Pharmaceutical Company Ratio Analysis: A Financial Performance Review

VerifiedAdded on 2023/06/12

|23

|4360

|364

Report

AI Summary

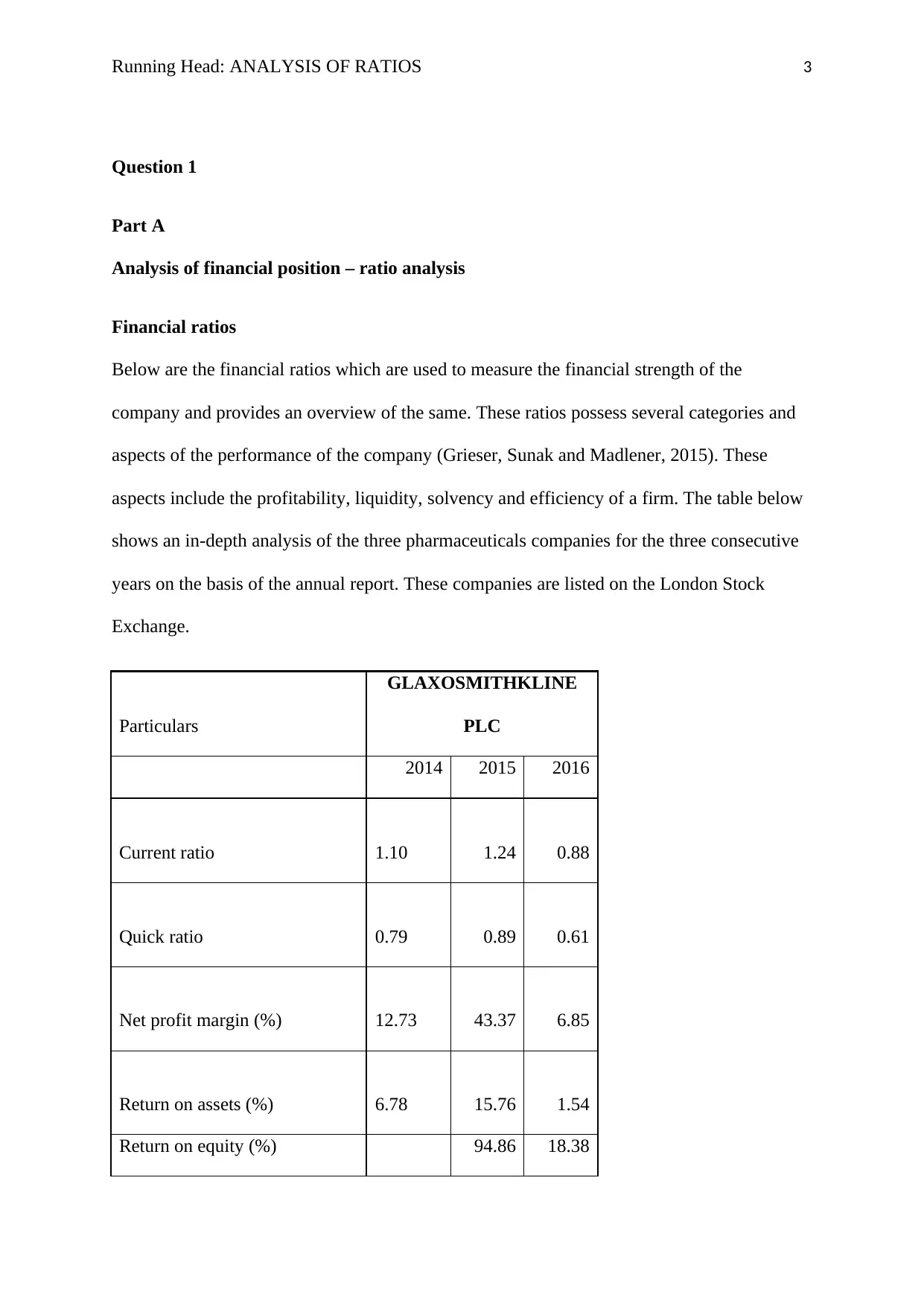

