Clariton Ltd: Financial Sources, Planning, and Decision Making Report

VerifiedAdded on 2020/02/17

|18

|4360

|34

Report

AI Summary

This report analyzes the financial strategies of Clariton Antiques Ltd, focusing on its expansion plans and the need for funding. It explores various sources of finance, including personal savings, sales of assets, bank loans, venture capitalists, and government grants, evaluating the implications of each. The report identifies venture capitalists and bank loans as suitable sources, comparing their advantages and disadvantages. It further analyzes the costs and tax implications of these financing options, including dividends and interest. Financial planning, including budgeting and cash management, is highlighted as crucial for success. The report assesses the information needs of different decision-makers, such as partners, venture capitalists, and finance brokers. It also examines the impact of chosen financial sources on the company's final accounts, including profit and loss statements and balance sheets. A cash budget is prepared and analyzed to aid in decision-making, followed by the calculation of unit costs for pricing decisions and an evaluation of proposed investments. The report concludes with a discussion of financial statement components and the interpretation of Clariton's financial statements using ratio analysis.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

1.1 Sources of finance available to Clariton Ltd....................................................................3

1.2 Evaluating the implications of different sources of finance.............................................4

1.3 Identifying the suitable financial source of business.......................................................5

TASK 2......................................................................................................................................6

2.1 Analyse the cost of two source of finance with their tax implications............................6

2.2 Importance of financial planning for Clariton Antiques..................................................7

2.3 Assessing the information need of different decision makers.........................................7

2.4 Impact of financial source on final accounts....................................................................7

TASK 3......................................................................................................................................8

3.1 Preparing and analyzing cash budget for the purpose of decision making......................8

3.2 Calculating unit cost for taking pricing decision.............................................................9

3.3 Evaluating the viability of proposed investments..........................................................10

TASK 4....................................................................................................................................12

4.1 Discussing the components of financial statements.......................................................12

4.2 Comparison of the formats used by Clariton Antiques to present their financial

statements.............................................................................................................................13

4.3 Interpreting the financial statements of Clariton using ratios of current and previous

year.......................................................................................................................................13

CONCLUSION........................................................................................................................15

REFERENCES.........................................................................................................................16

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

1.1 Sources of finance available to Clariton Ltd....................................................................3

1.2 Evaluating the implications of different sources of finance.............................................4

1.3 Identifying the suitable financial source of business.......................................................5

TASK 2......................................................................................................................................6

2.1 Analyse the cost of two source of finance with their tax implications............................6

2.2 Importance of financial planning for Clariton Antiques..................................................7

2.3 Assessing the information need of different decision makers.........................................7

2.4 Impact of financial source on final accounts....................................................................7

TASK 3......................................................................................................................................8

3.1 Preparing and analyzing cash budget for the purpose of decision making......................8

3.2 Calculating unit cost for taking pricing decision.............................................................9

3.3 Evaluating the viability of proposed investments..........................................................10

TASK 4....................................................................................................................................12

4.1 Discussing the components of financial statements.......................................................12

4.2 Comparison of the formats used by Clariton Antiques to present their financial

statements.............................................................................................................................13

4.3 Interpreting the financial statements of Clariton using ratios of current and previous

year.......................................................................................................................................13

CONCLUSION........................................................................................................................15

REFERENCES.........................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management of financial resources is the main tasks or activity of the firm which lays

high level of emphasis on the assessment of deviations. By using monetary tools business

entity can identify the causes of deviations and thereby becomes able to develop highly

competent framework. This assignment is based Clariton Antique Ltd which is planning to

expand business operations and functions with the motive to widen the research. For

expansion purpose, business entities require fund for the establishment of another unit. In

this, report will describe the financial sources that can be undertaken by the owner to raise

funds. In addition to this, the main focus on such study is to highlight the manner in which

monetary tools and technique facilitate better and effective decision making.

TASK 1

1.1 Sources of finance available to Clariton Ltd

Unincorporated business

Personal savings: By using own savings sole trader can start venture more effectively

and efficiently. In this, business entity is not entitled to pay any kind of interest to

others which in turn may result into high savings.

Sales of fixed assets: Business entity of Clariton Ltd can enhance fund by selling

unused assets such as land, plant etc at their scrap value.

Short term lease: It is the most suitable source that can be undertaken by an

entrepreneur for fulfilling financial needs. On the basis of this aspect, by taking assets

like machinery, land & buildings, furniture’s and fixtures on lease entrepreneur can

implement the business idea within the suitable time frame.

