Managerial Finance: Ratio Analysis and Investment Appraisal Report

VerifiedAdded on 2022/12/29

|18

|4158

|1

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco plc and Sainsbury plc, two leading UK retail chains. The analysis begins with an overview of both companies, followed by a detailed examination of their financial performance using ratio analysis, including current ratio, quick ratio, gross profit margin, net profit margin, P/E ratio, gearing ratio, return on capital employed, inventory turnover, dividend payout ratio, and earnings per share. The report interprets these ratios, comparing the performance of both companies and offering recommendations. Furthermore, the report delves into investment appraisal techniques, evaluating project A and project B, and discusses the limitations of these techniques for long-term decision-making. The conclusion summarizes the key findings, highlighting the strengths and weaknesses of each company's financial position and investment strategies.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1................................................................................................................................3

Ratio analysis:..............................................................................................................................4

Interpretation:..............................................................................................................................5

Recommendations:....................................................................................................................11

Limitations for using ratio analysis for knowing firms financial position:...............................11

PORTFOLIO 2..............................................................................................................................12

Investment appraisal techniques for project A and project B:...................................................12

Limitations of using investment appraisal techniques for long term decision-making:............14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

PORTFOLIO 1................................................................................................................................3

Ratio analysis:..............................................................................................................................4

Interpretation:..............................................................................................................................5

Recommendations:....................................................................................................................11

Limitations for using ratio analysis for knowing firms financial position:...............................11

PORTFOLIO 2..............................................................................................................................12

Investment appraisal techniques for project A and project B:...................................................12

Limitations of using investment appraisal techniques for long term decision-making:............14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Managing Finance is primarily a combination of finance/economics and accounting.

Initially, finance officers utilize accounting reports, cashflows reports and other key reports to

plan and allocate the fiscal resources of the firm. In addition, managers use economic principles

as a basis for strategic decision-makings which meets the needs of the business. In simplistic

terms, finances are an aspect of economics driven by financial skills. Because finance and its

related activities add values to the whole enterprise, finance managers are crucial personnel for

the most of organisations (Abor, 2016). Financial managers analyse the sustainability of the

business, comprehend the financial effects, trends, and consider how to manage the company's

assets for long-term success of entity. The study includes the financial review of UK's top retail

chains, notably Tesco plc and Sainsbury, as well as gives suggestions to enterprises. It also

covers practical case study on the investment appraisal strategies and the main shortcomings of

these techniques.

PORTFOLIO 1

Overview of Companies:

Tesco Plc: It's a grocery store chain company. The Organization is active in Online retail and

other operations like Retail Banking business, Insurance Services business. Company also

operates its business throughout United Kingdom, Republic of Ireland, areas of Centre Europe,

which also comprise Czech Republic, Poland, Slovakia, Hungary. Company also operates as

Tesco Banks, which carry financial services, insurance and banking operations in UK.

Corporation's sector consists of United Kingdom, Czech State, United Kingdom. The Company

delivers a series of personal banking product lines and resources, including lending. The

Company delivers a range of personal finance product categories and programmes, comprising

credit cards, credits receivables, personal loans and advances.

Sainsbury Plc: Sainsbury is the top-leading retailer of products across the Uk. The Company

functions in following areas: Retail segment, Financial Activities and Investing. The supermarket

section is active in the operation of grocery stores and grocery stores. The segment on fiscal

product encompasses the operational processes of Sainsbury's Banks. The Commercial property

Investments segment comprises of mutual ventures between the Company and British Property

Corporation, namely Land Securities Company. Sainsbury Bank aims at providing a wide array

Managing Finance is primarily a combination of finance/economics and accounting.

Initially, finance officers utilize accounting reports, cashflows reports and other key reports to

plan and allocate the fiscal resources of the firm. In addition, managers use economic principles

as a basis for strategic decision-makings which meets the needs of the business. In simplistic

terms, finances are an aspect of economics driven by financial skills. Because finance and its

related activities add values to the whole enterprise, finance managers are crucial personnel for

the most of organisations (Abor, 2016). Financial managers analyse the sustainability of the

business, comprehend the financial effects, trends, and consider how to manage the company's

assets for long-term success of entity. The study includes the financial review of UK's top retail

chains, notably Tesco plc and Sainsbury, as well as gives suggestions to enterprises. It also

covers practical case study on the investment appraisal strategies and the main shortcomings of

these techniques.

PORTFOLIO 1

Overview of Companies:

Tesco Plc: It's a grocery store chain company. The Organization is active in Online retail and

other operations like Retail Banking business, Insurance Services business. Company also

operates its business throughout United Kingdom, Republic of Ireland, areas of Centre Europe,

which also comprise Czech Republic, Poland, Slovakia, Hungary. Company also operates as

Tesco Banks, which carry financial services, insurance and banking operations in UK.

Corporation's sector consists of United Kingdom, Czech State, United Kingdom. The Company

delivers a series of personal banking product lines and resources, including lending. The

Company delivers a range of personal finance product categories and programmes, comprising

credit cards, credits receivables, personal loans and advances.

Sainsbury Plc: Sainsbury is the top-leading retailer of products across the Uk. The Company

functions in following areas: Retail segment, Financial Activities and Investing. The supermarket

section is active in the operation of grocery stores and grocery stores. The segment on fiscal

product encompasses the operational processes of Sainsbury's Banks. The Commercial property

Investments segment comprises of mutual ventures between the Company and British Property

Corporation, namely Land Securities Company. Sainsbury Bank aims at providing a wide array

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of services, such as savings, secured loans, savings and mortgage debt. Sainsbury Bank gives

automobile, home, animal insurance, and health insurance plans. Sainsbury's Power delivers

gasoline and electricity, and also a number of power generators. Sainsbury's

Entertainments offers films and shows, tracks, books, sports and other entertainment media.

