Portfolio Investment Management: Stock and ETF Analysis Report

VerifiedAdded on 2020/06/06

|15

|3614

|64

Report

AI Summary

This report provides a comprehensive analysis of portfolio investment management, focusing on the construction and evaluation of various portfolios. It begins with an introduction to portfolio investment, defining its objectives and components, and then proceeds to compute the risk and return of selected stocks (Genting Malaysia and PPB Group) and an Exchange Traded Fund (CIMB FTSE ASEAN 40 Malaysia). The report calculates monthly returns, expected returns using the CAPM model, and correlations between the assets. Subsequently, it constructs four distinct portfolios, each comprising different combinations of the stocks and the ETF. The risk and return of each portfolio are calculated and compared, enabling an assessment of the diversification benefits. The analysis includes a covariance matrix and concludes with a comparison of the portfolios' performance, offering insights into effective portfolio management strategies.

PORTFOLIO INVESTMENT

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Computation of risk and return of common stock & exchange traded fund................................1

Calculation of monthly return on Stock 1 and 2..........................................................................2

Calculation of monthly return on CIMB FTSE Asean 40 Malaysia ETF....................................4

Calculation of correlation between Genting Group and PPB Group...........................................5

Calculation of correlation between Genting Group and CIMB FTSE ASEAN 40 Malaysia......5

Calculation of correlation between PPB Group and CIMB FTSE ASEAN 40 Malaysia............6

PORTFOLIO CONSTRUCTION...................................................................................................7

Portfolio 1: Stock 1 and ETF.......................................................................................................7

Portfolio 2: Stock 2 and ETF.......................................................................................................7

Portfolio 3: Stock 1 and stock 2...................................................................................................8

Portfolio 4: Stock 1, Stock 2 and ETF.........................................................................................8

COMPARISON OF RISK OF THE PORTFOLIOS.......................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Computation of risk and return of common stock & exchange traded fund................................1

Calculation of monthly return on Stock 1 and 2..........................................................................2

Calculation of monthly return on CIMB FTSE Asean 40 Malaysia ETF....................................4

Calculation of correlation between Genting Group and PPB Group...........................................5

Calculation of correlation between Genting Group and CIMB FTSE ASEAN 40 Malaysia......5

Calculation of correlation between PPB Group and CIMB FTSE ASEAN 40 Malaysia............6

PORTFOLIO CONSTRUCTION...................................................................................................7

Portfolio 1: Stock 1 and ETF.......................................................................................................7

Portfolio 2: Stock 2 and ETF.......................................................................................................7

Portfolio 3: Stock 1 and stock 2...................................................................................................8

Portfolio 4: Stock 1, Stock 2 and ETF.........................................................................................8

COMPARISON OF RISK OF THE PORTFOLIOS.......................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Index of tables

Table 1 Calculation of monthly return of Genting Malaysia and PPB Group.................................2

Table 2 Calculation of expected return on Genting Malaysia.........................................................4

Table 3 Calculation of expected return on PPB Group...................................................................4

Table 4 Calculation of monthly return on CIMB FTSE ASEAN 40 Malaysia...............................4

Table 5 Calculation of correlation between PPB Group & Genting Group....................................5

Table 6 Calculation of correlation between Genting Group & ETF...............................................5

Table 7 Calculation of correlation PPB Group and ETF.................................................................6

Table 8 Calculation of risk and return of portfolio 1.......................................................................7

Table 9 Calculation of return and risk of portfolio 2.......................................................................7

Table 10 Calculation of risk and return of portfolio 3.....................................................................8

Table 11 Calculation of return and risk of portfolio 4.....................................................................8

Table 12 Covariance matrix.............................................................................................................8

Table 1 Calculation of monthly return of Genting Malaysia and PPB Group.................................2

Table 2 Calculation of expected return on Genting Malaysia.........................................................4

Table 3 Calculation of expected return on PPB Group...................................................................4

Table 4 Calculation of monthly return on CIMB FTSE ASEAN 40 Malaysia...............................4

Table 5 Calculation of correlation between PPB Group & Genting Group....................................5

Table 6 Calculation of correlation between Genting Group & ETF...............................................5

Table 7 Calculation of correlation PPB Group and ETF.................................................................6

Table 8 Calculation of risk and return of portfolio 1.......................................................................7

Table 9 Calculation of return and risk of portfolio 2.......................................................................7

Table 10 Calculation of risk and return of portfolio 3.....................................................................8

Table 11 Calculation of return and risk of portfolio 4.....................................................................8

Table 12 Covariance matrix.............................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Portfolio investment refers to the investment made by investor in different securities i.e.

