Ratio Evaluation and Financial Analysis: Tesco Group & Sainsbury Plc

VerifiedAdded on 2022/12/30

|18

|3959

|4

Report

AI Summary

This report presents a comprehensive financial analysis of Tesco and Sainsbury, two major players in the UK retail market. The analysis begins with a detailed ratio evaluation of both companies, covering key financial ratios such as current ratio, quick ratio, gross profit ratio, net profit ratio, P/E ratio, gearing, return on capital employed, inventory turnover, dividend pay-out ratio, and earnings per share. The study compares the financial performance of Tesco and Sainsbury over the period of 2018-2019. The report further explores investment appraisal methods for hypothetical projects and discusses the limitations of these methods in future decision-making. Finally, the report concludes with recommendations for both companies, focusing on strategies to improve financial performance and enhance shareholder value. The analysis highlights that Sainsbury's short-term profitability and monetary sustainability forecast is better than Tesco, but Tesco is more efficient in gross net and overall efficiency score. The report also highlights the importance of considering various ratios to understand financial health and make informed investment decisions.

Portfolio 1 and Portfolio 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

PORTFOLIO 1.................................................................................................................................3

Ratio evaluation of both companies:......................................................................................3

Recommendations:...............................................................................................................12

Restrictions for consuming ratio breakdown for determining firms financial status...........12

PORTFOLIO 2...............................................................................................................................13

Investment appraisal methods for both project A and B:.....................................................13

b. Limits of implementing investment appraisal methods for future decision:....................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

PORTFOLIO 1.................................................................................................................................3

Ratio evaluation of both companies:......................................................................................3

Recommendations:...............................................................................................................12

Restrictions for consuming ratio breakdown for determining firms financial status...........12

PORTFOLIO 2...............................................................................................................................13

Investment appraisal methods for both project A and B:.....................................................13

b. Limits of implementing investment appraisal methods for future decision:....................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

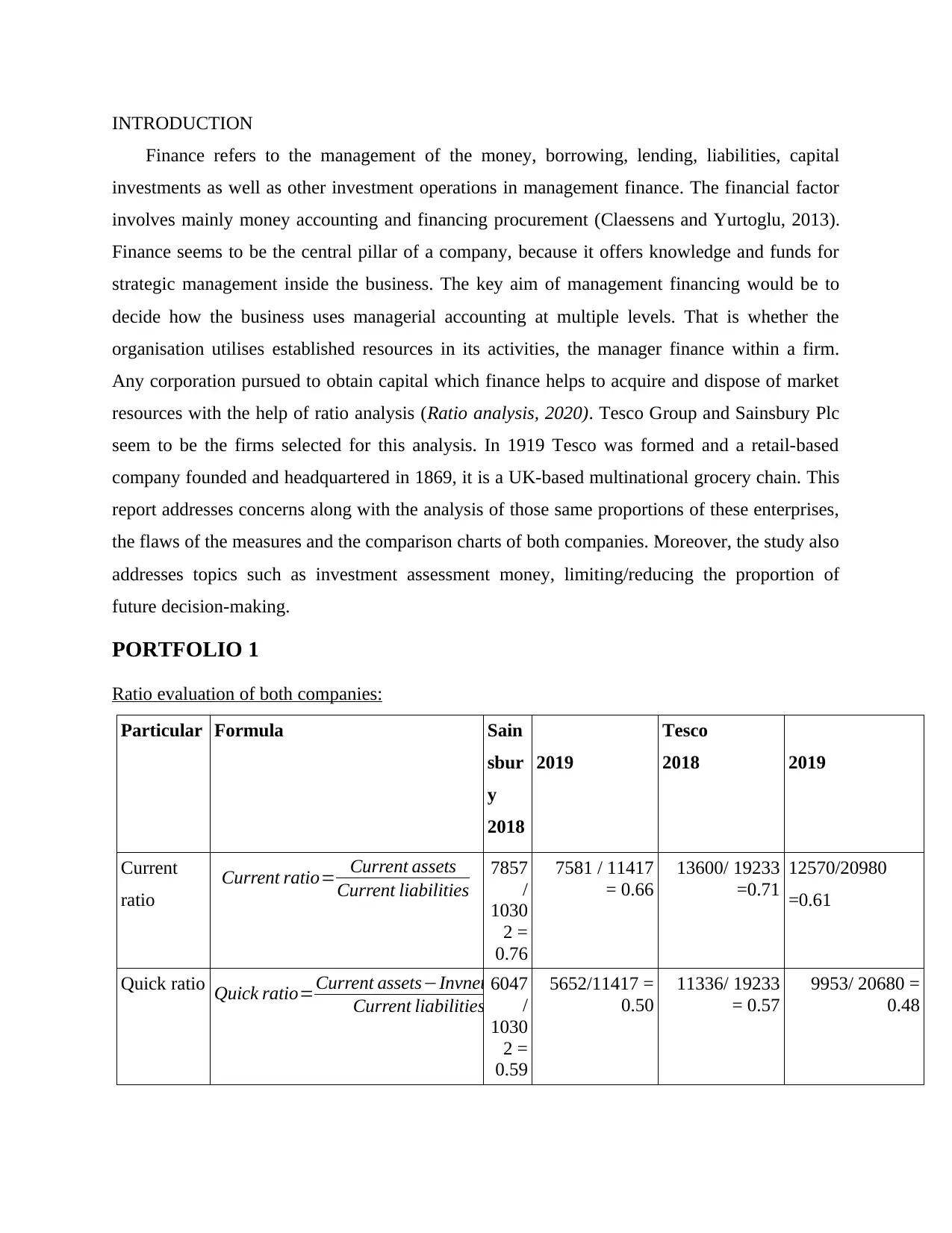

INTRODUCTION

Finance refers to the management of the money, borrowing, lending, liabilities, capital

investments as well as other investment operations in management finance. The financial factor

involves mainly money accounting and financing procurement (Claessens and Yurtoglu, 2013).

Finance seems to be the central pillar of a company, because it offers knowledge and funds for

strategic management inside the business. The key aim of management financing would be to

decide how the business uses managerial accounting at multiple levels. That is whether the

organisation utilises established resources in its activities, the manager finance within a firm.

Any corporation pursued to obtain capital which finance helps to acquire and dispose of market

resources with the help of ratio analysis (Ratio analysis, 2020). Tesco Group and Sainsbury Plc

seem to be the firms selected for this analysis. In 1919 Tesco was formed and a retail-based

company founded and headquartered in 1869, it is a UK-based multinational grocery chain. This

report addresses concerns along with the analysis of those same proportions of these enterprises,

the flaws of the measures and the comparison charts of both companies. Moreover, the study also

addresses topics such as investment assessment money, limiting/reducing the proportion of

future decision-making.

PORTFOLIO 1

Ratio evaluation of both companies:

Particular Formula Sain

sbur

y

2018

2019

Tesco

2018 2019

Current

ratio

Current ratio= Current assets

Current liabilities

7857

/

1030

2 =

0.76

7581 / 11417

= 0.66

13600/ 19233

=0.71

12570/20980

=0.61

Quick ratio Quick ratio=Current assets−Invnetories

Current liabilities

6047

/

1030

2 =

0.59

5652/11417 =

0.50

11336/ 19233

= 0.57

9953/ 20680 =

0.48

Finance refers to the management of the money, borrowing, lending, liabilities, capital

investments as well as other investment operations in management finance. The financial factor

involves mainly money accounting and financing procurement (Claessens and Yurtoglu, 2013).

Finance seems to be the central pillar of a company, because it offers knowledge and funds for

strategic management inside the business. The key aim of management financing would be to

decide how the business uses managerial accounting at multiple levels. That is whether the

organisation utilises established resources in its activities, the manager finance within a firm.