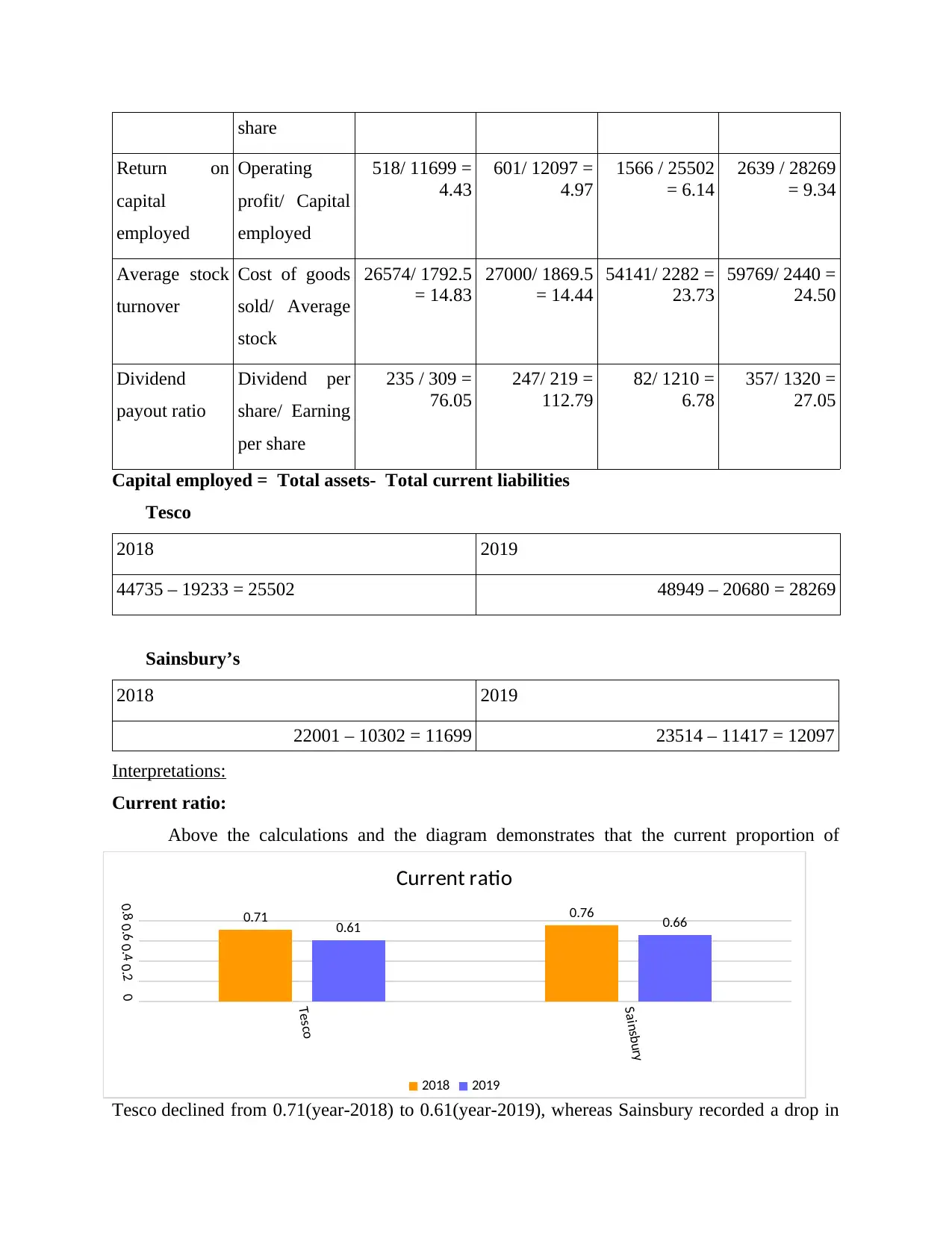

Ratio analysis:

Particular Formula Sainsbury

2018 2019

Tesco

2018 2019

Current ratio Current

assets /

Current

liabilities

7857/ 10302 =

0.76

7581 / 11417

= 0.66

13600/ 19233

=0.71

12570/20980

=0.61

Quick ratio Quick assets/

Current

liabilities

6047/ 10302 =

0.59

5652/11417 =

0.50

11336/ 19233

= 0.57

9953/ 20680 =

0.48

Net profit ratio Net profit/

Sales*100

1210/ 57493 =

2.10

1320/ 63911 =

2.07

309/ 28456 =

1.09

219/ 29007 =

0.75

Gross profit

ratio

Gross profit/

Sales *100

1882/28456=

6.61

2007/ 29007 =

6.92

3352/ 57493 =

5.83

4144/ 63911 =

6.48

Gearing ratio Total debt /

Capital

employed

14590/ 7411 =

1.97

15085/ 8456 =

1.78

34404/ 10480

= 3.28

34213 / 14834

= 2.31

P/E ratio Market value

per share/

Earning per

share

264.9/ 2.49

=106.39

229.9 / 1.86 =

123.60

189.55/4.96 =

38.22

255.2/ 6.14 =

41.56

Earning per

share ratio

Net income/

Number of

outstanding

309/ 65 = 4.75 219/ 54 = 4.06 1210/ 244 =

4.96

1320/ 215 =

6.14

automobile, home, animal insurance, and health insurance plans. Sainsbury's Power delivers

gasoline and electricity, and also a number of power generators. Sainsbury's

Entertainments offers films and shows, tracks, books, sports and other entertainment media.

Ratio analysis:

