Plant and Equipment Asset Management Plan

VerifiedAdded on 2023/01/16

|26

|5635

|42

AI Summary

This document is a Plant and Equipment Asset Management Plan that outlines strategies for managing and optimizing assets for efficient service delivery. It covers topics such as funding, levels of service, demand management, and lifecycle management. The plan aims to provide a financially sustainable approach to asset management and ensure the desired levels of service are met.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Plant and Equipment

Asset Management Plan

Executive Summary: The council operates and maintains a fleet of construction plant, truck and

trailers, business vehicles and traveler vehicles along with piece of furniture and fittings These

assets are worth $3,316,000.

The projected value to produce the services lined by this quality Management set up includes

operations, maintenance, renewal and upgrade of existing assets over the ten year coming up

with amount is $4,549,000 or $455,000 p.a.

Council’s calculable obtainable funding for this era is $4,549,000 or $455,000 p.a. that is 100%

of the value to produce the service.

Council plans to produce operation, maintenance, renewal and upgrade of plant and

instrumentality service assets to fulfill service levels set by council in annual budgets among the

ten year coming up with amount.

Council doesn't have enough funding give to all services at the required service levels or provide

new services.

There are a unit risks related to providing the service and not having the ability to finish all

known activities and comes. we've got known major risks as: deficient resources as well as

funding and employees to replace quality in an exceedingly accordance with renewal forecasts

and Incomplete/inaccurate asset knowledge, significantly the condition of the road, docking

facility and customary effluent assets.

We will endeavor to manage these risks among obtainable funding by Conducting regular

condition assessments and website inspections to work out the remaining helpful lifetime of

assets and maintenance needs and Request funding for renewals and monitor trends of

maintenance.

The actions ensuing from this quality management set up are: still improvement the info in

relevancy condition assessments of plant and instrumentality assets and Use the condition

assessments of plant and instrumentality assets to raised confirm the remaining helpful life.

1

Asset Management Plan

Executive Summary: The council operates and maintains a fleet of construction plant, truck and

trailers, business vehicles and traveler vehicles along with piece of furniture and fittings These

assets are worth $3,316,000.

The projected value to produce the services lined by this quality Management set up includes

operations, maintenance, renewal and upgrade of existing assets over the ten year coming up

with amount is $4,549,000 or $455,000 p.a.

Council’s calculable obtainable funding for this era is $4,549,000 or $455,000 p.a. that is 100%

of the value to produce the service.

Council plans to produce operation, maintenance, renewal and upgrade of plant and

instrumentality service assets to fulfill service levels set by council in annual budgets among the

ten year coming up with amount.

Council doesn't have enough funding give to all services at the required service levels or provide

new services.

There are a unit risks related to providing the service and not having the ability to finish all

known activities and comes. we've got known major risks as: deficient resources as well as

funding and employees to replace quality in an exceedingly accordance with renewal forecasts

and Incomplete/inaccurate asset knowledge, significantly the condition of the road, docking

facility and customary effluent assets.

We will endeavor to manage these risks among obtainable funding by Conducting regular

condition assessments and website inspections to work out the remaining helpful lifetime of

assets and maintenance needs and Request funding for renewals and monitor trends of

maintenance.

The actions ensuing from this quality management set up are: still improvement the info in

relevancy condition assessments of plant and instrumentality assets and Use the condition

assessments of plant and instrumentality assets to raised confirm the remaining helpful life.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Background

This plus management arrange is to demonstrate responsive management of assets (and services

provided from assets), compliance with regulative needs, and to speak funding required to supply

the specified levels of service.

The plus management arrange is to be browse with the Council’s plus Management Policy, plus

Management Strategy and also the following associated coming up with documents:

• District Council of gown Strategic arrange 2014-2018

• District Council of gown long run finances 2016-2025

• Development arrange

• Annual Budget

The assets covered by this asset management plan are shown below.

Table 2.1: Assets covered by this Plan

Asset category Replacement Value

Plant Machinery & Equipment $2,811,000

Furniture & Fittings $ 487,000

TOTAL $3,316,000

Goals and Objectives of Asset Management

The Council exists to supply services to its community. a number of these services are provided

by assets. Council has noni heritable plant and instrumentation assets by contract, construction

by council workers and by donation of assets created by developers et al. to satisfy augmented

levels of service.

Council’s goal in managing assets is to satisfy the desired level of service within the most

efficient manner for gift and future shoppers. The key components of plant and instrumentation

plus management are:

• Taking a life-cycle approach,

• Developing efficient management methods for the future,

• Providing an outlined level of service and observance performance,

• Understanding and meeting the stress of growth through demand management and plant

and instrumentation investment,

• Managing risks related to plus failures,

• Sustainable use of physical resources,

• Continuous improvement in plus management practices.

The goal of this plus management arrange is to:

2

Background

This plus management arrange is to demonstrate responsive management of assets (and services

provided from assets), compliance with regulative needs, and to speak funding required to supply

the specified levels of service.

The plus management arrange is to be browse with the Council’s plus Management Policy, plus

Management Strategy and also the following associated coming up with documents:

• District Council of gown Strategic arrange 2014-2018

• District Council of gown long run finances 2016-2025

• Development arrange

• Annual Budget

The assets covered by this asset management plan are shown below.

Table 2.1: Assets covered by this Plan

Asset category Replacement Value

Plant Machinery & Equipment $2,811,000

Furniture & Fittings $ 487,000

TOTAL $3,316,000

Goals and Objectives of Asset Management

The Council exists to supply services to its community. a number of these services are provided

by assets. Council has noni heritable plant and instrumentation assets by contract, construction

by council workers and by donation of assets created by developers et al. to satisfy augmented

levels of service.

Council’s goal in managing assets is to satisfy the desired level of service within the most

efficient manner for gift and future shoppers. The key components of plant and instrumentation

plus management are:

• Taking a life-cycle approach,

• Developing efficient management methods for the future,

• Providing an outlined level of service and observance performance,

• Understanding and meeting the stress of growth through demand management and plant

and instrumentation investment,

• Managing risks related to plus failures,

• Sustainable use of physical resources,

• Continuous improvement in plus management practices.

The goal of this plus management arrange is to:

2

•Document the services/service levels to be provided and therefore the prices of providing

the service,

•Communicate the results for service levels and risk, wherever desired funding isn't on the

market, and

•Provide data to help call manufacturers in commercialism off service levels, prices and

risks to supply services in an exceedingly financially property manner.

Table 2.2: Organization Goals

Goal Objective How Goal and Objectives are addressed in

AMP

Governance and

Financial

sustainability –

Provide leadership,

good governance,

and efficient,

effective and

responsive Council

services

•

•

•

Safeguarding Council

assets by implementing

appropriate asset

management strategies

and appropriate financial

resources for those

assets. Creating an

environment where

Council Elected

Members and senior staff

take an integral part in

overall management of

Council assets by

creating and sustaining

an asset management

awareness throughout the

organization by training

and development.

Meeting legislative

requirements for asset

management.

This asset management plan documents the

strategies and funding levels for asset

replacement, renewal & upgrades over the

long-term to ensure the ongoing financial

sustainability of the Council.

3

the service,

•Communicate the results for service levels and risk, wherever desired funding isn't on the

market, and

•Provide data to help call manufacturers in commercialism off service levels, prices and

risks to supply services in an exceedingly financially property manner.

Table 2.2: Organization Goals

Goal Objective How Goal and Objectives are addressed in

AMP

Governance and

Financial

sustainability –

Provide leadership,

good governance,

and efficient,

effective and

responsive Council

services

•

•

•

Safeguarding Council

assets by implementing

appropriate asset

management strategies

and appropriate financial

resources for those

assets. Creating an

environment where

Council Elected

Members and senior staff

take an integral part in

overall management of

Council assets by

creating and sustaining

an asset management

awareness throughout the

organization by training

and development.

Meeting legislative

requirements for asset

management.

This asset management plan documents the

strategies and funding levels for asset

replacement, renewal & upgrades over the

long-term to ensure the ongoing financial

sustainability of the Council.

3

Plan Framework

Key components of the arrange square measure

•Levels of service – specifies the services and levels of service to be provided by the

council.

•Future demand – however this may impact on future service delivery and the way this is

often to be met.

•Life cycle management – however the organization can manage its existing and future

assets to supply the desired services

•Financial outline – what funds square measure needed to supply the desired services.

•Asset management practices

•Monitoring – however the arrange are going to be monitored to confirm it's meeting the

organization’s objectives.

•Asset management improvement arrange

Core and Advanced Asset Management

This plus management set up is ready as a primary cut ‘core’ plus management set up in

accordance with the International Plant and instrumentality Management Manual. it's ready to

satisfy minimum legislative and structure needs for property service delivery and future

monetary designing and reportage. Core plus management could be a ‘top-down’ approach

wherever analysis is applied at the ‘system’ or ‘network’ level.

Community Consultation

This ‘core’ plus management set up is ready to facilitate community consultation ab initio

through feedback on public show of draft plus management plans before adoption by the

Council. Future revisions of the plus management set up can incorporate community

consultation on service levels and prices of providing the service. this may assist the Council

and also the community in matching the amount of service required by the community, service

risks and consequences with the community’s ability to pay money for the service.

LEVELS OF SERVICE

4

Key components of the arrange square measure

•Levels of service – specifies the services and levels of service to be provided by the

council.

•Future demand – however this may impact on future service delivery and the way this is

often to be met.

•Life cycle management – however the organization can manage its existing and future

assets to supply the desired services

•Financial outline – what funds square measure needed to supply the desired services.

•Asset management practices

•Monitoring – however the arrange are going to be monitored to confirm it's meeting the

organization’s objectives.

•Asset management improvement arrange

Core and Advanced Asset Management

This plus management set up is ready as a primary cut ‘core’ plus management set up in

accordance with the International Plant and instrumentality Management Manual. it's ready to

satisfy minimum legislative and structure needs for property service delivery and future

monetary designing and reportage. Core plus management could be a ‘top-down’ approach

wherever analysis is applied at the ‘system’ or ‘network’ level.

Community Consultation

This ‘core’ plus management set up is ready to facilitate community consultation ab initio

through feedback on public show of draft plus management plans before adoption by the

Council. Future revisions of the plus management set up can incorporate community

consultation on service levels and prices of providing the service. this may assist the Council

and also the community in matching the amount of service required by the community, service

risks and consequences with the community’s ability to pay money for the service.

LEVELS OF SERVICE

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

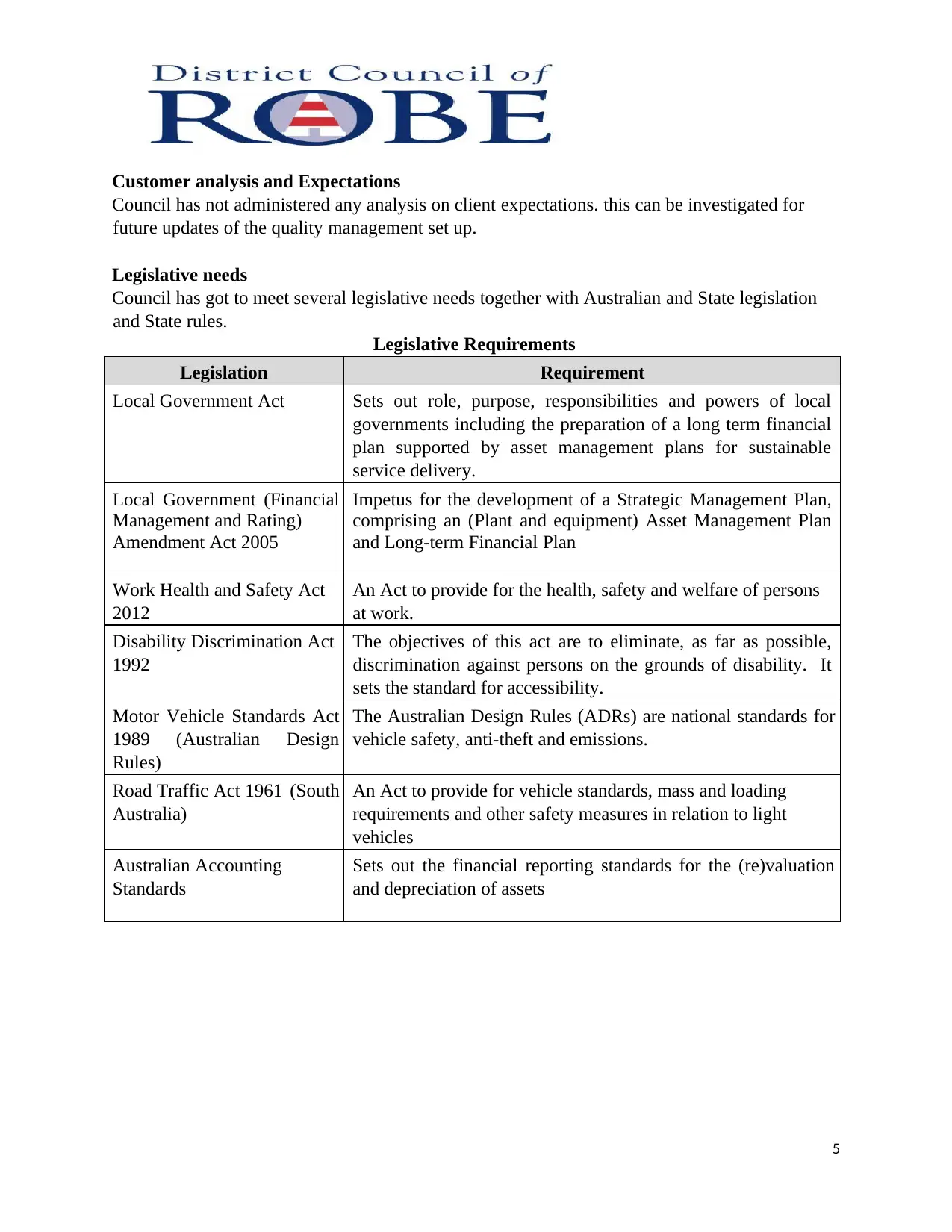

Customer analysis and Expectations

Council has not administered any analysis on client expectations. this can be investigated for