Any corporation pursued to obtain capital which finance helps to acquire and dispose of market

resources with the help of ratio analysis (Ratio analysis, 2020). Tesco Group and Sainsbury Plc

seem to be the firms selected for this analysis. In 1919 Tesco was formed and a retail-based

company founded and headquartered in 1869, it is a UK-based multinational grocery chain. This

report addresses concerns along with the analysis of those same proportions of these enterprises,

the flaws of the measures and the comparison charts of both companies. Moreover, the study also

addresses topics such as investment assessment money, limiting/reducing the proportion of

future decision-making.

PORTFOLIO 1

Ratio evaluation of both companies:

Particular Formula Sain

sbur

y

2018

2019

Tesco

2018 2019

Current

ratio

Current ratio= Current assets

Current liabilities

7857

/

1030

2 =

0.76

7581 / 11417

= 0.66

13600/ 19233

=0.71

12570/20980

=0.61

Quick ratio Quick ratio=Current assets−Invnetories

Current liabilities

6047

/

1030

2 =

0.59

5652/11417 =

0.50

11336/ 19233

= 0.57

9953/ 20680 =

0.48

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit

ratio

Net profit margin= Net profit

Salesrevenue ×100

1210

/

5749

3 =

2.10

1320/ 63911 =

2.07

309/ 28456 =

1.09

219/ 29007 =

0.75

Gross

profit ratio

Gross profit margin= Gross profit

Sales revenue ×100

1882

/284

56=

6.61

2007/ 29007 =

6.92

3352/ 57493 =

5.83

4144/ 63911 =

6.48

Gearing

ratio

Total debt / Capital employed 1459

0/

7411

=

1.97

15085/ 8456 =

1.78

34404/ 10480

= 3.28

34213 / 14834 =

2.31

P/E ratio P

E ratio= Share price

EPS

264.

9/

2.49

=106

.39

229.9 / 1.86 =

123.60

189.55/4.96 =

38.22

255.2/ 6.14 =

41.56

Earning

per share

ratio

Earning per share= Net profit

Number of shares

309/

65 =

4.75

219/ 54 = 4.06 1210/ 244 =

4.96

1320/ 215 = 6.14

Return on

capital

employed

ROCE= Operating profit

Equity+ Non−current liabilities ×100

518/

1169

9 =

4.43

601/ 12097 =

4.97

1566 / 25502 =

6.14

2639 / 28269 =

9.34

Average

stock

turnover

Cost of goods sold/ Average stock 2657

4/

1792

.5 =

14.8

3

27000/ 1869.5

= 14.44

54141/ 2282 =

23.73

59769/ 2440 =

24.50

Dividend

pay-out

ratio

Dividend per share/ Earning per

share

235 /

309

=

76.0

5

247/ 219 =

112.79

82/ 1210 =

6.78

357/ 1320 =

27.05

Evaluation

Capital employed = TA - TCL

Tesco

ratio

Net profit margin= Net profit

Salesrevenue ×100

1210

/

5749

3 =

2.10

1320/ 63911 =

2.07

309/ 28456 =

1.09

219/ 29007 =

0.75

Gross

profit ratio

Gross profit margin= Gross profit

Sales revenue ×100

1882

/284

56=

6.61

2007/ 29007 =

6.92

3352/ 57493 =

5.83

4144/ 63911 =

6.48

Gearing

ratio

Total debt / Capital employed 1459

0/

7411

=

1.97

15085/ 8456 =

1.78

34404/ 10480

= 3.28

34213 / 14834 =

2.31

P/E ratio P

E ratio= Share price

EPS

264.

9/

2.49

=106

.39

229.9 / 1.86 =

123.60

189.55/4.96 =

38.22

255.2/ 6.14 =

41.56

Earning

per share

ratio

Earning per share= Net profit

Number of shares

309/

65 =

4.75

219/ 54 = 4.06 1210/ 244 =

4.96

1320/ 215 = 6.14

Return on

capital

employed

ROCE= Operating profit

Equity+ Non−current liabilities ×100

518/

1169

9 =

4.43

601/ 12097 =

4.97

1566 / 25502 =

6.14

2639 / 28269 =

9.34

Average

stock

turnover

Cost of goods sold/ Average stock 2657

4/

1792

.5 =

14.8

3

27000/ 1869.5

= 14.44

54141/ 2282 =

23.73

59769/ 2440 =

24.50

Dividend

pay-out

ratio

Dividend per share/ Earning per

share

235 /

309

=

76.0

5

247/ 219 =

112.79

82/ 1210 =

6.78

357/ 1320 =

27.05

Evaluation

Capital employed = TA - TCL

Tesco

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 2019

44735 – 19233 = 25502 48949 – 20680 = 28269

Sainsbury

2018 2019

22001 – 10302 = 11699 23514 – 11417 = 12097

Analysis: The study of the proportion will reveal the importance of Tesco as well as Sainsbury's

sustainability situation, financial security and performance (Claessens, 2015). The table above

displays 2018 through 2019 annual ratios which will allow hep to classify the financial condition

of the firms for this time. In this respect, the report is a partial and systematic assessment of the

various ratios:

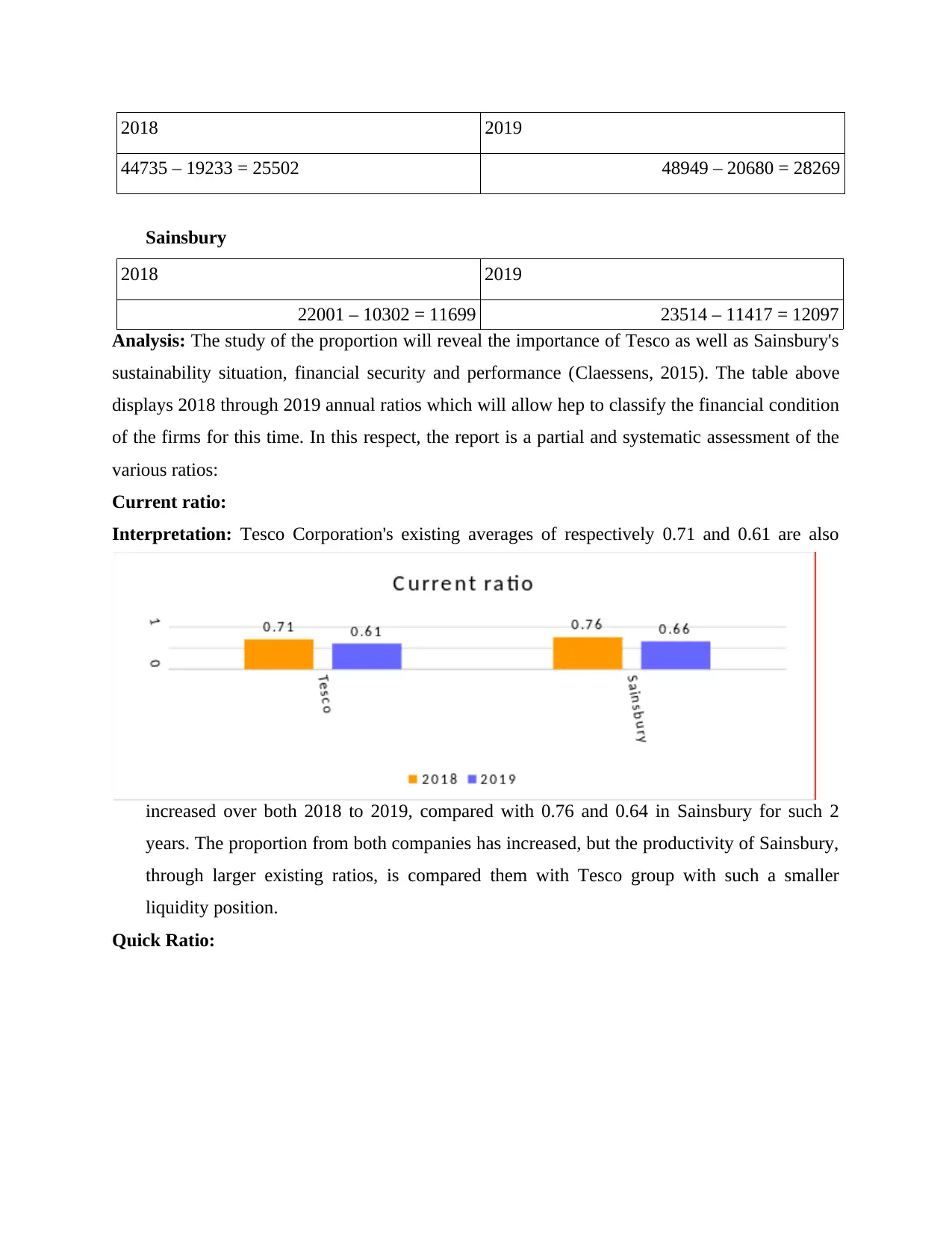

Current ratio:

Interpretation: Tesco Corporation's existing averages of respectively 0.71 and 0.61 are also

increased over both 2018 to 2019, compared with 0.76 and 0.64 in Sainsbury for such 2

years. The proportion from both companies has increased, but the productivity of Sainsbury,

through larger existing ratios, is compared them with Tesco group with such a smaller

liquidity position.

Quick Ratio:

44735 – 19233 = 25502 48949 – 20680 = 28269

Sainsbury

2018 2019

22001 – 10302 = 11699 23514 – 11417 = 12097

Analysis: The study of the proportion will reveal the importance of Tesco as well as Sainsbury's

sustainability situation, financial security and performance (Claessens, 2015). The table above

displays 2018 through 2019 annual ratios which will allow hep to classify the financial condition

of the firms for this time. In this respect, the report is a partial and systematic assessment of the

various ratios:

Current ratio:

Interpretation: Tesco Corporation's existing averages of respectively 0.71 and 0.61 are also

increased over both 2018 to 2019, compared with 0.76 and 0.64 in Sainsbury for such 2

years. The proportion from both companies has increased, but the productivity of Sainsbury,

through larger existing ratios, is compared them with Tesco group with such a smaller

liquidity position.

Quick Ratio:

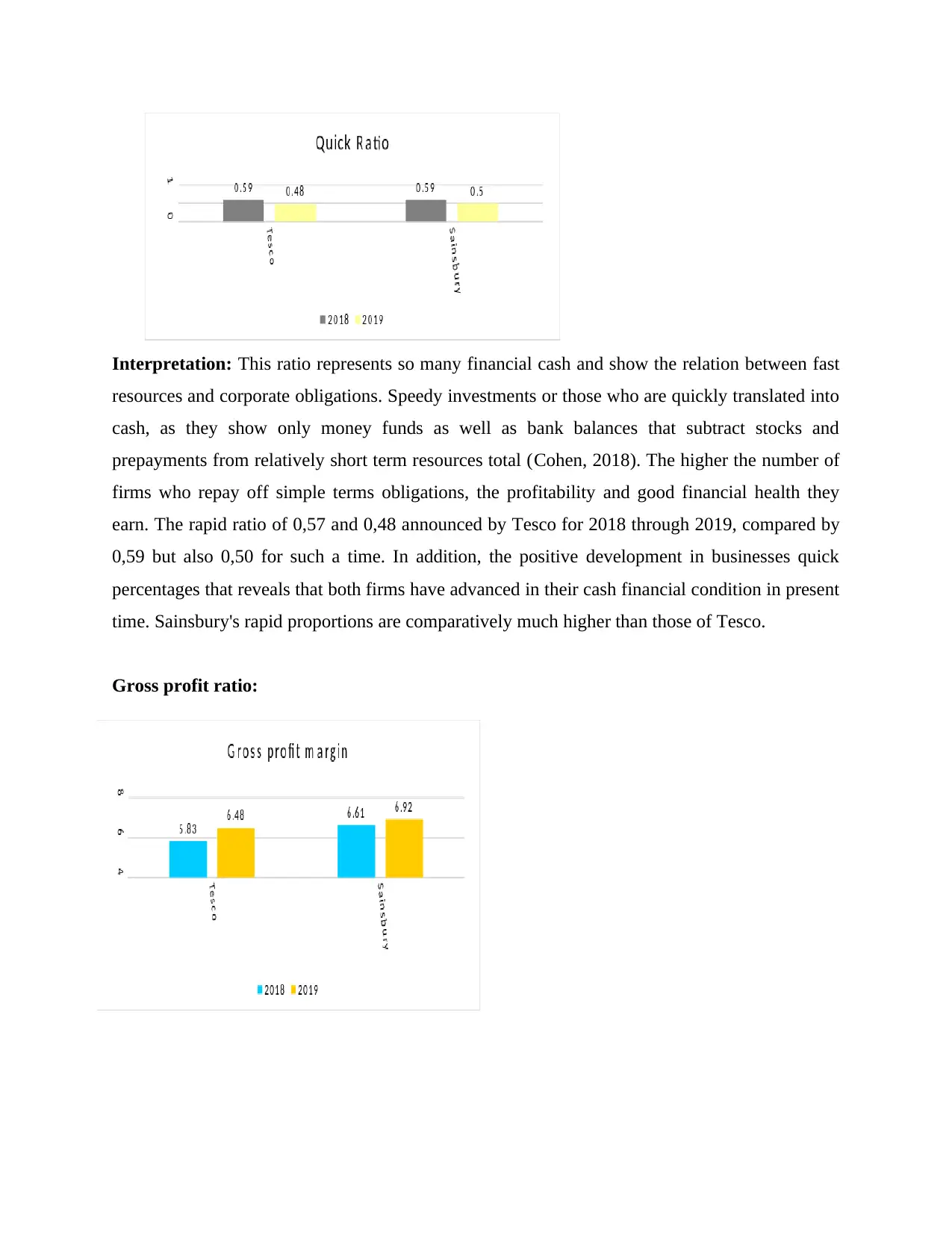

Interpretation: This ratio represents so many financial cash and show the relation between fast

resources and corporate obligations. Speedy investments or those who are quickly translated into

cash, as they show only money funds as well as bank balances that subtract stocks and

prepayments from relatively short term resources total (Cohen, 2018). The higher the number of

firms who repay off simple terms obligations, the profitability and good financial health they

earn. The rapid ratio of 0,57 and 0,48 announced by Tesco for 2018 through 2019, compared by

0,59 but also 0,50 for such a time. In addition, the positive development in businesses quick

percentages that reveals that both firms have advanced in their cash financial condition in present

time. Sainsbury's rapid proportions are comparatively much higher than those of Tesco.

Gross profit ratio:

resources and corporate obligations. Speedy investments or those who are quickly translated into

cash, as they show only money funds as well as bank balances that subtract stocks and

prepayments from relatively short term resources total (Cohen, 2018). The higher the number of

firms who repay off simple terms obligations, the profitability and good financial health they

earn. The rapid ratio of 0,57 and 0,48 announced by Tesco for 2018 through 2019, compared by

0,59 but also 0,50 for such a time. In addition, the positive development in businesses quick

percentages that reveals that both firms have advanced in their cash financial condition in present

time. Sainsbury's rapid proportions are comparatively much higher than those of Tesco.