Incorporated business

Clariton Ltd comes under the category of incorporated business that can raise funds

by considering following sources:

Bank loan: Entrepreneur can meet financial requirements by approaching to financial

institution. Interest is the major sources of income for banking institutions (Bergbrant,

Management of financial resources is the main tasks or activity of the firm which lays

high level of emphasis on the assessment of deviations. By using monetary tools business

entity can identify the causes of deviations and thereby becomes able to develop highly

competent framework. This assignment is based Clariton Antique Ltd which is planning to

expand business operations and functions with the motive to widen the research. For

expansion purpose, business entities require fund for the establishment of another unit. In

this, report will describe the financial sources that can be undertaken by the owner to raise

funds. In addition to this, the main focus on such study is to highlight the manner in which

monetary tools and technique facilitate better and effective decision making.

TASK 1

1.1 Sources of finance available to Clariton Ltd

Unincorporated business

Personal savings: By using own savings sole trader can start venture more effectively

and efficiently. In this, business entity is not entitled to pay any kind of interest to

others which in turn may result into high savings.

Sales of fixed assets: Business entity of Clariton Ltd can enhance fund by selling

unused assets such as land, plant etc at their scrap value.

Short term lease: It is the most suitable source that can be undertaken by an

entrepreneur for fulfilling financial needs. On the basis of this aspect, by taking assets

like machinery, land & buildings, furniture’s and fixtures on lease entrepreneur can

implement the business idea within the suitable time frame.

Incorporated business

Clariton Ltd comes under the category of incorporated business that can raise funds

by considering following sources:

Bank loan: Entrepreneur can meet financial requirements by approaching to financial

institution. Interest is the major sources of income for banking institutions (Bergbrant,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bradley and Hunter, 2017). Due to this, firms operated in banking sector are always

ready to offer financial assistance on the basis of collateral security.

Venture capitalists: With the aim to get higher returns now there are several venture

capitalists firm which offer financial advice to the firm (Abor, 2017). Such firms offer

both monetary and non-monetary advice to the entrepreneur and thereby make

contribution in the attainment of goals.

Government or European Union grant: To encourage entrepreneurial activities now

European Union provides monetary assistance to the business entities at cost effective

rates. Hence, by presenting plan to European Union committee firm can raise fund to

the significant level.

1.2 Evaluating the implications of different sources of finance

Sources of

finance

Financial Bankruptcy

(priority in

getting back

money: High to

low)

Legal Dilution of

control

Internal source of finance

Personal savings Opportunity cost

in the form of

loss on interest

on capital.

Least No legal

obligations

Low

Sales of assets Expenses in

relation to

registry,

advertisement

are considered

as financial

expenses.

Least Transfer of

ownership rights

Low

External sources of finance

Bank loan Interest on bank

loan

First priority Fulfillment of

documentary

formalities (Kim,

Song and Wang,

Moderate

ready to offer financial assistance on the basis of collateral security.

Venture capitalists: With the aim to get higher returns now there are several venture

capitalists firm which offer financial advice to the firm (Abor, 2017). Such firms offer

both monetary and non-monetary advice to the entrepreneur and thereby make

contribution in the attainment of goals.

Government or European Union grant: To encourage entrepreneurial activities now

European Union provides monetary assistance to the business entities at cost effective

rates. Hence, by presenting plan to European Union committee firm can raise fund to

the significant level.

1.2 Evaluating the implications of different sources of finance

Sources of

finance

Financial Bankruptcy

(priority in

getting back

money: High to

low)

Legal Dilution of

control

Internal source of finance

Personal savings Opportunity cost

in the form of

loss on interest

on capital.

Least No legal

obligations

Low

Sales of assets Expenses in

relation to

registry,

advertisement

are considered

as financial

expenses.

Least Transfer of

ownership rights

Low

External sources of finance

Bank loan Interest on bank

loan

First priority Fulfillment of

documentary

formalities (Kim,

Song and Wang,

Moderate

2017)

Leasing Rent on leased

assets

Lessor has right

to demand for

leased assets at

the time of

bankruptcy.

According to

legal aspects

business entity

is obliged to

make use of

assets in line

with the

contractual

terms.

Limited to

leased assets

European union

grant

In this, business

entity is obliged

to pay interest to

government

authority.

However,

interest rate is

negligible in the

case of

government

grant.

Government

authority also

has right to

demand for

monetary

assistance

provided when

business unit

becomes

bankrupt.