Exchange traded fund, money market securities, fixed income securities, equity funds and others

with the aim of receiving target return. Thus, portfolio consists of different type of assets i.e.

equity includes ordinary stock and debt i.e. bonds, debentures, banknotes and others (Leung, S.L

and et.al., 2016). Investment in different securities usually involves both risk and return

therefore, it is essential for the investor to make appropriate decisions regarding their assets

allocation and others so as to manage portfolio risk and earn good return. The present report lay

emphasizes upon creation of an efficient portfolio comprising the stock of two Malaysian

companies named Genting Malaysia and PPB Group listed on FTSE Bursa Malaysia Index

KLCI. Moreover, an ETFA CIMB FTSE ASEAN 40 Malaysia also have been incorporated for

the portfolio construction.

Computation of risk and return of common stock & exchange traded fund

Companies selected for the portfolio creation

Companies Industry

Genting Malaysia Berhad Real Estate

PPB Group Conglomerate industry

CIMB FTSE ASEAN 40 Malaysia Exchange Traded fund (ETF)

Genting Malaysia Bhd is a public limited company which is founded in the year 1980. It

provides hospitality and leisure service to the consumers i.e. hotel accommodation, gaming,

entertainment and others. It has two operational segments one is leisure and hospitality and

another is properties. First is involved in delivering travel and tourism related services whereas

second segment is engaged in property investment, development and its management.

PPB Group Bhd is a conglomerate company which is listed on FTSE Bursa Malaysia

KLCI and engaged in food production, property investment, waste management, and agriculture

and property development functions.

ETFA CIMB FTSE ASEAN 40 Malaysia ETF is a composition of the market value of

the biggest 40 businesses listed on the Indonesia, Malaysia, Philippines Singapore & Thailand’s

1

Portfolio investment refers to the investment made by investor in different securities i.e.

Exchange traded fund, money market securities, fixed income securities, equity funds and others

with the aim of receiving target return. Thus, portfolio consists of different type of assets i.e.

equity includes ordinary stock and debt i.e. bonds, debentures, banknotes and others (Leung, S.L

and et.al., 2016). Investment in different securities usually involves both risk and return

therefore, it is essential for the investor to make appropriate decisions regarding their assets

allocation and others so as to manage portfolio risk and earn good return. The present report lay

emphasizes upon creation of an efficient portfolio comprising the stock of two Malaysian

companies named Genting Malaysia and PPB Group listed on FTSE Bursa Malaysia Index

KLCI. Moreover, an ETFA CIMB FTSE ASEAN 40 Malaysia also have been incorporated for

the portfolio construction.

Computation of risk and return of common stock & exchange traded fund

Companies selected for the portfolio creation

Companies Industry

Genting Malaysia Berhad Real Estate

PPB Group Conglomerate industry

CIMB FTSE ASEAN 40 Malaysia Exchange Traded fund (ETF)

Genting Malaysia Bhd is a public limited company which is founded in the year 1980. It

provides hospitality and leisure service to the consumers i.e. hotel accommodation, gaming,

entertainment and others. It has two operational segments one is leisure and hospitality and

another is properties. First is involved in delivering travel and tourism related services whereas

second segment is engaged in property investment, development and its management.

PPB Group Bhd is a conglomerate company which is listed on FTSE Bursa Malaysia

KLCI and engaged in food production, property investment, waste management, and agriculture

and property development functions.