Gross profit ratio:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: The operating income ratio indicates how effective the organisation is already in

profit production from core business. This indicates the connection between profits and

operating margins. The Tesco Group's overall profitability levels are around 5.82%

throughout 2018 but 6.48% through 2019, whereas the Sainsbury Gross profit figures are

also at 6.61% through 6.92% throughout 2018 as well as 2019. Investigation shows that

Sainsbury is much more efficient than Tesco with a higher gross profit share, by increasing

sales itself from primary jobs that are beneficial for the business growth.

Net Profit/margin ratio:

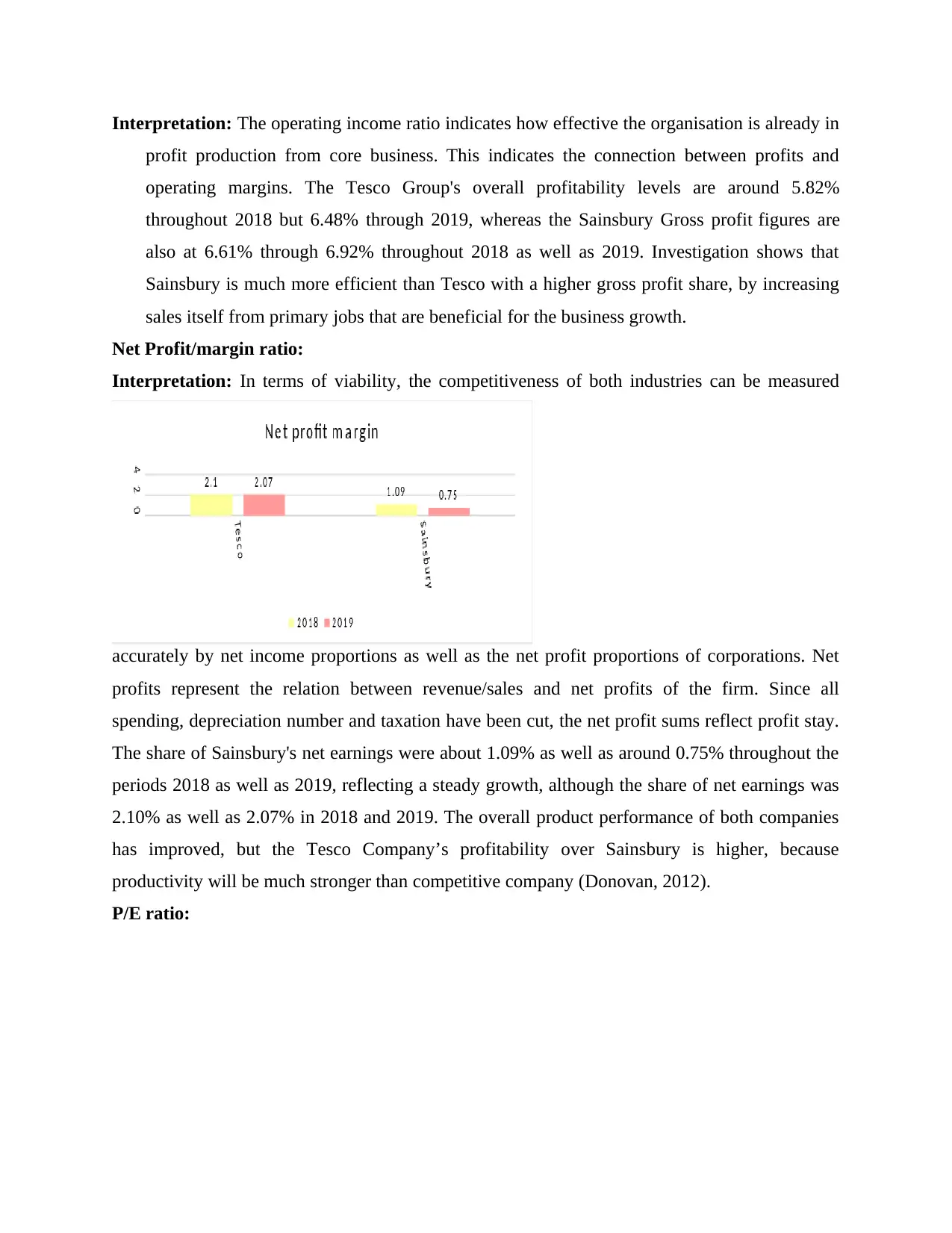

Interpretation: In terms of viability, the competitiveness of both industries can be measured

accurately by net income proportions as well as the net profit proportions of corporations. Net

profits represent the relation between revenue/sales and net profits of the firm. Since all

spending, depreciation number and taxation have been cut, the net profit sums reflect profit stay.

The share of Sainsbury's net earnings were about 1.09% as well as around 0.75% throughout the

periods 2018 as well as 2019, reflecting a steady growth, although the share of net earnings was

2.10% as well as 2.07% in 2018 and 2019. The overall product performance of both companies

has improved, but the Tesco Company’s profitability over Sainsbury is higher, because

productivity will be much stronger than competitive company (Donovan, 2012).

P/E ratio:

profit production from core business. This indicates the connection between profits and

operating margins. The Tesco Group's overall profitability levels are around 5.82%

throughout 2018 but 6.48% through 2019, whereas the Sainsbury Gross profit figures are

also at 6.61% through 6.92% throughout 2018 as well as 2019. Investigation shows that

Sainsbury is much more efficient than Tesco with a higher gross profit share, by increasing

sales itself from primary jobs that are beneficial for the business growth.

Net Profit/margin ratio:

Interpretation: In terms of viability, the competitiveness of both industries can be measured

accurately by net income proportions as well as the net profit proportions of corporations. Net

profits represent the relation between revenue/sales and net profits of the firm. Since all

spending, depreciation number and taxation have been cut, the net profit sums reflect profit stay.

The share of Sainsbury's net earnings were about 1.09% as well as around 0.75% throughout the

periods 2018 as well as 2019, reflecting a steady growth, although the share of net earnings was

2.10% as well as 2.07% in 2018 and 2019. The overall product performance of both companies

has improved, but the Tesco Company’s profitability over Sainsbury is higher, because

productivity will be much stronger than competitive company (Donovan, 2012).

