Financial Ratio Analysis and Capital Investment Appraisal Report

VerifiedAdded on 2020/06/04

Paraphrase This Document

INTRODUCTION...........................................................................................................................1

Portfolio 1........................................................................................................................................1

A. Computation of 10 financial ratios....................................................................................1

B. Interpretation of above calculated financial ratios.............................................................3

C. Recommendations to increase performance of companies..............................................13

D. Discuss limitations of ratios............................................................................................14

Portfolio 2......................................................................................................................................15

Capital Investment Appraisal ........................................................................................................15

A. NPV, ARR and Payback period calculations..................................................................15

B. Limitations of the investment appraisal...........................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

Financial statements are important elements of business. From this, financial ratios are

computed which provides financial position of the company and are useful for comparison as

well with another company. This report deals with comparison of two companies such as Sports

direct plc and JD Sports organisation which are retailers of sport goods. For such comparison,

financial ratios are being calculated so that financial position of both the organisations may be

highlighted with much ease (Rodrigues and Rodrigues, 2018). Various capital investment

appraisal techniques are also highlighted and there limitations as well. Both the firms are

required that they perform well in the market by increasing efficiency so that financial position

may be strengthen up to great extent with much ease. The poor performance of both of them may

be reduced by implementing strategies so that they may gain efficiency in the market with much

ease.

Portfolio 1

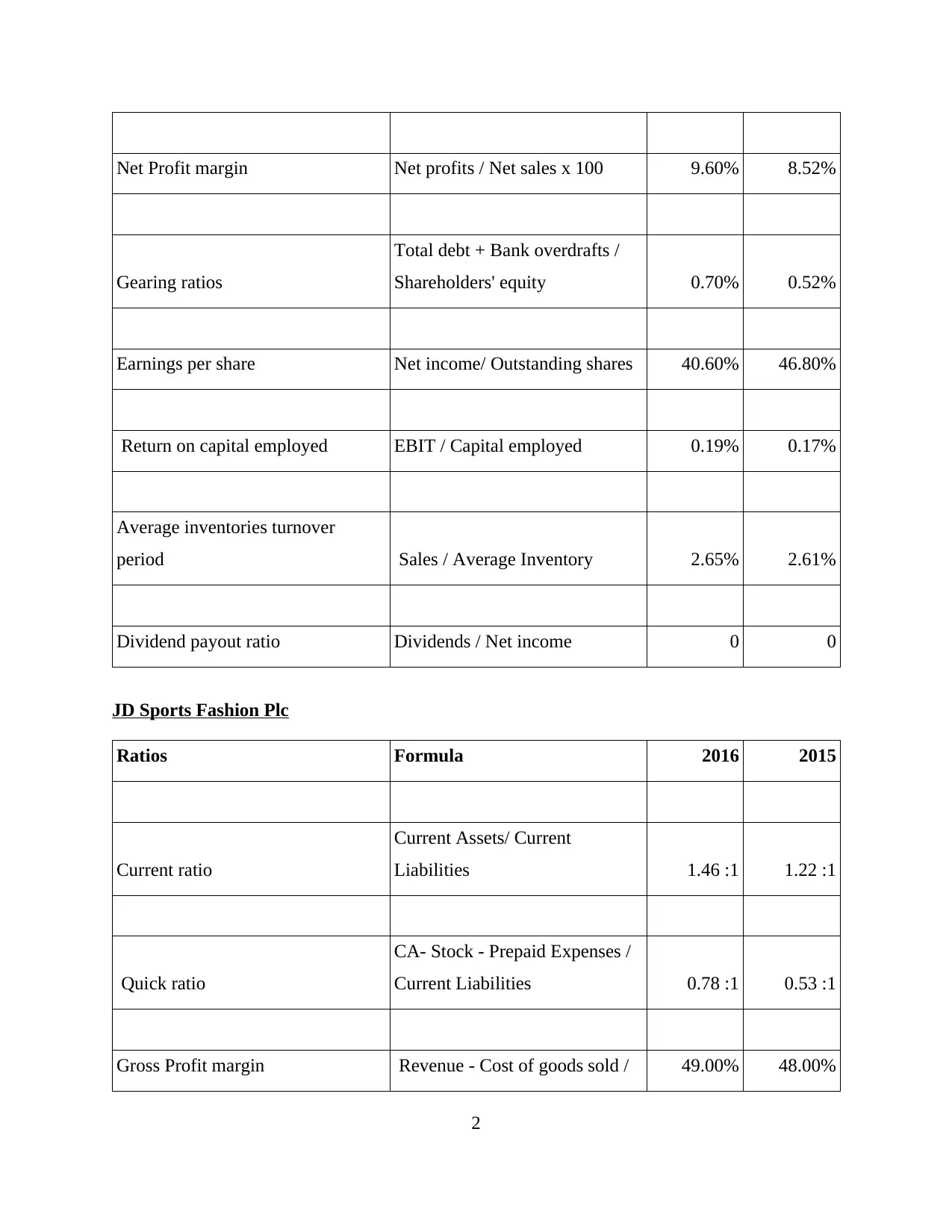

A. Computation of 10 financial ratios

Sports Direct International Plc

Ratios Formula 2016 2015

Current ratio

Current Assets/ Current

Liabilities 2.43 :1 2.3 :1

Quick ratio

CA- Stock - Prepaid Expenses /

Current Liabilities 0.62 :1 0.94 :1

Gross Profit margin

Revenue - Cost of goods sold /

Revenue 44.00% 43.00%

Operating Profit margin

Operating income / Net sales *

100 7.68% 10.43%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gearing ratios