ETFA CIMB FTSE ASEAN 40 Malaysia ETF is a composition of the market value of

the biggest 40 businesses listed on the Indonesia, Malaysia, Philippines Singapore & Thailand’s

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

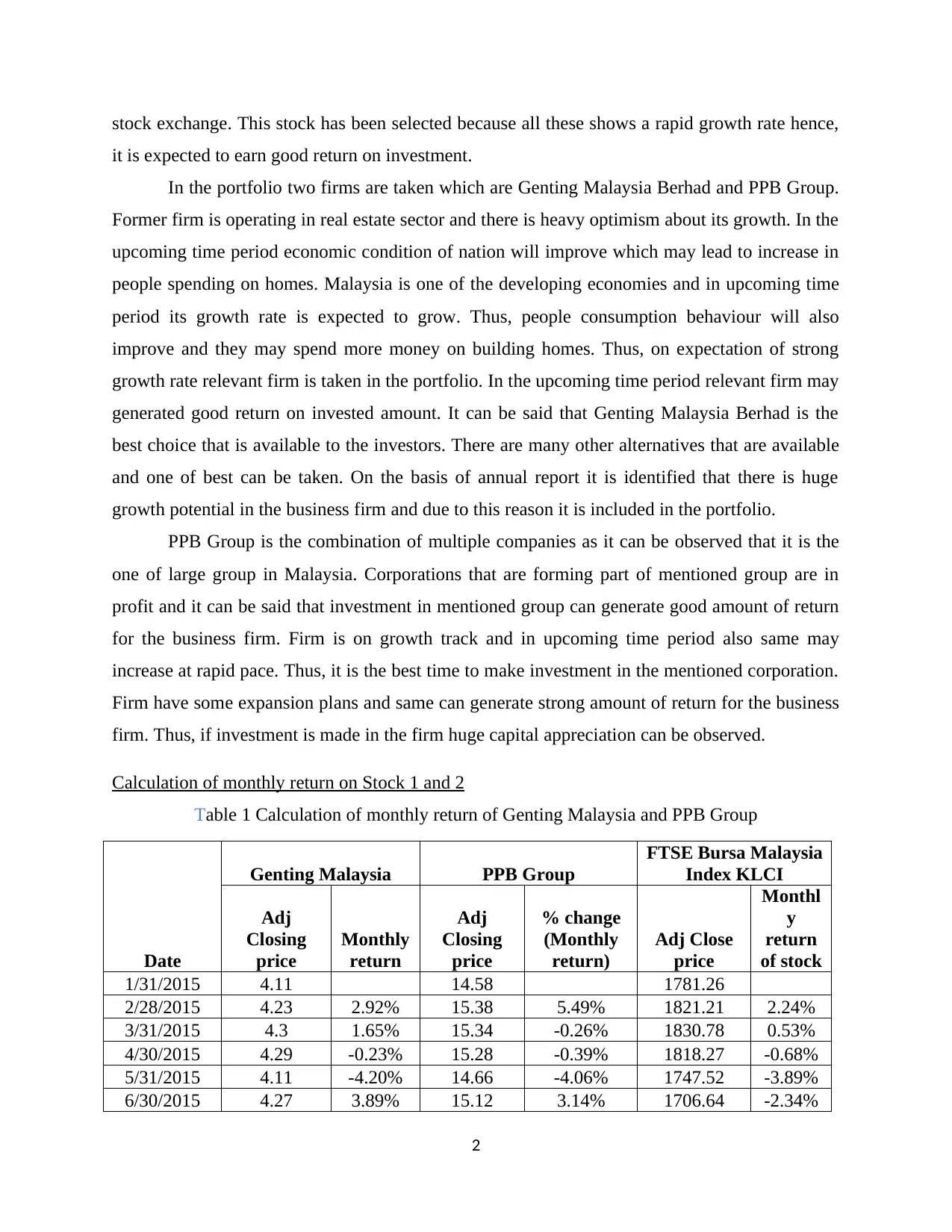

stock exchange. This stock has been selected because all these shows a rapid growth rate hence,

it is expected to earn good return on investment.

In the portfolio two firms are taken which are Genting Malaysia Berhad and PPB Group.