Disclosure of

suitable

information

regarding

business plan

Limited

Venture

capitalists

Dividend

imposes cost in

front of business

unit and thereby

affects

profitability

margin of firm

(Mehri, Jouaber-

Snoussi and

Hassan, 2017).

Least priority Offering of

shareholding

right to investors

such as

participation in

decision making

through voting.

1.3 Identifying the suitable financial source of business

Leasing Rent on leased

assets

Lessor has right

to demand for

leased assets at

the time of

bankruptcy.

According to

legal aspects

business entity

is obliged to

make use of

assets in line

with the

contractual

terms.

Limited to

leased assets

European union

grant

In this, business

entity is obliged

to pay interest to

government

authority.

However,

interest rate is

negligible in the

case of

government

grant.

Government

authority also

has right to

demand for

monetary

assistance

provided when

business unit

becomes

bankrupt.

Disclosure of

suitable

information

regarding

business plan

Limited

Venture

capitalists

Dividend

imposes cost in

front of business

unit and thereby

affects

profitability

margin of firm

(Mehri, Jouaber-

Snoussi and

Hassan, 2017).

Least priority Offering of

shareholding

right to investors

such as

participation in

decision making

through voting.

1.3 Identifying the suitable financial source of business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Clariton Antiques Ltd can meet monetary funds and requirements by undertaking

venture capitalists and bank loan source. Both such sources have following advantages and

disadvantage is enumerated below:

Venture capitalists

Advantages: In venture capitalists source, business entity offers dividend to investors

only when it earns enough amounts of profit. Thus, such source does not impose fixed

burden in front of company.

Disadvantages: Interference of investors in decision making is high in the case of

venture capitalists source (Mishra, Bag and Misra, 2017). Moreover, venture

capitalists have right to take part in the decision making aspect because they have

more concern towards the monetary aspect.

Bank loan

Advantages: In the case of bank loan, company enjoys tax exemption. This in turn

helps company in enhancing the profitability aspect to a great extent. Along with this,

in bank loan business unit repays the amount of loan in the form of installment

(Houston, Itzkowitz and Naranjo, 2017). In this way, such source offers high level of

convenience to the organization.

Disadvantages: In the case of loan, business entity to make payment of interest at

fixed rate which in turn affects working capital and financial position of firm.

TASK 2

2.1 Analyse the cost of two source of finance with their tax implications

Either collecting capital in the form of debt borrowings or going to public charges

several financial costs which are presented here as under:

Dividend: It is the monetary return which is required to be paid by Clariton Antiques

by distribution of profitability. With the current case, it is stated that company can gather

capital by transferring 20% stake to the venture capitalists and in return, firm has to distribute

a proportion of their net profitability in the form of dividend to their investors.

Interest: Clariton can also raise long-term debt borrowings from the commercial banks

and for such financial risk, bank will charge a fixed interest rate (Gilbert and et.al., 2017).

venture capitalists and bank loan source. Both such sources have following advantages and

disadvantage is enumerated below:

Venture capitalists

Advantages: In venture capitalists source, business entity offers dividend to investors

only when it earns enough amounts of profit. Thus, such source does not impose fixed

burden in front of company.

Disadvantages: Interference of investors in decision making is high in the case of

venture capitalists source (Mishra, Bag and Misra, 2017). Moreover, venture

capitalists have right to take part in the decision making aspect because they have

more concern towards the monetary aspect.

Bank loan

Advantages: In the case of bank loan, company enjoys tax exemption. This in turn

helps company in enhancing the profitability aspect to a great extent. Along with this,

in bank loan business unit repays the amount of loan in the form of installment

(Houston, Itzkowitz and Naranjo, 2017). In this way, such source offers high level of

convenience to the organization.

Disadvantages: In the case of loan, business entity to make payment of interest at

fixed rate which in turn affects working capital and financial position of firm.

TASK 2

2.1 Analyse the cost of two source of finance with their tax implications

Either collecting capital in the form of debt borrowings or going to public charges

several financial costs which are presented here as under:

Dividend: It is the monetary return which is required to be paid by Clariton Antiques

by distribution of profitability. With the current case, it is stated that company can gather

capital by transferring 20% stake to the venture capitalists and in return, firm has to distribute

a proportion of their net profitability in the form of dividend to their investors.

