Personal Wealth Management: Investment Portfolio Analysis Report

VerifiedAdded on 2021/06/18

|12

|2578

|17

Report

AI Summary

This report delves into personal wealth management, analyzing the financial situation of Janet and Steven. It begins by calculating their savings ratio and after-tax income, and then suggests strategies for reducing tax liability, referencing Australian tax provisions. The report then reviews their inves...

Running head: PERSONAL WEALTH MANAGEMENT

Personal Wealth Management

Name of the Student:

Name of the University:

Authors Note:

Personal Wealth Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PERSONAL WEALTH MANAGEMENT

1

Table of Contents

Question 1:.................................................................................................................................2

1. Calculating savings ratio and after-tax income of Janet and Steven for the current year,

while depicting the strategy for reducing tax liability:..............................................................2

2. Reviewing blades investment portfolio and explaining whether they are diversified

adequately, while considering both the investment across different asset classes and making

two different recommendations on how they should change their portfolio:............................4

3. Calculating future value of contribution and investment portfolio after 10 years, where the

interest rate is at 5% p.a, which could help support the deposit required of Janet and Stephen :

....................................................................................................................................................6

Question 2:.................................................................................................................................9

Portraying the key similarities and difference between small equity fund and large cap fund: 9

Reference and Bibliography:....................................................................................................10

1

Table of Contents

Question 1:.................................................................................................................................2

1. Calculating savings ratio and after-tax income of Janet and Steven for the current year,

while depicting the strategy for reducing tax liability:..............................................................2

2. Reviewing blades investment portfolio and explaining whether they are diversified

adequately, while considering both the investment across different asset classes and making

two different recommendations on how they should change their portfolio:............................4

3. Calculating future value of contribution and investment portfolio after 10 years, where the

interest rate is at 5% p.a, which could help support the deposit required of Janet and Stephen :

....................................................................................................................................................6

Question 2:.................................................................................................................................9

Portraying the key similarities and difference between small equity fund and large cap fund: 9

Reference and Bibliography:....................................................................................................10

PERSONAL WEALTH MANAGEMENT

2

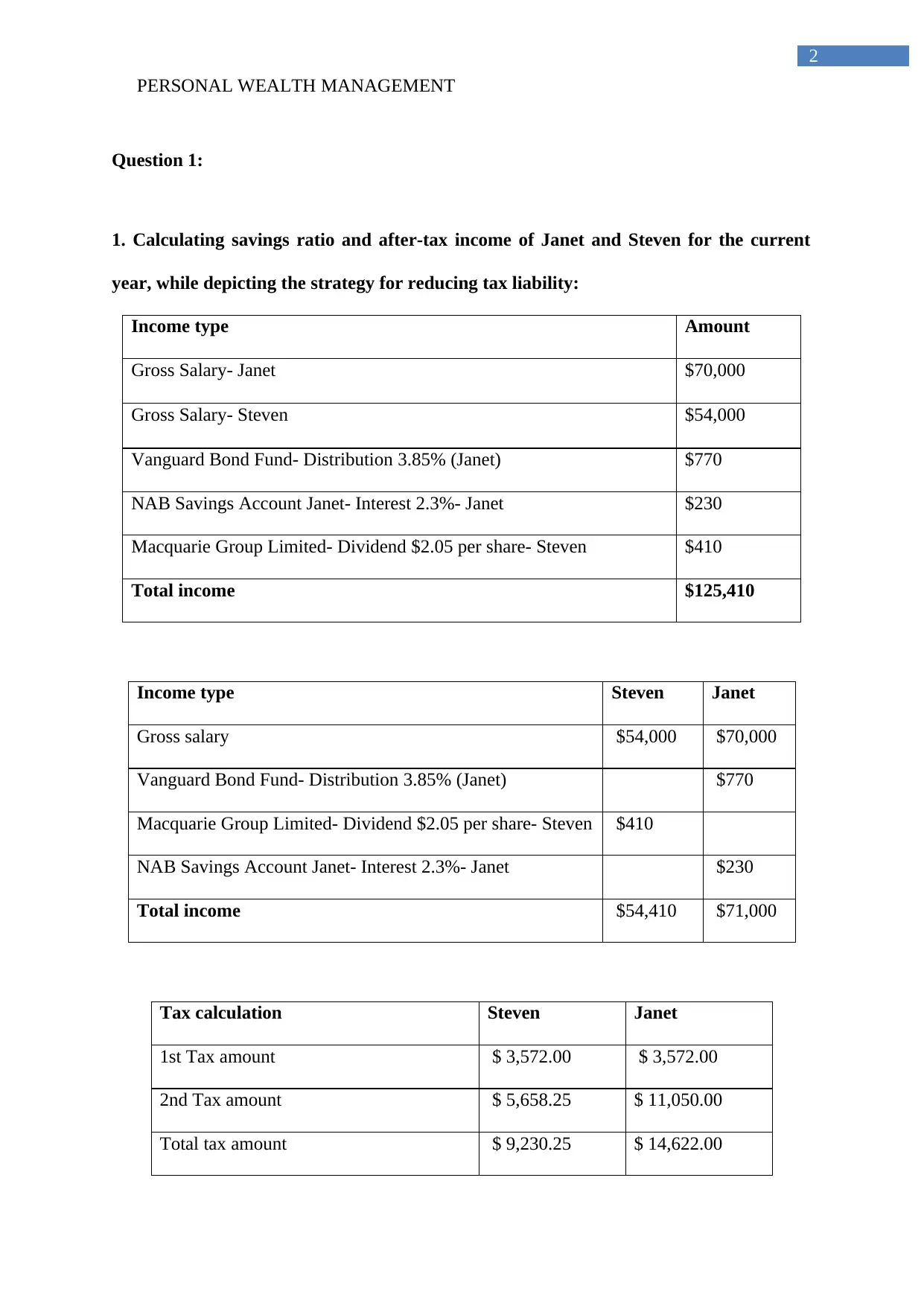

Question 1:

1. Calculating savings ratio and after-tax income of Janet and Steven for the current

year, while depicting the strategy for reducing tax liability:

Income type Amount

Gross Salary- Janet $70,000

Gross Salary- Steven $54,000

Vanguard Bond Fund- Distribution 3.85% (Janet) $770

NAB Savings Account Janet- Interest 2.3%- Janet $230

Macquarie Group Limited- Dividend $2.05 per share- Steven $410

Total income $125,410

Income type Steven Janet

Gross salary $54,000 $70,000

Vanguard Bond Fund- Distribution 3.85% (Janet) $770

Macquarie Group Limited- Dividend $2.05 per share- Steven $410

NAB Savings Account Janet- Interest 2.3%- Janet $230

Total income $54,410 $71,000

Tax calculation Steven Janet

1st Tax amount $ 3,572.00 $ 3,572.00

2nd Tax amount $ 5,658.25 $ 11,050.00

Total tax amount $ 9,230.25 $ 14,622.00

2

Question 1:

1. Calculating savings ratio and after-tax income of Janet and Steven for the current

year, while depicting the strategy for reducing tax liability:

Income type Amount

Gross Salary- Janet $70,000

Gross Salary- Steven $54,000

Vanguard Bond Fund- Distribution 3.85% (Janet) $770

NAB Savings Account Janet- Interest 2.3%- Janet $230

Macquarie Group Limited- Dividend $2.05 per share- Steven $410

Total income $125,410

Income type Steven Janet

Gross salary $54,000 $70,000

Vanguard Bond Fund- Distribution 3.85% (Janet) $770

Macquarie Group Limited- Dividend $2.05 per share- Steven $410

NAB Savings Account Janet- Interest 2.3%- Janet $230

Total income $54,410 $71,000

Tax calculation Steven Janet

1st Tax amount $ 3,572.00 $ 3,572.00

2nd Tax amount $ 5,658.25 $ 11,050.00

Total tax amount $ 9,230.25 $ 14,622.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PERSONAL WEALTH MANAGEMENT

