Financial Performance of A Plc: Detailed Ratio and Investment Analysis

VerifiedAdded on 2023/06/11

|10

|1854

|417

Report

AI Summary

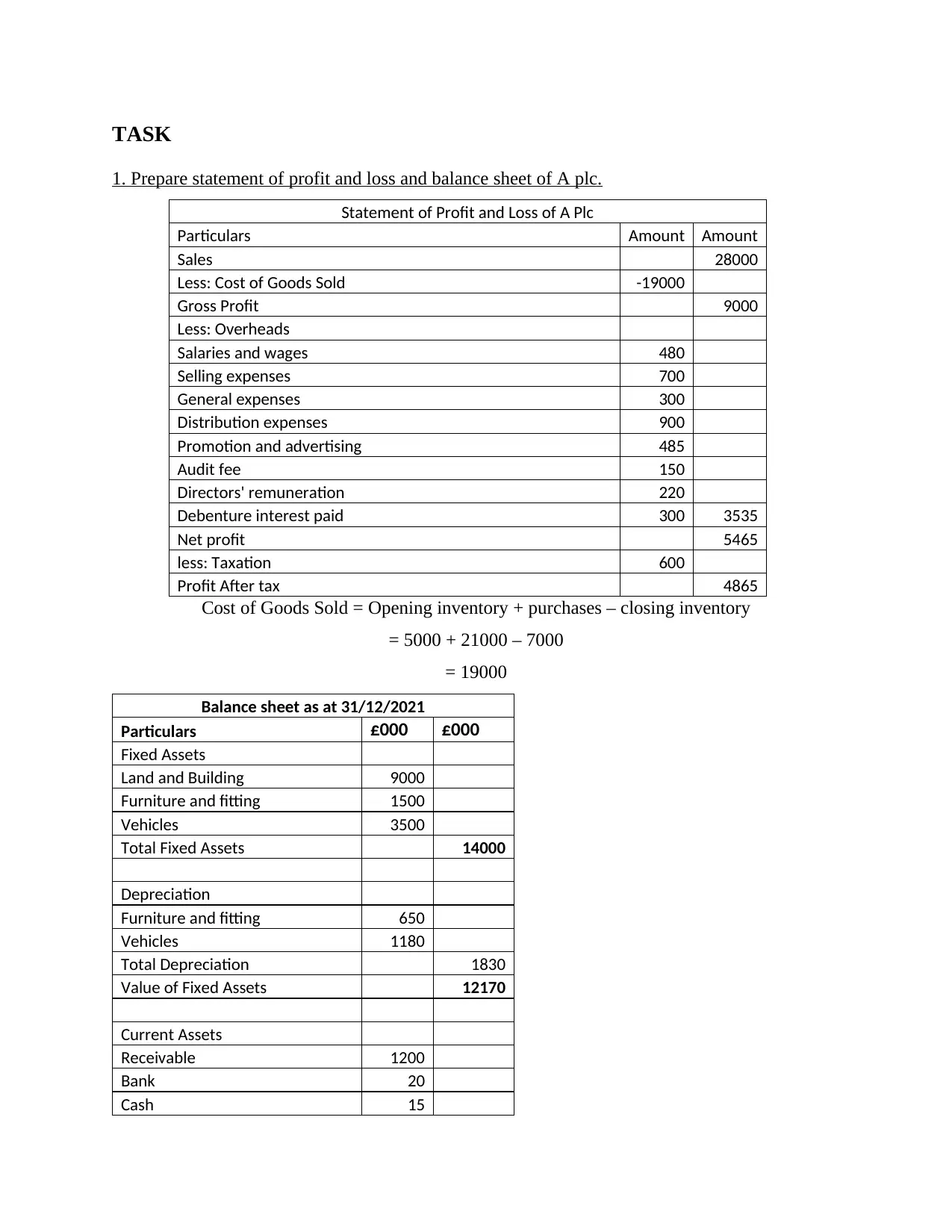