Interest: Clariton can also raise long-term debt borrowings from the commercial banks

and for such financial risk, bank will charge a fixed interest rate (Gilbert and et.al., 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Here, it is presented that Clariton can borrow required fund at 2% interest rate and also have

to pay brokerage at 1%. Thus, its cost can be computed here as under:

Interest: 500,000*2% = 10,000

Brokerage: 500,000*1% = 5,000

Cost of debt: 15,000/500,000*100 = 3%

Taxation: With respect to dividend, there is no tax benefits or relief will be exists to

the Clariton. In contrast, interest payment offers taxation allowance to the business because in

UK, regulatory body, HMRC provides tax relief to the establishment.

2.2 Importance of financial planning for Clariton Antiques

Financial planning is an important area of corporate growth and success which refers to

the procurement of required capital, its optimum & efficient utilization of the fund, cost-

curtailment, cash management and so on. The significance of monetary planning for Clariton

Antiques Ltd is enumerated below:

Budgeting: It is the most critical and important aspect which is regarded as the process

of estimating or anticipating potential capital requirement and possible cost that it will incur

in the forthcoming years. By making budgets for every year, Clariton can detect possible

monetary consequences and design remedial strategies accordingly (Bonaimé, Hankins and

Jordan, 2016).

Consequences of failure to manage funds: Not only the collection of fund is sufficient

for the Clariton to support its expansion plan but also it is essential to make sure that the

funds has been utilized in an efficient and proper way at minimal cost in order to drive better

return. Lack of funds may cause serious cash problems and affects corporate functions in an

adverse manner.

Over-trading: Aggressive expansion and sudden increase in the borrowed capital can

cause excessive cash shortfall due to shortage of cash and affects day-to-day activities of

business in an adverse way (Gilbert and et.al., 2017). It may liquidity and working capital

problems, therefore, Clariton must take extra care to eliminate such situation.

2.3 Assessing the information need of different decision makers

Partners: They are highly concerned towards the financial performance and position

of firm. Hence, after making assessment of monetary aspects partners decide whether

they need to invest additional funds or not.

Venture capitalists: Firms like ‘we finance limited’ evaluates the viability of business

plan. Thus, venture capitalists make assessment of market trend, competitor’s strategy

to pay brokerage at 1%. Thus, its cost can be computed here as under:

Interest: 500,000*2% = 10,000

Brokerage: 500,000*1% = 5,000

Cost of debt: 15,000/500,000*100 = 3%

Taxation: With respect to dividend, there is no tax benefits or relief will be exists to

the Clariton. In contrast, interest payment offers taxation allowance to the business because in

UK, regulatory body, HMRC provides tax relief to the establishment.

2.2 Importance of financial planning for Clariton Antiques

Financial planning is an important area of corporate growth and success which refers to

the procurement of required capital, its optimum & efficient utilization of the fund, cost-

curtailment, cash management and so on. The significance of monetary planning for Clariton

Antiques Ltd is enumerated below:

Budgeting: It is the most critical and important aspect which is regarded as the process

of estimating or anticipating potential capital requirement and possible cost that it will incur

in the forthcoming years. By making budgets for every year, Clariton can detect possible

monetary consequences and design remedial strategies accordingly (Bonaimé, Hankins and

Jordan, 2016).

Consequences of failure to manage funds: Not only the collection of fund is sufficient

for the Clariton to support its expansion plan but also it is essential to make sure that the

funds has been utilized in an efficient and proper way at minimal cost in order to drive better

return. Lack of funds may cause serious cash problems and affects corporate functions in an

adverse manner.

Over-trading: Aggressive expansion and sudden increase in the borrowed capital can

cause excessive cash shortfall due to shortage of cash and affects day-to-day activities of

business in an adverse way (Gilbert and et.al., 2017). It may liquidity and working capital

problems, therefore, Clariton must take extra care to eliminate such situation.

2.3 Assessing the information need of different decision makers

Partners: They are highly concerned towards the financial performance and position

of firm. Hence, after making assessment of monetary aspects partners decide whether

they need to invest additional funds or not.

Venture capitalists: Firms like ‘we finance limited’ evaluates the viability of business

plan. Thus, venture capitalists make assessment of market trend, competitor’s strategy

and position, current performance, customer base etc (Abor, 2017). By evaluating all

such aspect venture capitalists firm take investment decision.

Finance broker: To prepare sound plan finance broker requires information regarding

the profitability, liquidity and solvency aspect. Thus, after making assessment of all

such aspects broker can make competent plan.