3

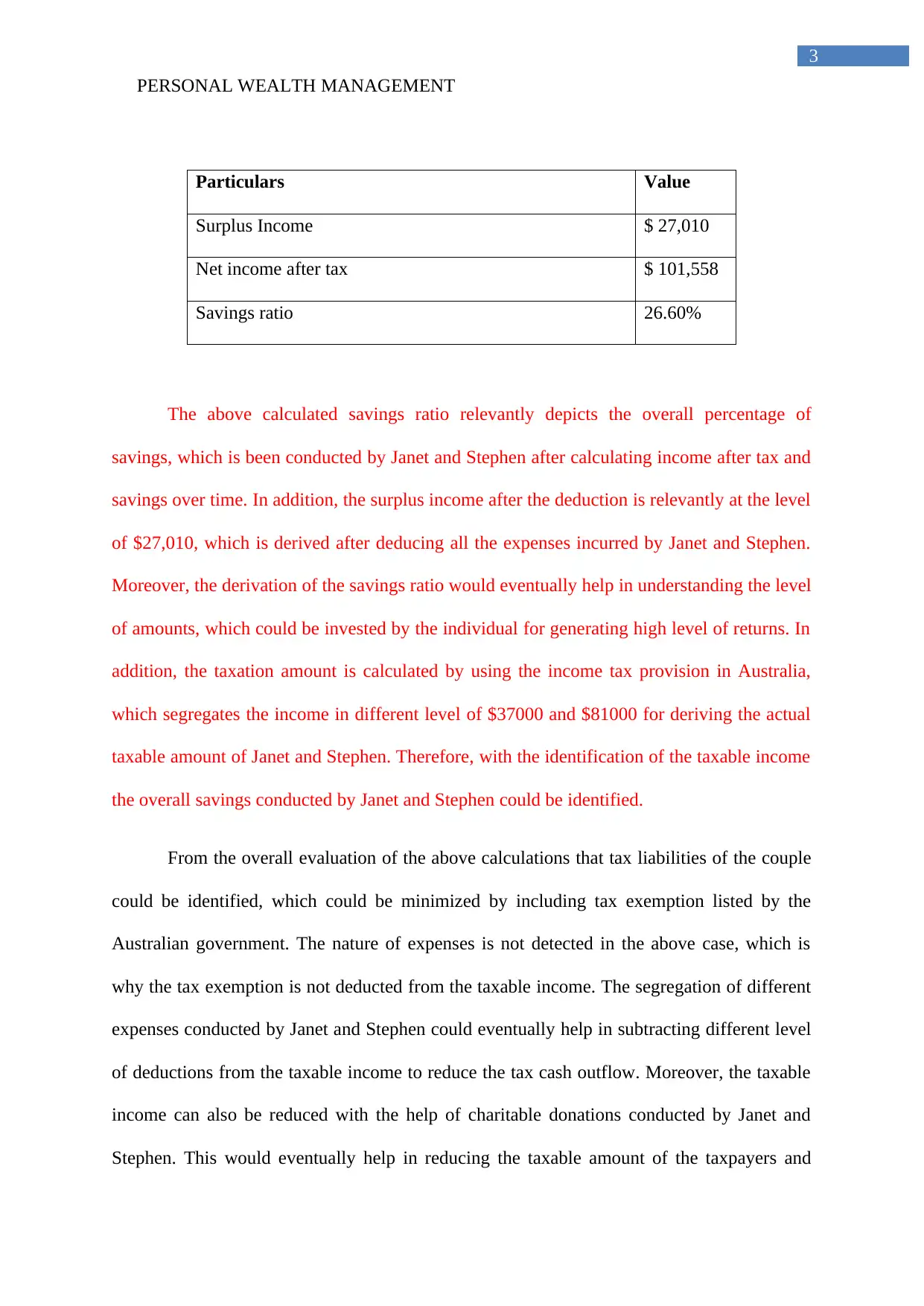

Particulars Value

Surplus Income $ 27,010

Net income after tax $ 101,558

Savings ratio 26.60%

The above calculated savings ratio relevantly depicts the overall percentage of

savings, which is been conducted by Janet and Stephen after calculating income after tax and

savings over time. In addition, the surplus income after the deduction is relevantly at the level

of $27,010, which is derived after deducing all the expenses incurred by Janet and Stephen.

Moreover, the derivation of the savings ratio would eventually help in understanding the level

of amounts, which could be invested by the individual for generating high level of returns. In

addition, the taxation amount is calculated by using the income tax provision in Australia,

which segregates the income in different level of $37000 and $81000 for deriving the actual

taxable amount of Janet and Stephen. Therefore, with the identification of the taxable income

the overall savings conducted by Janet and Stephen could be identified.

From the overall evaluation of the above calculations that tax liabilities of the couple

could be identified, which could be minimized by including tax exemption listed by the

Australian government. The nature of expenses is not detected in the above case, which is

why the tax exemption is not deducted from the taxable income. The segregation of different

expenses conducted by Janet and Stephen could eventually help in subtracting different level

of deductions from the taxable income to reduce the tax cash outflow. Moreover, the taxable

income can also be reduced with the help of charitable donations conducted by Janet and

Stephen. This would eventually help in reducing the taxable amount of the taxpayers and

3

Particulars Value

Surplus Income $ 27,010

Net income after tax $ 101,558

Savings ratio 26.60%

The above calculated savings ratio relevantly depicts the overall percentage of

savings, which is been conducted by Janet and Stephen after calculating income after tax and

savings over time. In addition, the surplus income after the deduction is relevantly at the level

of $27,010, which is derived after deducing all the expenses incurred by Janet and Stephen.

Moreover, the derivation of the savings ratio would eventually help in understanding the level

of amounts, which could be invested by the individual for generating high level of returns. In

addition, the taxation amount is calculated by using the income tax provision in Australia,

which segregates the income in different level of $37000 and $81000 for deriving the actual

taxable amount of Janet and Stephen. Therefore, with the identification of the taxable income

the overall savings conducted by Janet and Stephen could be identified.

From the overall evaluation of the above calculations that tax liabilities of the couple

could be identified, which could be minimized by including tax exemption listed by the

Australian government. The nature of expenses is not detected in the above case, which is

why the tax exemption is not deducted from the taxable income. The segregation of different

expenses conducted by Janet and Stephen could eventually help in subtracting different level

of deductions from the taxable income to reduce the tax cash outflow. Moreover, the taxable

income can also be reduced with the help of charitable donations conducted by Janet and

Stephen. This would eventually help in reducing the taxable amount of the taxpayers and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PERSONAL WEALTH MANAGEMENT

4

maximizing income retention capacity. Hitt and Duane (2017) mentioned that with the help

of tax reduction measures individuals are able to minimize their tax expenses, while

maximizing the savings on yearly basis.

The current tax amount is relevantly high for Janet and Stephen, which is due to the

non-segregations of all the expenses incurred by the company. Moreover, the use of relevant

segregation of different expenditures could eventually help in identifying the overall tax

exemptions, which could be used in minimising the level of taxable income of Janet and

Stephen. The identification of the tax provisions might eventually allow Janet and Stephen to

improve the level of their savings, after conduiting relevant expenses and tax provisions.

Moreover, the Income Tax Assessment Act 1997 disclosed in Austria relevantly provides the

details regarding the level of tax provisions that needs to be conducted by individuals.

Therefore, with the strategy of utilising the level of adequate tax provisions Janet and

Stephen could eventually reduce their overall tax liability and minimise their tax cash

outflow. On the other hand, Dang, Forsyth and Vetzal (2017) argued that without the

segregation of expenses the individual is not able to detect the overall taxable amount, which

is due to the Australian government.