P/E ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

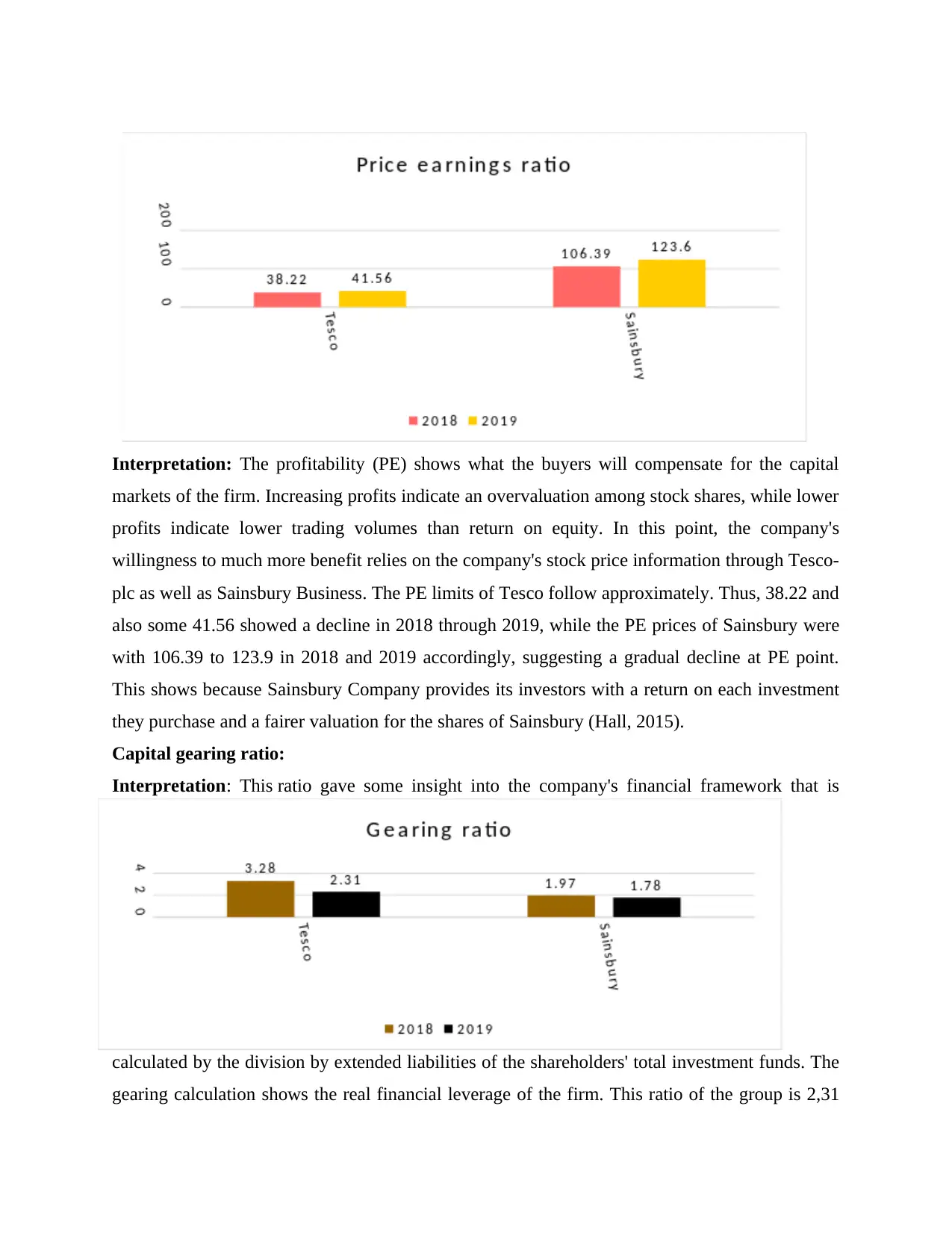

Interpretation: The profitability (PE) shows what the buyers will compensate for the capital

markets of the firm. Increasing profits indicate an overvaluation among stock shares, while lower

profits indicate lower trading volumes than return on equity. In this point, the company's

willingness to much more benefit relies on the company's stock price information through Tesco-

plc as well as Sainsbury Business. The PE limits of Tesco follow approximately. Thus, 38.22 and

also some 41.56 showed a decline in 2018 through 2019, while the PE prices of Sainsbury were

with 106.39 to 123.9 in 2018 and 2019 accordingly, suggesting a gradual decline at PE point.

This shows because Sainsbury Company provides its investors with a return on each investment

they purchase and a fairer valuation for the shares of Sainsbury (Hall, 2015).

Capital gearing ratio:

Interpretation: This ratio gave some insight into the company's financial framework that is

calculated by the division by extended liabilities of the shareholders' total investment funds. The

gearing calculation shows the real financial leverage of the firm. This ratio of the group is 2,31

markets of the firm. Increasing profits indicate an overvaluation among stock shares, while lower

profits indicate lower trading volumes than return on equity. In this point, the company's

willingness to much more benefit relies on the company's stock price information through Tesco-

plc as well as Sainsbury Business. The PE limits of Tesco follow approximately. Thus, 38.22 and

also some 41.56 showed a decline in 2018 through 2019, while the PE prices of Sainsbury were

with 106.39 to 123.9 in 2018 and 2019 accordingly, suggesting a gradual decline at PE point.

This shows because Sainsbury Company provides its investors with a return on each investment

they purchase and a fairer valuation for the shares of Sainsbury (Hall, 2015).

Capital gearing ratio:

Interpretation: This ratio gave some insight into the company's financial framework that is

calculated by the division by extended liabilities of the shareholders' total investment funds. The

gearing calculation shows the real financial leverage of the firm. This ratio of the group is 2,31

throughout the 2019 year as well 3,28 mostly in 2018 year, while the rotational speeds of

Sainsbury were currently 1,97% and 1,78% simultaneously (2018 and 2019). Tesco seems to

have a greater share of the mortgage / loan load as compared with the Sainsbury due to greater

brand value in marketplace. As a consideration, the liquidity efficiency with Sainsbury appears

stronger than that of Tesco.

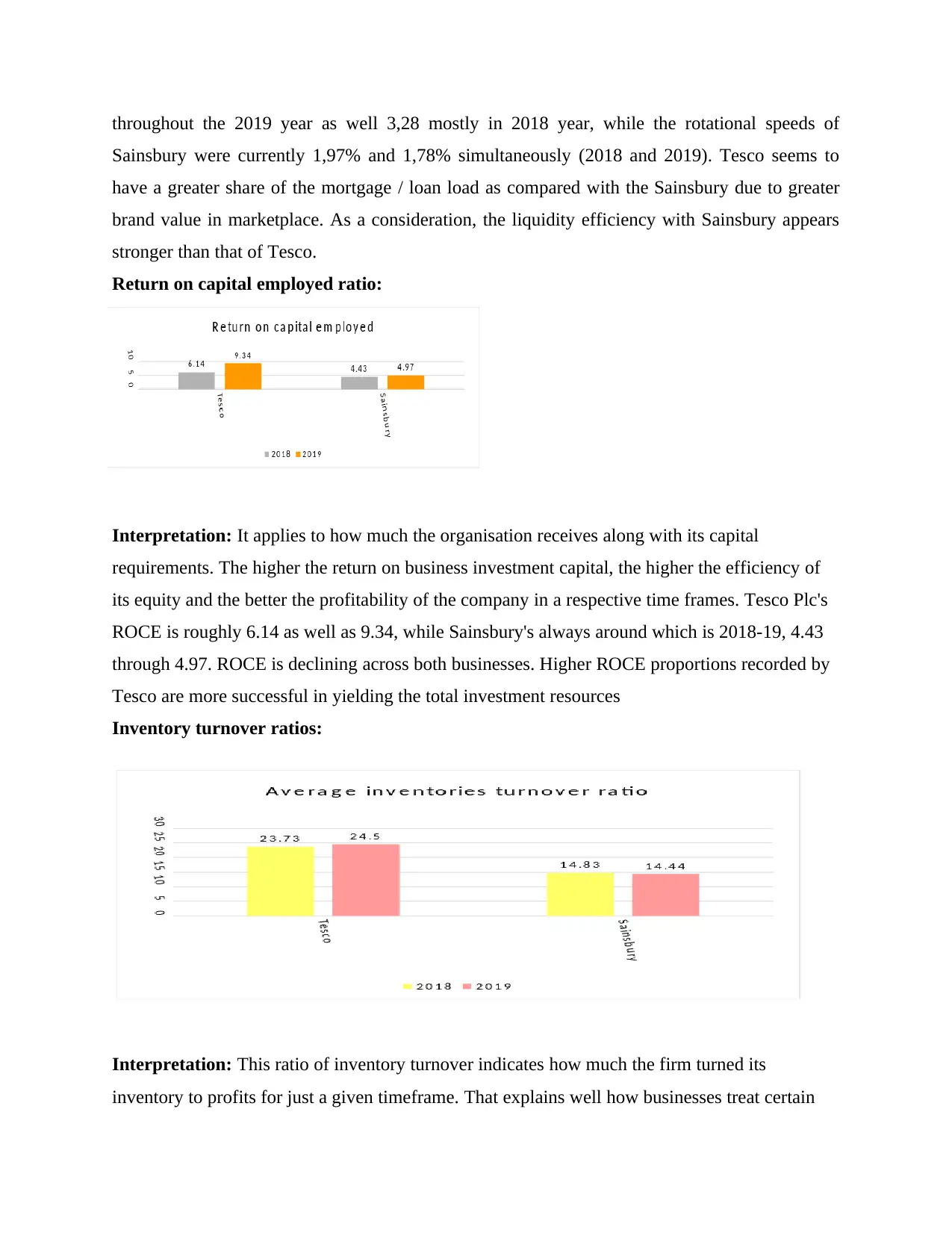

Return on capital employed ratio:

Interpretation: It applies to how much the organisation receives along with its capital

requirements. The higher the return on business investment capital, the higher the efficiency of

its equity and the better the profitability of the company in a respective time frames. Tesco Plc's

ROCE is roughly 6.14 as well as 9.34, while Sainsbury's always around which is 2018-19, 4.43

through 4.97. ROCE is declining across both businesses. Higher ROCE proportions recorded by

Tesco are more successful in yielding the total investment resources

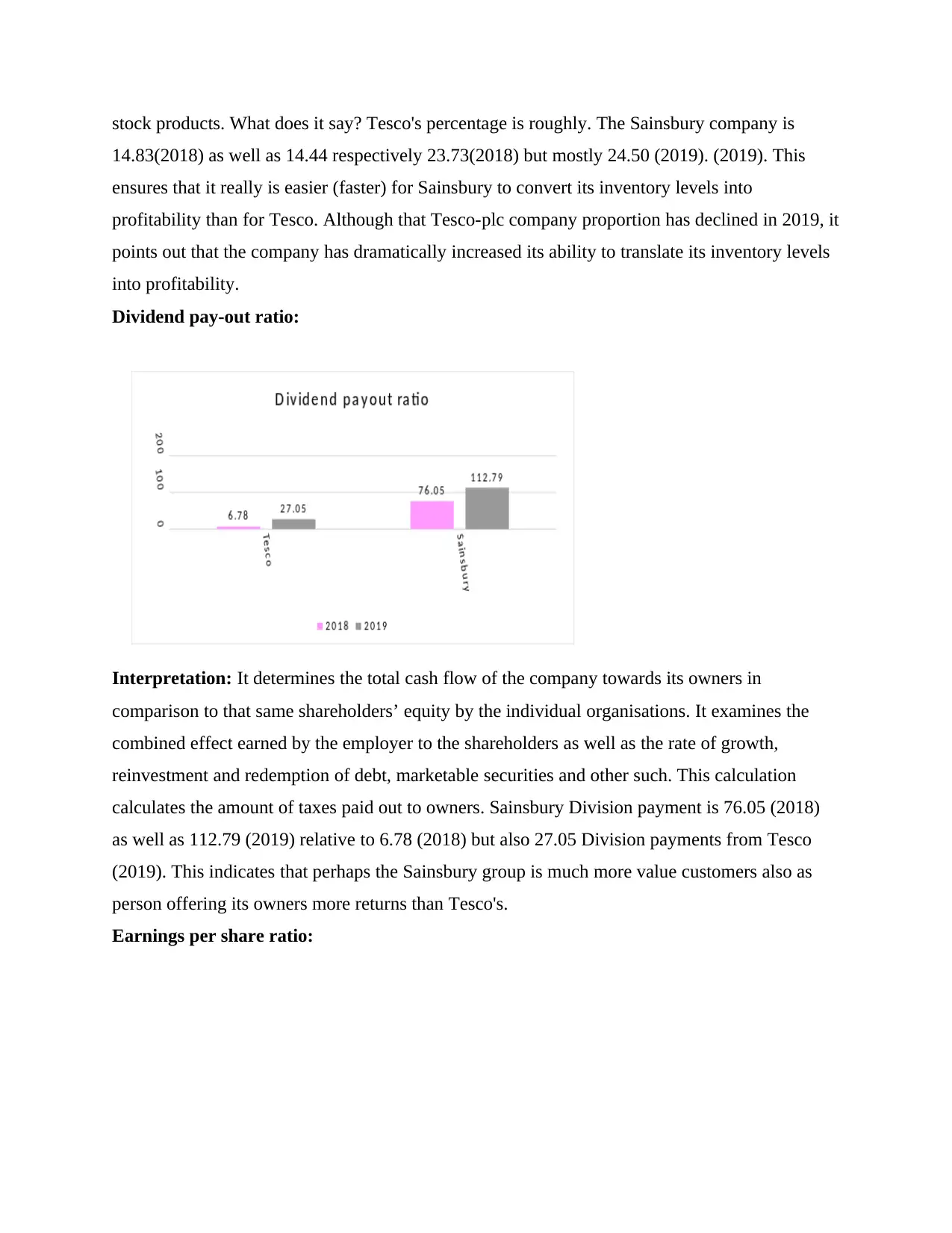

Inventory turnover ratios:

Interpretation: This ratio of inventory turnover indicates how much the firm turned its

inventory to profits for just a given timeframe. That explains well how businesses treat certain

Sainsbury were currently 1,97% and 1,78% simultaneously (2018 and 2019). Tesco seems to

have a greater share of the mortgage / loan load as compared with the Sainsbury due to greater

brand value in marketplace. As a consideration, the liquidity efficiency with Sainsbury appears

stronger than that of Tesco.

Return on capital employed ratio:

Interpretation: It applies to how much the organisation receives along with its capital

requirements. The higher the return on business investment capital, the higher the efficiency of

its equity and the better the profitability of the company in a respective time frames. Tesco Plc's

ROCE is roughly 6.14 as well as 9.34, while Sainsbury's always around which is 2018-19, 4.43

through 4.97. ROCE is declining across both businesses. Higher ROCE proportions recorded by

Tesco are more successful in yielding the total investment resources

Inventory turnover ratios:

Interpretation: This ratio of inventory turnover indicates how much the firm turned its

inventory to profits for just a given timeframe. That explains well how businesses treat certain

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

stock products. What does it say? Tesco's percentage is roughly. The Sainsbury company is

14.83(2018) as well as 14.44 respectively 23.73(2018) but mostly 24.50 (2019). (2019). This

ensures that it really is easier (faster) for Sainsbury to convert its inventory levels into

profitability than for Tesco. Although that Tesco-plc company proportion has declined in 2019, it

points out that the company has dramatically increased its ability to translate its inventory levels

into profitability.

