Management Accounting and Finance for Decision Making Report Analysis

VerifiedAdded on 2023/01/11

|22

|6308

|90

Report

AI Summary

This report, focusing on Management Accounting and Finance for Decision Making, delves into the critical evaluation of International Financial Reporting Standards (IFRS) adoption and its impact on accounting practice harmonization. It analyzes financial statements, including balance sheets and income statements, for Honey Badger Plc and Alpha Ltd, computing working capital, working capital needs, and net cash. The report includes a common-size income statement analysis and a critical evaluation of company performance using profitability ratios. Task 2 focuses on Alpha Ltd's cash budgets, considering factors for decision-making, and a discussion of budgeting principles. The report examines the role and value of financial statements in strategic decision-making, covering both local and international contexts. It uses case studies to illustrate concepts and provides a comprehensive overview of financial reporting, analysis, and strategic management accounting models and concepts.

Management Accounting

And

Finance for Decision

Making

And

Finance for Decision

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

1. Evaluation of International Financial Reporting Standards (IFRS) adoption from the

perspective of prompting accounting practice harmonization................................................3

2. Simplified balance sheet with three sub-headings in the assets and three subheadings in the

equity and liabilities:..............................................................................................................6

3. Computing the working capital, working capital need and net cash:.................................8

4. The common-size income statements for the 2016-2019 periods:.....................................9

5. Analysis of statements (Balance sheet & Income statement) and critical evaluation

performance of the company................................................................................................10

6. Computation of Profitability Ratios and analyses them from the perspective of gaining

insight into efficiency of use of company resources:...........................................................12

TASK 2..........................................................................................................................................14

1. Alpha Ltd’s cash budgets for months: October, November, and December this year and

January and February next:..................................................................................................14

2. List and comment on other factors that should be taken into account by the company

management when considering this proposal:......................................................................16

3. Budgeting:........................................................................................................................17

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

1. Evaluation of International Financial Reporting Standards (IFRS) adoption from the

perspective of prompting accounting practice harmonization................................................3

2. Simplified balance sheet with three sub-headings in the assets and three subheadings in the

equity and liabilities:..............................................................................................................6

3. Computing the working capital, working capital need and net cash:.................................8

4. The common-size income statements for the 2016-2019 periods:.....................................9

5. Analysis of statements (Balance sheet & Income statement) and critical evaluation

performance of the company................................................................................................10

6. Computation of Profitability Ratios and analyses them from the perspective of gaining

insight into efficiency of use of company resources:...........................................................12

TASK 2..........................................................................................................................................14

1. Alpha Ltd’s cash budgets for months: October, November, and December this year and

January and February next:..................................................................................................14

2. List and comment on other factors that should be taken into account by the company

management when considering this proposal:......................................................................16

3. Budgeting:........................................................................................................................17

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

INTRODUCTION

Phase of decision-making can be seen as a control and balance mechanism which

keeps business rising vertically and linearly. That implies that the decision-making is directed at

a objective. The priorities are pre-set strategic targets, strategic planning and vision. The

organization may face several challenges in financial, organizational, marketing and tactical

spheres in achieving these objectives (Goh, 2019). These problems are addressed through

thorough decision-making. Management accounting and finance are two major aspects of

decision-making phase within every business enterprise. These both aspects cover almost all the

managerial and financial functions which are directly or indirectly assist or support decision

making. Further, such aspects also involve processes related to financial reporting, analysis of

financial reports and some models or concepts for strategic decision making (Quattrone, 2016).

The study covers critical examination of international financial reporting aspect and

current crucial international financial reporting challenges; and Comprehending role and

importance of the financial statements by evaluation and interpretation of the for the strategic

decision-making. Further study consists of critical review od range of major strategic

management-accounting-models and key concepts along with its crucial roles at the local &

international level. Study for all these purposes consists of two assessment based on case study

of (i) Honey Badger corporation which is primarily a producer, distributor and marketing entity

of the non-alcoholic product concentrates and syrup; and (ii) Alpha limited which makes a range

of products all of which follow a similar production process and have the same cost structure.

MAIN BODY

TASK 1

1. Evaluation of International Financial Reporting Standards (IFRS) adoption from the

perspective of prompting accounting practice harmonization

Most of world's countries have reshaped their accounting procedures in last few years of 21st

century particularly. These developments include adopting and modifying local accounting

procedures, and harmonization with International Financial Reporting Standards (IFRS) –

previously International Accounting Standards (IAS). Process of integration of the international

trade and corporate globalisation are on the rise. As a consequence, financial statements

compelled in accordance with local accounting system of nation can hardly fulfil needs of

Phase of decision-making can be seen as a control and balance mechanism which

keeps business rising vertically and linearly. That implies that the decision-making is directed at

a objective. The priorities are pre-set strategic targets, strategic planning and vision. The

organization may face several challenges in financial, organizational, marketing and tactical

spheres in achieving these objectives (Goh, 2019). These problems are addressed through

thorough decision-making. Management accounting and finance are two major aspects of

decision-making phase within every business enterprise. These both aspects cover almost all the

managerial and financial functions which are directly or indirectly assist or support decision

making. Further, such aspects also involve processes related to financial reporting, analysis of

financial reports and some models or concepts for strategic decision making (Quattrone, 2016).

The study covers critical examination of international financial reporting aspect and

current crucial international financial reporting challenges; and Comprehending role and

importance of the financial statements by evaluation and interpretation of the for the strategic

decision-making. Further study consists of critical review od range of major strategic

management-accounting-models and key concepts along with its crucial roles at the local &

international level. Study for all these purposes consists of two assessment based on case study

of (i) Honey Badger corporation which is primarily a producer, distributor and marketing entity

of the non-alcoholic product concentrates and syrup; and (ii) Alpha limited which makes a range

of products all of which follow a similar production process and have the same cost structure.

MAIN BODY

TASK 1

1. Evaluation of International Financial Reporting Standards (IFRS) adoption from the

perspective of prompting accounting practice harmonization

Most of world's countries have reshaped their accounting procedures in last few years of 21st

century particularly. These developments include adopting and modifying local accounting

procedures, and harmonization with International Financial Reporting Standards (IFRS) –

previously International Accounting Standards (IAS). Process of integration of the international

trade and corporate globalisation are on the rise. As a consequence, financial statements

compelled in accordance with local accounting system of nation can hardly fulfil needs of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

foreign investors, business partnerships, bankers and judgment-makers who are familiar with

global standards (Fuzi, Habidin, Janudin and Ong, 2019). In meantime, growing and evolving

markets are focus of world's leading sectors that operate in saturated western nations. To carry

out their operations in developed countries effectively; they have to follow the relevant

international-accounting standards. Furthermore, foreign direct investment is a big booster for

developing nations ' economies, and investor can require vivid and coherent financial

information-emphasizing why developing nations need to follow international financial reporting

standards. To overcome gap between country-specific reporting standards, International

Accounting Standards Committee (IASC) formed in 1973 by group of qualified accounting

professionals with goal of formulating universal and universal accounting practices towards

minimizing gaps in worldwide accounting principles as well as the reporting practices. In this

regard, it was suggested the International Accounting Standard (IAS), that has been vigorously

championing uniformity and uniformity of all the accounting standards. After that, IASB has

taken over from International Accounting Standard or IASC in Apr. 2001 setting of international

accounting standards. IASB has now revised and agreed to International Financial Reporting

Standards or IFRS as International Accounting Standard (IAS) and After that IFRS almost took

place of IAS (Inani and Gupta, 2017).