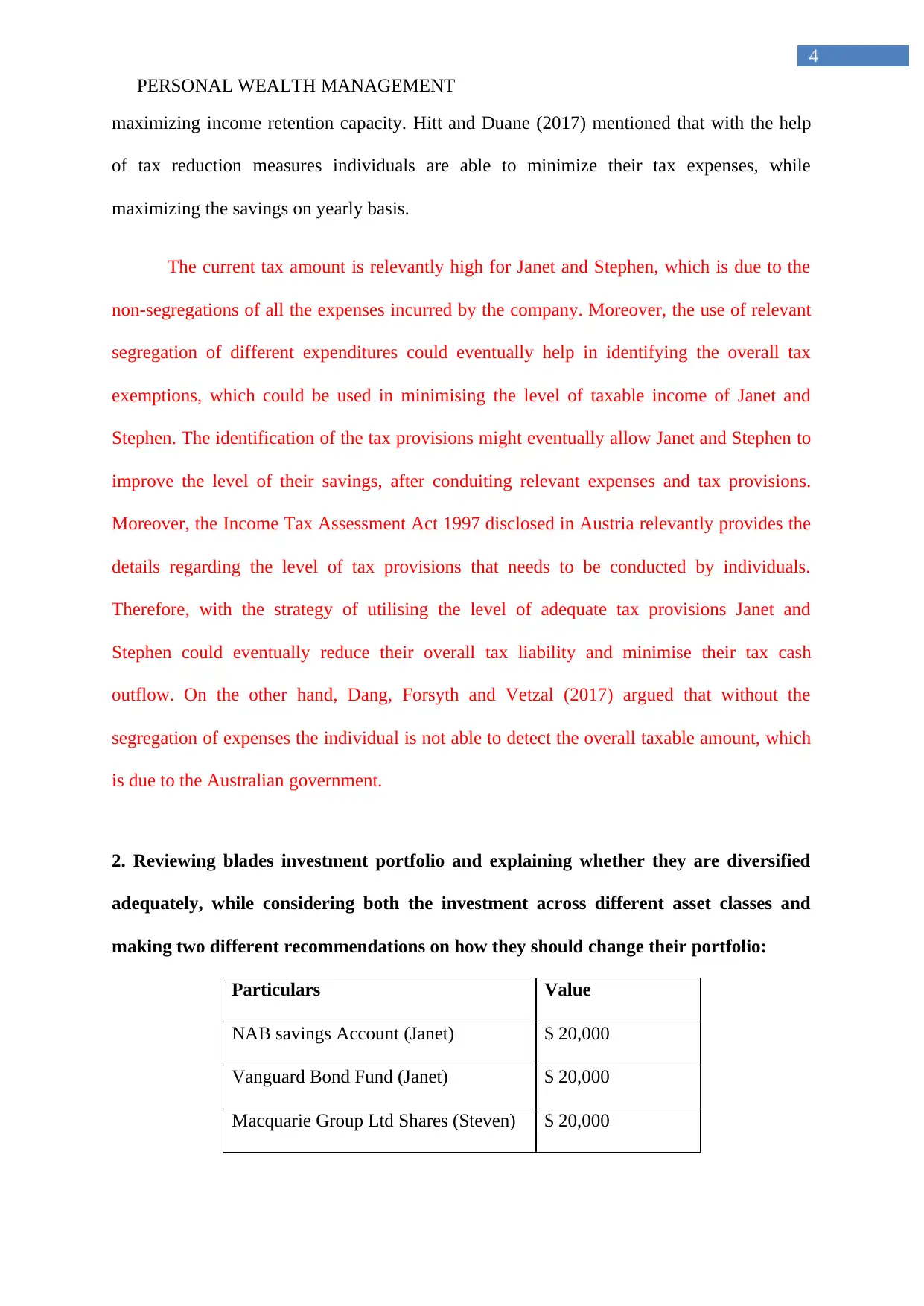

2. Reviewing blades investment portfolio and explaining whether they are diversified

adequately, while considering both the investment across different asset classes and

making two different recommendations on how they should change their portfolio:

Particulars Value

NAB savings Account (Janet) $ 20,000

Vanguard Bond Fund (Janet) $ 20,000

Macquarie Group Ltd Shares (Steven) $ 20,000

4

maximizing income retention capacity. Hitt and Duane (2017) mentioned that with the help

of tax reduction measures individuals are able to minimize their tax expenses, while

maximizing the savings on yearly basis.

The current tax amount is relevantly high for Janet and Stephen, which is due to the

non-segregations of all the expenses incurred by the company. Moreover, the use of relevant

segregation of different expenditures could eventually help in identifying the overall tax

exemptions, which could be used in minimising the level of taxable income of Janet and

Stephen. The identification of the tax provisions might eventually allow Janet and Stephen to

improve the level of their savings, after conduiting relevant expenses and tax provisions.

Moreover, the Income Tax Assessment Act 1997 disclosed in Austria relevantly provides the

details regarding the level of tax provisions that needs to be conducted by individuals.

Therefore, with the strategy of utilising the level of adequate tax provisions Janet and

Stephen could eventually reduce their overall tax liability and minimise their tax cash

outflow. On the other hand, Dang, Forsyth and Vetzal (2017) argued that without the

segregation of expenses the individual is not able to detect the overall taxable amount, which

is due to the Australian government.