future updates of the quality management set up.

Legislative needs

Council has got to meet several legislative needs together with Australian and State legislation

and State rules.

Legislative Requirements

Legislation Requirement

Local Government Act Sets out role, purpose, responsibilities and powers of local

governments including the preparation of a long term financial

plan supported by asset management plans for sustainable

service delivery.

Local Government (Financial

Management and Rating)

Amendment Act 2005

Impetus for the development of a Strategic Management Plan,

comprising an (Plant and equipment) Asset Management Plan

and Long-term Financial Plan

Work Health and Safety Act

2012

An Act to provide for the health, safety and welfare of persons

at work.

Disability Discrimination Act

1992

The objectives of this act are to eliminate, as far as possible,

discrimination against persons on the grounds of disability. It

sets the standard for accessibility.

Motor Vehicle Standards Act

1989 (Australian Design

Rules)

The Australian Design Rules (ADRs) are national standards for

vehicle safety, anti-theft and emissions.

Road Traffic Act 1961 (South

Australia)

An Act to provide for vehicle standards, mass and loading

requirements and other safety measures in relation to light

vehicles

Australian Accounting

Standards

Sets out the financial reporting standards for the (re)valuation

and depreciation of assets

5

Council has not administered any analysis on client expectations. this can be investigated for

future updates of the quality management set up.

Legislative needs

Council has got to meet several legislative needs together with Australian and State legislation

and State rules.

Legislative Requirements

Legislation Requirement

Local Government Act Sets out role, purpose, responsibilities and powers of local

governments including the preparation of a long term financial

plan supported by asset management plans for sustainable

service delivery.

Local Government (Financial

Management and Rating)

Amendment Act 2005

Impetus for the development of a Strategic Management Plan,

comprising an (Plant and equipment) Asset Management Plan

and Long-term Financial Plan

Work Health and Safety Act

2012

An Act to provide for the health, safety and welfare of persons

at work.

Disability Discrimination Act

1992

The objectives of this act are to eliminate, as far as possible,

discrimination against persons on the grounds of disability. It

sets the standard for accessibility.

Motor Vehicle Standards Act

1989 (Australian Design

Rules)

The Australian Design Rules (ADRs) are national standards for

vehicle safety, anti-theft and emissions.

Road Traffic Act 1961 (South

Australia)

An Act to provide for vehicle standards, mass and loading

requirements and other safety measures in relation to light

vehicles

Australian Accounting

Standards

Sets out the financial reporting standards for the (re)valuation

and depreciation of assets

5

Current Levels of Service

Current Service Levels

Key

Performanc

e Measure

Level of

Service

Objective

Performance Measure Process Desired

Level of

Service

Current

Level of

Service

COMMUNITY LEVELS

OF SERVICE

Quality Provide

Plant and

Equipment

which is

operational

• Maintenance Failures

• Labor Rates

• Scheduled/

unscheduled maintenance

ratio

Plant and

Equipment

assets are

managed

using

adopted

policies

and best

practice

standards

Plant and

Equipment

assets are

managed

using

adopted

policies and

best practice

standards

Function Provide

sufficient

Plant and

Equipment

assets to

meet the

communitie

s

desired

levels of

services

• Specification for equipment

meets operator needs

Sufficient

assets are

available

to meet

levels of

service

Sufficient

assets are

available to

meet levels of

service

Safety Ensure

assets are

operated,

maintained,

serviced and

• Accidents/injuries/near miss

statistics

Nil

preventabl

e

injuries per

annum

Nil

preventable

injuries per

annum

6

Current Service Levels

Key

Performanc

e Measure

Level of

Service

Objective

Performance Measure Process Desired

Level of

Service

Current

Level of

Service

COMMUNITY LEVELS

OF SERVICE

Quality Provide

Plant and

Equipment

which is

operational

• Maintenance Failures

• Labor Rates

• Scheduled/

unscheduled maintenance

ratio

Plant and

Equipment

assets are

managed

using

adopted

policies

and best

practice

standards

Plant and

Equipment

assets are

managed

using

adopted

policies and

best practice

standards

Function Provide

sufficient

Plant and

Equipment

assets to

meet the

communitie

s

desired

levels of

services

• Specification for equipment

meets operator needs

Sufficient

assets are

available

to meet

levels of

service

Sufficient

assets are

available to

meet levels of

service

Safety Ensure

assets are

operated,

maintained,

serviced and

• Accidents/injuries/near miss

statistics

Nil

preventabl

e

injuries per

annum

Nil

preventable

injuries per

annum

6

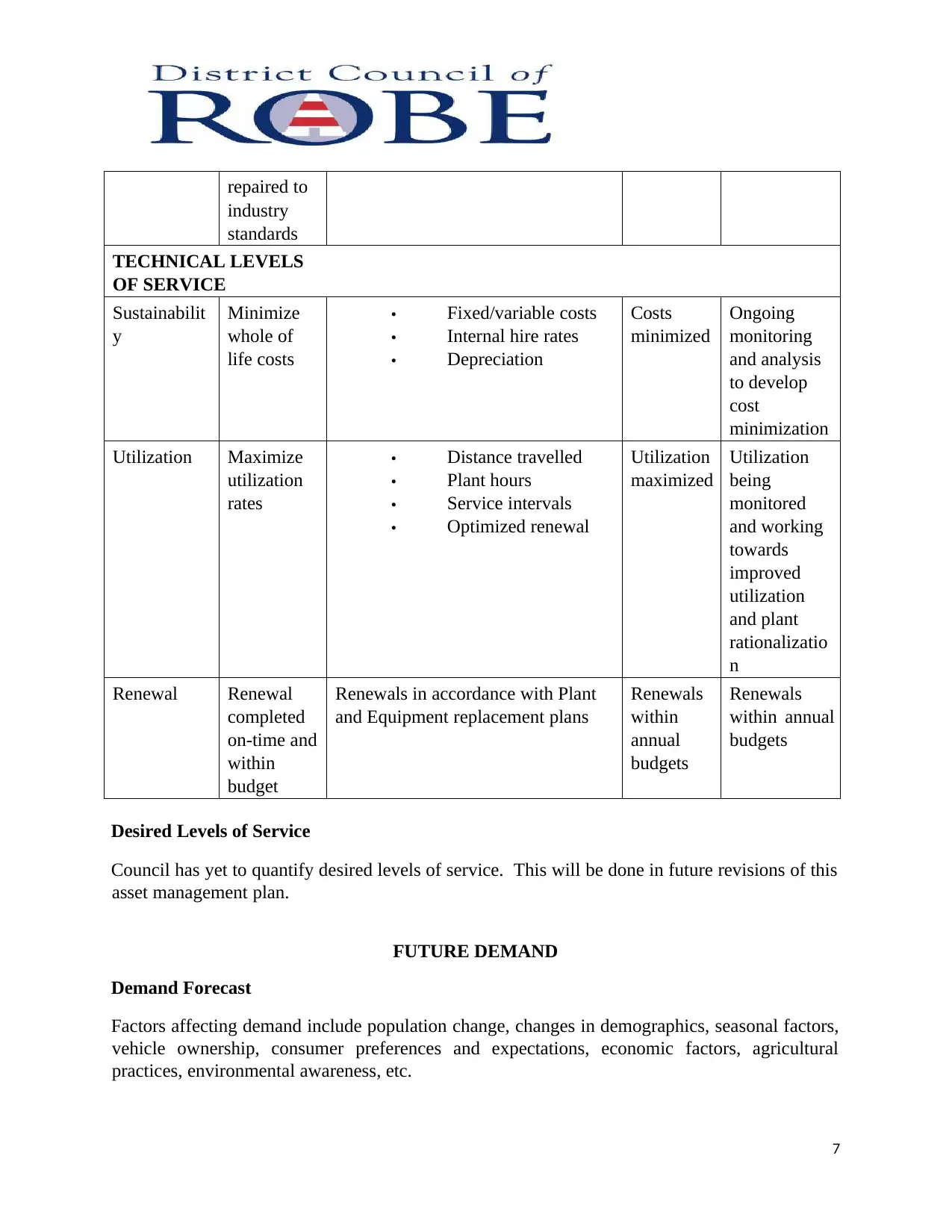

repaired to

industry

standards

TECHNICAL LEVELS

OF SERVICE

Sustainabilit

y

Minimize

whole of

life costs

• Fixed/variable costs

• Internal hire rates

• Depreciation

Costs

minimized

Ongoing

monitoring

and analysis

to develop

cost

minimization

Utilization Maximize

utilization

rates

• Distance travelled

• Plant hours

• Service intervals

• Optimized renewal

Utilization

maximized

Utilization

being

monitored

and working

towards

improved

utilization

and plant

rationalizatio

n

Renewal Renewal

completed

on-time and

within

budget

Renewals in accordance with Plant

and Equipment replacement plans

Renewals

within

annual

budgets

Renewals

within annual

budgets

Desired Levels of Service

Council has yet to quantify desired levels of service. This will be done in future revisions of this

asset management plan.

FUTURE DEMAND

Demand Forecast

Factors affecting demand include population change, changes in demographics, seasonal factors,

vehicle ownership, consumer preferences and expectations, economic factors, agricultural

practices, environmental awareness, etc.

7

industry

standards

TECHNICAL LEVELS

OF SERVICE

Sustainabilit

y

Minimize

whole of

life costs

• Fixed/variable costs

• Internal hire rates

• Depreciation

Costs

minimized

Ongoing

monitoring

and analysis

to develop

cost

minimization

Utilization Maximize

utilization

rates

• Distance travelled

• Plant hours

• Service intervals

• Optimized renewal

Utilization

maximized

Utilization

being

monitored

and working

towards

improved

utilization

and plant

rationalizatio

n

Renewal Renewal

completed

on-time and

within

budget

Renewals in accordance with Plant

and Equipment replacement plans

Renewals

within

annual

budgets

Renewals

within annual

budgets

Desired Levels of Service

Council has yet to quantify desired levels of service. This will be done in future revisions of this

asset management plan.