Harmonization is a method of rising the degree of International harmonization allows different

nations to follow same rules whilst producing a financial statement, such particular practices

allow different bookkeepers and professionals to understand financial reports of numerous

businesses corporations nationally or globally. Harmonization also makes it possible for

international investors, financial experts and global borrowers to grasp international corporations

' financial statements and comparing investment incentives and enable them make best

investment decisions. The national accounting harmonization framework viewed harmonization

as happening within geographically proximate nations. The foreign accounting harmonised

paradigm provides for border-less world in which accounting information are comparable

between nations and freely accessible to foreign users. consensus between nations as regards

accounting standards as well as practices and procedures. The adoption of the IFRS by a

corporation provides significant economic advantages in countries where financial reporting is

subject to strict regulation. Such advantages include an rise in fair market value of stock, a rise in

market competitiveness and a decrease in capital costs. When backed by a good regulatory

global standards (Fuzi, Habidin, Janudin and Ong, 2019). In meantime, growing and evolving

markets are focus of world's leading sectors that operate in saturated western nations. To carry

out their operations in developed countries effectively; they have to follow the relevant

international-accounting standards. Furthermore, foreign direct investment is a big booster for

developing nations ' economies, and investor can require vivid and coherent financial

information-emphasizing why developing nations need to follow international financial reporting

standards. To overcome gap between country-specific reporting standards, International

Accounting Standards Committee (IASC) formed in 1973 by group of qualified accounting

professionals with goal of formulating universal and universal accounting practices towards

minimizing gaps in worldwide accounting principles as well as the reporting practices. In this

regard, it was suggested the International Accounting Standard (IAS), that has been vigorously

championing uniformity and uniformity of all the accounting standards. After that, IASB has

taken over from International Accounting Standard or IASC in Apr. 2001 setting of international

accounting standards. IASB has now revised and agreed to International Financial Reporting

Standards or IFRS as International Accounting Standard (IAS) and After that IFRS almost took

place of IAS (Inani and Gupta, 2017).

Harmonization is a method of rising the degree of International harmonization allows different

nations to follow same rules whilst producing a financial statement, such particular practices

allow different bookkeepers and professionals to understand financial reports of numerous

businesses corporations nationally or globally. Harmonization also makes it possible for

international investors, financial experts and global borrowers to grasp international corporations

' financial statements and comparing investment incentives and enable them make best

investment decisions. The national accounting harmonization framework viewed harmonization

as happening within geographically proximate nations. The foreign accounting harmonised

paradigm provides for border-less world in which accounting information are comparable

between nations and freely accessible to foreign users. consensus between nations as regards

accounting standards as well as practices and procedures. The adoption of the IFRS by a

corporation provides significant economic advantages in countries where financial reporting is

subject to strict regulation. Such advantages include an rise in fair market value of stock, a rise in

market competitiveness and a decrease in capital costs. When backed by a good regulatory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

climate, businesses with significant gaps in GAAP and IFRS requirements display the maximum

benefit. In fact, in earlier adopting companies, advantages are high not only in year of IFRS

transition but also in year that reporting process is formally required. Results support the

perception that good implementation of reporting requirements not only strengthens investor

clarity but also improves adopter's market share (Mirzaey, Jamshidi and Hojatpour, 2017).

Harmonization relaxes the growing complexities for financial bookkeepers in formulating and

consolidating financial statements, since they become considerably streamlined after

IFRS guidelines become followed. The MNCs benefit primarily from this. As the various

reporting obligations are decreased, which entails direct costs like data processing, categorisation

and auditing whereas still including indirect costs, primarily owing to reporting

requirements discrepancies. Although harmonising reduces users' total costs, especially in case

of MNCs, while adopting criteria in short run, it may increase costs, particularly where

investment in the capital assets is implicated. For example, accounting profession will need to be

excellently-aware and educated regarding the new guidelines, whilst adopting IFRSs. Similar

manner, colleges and universities will also need to rethink their curricula, especially concerned

to accounting profession.

Accounting harmonisation may intensify cross-border contamination, as this has been

seen that widespread adoption of IFRS decreases obstacles to cross-border investments and

encourages substantial foreign equity investments within jurisdictions adopted by IFRS. As a

reaction to their local detrimental market disruptions, the enhanced globalization of

investors bases encouraged by IFRS adoption allows local markets increasingly vulnerable to

international threats via foreign investor exchange. In response to direct transfer of contagion

owing to trading activity by international investors, accounting harmonization will promote

comparative comparability throughout 20 national boundaries between companies and

marketplaces. For example, unfavourable circumstances can escalate to financial uncertainty in

one nation may alter investor expectations about yet another nation's financial stability, leading

other investors to withdrawal of capital for fear of more market stresses. In the face of

incomplete information, investors could exaggerate the degree to which data signals can be

extrapolated across nations, leading in inaccurate cross-inferences as well as contagion

(Rikhardsson and Yigitbasioglu, 2018).

benefit. In fact, in earlier adopting companies, advantages are high not only in year of IFRS

transition but also in year that reporting process is formally required. Results support the

perception that good implementation of reporting requirements not only strengthens investor

clarity but also improves adopter's market share (Mirzaey, Jamshidi and Hojatpour, 2017).

Harmonization relaxes the growing complexities for financial bookkeepers in formulating and

consolidating financial statements, since they become considerably streamlined after

IFRS guidelines become followed. The MNCs benefit primarily from this. As the various

reporting obligations are decreased, which entails direct costs like data processing, categorisation

and auditing whereas still including indirect costs, primarily owing to reporting

requirements discrepancies. Although harmonising reduces users' total costs, especially in case

of MNCs, while adopting criteria in short run, it may increase costs, particularly where

investment in the capital assets is implicated. For example, accounting profession will need to be

excellently-aware and educated regarding the new guidelines, whilst adopting IFRSs. Similar

manner, colleges and universities will also need to rethink their curricula, especially concerned

to accounting profession.