Former firm is operating in real estate sector and there is heavy optimism about its growth. In the

upcoming time period economic condition of nation will improve which may lead to increase in

people spending on homes. Malaysia is one of the developing economies and in upcoming time

period its growth rate is expected to grow. Thus, people consumption behaviour will also

improve and they may spend more money on building homes. Thus, on expectation of strong

growth rate relevant firm is taken in the portfolio. In the upcoming time period relevant firm may

generated good return on invested amount. It can be said that Genting Malaysia Berhad is the

best choice that is available to the investors. There are many other alternatives that are available

and one of best can be taken. On the basis of annual report it is identified that there is huge

growth potential in the business firm and due to this reason it is included in the portfolio.

PPB Group is the combination of multiple companies as it can be observed that it is the

one of large group in Malaysia. Corporations that are forming part of mentioned group are in

profit and it can be said that investment in mentioned group can generate good amount of return

for the business firm. Firm is on growth track and in upcoming time period also same may

increase at rapid pace. Thus, it is the best time to make investment in the mentioned corporation.

Firm have some expansion plans and same can generate strong amount of return for the business

firm. Thus, if investment is made in the firm huge capital appreciation can be observed.

Calculation of monthly return on Stock 1 and 2

Table 1 Calculation of monthly return of Genting Malaysia and PPB Group

Date

Genting Malaysia PPB Group

FTSE Bursa Malaysia

Index KLCI

Adj

Closing

price

Monthly

return

Adj

Closing

price

% change

(Monthly

return)

Adj Close

price

Monthl

y

return

of stock

1/31/2015 4.11 14.58 1781.26

2/28/2015 4.23 2.92% 15.38 5.49% 1821.21 2.24%

3/31/2015 4.3 1.65% 15.34 -0.26% 1830.78 0.53%

4/30/2015 4.29 -0.23% 15.28 -0.39% 1818.27 -0.68%

5/31/2015 4.11 -4.20% 14.66 -4.06% 1747.52 -3.89%

6/30/2015 4.27 3.89% 15.12 3.14% 1706.64 -2.34%

2

it is expected to earn good return on investment.

In the portfolio two firms are taken which are Genting Malaysia Berhad and PPB Group.

Former firm is operating in real estate sector and there is heavy optimism about its growth. In the

upcoming time period economic condition of nation will improve which may lead to increase in

people spending on homes. Malaysia is one of the developing economies and in upcoming time

period its growth rate is expected to grow. Thus, people consumption behaviour will also

improve and they may spend more money on building homes. Thus, on expectation of strong

growth rate relevant firm is taken in the portfolio. In the upcoming time period relevant firm may

generated good return on invested amount. It can be said that Genting Malaysia Berhad is the

best choice that is available to the investors. There are many other alternatives that are available

and one of best can be taken. On the basis of annual report it is identified that there is huge

growth potential in the business firm and due to this reason it is included in the portfolio.

PPB Group is the combination of multiple companies as it can be observed that it is the

one of large group in Malaysia. Corporations that are forming part of mentioned group are in

profit and it can be said that investment in mentioned group can generate good amount of return

for the business firm. Firm is on growth track and in upcoming time period also same may

increase at rapid pace. Thus, it is the best time to make investment in the mentioned corporation.

Firm have some expansion plans and same can generate strong amount of return for the business

firm. Thus, if investment is made in the firm huge capital appreciation can be observed.

Calculation of monthly return on Stock 1 and 2

Table 1 Calculation of monthly return of Genting Malaysia and PPB Group

Date

Genting Malaysia PPB Group

FTSE Bursa Malaysia

Index KLCI

Adj

Closing

price

Monthly

return

Adj

Closing

price

% change

(Monthly

return)