Total debt + Bank overdrafts /

Shareholders' equity 0.70% 0.52%

Earnings per share Net income/ Outstanding shares 40.60% 46.80%

Return on capital employed EBIT / Capital employed 0.19% 0.17%

Average inventories turnover

period Sales / Average Inventory 2.65% 2.61%

Dividend payout ratio Dividends / Net income 0 0

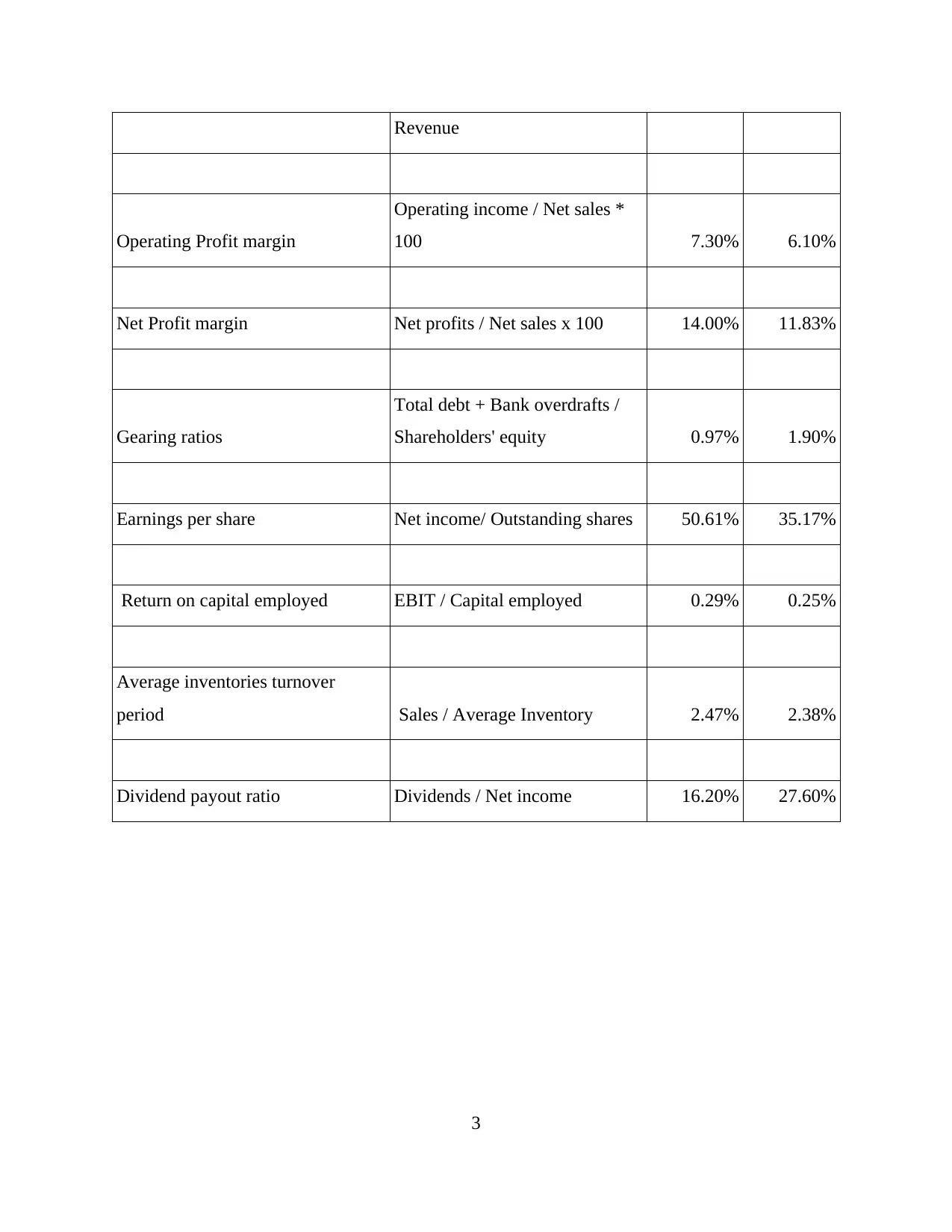

JD Sports Fashion Plc

Ratios Formula 2016 2015

Current ratio

Current Assets/ Current

Liabilities 1.46 :1 1.22 :1

Quick ratio

CA- Stock - Prepaid Expenses /

Current Liabilities 0.78 :1 0.53 :1

Gross Profit margin Revenue - Cost of goods sold / 49.00% 48.00%

2

Paraphrase This Document

Operating Profit margin

Operating income / Net sales *

100 7.30% 6.10%

Net Profit margin Net profits / Net sales x 100 14.00% 11.83%

Gearing ratios

Total debt + Bank overdrafts /

Shareholders' equity 0.97% 1.90%

Earnings per share Net income/ Outstanding shares 50.61% 35.17%

Return on capital employed EBIT / Capital employed 0.29% 0.25%

Average inventories turnover

period Sales / Average Inventory 2.47% 2.38%

Dividend payout ratio Dividends / Net income 16.20% 27.60%

3

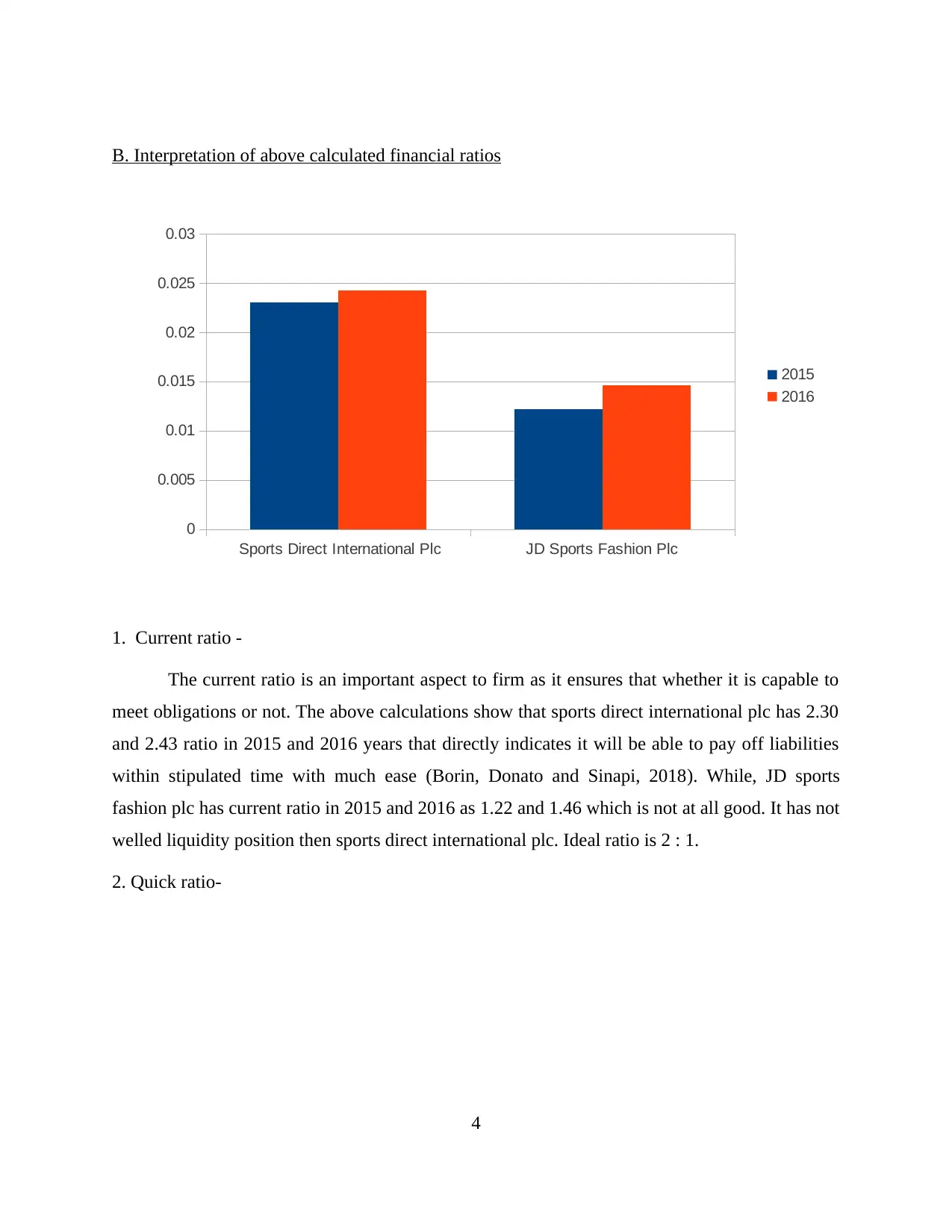

1. Current ratio -

The current ratio is an important aspect to firm as it ensures that whether it is capable to

meet obligations or not. The above calculations show that sports direct international plc has 2.30

and 2.43 ratio in 2015 and 2016 years that directly indicates it will be able to pay off liabilities

within stipulated time with much ease (Borin, Donato and Sinapi, 2018). While, JD sports

fashion plc has current ratio in 2015 and 2016 as 1.22 and 1.46 which is not at all good. It has not

welled liquidity position then sports direct international plc. Ideal ratio is 2 : 1.

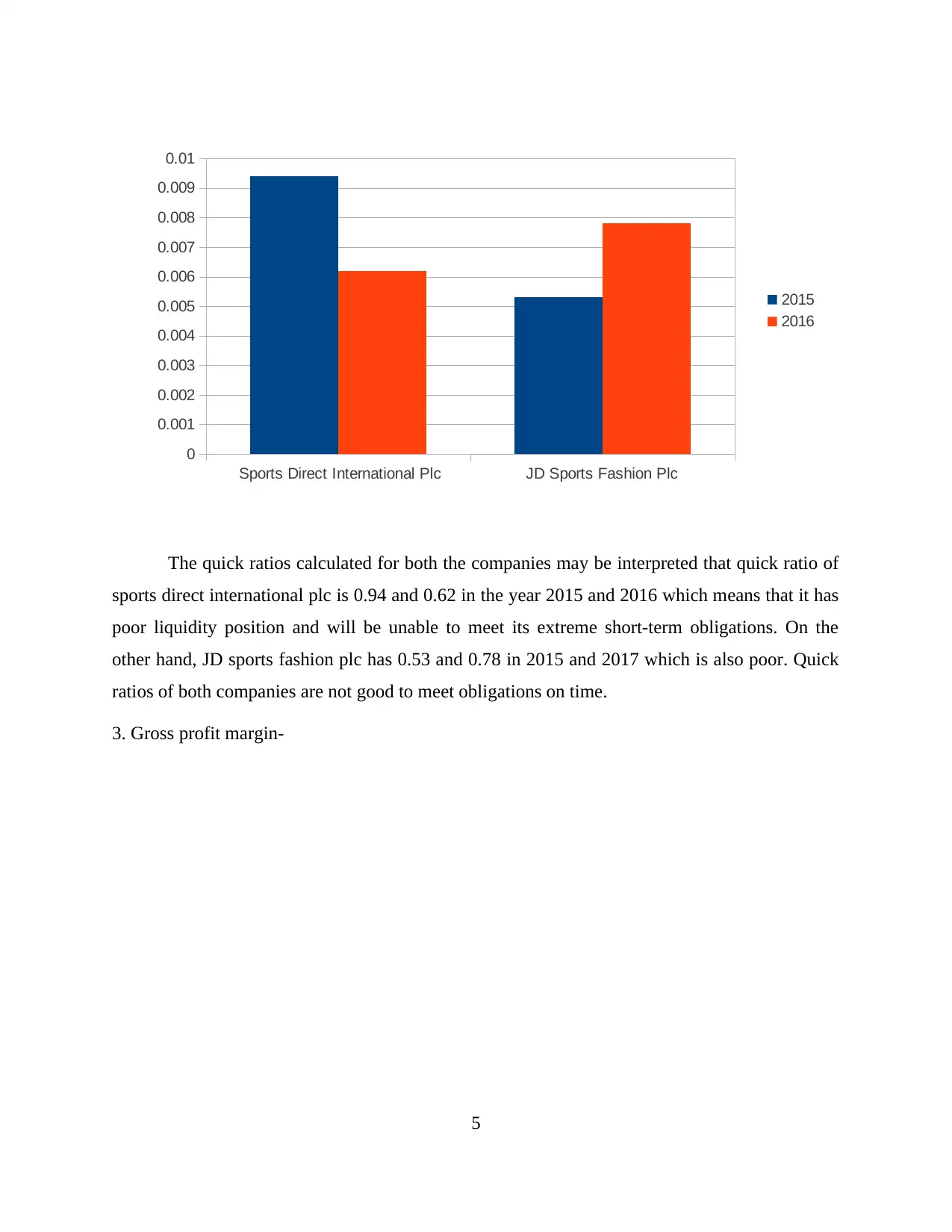

2. Quick ratio-

4

Sports Direct International Plc JD Sports Fashion Plc

0

0.005

0.01

0.015

0.02

0.025

0.03

2015

2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sports direct international plc is 0.94 and 0.62 in the year 2015 and 2016 which means that it has

poor liquidity position and will be unable to meet its extreme short-term obligations. On the

other hand, JD sports fashion plc has 0.53 and 0.78 in 2015 and 2017 which is also poor. Quick

ratios of both companies are not good to meet obligations on time.