Accounting harmonisation may intensify cross-border contamination, as this has been

seen that widespread adoption of IFRS decreases obstacles to cross-border investments and

encourages substantial foreign equity investments within jurisdictions adopted by IFRS. As a

reaction to their local detrimental market disruptions, the enhanced globalization of

investors bases encouraged by IFRS adoption allows local markets increasingly vulnerable to

international threats via foreign investor exchange. In response to direct transfer of contagion

owing to trading activity by international investors, accounting harmonization will promote

comparative comparability throughout 20 national boundaries between companies and

marketplaces. For example, unfavourable circumstances can escalate to financial uncertainty in

one nation may alter investor expectations about yet another nation's financial stability, leading

other investors to withdrawal of capital for fear of more market stresses. In the face of

incomplete information, investors could exaggerate the degree to which data signals can be

extrapolated across nations, leading in inaccurate cross-inferences as well as contagion

(Rikhardsson and Yigitbasioglu, 2018).

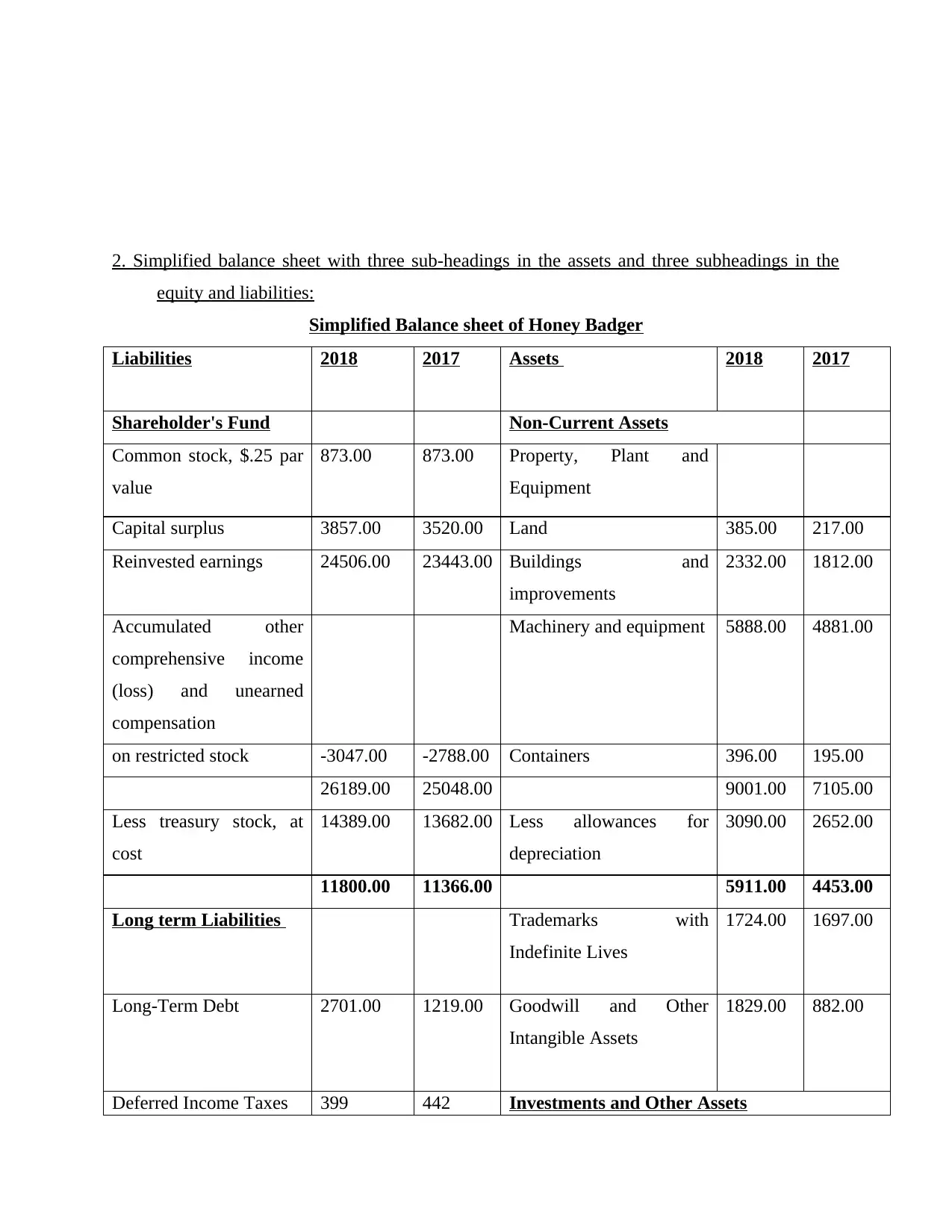

2. Simplified balance sheet with three sub-headings in the assets and three subheadings in the

equity and liabilities:

Simplified Balance sheet of Honey Badger

Liabilities 2018 2017 Assets 2018 2017

Shareholder's Fund Non-Current Assets

Common stock, $.25 par

value

873.00 873.00 Property, Plant and

Equipment

Capital surplus 3857.00 3520.00 Land 385.00 217.00

Reinvested earnings 24506.00 23443.00 Buildings and

improvements

2332.00 1812.00

Accumulated other

comprehensive income

(loss) and unearned

compensation

Machinery and equipment 5888.00 4881.00

on restricted stock -3047.00 -2788.00 Containers 396.00 195.00

26189.00 25048.00 9001.00 7105.00

Less treasury stock, at

cost

14389.00 13682.00 Less allowances for

depreciation

3090.00 2652.00

11800.00 11366.00 5911.00 4453.00

Long term Liabilities Trademarks with

Indefinite Lives

1724.00 1697.00

Long-Term Debt 2701.00 1219.00 Goodwill and Other

Intangible Assets

1829.00 882.00

Deferred Income Taxes 399 442 Investments and Other Assets

equity and liabilities:

Simplified Balance sheet of Honey Badger

Liabilities 2018 2017 Assets 2018 2017

Shareholder's Fund Non-Current Assets

Common stock, $.25 par

value

873.00 873.00 Property, Plant and

Equipment

Capital surplus 3857.00 3520.00 Land 385.00 217.00

Reinvested earnings 24506.00 23443.00 Buildings and

improvements

2332.00 1812.00

Accumulated other

comprehensive income

(loss) and unearned

compensation

Machinery and equipment 5888.00 4881.00

on restricted stock -3047.00 -2788.00 Containers 396.00 195.00

26189.00 25048.00 9001.00 7105.00

Less treasury stock, at

cost

14389.00 13682.00 Less allowances for

depreciation

3090.00 2652.00

11800.00 11366.00 5911.00 4453.00

Long term Liabilities Trademarks with

Indefinite Lives

1724.00 1697.00

Long-Term Debt 2701.00 1219.00 Goodwill and Other

Intangible Assets

1829.00 882.00

Deferred Income Taxes 399 442 Investments and Other Assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