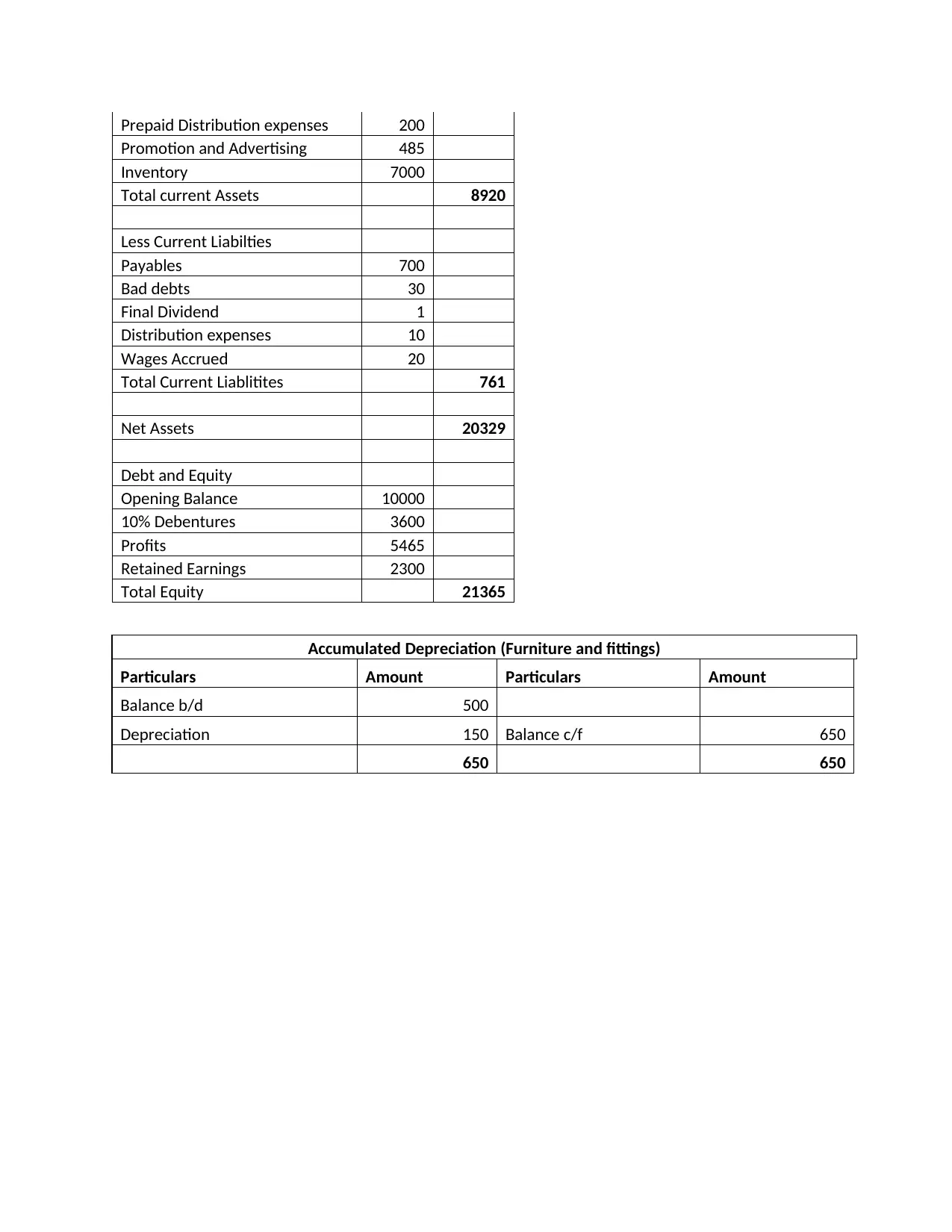

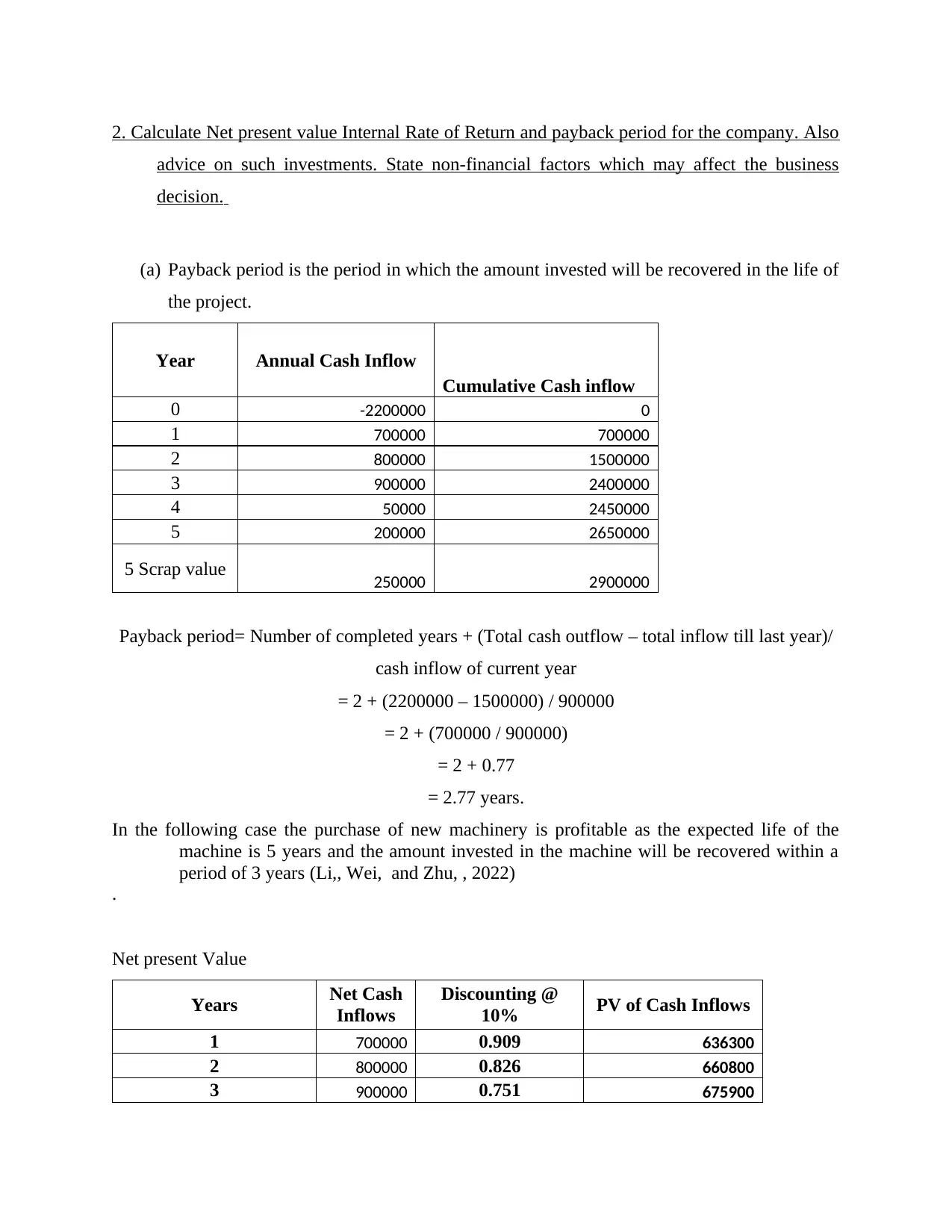

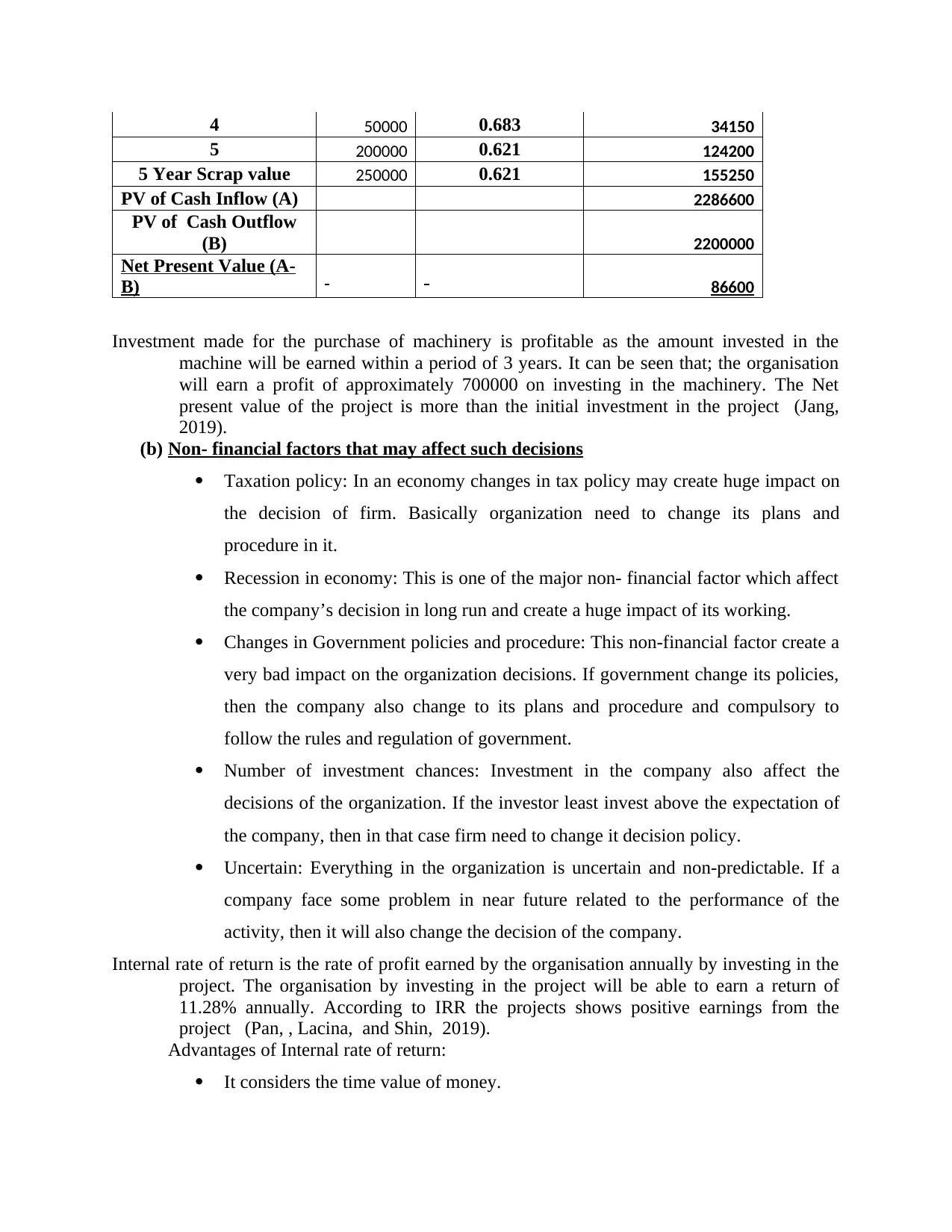

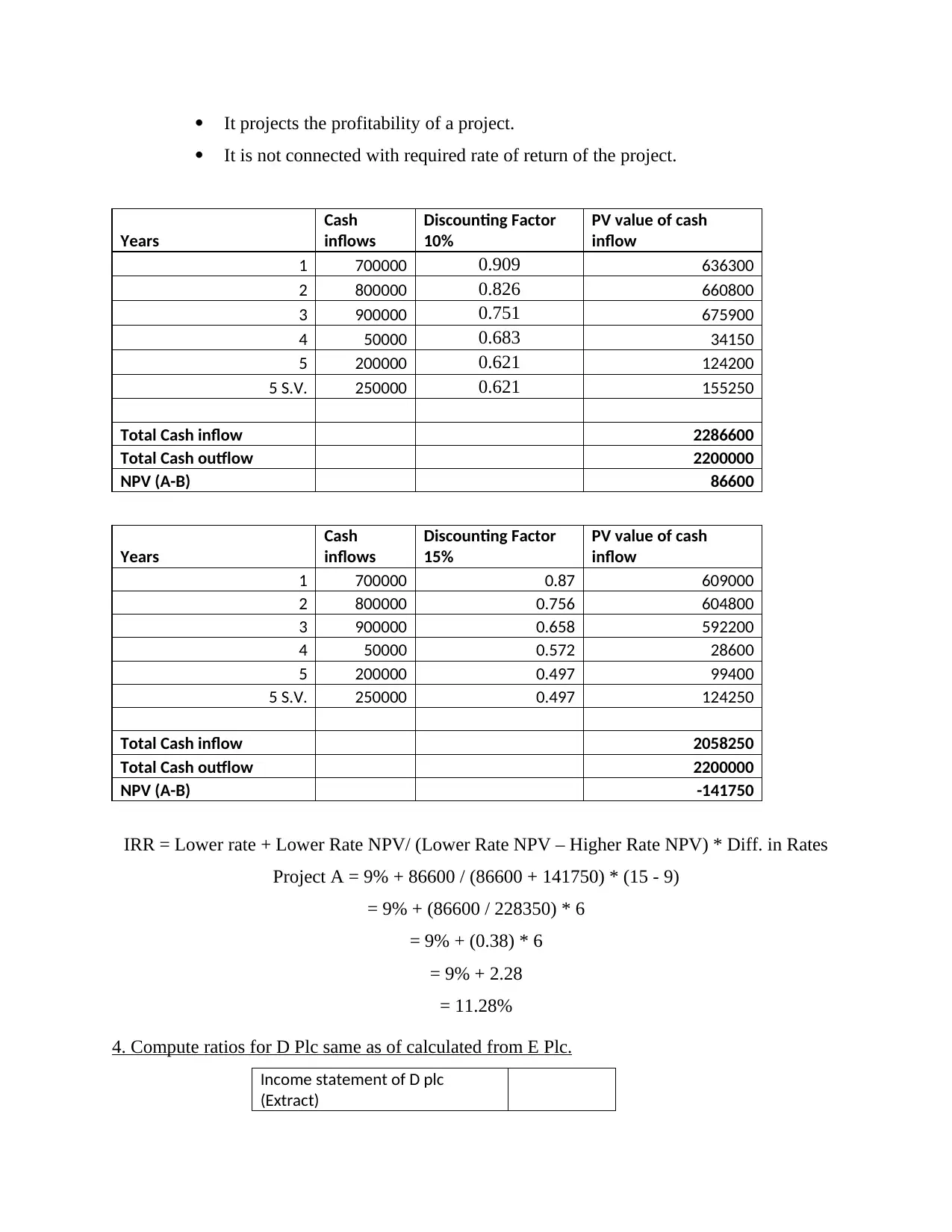

