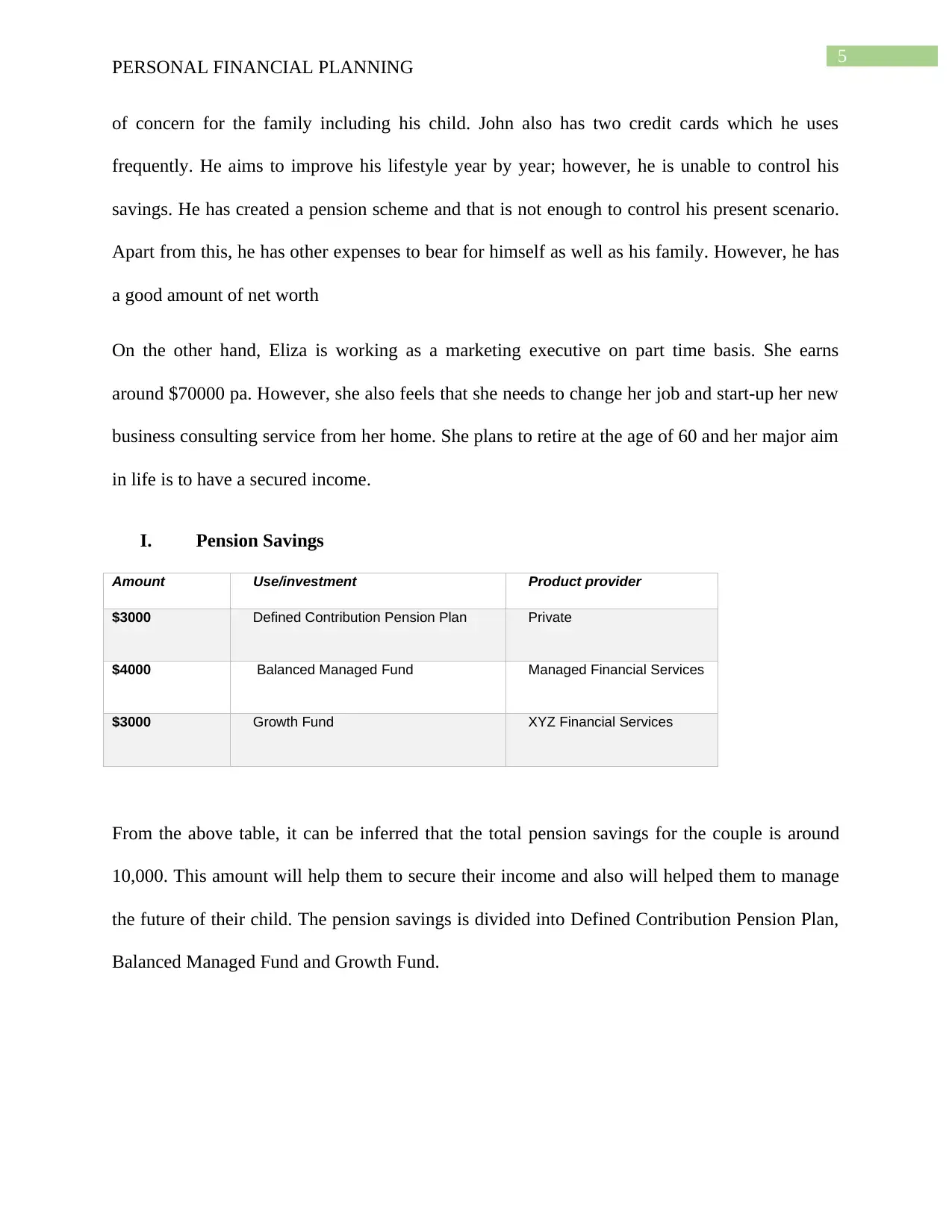

Case Study

AI Summary

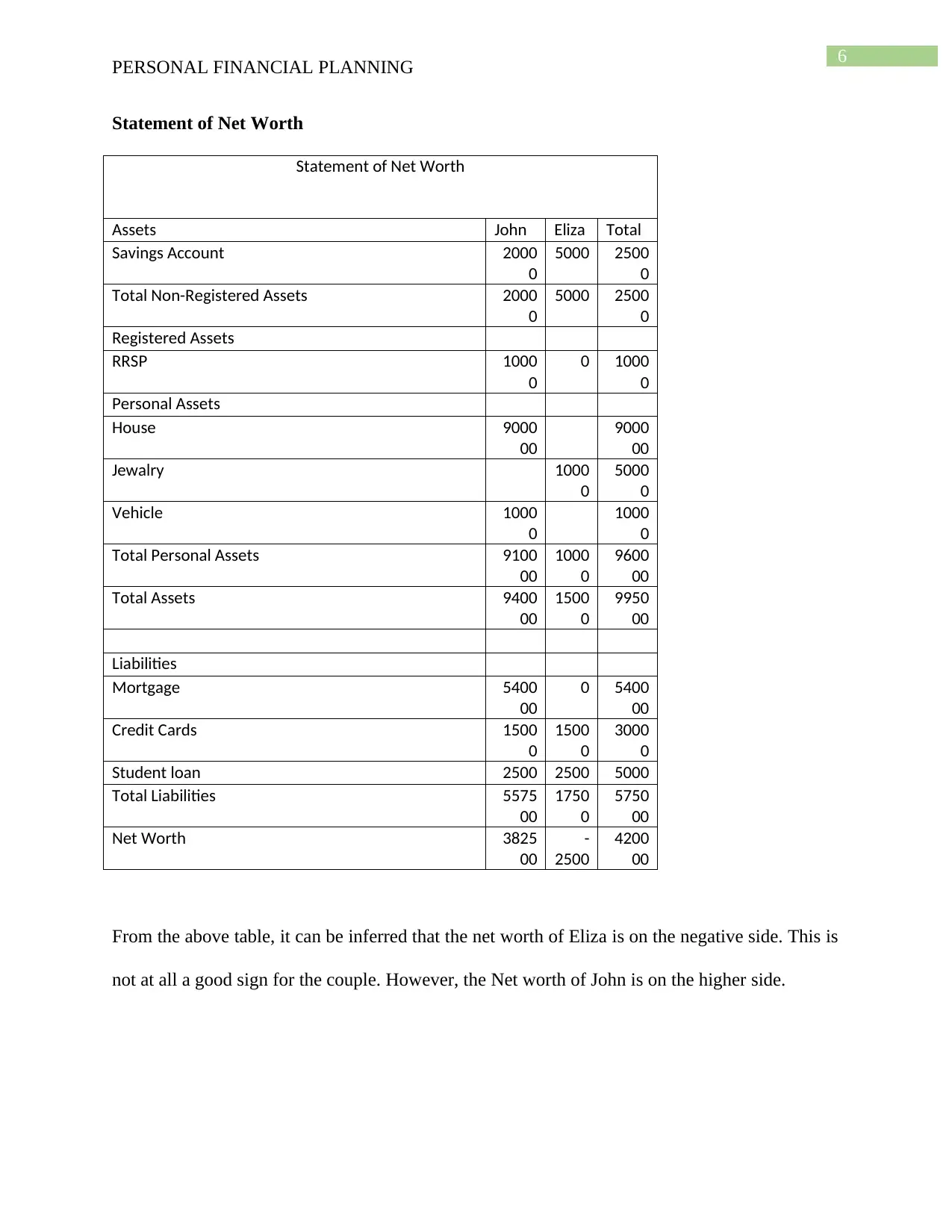

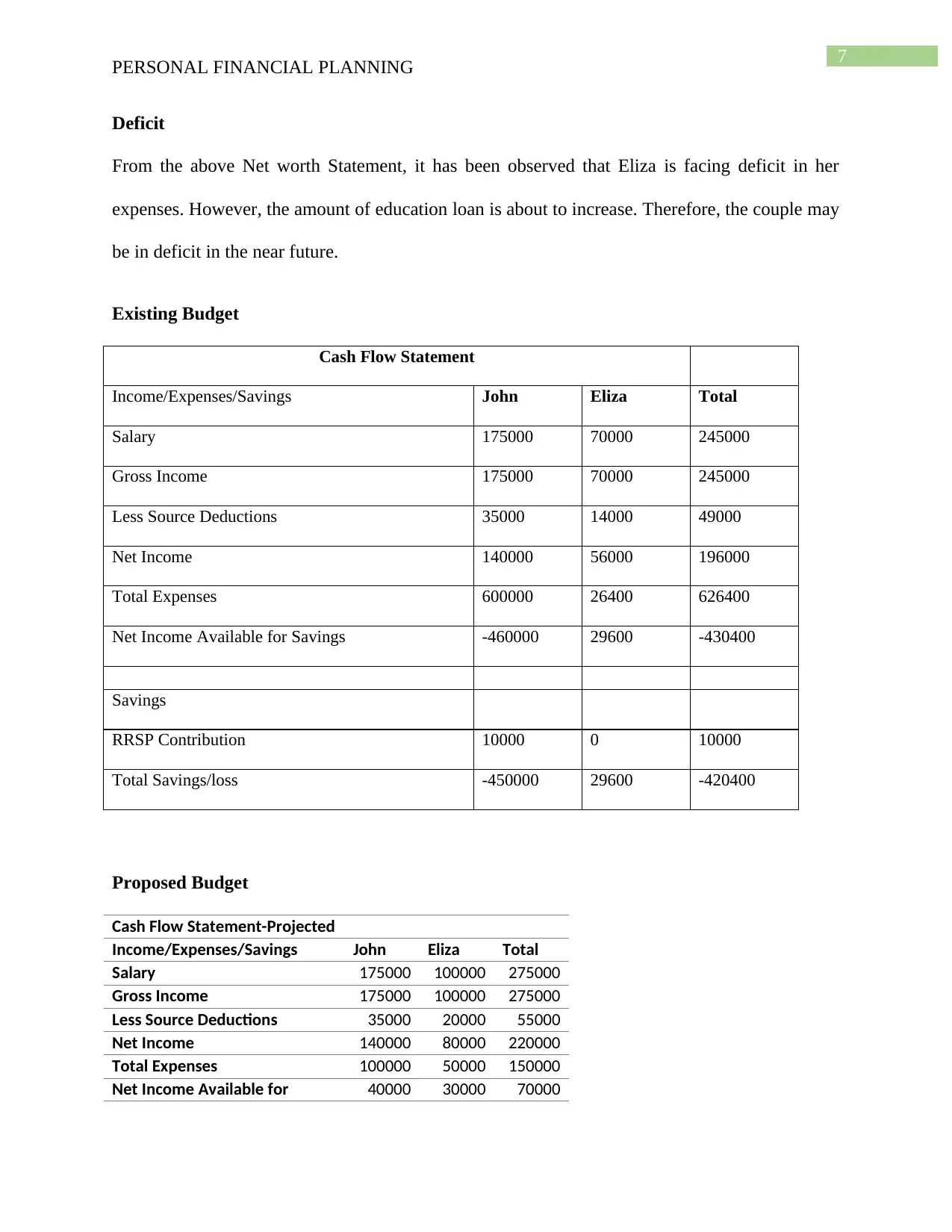

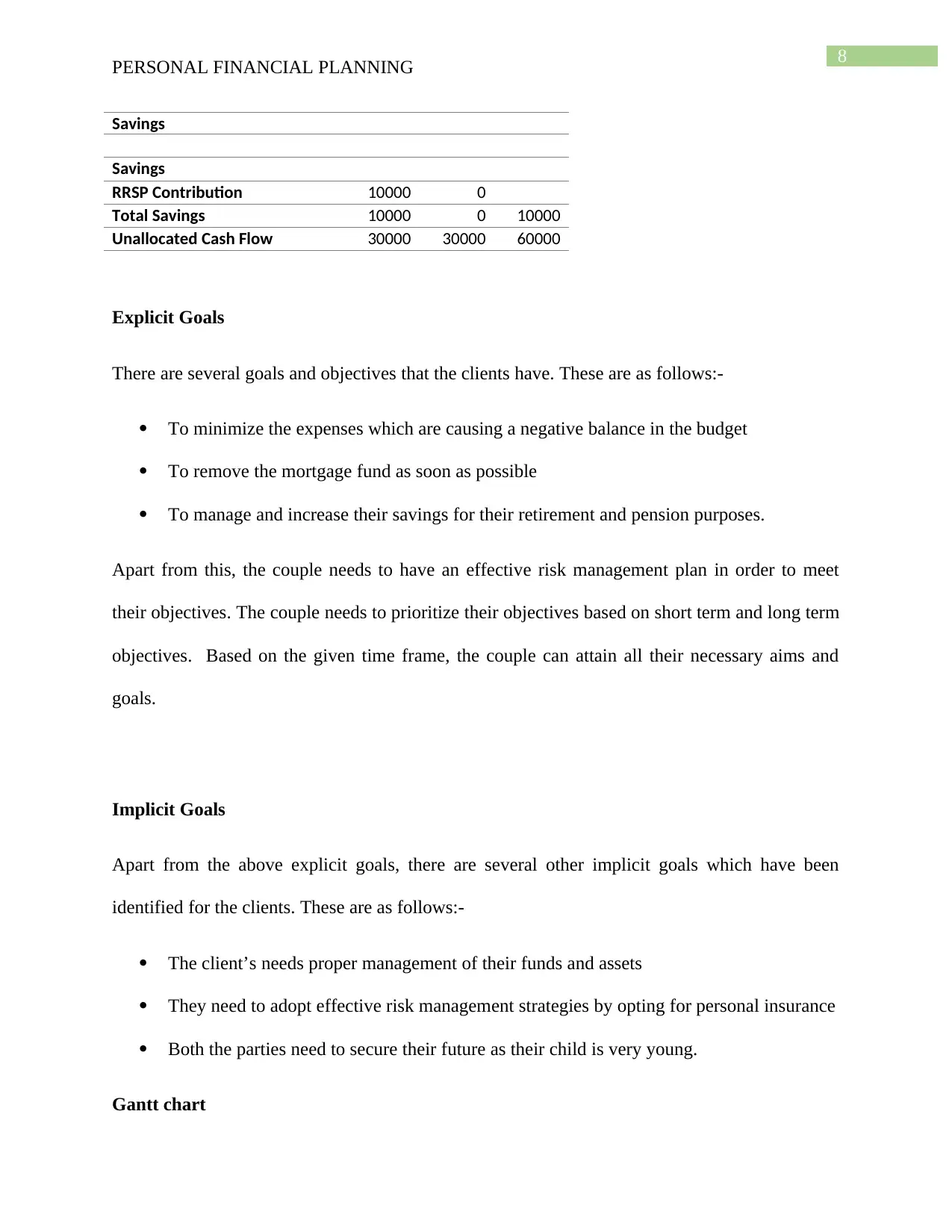

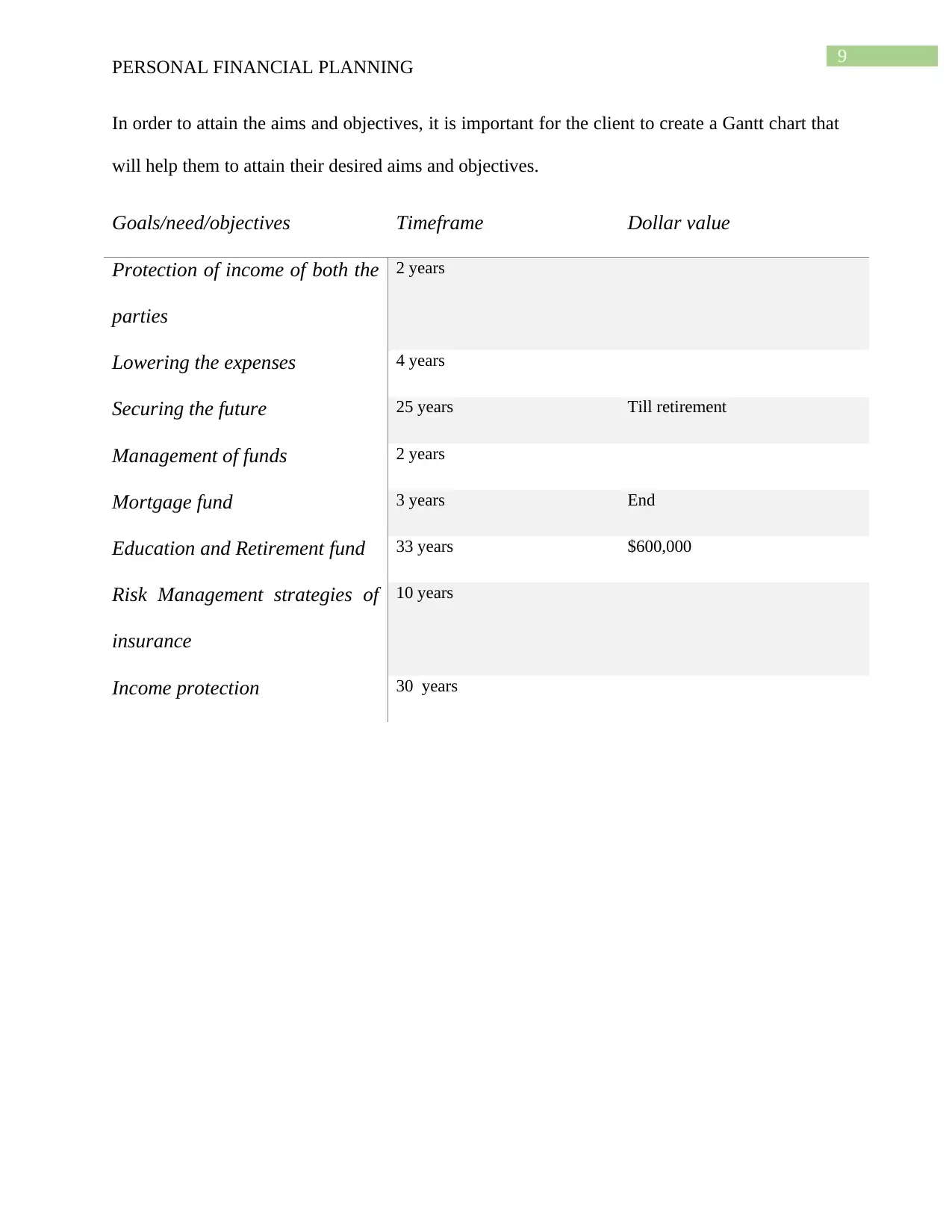

This case study presents the financial situation of Eliza and John Smith, a young married couple with a child, focusing on their income, expenses, assets, and liabilities. The analysis includes a personality profile, current employment details, and a statement of net worth. The couple faces challenges like high expenses, particularly a large mortgage, and a negative cash flow. The assignment outlines explicit and implicit goals, such as minimizing expenses, managing debt, and securing their financial future, including retirement planning and risk management. The case study utilizes a cash flow statement, a statement of net worth, and a Gantt chart to help the couple achieve their financial objectives, emphasizing the need for expense reduction, investment strategies, and insurance coverage. The case study provides a detailed overview of the couple's financial health and provides a roadmap for them to improve their financial standing.

1 out of 9

Related Documents

![Assignment 2: Financial Plan for Allen Family - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fqc%2F6af4f680480942c1a286e877fbe6432e.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.