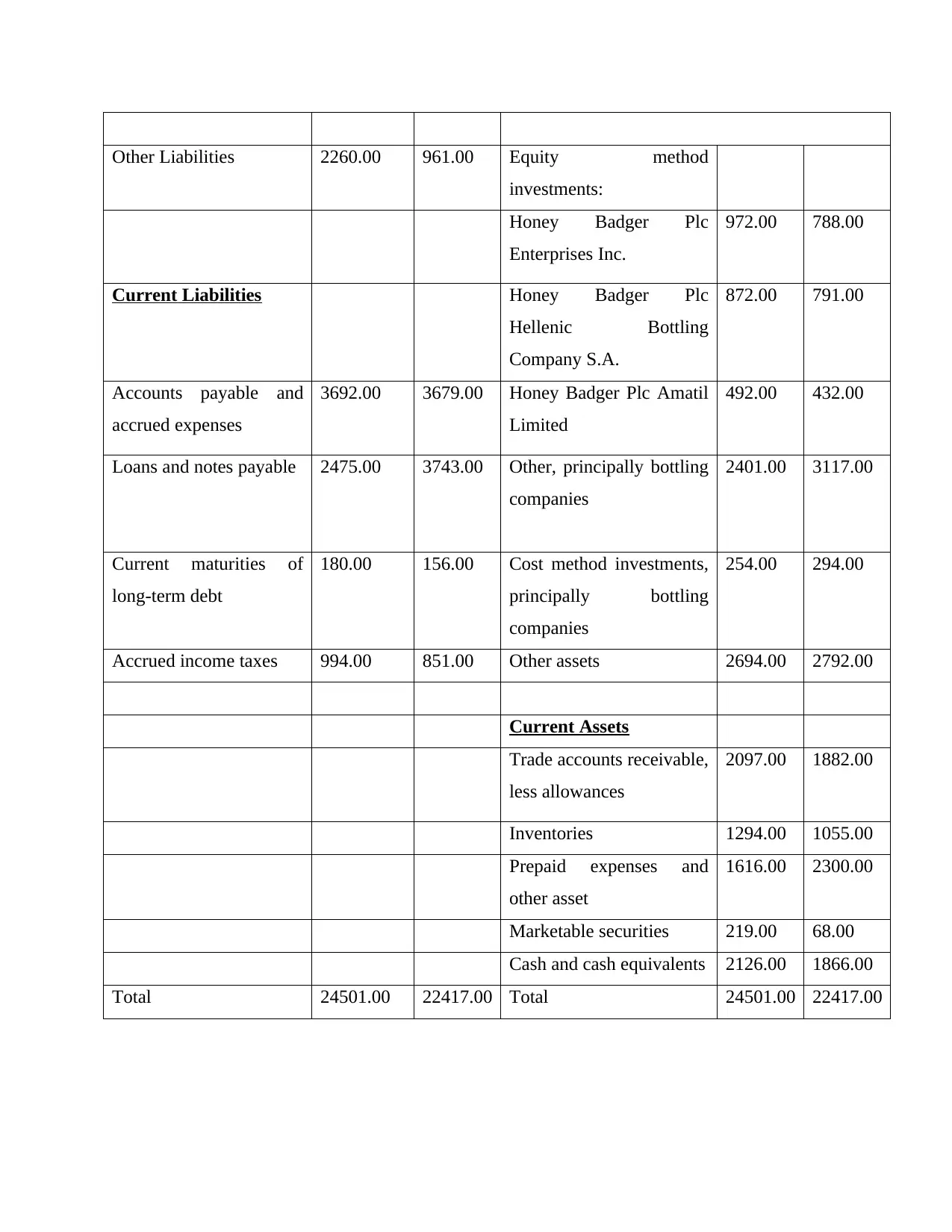

Other Liabilities 2260.00 961.00 Equity method

investments:

Honey Badger Plc

Enterprises Inc.

972.00 788.00

Current Liabilities Honey Badger Plc

Hellenic Bottling

Company S.A.

872.00 791.00

Accounts payable and

accrued expenses

3692.00 3679.00 Honey Badger Plc Amatil

Limited

492.00 432.00

Loans and notes payable 2475.00 3743.00 Other, principally bottling

companies

2401.00 3117.00

Current maturities of

long-term debt

180.00 156.00 Cost method investments,

principally bottling

companies

254.00 294.00

Accrued income taxes 994.00 851.00 Other assets 2694.00 2792.00

Current Assets

Trade accounts receivable,

less allowances

2097.00 1882.00

Inventories 1294.00 1055.00

Prepaid expenses and

other asset

1616.00 2300.00

Marketable securities 219.00 68.00

Cash and cash equivalents 2126.00 1866.00

Total 24501.00 22417.00 Total 24501.00 22417.00

investments:

Honey Badger Plc

Enterprises Inc.

972.00 788.00

Current Liabilities Honey Badger Plc

Hellenic Bottling

Company S.A.

872.00 791.00

Accounts payable and

accrued expenses

3692.00 3679.00 Honey Badger Plc Amatil

Limited

492.00 432.00

Loans and notes payable 2475.00 3743.00 Other, principally bottling

companies

2401.00 3117.00

Current maturities of

long-term debt

180.00 156.00 Cost method investments,

principally bottling

companies

254.00 294.00

Accrued income taxes 994.00 851.00 Other assets 2694.00 2792.00

Current Assets

Trade accounts receivable,

less allowances

2097.00 1882.00

Inventories 1294.00 1055.00

Prepaid expenses and

other asset

1616.00 2300.00

Marketable securities 219.00 68.00

Cash and cash equivalents 2126.00 1866.00

Total 24501.00 22417.00 Total 24501.00 22417.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