2.4 Impact of financial source on final accounts

Selected sources of finance have following impact on final accounts in the following

manner:

Venture capitalists: In the case of venture capitalists Clariton Ltd will offer return to

the investors in the form of dividend. Hence, it is cost for the company so dividend

expenses are recorded in the debit side of profitability statement. In addition to this,

venture capitalists fund is recorded in liabilities side because firm has to repay this at

the time of dissolution of firm (Mehri, Jouaber-Snoussi and Hassan, 2017). Further,

cash side of balance sheet will also increase with the similar amount that is invested

by venture capitalists firm such as ‘We Finance Ltd’.

Bank loan and Finance broker: Interest and brokerage are the main expenses which

are associated with such source. Hence, both these expenses are recorded in the debit

side of income statement. Along with this, bank loan is recognized as liability or long

term obligation which business unit has to fulfill after specific time period. In

accordance with dual side effect cash side of balance sheet will incline significantly.

TASK 3

3.1 Preparing and analyzing cash budget for the purpose of decision making

Cash budget may be served as a framework which exhibits monetary inflow and

outflow (Abor, 2017). Budget acts as a guide which in turn provides assistance to the

personnel in spending money more effectually.

Cash budget from the period of January to June is enumerated below:

Particula

rs

Januar

y (in £)

Februar

y (in £)

Marc

h (in

£)

April

(in £)

May

(in £)

June

(in £)

Opening

cash 110000 -539750

-

39200

-

76750 48500

16625

0

such aspect venture capitalists firm take investment decision.

Finance broker: To prepare sound plan finance broker requires information regarding

the profitability, liquidity and solvency aspect. Thus, after making assessment of all

such aspects broker can make competent plan.

2.4 Impact of financial source on final accounts

Selected sources of finance have following impact on final accounts in the following

manner:

Venture capitalists: In the case of venture capitalists Clariton Ltd will offer return to

the investors in the form of dividend. Hence, it is cost for the company so dividend

expenses are recorded in the debit side of profitability statement. In addition to this,

venture capitalists fund is recorded in liabilities side because firm has to repay this at

the time of dissolution of firm (Mehri, Jouaber-Snoussi and Hassan, 2017). Further,

cash side of balance sheet will also increase with the similar amount that is invested

by venture capitalists firm such as ‘We Finance Ltd’.

Bank loan and Finance broker: Interest and brokerage are the main expenses which

are associated with such source. Hence, both these expenses are recorded in the debit

side of income statement. Along with this, bank loan is recognized as liability or long

term obligation which business unit has to fulfill after specific time period. In

accordance with dual side effect cash side of balance sheet will incline significantly.

TASK 3

3.1 Preparing and analyzing cash budget for the purpose of decision making

Cash budget may be served as a framework which exhibits monetary inflow and

outflow (Abor, 2017). Budget acts as a guide which in turn provides assistance to the

personnel in spending money more effectually.

Cash budget from the period of January to June is enumerated below:

Particula

rs

Januar

y (in £)

Februar

y (in £)

Marc

h (in

£)

April

(in £)

May

(in £)

June

(in £)

Opening

cash 110000 -539750

-

39200

-

76750 48500

16625

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

balance or

position 0

Cash sales

received

in similar

month 15000 22500 30000 15000 15000 3750

Amount

of sales

received

from

debtor (in

one

month) 120000 240000

36000

0

48000

0

24000

0

24000

0

Cash

Received

(in two

months) 22500 22500 45000 67500 90000 45000

Total

cash

receipts 267500 -254750 43000

48575

0

39350

0

45500

0

Cash outflows

Suppliers

payment 807250 137250

11975

0

43725

0

22725

0

21975

0

Closing

cash

balance

or

position

-

539750 -392000

-

76750 48500

16625

0

23525

0

The above mentioned cash budget shows that Clariton Antiques Ltd received higher

cash from debtors after one month. Further, total cash receipts of firm inclined from £267500

to £455000 at the end of June. During the period of 6 months total cash receipts of firm

fluctuated. Further, supplier’s payment also declined after the month of April. Thus, it can be

stated that business unit is required to make proper estimation of income and expenses after

making evaluation of each business activity.

3.2 Calculating unit cost for taking pricing decision

For the determination of suitable price firm is required to assess unit cost which it is

going to offer customers (Unit cost, 2017). Hence, by adding margin in unit cost entrepreneur

can determine suitable price Clariton antiques Ltd can get desired level of profit.

