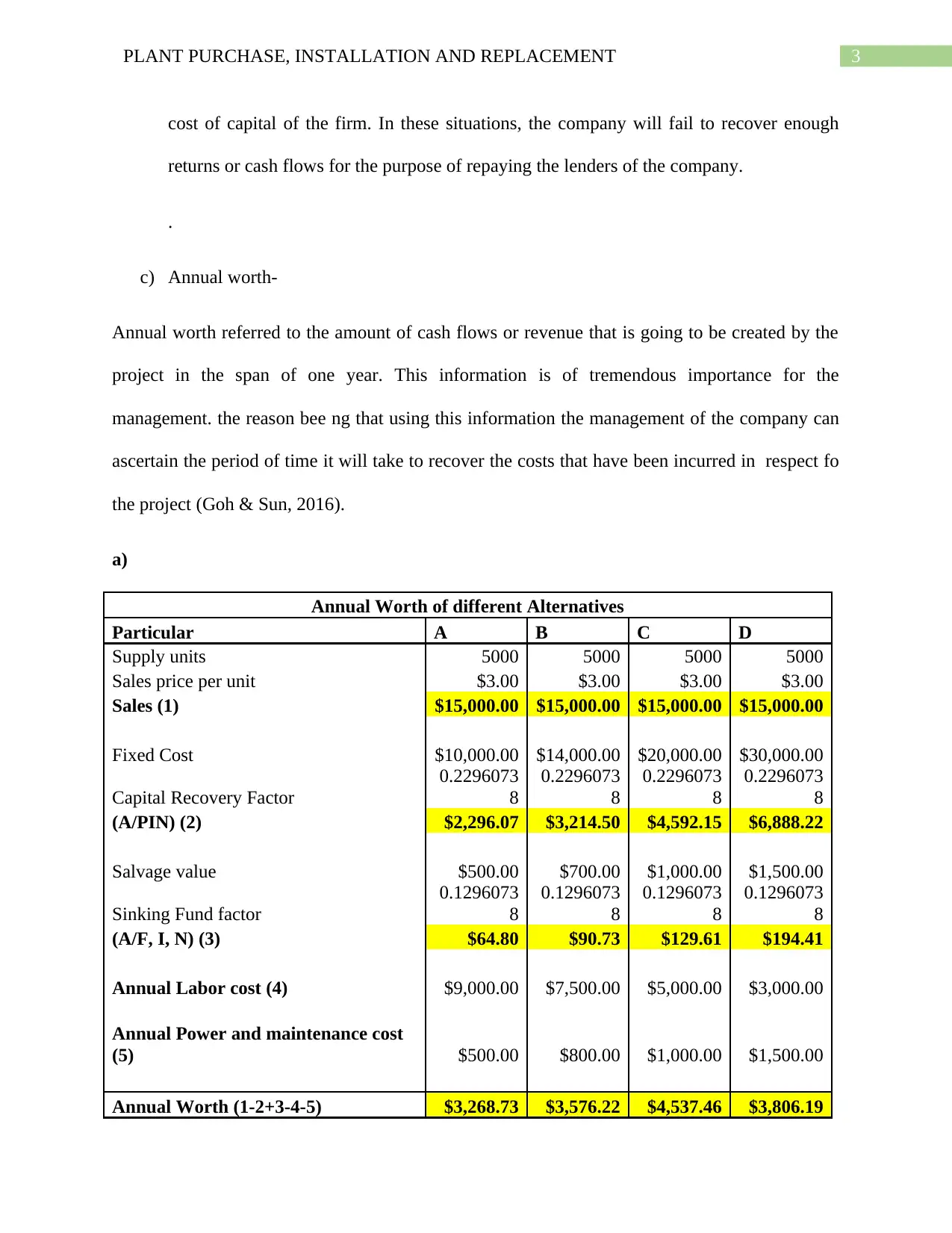

Answer to Question 1 2 5 Answer to Question 4 8 Answer to Question 4 8 Answer to Question 4 8 Answer to Question 5 8 Answer to Question 4 8 Answer to Question 5 8 Answer to Question 4 8 Answer to Ques

VerifiedAdded on 2021/06/15

|14

|3332

|481

AI Summary

The reason for their utility is as follows: Present Worth- FO rate purpose of determining the real value of the returns generated by the project the company makes sure that the cash flow received from the project is discounted for factors like fluctuations in the inflation rate, the risk that is borne and the corresponding return expected by the shareholders and variety of other factors. the reason bee ng that using this information the management of the company can ascertain the period of time it will take to recover the costs that have

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Plant purchase, Installation and replacement

Name of the Student:

Name of the University:

Authors Note:

Plant purchase, Installation and replacement

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................3

b)..................................................................................................................................................4

c)..................................................................................................................................................4

Answer to Question 2......................................................................................................................5

Answer to Question 3......................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Answer to Question 4......................................................................................................................8

Answer to Question 5......................................................................................................................8

Reference.......................................................................................................................................12

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................3

b)..................................................................................................................................................4

c)..................................................................................................................................................4

Answer to Question 2......................................................................................................................5

Answer to Question 3......................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Answer to Question 4......................................................................................................................8

Answer to Question 5......................................................................................................................8

Reference.......................................................................................................................................12

2PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Answer to Question 1

The usage of the methods of present worth, annual worth and internal rate fo return are

extensive in case of the various capital budgeting decision making processes. The reason for

their utility is as follows:

a) Present Worth-

FO rate purpose of determining the real value of the returns generated by the project the

company makes sure that the cash flow received from the project is discounted for factors

like fluctuations in the inflation rate, the risk that is borne and the corresponding return

expected by the shareholders and variety of other factors. After the cash flows of the

entity are discounted to factor in these elements, the present value of the cash flow is

received by the management (Ciroth et al., 2015). This is a significant tool FO the

purpose of decision making by the company.

b) Internal rate of return-

This is referred to the percentage of returns that is being created by the project for the

stakeholders in its entire lifetime. The internal rate of return of the project must at all

items be more than the cost of capital of the company. Cost of capital refers to the

amount that the company will have to the lenders and the financial institutions that

provided the company with the requisite funds for the project on the form of interest ND

the repayment of the principle amount. It also considers the return that is expected by the

shareholders of the company (Bierer et al., 2015). In many case it is found that the net

present value of the project is positive, but the internal rate of return is lower Thant the