FUTURE DEMAND

Demand Forecast

Factors affecting demand include population change, changes in demographics, seasonal factors,

vehicle ownership, consumer preferences and expectations, economic factors, agricultural

practices, environmental awareness, etc.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

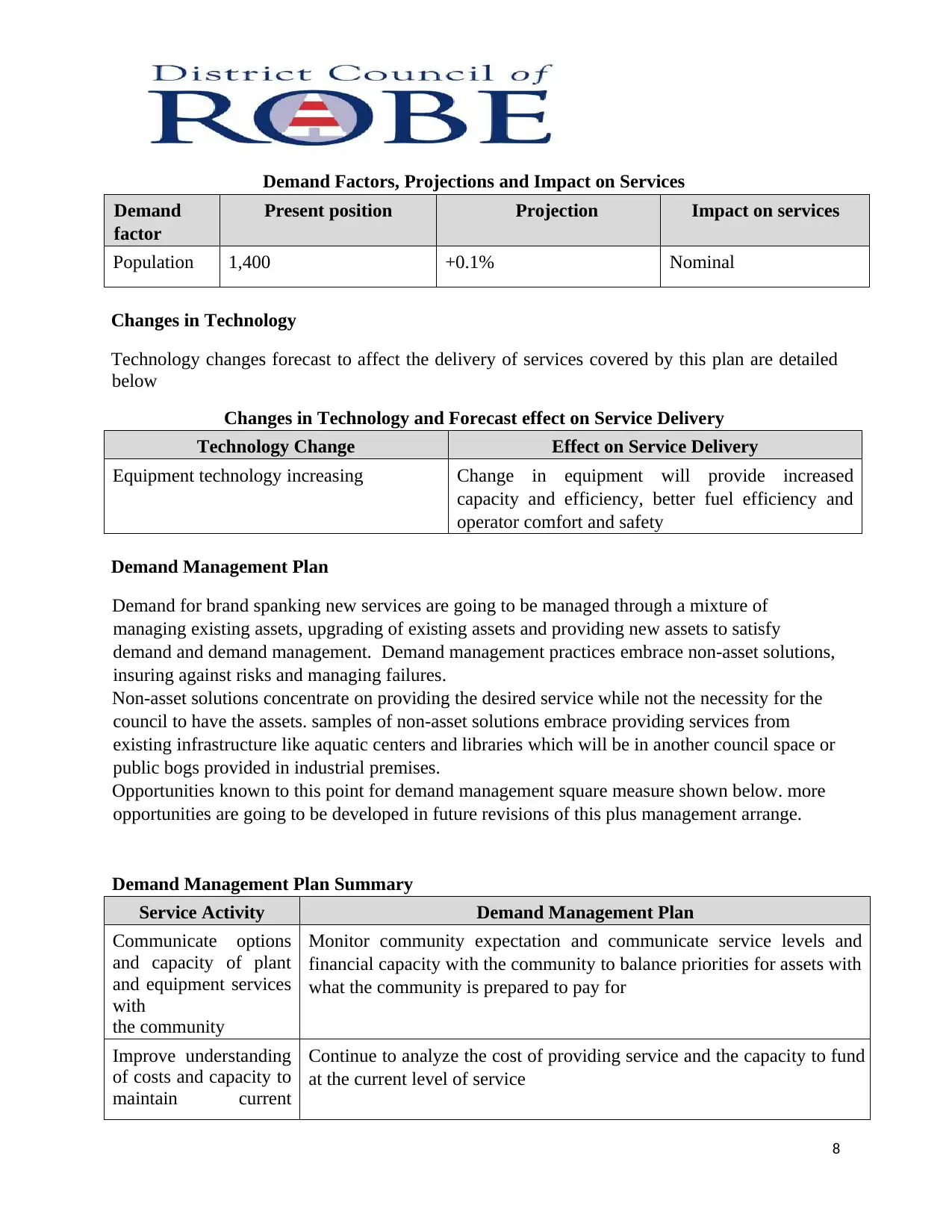

Demand Factors, Projections and Impact on Services

Demand

factor

Present position Projection Impact on services

Population 1,400 +0.1% Nominal

Changes in Technology

Technology changes forecast to affect the delivery of services covered by this plan are detailed

below

Changes in Technology and Forecast effect on Service Delivery

Technology Change Effect on Service Delivery

Equipment technology increasing Change in equipment will provide increased

capacity and efficiency, better fuel efficiency and

operator comfort and safety

Demand Management Plan

Demand for brand spanking new services are going to be managed through a mixture of

managing existing assets, upgrading of existing assets and providing new assets to satisfy

demand and demand management. Demand management practices embrace non-asset solutions,

insuring against risks and managing failures.

Non-asset solutions concentrate on providing the desired service while not the necessity for the

council to have the assets. samples of non-asset solutions embrace providing services from

existing infrastructure like aquatic centers and libraries which will be in another council space or

public bogs provided in industrial premises.

Opportunities known to this point for demand management square measure shown below. more

opportunities are going to be developed in future revisions of this plus management arrange.

Demand Management Plan Summary

Service Activity Demand Management Plan

Communicate options

and capacity of plant

and equipment services

with

the community

Monitor community expectation and communicate service levels and

financial capacity with the community to balance priorities for assets with

what the community is prepared to pay for

Improve understanding

of costs and capacity to

maintain current

Continue to analyze the cost of providing service and the capacity to fund

at the current level of service

8

Demand

factor

Present position Projection Impact on services

Population 1,400 +0.1% Nominal

Changes in Technology

Technology changes forecast to affect the delivery of services covered by this plan are detailed

below

Changes in Technology and Forecast effect on Service Delivery

Technology Change Effect on Service Delivery

Equipment technology increasing Change in equipment will provide increased

capacity and efficiency, better fuel efficiency and

operator comfort and safety

Demand Management Plan

Demand for brand spanking new services are going to be managed through a mixture of

managing existing assets, upgrading of existing assets and providing new assets to satisfy

demand and demand management. Demand management practices embrace non-asset solutions,

insuring against risks and managing failures.

Non-asset solutions concentrate on providing the desired service while not the necessity for the

council to have the assets. samples of non-asset solutions embrace providing services from

existing infrastructure like aquatic centers and libraries which will be in another council space or

public bogs provided in industrial premises.

Opportunities known to this point for demand management square measure shown below. more

opportunities are going to be developed in future revisions of this plus management arrange.

Demand Management Plan Summary

Service Activity Demand Management Plan

Communicate options

and capacity of plant

and equipment services

with

the community

Monitor community expectation and communicate service levels and

financial capacity with the community to balance priorities for assets with

what the community is prepared to pay for

Improve understanding

of costs and capacity to

maintain current

Continue to analyze the cost of providing service and the capacity to fund

at the current level of service

8

service

levels

New Assets for Growth

No additional plant and equipment is proposed during the period of the long term financial plan

or asset management plan.

LIFECYCLE MANAGEMENT PLAN

The lifecycle management plan details how Council plans to manage and operate the assets at the

agreed levels of service while optimizing life cycle costs.

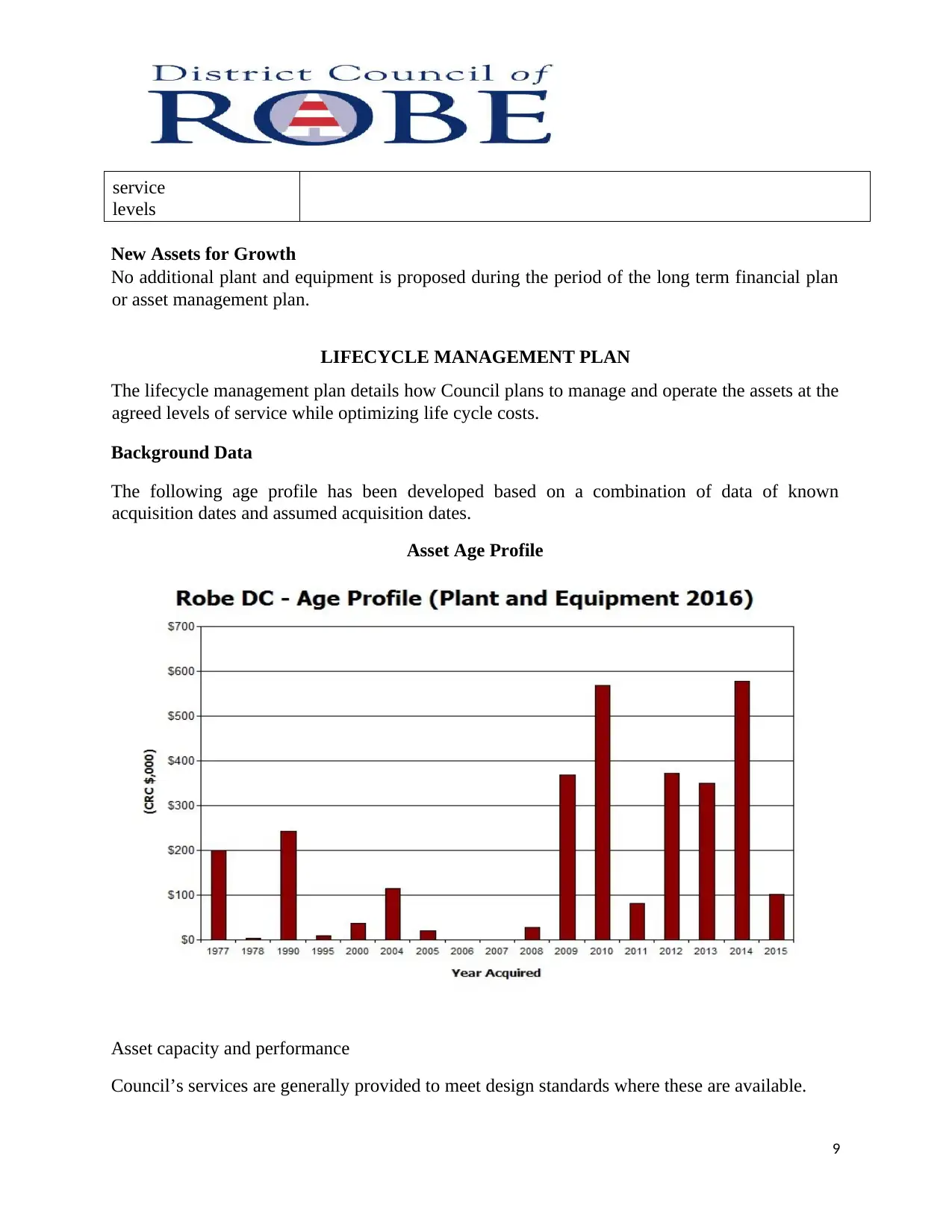

Background Data

The following age profile has been developed based on a combination of data of known

acquisition dates and assumed acquisition dates.

Asset Age Profile

Asset capacity and performance

Council’s services are generally provided to meet design standards where these are available.

9

levels

New Assets for Growth

No additional plant and equipment is proposed during the period of the long term financial plan

or asset management plan.

LIFECYCLE MANAGEMENT PLAN

The lifecycle management plan details how Council plans to manage and operate the assets at the

agreed levels of service while optimizing life cycle costs.

Background Data

The following age profile has been developed based on a combination of data of known

acquisition dates and assumed acquisition dates.

Asset Age Profile

Asset capacity and performance

Council’s services are generally provided to meet design standards where these are available.

9

Known Service Performance Deficiencies

Location Service Deficiency

Fleet Maintenance facilities Review workshop facilities and capacity to meet current and

future fleet maintenance requirements

Utilization Underutilized plant that are a result of staffing, seasonal weather

and communication across departments

Asset condition

Asset condition information is not currently available

Asset valuations

The value of assets recorded in the asset register as at 30/06/2017 covered by this asset

management plan is shown below. Assets were last revalued at 30/06/2014.

Current Replacement Cost $3,316,000

Depreciable Amount $3,107,000

Depreciated Replacement Cost $1,182,000

Annual Depreciation Expense $ 287,000

Council’s sustainability reporting reports the rate of annual asset consumption and compares this

to asset renewal and asset upgrade and expansion.

Asset Consumption 9.2%

(Depreciation/Depreciable Amount)

Asset renewal 8.9%

(Capital renewal exp/Depreciable amount)

Annual Upgrade/New 0%

(Capital upgrade exp/Depreciable amount)

Annual Upgrade/New 0%

(including contributed assets)

Council is currently renewing assets at 96.9% of the rate they are being consumed and increasing

its asset stock by 0% each year.

To provide services in an exceedingly financially property manner, Council can ought to make

sure that it's revitalizing assets at the speed they're being consumed over the medium-long term

and funding the life cycle prices for all new assets and services in its long run budget.

10

Location Service Deficiency

Fleet Maintenance facilities Review workshop facilities and capacity to meet current and

future fleet maintenance requirements

Utilization Underutilized plant that are a result of staffing, seasonal weather

and communication across departments

Asset condition

Asset condition information is not currently available

Asset valuations

The value of assets recorded in the asset register as at 30/06/2017 covered by this asset

management plan is shown below. Assets were last revalued at 30/06/2014.