Calculation of unit cost

position 0

Cash sales

received

in similar

month 15000 22500 30000 15000 15000 3750

Amount

of sales

received

from

debtor (in

one

month) 120000 240000

36000

0

48000

0

24000

0

24000

0

Cash

Received

(in two

months) 22500 22500 45000 67500 90000 45000

Total

cash

receipts 267500 -254750 43000

48575

0

39350

0

45500

0

Cash outflows

Suppliers

payment 807250 137250

11975

0

43725

0

22725

0

21975

0

Closing

cash

balance

or

position

-

539750 -392000

-

76750 48500

16625

0

23525

0

The above mentioned cash budget shows that Clariton Antiques Ltd received higher

cash from debtors after one month. Further, total cash receipts of firm inclined from £267500

to £455000 at the end of June. During the period of 6 months total cash receipts of firm

fluctuated. Further, supplier’s payment also declined after the month of April. Thus, it can be

stated that business unit is required to make proper estimation of income and expenses after

making evaluation of each business activity.

3.2 Calculating unit cost for taking pricing decision

For the determination of suitable price firm is required to assess unit cost which it is

going to offer customers (Unit cost, 2017). Hence, by adding margin in unit cost entrepreneur

can determine suitable price Clariton antiques Ltd can get desired level of profit.