Answer to Question 1

The usage of the methods of present worth, annual worth and internal rate fo return are

extensive in case of the various capital budgeting decision making processes. The reason for

their utility is as follows:

a) Present Worth-

FO rate purpose of determining the real value of the returns generated by the project the

company makes sure that the cash flow received from the project is discounted for factors

like fluctuations in the inflation rate, the risk that is borne and the corresponding return

expected by the shareholders and variety of other factors. After the cash flows of the

entity are discounted to factor in these elements, the present value of the cash flow is

received by the management (Ciroth et al., 2015). This is a significant tool FO the

purpose of decision making by the company.

b) Internal rate of return-

This is referred to the percentage of returns that is being created by the project for the

stakeholders in its entire lifetime. The internal rate of return of the project must at all

items be more than the cost of capital of the company. Cost of capital refers to the

amount that the company will have to the lenders and the financial institutions that

provided the company with the requisite funds for the project on the form of interest ND

the repayment of the principle amount. It also considers the return that is expected by the

shareholders of the company (Bierer et al., 2015). In many case it is found that the net

present value of the project is positive, but the internal rate of return is lower Thant the

3PLANT PURCHASE, INSTALLATION AND REPLACEMENT

cost of capital of the firm. In these situations, the company will fail to recover enough

returns or cash flows for the purpose of repaying the lenders of the company.

.

c) Annual worth-

Annual worth referred to the amount of cash flows or revenue that is going to be created by the

project in the span of one year. This information is of tremendous importance for the

management. the reason bee ng that using this information the management of the company can

ascertain the period of time it will take to recover the costs that have been incurred in respect fo

the project (Goh & Sun, 2016).

a)

Annual Worth of different Alternatives

Particular A B C D

Supply units 5000 5000 5000 5000

Sales price per unit $3.00 $3.00 $3.00 $3.00

Sales (1) $15,000.00 $15,000.00 $15,000.00 $15,000.00

Fixed Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Capital Recovery Factor

0.2296073

8

0.2296073

8

0.2296073

8

0.2296073

8

(A/PIN) (2) $2,296.07 $3,214.50 $4,592.15 $6,888.22

Salvage value $500.00 $700.00 $1,000.00 $1,500.00

Sinking Fund factor

0.1296073

8

0.1296073

8

0.1296073

8

0.1296073

8

(A/F, I, N) (3) $64.80 $90.73 $129.61 $194.41

Annual Labor cost (4) $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost

(5) $500.00 $800.00 $1,000.00 $1,500.00

Annual Worth (1-2+3-4-5) $3,268.73 $3,576.22 $4,537.46 $3,806.19

cost of capital of the firm. In these situations, the company will fail to recover enough

returns or cash flows for the purpose of repaying the lenders of the company.

.

c) Annual worth-

Annual worth referred to the amount of cash flows or revenue that is going to be created by the

project in the span of one year. This information is of tremendous importance for the

management. the reason bee ng that using this information the management of the company can

ascertain the period of time it will take to recover the costs that have been incurred in respect fo

the project (Goh & Sun, 2016).

a)

Annual Worth of different Alternatives

Particular A B C D

Supply units 5000 5000 5000 5000

Sales price per unit $3.00 $3.00 $3.00 $3.00

Sales (1) $15,000.00 $15,000.00 $15,000.00 $15,000.00

Fixed Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Capital Recovery Factor

0.2296073

8

0.2296073

8

0.2296073

8

0.2296073

8

(A/PIN) (2) $2,296.07 $3,214.50 $4,592.15 $6,888.22

Salvage value $500.00 $700.00 $1,000.00 $1,500.00

Sinking Fund factor

0.1296073

8

0.1296073

8

0.1296073

8

0.1296073

8

(A/F, I, N) (3) $64.80 $90.73 $129.61 $194.41

Annual Labor cost (4) $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost

(5) $500.00 $800.00 $1,000.00 $1,500.00

Annual Worth (1-2+3-4-5) $3,268.73 $3,576.22 $4,537.46 $3,806.19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4PLANT PURCHASE, INSTALLATION AND REPLACEMENT