Particular Formula Sainsbury

2018 2019

Tesco

2018 2019

Current ratio Current

assets /

Current

liabilities

7857/ 10302 =

0.76

7581 / 11417

= 0.66

13600/ 19233

=0.71

12570/20980

=0.61

Quick ratio Quick assets/

Current

liabilities

6047/ 10302 =

0.59

5652/11417 =

0.50

11336/ 19233

= 0.57

9953/ 20680 =

0.48

Net profit ratio Net profit/

Sales*100

1210/ 57493 =

2.10

1320/ 63911 =

2.07

309/ 28456 =

1.09

219/ 29007 =

0.75

Gross profit

ratio

Gross profit/

Sales *100

1882/28456=

6.61

2007/ 29007 =

6.92

3352/ 57493 =

5.83

4144/ 63911 =

6.48

Gearing ratio Total debt /

Capital

employed

14590/ 7411 =

1.97

15085/ 8456 =

1.78

34404/ 10480

= 3.28

34213 / 14834

= 2.31

P/E ratio Market value

per share/

Earning per

share

264.9/ 2.49

=106.39

229.9 / 1.86 =

123.60

189.55/4.96 =

38.22

255.2/ 6.14 =

41.56

Earning per

share ratio

Net income/

Number of

outstanding

309/ 65 = 4.75 219/ 54 = 4.06 1210/ 244 =

4.96

1320/ 215 =

6.14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tesco

Sainsbury

00.20.40.60.8 0.71 0.76

0.61 0.66

Current ratio

2018 2019

share

Return on

capital

employed

Operating

profit/ Capital

employed

518/ 11699 =

4.43

601/ 12097 =

4.97

1566 / 25502

= 6.14

2639 / 28269

= 9.34

Average stock

turnover

Cost of goods

sold/ Average

stock

26574/ 1792.5

= 14.83

27000/ 1869.5

= 14.44

54141/ 2282 =

23.73

59769/ 2440 =

24.50

Dividend

payout ratio

Dividend per

share/ Earning

per share

235 / 309 =

76.05

247/ 219 =

112.79

82/ 1210 =

6.78

357/ 1320 =

27.05

Capital employed = Total assets- Total current liabilities

Tesco

2018 2019

44735 – 19233 = 25502 48949 – 20680 = 28269

Sainsbury’s

2018 2019

22001 – 10302 = 11699 23514 – 11417 = 12097

Interpretations:

Current ratio:

Above the calculations and the diagram demonstrates that the current proportion of

Tesco declined from 0.71(year-2018) to 0.61(year-2019), whereas Sainsbury recorded a drop in

Sainsbury

00.20.40.60.8 0.71 0.76

0.61 0.66

Current ratio

2018 2019

share

Return on

capital

employed

Operating

profit/ Capital

employed

518/ 11699 =

4.43

601/ 12097 =

4.97

1566 / 25502

= 6.14

2639 / 28269

= 9.34

Average stock

turnover

Cost of goods

sold/ Average

stock

26574/ 1792.5

= 14.83

27000/ 1869.5

= 14.44

54141/ 2282 =

23.73

59769/ 2440 =

24.50

Dividend

payout ratio

Dividend per

share/ Earning

per share

235 / 309 =

76.05

247/ 219 =

112.79

82/ 1210 =

6.78

357/ 1320 =

27.05

Capital employed = Total assets- Total current liabilities

Tesco

2018 2019

44735 – 19233 = 25502 48949 – 20680 = 28269

Sainsbury’s

2018 2019

22001 – 10302 = 11699 23514 – 11417 = 12097

Interpretations:

Current ratio:

Above the calculations and the diagram demonstrates that the current proportion of

Tesco declined from 0.71(year-2018) to 0.61(year-2019), whereas Sainsbury recorded a drop in

the proportion from 0.76 (year-2018) to 0.66 (year-2019). Each corporate enterprise reported a

reduction in the current proportion, but the current proportion of Sainsbury-plc has become 0.66

in year-2019, which is higher than in year-2018, which reveals that Sainsbury has relatively

more effective short-term liquidity position than to Tesco.

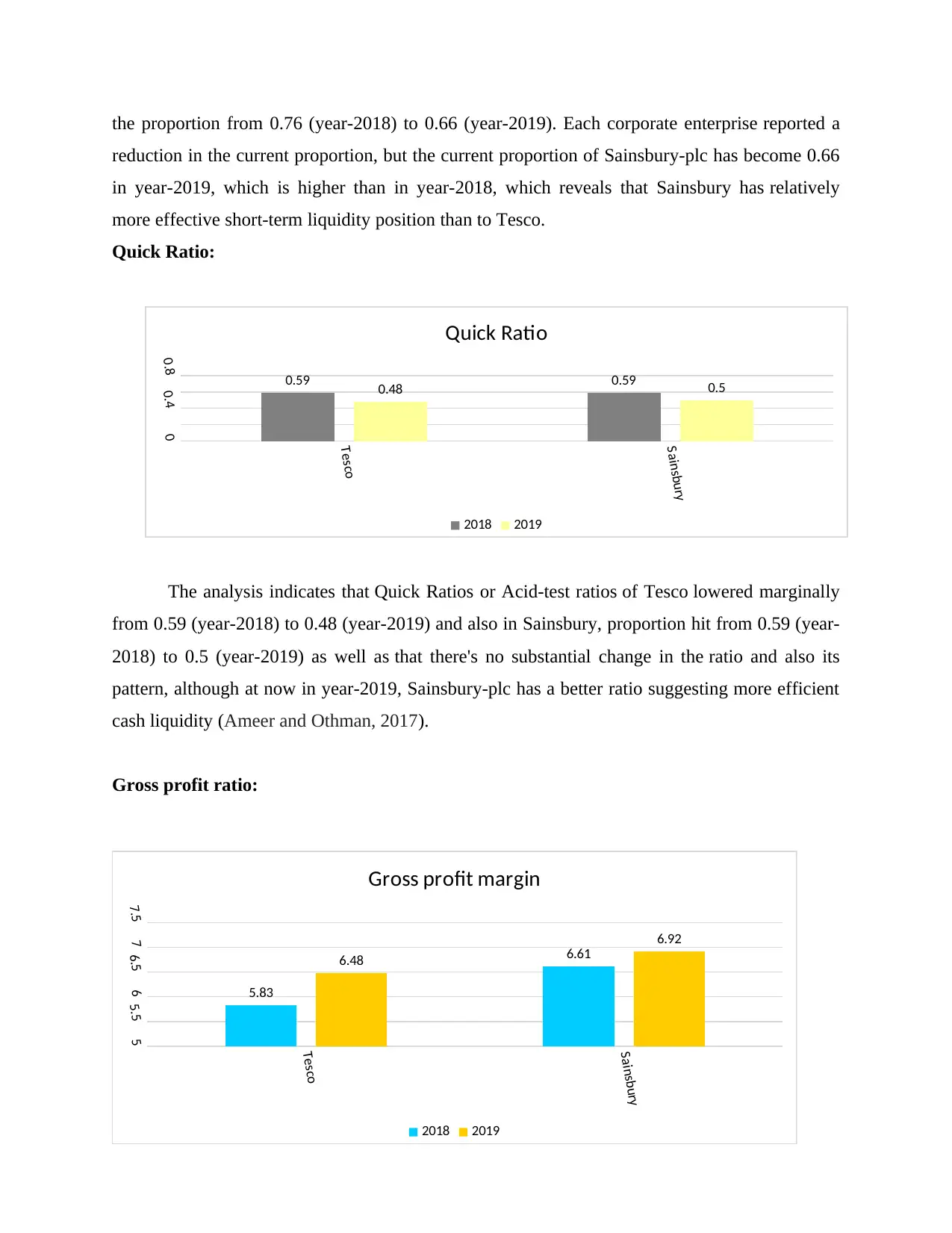

Quick Ratio:

The analysis indicates that Quick Ratios or Acid-test ratios of Tesco lowered marginally

from 0.59 (year-2018) to 0.48 (year-2019) and also in Sainsbury, proportion hit from 0.59 (year-

2018) to 0.5 (year-2019) as well as that there's no substantial change in the ratio and also its

pattern, although at now in year-2019, Sainsbury-plc has a better ratio suggesting more efficient

cash liquidity (Ameer and Othman, 2017).

Gross profit ratio:

Tesco

Sainsbury

00.40.8 0.59 0.59

0.48 0.5

Quick Ratio

2018 2019

Tesco

Sainsbury

55.566.577.5

5.83

6.616.48

6.92

Gross profit margin

2018 2019

reduction in the current proportion, but the current proportion of Sainsbury-plc has become 0.66

in year-2019, which is higher than in year-2018, which reveals that Sainsbury has relatively

more effective short-term liquidity position than to Tesco.

Quick Ratio:

The analysis indicates that Quick Ratios or Acid-test ratios of Tesco lowered marginally

from 0.59 (year-2018) to 0.48 (year-2019) and also in Sainsbury, proportion hit from 0.59 (year-

2018) to 0.5 (year-2019) as well as that there's no substantial change in the ratio and also its

pattern, although at now in year-2019, Sainsbury-plc has a better ratio suggesting more efficient

cash liquidity (Ameer and Othman, 2017).

Gross profit ratio:

Tesco

Sainsbury

00.40.8 0.59 0.59

0.48 0.5

Quick Ratio

2018 2019

Tesco

Sainsbury

55.566.577.5

5.83

6.616.48

6.92

Gross profit margin

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The overall profitability ratio was enhanced from 5.83 per cent (year-2018) to 6.48 per

cent (year-2019), while those of Sainsbury rose from 6.61 (year-2018) to 6,92 (year-2019). So

both enterprises are displaying gradual trends in gross margins. While Sainsbury had a higher

gross margin-rate in year-2019. Which tends to suggest that Sainsbury-plc is more effective of

producing operating income via their base business operations/activities.

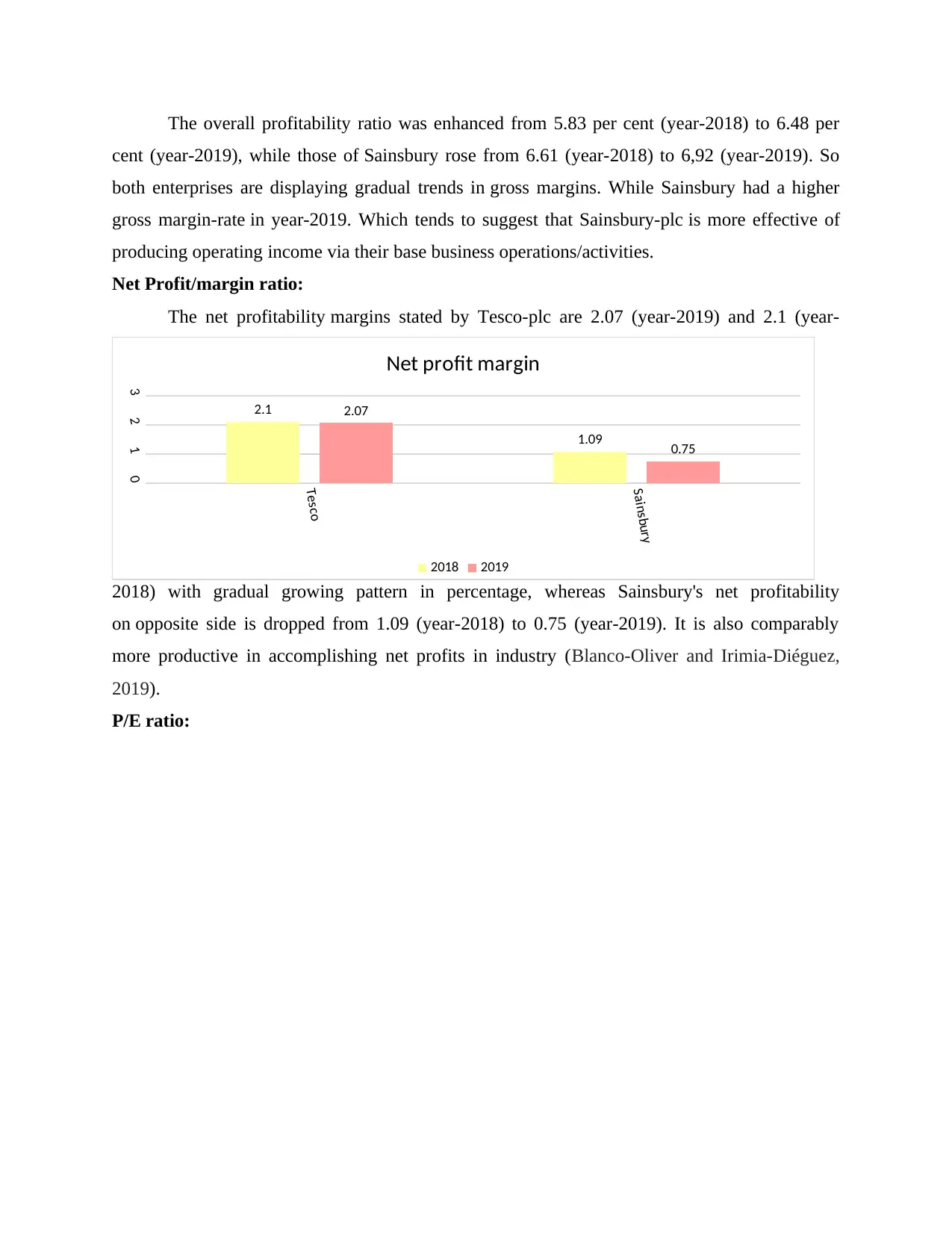

Net Profit/margin ratio:

The net profitability margins stated by Tesco-plc are 2.07 (year-2019) and 2.1 (year-

2018) with gradual growing pattern in percentage, whereas Sainsbury's net profitability

on opposite side is dropped from 1.09 (year-2018) to 0.75 (year-2019). It is also comparably

more productive in accomplishing net profits in industry (Blanco-Oliver and Irimia-Diéguez,

2019).