2. Reviewing blades investment portfolio and explaining whether they are diversified

adequately, while considering both the investment across different asset classes and

making two different recommendations on how they should change their portfolio:

Particulars Value

NAB savings Account (Janet) $ 20,000

Vanguard Bond Fund (Janet) $ 20,000

Macquarie Group Ltd Shares (Steven) $ 20,000

PERSONAL WEALTH MANAGEMENT

5

The current portfolio maintained by Janet and Stephen is relatively diversified and

has all the relevant investment instruments which could generate adequate returns from

investment. In addition, the composition of the portfolio is relatively conservative, where

66.67% of the total portfolio is comprised of risk free asset, why 33.33% comprises of growth

assets. This relatively minimizes the chance of obtaining higher returns from investment, as

the portfolio focuses on fixed returns. Therefore, the current changes in the portfolio could be

conducted where 66.67% will consist of growth stocks while the other 33.33% will consist of

risk free asset for reducing volatility of the capital market. This provision would eventually

allow Janet and Stephen to generate higher rate of return from their investment (Dang,

Forsyth and Vetzal 2017).

The current portfolio that is been maintained by Janet and Stephen is mainly

considered conservative, as it is invested in risk free assets, while the change in the portfolio

could be conducted to improve the level of profits from investment. The conservative nature

of the portfolio could be improved to growth phase, which might help in maximizing the

level of profits from operations. The chances in overall portfolio could be conducted, where

maximum of the returns will be generated from shares. Therefore, the portfolio could

eventually help in generating high level of returns from investment, while increasing the risk

from investment. According to May (2017), investment conducted in different asset classes

allow the investors to minimize the risk from investment, while generating high level of

returns from investment.

The second recommendation that could be conducted by Janet and Stephen is the use

of standard portfolio, where both conservative and growth financial instrument are used in

generating high level of return from investment. In addition, the segregation of the portfolio

could be conducted, where 50% of the investment will be conducted in Macquarie Group Ltd

Shares, which is considered to fall under growth perspective. On the other hand, the second

5

The current portfolio maintained by Janet and Stephen is relatively diversified and

has all the relevant investment instruments which could generate adequate returns from

investment. In addition, the composition of the portfolio is relatively conservative, where

66.67% of the total portfolio is comprised of risk free asset, why 33.33% comprises of growth

assets. This relatively minimizes the chance of obtaining higher returns from investment, as

the portfolio focuses on fixed returns. Therefore, the current changes in the portfolio could be

conducted where 66.67% will consist of growth stocks while the other 33.33% will consist of

risk free asset for reducing volatility of the capital market. This provision would eventually

allow Janet and Stephen to generate higher rate of return from their investment (Dang,

Forsyth and Vetzal 2017).

The current portfolio that is been maintained by Janet and Stephen is mainly

considered conservative, as it is invested in risk free assets, while the change in the portfolio

could be conducted to improve the level of profits from investment. The conservative nature

of the portfolio could be improved to growth phase, which might help in maximizing the

level of profits from operations. The chances in overall portfolio could be conducted, where

maximum of the returns will be generated from shares. Therefore, the portfolio could

eventually help in generating high level of returns from investment, while increasing the risk

from investment. According to May (2017), investment conducted in different asset classes

allow the investors to minimize the risk from investment, while generating high level of

returns from investment.

The second recommendation that could be conducted by Janet and Stephen is the use

of standard portfolio, where both conservative and growth financial instrument are used in

generating high level of return from investment. In addition, the segregation of the portfolio

could be conducted, where 50% of the investment will be conducted in Macquarie Group Ltd

Shares, which is considered to fall under growth perspective. On the other hand, the second

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PERSONAL WEALTH MANAGEMENT

6

50% investment needs to be conducted in NAB savings Account and Vanguard Bond Fund,

which relevantly has no risk from investment. This could eventually have slow growth as

50% of the returns from investment will be fixed due to the investment in risk free assets.

Hence, with the help second recommendation the overall prolific could minimize the risk

from investment and obtain higher rate of returns from investment, as compared to

recommendation one. Hitt and Duane (2017) stated that investors with identified risk and

return measure of stock are able to formulate portfolio, which might reduce risk from

investment and generate higher rate of returns.

3. Calculating future value of contribution and investment portfolio after 10 years,

where the interest rate is at 5% p.a, which could help support the deposit required of

Janet and Stephen :

Particulars Value

Vanguard Bond Fund (Janet) $ 20,000

NAB savings Account (Janet) $ 20,000

Macquarie Group Ltd Shares (Steven) $ 20,000

Current investment $ 60,000

Return on investment 5%

Time 10

Future value $ 97,734

The above valuation mainly represents overall future value of investment conducted

in the current investment of Vanguard Bond Fund, NAB savings Account and Macquarie

Group Ltd Shares. Moreover, the calculation relevantly represents the overall use of 5%

return till 10 years on annual basis, which will generate an overall return of $97,734. The

6

50% investment needs to be conducted in NAB savings Account and Vanguard Bond Fund,

which relevantly has no risk from investment. This could eventually have slow growth as

50% of the returns from investment will be fixed due to the investment in risk free assets.

Hence, with the help second recommendation the overall prolific could minimize the risk

from investment and obtain higher rate of returns from investment, as compared to

recommendation one. Hitt and Duane (2017) stated that investors with identified risk and

return measure of stock are able to formulate portfolio, which might reduce risk from

investment and generate higher rate of returns.