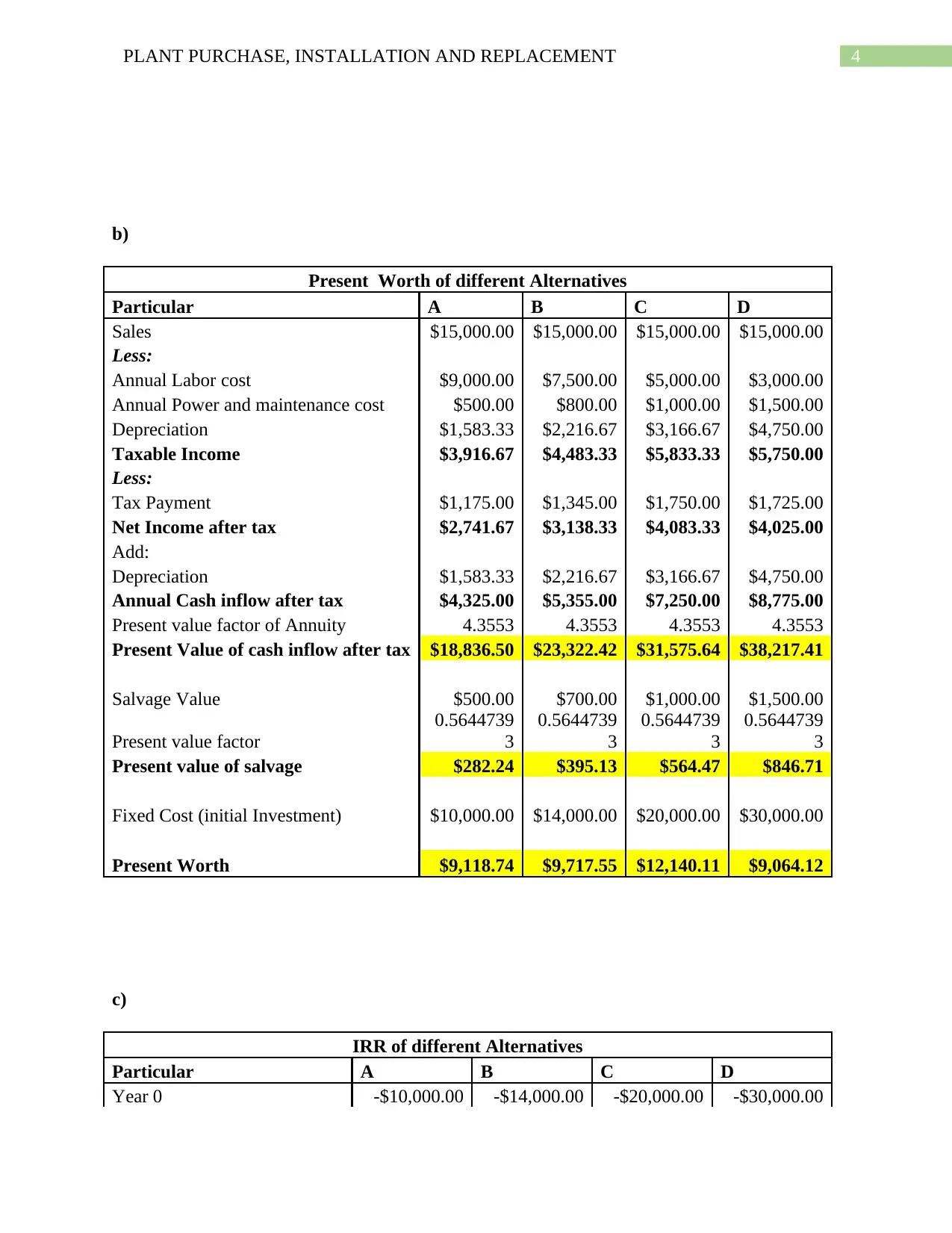

b)

Present Worth of different Alternatives

Particular A B C D

Sales $15,000.00 $15,000.00 $15,000.00 $15,000.00

Less:

Annual Labor cost $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost $500.00 $800.00 $1,000.00 $1,500.00

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Taxable Income $3,916.67 $4,483.33 $5,833.33 $5,750.00

Less:

Tax Payment $1,175.00 $1,345.00 $1,750.00 $1,725.00

Net Income after tax $2,741.67 $3,138.33 $4,083.33 $4,025.00

Add:

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Annual Cash inflow after tax $4,325.00 $5,355.00 $7,250.00 $8,775.00

Present value factor of Annuity 4.3553 4.3553 4.3553 4.3553

Present Value of cash inflow after tax $18,836.50 $23,322.42 $31,575.64 $38,217.41

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

Present value factor

0.5644739

3

0.5644739

3

0.5644739

3

0.5644739

3

Present value of salvage $282.24 $395.13 $564.47 $846.71

Fixed Cost (initial Investment) $10,000.00 $14,000.00 $20,000.00 $30,000.00

Present Worth $9,118.74 $9,717.55 $12,140.11 $9,064.12

c)

IRR of different Alternatives

Particular A B C D

Year 0 -$10,000.00 -$14,000.00 -$20,000.00 -$30,000.00

b)

Present Worth of different Alternatives

Particular A B C D

Sales $15,000.00 $15,000.00 $15,000.00 $15,000.00

Less:

Annual Labor cost $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost $500.00 $800.00 $1,000.00 $1,500.00

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Taxable Income $3,916.67 $4,483.33 $5,833.33 $5,750.00

Less:

Tax Payment $1,175.00 $1,345.00 $1,750.00 $1,725.00

Net Income after tax $2,741.67 $3,138.33 $4,083.33 $4,025.00

Add:

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Annual Cash inflow after tax $4,325.00 $5,355.00 $7,250.00 $8,775.00

Present value factor of Annuity 4.3553 4.3553 4.3553 4.3553

Present Value of cash inflow after tax $18,836.50 $23,322.42 $31,575.64 $38,217.41

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

Present value factor

0.5644739

3

0.5644739

3

0.5644739

3

0.5644739

3

Present value of salvage $282.24 $395.13 $564.47 $846.71

Fixed Cost (initial Investment) $10,000.00 $14,000.00 $20,000.00 $30,000.00

Present Worth $9,118.74 $9,717.55 $12,140.11 $9,064.12

c)