Current Replacement Cost $3,316,000

Depreciable Amount $3,107,000

Depreciated Replacement Cost $1,182,000

Annual Depreciation Expense $ 287,000

Council’s sustainability reporting reports the rate of annual asset consumption and compares this

to asset renewal and asset upgrade and expansion.

Asset Consumption 9.2%

(Depreciation/Depreciable Amount)

Asset renewal 8.9%

(Capital renewal exp/Depreciable amount)

Annual Upgrade/New 0%

(Capital upgrade exp/Depreciable amount)

Annual Upgrade/New 0%

(including contributed assets)

Council is currently renewing assets at 96.9% of the rate they are being consumed and increasing

its asset stock by 0% each year.

To provide services in an exceedingly financially property manner, Council can ought to make

sure that it's revitalizing assets at the speed they're being consumed over the medium-long term

and funding the life cycle prices for all new assets and services in its long run budget.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Quality hierarchy

A quality hierarchy provides a framework for structuring information in associate data system to

help in assortment of knowledge, coverage data and creating selections. The hierarchy includes

the quality category and part used for quality coming up with and money coverage and repair

level hierarchy used for service coming up with and delivery.

Council has not however developed associate quality hierarchy this may be developed for future

plans.

Risk Management arrange

An assessment of risks related to service delivery from plant and instrumentality assets has

known crucial risks which will lead to loss or reduction in commission from plant and

instrumentality assets or a ‘financial shock’ to the organization. the danger assessment method

identifies credible risks, the probability of the danger event occurring, the results ought to the

event occur, develops a risk rating, evaluates the danger and develops a risk treatment arrange

for non-acceptable risks.

Critical risks, being those assessed as ‘Very High’ - requiring immediate corrective action and

‘High’ – requiring prioritized corrective action known within the arranged and instrumentality

Risk Management Plan are summarized below.

Critical Risks and Treatment Plans

Service or

Asset at Risk

What can Happen Risk

Rating

(VH,

H)

Risk Treatment Plan

11

A quality hierarchy provides a framework for structuring information in associate data system to

help in assortment of knowledge, coverage data and creating selections. The hierarchy includes

the quality category and part used for quality coming up with and money coverage and repair

level hierarchy used for service coming up with and delivery.

Council has not however developed associate quality hierarchy this may be developed for future

plans.

Risk Management arrange

An assessment of risks related to service delivery from plant and instrumentality assets has

known crucial risks which will lead to loss or reduction in commission from plant and

instrumentality assets or a ‘financial shock’ to the organization. the danger assessment method

identifies credible risks, the probability of the danger event occurring, the results ought to the

event occur, develops a risk rating, evaluates the danger and develops a risk treatment arrange

for non-acceptable risks.

Critical risks, being those assessed as ‘Very High’ - requiring immediate corrective action and

‘High’ – requiring prioritized corrective action known within the arranged and instrumentality

Risk Management Plan are summarized below.

Critical Risks and Treatment Plans

Service or

Asset at Risk

What can Happen Risk

Rating

(VH,

H)

Risk Treatment Plan

11

Aging fleet

technical

obsolescence

or • High

incidence of

breakdowns

• Increase

d maintenance

costs

• Increase

d downtime

• Increase

product costs

and poor

efficiency

• Work

programs run

behind schedule

•

High • Service in

accordance with

manufactures

requirements

• Investigate

and replace

equipment at

optimal time to give

the lowest lifecycle

cost

• Regular

condition

assessment of key

equipment to assist

in predicting

maintenance and

renewal needs

• Maintenance

is managed

appropriately at

an

operational level

Plant and

Equipment

reduced safety

Underfunding of

renewals in the future

High Investigate and replace

equipment at optimal time

to give the lowest lifecycle

cost and improved safety

Routine Maintenance plan

Routine maintenance is that the regular on-going work that's necessary to stay assets in

operation, together with instances wherever parts of the quality fail and want immediate repair to

create the quality operational once more.

Maintenance plan

Maintenance includes reactive, planned and specific maintenance work activities.

Reactive maintenance is unplanned repair work allotted in response to service requests and

management/supervisory directions.

Planned maintenance is repair work that's known and managed through a maintenance

management system (MMS). MMS activities embrace examination, assessing the condition

against failure/breakdown expertise, prioritizing, scheduling, auctioning the work and news what

12

technical

obsolescence

or • High

incidence of

breakdowns

• Increase

d maintenance

costs

• Increase

d downtime

• Increase

product costs

and poor

efficiency

• Work

programs run

behind schedule

•

High • Service in

accordance with

manufactures

requirements

• Investigate

and replace

equipment at

optimal time to give

the lowest lifecycle

cost

• Regular

condition

assessment of key

equipment to assist

in predicting

maintenance and

renewal needs

• Maintenance

is managed

appropriately at

an

operational level

Plant and

Equipment

reduced safety

Underfunding of

renewals in the future

High Investigate and replace

equipment at optimal time

to give the lowest lifecycle

cost and improved safety

Routine Maintenance plan

Routine maintenance is that the regular on-going work that's necessary to stay assets in

operation, together with instances wherever parts of the quality fail and want immediate repair to

create the quality operational once more.

Maintenance plan

Maintenance includes reactive, planned and specific maintenance work activities.

Reactive maintenance is unplanned repair work allotted in response to service requests and

management/supervisory directions.

Planned maintenance is repair work that's known and managed through a maintenance

management system (MMS). MMS activities embrace examination, assessing the condition

against failure/breakdown expertise, prioritizing, scheduling, auctioning the work and news what

12

was done to develop a maintenance history and improve maintenance and repair delivery

performance.

Specific maintenance is that the replacement of upper worth components/sub-components of

assets that's undertaken on a

regular cycle together with repainting, building roof replacement, etc. This work usually falls

below the capital/maintenance threshold however might need a particular budget allocation.

Actual past maintenance expenditure is shown in below. Maintenance Expenditure Trends

Year Maintenance Expenditure

Previous Year 2015 $141,000

Previous Year 2016 $153,000

Last Year 2017 $145,000

Current maintenance expenditure levels are thought of to be adequate meet needed service levels.

A future revision of this plus management arrange can embrace linking needed maintenance

expenditures with needed service levels.

Assessment and prioritization of reactive maintenance are undertaken by operational employee’s

mistreatment expertise and judgment.

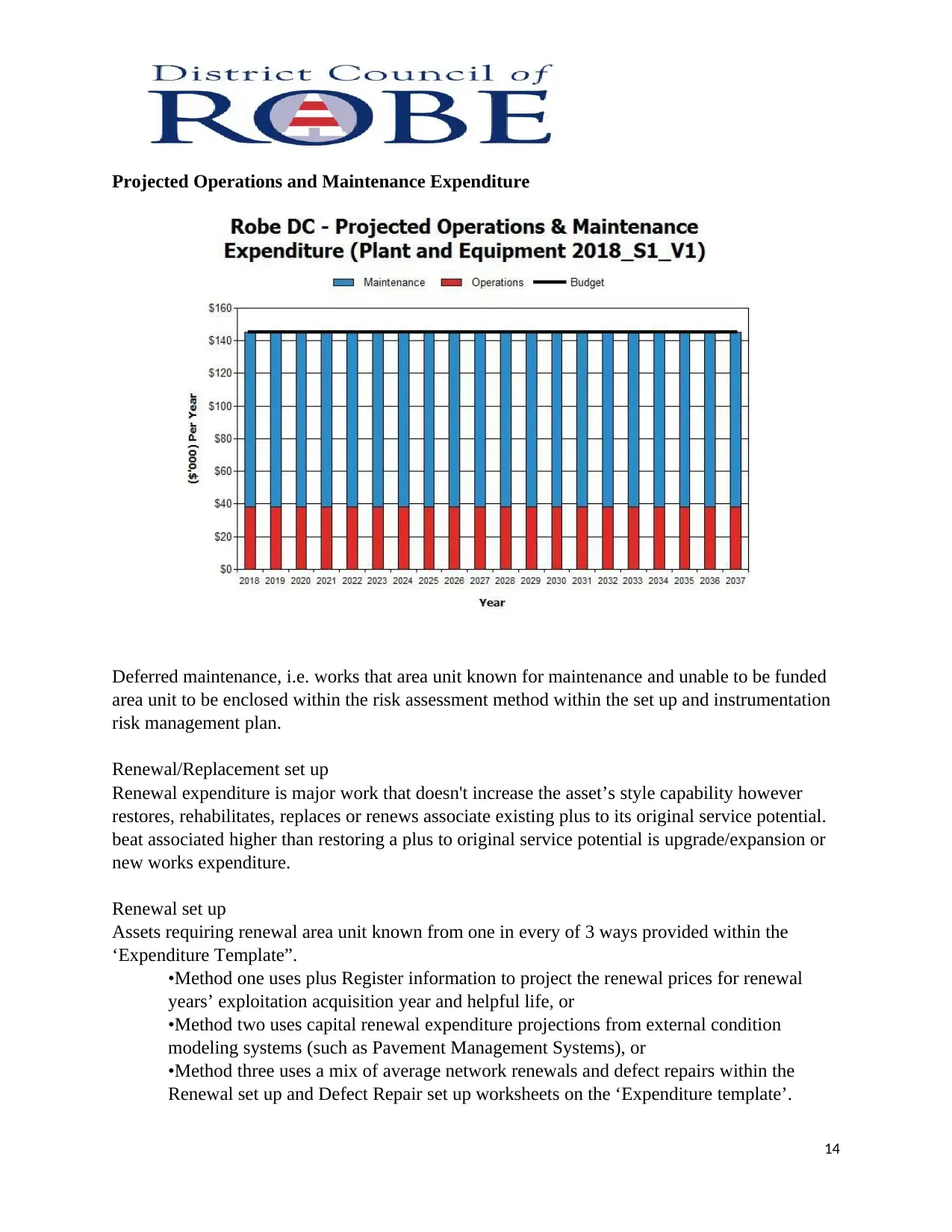

Outline of future operations and maintenance expenditures

Future operations and maintenance expenditure are forecast to trend in line with the worth of the

plus stock as shown below. Note that everyone prices are shown in 2017 dollar values.

13

performance.

Specific maintenance is that the replacement of upper worth components/sub-components of

assets that's undertaken on a

regular cycle together with repainting, building roof replacement, etc. This work usually falls

below the capital/maintenance threshold however might need a particular budget allocation.

Actual past maintenance expenditure is shown in below. Maintenance Expenditure Trends

Year Maintenance Expenditure

Previous Year 2015 $141,000

Previous Year 2016 $153,000

Last Year 2017 $145,000

Current maintenance expenditure levels are thought of to be adequate meet needed service levels.

A future revision of this plus management arrange can embrace linking needed maintenance

expenditures with needed service levels.

Assessment and prioritization of reactive maintenance are undertaken by operational employee’s

mistreatment expertise and judgment.

Outline of future operations and maintenance expenditures

Future operations and maintenance expenditure are forecast to trend in line with the worth of the

plus stock as shown below. Note that everyone prices are shown in 2017 dollar values.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Projected Operations and Maintenance Expenditure

Deferred maintenance, i.e. works that area unit known for maintenance and unable to be funded

area unit to be enclosed within the risk assessment method within the set up and instrumentation

risk management plan.

Renewal/Replacement set up

Renewal expenditure is major work that doesn't increase the asset’s style capability however

restores, rehabilitates, replaces or renews associate existing plus to its original service potential.

beat associated higher than restoring a plus to original service potential is upgrade/expansion or

new works expenditure.

Renewal set up

Assets requiring renewal area unit known from one in every of 3 ways provided within the

‘Expenditure Template”.

•Method one uses plus Register information to project the renewal prices for renewal

years’ exploitation acquisition year and helpful life, or

•Method two uses capital renewal expenditure projections from external condition

modeling systems (such as Pavement Management Systems), or

•Method three uses a mix of average network renewals and defect repairs within the

Renewal set up and Defect Repair set up worksheets on the ‘Expenditure template’.

14

Deferred maintenance, i.e. works that area unit known for maintenance and unable to be funded

area unit to be enclosed within the risk assessment method within the set up and instrumentation

risk management plan.