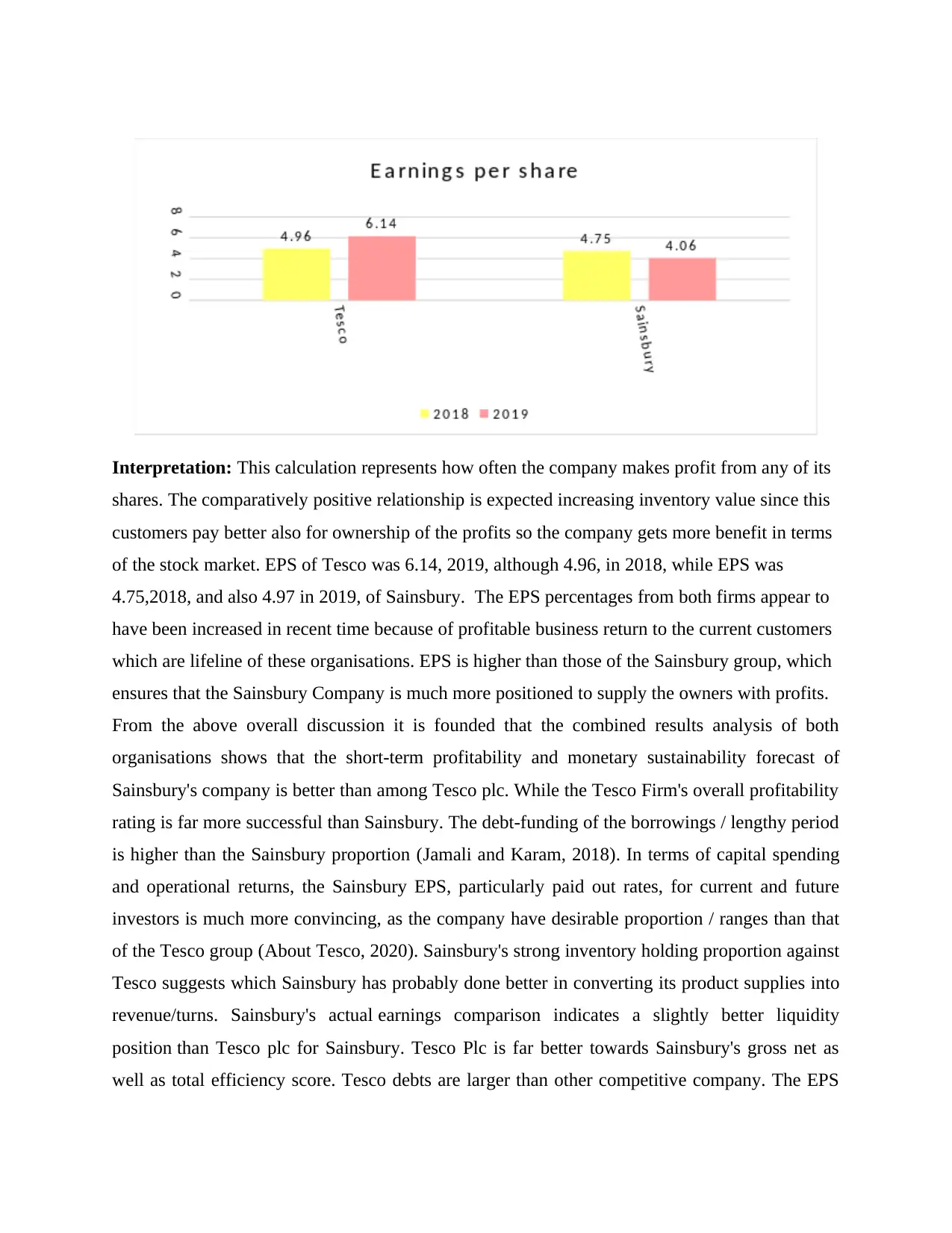

Dividend pay-out ratio:

Interpretation: It determines the total cash flow of the company towards its owners in

comparison to that same shareholders’ equity by the individual organisations. It examines the

combined effect earned by the employer to the shareholders as well as the rate of growth,

reinvestment and redemption of debt, marketable securities and other such. This calculation

calculates the amount of taxes paid out to owners. Sainsbury Division payment is 76.05 (2018)

as well as 112.79 (2019) relative to 6.78 (2018) but also 27.05 Division payments from Tesco

(2019). This indicates that perhaps the Sainsbury group is much more value customers also as

person offering its owners more returns than Tesco's.

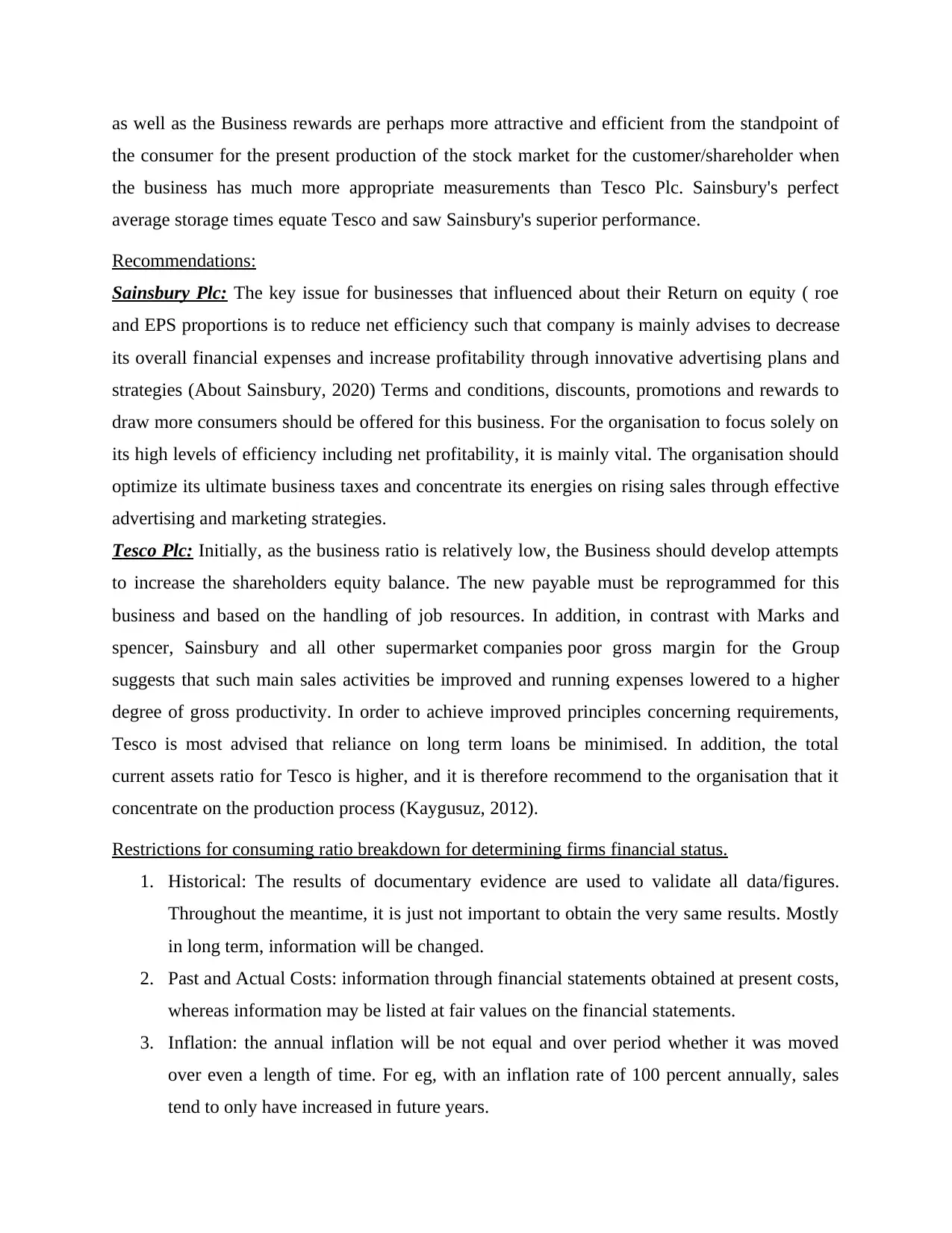

Earnings per share ratio:

14.83(2018) as well as 14.44 respectively 23.73(2018) but mostly 24.50 (2019). (2019). This

ensures that it really is easier (faster) for Sainsbury to convert its inventory levels into

profitability than for Tesco. Although that Tesco-plc company proportion has declined in 2019, it

points out that the company has dramatically increased its ability to translate its inventory levels

into profitability.