IRR of different Alternatives

Particular A B C D

Year 0 -$10,000.00 -$14,000.00 -$20,000.00 -$30,000.00

5PLANT PURCHASE, INSTALLATION AND REPLACEMENT

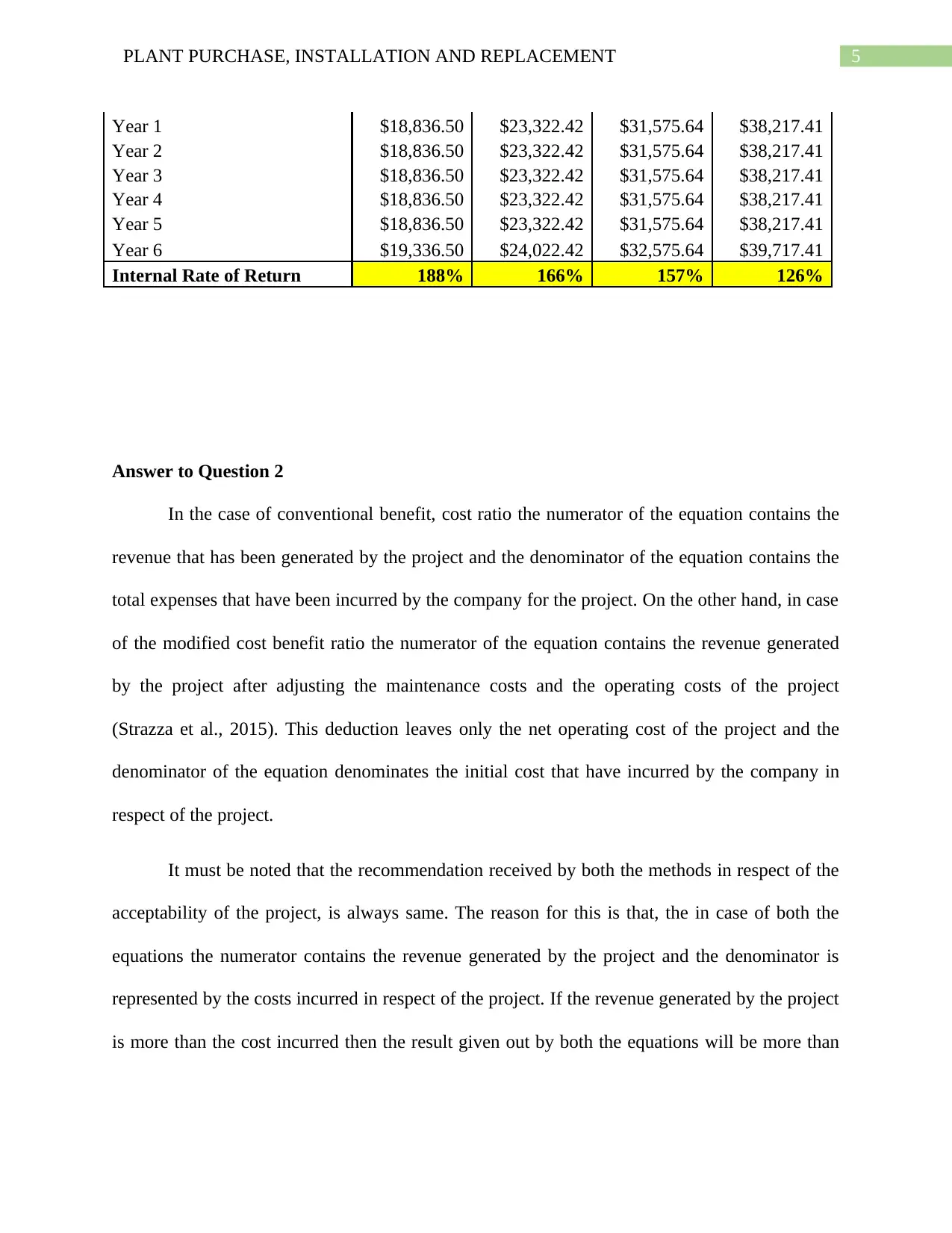

Year 1 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 2 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 3 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 4 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 5 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 6 $19,336.50 $24,022.42 $32,575.64 $39,717.41

Internal Rate of Return 188% 166% 157% 126%

Answer to Question 2

In the case of conventional benefit, cost ratio the numerator of the equation contains the

revenue that has been generated by the project and the denominator of the equation contains the

total expenses that have been incurred by the company for the project. On the other hand, in case

of the modified cost benefit ratio the numerator of the equation contains the revenue generated

by the project after adjusting the maintenance costs and the operating costs of the project

(Strazza et al., 2015). This deduction leaves only the net operating cost of the project and the

denominator of the equation denominates the initial cost that have incurred by the company in

respect of the project.

It must be noted that the recommendation received by both the methods in respect of the

acceptability of the project, is always same. The reason for this is that, the in case of both the

equations the numerator contains the revenue generated by the project and the denominator is

represented by the costs incurred in respect of the project. If the revenue generated by the project

is more than the cost incurred then the result given out by both the equations will be more than

Year 1 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 2 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 3 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 4 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 5 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 6 $19,336.50 $24,022.42 $32,575.64 $39,717.41

Internal Rate of Return 188% 166% 157% 126%

Answer to Question 2

In the case of conventional benefit, cost ratio the numerator of the equation contains the

revenue that has been generated by the project and the denominator of the equation contains the

total expenses that have been incurred by the company for the project. On the other hand, in case

of the modified cost benefit ratio the numerator of the equation contains the revenue generated

by the project after adjusting the maintenance costs and the operating costs of the project

(Strazza et al., 2015). This deduction leaves only the net operating cost of the project and the

denominator of the equation denominates the initial cost that have incurred by the company in

respect of the project.

It must be noted that the recommendation received by both the methods in respect of the

acceptability of the project, is always same. The reason for this is that, the in case of both the

equations the numerator contains the revenue generated by the project and the denominator is

represented by the costs incurred in respect of the project. If the revenue generated by the project

is more than the cost incurred then the result given out by both the equations will be more than

6PLANT PURCHASE, INSTALLATION AND REPLACEMENT

one. In case the costs incurred by the project are more than the revenue generated by the project,

the result will be less than one (Auer et al., 2017).

Hence, in case of capital budgeting decisions this method can be used effectively. If the

result I given out as more than one the project must be accepted, if the result is below one then

the project must be dismissed.

