Managerial Accounting: Analysis of PH Company's Divisions

Added on 2023-06-04

4 Pages581 Words187 Views

MANAGERIAL ACCOUNTING

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

a) The company (PH) should not discontinue either of the units as the high profit witnessed in

Construction is owing to the low profitability and losses that the prefabrication and

construction division are witnessing. By discontinuing one or both of the divisions, the

sourcing of the prefabricated components and relevant transportation would be from an

outside vendor which may charge a higher price since it would not run the operations in loss

(Heisinger, 2014). This premise is being made on the assumption that the operations of

prefabrication and construction are efficient. It seems that the current crisis may be attributed

to the transfer not being at arm’s length thereby lowering the revenue realisation. On the

other hand, if there are efficiency issues with the prefabrication and construction, then the

same should be fixed and only in the event of these issues not being fixed should an outside

vendor be explored (Bhimani et. al., 2017).

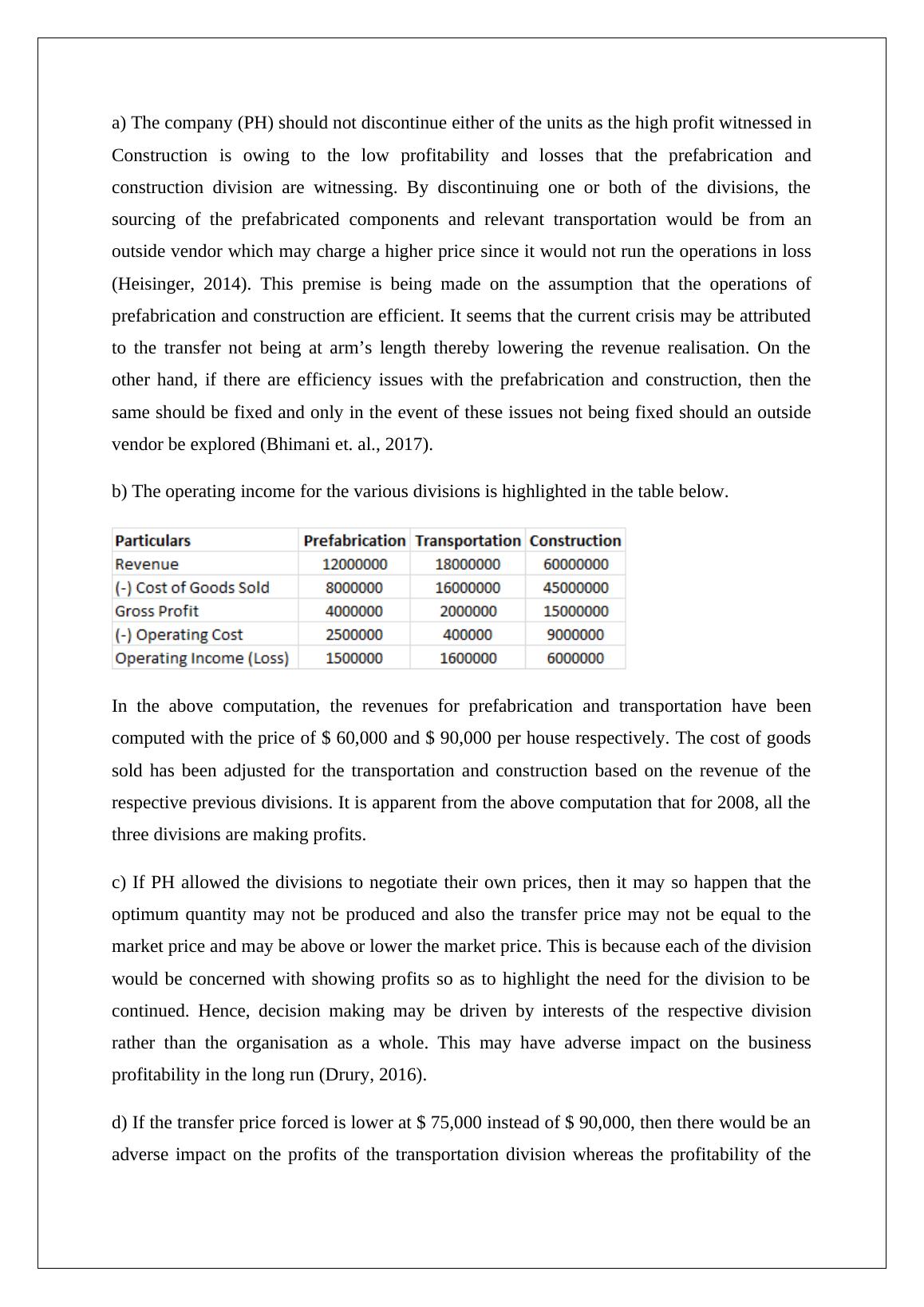

b) The operating income for the various divisions is highlighted in the table below.

In the above computation, the revenues for prefabrication and transportation have been

computed with the price of $ 60,000 and $ 90,000 per house respectively. The cost of goods

sold has been adjusted for the transportation and construction based on the revenue of the

respective previous divisions. It is apparent from the above computation that for 2008, all the

three divisions are making profits.

c) If PH allowed the divisions to negotiate their own prices, then it may so happen that the

optimum quantity may not be produced and also the transfer price may not be equal to the

market price and may be above or lower the market price. This is because each of the division

would be concerned with showing profits so as to highlight the need for the division to be

continued. Hence, decision making may be driven by interests of the respective division

rather than the organisation as a whole. This may have adverse impact on the business

profitability in the long run (Drury, 2016).

d) If the transfer price forced is lower at $ 75,000 instead of $ 90,000, then there would be an

adverse impact on the profits of the transportation division whereas the profitability of the

Construction is owing to the low profitability and losses that the prefabrication and

construction division are witnessing. By discontinuing one or both of the divisions, the

sourcing of the prefabricated components and relevant transportation would be from an

outside vendor which may charge a higher price since it would not run the operations in loss

(Heisinger, 2014). This premise is being made on the assumption that the operations of

prefabrication and construction are efficient. It seems that the current crisis may be attributed

to the transfer not being at arm’s length thereby lowering the revenue realisation. On the

other hand, if there are efficiency issues with the prefabrication and construction, then the

same should be fixed and only in the event of these issues not being fixed should an outside

vendor be explored (Bhimani et. al., 2017).

b) The operating income for the various divisions is highlighted in the table below.

In the above computation, the revenues for prefabrication and transportation have been

computed with the price of $ 60,000 and $ 90,000 per house respectively. The cost of goods

sold has been adjusted for the transportation and construction based on the revenue of the

respective previous divisions. It is apparent from the above computation that for 2008, all the

three divisions are making profits.

c) If PH allowed the divisions to negotiate their own prices, then it may so happen that the

optimum quantity may not be produced and also the transfer price may not be equal to the

market price and may be above or lower the market price. This is because each of the division

would be concerned with showing profits so as to highlight the need for the division to be

continued. Hence, decision making may be driven by interests of the respective division

rather than the organisation as a whole. This may have adverse impact on the business

profitability in the long run (Drury, 2016).

d) If the transfer price forced is lower at $ 75,000 instead of $ 90,000, then there would be an

adverse impact on the profits of the transportation division whereas the profitability of the

End of preview

Want to access all the pages? Upload your documents or become a member.