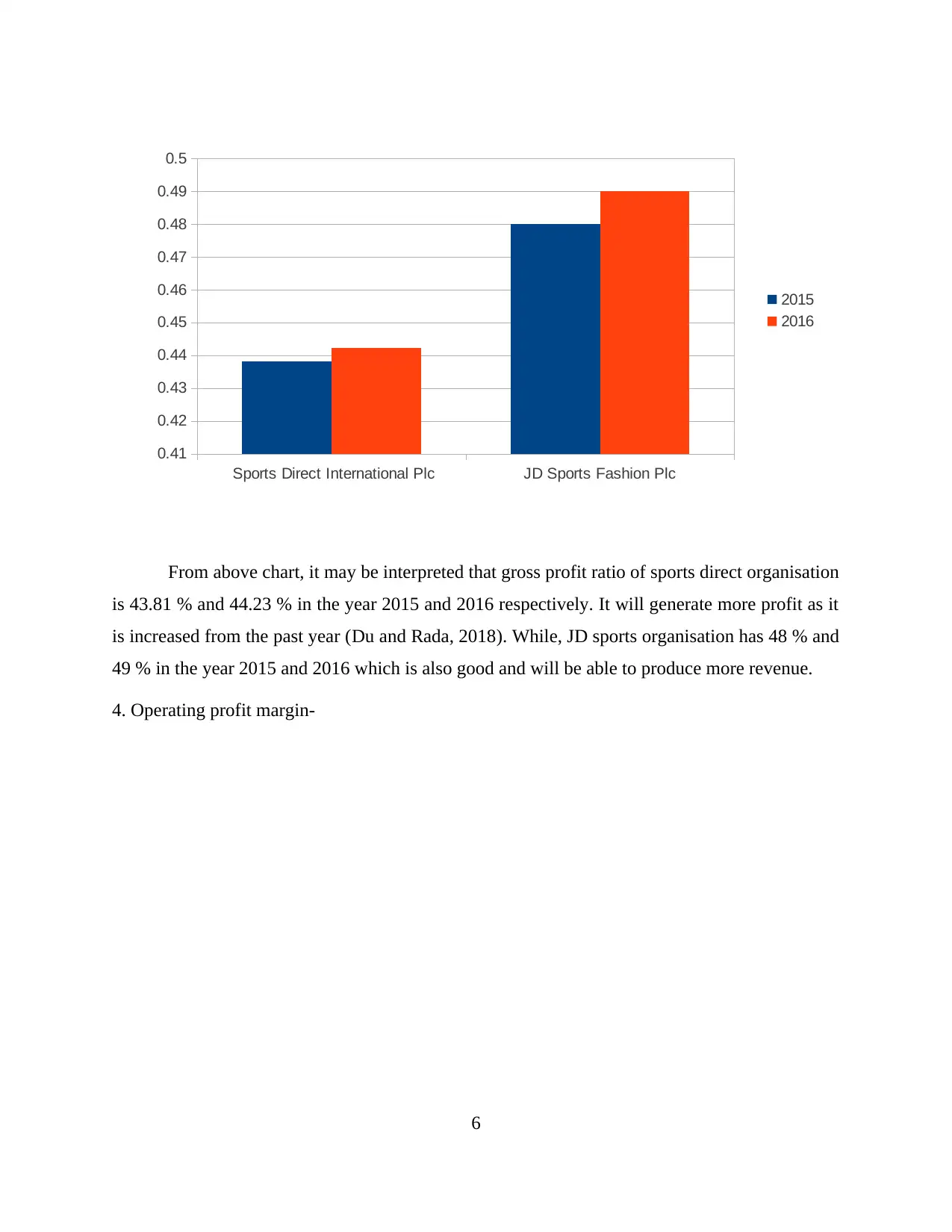

3. Gross profit margin-

5

Sports Direct International Plc JD Sports Fashion Plc

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008

0.009

0.01

2015

2016

Paraphrase This Document

is 43.81 % and 44.23 % in the year 2015 and 2016 respectively. It will generate more profit as it

is increased from the past year (Du and Rada, 2018). While, JD sports organisation has 48 % and

49 % in the year 2015 and 2016 which is also good and will be able to produce more revenue.

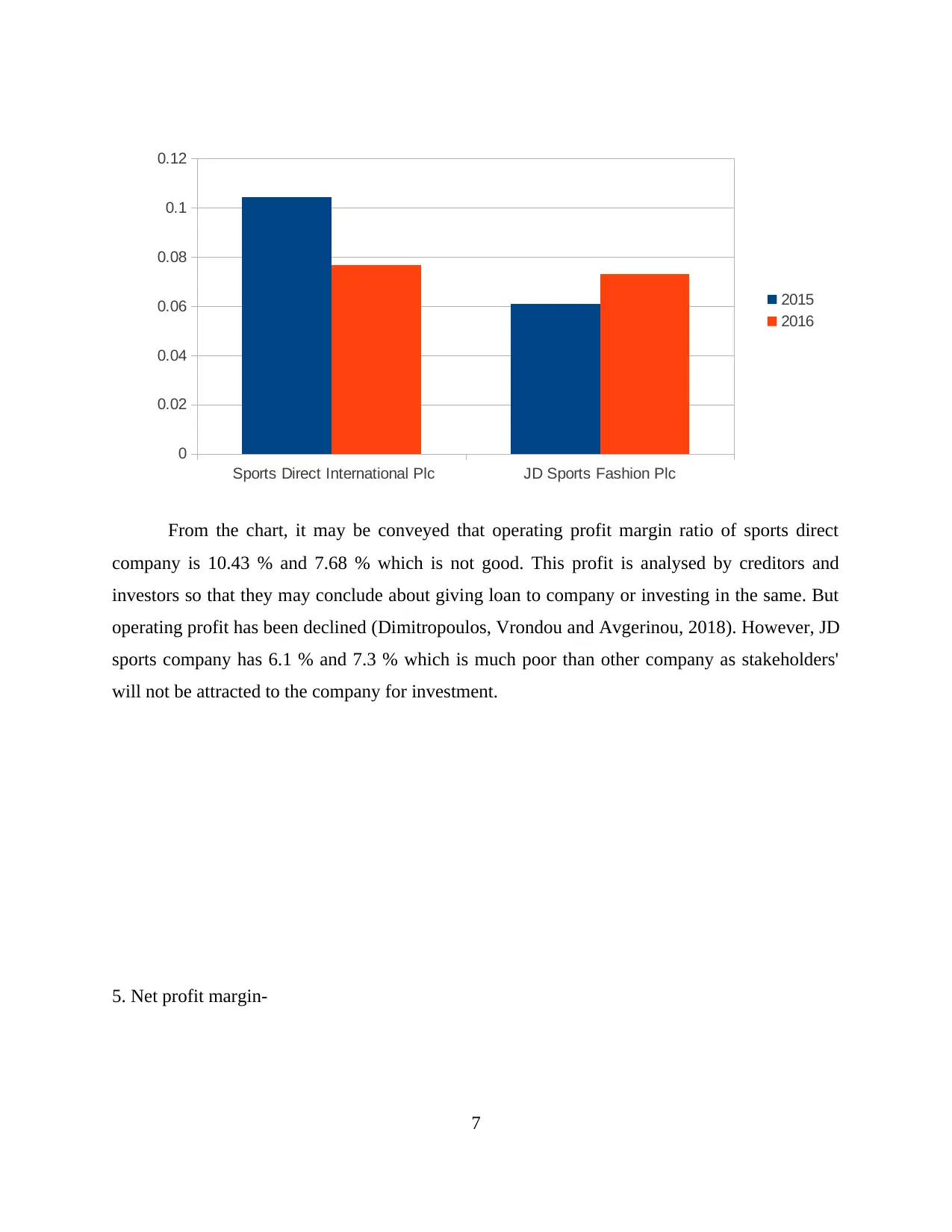

4. Operating profit margin-

6

Sports Direct International Plc JD Sports Fashion Plc

0.41

0.42

0.43

0.44

0.45

0.46

0.47

0.48

0.49

0.5

2015

2016

company is 10.43 % and 7.68 % which is not good. This profit is analysed by creditors and

investors so that they may conclude about giving loan to company or investing in the same. But

operating profit has been declined (Dimitropoulos, Vrondou and Avgerinou, 2018). However, JD

sports company has 6.1 % and 7.3 % which is much poor than other company as stakeholders'

will not be attracted to the company for investment.