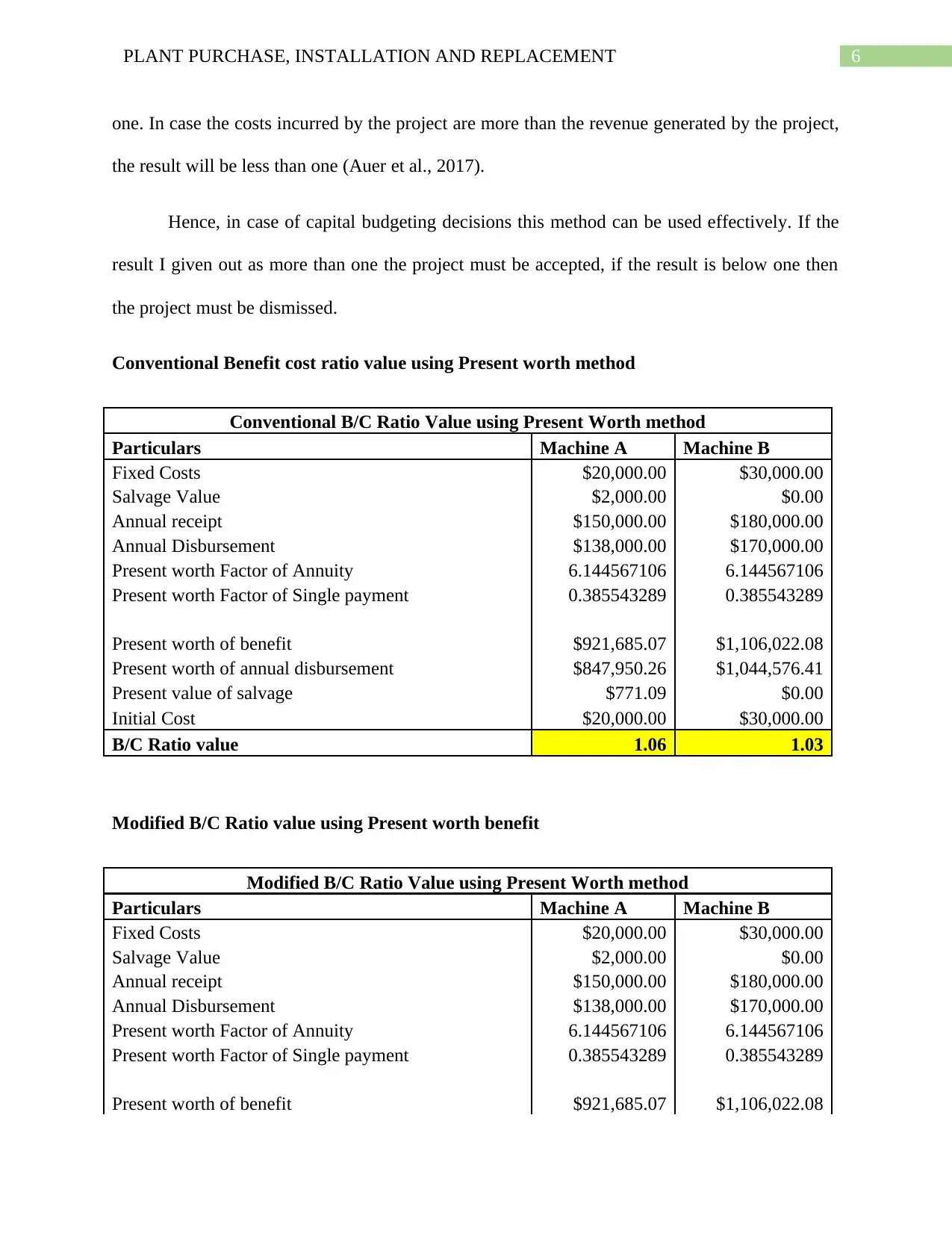

Conventional Benefit cost ratio value using Present worth method

Conventional B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 1.06 1.03

Modified B/C Ratio value using Present worth benefit

Modified B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

one. In case the costs incurred by the project are more than the revenue generated by the project,

the result will be less than one (Auer et al., 2017).

Hence, in case of capital budgeting decisions this method can be used effectively. If the

result I given out as more than one the project must be accepted, if the result is below one then

the project must be dismissed.

Conventional Benefit cost ratio value using Present worth method

Conventional B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 1.06 1.03

Modified B/C Ratio value using Present worth benefit

Modified B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 3.83 2.05

Answer to Question 3

1.

Calculation of the After Tax Cash flow of the Leasing alternatives

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost 80000 60000 50000 50000 50000 50000 50000 50000 50000 50000

Other costs 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Total Costs 84000 64000 54000 54000 54000 54000 54000 54000 54000 54000

Tax savings on expenses 25200 19200 16200 16200 16200 16200 16200 16200 16200 16200

After Tax Cash Flow 58800 44800 37800 37800 37800 37800 37800 37800 37800 37800

2

Calculation of Equivalent Annual cost for the alternative ($)

Particulars 1 2 3 4 5 6 7 8 9 10

After Tax Cash Flow 56000 42000 35000 35000 35000 35000 35000 35000 35000 35000

PV factor 0.9091

0.826

4

0.751

3

0.683

0

0.620

9

0.564

5

0.513

2

0.466

5

0.424

1

0.385

5

PV of Cash flow 50909 34711 26296 23905 21732 19757 17961 16328 14843 13494

Net Present Value 239936

Annuity Factor

6.14456710

6

Equivalent Annual Leasing Costs 39048

Other costs 4000

Equivalent Annual Cost 43048

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 3.83 2.05

Answer to Question 3

1.

Calculation of the After Tax Cash flow of the Leasing alternatives

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost 80000 60000 50000 50000 50000 50000 50000 50000 50000 50000

Other costs 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Total Costs 84000 64000 54000 54000 54000 54000 54000 54000 54000 54000

Tax savings on expenses 25200 19200 16200 16200 16200 16200 16200 16200 16200 16200

After Tax Cash Flow 58800 44800 37800 37800 37800 37800 37800 37800 37800 37800

2

Calculation of Equivalent Annual cost for the alternative ($)