Renewal/Replacement set up

Renewal expenditure is major work that doesn't increase the asset’s style capability however

restores, rehabilitates, replaces or renews associate existing plus to its original service potential.

beat associated higher than restoring a plus to original service potential is upgrade/expansion or

new works expenditure.

Renewal set up

Assets requiring renewal area unit known from one in every of 3 ways provided within the

‘Expenditure Template”.

•Method one uses plus Register information to project the renewal prices for renewal

years’ exploitation acquisition year and helpful life, or

•Method two uses capital renewal expenditure projections from external condition

modeling systems (such as Pavement Management Systems), or

•Method three uses a mix of average network renewals and defect repairs within the

Renewal set up and Defect Repair set up worksheets on the ‘Expenditure template’.

14

Renewal work is allotted in accordance with the subsequent Standards and Specifications.

•Relevant Australian Standards

•Compliance with current laws, laws, and statues

•Industry Best apply

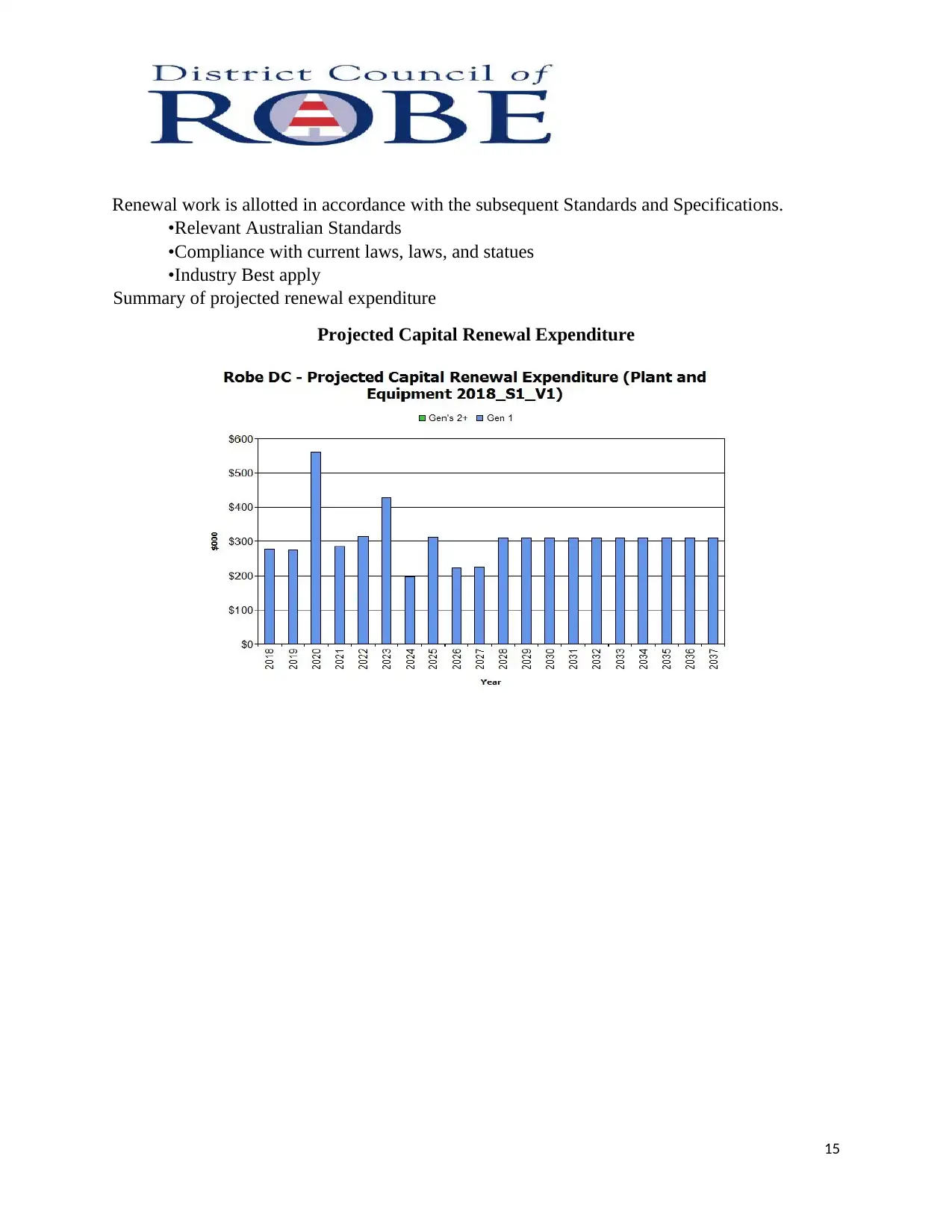

Summary of projected renewal expenditure

Projected Capital Renewal Expenditure

15

•Relevant Australian Standards

•Compliance with current laws, laws, and statues

•Industry Best apply

Summary of projected renewal expenditure

Projected Capital Renewal Expenditure

15

Deferred renewal, i.e. those assets known for renewal and not regular for renewal in capital

works programs square measure to be enclosed within the risk assessment method within the

risk management arrange.

.

Creation/Acquisition/Upgrade arrange

New works square measure those works that make a brand new quality that failed to

antecedently exist, or works that upgrade or improve associate existing quality on the far side its

existing capability. they will result from growth, social or environmental wants. Assets might

also be non-heritable at no price to the Council from development.

Selection criteria

New assets and upgrade/expansion of existing assets square measure known from varied sources

like counselor or community requests, proposals known by strategic plans or partnerships with

alternative organizations. Candidate proposals square measure inspected to verify want and to

develop a preliminary estimate. Verified proposals square measure hierarchic by priority and

offered funds and regular in future works programs. The District Council of gown doesn't have

a ranking system or criteria for creation/acquisition/upgrading of plant and instrumentation

assets and it's envisaged this can be developed in future plans.

Disposal arrange

Disposal includes any activity related to the disposal of a decommissioned quality together with

the sale, demolition or relocation. Assets known for attainable decommissioning and disposal

square measure shown below beside calculable annual savings from not having to fund

operations and maintenance of the assets. These assets are going to be more reinvestigated to

work out the desired levels of service and see what choices square measure offered for alternate

service delivery if any.

Where income projections from quality disposals aren't offered, these are going to be developed

in future revisions of this quality management arrange.

Assets identified for Disposal

Asset Reason for Disposal Timing Net Disposal

Expenditure

(Expend

+ve, Revenue –

ve)

Operations &

Maintenance

Annual Savings

N/A N/A N/A N/A N/A

16

works programs square measure to be enclosed within the risk assessment method within the

risk management arrange.

.

Creation/Acquisition/Upgrade arrange

New works square measure those works that make a brand new quality that failed to

antecedently exist, or works that upgrade or improve associate existing quality on the far side its

existing capability. they will result from growth, social or environmental wants. Assets might

also be non-heritable at no price to the Council from development.

Selection criteria

New assets and upgrade/expansion of existing assets square measure known from varied sources

like counselor or community requests, proposals known by strategic plans or partnerships with

alternative organizations. Candidate proposals square measure inspected to verify want and to

develop a preliminary estimate. Verified proposals square measure hierarchic by priority and

offered funds and regular in future works programs. The District Council of gown doesn't have

a ranking system or criteria for creation/acquisition/upgrading of plant and instrumentation

assets and it's envisaged this can be developed in future plans.

Disposal arrange

Disposal includes any activity related to the disposal of a decommissioned quality together with

the sale, demolition or relocation. Assets known for attainable decommissioning and disposal

square measure shown below beside calculable annual savings from not having to fund

operations and maintenance of the assets. These assets are going to be more reinvestigated to

work out the desired levels of service and see what choices square measure offered for alternate

service delivery if any.

Where income projections from quality disposals aren't offered, these are going to be developed

in future revisions of this quality management arrange.

Assets identified for Disposal

Asset Reason for Disposal Timing Net Disposal

Expenditure

(Expend

+ve, Revenue –

ve)

Operations &

Maintenance

Annual Savings

N/A N/A N/A N/A N/A

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

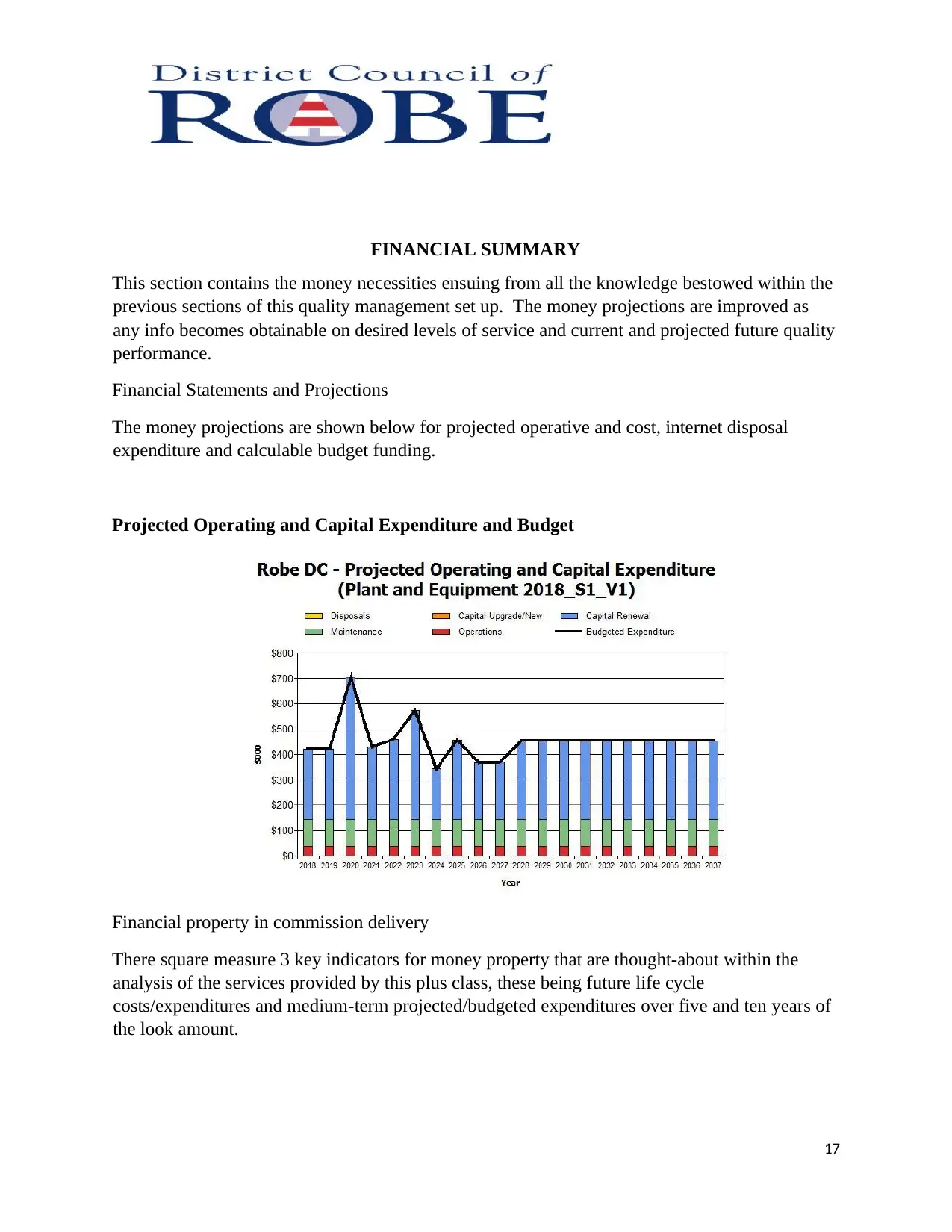

FINANCIAL SUMMARY

This section contains the money necessities ensuing from all the knowledge bestowed within the

previous sections of this quality management set up. The money projections are improved as

any info becomes obtainable on desired levels of service and current and projected future quality

performance.

Financial Statements and Projections

The money projections are shown below for projected operative and cost, internet disposal

expenditure and calculable budget funding.

Projected Operating and Capital Expenditure and Budget

Financial property in commission delivery

There square measure 3 key indicators for money property that are thought-about within the

analysis of the services provided by this plus class, these being future life cycle

costs/expenditures and medium-term projected/budgeted expenditures over five and ten years of

the look amount.

17

This section contains the money necessities ensuing from all the knowledge bestowed within the

previous sections of this quality management set up. The money projections are improved as

any info becomes obtainable on desired levels of service and current and projected future quality

performance.