Dividend pay-out ratio:

Interpretation: It determines the total cash flow of the company towards its owners in

comparison to that same shareholders’ equity by the individual organisations. It examines the

combined effect earned by the employer to the shareholders as well as the rate of growth,

reinvestment and redemption of debt, marketable securities and other such. This calculation

calculates the amount of taxes paid out to owners. Sainsbury Division payment is 76.05 (2018)

as well as 112.79 (2019) relative to 6.78 (2018) but also 27.05 Division payments from Tesco

(2019). This indicates that perhaps the Sainsbury group is much more value customers also as

person offering its owners more returns than Tesco's.

Earnings per share ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: This calculation represents how often the company makes profit from any of its

shares. The comparatively positive relationship is expected increasing inventory value since this

customers pay better also for ownership of the profits so the company gets more benefit in terms

of the stock market. EPS of Tesco was 6.14, 2019, although 4.96, in 2018, while EPS was

4.75,2018, and also 4.97 in 2019, of Sainsbury. The EPS percentages from both firms appear to

have been increased in recent time because of profitable business return to the current customers

which are lifeline of these organisations. EPS is higher than those of the Sainsbury group, which

ensures that the Sainsbury Company is much more positioned to supply the owners with profits.

From the above overall discussion it is founded that the combined results analysis of both

organisations shows that the short-term profitability and monetary sustainability forecast of

Sainsbury's company is better than among Tesco plc. While the Tesco Firm's overall profitability

rating is far more successful than Sainsbury. The debt-funding of the borrowings / lengthy period

is higher than the Sainsbury proportion (Jamali and Karam, 2018). In terms of capital spending

and operational returns, the Sainsbury EPS, particularly paid out rates, for current and future

investors is much more convincing, as the company have desirable proportion / ranges than that

of the Tesco group (About Tesco, 2020). Sainsbury's strong inventory holding proportion against

Tesco suggests which Sainsbury has probably done better in converting its product supplies into

revenue/turns. Sainsbury's actual earnings comparison indicates a slightly better liquidity

position than Tesco plc for Sainsbury. Tesco Plc is far better towards Sainsbury's gross net as

well as total efficiency score. Tesco debts are larger than other competitive company. The EPS

shares. The comparatively positive relationship is expected increasing inventory value since this

customers pay better also for ownership of the profits so the company gets more benefit in terms

of the stock market. EPS of Tesco was 6.14, 2019, although 4.96, in 2018, while EPS was

4.75,2018, and also 4.97 in 2019, of Sainsbury. The EPS percentages from both firms appear to

have been increased in recent time because of profitable business return to the current customers

which are lifeline of these organisations. EPS is higher than those of the Sainsbury group, which

ensures that the Sainsbury Company is much more positioned to supply the owners with profits.

From the above overall discussion it is founded that the combined results analysis of both

organisations shows that the short-term profitability and monetary sustainability forecast of

Sainsbury's company is better than among Tesco plc. While the Tesco Firm's overall profitability

rating is far more successful than Sainsbury. The debt-funding of the borrowings / lengthy period

is higher than the Sainsbury proportion (Jamali and Karam, 2018). In terms of capital spending

and operational returns, the Sainsbury EPS, particularly paid out rates, for current and future

investors is much more convincing, as the company have desirable proportion / ranges than that

of the Tesco group (About Tesco, 2020). Sainsbury's strong inventory holding proportion against

Tesco suggests which Sainsbury has probably done better in converting its product supplies into

revenue/turns. Sainsbury's actual earnings comparison indicates a slightly better liquidity

position than Tesco plc for Sainsbury. Tesco Plc is far better towards Sainsbury's gross net as

well as total efficiency score. Tesco debts are larger than other competitive company. The EPS

as well as the Business rewards are perhaps more attractive and efficient from the standpoint of

the consumer for the present production of the stock market for the customer/shareholder when

the business has much more appropriate measurements than Tesco Plc. Sainsbury's perfect

average storage times equate Tesco and saw Sainsbury's superior performance.

Recommendations:

Sainsbury Plc: The key issue for businesses that influenced about their Return on equity ( roe

and EPS proportions is to reduce net efficiency such that company is mainly advises to decrease

its overall financial expenses and increase profitability through innovative advertising plans and

strategies (About Sainsbury, 2020) Terms and conditions, discounts, promotions and rewards to

draw more consumers should be offered for this business. For the organisation to focus solely on

its high levels of efficiency including net profitability, it is mainly vital. The organisation should

optimize its ultimate business taxes and concentrate its energies on rising sales through effective

advertising and marketing strategies.

Tesco Plc: Initially, as the business ratio is relatively low, the Business should develop attempts

to increase the shareholders equity balance. The new payable must be reprogrammed for this

business and based on the handling of job resources. In addition, in contrast with Marks and

spencer, Sainsbury and all other supermarket companies poor gross margin for the Group

suggests that such main sales activities be improved and running expenses lowered to a higher

degree of gross productivity. In order to achieve improved principles concerning requirements,

Tesco is most advised that reliance on long term loans be minimised. In addition, the total

current assets ratio for Tesco is higher, and it is therefore recommend to the organisation that it

concentrate on the production process (Kaygusuz, 2012).

Restrictions for consuming ratio breakdown for determining firms financial status.

1. Historical: The results of documentary evidence are used to validate all data/figures.

Throughout the meantime, it is just not important to obtain the very same results. Mostly

in long term, information will be changed.

2. Past and Actual Costs: information through financial statements obtained at present costs,

whereas information may be listed at fair values on the financial statements.

3. Inflation: the annual inflation will be not equal and over period whether it was moved

over even a length of time. For eg, with an inflation rate of 100 percent annually, sales

tend to only have increased in future years.

the consumer for the present production of the stock market for the customer/shareholder when

the business has much more appropriate measurements than Tesco Plc. Sainsbury's perfect

average storage times equate Tesco and saw Sainsbury's superior performance.

Recommendations:

Sainsbury Plc: The key issue for businesses that influenced about their Return on equity ( roe

and EPS proportions is to reduce net efficiency such that company is mainly advises to decrease

its overall financial expenses and increase profitability through innovative advertising plans and

strategies (About Sainsbury, 2020) Terms and conditions, discounts, promotions and rewards to

draw more consumers should be offered for this business. For the organisation to focus solely on

its high levels of efficiency including net profitability, it is mainly vital. The organisation should

optimize its ultimate business taxes and concentrate its energies on rising sales through effective

advertising and marketing strategies.

Tesco Plc: Initially, as the business ratio is relatively low, the Business should develop attempts

to increase the shareholders equity balance. The new payable must be reprogrammed for this

business and based on the handling of job resources. In addition, in contrast with Marks and

spencer, Sainsbury and all other supermarket companies poor gross margin for the Group

suggests that such main sales activities be improved and running expenses lowered to a higher

degree of gross productivity. In order to achieve improved principles concerning requirements,

Tesco is most advised that reliance on long term loans be minimised. In addition, the total

current assets ratio for Tesco is higher, and it is therefore recommend to the organisation that it

concentrate on the production process (Kaygusuz, 2012).

Restrictions for consuming ratio breakdown for determining firms financial status.

1. Historical: The results of documentary evidence are used to validate all data/figures.

Throughout the meantime, it is just not important to obtain the very same results. Mostly

in long term, information will be changed.

2. Past and Actual Costs: information through financial statements obtained at present costs,

whereas information may be listed at fair values on the financial statements.

3. Inflation: the annual inflation will be not equal and over period whether it was moved

over even a length of time. For eg, with an inflation rate of 100 percent annually, sales

tend to only have increased in future years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.