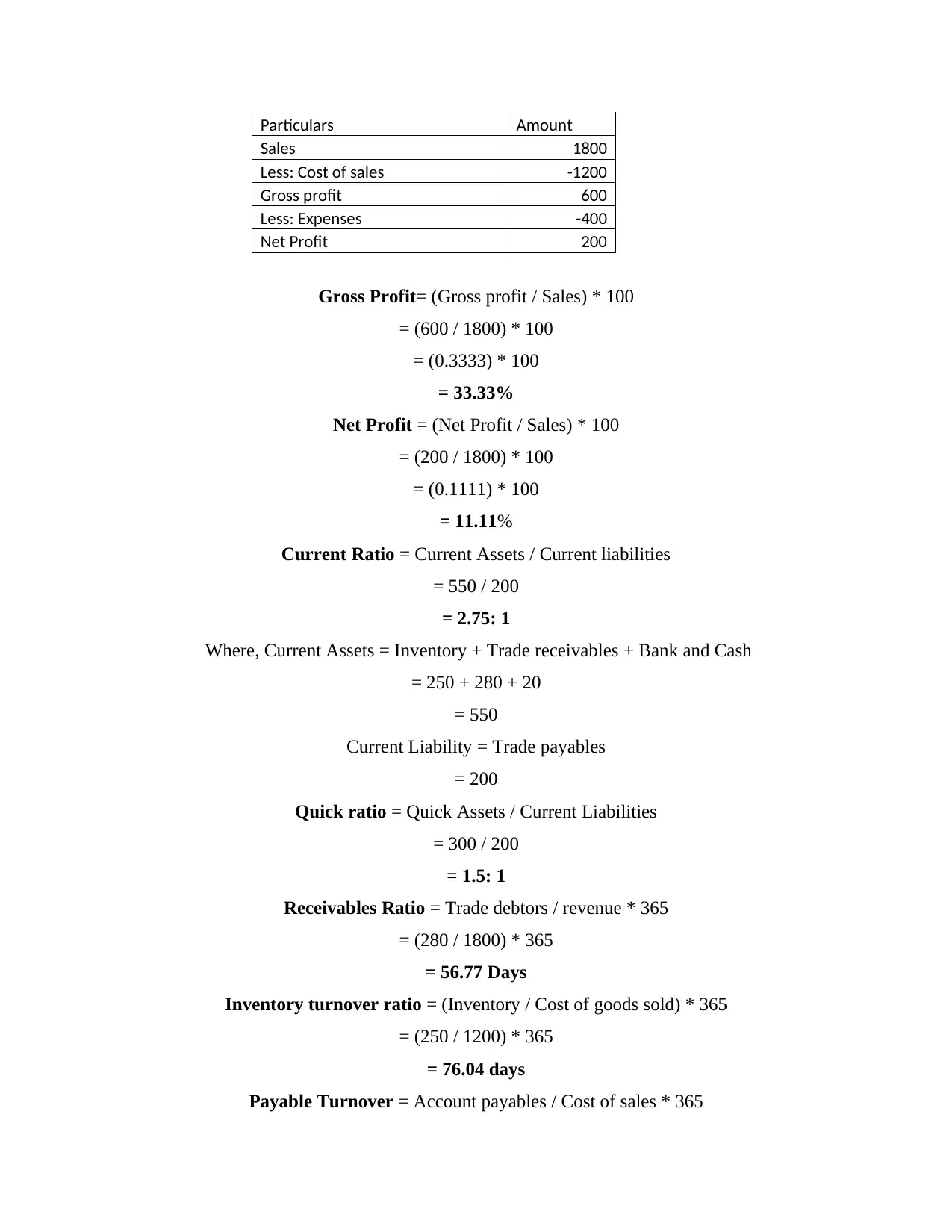

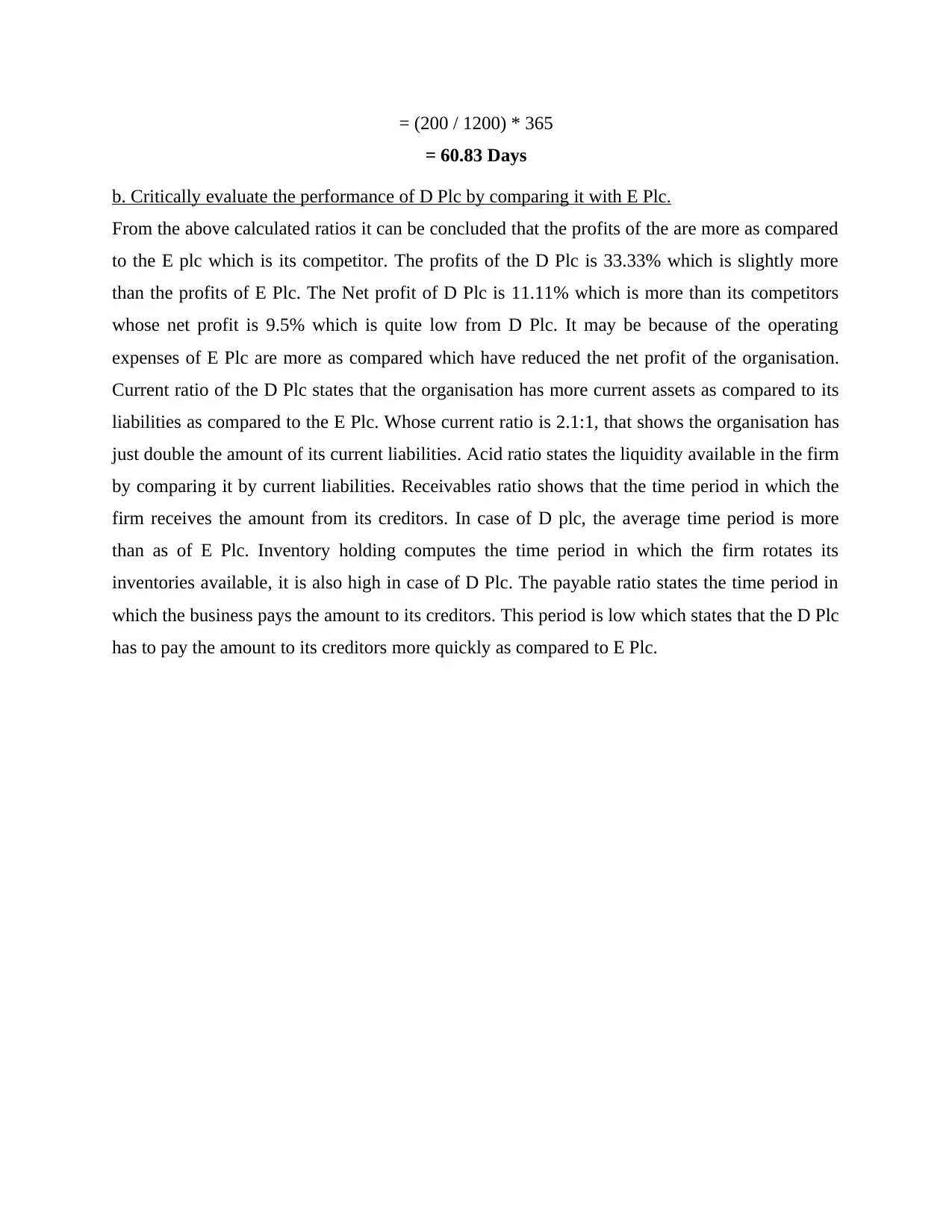

This assignment provides a comprehensive financial analysis of A Plc, including the preparation of an income statement and balance sheet. It calculates key investment metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), and payback period to advise on investment decisions, also considering non-financial factors. Furthermore, the report computes financial ratios for D Plc and critically evaluates its performance by comparing it with E Plc, focusing on profitability, liquidity, and efficiency ratios. The analysis includes detailed calculations for gross profit margin, net profit margin, current ratio, quick ratio, receivables ratio, inventory turnover ratio, and payable turnover ratio, providing a thorough assessment of the companies' financial health and competitive positioning.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.