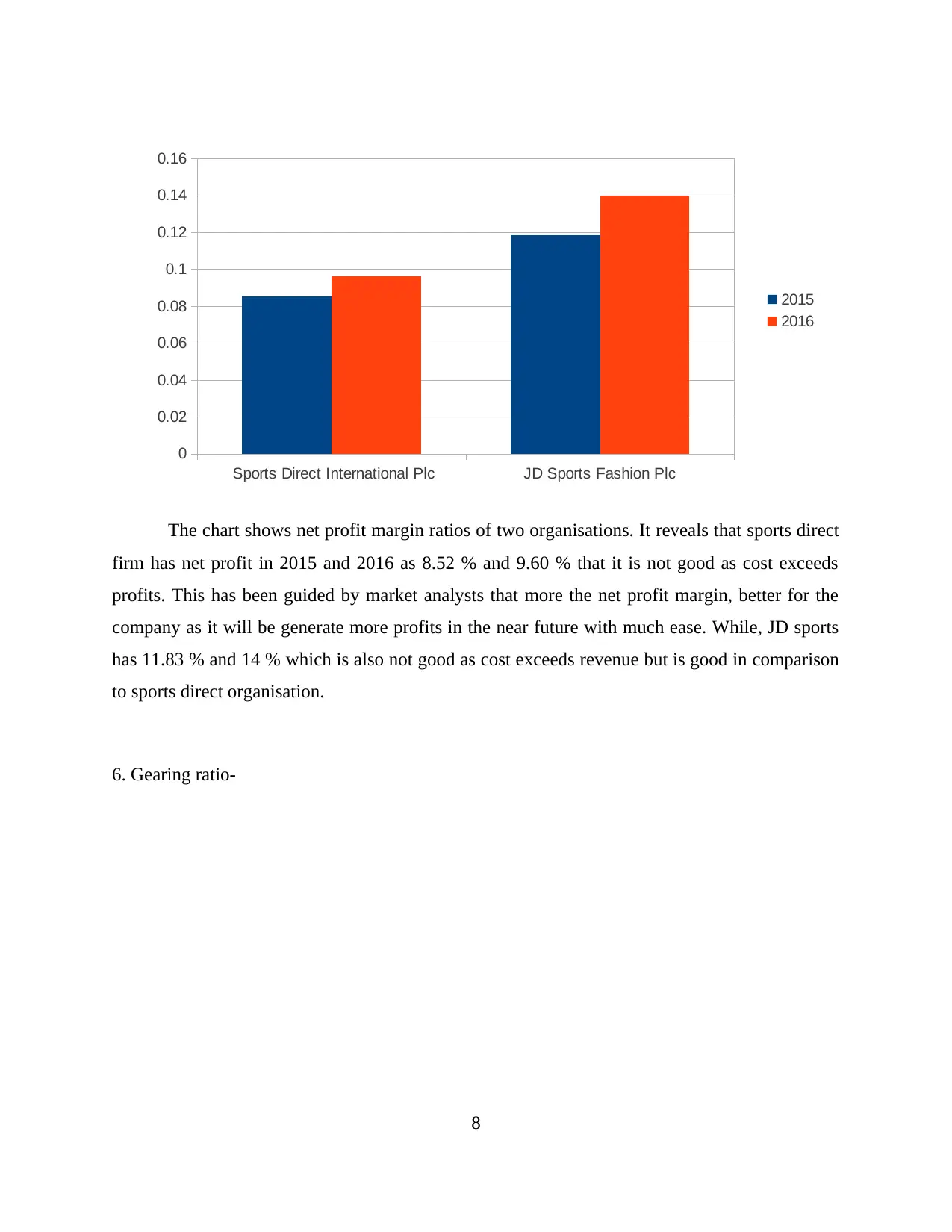

5. Net profit margin-

7

Sports Direct International Plc JD Sports Fashion Plc

0

0.02

0.04

0.06

0.08

0.1

0.12

2015

2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

firm has net profit in 2015 and 2016 as 8.52 % and 9.60 % that it is not good as cost exceeds

profits. This has been guided by market analysts that more the net profit margin, better for the

company as it will be generate more profits in the near future with much ease. While, JD sports

has 11.83 % and 14 % which is also not good as cost exceeds revenue but is good in comparison

to sports direct organisation.

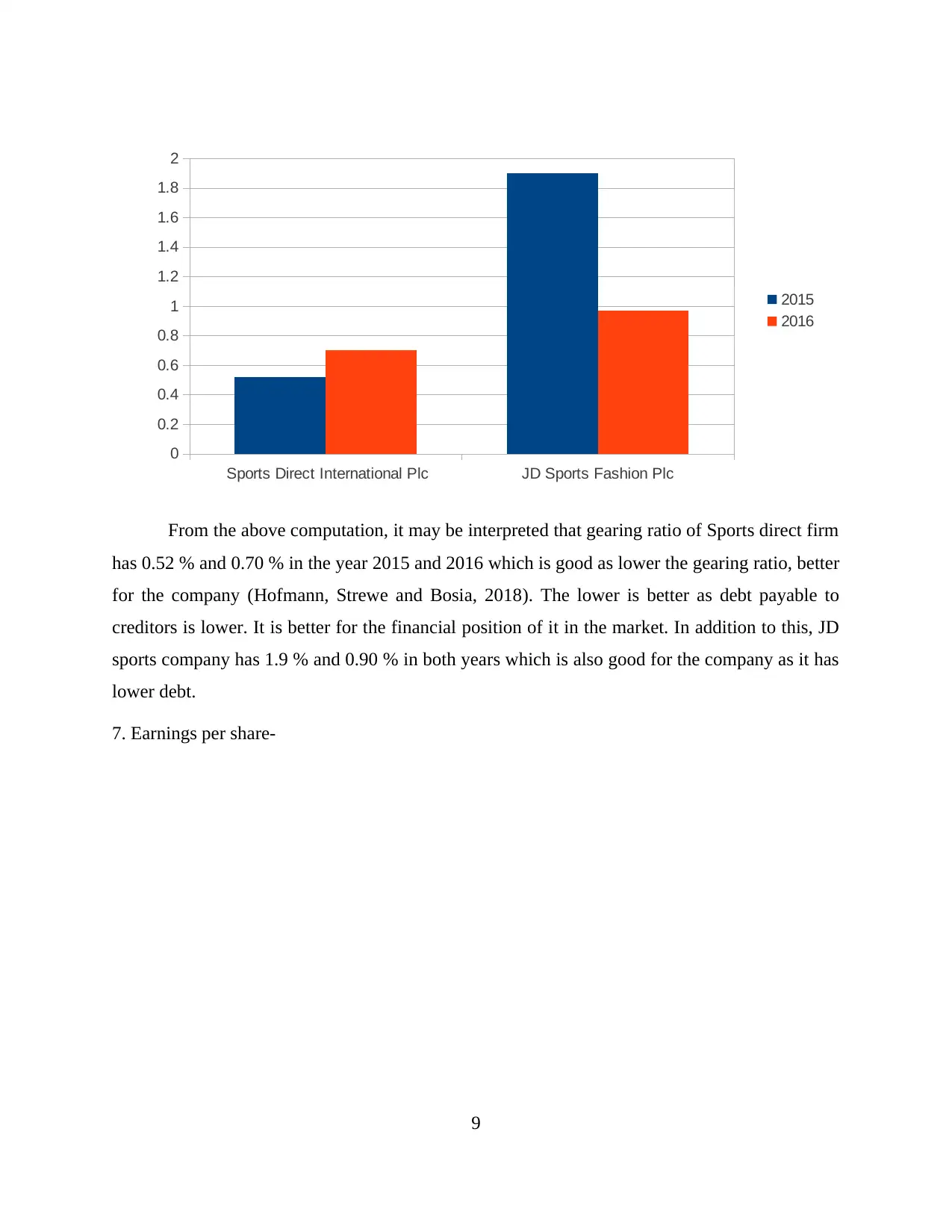

6. Gearing ratio-

8

Sports Direct International Plc JD Sports Fashion Plc

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

2015

2016

Paraphrase This Document

has 0.52 % and 0.70 % in the year 2015 and 2016 which is good as lower the gearing ratio, better

for the company (Hofmann, Strewe and Bosia, 2018). The lower is better as debt payable to

creditors is lower. It is better for the financial position of it in the market. In addition to this, JD

sports company has 1.9 % and 0.90 % in both years which is also good for the company as it has

lower debt.