P/E ratio:

Tesco

Sainsbury

0123

2.1

1.09

2.07

0.75

Net profit margin

2018 2019

cent (year-2019), while those of Sainsbury rose from 6.61 (year-2018) to 6,92 (year-2019). So

both enterprises are displaying gradual trends in gross margins. While Sainsbury had a higher

gross margin-rate in year-2019. Which tends to suggest that Sainsbury-plc is more effective of

producing operating income via their base business operations/activities.

Net Profit/margin ratio:

The net profitability margins stated by Tesco-plc are 2.07 (year-2019) and 2.1 (year-

2018) with gradual growing pattern in percentage, whereas Sainsbury's net profitability

on opposite side is dropped from 1.09 (year-2018) to 0.75 (year-2019). It is also comparably

more productive in accomplishing net profits in industry (Blanco-Oliver and Irimia-Diéguez,

2019).

P/E ratio:

Tesco

Sainsbury

0123

2.1

1.09

2.07

0.75

Net profit margin

2018 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

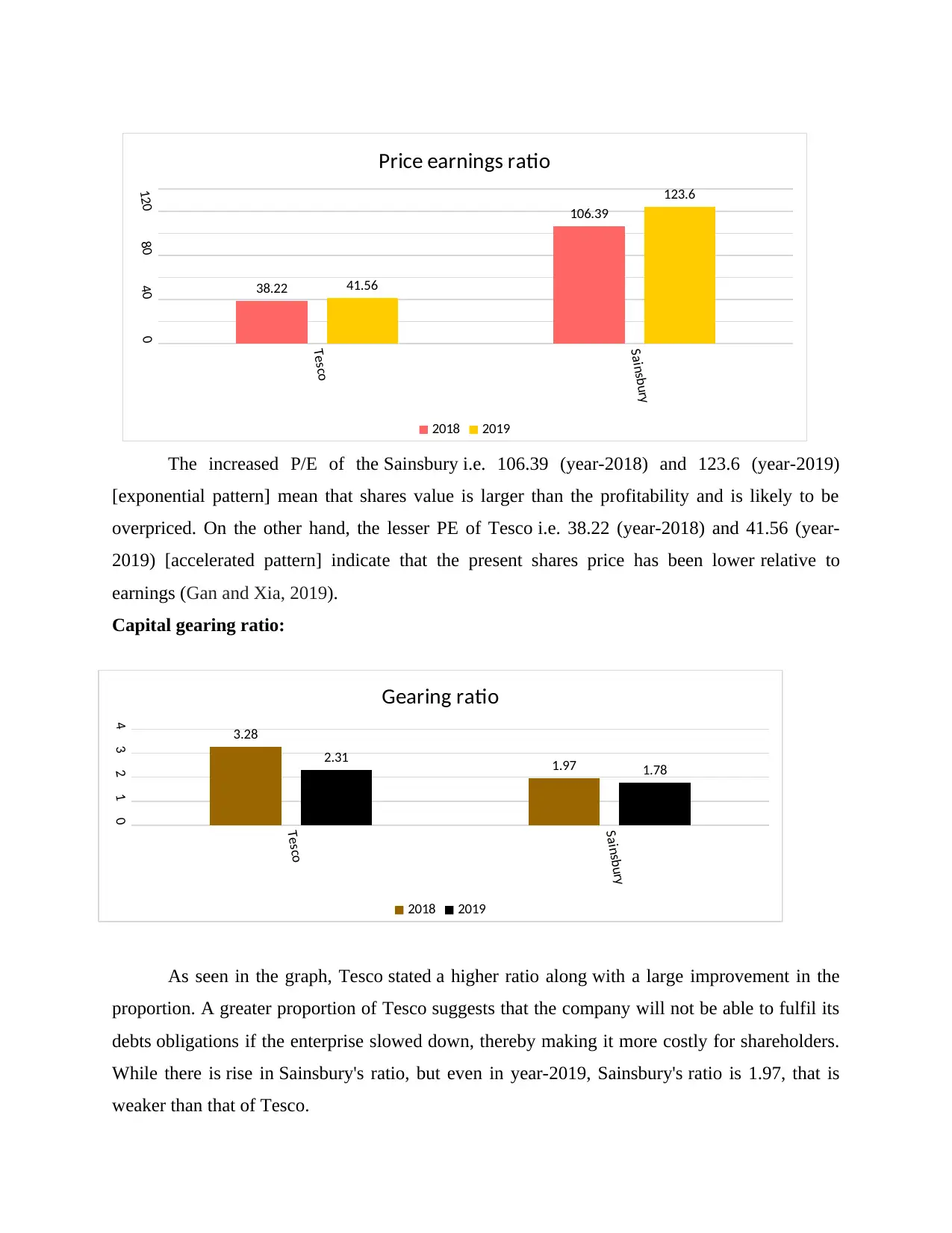

The increased P/E of the Sainsbury i.e. 106.39 (year-2018) and 123.6 (year-2019)

[exponential pattern] mean that shares value is larger than the profitability and is likely to be

overpriced. On the other hand, the lesser PE of Tesco i.e. 38.22 (year-2018) and 41.56 (year-

2019) [accelerated pattern] indicate that the present shares price has been lower relative to

earnings (Gan and Xia, 2019).

Capital gearing ratio:

As seen in the graph, Tesco stated a higher ratio along with a large improvement in the

proportion. A greater proportion of Tesco suggests that the company will not be able to fulfil its

debts obligations if the enterprise slowed down, thereby making it more costly for shareholders.

While there is rise in Sainsbury's ratio, but even in year-2019, Sainsbury's ratio is 1.97, that is

weaker than that of Tesco.