3. Calculating future value of contribution and investment portfolio after 10 years,

where the interest rate is at 5% p.a, which could help support the deposit required of

Janet and Stephen :

Particulars Value

Vanguard Bond Fund (Janet) $ 20,000

NAB savings Account (Janet) $ 20,000

Macquarie Group Ltd Shares (Steven) $ 20,000

Current investment $ 60,000

Return on investment 5%

Time 10

Future value $ 97,734

The above valuation mainly represents overall future value of investment conducted

in the current investment of Vanguard Bond Fund, NAB savings Account and Macquarie

Group Ltd Shares. Moreover, the calculation relevantly represents the overall use of 5%

return till 10 years on annual basis, which will generate an overall return of $97,734. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PERSONAL WEALTH MANAGEMENT

7

returns generated by the current portfolio is relevantly low, as the provisions that is

conducted by the investment is not adequate. Additionally, Alam, Gupta, and Shanmugam

(2017) stated that portfolio could only provide higher rate of returns from investment when

high growth stock with high risk is accumulated in the portfolio of the investor.

Particulars Contribution FV

Year 1 $5,000 $8,144

Year 2 $5,000 $7,757

Year 3 $5,000 $7,387

Year 4 $5,000 $7,036

Year 5 $5,000 $6,700

Year 6 $10,000 $12,763

Year 7 $10,000 $12,155

Year 8 $10,000 $11,576

Year 9 $10,000 $11,025

Year 10 $10,000 $10,500

Total Contribution from savings $ 95,043.50

The above calculation is relevantly conducted to identify the return that will be

generated from contribution investment. in addition, the contribution investment mainly

provides return of $95,043.50, which is not sufficient for supporting the overall deposit

requirement of Janet and Stephen. The contribution conducted by Janet and Stephen on

yearly basis will provide a total return of 5%, which could help in generating a constant

retune from investment.

Particulars Amount

7

returns generated by the current portfolio is relevantly low, as the provisions that is

conducted by the investment is not adequate. Additionally, Alam, Gupta, and Shanmugam

(2017) stated that portfolio could only provide higher rate of returns from investment when

high growth stock with high risk is accumulated in the portfolio of the investor.

Particulars Contribution FV

Year 1 $5,000 $8,144

Year 2 $5,000 $7,757

Year 3 $5,000 $7,387

Year 4 $5,000 $7,036

Year 5 $5,000 $6,700

Year 6 $10,000 $12,763

Year 7 $10,000 $12,155

Year 8 $10,000 $11,576

Year 9 $10,000 $11,025

Year 10 $10,000 $10,500

Total Contribution from savings $ 95,043.50

The above calculation is relevantly conducted to identify the return that will be

generated from contribution investment. in addition, the contribution investment mainly

provides return of $95,043.50, which is not sufficient for supporting the overall deposit

requirement of Janet and Stephen. The contribution conducted by Janet and Stephen on

yearly basis will provide a total return of 5%, which could help in generating a constant

retune from investment.

Particulars Amount

PERSONAL WEALTH MANAGEMENT

8

Required deposit goal $200,000

Total Contribution from savings $95,043

Future value of investment $97,734

Total returns after 10 years $192,777

Additional deposit needed $7,223

Extra investment needed by Janet and

Stephen

$574

The above calculations represent the minimum requirement of additional investment

that needs to be conducted by Janet and Stephen to fulfill the required deposit of $200,000.

The investment of $574.25 on yearly basis would eventually help Janet and Stephen to

generate the required rate of returns from investment. Both the investments in portfolio and

contribution mainly provides a return of $192,777 in 10 years with a total return on 5%, while

the deposit amount was $200,000. Therefore, keeping in mind the deposit amount of

$200,000, an additional investment of $574.25 need to be conducted on every year till the

next 10 years of investment.

The above calculation would eventually help in detecting the extra investment that

need to be conducted by Janet and Stephen for obtaining the level of desired deposit amount.

In addition, the investment can be conducted in different levels, which might be helpful in

improving the level of returns from investment. Therefore, with the implementation of

investment $574.25 could directly allow Janet and Stephen to improve their return generating

capability. Furthermore, with the implementation of the required level of profits would

eventually help in generating high level of returns. In this contest, Takacs et al. (2017) stated

8

Required deposit goal $200,000

Total Contribution from savings $95,043

Future value of investment $97,734

Total returns after 10 years $192,777

Additional deposit needed $7,223

Extra investment needed by Janet and

Stephen

$574

The above calculations represent the minimum requirement of additional investment

that needs to be conducted by Janet and Stephen to fulfill the required deposit of $200,000.

The investment of $574.25 on yearly basis would eventually help Janet and Stephen to

generate the required rate of returns from investment. Both the investments in portfolio and

contribution mainly provides a return of $192,777 in 10 years with a total return on 5%, while

the deposit amount was $200,000. Therefore, keeping in mind the deposit amount of

$200,000, an additional investment of $574.25 need to be conducted on every year till the

next 10 years of investment.

The above calculation would eventually help in detecting the extra investment that

need to be conducted by Janet and Stephen for obtaining the level of desired deposit amount.