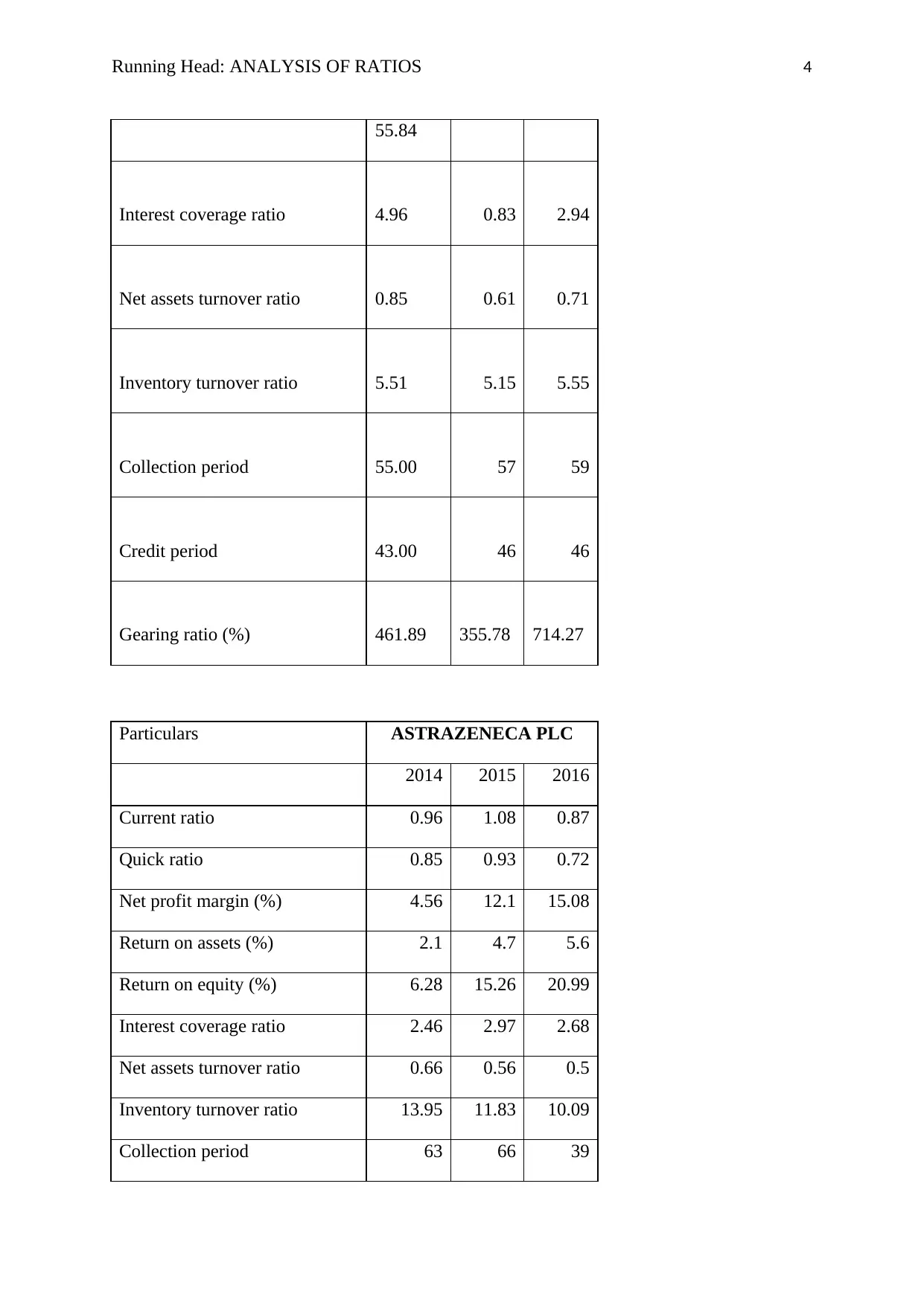

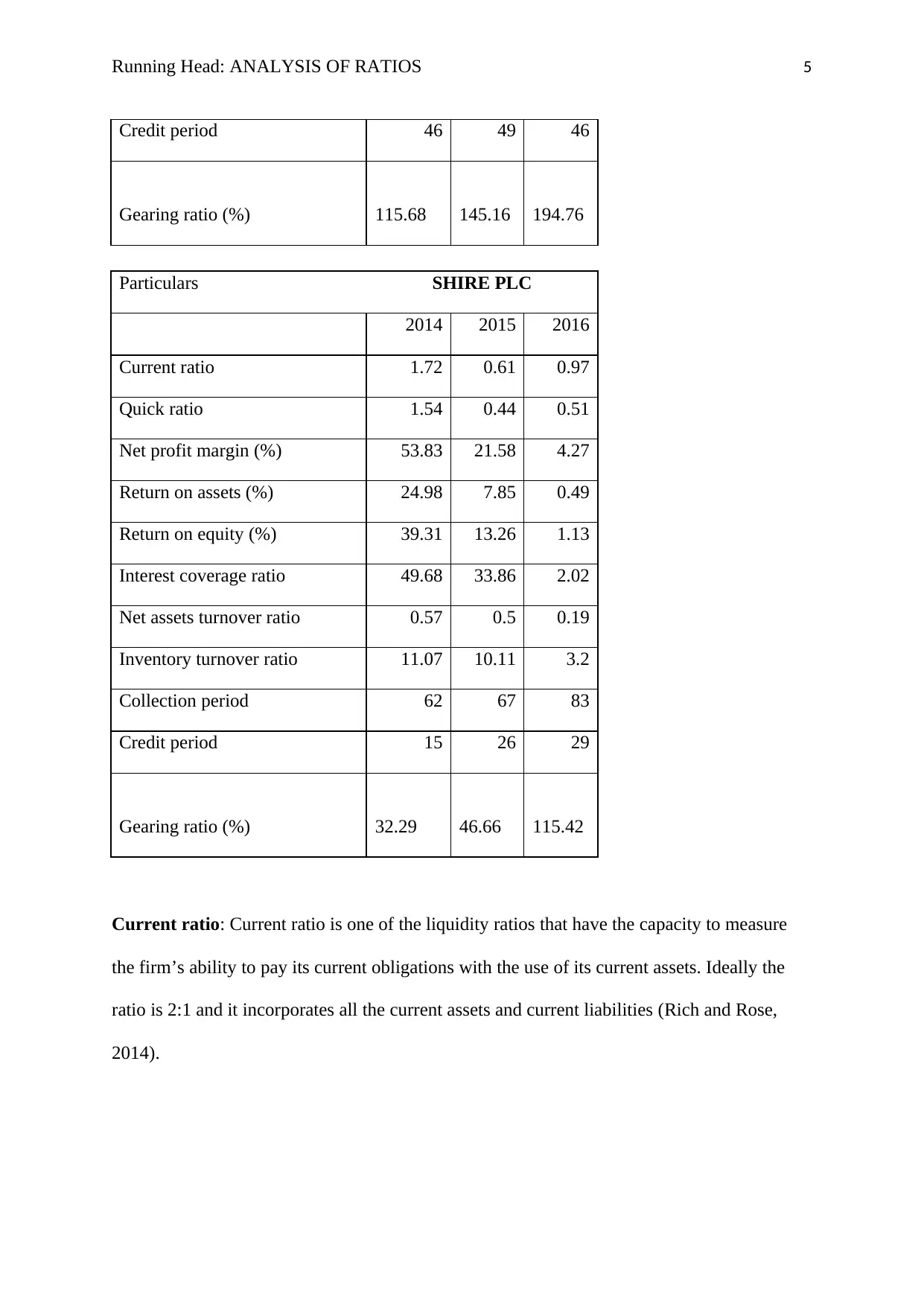

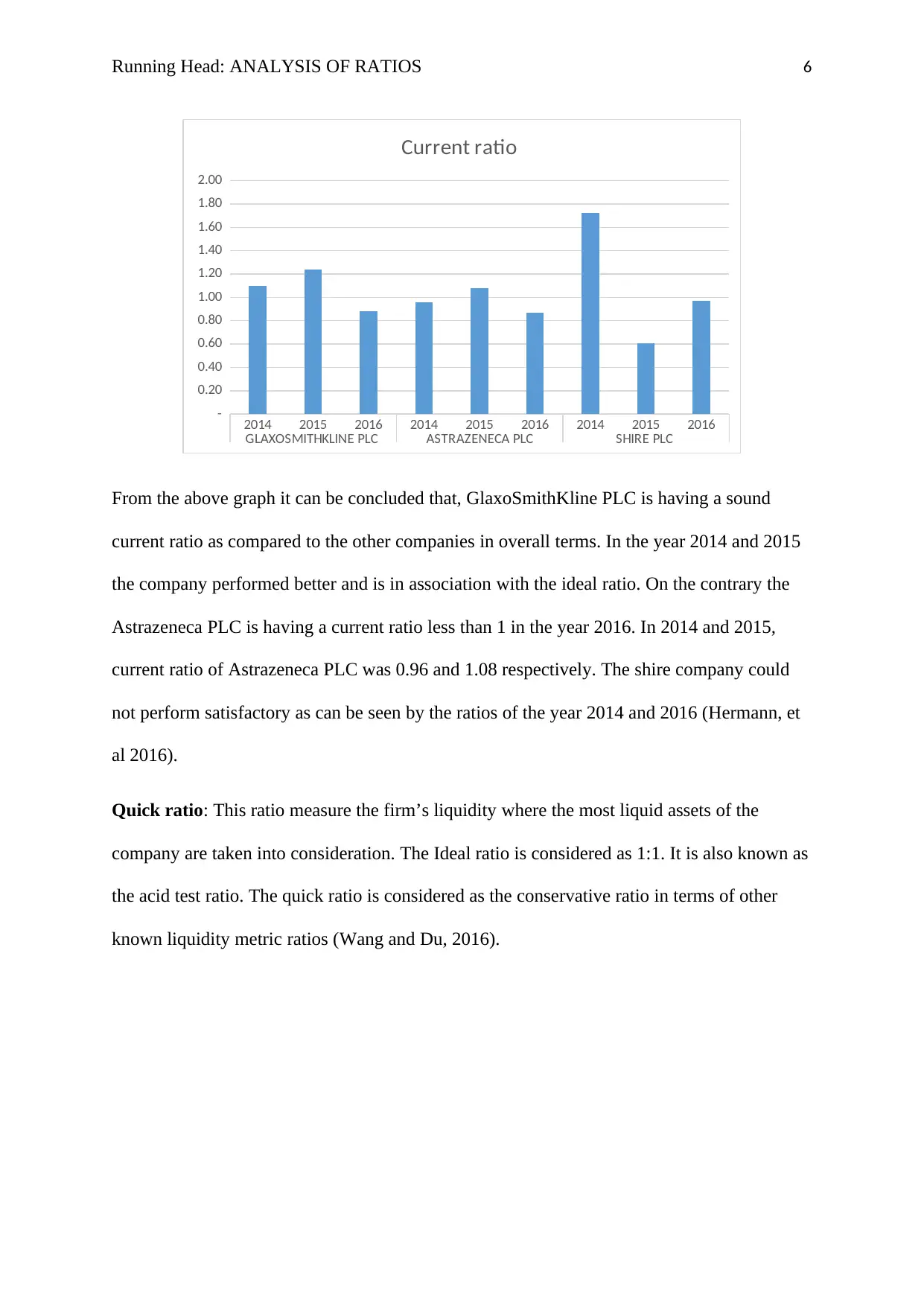

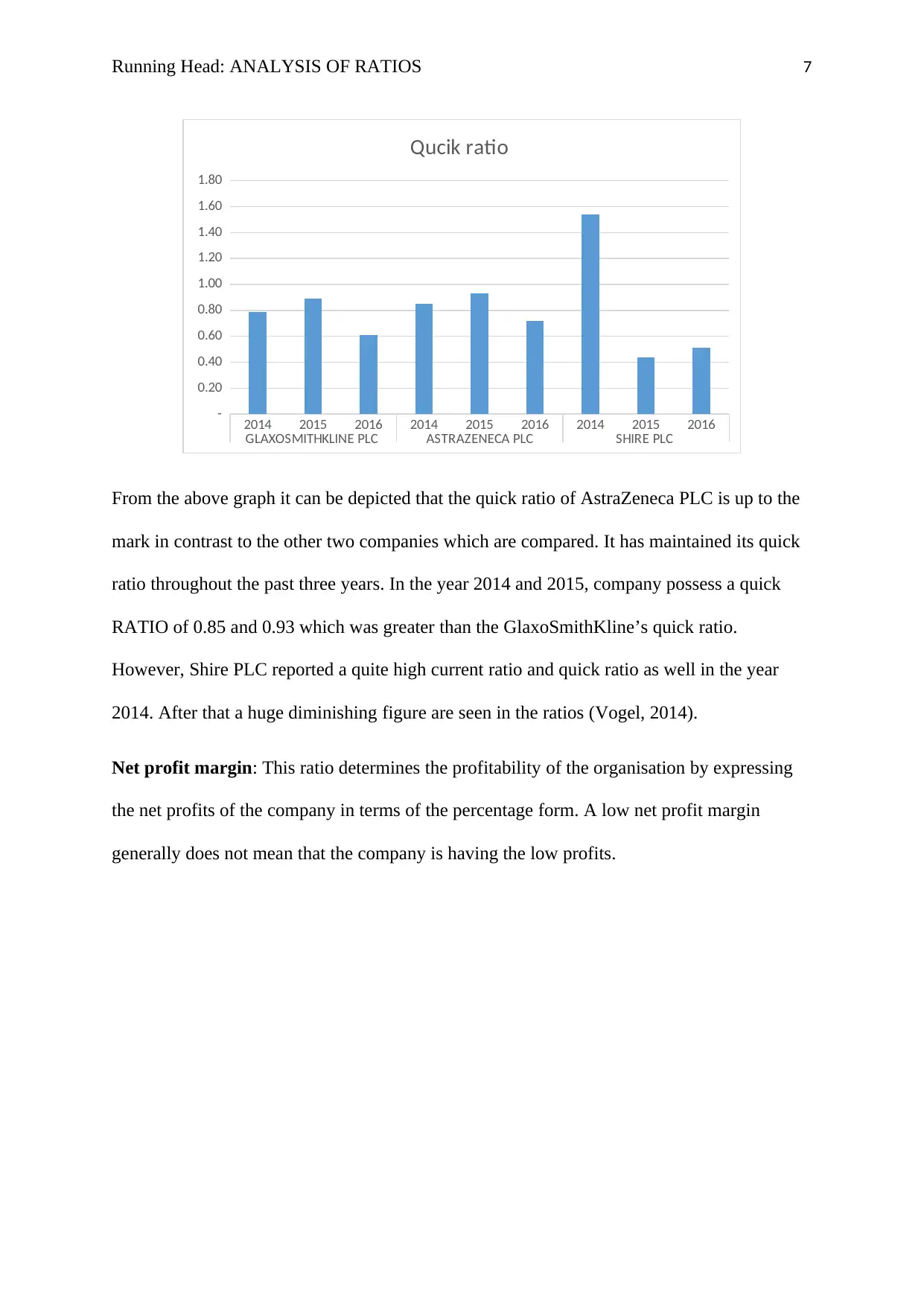