Particulars 1 2 3 4 5 6 7 8 9 10

After Tax Cash Flow 56000 42000 35000 35000 35000 35000 35000 35000 35000 35000

PV factor 0.9091

0.826

4

0.751

3

0.683

0

0.620

9

0.564

5

0.513

2

0.466

5

0.424

1

0.385

5

PV of Cash flow 50909 34711 26296 23905 21732 19757 17961 16328 14843 13494

Net Present Value 239936

Annuity Factor

6.14456710

6

Equivalent Annual Leasing Costs 39048

Other costs 4000

Equivalent Annual Cost 43048

8PLANT PURCHASE, INSTALLATION AND REPLACEMENT

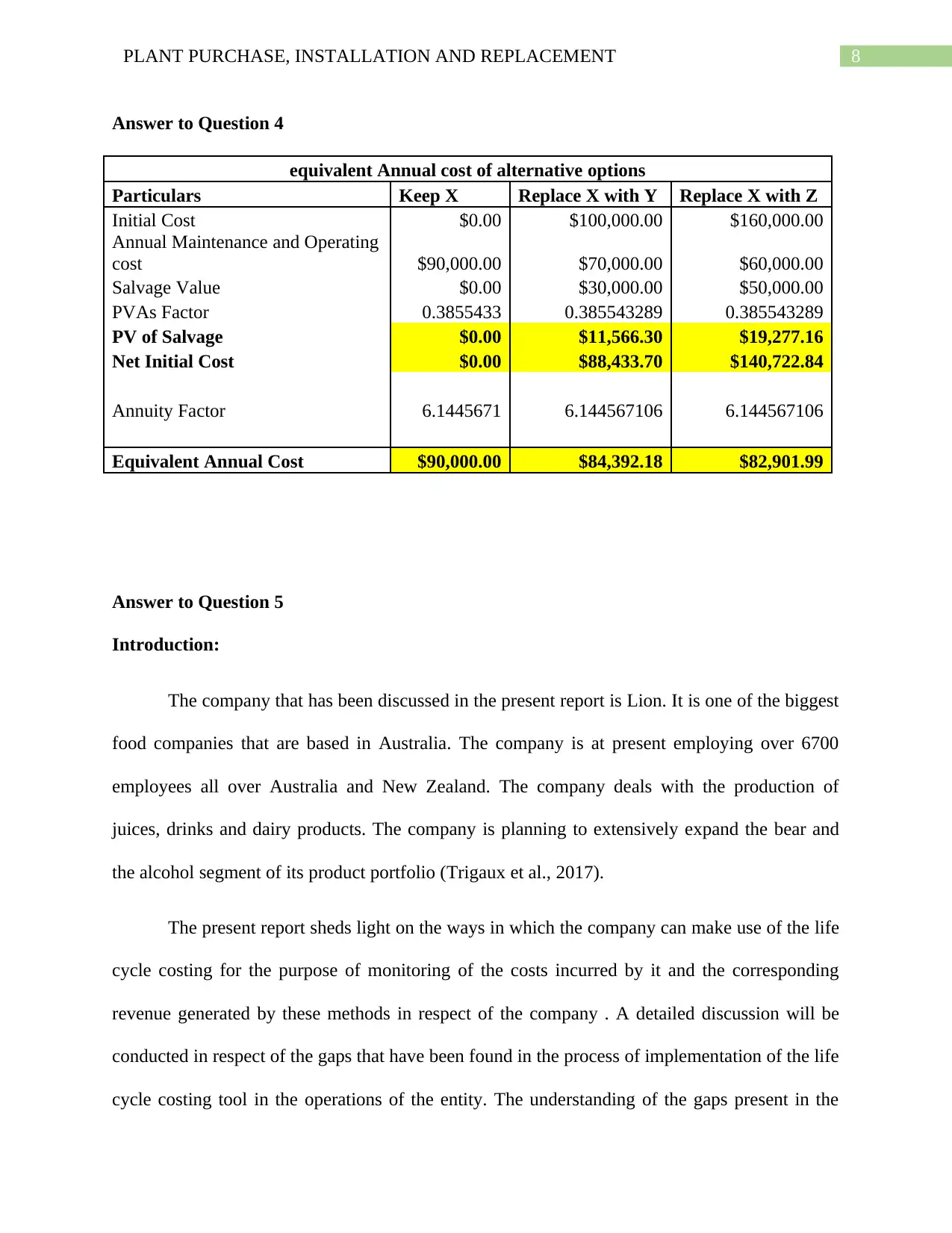

Answer to Question 4

equivalent Annual cost of alternative options

Particulars Keep X Replace X with Y Replace X with Z

Initial Cost $0.00 $100,000.00 $160,000.00

Annual Maintenance and Operating

cost $90,000.00 $70,000.00 $60,000.00

Salvage Value $0.00 $30,000.00 $50,000.00

PVAs Factor 0.3855433 0.385543289 0.385543289

PV of Salvage $0.00 $11,566.30 $19,277.16

Net Initial Cost $0.00 $88,433.70 $140,722.84

Annuity Factor 6.1445671 6.144567106 6.144567106

Equivalent Annual Cost $90,000.00 $84,392.18 $82,901.99

Answer to Question 5

Introduction:

The company that has been discussed in the present report is Lion. It is one of the biggest

food companies that are based in Australia. The company is at present employing over 6700

employees all over Australia and New Zealand. The company deals with the production of

juices, drinks and dairy products. The company is planning to extensively expand the bear and

the alcohol segment of its product portfolio (Trigaux et al., 2017).

The present report sheds light on the ways in which the company can make use of the life

cycle costing for the purpose of monitoring of the costs incurred by it and the corresponding

revenue generated by these methods in respect of the company . A detailed discussion will be

conducted in respect of the gaps that have been found in the process of implementation of the life

cycle costing tool in the operations of the entity. The understanding of the gaps present in the

Answer to Question 4

equivalent Annual cost of alternative options

Particulars Keep X Replace X with Y Replace X with Z

Initial Cost $0.00 $100,000.00 $160,000.00

Annual Maintenance and Operating

cost $90,000.00 $70,000.00 $60,000.00

Salvage Value $0.00 $30,000.00 $50,000.00

PVAs Factor 0.3855433 0.385543289 0.385543289

PV of Salvage $0.00 $11,566.30 $19,277.16

Net Initial Cost $0.00 $88,433.70 $140,722.84

Annuity Factor 6.1445671 6.144567106 6.144567106

Equivalent Annual Cost $90,000.00 $84,392.18 $82,901.99

Answer to Question 5

Introduction:

The company that has been discussed in the present report is Lion. It is one of the biggest

food companies that are based in Australia. The company is at present employing over 6700

employees all over Australia and New Zealand. The company deals with the production of

juices, drinks and dairy products. The company is planning to extensively expand the bear and

the alcohol segment of its product portfolio (Trigaux et al., 2017).

The present report sheds light on the ways in which the company can make use of the life

cycle costing for the purpose of monitoring of the costs incurred by it and the corresponding

revenue generated by these methods in respect of the company . A detailed discussion will be

conducted in respect of the gaps that have been found in the process of implementation of the life

cycle costing tool in the operations of the entity. The understanding of the gaps present in the

9PLANT PURCHASE, INSTALLATION AND REPLACEMENT

implementation process of the tools used by the company must be understood for the purpose of

facilitating the process of alleviating them. After developing an understanding the issues faced

by the company some significant recommendations will be made in this respect to the

management of the company (Bhochhibhoya et al., 2017).