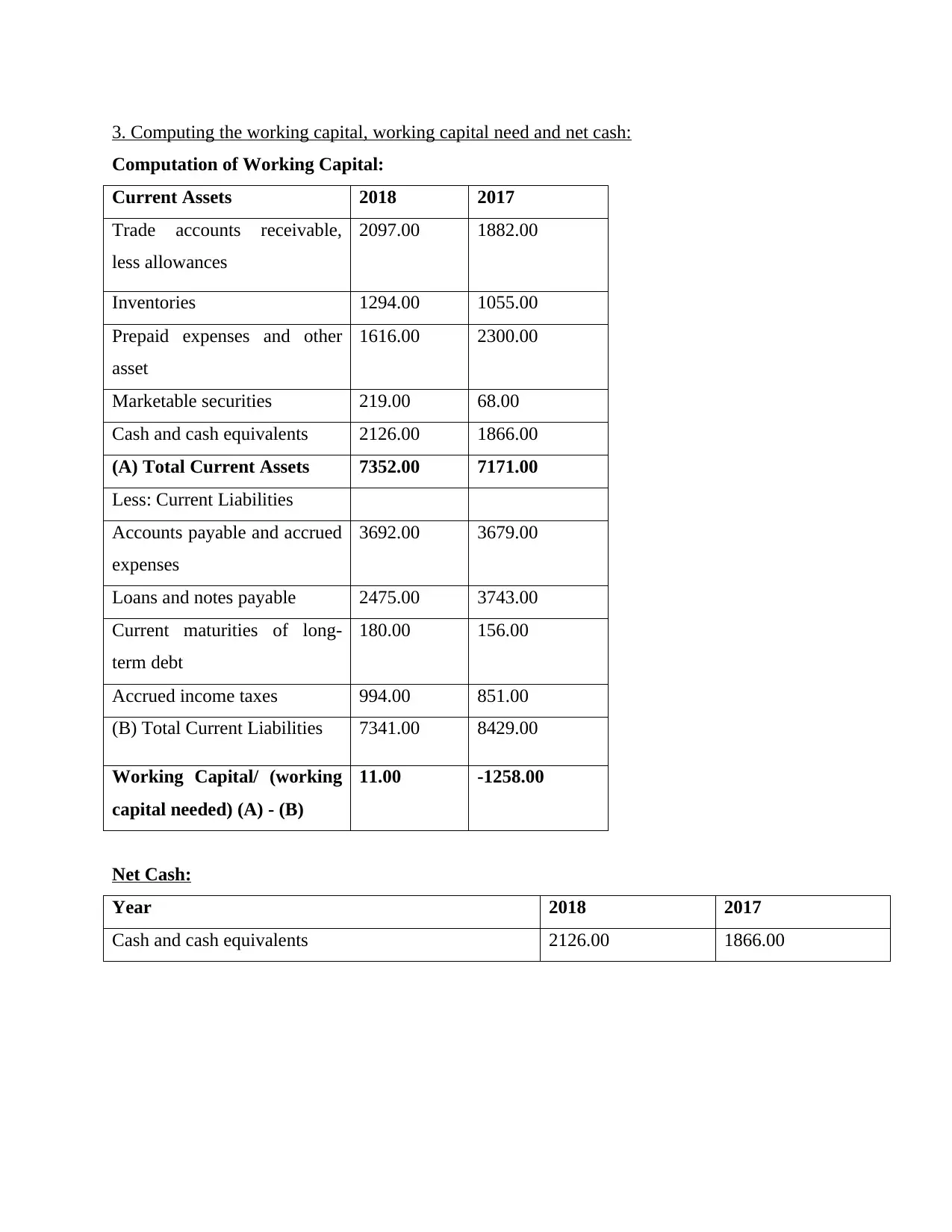

3. Computing the working capital, working capital need and net cash:

Computation of Working Capital:

Current Assets 2018 2017

Trade accounts receivable,

less allowances

2097.00 1882.00

Inventories 1294.00 1055.00

Prepaid expenses and other

asset

1616.00 2300.00

Marketable securities 219.00 68.00

Cash and cash equivalents 2126.00 1866.00

(A) Total Current Assets 7352.00 7171.00

Less: Current Liabilities

Accounts payable and accrued

expenses

3692.00 3679.00

Loans and notes payable 2475.00 3743.00

Current maturities of long-

term debt

180.00 156.00

Accrued income taxes 994.00 851.00

(B) Total Current Liabilities 7341.00 8429.00

Working Capital/ (working

capital needed) (A) - (B)

11.00 -1258.00

Net Cash:

Year 2018 2017

Cash and cash equivalents 2126.00 1866.00

Computation of Working Capital:

Current Assets 2018 2017

Trade accounts receivable,

less allowances

2097.00 1882.00

Inventories 1294.00 1055.00

Prepaid expenses and other

asset

1616.00 2300.00

Marketable securities 219.00 68.00

Cash and cash equivalents 2126.00 1866.00

(A) Total Current Assets 7352.00 7171.00

Less: Current Liabilities

Accounts payable and accrued

expenses

3692.00 3679.00

Loans and notes payable 2475.00 3743.00

Current maturities of long-

term debt

180.00 156.00

Accrued income taxes 994.00 851.00

(B) Total Current Liabilities 7341.00 8429.00

Working Capital/ (working

capital needed) (A) - (B)

11.00 -1258.00

Net Cash:

Year 2018 2017

Cash and cash equivalents 2126.00 1866.00

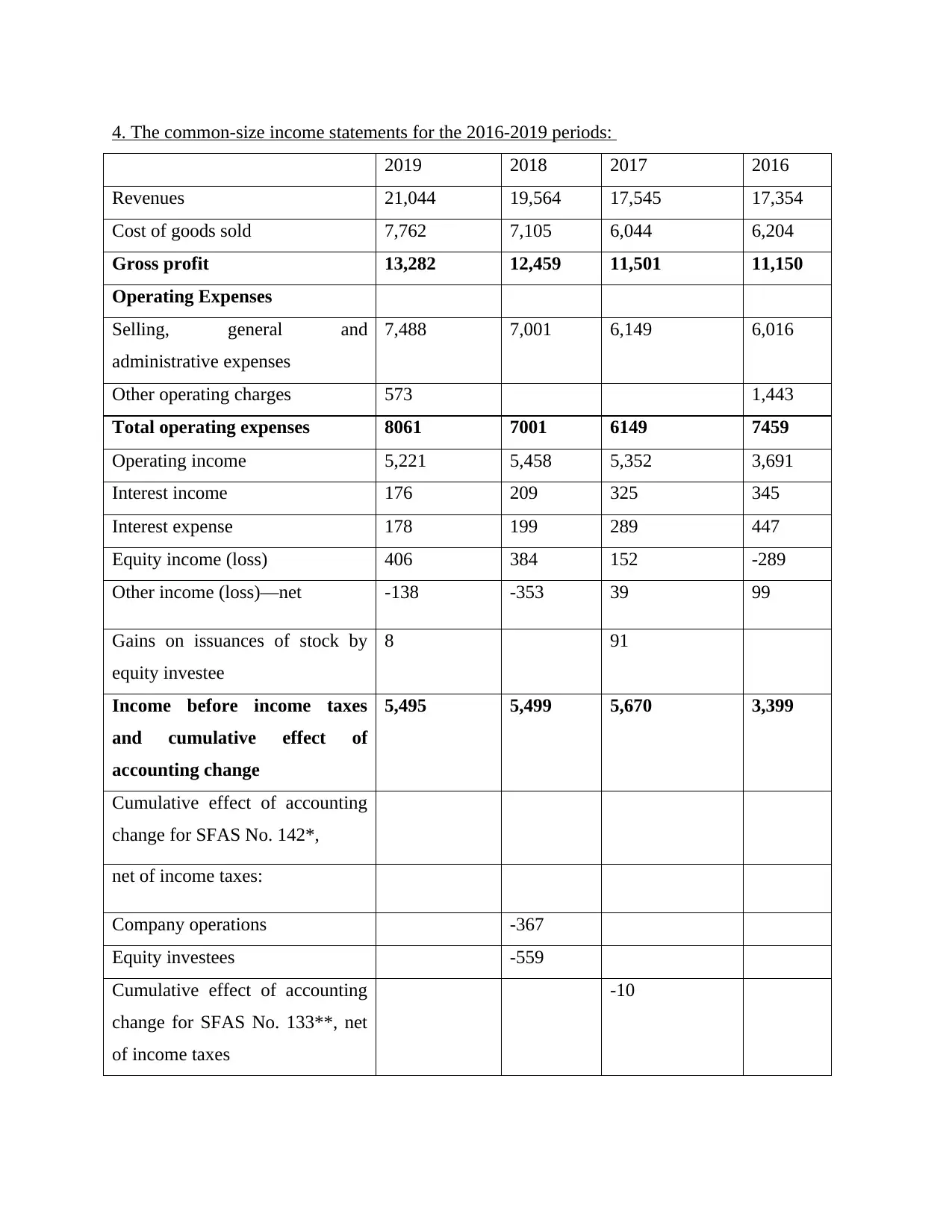

4. The common-size income statements for the 2016-2019 periods:

2019 2018 2017 2016

Revenues 21,044 19,564 17,545 17,354

Cost of goods sold 7,762 7,105 6,044 6,204

Gross profit 13,282 12,459 11,501 11,150

Operating Expenses

Selling, general and

administrative expenses

7,488 7,001 6,149 6,016

Other operating charges 573 1,443

Total operating expenses 8061 7001 6149 7459

Operating income 5,221 5,458 5,352 3,691

Interest income 176 209 325 345

Interest expense 178 199 289 447

Equity income (loss) 406 384 152 -289

Other income (loss)—net -138 -353 39 99

Gains on issuances of stock by

equity investee

8 91

Income before income taxes

and cumulative effect of

accounting change

5,495 5,499 5,670 3,399

Cumulative effect of accounting

change for SFAS No. 142*,

net of income taxes:

Company operations -367

Equity investees -559

Cumulative effect of accounting

change for SFAS No. 133**, net

of income taxes

-10

2019 2018 2017 2016

Revenues 21,044 19,564 17,545 17,354

Cost of goods sold 7,762 7,105 6,044 6,204

Gross profit 13,282 12,459 11,501 11,150

Operating Expenses

Selling, general and

administrative expenses

7,488 7,001 6,149 6,016

Other operating charges 573 1,443

Total operating expenses 8061 7001 6149 7459

Operating income 5,221 5,458 5,352 3,691

Interest income 176 209 325 345

Interest expense 178 199 289 447

Equity income (loss) 406 384 152 -289

Other income (loss)—net -138 -353 39 99

Gains on issuances of stock by

equity investee

8 91

Income before income taxes

and cumulative effect of

accounting change

5,495 5,499 5,670 3,399

Cumulative effect of accounting

change for SFAS No. 142*,

net of income taxes:

Company operations -367

Equity investees -559

Cumulative effect of accounting

change for SFAS No. 133**, net

of income taxes

-10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

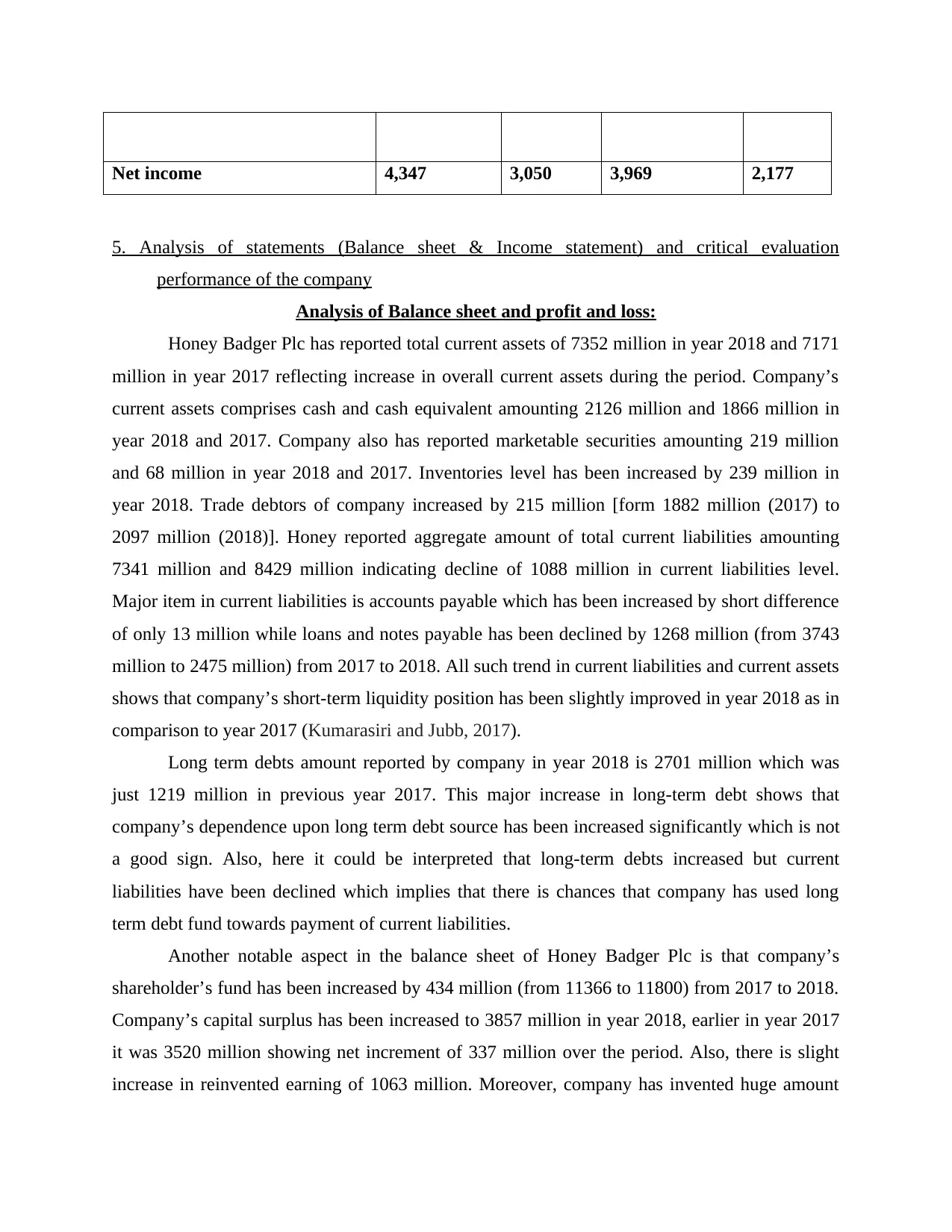

Net income 4,347 3,050 3,969 2,177

5. Analysis of statements (Balance sheet & Income statement) and critical evaluation

performance of the company

Analysis of Balance sheet and profit and loss:

Honey Badger Plc has reported total current assets of 7352 million in year 2018 and 7171

million in year 2017 reflecting increase in overall current assets during the period. Company’s

current assets comprises cash and cash equivalent amounting 2126 million and 1866 million in

year 2018 and 2017. Company also has reported marketable securities amounting 219 million

and 68 million in year 2018 and 2017. Inventories level has been increased by 239 million in

year 2018. Trade debtors of company increased by 215 million [form 1882 million (2017) to

2097 million (2018)]. Honey reported aggregate amount of total current liabilities amounting

7341 million and 8429 million indicating decline of 1088 million in current liabilities level.