In addition, the investment can be conducted in different levels, which might be helpful in

improving the level of returns from investment. Therefore, with the implementation of

investment $574.25 could directly allow Janet and Stephen to improve their return generating

capability. Furthermore, with the implementation of the required level of profits would

eventually help in generating high level of returns. In this contest, Takacs et al. (2017) stated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PERSONAL WEALTH MANAGEMENT

9

that with the use of adequate investment options the investors are able to maximizes their

return while minimizing the risk from investment. On the other hand, Nolan, Wu and Low

(2018) criticizes that due to the negative impact from capital market the overall portfolio

losses relevant increases from investment, while hampering the actual investment capital.

Therefore, Janet and Stephen could adequately conducted the extra investment in their

portfolio for improving the level of returns from investment.

Question 2:

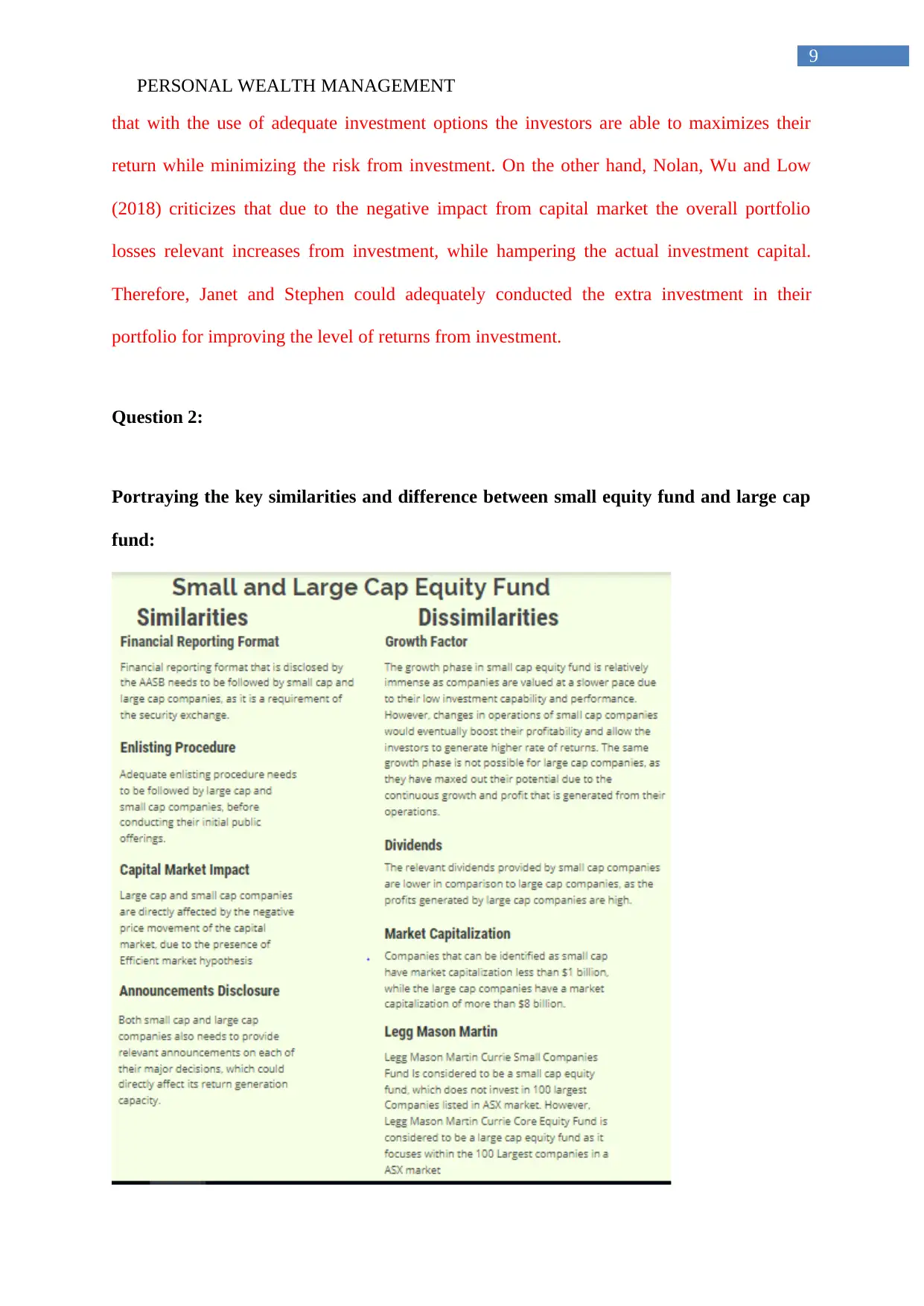

Portraying the key similarities and difference between small equity fund and large cap

fund:

9

that with the use of adequate investment options the investors are able to maximizes their

return while minimizing the risk from investment. On the other hand, Nolan, Wu and Low

(2018) criticizes that due to the negative impact from capital market the overall portfolio

losses relevant increases from investment, while hampering the actual investment capital.

Therefore, Janet and Stephen could adequately conducted the extra investment in their

portfolio for improving the level of returns from investment.

Question 2:

Portraying the key similarities and difference between small equity fund and large cap

fund:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PERSONAL WEALTH MANAGEMENT

10

Reference and Bibliography:

Alam, N., Gupta, L. and Shanmugam, B., 2017. Islamic Wealth Management. In Islamic

Finance (pp. 451-473). Palgrave Macmillan, Cham.