Financial Statements and Projections

The money projections are shown below for projected operative and cost, internet disposal

expenditure and calculable budget funding.

Projected Operating and Capital Expenditure and Budget

Financial property in commission delivery

There square measure 3 key indicators for money property that are thought-about within the

analysis of the services provided by this plus class, these being future life cycle

costs/expenditures and medium-term projected/budgeted expenditures over five and ten years of

the look amount.

17

Long term - Life Cycle Cost

Life cycle costs (or whole of life costs) are the average costs that are required to sustain the

service levels over the longest asset life. Life cycle costs include operations and maintenance

expenditure and asset consumption (depreciation expense). The life cycle cost for the services

covered in this asset management plan is $432,000 per year (operations and maintenance

expenditure plus depreciation expense in year 1).

Life cycle costs can be compared to life cycle expenditure to give an indicator of sustainability

in service provision. Life cycle expenditure includes operations, maintenance and capital

renewal expenditure in year 1. Life cycle expenditure will vary depending on the timing of asset

renewals. The life cycle expenditure at the start of the plan is $455,000(operations and

maintenance expenditure plus budgeted capital renewal expenditure in year 1).

A shortfall between life cycle cost and life cycle expenditure is the life cycle gap.

The life cycle gap for services covered by this asset management plan is $23,000 per year (-ve =

gap, +ve = surplus).

Life cycle expenditure is 105% of life cycle costs giving a life cycle sustainability index of 1.05

The life cycle costs and life cycle expenditure comparison highlights any difference between

present outlays and the average cost of providing the service over the long term. If the life cycle

expenditure is less than that life cycle cost, it is most likely that outlays will need to be increased

or cuts in services made in the future.

Knowing the extent and timing of any required increase in outlays and the service consequences

if funding is not available will assist organizations in providing services to their communities in

a financially sustainable manner. This is the purpose of the asset management plans and long

term financial plan.

Medium term – 10-year financial planning period

This asset management plan identifies the projected operations, maintenance and capital renewal

expenditures required to provide an agreed level of service to the community over a 10-year

period. This provides input into 10 year financial and funding plans aimed at providing the

required services in a sustainable manner.

These projected expenditures may be compared to budgeted expenditures in the 10-year period

to identify any funding shortfall. In a core asset management plan, a gap is generally due to

increasing asset renewals for ageing assets.

The projected operations, maintenance and capital renewal expenditure required over the 10 year

planning period is $455,000 per year.

18

Life cycle costs (or whole of life costs) are the average costs that are required to sustain the

service levels over the longest asset life. Life cycle costs include operations and maintenance

expenditure and asset consumption (depreciation expense). The life cycle cost for the services

covered in this asset management plan is $432,000 per year (operations and maintenance

expenditure plus depreciation expense in year 1).

Life cycle costs can be compared to life cycle expenditure to give an indicator of sustainability

in service provision. Life cycle expenditure includes operations, maintenance and capital

renewal expenditure in year 1. Life cycle expenditure will vary depending on the timing of asset

renewals. The life cycle expenditure at the start of the plan is $455,000(operations and

maintenance expenditure plus budgeted capital renewal expenditure in year 1).

A shortfall between life cycle cost and life cycle expenditure is the life cycle gap.

The life cycle gap for services covered by this asset management plan is $23,000 per year (-ve =

gap, +ve = surplus).

Life cycle expenditure is 105% of life cycle costs giving a life cycle sustainability index of 1.05

The life cycle costs and life cycle expenditure comparison highlights any difference between

present outlays and the average cost of providing the service over the long term. If the life cycle

expenditure is less than that life cycle cost, it is most likely that outlays will need to be increased

or cuts in services made in the future.

Knowing the extent and timing of any required increase in outlays and the service consequences

if funding is not available will assist organizations in providing services to their communities in

a financially sustainable manner. This is the purpose of the asset management plans and long

term financial plan.

Medium term – 10-year financial planning period

This asset management plan identifies the projected operations, maintenance and capital renewal

expenditures required to provide an agreed level of service to the community over a 10-year

period. This provides input into 10 year financial and funding plans aimed at providing the

required services in a sustainable manner.

These projected expenditures may be compared to budgeted expenditures in the 10-year period

to identify any funding shortfall. In a core asset management plan, a gap is generally due to

increasing asset renewals for ageing assets.

The projected operations, maintenance and capital renewal expenditure required over the 10 year

planning period is $455,000 per year.

18

Estimated (budget) operations, maintenance and capital renewal funding is $455,000 per year

giving a 10-year funding shortfall of $0 per year and a 10-year sustainability indicator of 1.00.

This indicates that Council has 100% of the projected expenditures needed to provide the

services documented in the asset management plan.

Medium Term – 5-year financial planning period

The projected operations, maintenance and capital renewal expenditure required over the first 5

years of the planning period is $488,000 per year.

Estimated (budget) operations, maintenance and capital renewal funding is $488,000 per year

giving a 5-year funding shortfall of $0. This is 100% of projected expenditures giving a 5-year

sustainability indicator of 1.00.

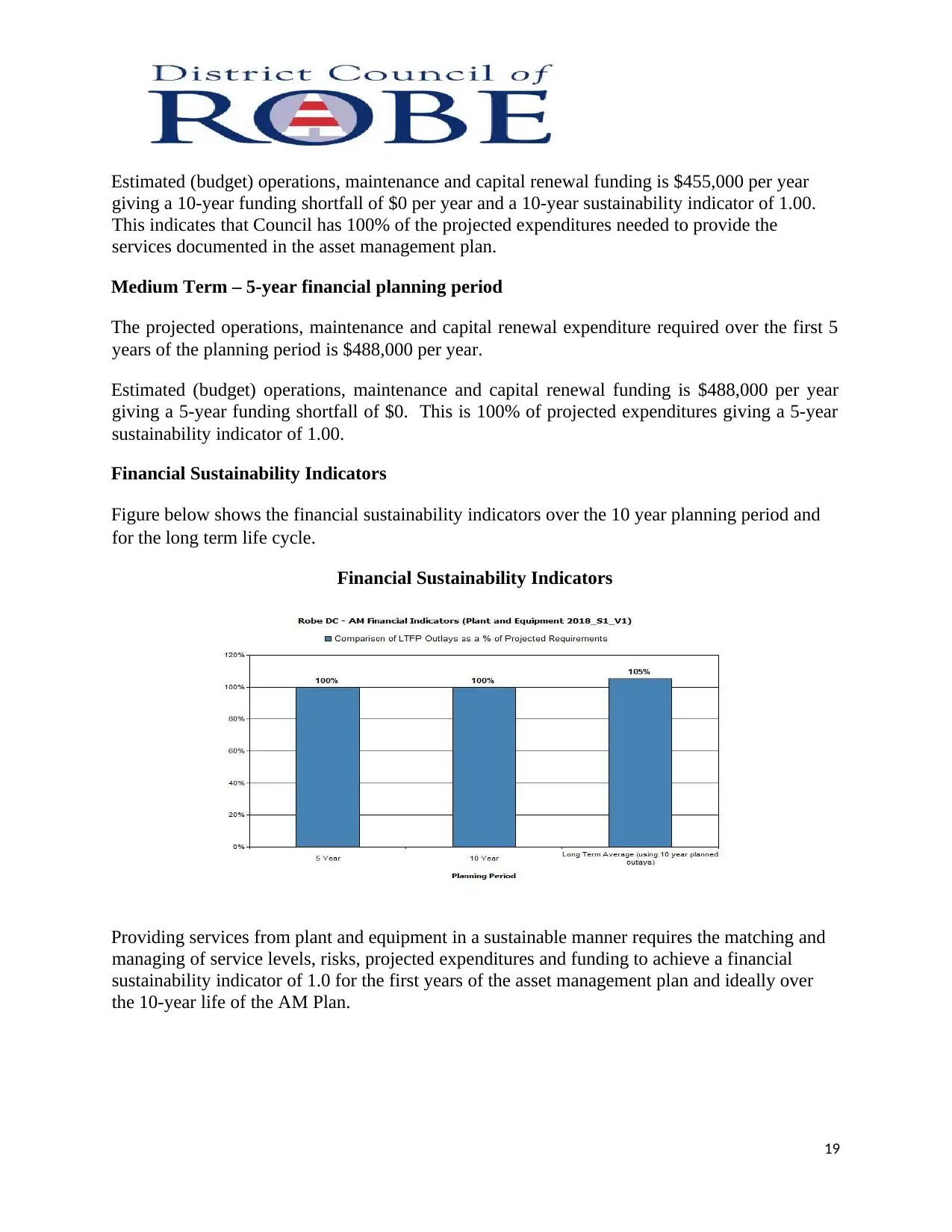

Financial Sustainability Indicators

Figure below shows the financial sustainability indicators over the 10 year planning period and

for the long term life cycle.

Financial Sustainability Indicators

Providing services from plant and equipment in a sustainable manner requires the matching and

managing of service levels, risks, projected expenditures and funding to achieve a financial

sustainability indicator of 1.0 for the first years of the asset management plan and ideally over

the 10-year life of the AM Plan.

19

giving a 10-year funding shortfall of $0 per year and a 10-year sustainability indicator of 1.00.

This indicates that Council has 100% of the projected expenditures needed to provide the

services documented in the asset management plan.

Medium Term – 5-year financial planning period

The projected operations, maintenance and capital renewal expenditure required over the first 5

years of the planning period is $488,000 per year.

Estimated (budget) operations, maintenance and capital renewal funding is $488,000 per year

giving a 5-year funding shortfall of $0. This is 100% of projected expenditures giving a 5-year

sustainability indicator of 1.00.

Financial Sustainability Indicators

Figure below shows the financial sustainability indicators over the 10 year planning period and

for the long term life cycle.

Financial Sustainability Indicators

Providing services from plant and equipment in a sustainable manner requires the matching and

managing of service levels, risks, projected expenditures and funding to achieve a financial

sustainability indicator of 1.0 for the first years of the asset management plan and ideally over

the 10-year life of the AM Plan.

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

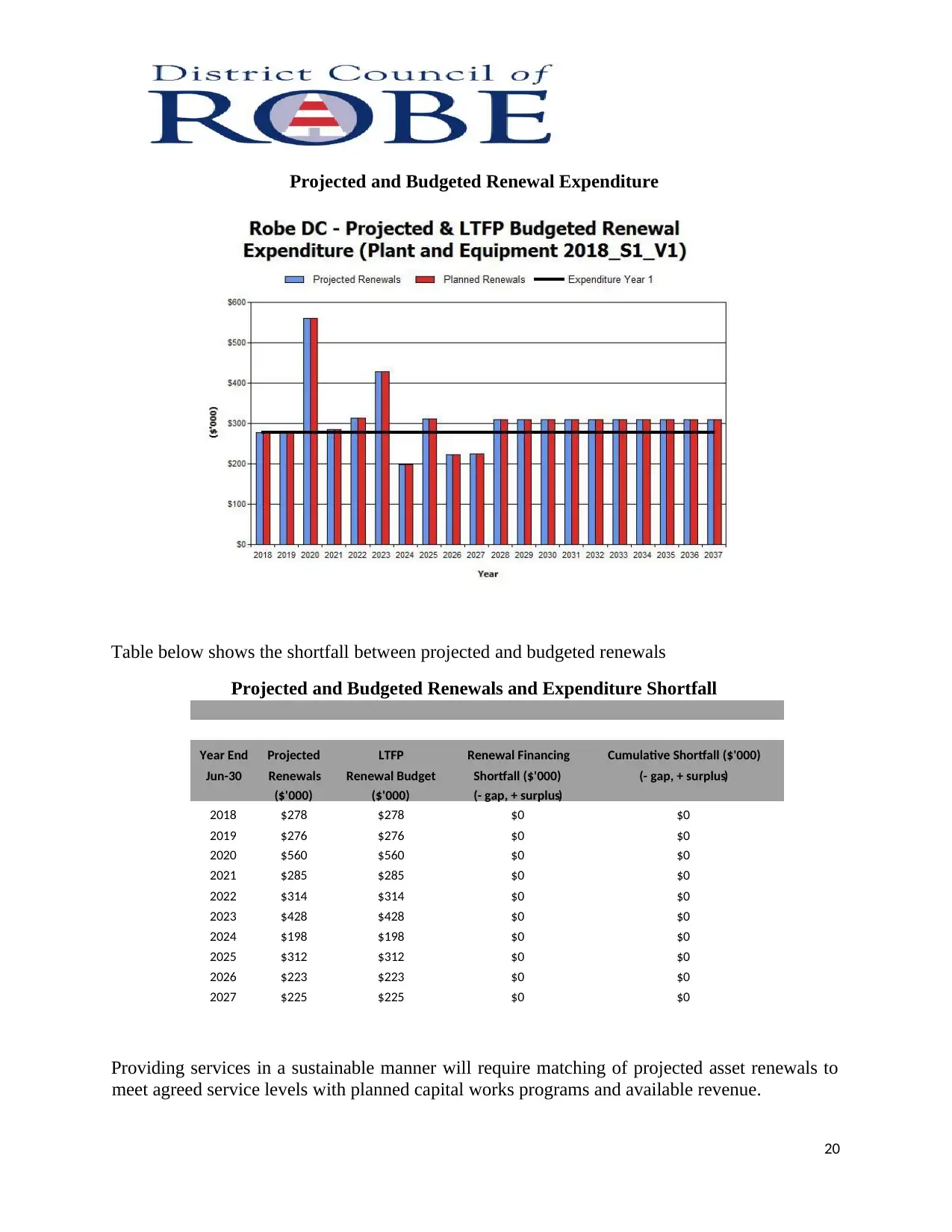

Projected and Budgeted Renewal Expenditure

Table below shows the shortfall between projected and budgeted renewals

Projected and Budgeted Renewals and Expenditure Shortfall

Providing services in a sustainable manner will require matching of projected asset renewals to

meet agreed service levels with planned capital works programs and available revenue.