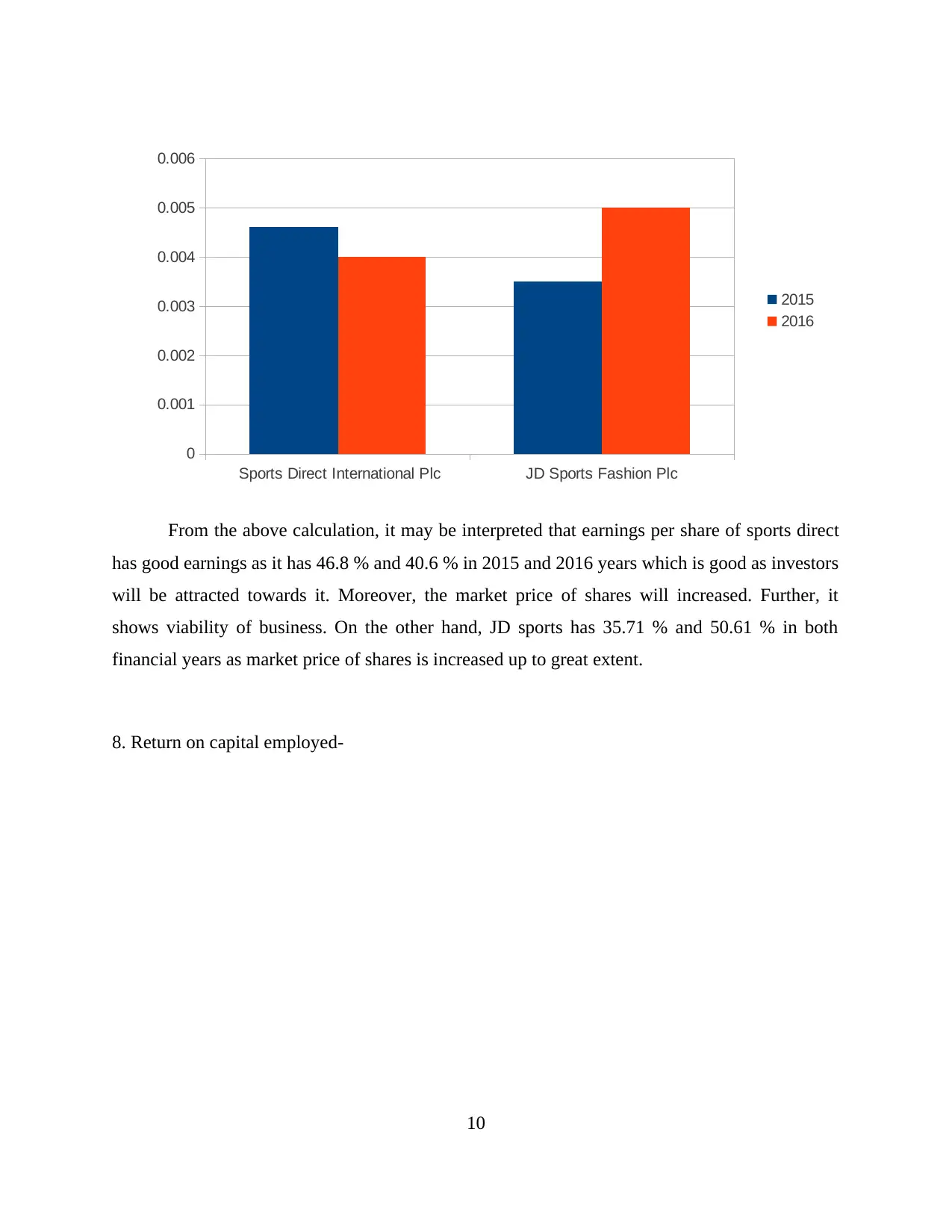

7. Earnings per share-

9

Sports Direct International Plc JD Sports Fashion Plc

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2015

2016

has good earnings as it has 46.8 % and 40.6 % in 2015 and 2016 years which is good as investors

will be attracted towards it. Moreover, the market price of shares will increased. Further, it

shows viability of business. On the other hand, JD sports has 35.71 % and 50.61 % in both

financial years as market price of shares is increased up to great extent.

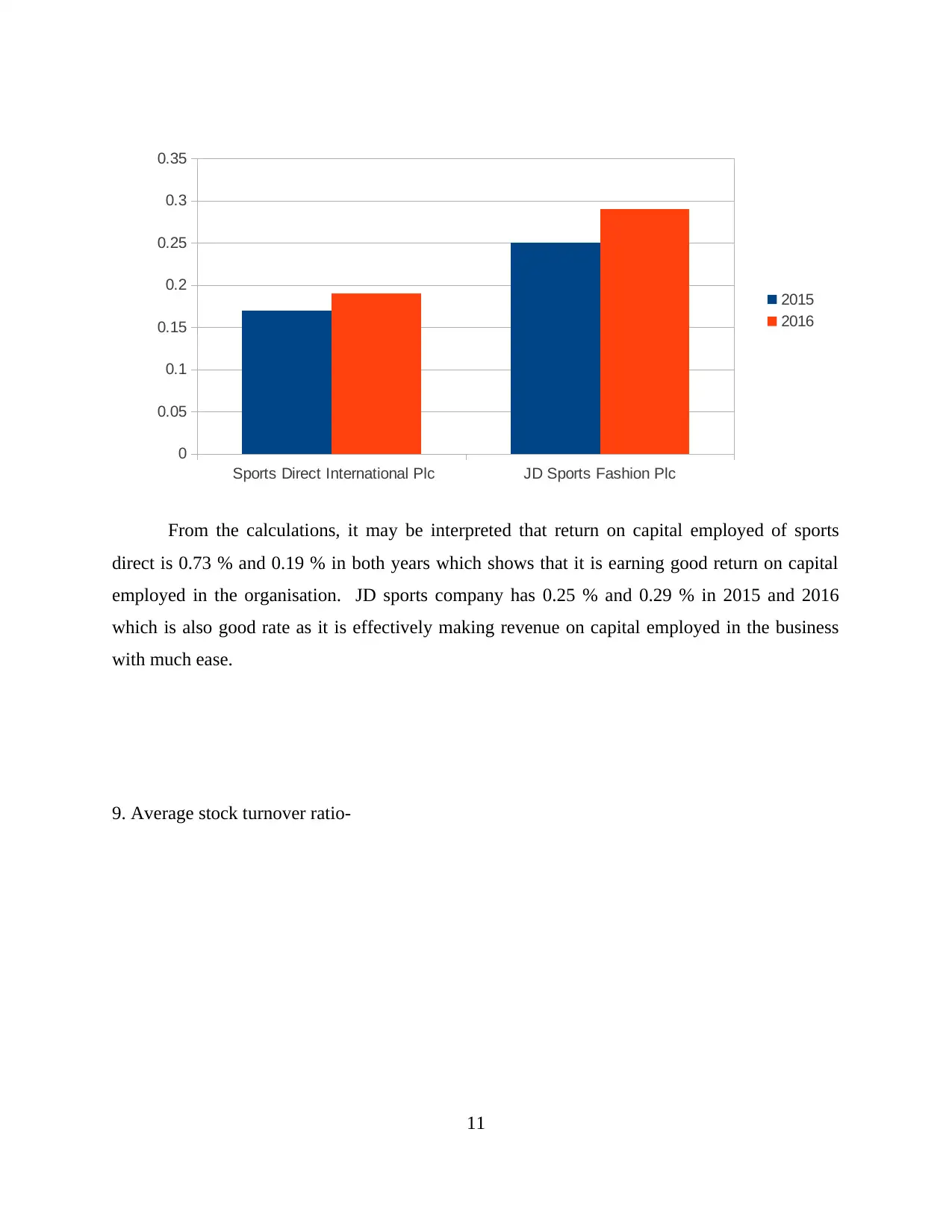

8. Return on capital employed-

10

Sports Direct International Plc JD Sports Fashion Plc

0

0.001

0.002

0.003

0.004

0.005

0.006

2015

2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

direct is 0.73 % and 0.19 % in both years which shows that it is earning good return on capital

employed in the organisation. JD sports company has 0.25 % and 0.29 % in 2015 and 2016

which is also good rate as it is effectively making revenue on capital employed in the business

with much ease.

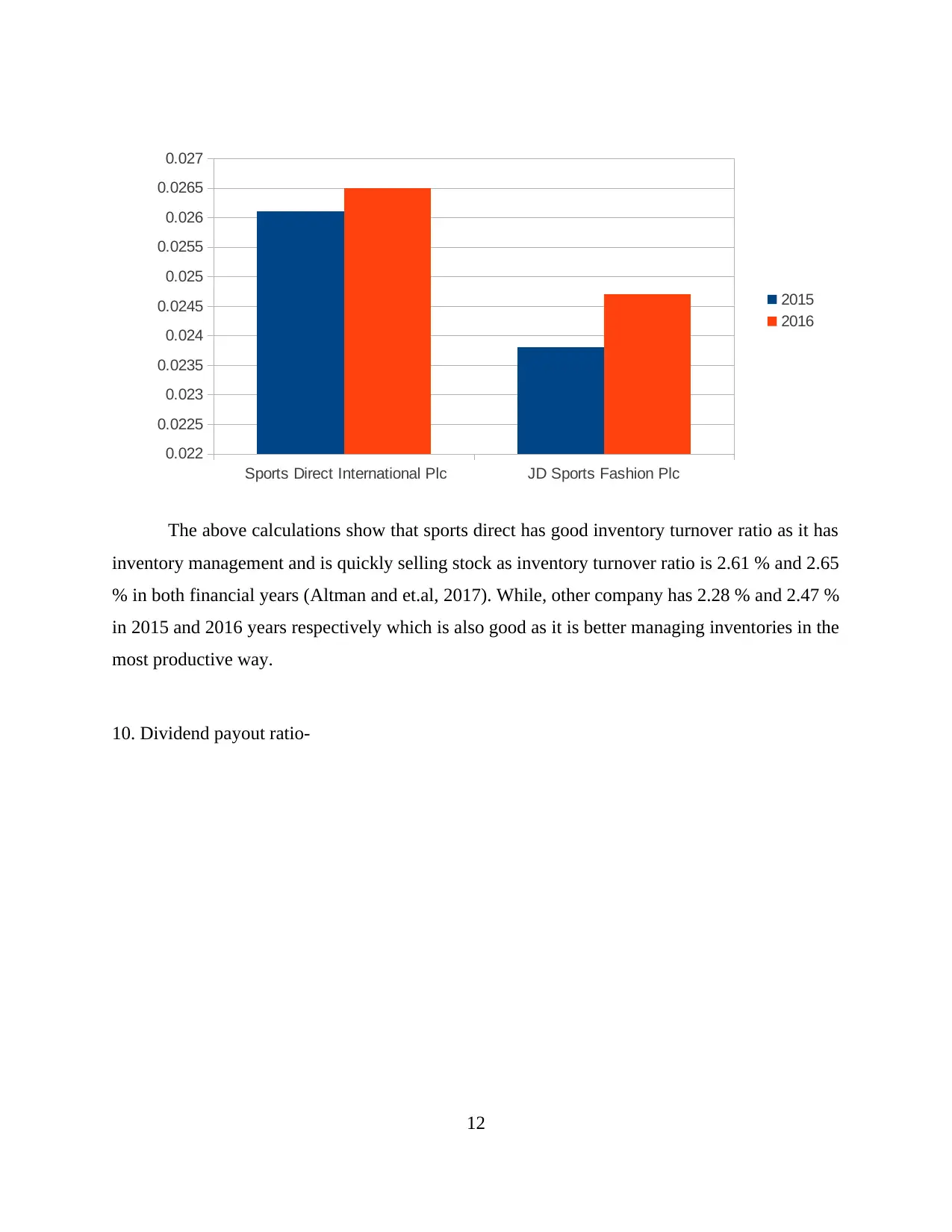

9. Average stock turnover ratio-

11

Sports Direct International Plc JD Sports Fashion Plc

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

2015

2016

Paraphrase This Document

inventory management and is quickly selling stock as inventory turnover ratio is 2.61 % and 2.65

% in both financial years (Altman and et.al, 2017). While, other company has 2.28 % and 2.47 %

in 2015 and 2016 years respectively which is also good as it is better managing inventories in the

most productive way.