Tesco

Sainsbury

0

40

80

120

38.22

106.39

41.56

123.6

Price earnings ratio

2018 2019

Tesco

Sainsbury

01234 3.28

1.97

2.31 1.78

Gearing ratio

2018 2019

[exponential pattern] mean that shares value is larger than the profitability and is likely to be

overpriced. On the other hand, the lesser PE of Tesco i.e. 38.22 (year-2018) and 41.56 (year-

2019) [accelerated pattern] indicate that the present shares price has been lower relative to

earnings (Gan and Xia, 2019).

Capital gearing ratio:

As seen in the graph, Tesco stated a higher ratio along with a large improvement in the

proportion. A greater proportion of Tesco suggests that the company will not be able to fulfil its

debts obligations if the enterprise slowed down, thereby making it more costly for shareholders.

While there is rise in Sainsbury's ratio, but even in year-2019, Sainsbury's ratio is 1.97, that is

weaker than that of Tesco.

Tesco

Sainsbury

0

40

80

120

38.22

106.39

41.56

123.6

Price earnings ratio

2018 2019

Tesco

Sainsbury

01234 3.28

1.97

2.31 1.78

Gearing ratio

2018 2019

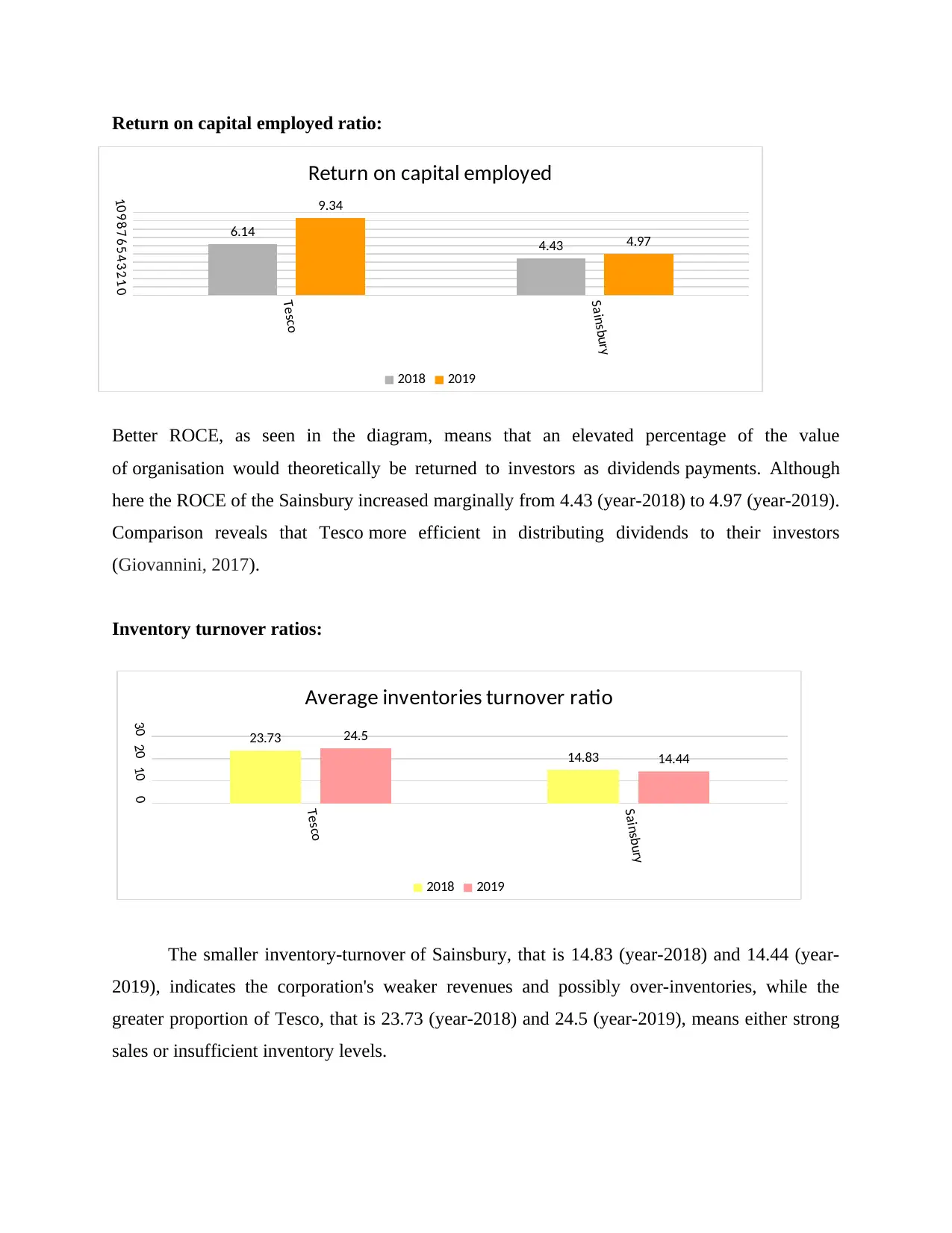

Return on capital employed ratio:

Better ROCE, as seen in the diagram, means that an elevated percentage of the value

of organisation would theoretically be returned to investors as dividends payments. Although

here the ROCE of the Sainsbury increased marginally from 4.43 (year-2018) to 4.97 (year-2019).

Comparison reveals that Tesco more efficient in distributing dividends to their investors

(Giovannini, 2017).

Inventory turnover ratios:

The smaller inventory-turnover of Sainsbury, that is 14.83 (year-2018) and 14.44 (year-

2019), indicates the corporation's weaker revenues and possibly over-inventories, while the

greater proportion of Tesco, that is 23.73 (year-2018) and 24.5 (year-2019), means either strong

sales or insufficient inventory levels.

Tesco

Sainsbury

012345678910

6.14

4.43

9.34

4.97

Return on capital employed

2018 2019

Tesco

Sainsbury

0102030 23.73

14.83

24.5

14.44

Average inventories turnover ratio

2018 2019

Better ROCE, as seen in the diagram, means that an elevated percentage of the value

of organisation would theoretically be returned to investors as dividends payments. Although

here the ROCE of the Sainsbury increased marginally from 4.43 (year-2018) to 4.97 (year-2019).