Calculation of unit cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

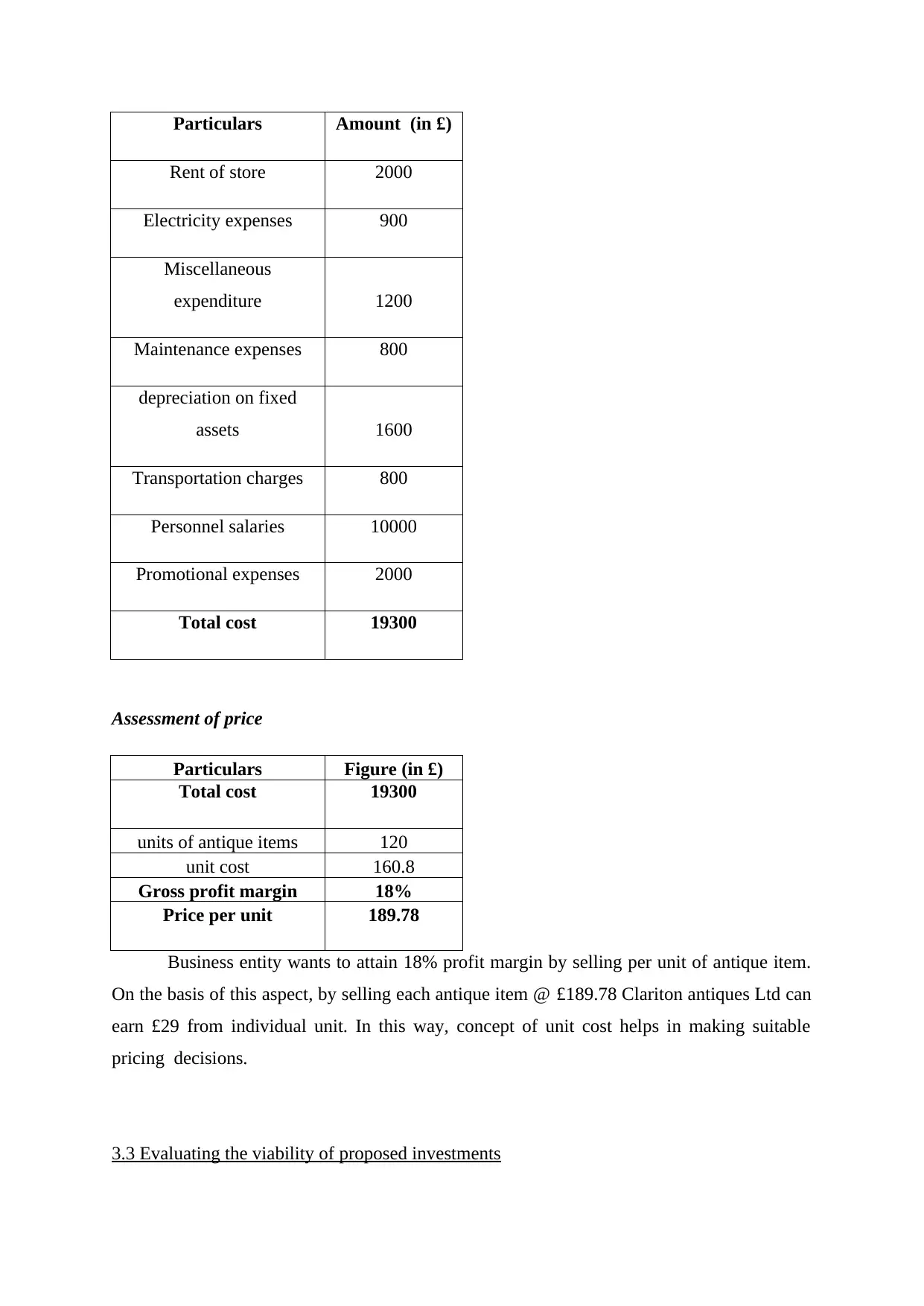

Particulars Amount (in £)

Rent of store 2000

Electricity expenses 900

Miscellaneous

expenditure 1200

Maintenance expenses 800

depreciation on fixed

assets 1600

Transportation charges 800

Personnel salaries 10000

Promotional expenses 2000

Total cost 19300

Assessment of price

Particulars Figure (in £)

Total cost 19300

units of antique items 120

unit cost 160.8

Gross profit margin 18%

Price per unit 189.78

Business entity wants to attain 18% profit margin by selling per unit of antique item.

On the basis of this aspect, by selling each antique item @ £189.78 Clariton antiques Ltd can

earn £29 from individual unit. In this way, concept of unit cost helps in making suitable

pricing decisions.

3.3 Evaluating the viability of proposed investments

Rent of store 2000

Electricity expenses 900

Miscellaneous

expenditure 1200

Maintenance expenses 800

depreciation on fixed

assets 1600

Transportation charges 800

Personnel salaries 10000

Promotional expenses 2000

Total cost 19300

Assessment of price

Particulars Figure (in £)

Total cost 19300

units of antique items 120

unit cost 160.8

Gross profit margin 18%

Price per unit 189.78

Business entity wants to attain 18% profit margin by selling per unit of antique item.

On the basis of this aspect, by selling each antique item @ £189.78 Clariton antiques Ltd can

earn £29 from individual unit. In this way, concept of unit cost helps in making suitable

pricing decisions.