10. Dividend payout ratio-

12

Sports Direct International Plc JD Sports Fashion Plc

0.022

0.0225

0.023

0.0235

0.024

0.0245

0.025

0.0255

0.026

0.0265

0.027

2015

2016

organisation is 0 in both financial years which implies that it is not earning profits and is in debt.

It also shows that it is retaining dividend amount which is payable to shareholders'. While, JD

Sports has 27.6 % and 16.2 % in 2015 and 2016 years which is good as it is imparting dividends

and is earning good quantum of profits.

13

Sports Direct International Plc JD Sports Fashion Plc

0

0.05

0.1

0.15

0.2

0.25

0.3

2015

2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Firstly coming to current ratios, Sport direct has ideal ratio as it will be able to pay off

current liabilities with much ease. But it is not good for JD Sports company. It is hereby

recommended that it should sell off unproductive assets as it increases costs and gains nothing to

the organisation (Dyreng, Mayew and Schipper, 2017). Moreover, it increases interest on it. In

addition, quick ratio of Sports direct company is better than JD sports company. It is

recommended that liabilities must be paid off on time.

Gross profit margin is not good for both the organisations. It is recommended that cash

discounts should be taken from the suppliers of raw materials. Taking discounts will initiate

more profit and as a result, company may be able to strengthen financial position. Further,

moving to operating profit margin, both the companies have poor operating profit margin. It may

be increased by minimising cost of goods sold. This may be done by reviewing expenses and

cutting down cost of sales. This will provide better operating profit to both firms.

Earnings per share can be increased by taking buy backs of shares. It is vital part of

organisation as shareholders' are attracted to invest in profitable company and make sure that

good returns are being generated. As such, Sports direct plc should buy backs shares. Stock

turnover ratio or inventory turnover ratio may be improved by buying less inventory from

suppliers as additional inventories increases costs for procurement. It leads to spoilage and

increases cost incurred in maintaining in warehouse. As such, it is recommended that companies

should buy only required inventories for production purpose as more inventories maximises

handling costs and gradually increases expenditures of the organisation.

Gearing ratios should also be lower down so that no burden of paying debt may arise.

However, debt should be taken but in less amount. Instead of this, organisation should make a

perfect blend or mixture of both debt and equity so that advantages of both of them may be used

by organisation (Atoom, Malkawi and Al Share, 2017). It is recommended that adequate mix of

debt and equity is better for both companies. Moreover, dividend payout ratio may be improved

by Sports direct as in both years, it has retained it and not distributed to shareholders' which is

not good as they may lose interest in the organisation. Company should increase performance so

that dividends may be provided to shareholders'.

14

Paraphrase This Document

Ratios impart effective results but has certain limitations as well. It is based on previous

accounting figures and facts which are deficient and may be manipulated. This impacts adversely

and as such, it does not provide concrete conclusions. Moreover, comparison is not possible as

one organisation charges different methods and other one uses different method for valuation

purpose and as such, it does not generate accurate results (Delen, Kuzey and Uyar, 2013). This

may be explained with an example, Sports direct company is using FIFO method for valuing

stock and JD sports uses LIFO method which shows variations and leads to inaccurate results.

Apart from this, different methods are charge for depreciation, preliminary expenses

which is difficult for comparison purpose as well. Accounting policies are also followed

differently by various companies. As such, JD Sports uses diminishing method for calculating

depreciation and at the same time, Sports direct plc uses straight line method and as a result,

conclusions drawn are different which is not provided by financial ratios and as such, they are

difficult to compare (Limitations of financial ratios).

Inflation may lead to difference in balance sheets as historical cost based balance sheets

and accounting figures are not adjusted as firms purchase assets on different dates and often lead

to misconception and does not provide appropriate results to organisation. As a result, without

adjustment false information is provided to business which is not meaningful. Apart from this,

financial ratios are not useful as it does not initiate operational changes which is required by the

company. This leads to misconception as ratios calculated years ago and then compared with

same ratios today produces inaccurate conclusions. As a result, misleading conclusions are laid

by financial ratios which provides improper conclusions.

Moreover, company follows different strategies for attracting customers'. As such, if JD

Sports plc follows low cost strategy and as such, low profit margin may be forecasted by it.

While, if Sports direct plc charges high prices of its products and following more profit margin,

then if two companies are compare on the basis of financial ratios, results will be misleading and

of no use to both companies (Buchman, Harris and Liu, 2016). As such, financial ratios are

unable to compare two companies which follows different methods and accounting polices. It is

not much reliable to calculate financial ratios as concrete results are not delivered by it.

15

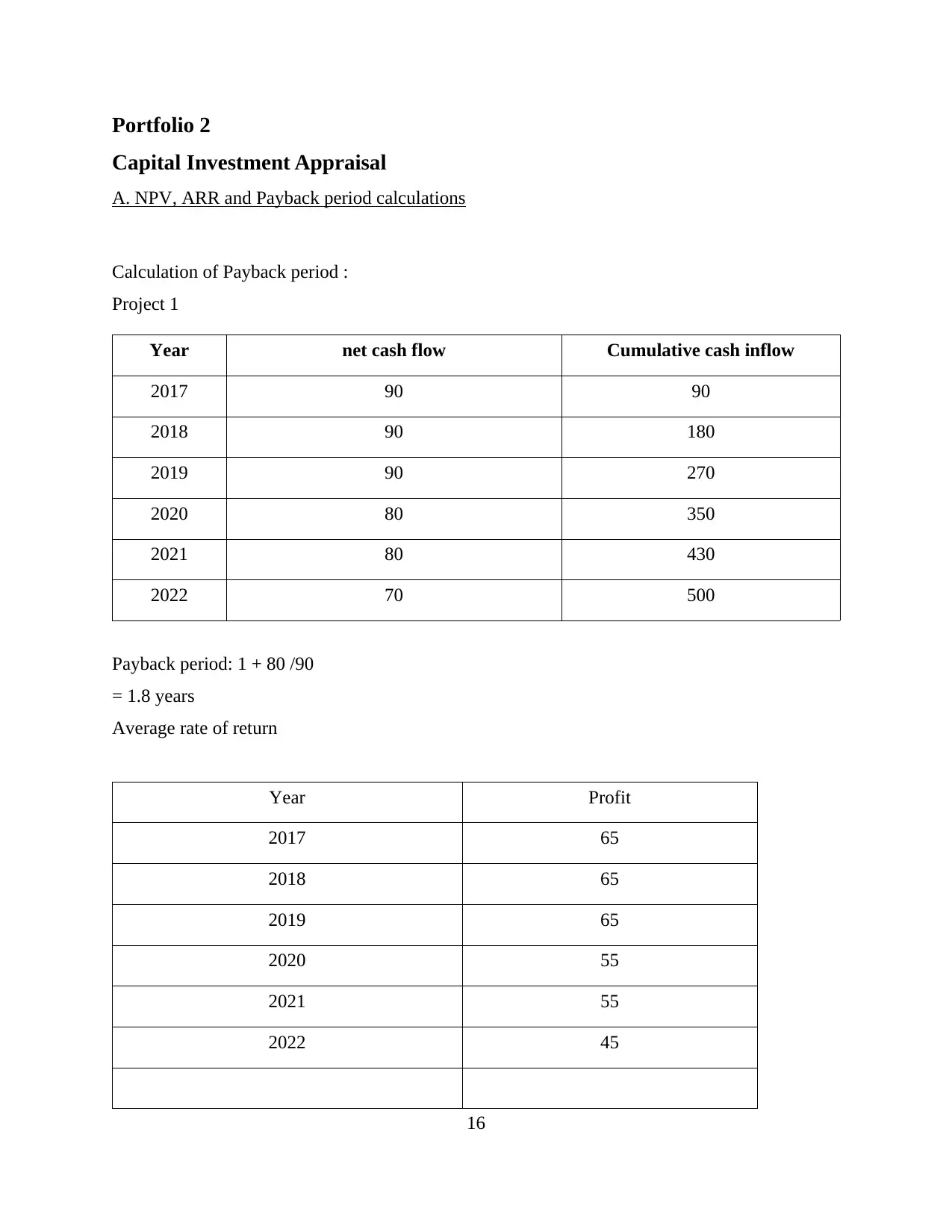

Capital Investment Appraisal

A. NPV, ARR and Payback period calculations

Calculation of Payback period :