Gaps that have been identified in the system:

It is unrealistic to assume that the implementation of a particular accounting or management

tool will not have any gaps or deficiencies. There can he several gaps in the implementation of

these procedures. The reason for these gaps can be wide ranging and May or Amy not is in the

control of the management. The gaps present in the tools must not deter the management from

making effective use of these tools for monitoring of the operations of the company and creating

value for the shareholders in the end. Proper understanding developed in respect of the gaps

present in the application of the tools in the operations of the company will ensure that the

company is able to alleviate these in the recent future.

a) For the purpose fo referring to the nominal cash flows generated by the project the

nominal rates must be utilised and for the purpose of making use of the actual rates, it

must be ensured by the management of the company that the cash flows or the revenue

generated by the company is adjusted with the variations in the price level index. In

addition to this, the fluctuations in the inflation rates must also be considered (Zanchi et

al., 2016).

b) The cost incurred by the company must also factor in the various systematic risks that are

being incurred by the investors of the company. The reason for considering the impact of

the systematic risk is that in return of the risk incurred by them they expect decent

amount of return from the management of the company.

implementation process of the tools used by the company must be understood for the purpose of

facilitating the process of alleviating them. After developing an understanding the issues faced

by the company some significant recommendations will be made in this respect to the

management of the company (Bhochhibhoya et al., 2017).

Gaps that have been identified in the system:

It is unrealistic to assume that the implementation of a particular accounting or management

tool will not have any gaps or deficiencies. There can he several gaps in the implementation of

these procedures. The reason for these gaps can be wide ranging and May or Amy not is in the

control of the management. The gaps present in the tools must not deter the management from

making effective use of these tools for monitoring of the operations of the company and creating

value for the shareholders in the end. Proper understanding developed in respect of the gaps

present in the application of the tools in the operations of the company will ensure that the

company is able to alleviate these in the recent future.

a) For the purpose fo referring to the nominal cash flows generated by the project the

nominal rates must be utilised and for the purpose of making use of the actual rates, it

must be ensured by the management of the company that the cash flows or the revenue

generated by the company is adjusted with the variations in the price level index. In

addition to this, the fluctuations in the inflation rates must also be considered (Zanchi et

al., 2016).

b) The cost incurred by the company must also factor in the various systematic risks that are

being incurred by the investors of the company. The reason for considering the impact of

the systematic risk is that in return of the risk incurred by them they expect decent

amount of return from the management of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10PLANT PURCHASE, INSTALLATION AND REPLACEMENT

c) For the determination of the weights to be used by the company with respect to the

capital budgeting decisions, the market value of the financial sources must be utilised by

the company (Teshnizi et al., 2018).

d) The discounting rate that is being used by the Lion group I susceptibility to change due to

the impact of several factors that may or may not be in the control of the management.

Some of the factors that can affect the discounting rate to be used by the company include

the inflation rate, the present capital structure of the company and the expected changes

in the future cash flows accruing in respect of the company from the project.

The various recommendations to the management in respect of cost/ benefit and risk

management:

It is of paramount importance that the costs incurred by the company are continuously

monitored by it along with the revenue that is being generated corresponding to the costs

incurred. If the monitoring of the cost incurred and the corresponding cash flows will not be

undertaken hay the management of the company then the use of various accounting and

management toll will be useless FO Rate Company. Hence, all the internal control system that

have been implemented or installed in the organisation is functioning properly. Hence, the

recommendation made by the management is as follows:

a) The company must make sure that the cost incurred by it in respect of measuring the

various carbon emissions and other environmental policy is able to generate intangible

assets for the company like that of goodwill. This will help the shareholders gain some

return rom it in the form of increase in the value FO the shares (Islam et al., 2015).

b) The various factors that affect the cash flow and the revenue generated by the company

must be taken into account by the discounting rate used by the management for capital

c) For the determination of the weights to be used by the company with respect to the

capital budgeting decisions, the market value of the financial sources must be utilised by

the company (Teshnizi et al., 2018).

d) The discounting rate that is being used by the Lion group I susceptibility to change due to

the impact of several factors that may or may not be in the control of the management.

Some of the factors that can affect the discounting rate to be used by the company include

the inflation rate, the present capital structure of the company and the expected changes

in the future cash flows accruing in respect of the company from the project.

The various recommendations to the management in respect of cost/ benefit and risk

management:

It is of paramount importance that the costs incurred by the company are continuously

monitored by it along with the revenue that is being generated corresponding to the costs

incurred. If the monitoring of the cost incurred and the corresponding cash flows will not be

undertaken hay the management of the company then the use of various accounting and

management toll will be useless FO Rate Company. Hence, all the internal control system that

have been implemented or installed in the organisation is functioning properly. Hence, the

recommendation made by the management is as follows:

a) The company must make sure that the cost incurred by it in respect of measuring the

various carbon emissions and other environmental policy is able to generate intangible

assets for the company like that of goodwill. This will help the shareholders gain some

return rom it in the form of increase in the value FO the shares (Islam et al., 2015).

b) The various factors that affect the cash flow and the revenue generated by the company

must be taken into account by the discounting rate used by the management for capital

11PLANT PURCHASE, INSTALLATION AND REPLACEMENT

budgeting decisions. The factors to be used contain elements like increase in the inflation

rate, the expected future cash flows and the systematic risks undertaken by the investors

of the company.

c) For the purpose of determination of the weights to be used by the company, the market

value of the financial resources must be used by the management (Farr et al., 2016).

Conclusion:

The consistence and the maintenance of the cash flows or there avenue generated hay the

company is significantly affected by the various decisions taken up by the management ND their

corresponding cost implications. The returns that are expected by the shareholders FO the

company are also to be factored in the by the management of the company. In addition, an

understanding has to be developed regarding the importance of the fixed assets in the operations

of the business entity. This is because it is by the use of these fixed assets by the company it is

able to generate revenue for the shareholders in the end. Hence, the decisions regarding the

acquisition and other related decisions are of paramount importance to the stakeholders of the

company. Hence, it must be ensured that the right kind of tools is being used by the management

for the purpose of decision-making.

budgeting decisions. The factors to be used contain elements like increase in the inflation

rate, the expected future cash flows and the systematic risks undertaken by the investors

of the company.

c) For the purpose of determination of the weights to be used by the company, the market

value of the financial resources must be used by the management (Farr et al., 2016).