3.3 Evaluating the viability of proposed investments

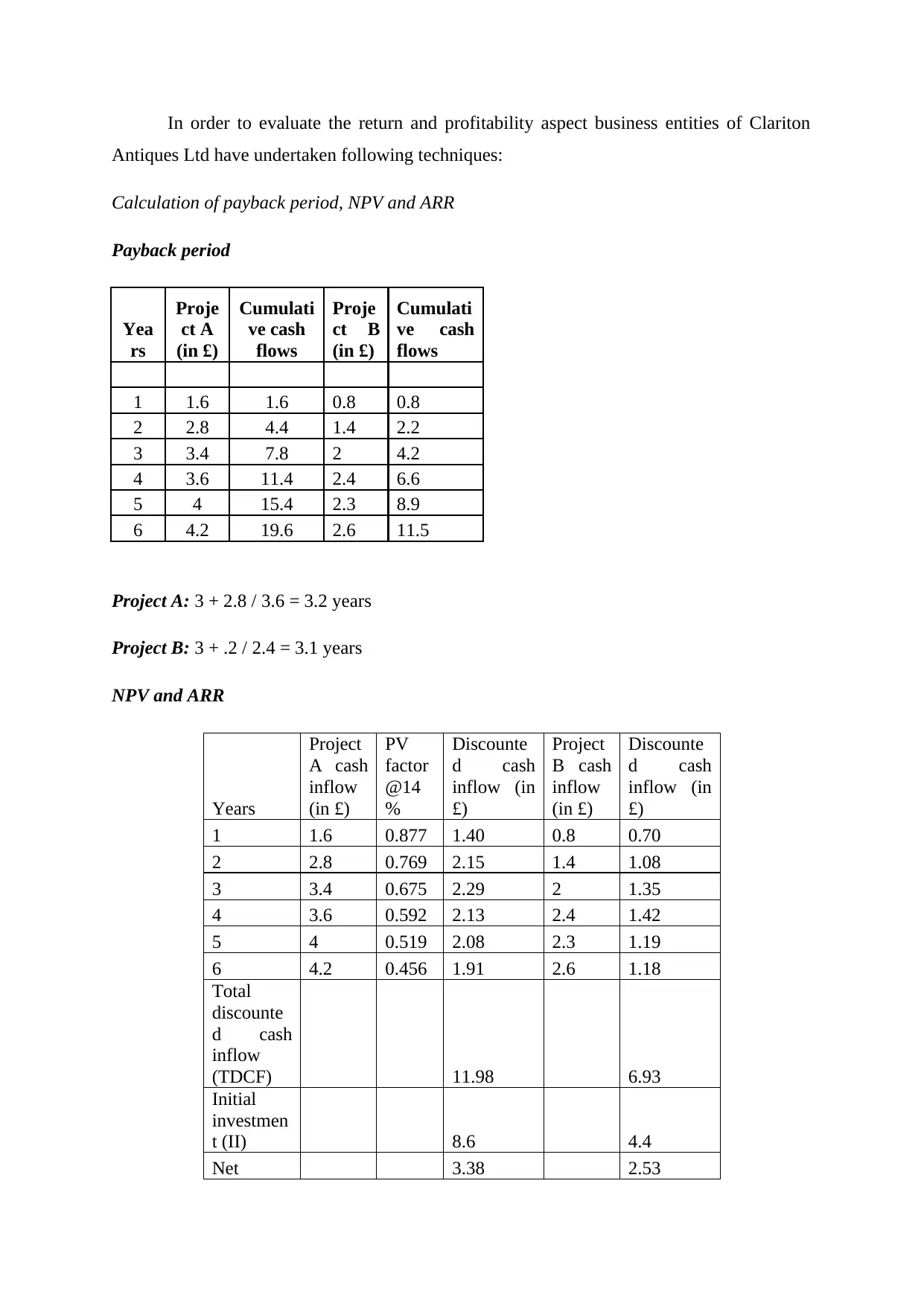

In order to evaluate the return and profitability aspect business entities of Clariton

Antiques Ltd have undertaken following techniques:

Calculation of payback period, NPV and ARR

Payback period

Yea

rs

Proje

ct A

(in £)

Cumulati

ve cash

flows

Proje

ct B

(in £)

Cumulati

ve cash

flows

1 1.6 1.6 0.8 0.8

2 2.8 4.4 1.4 2.2

3 3.4 7.8 2 4.2

4 3.6 11.4 2.4 6.6

5 4 15.4 2.3 8.9

6 4.2 19.6 2.6 11.5

Project A: 3 + 2.8 / 3.6 = 3.2 years

Project B: 3 + .2 / 2.4 = 3.1 years

NPV and ARR

Years

Project

A cash

inflow

(in £)

PV

factor

@14

%

Discounte

d cash

inflow (in

£)

Project

B cash

inflow

(in £)

Discounte

d cash

inflow (in

£)

1 1.6 0.877 1.40 0.8 0.70

2 2.8 0.769 2.15 1.4 1.08

3 3.4 0.675 2.29 2 1.35

4 3.6 0.592 2.13 2.4 1.42

5 4 0.519 2.08 2.3 1.19

6 4.2 0.456 1.91 2.6 1.18

Total

discounte

d cash

inflow

(TDCF) 11.98 6.93

Initial

investmen

t (II) 8.6 4.4

Net 3.38 2.53

Antiques Ltd have undertaken following techniques:

Calculation of payback period, NPV and ARR

Payback period

Yea

rs

Proje

ct A

(in £)

Cumulati

ve cash

flows

Proje

ct B

(in £)

Cumulati

ve cash

flows

1 1.6 1.6 0.8 0.8

2 2.8 4.4 1.4 2.2

3 3.4 7.8 2 4.2

4 3.6 11.4 2.4 6.6

5 4 15.4 2.3 8.9

6 4.2 19.6 2.6 11.5

Project A: 3 + 2.8 / 3.6 = 3.2 years

Project B: 3 + .2 / 2.4 = 3.1 years

NPV and ARR

Years

Project

A cash

inflow

(in £)

PV

factor

@14

%

Discounte

d cash

inflow (in

£)

Project

B cash

inflow

(in £)

Discounte

d cash

inflow (in

£)

1 1.6 0.877 1.40 0.8 0.70

2 2.8 0.769 2.15 1.4 1.08

3 3.4 0.675 2.29 2 1.35

4 3.6 0.592 2.13 2.4 1.42

5 4 0.519 2.08 2.3 1.19

6 4.2 0.456 1.91 2.6 1.18

Total

discounte

d cash

inflow

(TDCF) 11.98 6.93

Initial

investmen

t (II) 8.6 4.4

Net 3.38 2.53

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.