20

Year End Projected Cumulative Shortfall ($'000)LTFP Renewal Financing

gap, + surplusJun-30 Renewals )Renewal Budget (-Shortfall ($'000)

$'($'000) 000) (- gap, + surplus)(

$0$278 $2782018 $0

$2762019 $0 $0$276

$5602020 $0 $0$560

$2852021 $0 $0$285

$3142022 $0 $0$314

2023 $0$0$428 $428

2024 $0 $0$198 $198

$0$02025 $312 $312

$0$02026 $223 $223

$0$0$2252027 $225

Table below shows the shortfall between projected and budgeted renewals

Projected and Budgeted Renewals and Expenditure Shortfall

Providing services in a sustainable manner will require matching of projected asset renewals to

meet agreed service levels with planned capital works programs and available revenue.

20

Year End Projected Cumulative Shortfall ($'000)LTFP Renewal Financing

gap, + surplusJun-30 Renewals )Renewal Budget (-Shortfall ($'000)

$'($'000) 000) (- gap, + surplus)(

$0$278 $2782018 $0

$2762019 $0 $0$276

$5602020 $0 $0$560

$2852021 $0 $0$285

$3142022 $0 $0$314

2023 $0$0$428 $428

2024 $0 $0$198 $198

$0$02025 $312 $312

$0$02026 $223 $223

$0$0$2252027 $225

A gap between projected asset renewals, planned asset renewals and funding indicates that

further work is required to manage required service levels and funding to eliminate any funding

gap.

We will manage the ‘gap’ by developing this asset management plan to provide guidance on

future service levels and resources required to provide these services, and review future services,

service levels and costs with the community.

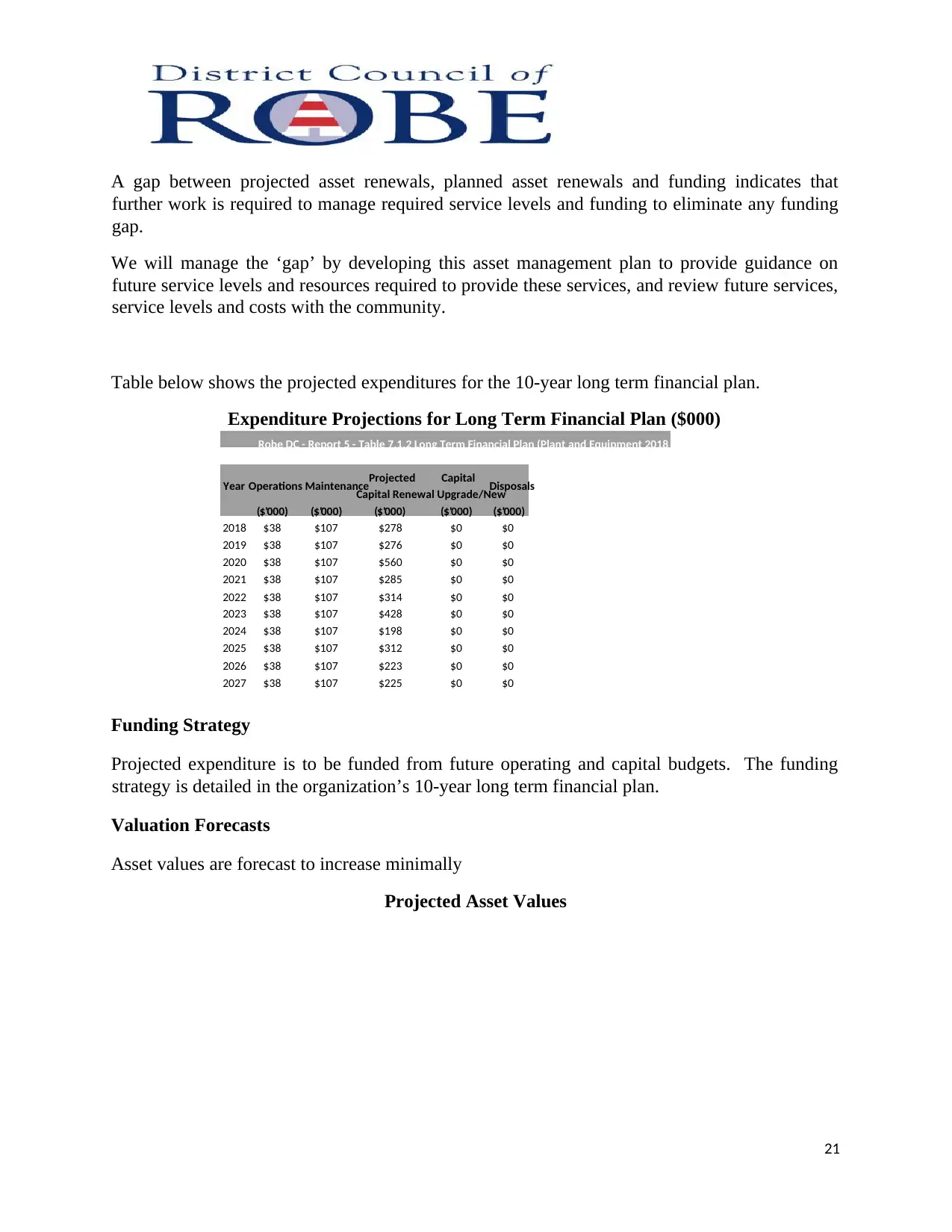

Table below shows the projected expenditures for the 10-year long term financial plan.

Expenditure Projections for Long Term Financial Plan ($000)

Funding Strategy

Projected expenditure is to be funded from future operating and capital budgets. The funding

strategy is detailed in the organization’s 10-year long term financial plan.

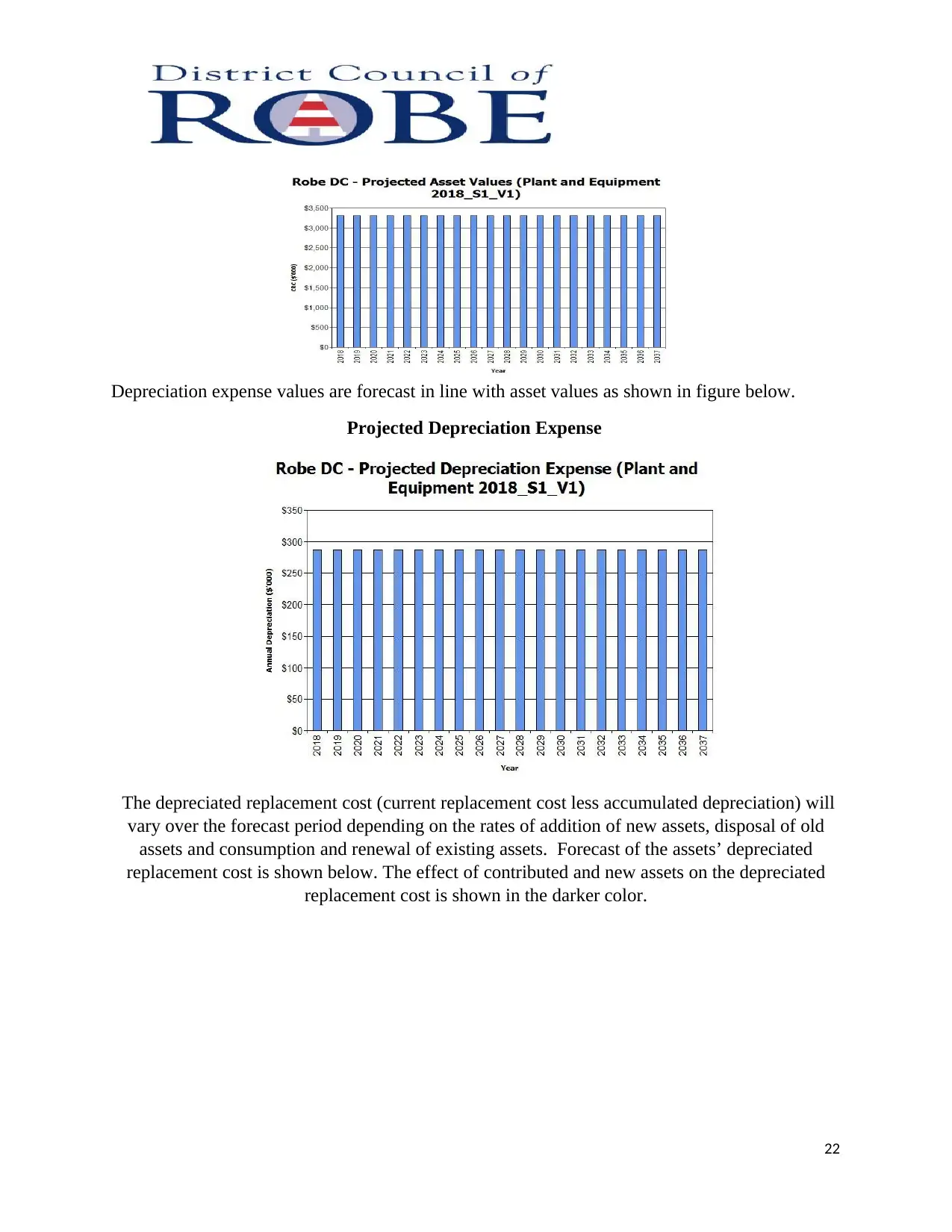

Valuation Forecasts

Asset values are forecast to increase minimally

Projected Asset Values

21

Projected Capital

Capital Renewal Upgrade/New

($'000) (($'000) $'($'000) 000)($'000)

$38 $0$278$1072018 $0

$276 $0$1072019 $0$38

2020 $0$107 $0$560$38

$0$107 $02021 $285$38

$1072022 $0$0$314$38

2023 $0$107 $0$38 $428

$0 $0$38 $1072024 $198

$0$0$382025 $107 $312

$0$0$38 $1072026 $223

$0$38 $0$1072027 $225

Robe DC - Report 5 - Table 7.1.2 Long Term Financial Plan (Plant and Equipment 2018_S1_V1)

DisposalsOperations MaintenanceYear

further work is required to manage required service levels and funding to eliminate any funding

gap.

We will manage the ‘gap’ by developing this asset management plan to provide guidance on

future service levels and resources required to provide these services, and review future services,

service levels and costs with the community.

Table below shows the projected expenditures for the 10-year long term financial plan.

Expenditure Projections for Long Term Financial Plan ($000)

Funding Strategy

Projected expenditure is to be funded from future operating and capital budgets. The funding

strategy is detailed in the organization’s 10-year long term financial plan.