Project 1

Year net cash flow Cumulative cash inflow

2017 90 90

2018 90 180

2019 90 270

2020 80 350

2021 80 430

2022 70 500

Payback period: 1 + 80 /90

= 1.8 years

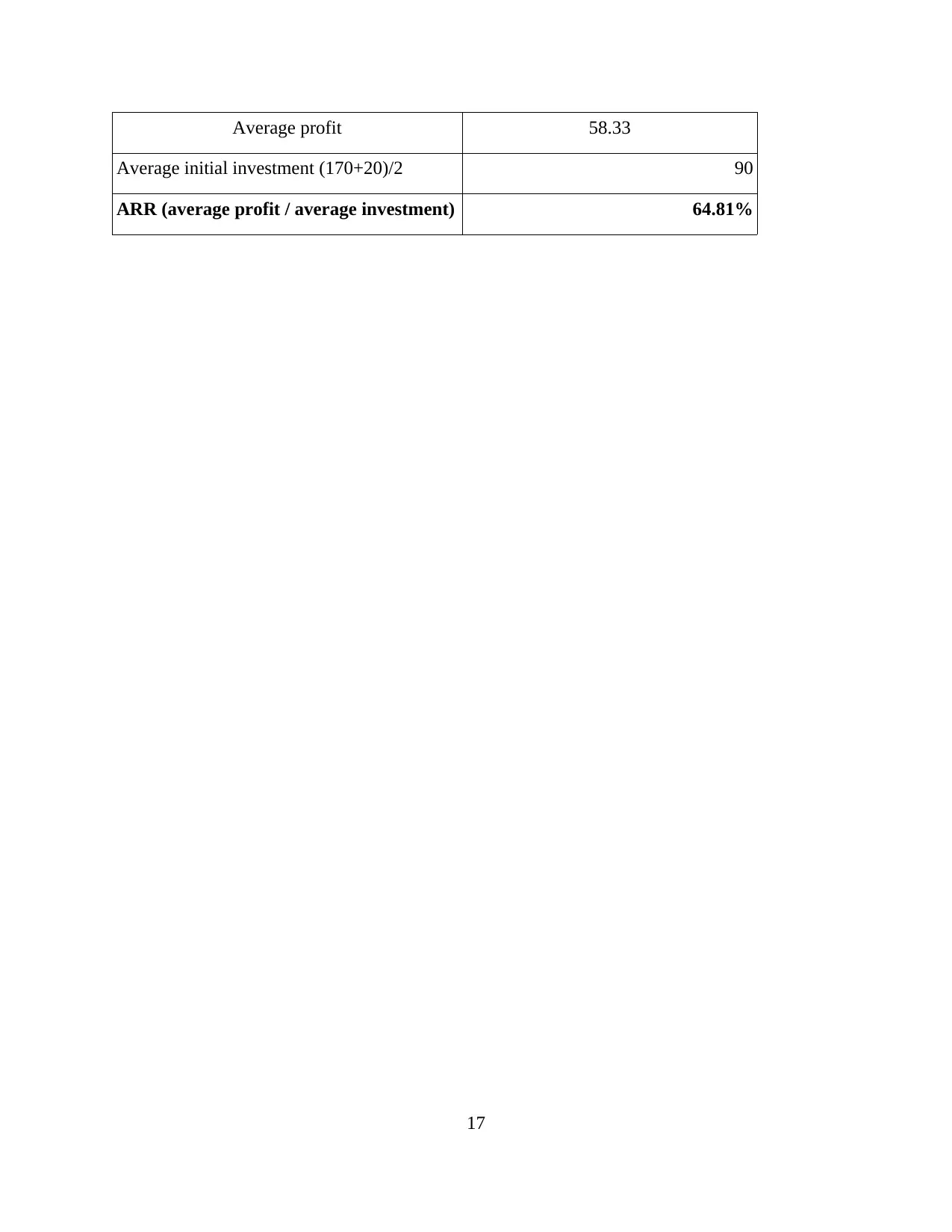

Average rate of return

Year Profit

2017 65

2018 65

2019 65

2020 55

2021 55

2022 45

16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Average initial investment (170+20)/2 90