Major item in current liabilities is accounts payable which has been increased by short difference

of only 13 million while loans and notes payable has been declined by 1268 million (from 3743

million to 2475 million) from 2017 to 2018. All such trend in current liabilities and current assets

shows that company’s short-term liquidity position has been slightly improved in year 2018 as in

comparison to year 2017 (Kumarasiri and Jubb, 2017).

Long term debts amount reported by company in year 2018 is 2701 million which was

just 1219 million in previous year 2017. This major increase in long-term debt shows that

company’s dependence upon long term debt source has been increased significantly which is not

a good sign. Also, here it could be interpreted that long-term debts increased but current

liabilities have been declined which implies that there is chances that company has used long

term debt fund towards payment of current liabilities.

Another notable aspect in the balance sheet of Honey Badger Plc is that company’s

shareholder’s fund has been increased by 434 million (from 11366 to 11800) from 2017 to 2018.

Company’s capital surplus has been increased to 3857 million in year 2018, earlier in year 2017

it was 3520 million showing net increment of 337 million over the period. Also, there is slight

increase in reinvented earning of 1063 million. Moreover, company has invented huge amount

5. Analysis of statements (Balance sheet & Income statement) and critical evaluation

performance of the company

Analysis of Balance sheet and profit and loss:

Honey Badger Plc has reported total current assets of 7352 million in year 2018 and 7171

million in year 2017 reflecting increase in overall current assets during the period. Company’s

current assets comprises cash and cash equivalent amounting 2126 million and 1866 million in

year 2018 and 2017. Company also has reported marketable securities amounting 219 million

and 68 million in year 2018 and 2017. Inventories level has been increased by 239 million in

year 2018. Trade debtors of company increased by 215 million [form 1882 million (2017) to

2097 million (2018)]. Honey reported aggregate amount of total current liabilities amounting

7341 million and 8429 million indicating decline of 1088 million in current liabilities level.

Major item in current liabilities is accounts payable which has been increased by short difference

of only 13 million while loans and notes payable has been declined by 1268 million (from 3743

million to 2475 million) from 2017 to 2018. All such trend in current liabilities and current assets

shows that company’s short-term liquidity position has been slightly improved in year 2018 as in

comparison to year 2017 (Kumarasiri and Jubb, 2017).

Long term debts amount reported by company in year 2018 is 2701 million which was

just 1219 million in previous year 2017. This major increase in long-term debt shows that

company’s dependence upon long term debt source has been increased significantly which is not

a good sign. Also, here it could be interpreted that long-term debts increased but current

liabilities have been declined which implies that there is chances that company has used long

term debt fund towards payment of current liabilities.

Another notable aspect in the balance sheet of Honey Badger Plc is that company’s

shareholder’s fund has been increased by 434 million (from 11366 to 11800) from 2017 to 2018.

Company’s capital surplus has been increased to 3857 million in year 2018, earlier in year 2017

it was 3520 million showing net increment of 337 million over the period. Also, there is slight

increase in reinvented earning of 1063 million. Moreover, company has invented huge amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

towards purchase and acquisition of Property, Plant and Equipment, since company has reported

Machinery and equipment amounting 4881 million in year 2017 which have been increased to

5888 million in year 2018. Company’s land value has been increased from 217 to 385 million

during 2017 to 2018. Building and improvements in year 2017 was 1812 million that have been

reached to 2332 million-year 2018. Containers was 195 million in year 2017 which have been

rise to 396 million in year 2018. These increase shows that company has made huge investment

towards capital assets. Company’s investment under equity method has been also increased

significantly. In Honey Badger Plc Enterprises Inc investment has been risen to 972 million in

year 2018 from 788 million in year 2017. Honey Badger Plc Hellenic Bottling Company S.A.

investment has been reached to 872 million from 791 million during 2017-2018. Investment in

Honey Badger Plc Amatil Limited has been increased to 492 million form 432 million while

investment in other, principally bottling companies has been declined from 3117 million to 2401

million from 2017 to 2018.

In intangible assets of company there is substantial increment has been reported. In year

2017 company has reported goodwill and other intangible asset of 882 million that has been

reached to 1829 million in year 2018. While value of Trademarks with Indefinite Lives has been

increased to 1724 million year 2018 which was of 1697 in year 2017. Other assets of company

have been changed form 2792 million to 2694 million showing a decline over the period. Overall

analysis of company’s balance sheet shows that company’s performance has been slightly

improved and as per analysis it will be improve more in coming years (Jackson, Lipe and

Waddoups, 2016).

In the income statement company has reported net operating revenue or sales amounting

21044 million, 19564 million, 17545 million and 17354 million in year 2019, 2018, 2017 and

2016 respectively displaying incremental trend in sales. Company’s gross profits are 13282

million, 12459 million, 11501million and 11150 million in year 2019, 2018, 2017 and 2016

respectively which reflect overall increasing or upward trend in gross profits. Selling expenses of

company have also been increased continuously during the period. Operating income of

company is 3691 million, 5352 million, 5458 million and 5221 million in year 2016, 2017, 2018

and 2019 showing upward trend in overall operating profits. Further company has reported Net

income of 4347 million,

Machinery and equipment amounting 4881 million in year 2017 which have been increased to

5888 million in year 2018. Company’s land value has been increased from 217 to 385 million

during 2017 to 2018. Building and improvements in year 2017 was 1812 million that have been

reached to 2332 million-year 2018. Containers was 195 million in year 2017 which have been

rise to 396 million in year 2018. These increase shows that company has made huge investment

towards capital assets. Company’s investment under equity method has been also increased

significantly. In Honey Badger Plc Enterprises Inc investment has been risen to 972 million in

year 2018 from 788 million in year 2017. Honey Badger Plc Hellenic Bottling Company S.A.

investment has been reached to 872 million from 791 million during 2017-2018. Investment in

Honey Badger Plc Amatil Limited has been increased to 492 million form 432 million while

investment in other, principally bottling companies has been declined from 3117 million to 2401

million from 2017 to 2018.