Alstadsæter, A., Johannesen, N. and Zucman, G., 2017. Who owns the wealth in tax havens?

Macro evidence and implications for global inequality (No. w23805). National Bureau of

Economic Research.

Beyer, C.B., 2017. Wealth Management Unwrapped, Revised and Expanded: Unwrap what

You Need to Know and Enjoy the Present. John Wiley & Sons.

BURTON, D., 2018. The US Racial Wealth Gap and the Implications for Financial Inclusion

and Wealth Management Policies. Journal of Social Policy, pp.1-18.

Dang, D.M., Forsyth, P.A. and Vetzal, K.R., 2017. The 4% strategy revisited: a pre-

commitment mean-variance optimal approach to wealth management. Quantitative

Finance, 17(3), pp.335-351.

Hitt, M. and Duane Ireland, R., 2017. The intersection of entrepreneurship and strategic

management research. The Blackwell handbook of entrepreneurship, pp.45-63.

Krongkaew, M., 2017. The Despot’s Guide to Wealth Management: On the International

Campaign Against Grand Corruption by Jason C. Sharman Cornell University Press, Ithaca,

NY, 2017 Pp. 274. ISBN 978 1 5017 0551 9. Asian‐Pacific Economic Literature, 31(2),

pp.145-148.

May, P.J., 2017. Art and Collectibles for Wealth Management. Financial Behavior: Players,

Services, Products, and Markets, p.422.

10

Reference and Bibliography:

Alam, N., Gupta, L. and Shanmugam, B., 2017. Islamic Wealth Management. In Islamic

Finance (pp. 451-473). Palgrave Macmillan, Cham.

Alstadsæter, A., Johannesen, N. and Zucman, G., 2017. Who owns the wealth in tax havens?

Macro evidence and implications for global inequality (No. w23805). National Bureau of

Economic Research.

Beyer, C.B., 2017. Wealth Management Unwrapped, Revised and Expanded: Unwrap what

You Need to Know and Enjoy the Present. John Wiley & Sons.

BURTON, D., 2018. The US Racial Wealth Gap and the Implications for Financial Inclusion

and Wealth Management Policies. Journal of Social Policy, pp.1-18.

Dang, D.M., Forsyth, P.A. and Vetzal, K.R., 2017. The 4% strategy revisited: a pre-

commitment mean-variance optimal approach to wealth management. Quantitative

Finance, 17(3), pp.335-351.

Hitt, M. and Duane Ireland, R., 2017. The intersection of entrepreneurship and strategic

management research. The Blackwell handbook of entrepreneurship, pp.45-63.

Krongkaew, M., 2017. The Despot’s Guide to Wealth Management: On the International

Campaign Against Grand Corruption by Jason C. Sharman Cornell University Press, Ithaca,

NY, 2017 Pp. 274. ISBN 978 1 5017 0551 9. Asian‐Pacific Economic Literature, 31(2),

pp.145-148.

May, P.J., 2017. Art and Collectibles for Wealth Management. Financial Behavior: Players,

Services, Products, and Markets, p.422.

PERSONAL WEALTH MANAGEMENT

11

Mc Laughlin, L. and Buchanan, J., 2017. Revenue Administration; Implementing a High-

Wealth Individual Compliance Program (No. 17/07). International Monetary Fund.

Nolan, R.C., Wu, T.H. and Low, K.F. eds., 2018. Trusts and Modern Wealth Management.

Cambridge University Press.

Sharman, J.C., 2017. The Despot's Guide to Wealth Management: On the International

Campaign Against Grand Corruption. Cornell University Press.

Steinbach, A.L., Holcomb, T.R., Holmes, R.M., Devers, C.E. and Cannella, A.A., 2017. Top

management team incentive heterogeneity, strategic investment behavior, and performance:

A contingency theory of incentive alignment. Strategic Management Journal, 38(8), pp.1701-

1720.

Takacs Haynes, K., Campbell, J.T. and Hitt, M.A., 2017. When more is not enough:

Executive greed and its influence on shareholder wealth. Journal of Management, 43(2),

pp.555-584.

Uhl, M. and Rohner, P., 2017. The Future of Digital Wealth Management.

11

Mc Laughlin, L. and Buchanan, J., 2017. Revenue Administration; Implementing a High-

Wealth Individual Compliance Program (No. 17/07). International Monetary Fund.

Nolan, R.C., Wu, T.H. and Low, K.F. eds., 2018. Trusts and Modern Wealth Management.

Cambridge University Press.

Sharman, J.C., 2017. The Despot's Guide to Wealth Management: On the International

Campaign Against Grand Corruption. Cornell University Press.

Steinbach, A.L., Holcomb, T.R., Holmes, R.M., Devers, C.E. and Cannella, A.A., 2017. Top

management team incentive heterogeneity, strategic investment behavior, and performance:

A contingency theory of incentive alignment. Strategic Management Journal, 38(8), pp.1701-

1720.

Takacs Haynes, K., Campbell, J.T. and Hitt, M.A., 2017. When more is not enough:

Executive greed and its influence on shareholder wealth. Journal of Management, 43(2),

pp.555-584.

Uhl, M. and Rohner, P., 2017. The Future of Digital Wealth Management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.