Comparison reveals that Tesco more efficient in distributing dividends to their investors

(Giovannini, 2017).

Inventory turnover ratios:

The smaller inventory-turnover of Sainsbury, that is 14.83 (year-2018) and 14.44 (year-

2019), indicates the corporation's weaker revenues and possibly over-inventories, while the

greater proportion of Tesco, that is 23.73 (year-2018) and 24.5 (year-2019), means either strong

sales or insufficient inventory levels.

Tesco

Sainsbury

012345678910

6.14

4.43

9.34

4.97

Return on capital employed

2018 2019

Tesco

Sainsbury

0102030 23.73

14.83

24.5

14.44

Average inventories turnover ratio

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dividend pay-out ratio:

Greater dividend pay-out ratios of Sainsbury i.e. 112.79 (2019) and 76.05 (2018) with

significant rise in ratio can suggest that company focusing on shorter-term increases in stock

prices at cost of reinvestments as well as longer-term growth. Also there is greater increase in

dividend pay-out of Tesco from 6.78 (2018) to 27.05 (2019) which is an indication that company

is trying to put short term increase in share prices (Gitman, 2019).

Earnings per share ratio:

Sainsbury's increased dividend pay-out percentages, that is 112.79 (year-2019) and 76.05

(year-2018), with a substantial improvement in the proportion, can indicate that a business that

Tesco

Sainsbury

04080120

6.78

76.05

27.05

112.79

Dividend payout ratio

2018 2019

Tesco

Sainsbury

01234567

4.96 4.75

6.14

4.06

Earnings per share

2018 2019

Greater dividend pay-out ratios of Sainsbury i.e. 112.79 (2019) and 76.05 (2018) with

significant rise in ratio can suggest that company focusing on shorter-term increases in stock

prices at cost of reinvestments as well as longer-term growth. Also there is greater increase in

dividend pay-out of Tesco from 6.78 (2018) to 27.05 (2019) which is an indication that company

is trying to put short term increase in share prices (Gitman, 2019).

Earnings per share ratio:

Sainsbury's increased dividend pay-out percentages, that is 112.79 (year-2019) and 76.05

(year-2018), with a substantial improvement in the proportion, can indicate that a business that

Tesco

Sainsbury

04080120

6.78

76.05

27.05

112.79

Dividend payout ratio

2018 2019

Tesco

Sainsbury

01234567

4.96 4.75

6.14

4.06

Earnings per share

2018 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

relies on shorter-term improvements in share prices at the costs of reinvestment and also some

longer-term enhancement. There is also a larger rise in dividend pay-outs from 6.78 (year-2018)

to 27.05 (year-2019), which shows that the corporation is seeking to boost shares values in the

near term (Jayanti, 2019).

Recommendations:

Tesco Plc: Tesco Company: the company should make an effort to raise its existing share of

current assets, when the reported proportion of the organization is comparatively lower. For

increasing their current assets, accounts payables should be re-scheduled or credit policies should

be modify as well as priority should be put on the handling of overall working-capital funds. In

conjunction, the business's reduced gross profits opposed to the Sainsbury imply that the retailer

should upgrade their core operating operations and optimise operational costs in efforts to

maximize cumulative gross margin status. This most preferably suggested that the rely upon

long-term obligations should be diminished in turn to ramp up the outcomes of overall gearing

ratio. In particular, the conventional inventories-turn ratio is too higher, and thus it would be

strongly suggested that the retailer should focus on the supply network, reorder volumes and

inventory controls in an effort to strengthen this percentage as far as possible.

Sainsbury Plc: Lowered net profitability is really a serious factor for the retailer, that has had an

implication mostly on ROCE along with EPS ratios, and thus advocates that Sainsbury

must minimise its overall business spending and increase its turnover via means of creative

promotional campaigns and policies. The company should include deals, discounts, incentives

and entitlements in efforts to bring more potential customers/buyers (Minnis and Sutherland,

2017).

Limitations for using ratio analysis for knowing firms financial position:

No testing parameters for the different sorts of percentages/ratios and measurements to be

used are known as widely acceptable. Many businesses may have a percentage of certain

items. And that becomes troublesome to bring the two companies on an equal ground.

The review of ratios ignores the practical efficiency of the organisation and thereby

comprises only the quantitative aspect.

Certain companies can mislead the figures to make changes to the proportions to provide

a better portrayal of the corporation. There are still opportunities of window dressings

using ratios in reports.

longer-term enhancement. There is also a larger rise in dividend pay-outs from 6.78 (year-2018)

to 27.05 (year-2019), which shows that the corporation is seeking to boost shares values in the

near term (Jayanti, 2019).

Recommendations:

Tesco Plc: Tesco Company: the company should make an effort to raise its existing share of

current assets, when the reported proportion of the organization is comparatively lower. For

increasing their current assets, accounts payables should be re-scheduled or credit policies should

be modify as well as priority should be put on the handling of overall working-capital funds. In

conjunction, the business's reduced gross profits opposed to the Sainsbury imply that the retailer

should upgrade their core operating operations and optimise operational costs in efforts to

maximize cumulative gross margin status. This most preferably suggested that the rely upon

long-term obligations should be diminished in turn to ramp up the outcomes of overall gearing

ratio. In particular, the conventional inventories-turn ratio is too higher, and thus it would be

strongly suggested that the retailer should focus on the supply network, reorder volumes and

inventory controls in an effort to strengthen this percentage as far as possible.

Sainsbury Plc: Lowered net profitability is really a serious factor for the retailer, that has had an

implication mostly on ROCE along with EPS ratios, and thus advocates that Sainsbury

must minimise its overall business spending and increase its turnover via means of creative

promotional campaigns and policies. The company should include deals, discounts, incentives

and entitlements in efforts to bring more potential customers/buyers (Minnis and Sutherland,

2017).

Limitations for using ratio analysis for knowing firms financial position:

No testing parameters for the different sorts of percentages/ratios and measurements to be

used are known as widely acceptable. Many businesses may have a percentage of certain

items. And that becomes troublesome to bring the two companies on an equal ground.

The review of ratios ignores the practical efficiency of the organisation and thereby

comprises only the quantitative aspect.

Certain companies can mislead the figures to make changes to the proportions to provide

a better portrayal of the corporation. There are still opportunities of window dressings

using ratios in reports.