In intangible assets of company there is substantial increment has been reported. In year

2017 company has reported goodwill and other intangible asset of 882 million that has been

reached to 1829 million in year 2018. While value of Trademarks with Indefinite Lives has been

increased to 1724 million year 2018 which was of 1697 in year 2017. Other assets of company

have been changed form 2792 million to 2694 million showing a decline over the period. Overall

analysis of company’s balance sheet shows that company’s performance has been slightly

improved and as per analysis it will be improve more in coming years (Jackson, Lipe and

Waddoups, 2016).

In the income statement company has reported net operating revenue or sales amounting

21044 million, 19564 million, 17545 million and 17354 million in year 2019, 2018, 2017 and

2016 respectively displaying incremental trend in sales. Company’s gross profits are 13282

million, 12459 million, 11501million and 11150 million in year 2019, 2018, 2017 and 2016

respectively which reflect overall increasing or upward trend in gross profits. Selling expenses of

company have also been increased continuously during the period. Operating income of

company is 3691 million, 5352 million, 5458 million and 5221 million in year 2016, 2017, 2018

and 2019 showing upward trend in overall operating profits. Further company has reported Net

income of 4347 million,

million, 3969 million and 2177 million in year 2016, 2017, 2018 and 2019 respectively

exhibiting overall upward incremental trend over the period however, due to Cumulative effect

of accounting change and other losses company’s net income in year 2018 has ben declined but

this is temporary trend, as company has re-achieved growth in net income in year 2019.

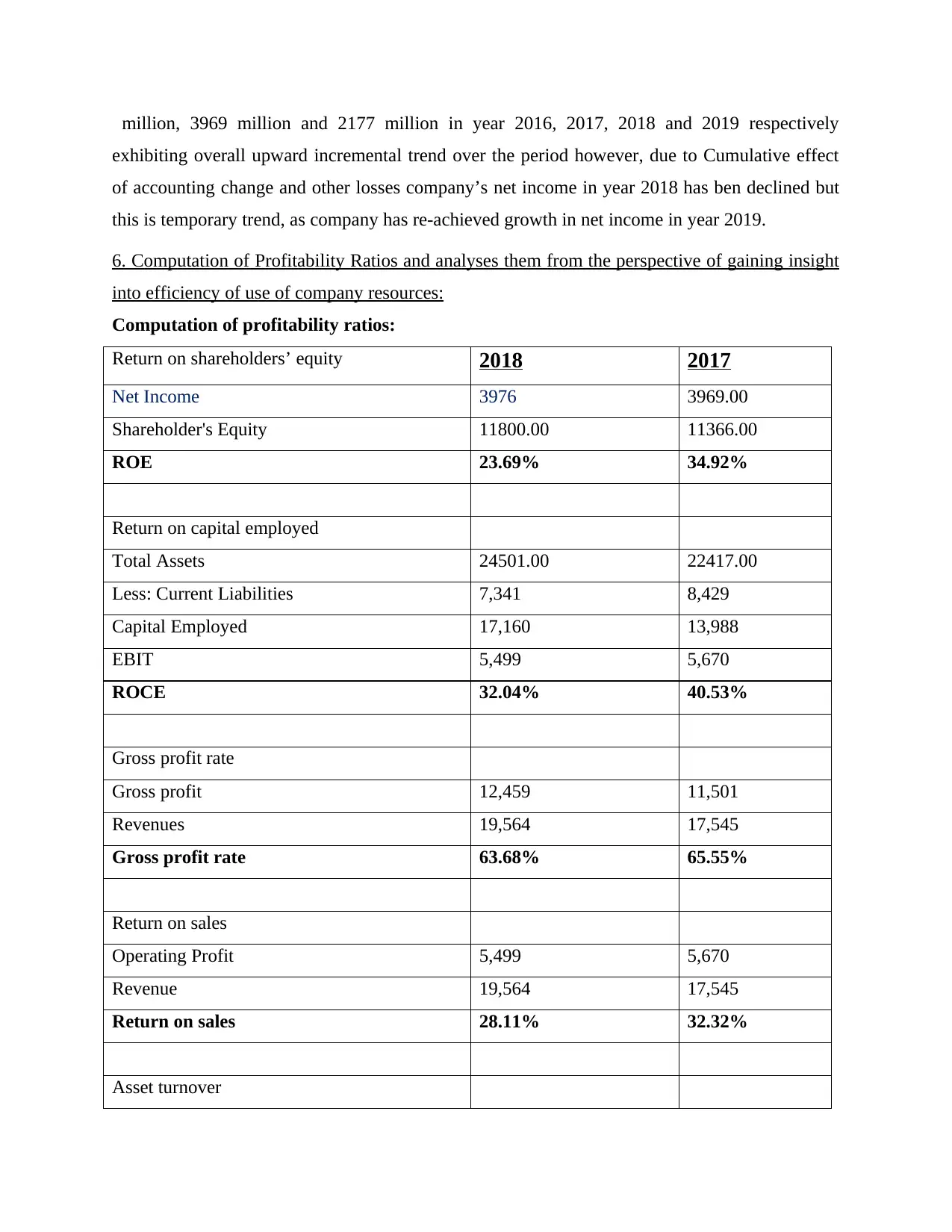

6. Computation of Profitability Ratios and analyses them from the perspective of gaining insight

into efficiency of use of company resources:

Computation of profitability ratios:

Return on shareholders’ equity 2018 2017

Net Income 3976 3969.00

Shareholder's Equity 11800.00 11366.00

ROE 23.69% 34.92%

Return on capital employed

Total Assets 24501.00 22417.00

Less: Current Liabilities 7,341 8,429

Capital Employed 17,160 13,988

EBIT 5,499 5,670

ROCE 32.04% 40.53%

Gross profit rate

Gross profit 12,459 11,501

Revenues 19,564 17,545

Gross profit rate 63.68% 65.55%

Return on sales

Operating Profit 5,499 5,670

Revenue 19,564 17,545

Return on sales 28.11% 32.32%

Asset turnover

exhibiting overall upward incremental trend over the period however, due to Cumulative effect

of accounting change and other losses company’s net income in year 2018 has ben declined but

this is temporary trend, as company has re-achieved growth in net income in year 2019.

6. Computation of Profitability Ratios and analyses them from the perspective of gaining insight

into efficiency of use of company resources:

Computation of profitability ratios:

Return on shareholders’ equity 2018 2017

Net Income 3976 3969.00

Shareholder's Equity 11800.00 11366.00

ROE 23.69% 34.92%

Return on capital employed

Total Assets 24501.00 22417.00

Less: Current Liabilities 7,341 8,429

Capital Employed 17,160 13,988

EBIT 5,499 5,670

ROCE 32.04% 40.53%

Gross profit rate

Gross profit 12,459 11,501

Revenues 19,564 17,545

Gross profit rate 63.68% 65.55%

Return on sales

Operating Profit 5,499 5,670

Revenue 19,564 17,545

Return on sales 28.11% 32.32%

Asset turnover

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.