ARR (average profit / average investment) 64.81%

17

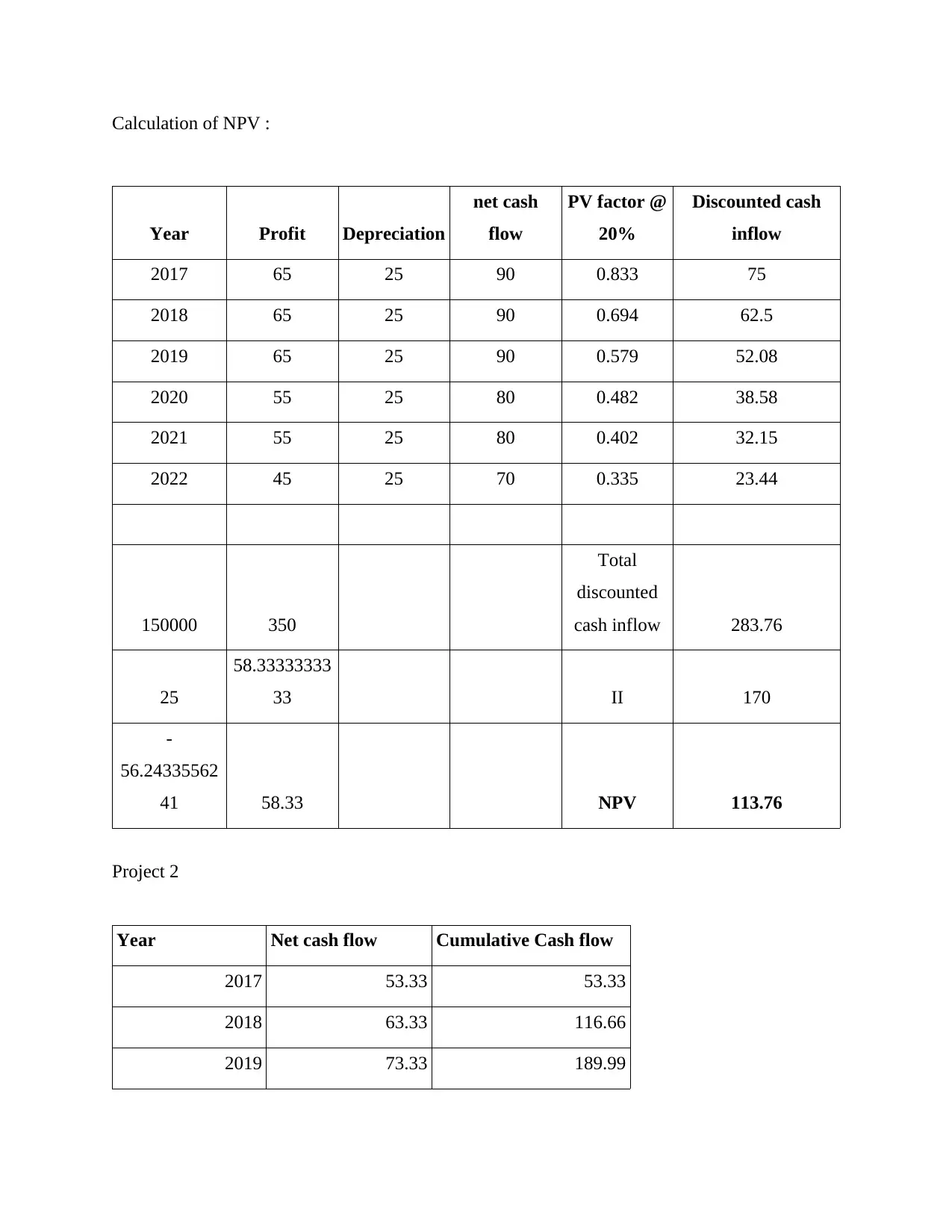

Paraphrase This Document

Year Profit Depreciation

net cash

flow

PV factor @

20%

Discounted cash

inflow

2017 65 25 90 0.833 75

2018 65 25 90 0.694 62.5

2019 65 25 90 0.579 52.08

2020 55 25 80 0.482 38.58

2021 55 25 80 0.402 32.15

2022 45 25 70 0.335 23.44

150000 350

Total

discounted

cash inflow 283.76

25

58.33333333

33 II 170

-

56.24335562

41 58.33 NPV 113.76

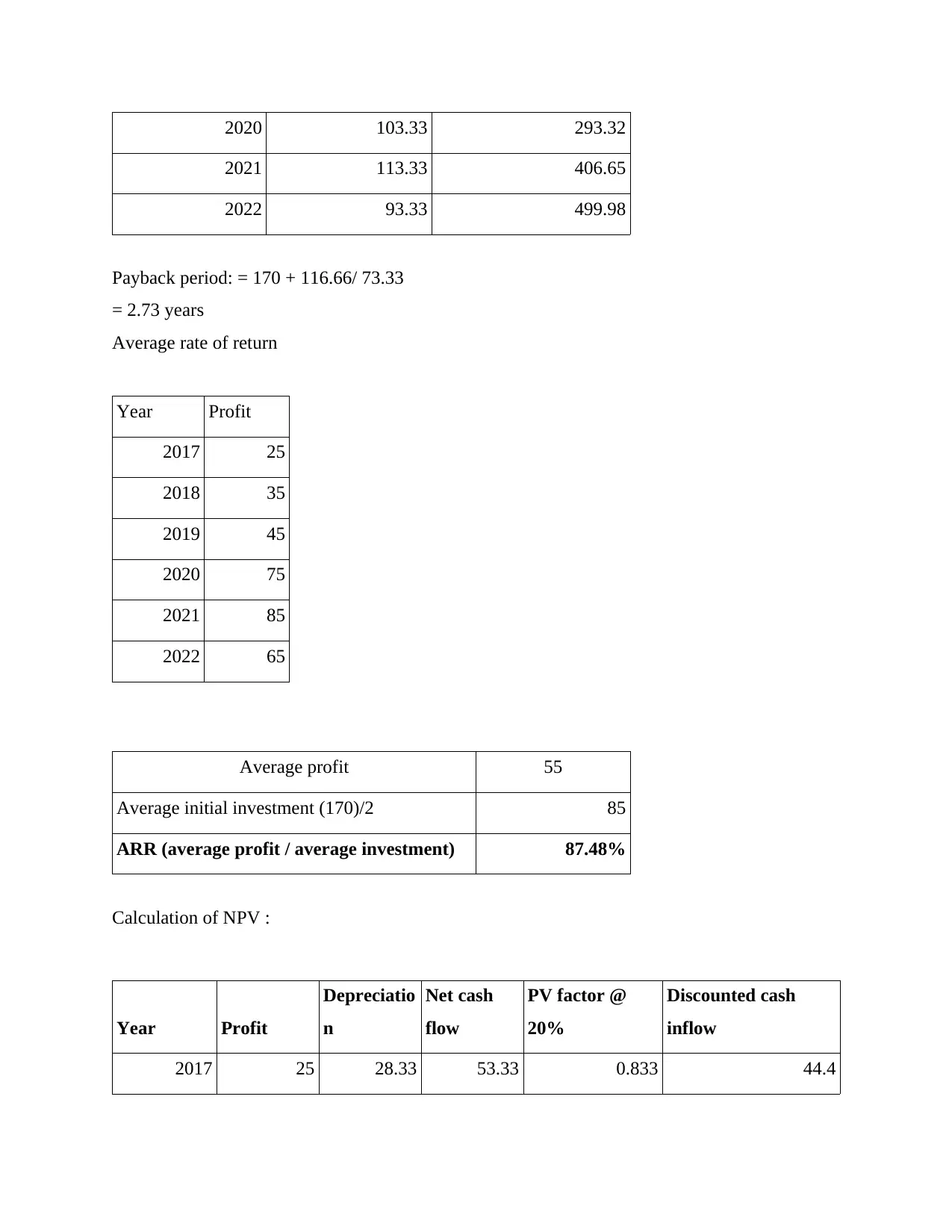

Project 2

Year Net cash flow Cumulative Cash flow

2017 53.33 53.33

2018 63.33 116.66

2019 73.33 189.99

2021 113.33 406.65

2022 93.33 499.98

Payback period: = 170 + 116.66/ 73.33

= 2.73 years

Average rate of return

Year Profit

2017 25

2018 35

2019 45

2020 75

2021 85

2022 65

Average profit 55

Average initial investment (170)/2 85

ARR (average profit / average investment) 87.48%

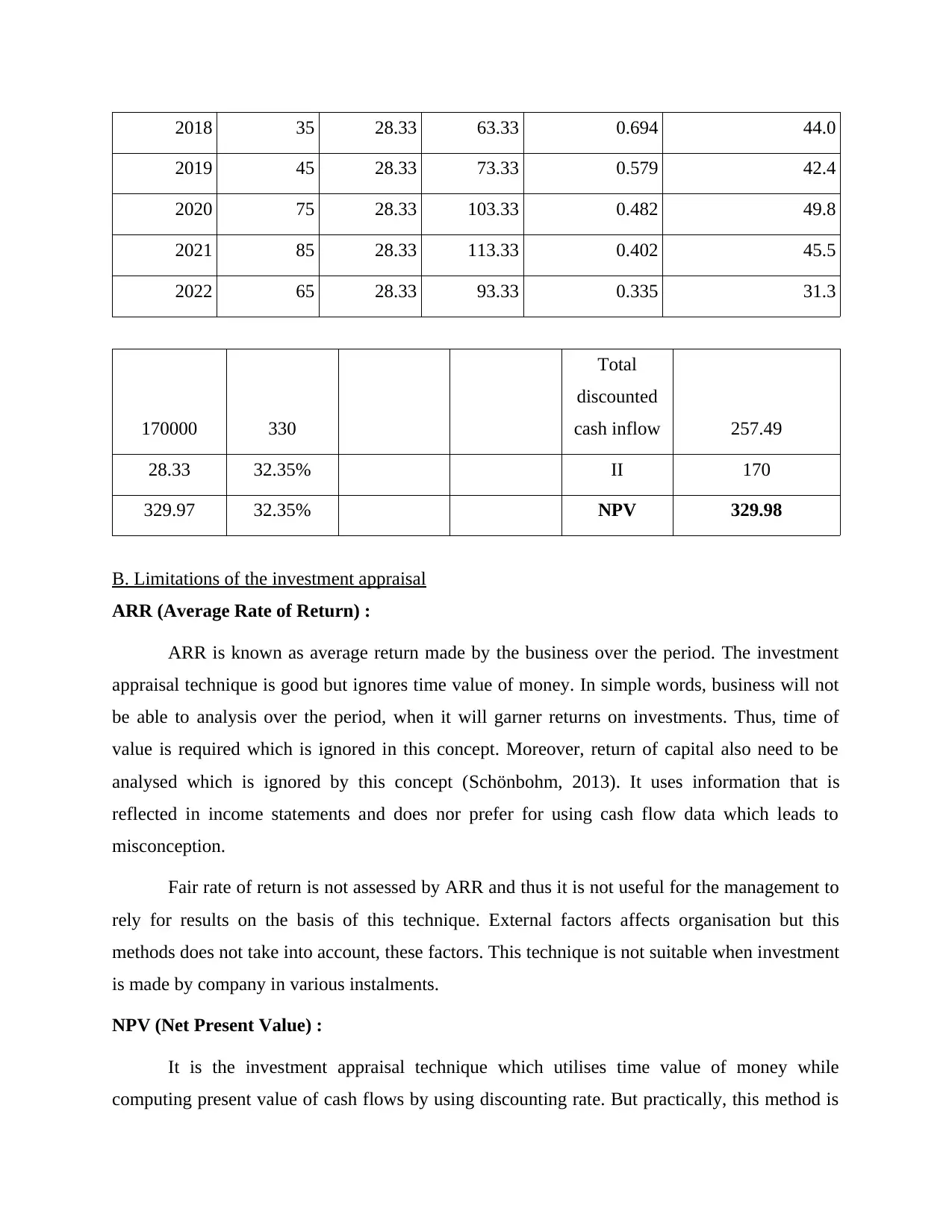

Calculation of NPV :

Year Profit

Depreciatio

n

Net cash

flow

PV factor @

20%

Discounted cash

inflow

2017 25 28.33 53.33 0.833 44.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2019 45 28.33 73.33 0.579 42.4

2020 75 28.33 103.33 0.482 49.8

2021 85 28.33 113.33 0.402 45.5

2022 65 28.33 93.33 0.335 31.3

170000 330

Total

discounted

cash inflow 257.49

28.33 32.35% II 170

329.97 32.35% NPV 329.98

B. Limitations of the investment appraisal

ARR (Average Rate of Return) :

ARR is known as average return made by the business over the period. The investment

appraisal technique is good but ignores time value of money. In simple words, business will not

be able to analysis over the period, when it will garner returns on investments. Thus, time of

value is required which is ignored in this concept. Moreover, return of capital also need to be

analysed which is ignored by this concept (Schönbohm, 2013). It uses information that is

reflected in income statements and does nor prefer for using cash flow data which leads to

misconception.

Fair rate of return is not assessed by ARR and thus it is not useful for the management to

rely for results on the basis of this technique. External factors affects organisation but this

methods does not take into account, these factors. This technique is not suitable when investment

is made by company in various instalments.

NPV (Net Present Value) :

It is the investment appraisal technique which utilises time value of money while

computing present value of cash flows by using discounting rate. But practically, this method is

Paraphrase This Document

Moreover, if amount of mutually exclusive projects are not similar, then inaccurate conclusions

are ascertained which are not useful for the company. Furthermore, this method uses discounting

rate for calculation. This is difficult to compute perfect discounting rate in practical life.

NPV is not good to use for comparing two projects which are unequal. It is difficult to

give correct decision when projects are of different size and are unequal largely. It provides

results which are not accurate and as a result, investors does not rely completely on NPV

(Gunawardena and et.al, 2015). Moreover, it provides estimations related to calculation and as a

result, no concrete conclusions are provided that can be used by management of the company

regarding new investment.

Payback Period :

This method is used as it provides time when will returns be achieved by the business and

as a result, it provides better results to organisation. However, it has certain demerits as well. The

profitability factor is not given by this technique. It only provides when firm will gain results

within time, but how much profits will be garnered is not provided by this concept. As a result,

concrete conclusions are not provided by payback period and as such, management cannot make

better and effective decisions.

This method gives priority to liquidity but does not consider profitability and ignores it

(Meriç, Kamışlı and Temizel, 2017). Thus, profitability aspect is important but is ignored by this

concept. Another limitation of payback period is that it considers only cash flow which is

occurred before calculating payback period and ignores calculation of cash flow which is

occurred after payback period and as a result, improper conclusions are drawn which are not

helpful to company. These capital investment techniques are widely used by the companies but

has certain limitations as well.

CONCLUSION

Hereby it can be concluded that financial ratios are widely used by companies as it gives

them concrete results regarding profitability and efficiency of it with other companies as well. It

is primary and useful tool for making comparison with one another. Both companies such as

Sports direct plc and JD Sports plc are performing poorly in the market. It can be concluded that

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.