Valuation Forecasts

Asset values are forecast to increase minimally

Projected Asset Values

21

Projected Capital

Capital Renewal Upgrade/New

($'000) (($'000) $'($'000) 000)($'000)

$38 $0$278$1072018 $0

$276 $0$1072019 $0$38

2020 $0$107 $0$560$38

$0$107 $02021 $285$38

$1072022 $0$0$314$38

2023 $0$107 $0$38 $428

$0 $0$38 $1072024 $198

$0$0$382025 $107 $312

$0$0$38 $1072026 $223

$0$38 $0$1072027 $225

Robe DC - Report 5 - Table 7.1.2 Long Term Financial Plan (Plant and Equipment 2018_S1_V1)

DisposalsOperations MaintenanceYear

Depreciation expense values are forecast in line with asset values as shown in figure below.

Projected Depreciation Expense

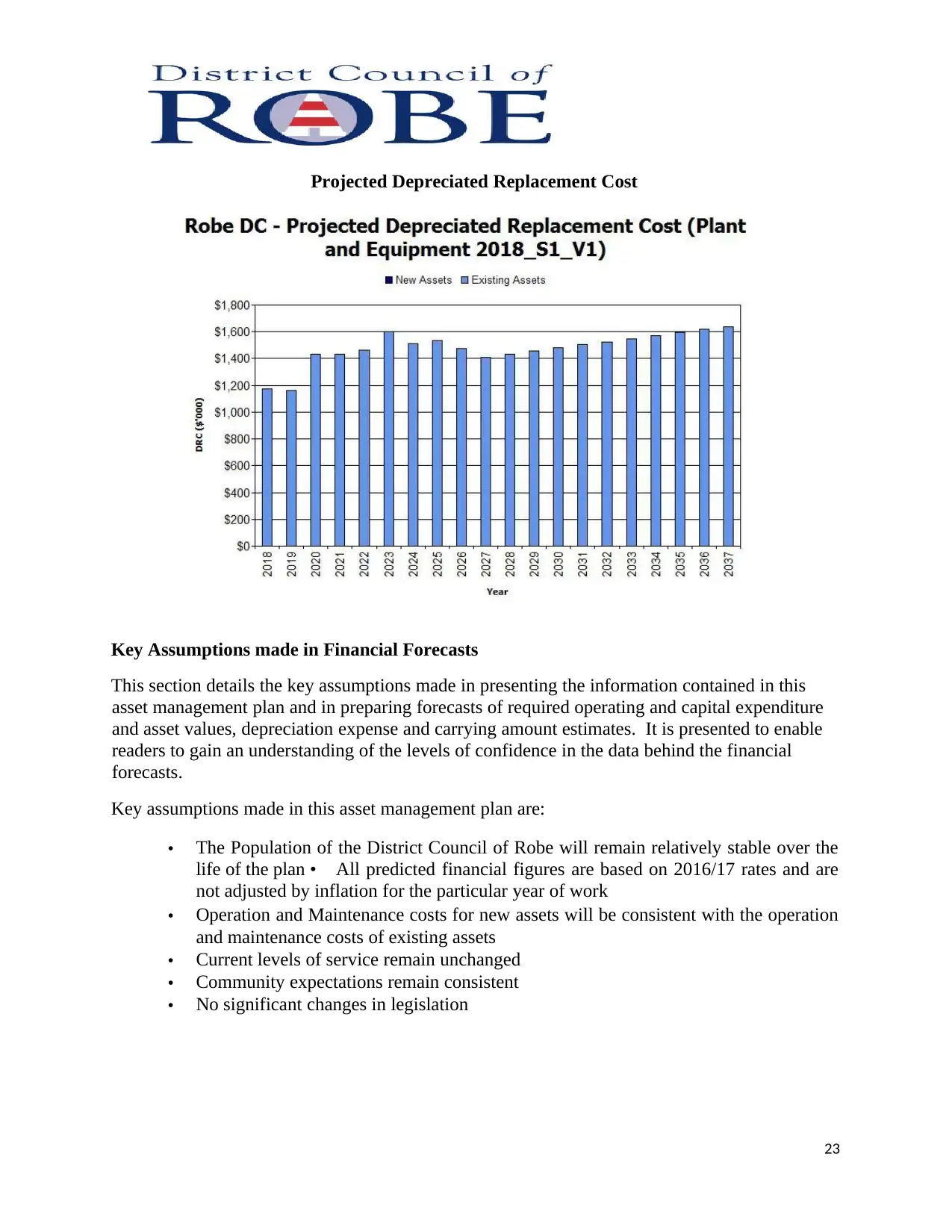

The depreciated replacement cost (current replacement cost less accumulated depreciation) will

vary over the forecast period depending on the rates of addition of new assets, disposal of old

assets and consumption and renewal of existing assets. Forecast of the assets’ depreciated

replacement cost is shown below. The effect of contributed and new assets on the depreciated

replacement cost is shown in the darker color.

22

Projected Depreciation Expense

The depreciated replacement cost (current replacement cost less accumulated depreciation) will

vary over the forecast period depending on the rates of addition of new assets, disposal of old

assets and consumption and renewal of existing assets. Forecast of the assets’ depreciated

replacement cost is shown below. The effect of contributed and new assets on the depreciated

replacement cost is shown in the darker color.

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Projected Depreciated Replacement Cost

Key Assumptions made in Financial Forecasts

This section details the key assumptions made in presenting the information contained in this

asset management plan and in preparing forecasts of required operating and capital expenditure

and asset values, depreciation expense and carrying amount estimates. It is presented to enable

readers to gain an understanding of the levels of confidence in the data behind the financial

forecasts.

Key assumptions made in this asset management plan are:

• The Population of the District Council of Robe will remain relatively stable over the

life of the plan • All predicted financial figures are based on 2016/17 rates and are

not adjusted by inflation for the particular year of work

• Operation and Maintenance costs for new assets will be consistent with the operation

and maintenance costs of existing assets

• Current levels of service remain unchanged

• Community expectations remain consistent

• No significant changes in legislation

23

Key Assumptions made in Financial Forecasts

This section details the key assumptions made in presenting the information contained in this

asset management plan and in preparing forecasts of required operating and capital expenditure

and asset values, depreciation expense and carrying amount estimates. It is presented to enable

readers to gain an understanding of the levels of confidence in the data behind the financial

forecasts.

Key assumptions made in this asset management plan are:

• The Population of the District Council of Robe will remain relatively stable over the

life of the plan • All predicted financial figures are based on 2016/17 rates and are

not adjusted by inflation for the particular year of work

• Operation and Maintenance costs for new assets will be consistent with the operation

and maintenance costs of existing assets

• Current levels of service remain unchanged

• Community expectations remain consistent

• No significant changes in legislation

23

ASSET MANAGEMENT PRACTICES

Accounting/Financial Systems

Accounting and financial systems

Council’s financial accounting system is a combination of ITVIsion’s Synergy Soft System and

Microsoft Spreadsheets. Synergy Soft is used to record the budgets for all projects and captures

all operating and capital expenses. This information is manually transferred to Council’s asset

registers located in Microsoft Excel which produces the required outputs.

Accountabilities for financial systems

Management of Synergy Soft and the Council’s Asset Registers is the responsibility of all staff.

Accounting standards and regulations

Council’s accounting practices comply with the Local Government Act 1999 and the Local

Government (Financial Management) Regulations and applicable Accounting Standards.

Council is also subject to regular independent audits of its accounting systems and practices.

Capital/maintenance threshold

Council’s Asset Capitalization and Materiality Threshold Policy states that the capitalization

threshold is $1,000.

Required changes to accounting financial systems arising from this AM Plan

To be considered in future revisions of this plan.

Asset Management Systems

Combination of Synergy Soft and Microsoft excel spreadsheets.

All Plant and equipment asset register data is held in Microsoft excel spreadsheets.

Currently all financial data is linked manually to the asset register.

Information Flow Requirements and Processes

The key information flows into this asset management plan are:

• Council strategic and operational plans,

• Service requests from the community,

• Network assets information,

• The unit rates for categories of work/materials,

• Current levels of service, expenditures, service deficiencies and service risks,

24

Accounting/Financial Systems

Accounting and financial systems

Council’s financial accounting system is a combination of ITVIsion’s Synergy Soft System and

Microsoft Spreadsheets. Synergy Soft is used to record the budgets for all projects and captures

all operating and capital expenses. This information is manually transferred to Council’s asset

registers located in Microsoft Excel which produces the required outputs.

Accountabilities for financial systems

Management of Synergy Soft and the Council’s Asset Registers is the responsibility of all staff.

Accounting standards and regulations

Council’s accounting practices comply with the Local Government Act 1999 and the Local

Government (Financial Management) Regulations and applicable Accounting Standards.

Council is also subject to regular independent audits of its accounting systems and practices.

Capital/maintenance threshold

Council’s Asset Capitalization and Materiality Threshold Policy states that the capitalization

threshold is $1,000.

Required changes to accounting financial systems arising from this AM Plan

To be considered in future revisions of this plan.

Asset Management Systems

Combination of Synergy Soft and Microsoft excel spreadsheets.

All Plant and equipment asset register data is held in Microsoft excel spreadsheets.

Currently all financial data is linked manually to the asset register.

Information Flow Requirements and Processes

The key information flows into this asset management plan are:

• Council strategic and operational plans,

• Service requests from the community,

• Network assets information,

• The unit rates for categories of work/materials,

• Current levels of service, expenditures, service deficiencies and service risks,

24

• Projections of various factors affecting future demand for services and new assets

acquired by Council, • Future capital works programs,

• Financial asset values.

The key information flows from this asset management plan are:

• The projected Works Program and trends,

• The resulting budget and long term financial plan expenditure projections,

• Financial sustainability indicators.

These will impact the Long Term Financial Plan, Strategic Longer-Term Plan, annual budget and

departmental business plans and budgets.

Standards and Guidelines

Standards, guidelines and policy documents referenced in this asset management plan are:

• District Council of Robe Asset Management Policy

• District Council of Robe Asset Management Strategy

• District Council of Robe Strategic Plan 2014-2018

PLAN IMPROVEMENT AND MONITORING

Performance Measures

The effectiveness of the asset management plan can be measured in the following ways:

• The degree to which the required cash flows identified in this asset management plan

are incorporated into the organization’s long term financial plan and

Community/Strategic Planning processes and documents,

• The degree to which 1-5 year detailed works programs, budgets, business plans and

organizational structures take into account the ‘global’ works program trends

provided by the asset management plan;

Improvement Plan

The asset management improvement plan generated from this asset management plan is shown in

below.

Improvement Plan

Task

No

Task Responsibility Resources

Required

Timeline

1 Collect condition data on all plant and

equipment assets

Senior

Managers

In house and

consultants

Ongoing

25

acquired by Council, • Future capital works programs,

• Financial asset values.

The key information flows from this asset management plan are:

• The projected Works Program and trends,

• The resulting budget and long term financial plan expenditure projections,

• Financial sustainability indicators.

These will impact the Long Term Financial Plan, Strategic Longer-Term Plan, annual budget and

departmental business plans and budgets.

Standards and Guidelines

Standards, guidelines and policy documents referenced in this asset management plan are:

• District Council of Robe Asset Management Policy

• District Council of Robe Asset Management Strategy

• District Council of Robe Strategic Plan 2014-2018

PLAN IMPROVEMENT AND MONITORING

Performance Measures

The effectiveness of the asset management plan can be measured in the following ways:

• The degree to which the required cash flows identified in this asset management plan

are incorporated into the organization’s long term financial plan and

Community/Strategic Planning processes and documents,

• The degree to which 1-5 year detailed works programs, budgets, business plans and

organizational structures take into account the ‘global’ works program trends

provided by the asset management plan;

Improvement Plan

The asset management improvement plan generated from this asset management plan is shown in

below.

Improvement Plan

Task

No

Task Responsibility Resources

Required

Timeline

1 Collect condition data on all plant and

equipment assets

Senior

Managers

In house and

consultants

Ongoing

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

3

4

5

6

7

8

9

10

Monitoring and Review Procedures

This asset management plan will be reviewed during annual budget preparation and amended to

recognize any material changes in service levels and/or resources available to provide those

services as a result of the budget decision process.

The Plan has a life of 4 years and is due for revision and updating annually.

26

3

4

5

6

7

8

9

10

Monitoring and Review Procedures

This asset management plan will be reviewed during annual budget preparation and amended to

recognize any material changes in service levels and/or resources available to provide those

services as a result of the budget decision process.

The Plan has a life of 4 years and is due for revision and updating annually.

26

1 out of 26

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.