Conclusion:

The consistence and the maintenance of the cash flows or there avenue generated hay the

company is significantly affected by the various decisions taken up by the management ND their

corresponding cost implications. The returns that are expected by the shareholders FO the

company are also to be factored in the by the management of the company. In addition, an

understanding has to be developed regarding the importance of the fixed assets in the operations

of the business entity. This is because it is by the use of these fixed assets by the company it is

able to generate revenue for the shareholders in the end. Hence, the decisions regarding the

acquisition and other related decisions are of paramount importance to the stakeholders of the

company. Hence, it must be ensured that the right kind of tools is being used by the management

for the purpose of decision-making.

12PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Reference

Auer, J., Bey, N., & Schäfer, J. M. (2017). Combined Life Cycle Assessment and Life Cycle

Costing in the Eco-Care-Matrix: A case study on the performance of a modernized

manufacturing system for glass containers. Journal of cleaner production, 141, 99-109.

Bhochhibhoya, S., Pizzol, M., Achten, W. M., Maskey, R. K., Zanetti, M., & Cavalli, R. (2017).

Comparative life cycle assessment and life cycle costing of lodging in the Himalaya. The

International Journal of Life Cycle Assessment, 22(11), 1851-1863.

Bierer, A., Götze, U., Meynerts, L., & Sygulla, R. (2015). Integrating life cycle costing and life

cycle assessment using extended material flow cost accounting. Journal of Cleaner

Production, 108, 1289-1301.

Ciroth, A., Hildenbrand, J., & Steen, B. (2015). Life cycle costing. Sustainability Assessment of

Renewables-Based Products: Methods and Case Studies,, 215-228.

Farr, J. V., Faber, I. J., Ganguly, A., Martin, W. A., & Larson, S. L. (2016). Simulation-based

costing for early phase life cycle cost analysis: Example application to an environmental

remediation project. The Engineering Economist, 61(3), 207-222.

Goh, B. H., & Sun, Y. (2016). The development of life-cycle costing for buildings. Building

Research & Information, 44(3), 319-333.

Islam, H., Jollands, M., & Setunge, S. (2015). Life cycle assessment and life cycle cost

implication of residential buildings—A review. Renewable and Sustainable Energy

Reviews, 42, 129-140.

Reference

Auer, J., Bey, N., & Schäfer, J. M. (2017). Combined Life Cycle Assessment and Life Cycle

Costing in the Eco-Care-Matrix: A case study on the performance of a modernized

manufacturing system for glass containers. Journal of cleaner production, 141, 99-109.

Bhochhibhoya, S., Pizzol, M., Achten, W. M., Maskey, R. K., Zanetti, M., & Cavalli, R. (2017).

Comparative life cycle assessment and life cycle costing of lodging in the Himalaya. The

International Journal of Life Cycle Assessment, 22(11), 1851-1863.

Bierer, A., Götze, U., Meynerts, L., & Sygulla, R. (2015). Integrating life cycle costing and life

cycle assessment using extended material flow cost accounting. Journal of Cleaner

Production, 108, 1289-1301.

Ciroth, A., Hildenbrand, J., & Steen, B. (2015). Life cycle costing. Sustainability Assessment of

Renewables-Based Products: Methods and Case Studies,, 215-228.

Farr, J. V., Faber, I. J., Ganguly, A., Martin, W. A., & Larson, S. L. (2016). Simulation-based

costing for early phase life cycle cost analysis: Example application to an environmental

remediation project. The Engineering Economist, 61(3), 207-222.

Goh, B. H., & Sun, Y. (2016). The development of life-cycle costing for buildings. Building

Research & Information, 44(3), 319-333.

Islam, H., Jollands, M., & Setunge, S. (2015). Life cycle assessment and life cycle cost

implication of residential buildings—A review. Renewable and Sustainable Energy

Reviews, 42, 129-140.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Soni, V., Singh, S. P., & Banwet, D. K. (2016). Sustainable coal consumption and energy

production in India using life cycle costing and real options analysis. Sustainable

Production and Consumption, 6, 26-37.

Strazza, C., Del Borghi, A., Costamagna, P., Gallo, M., Brignole, E., & Girdinio, P. (2015). Life

Cycle Assessment and Life Cycle Costing of a SOFC system for distributed power

generation. Energy conversion and management, 100, 64-77.

Teshnizi, Z., Pilon, A., Storey, S., Lopez, D., & Froese, T. M. (2018). Lessons Learned from Life

Cycle Assessment and Life Cycle Costing of Two Residential Towers at the University

of British Columbia. Procedia CIRP, 69, 172-177.

Trigaux, D., Wijnants, L., De Troyer, F., & Allacker, K. (2017). Life cycle assessment and life

cycle costing of road infrastructure in residential neighbourhoods. The International

Journal of Life Cycle Assessment, 22(6), 938-951.

Zanchi, L., Delogu, M., Ierides, M., & Vasiliadis, H. (2016). Life cycle assessment and life cycle

costing as supporting tools for EVs lightweight design. In Sustainable Design and

Manufacturing 2016 (pp. 335-348). Springer, Cham.

Soni, V., Singh, S. P., & Banwet, D. K. (2016). Sustainable coal consumption and energy

production in India using life cycle costing and real options analysis. Sustainable

Production and Consumption, 6, 26-37.

Strazza, C., Del Borghi, A., Costamagna, P., Gallo, M., Brignole, E., & Girdinio, P. (2015). Life

Cycle Assessment and Life Cycle Costing of a SOFC system for distributed power

generation. Energy conversion and management, 100, 64-77.

Teshnizi, Z., Pilon, A., Storey, S., Lopez, D., & Froese, T. M. (2018). Lessons Learned from Life

Cycle Assessment and Life Cycle Costing of Two Residential Towers at the University

of British Columbia. Procedia CIRP, 69, 172-177.

Trigaux, D., Wijnants, L., De Troyer, F., & Allacker, K. (2017). Life cycle assessment and life

cycle costing of road infrastructure in residential neighbourhoods. The International

Journal of Life Cycle Assessment, 22(6), 938-951.

Zanchi, L., Delogu, M., Ierides, M., & Vasiliadis, H. (2016). Life cycle assessment and life cycle

costing as supporting tools for EVs lightweight design. In Sustainable Design and

Manufacturing 2016 (pp. 335-348). Springer, Cham.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.