Conceptual analyses can also be inaccurate, as the inputs of P&L statements rely on

actual expenditures and earnings, while the inputs of the financial statements concentrate

on historical statistics. Differing inputs as a blend of both would always be inconsistent

and does not have the intended effect (Roloff, 2017).

For all those sums, Financial statement would be approved on last day of each financial

cycle. Accordingly, if some figures on that last day of fiscal period are suddenly shot or

eliminated, the as a whole ratio calculation would have a drastic impact.

PORTFOLIO 2

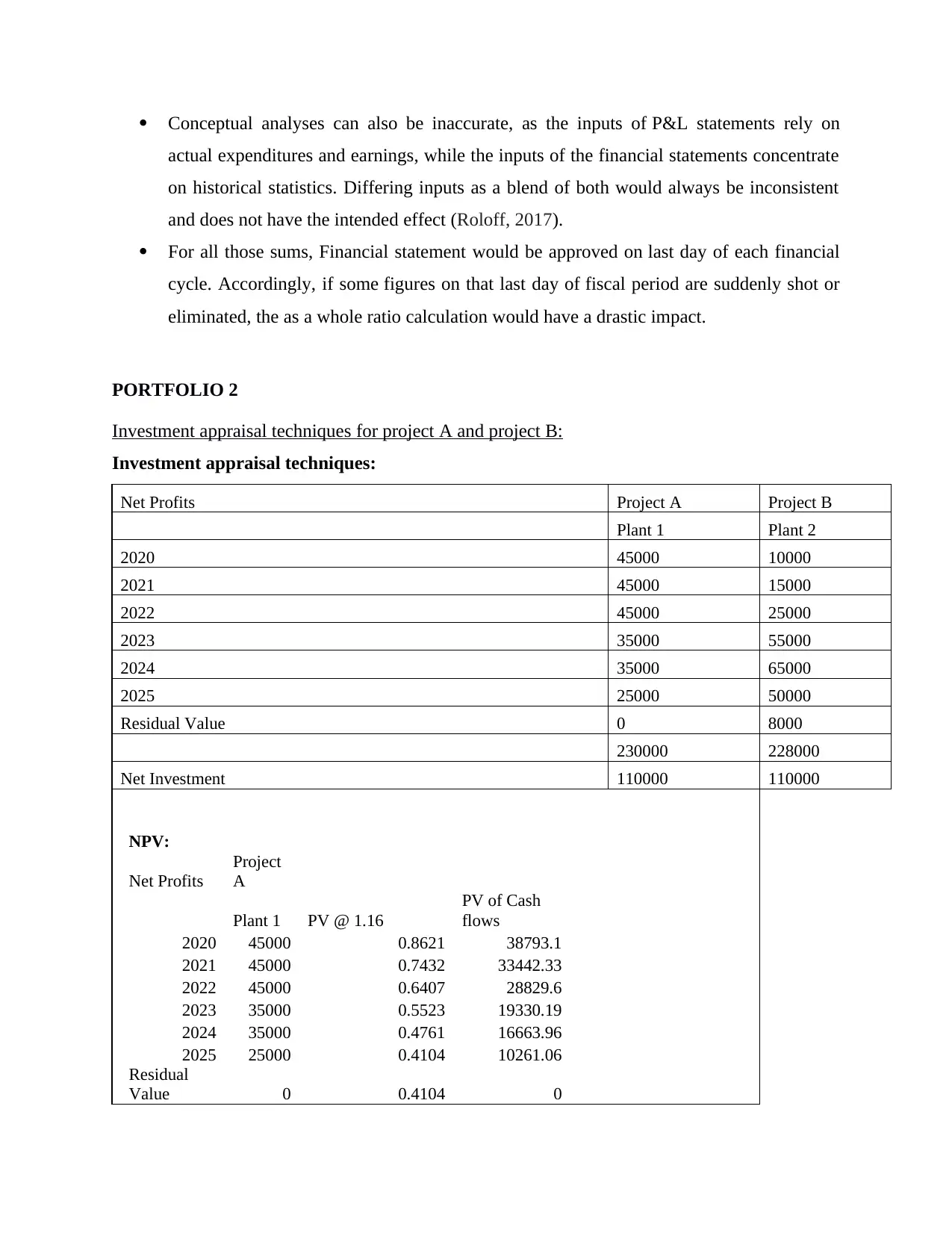

Investment appraisal techniques for project A and project B:

Investment appraisal techniques:

Net Profits Project A Project B

Plant 1 Plant 2

2020 45000 10000

2021 45000 15000

2022 45000 25000

2023 35000 55000

2024 35000 65000

2025 25000 50000

Residual Value 0 8000

230000 228000

Net Investment 110000 110000

NPV:

Net Profits

Project

A

Plant 1 PV @ 1.16

PV of Cash

flows

2020 45000 0.8621 38793.1

2021 45000 0.7432 33442.33

2022 45000 0.6407 28829.6

2023 35000 0.5523 19330.19

2024 35000 0.4761 16663.96

2025 25000 0.4104 10261.06

Residual

Value 0 0.4104 0

actual expenditures and earnings, while the inputs of the financial statements concentrate

on historical statistics. Differing inputs as a blend of both would always be inconsistent

and does not have the intended effect (Roloff, 2017).

For all those sums, Financial statement would be approved on last day of each financial

cycle. Accordingly, if some figures on that last day of fiscal period are suddenly shot or

eliminated, the as a whole ratio calculation would have a drastic impact.

PORTFOLIO 2

Investment appraisal techniques for project A and project B:

Investment appraisal techniques:

Net Profits Project A Project B

Plant 1 Plant 2

2020 45000 10000

2021 45000 15000

2022 45000 25000

2023 35000 55000

2024 35000 65000

2025 25000 50000

Residual Value 0 8000

230000 228000

Net Investment 110000 110000

NPV:

Net Profits

Project

A

Plant 1 PV @ 1.16

PV of Cash

flows

2020 45000 0.8621 38793.1

2021 45000 0.7432 33442.33

2022 45000 0.6407 28829.6

2023 35000 0.5523 19330.19

2024 35000 0.4761 16663.96

2025 25000 0.4104 10261.06

Residual

Value 0 0.4104 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.