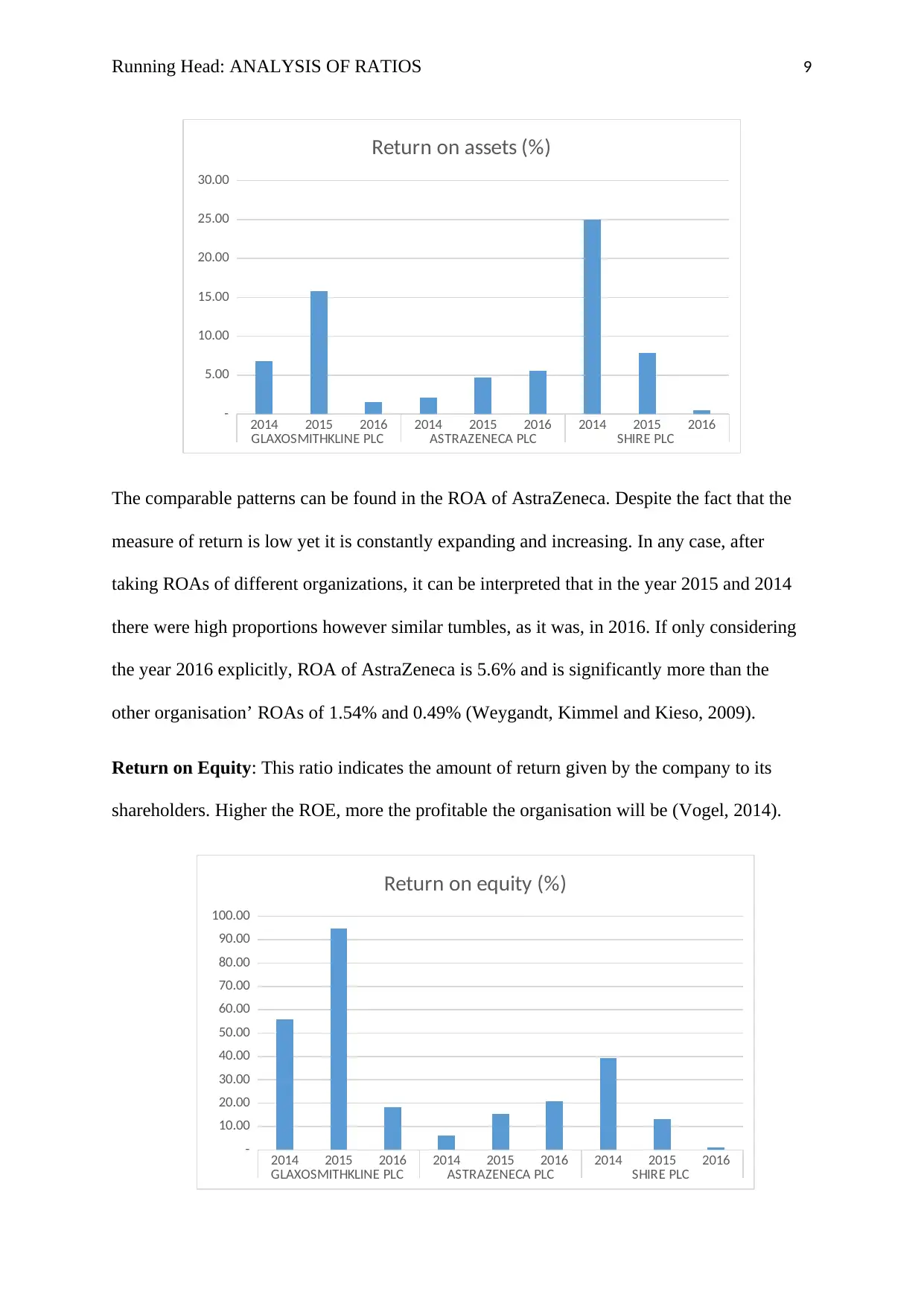

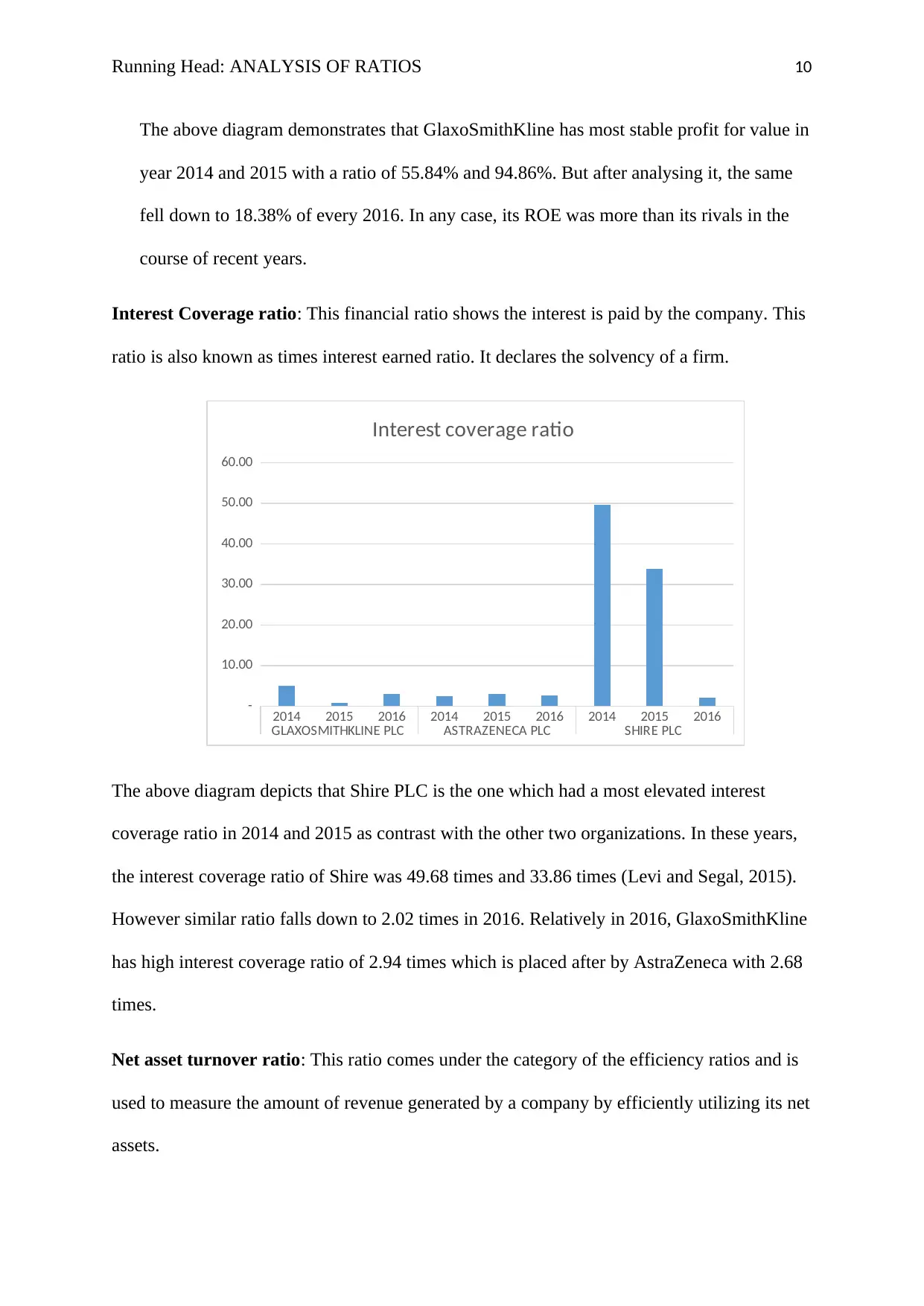

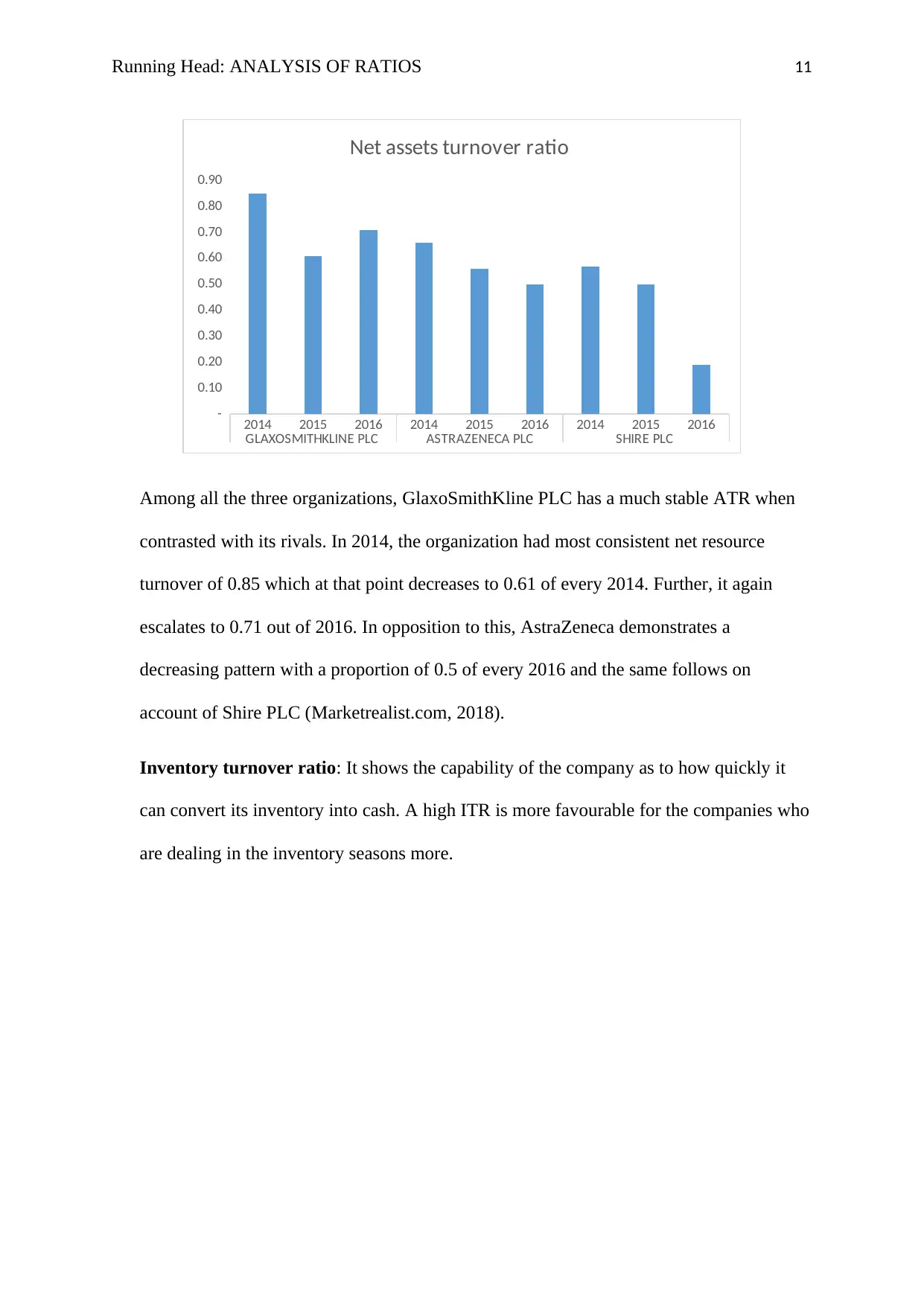

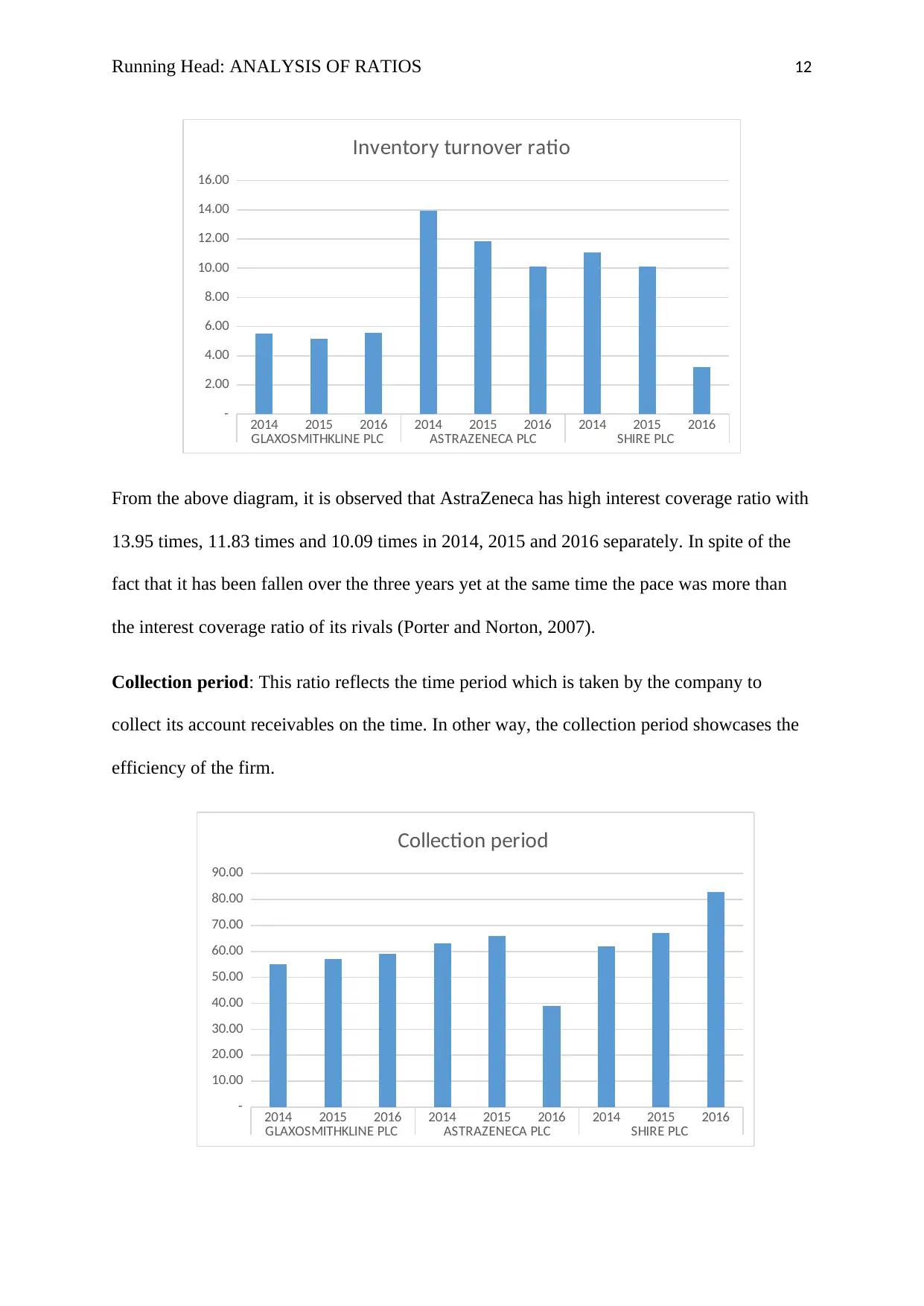

This report provides a detailed ratio analysis of three pharmaceutical companies listed on the London Stock Exchange: GlaxoSmithKline PLC, AstraZeneca PLC, and Shire PLC, over three consecutive years (2014-2016). It assesses their financial health using various financial ratios, including current ratio, quick ratio, net profit margin, return on assets, return on equity, interest coverage ratio, net asset turnover ratio, inventory turnover ratio, collection period, credit period, and gearing ratio. The analysis compares the performance of these companies across different dimensions such as liquidity, profitability, solvency, and efficiency, using graphs and interpretations to highlight key trends and differences. The report concludes by ranking the companies based on their overall financial performance and discusses potential implications for investors and stakeholders.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.