Adj Close

price

Monthl

y

return

of stock

1/31/2015 4.11 14.58 1781.26

2/28/2015 4.23 2.92% 15.38 5.49% 1821.21 2.24%

3/31/2015 4.3 1.65% 15.34 -0.26% 1830.78 0.53%

4/30/2015 4.29 -0.23% 15.28 -0.39% 1818.27 -0.68%

5/31/2015 4.11 -4.20% 14.66 -4.06% 1747.52 -3.89%

6/30/2015 4.27 3.89% 15.12 3.14% 1706.64 -2.34%

2

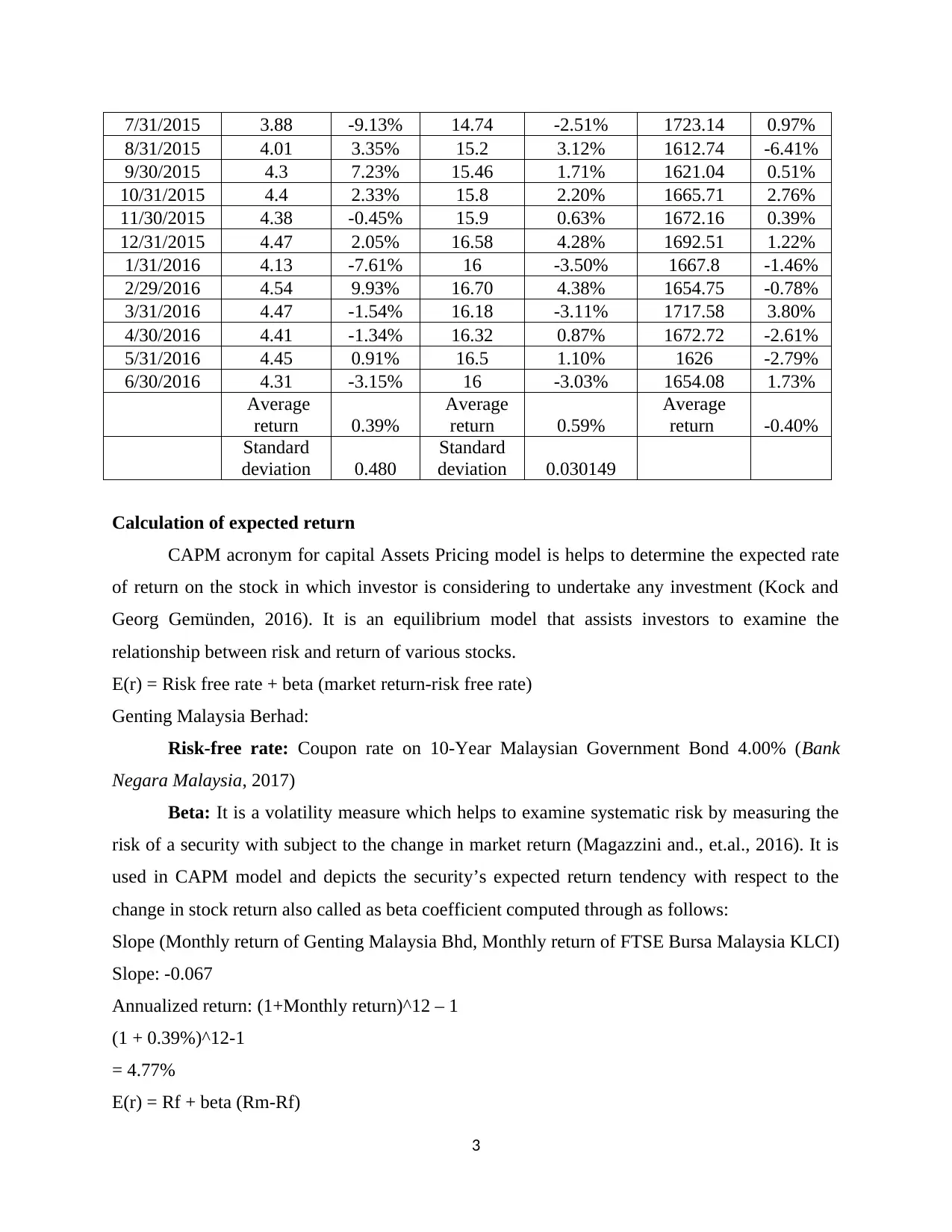

7/31/2015 3.88 -9.13% 14.74 -2.51% 1723.14 0.97%

8/31/2015 4.01 3.35% 15.2 3.12% 1612.74 -6.41%

9/30/2015 4.3 7.23% 15.46 1.71% 1621.04 0.51%

10/31/2015 4.4 2.33% 15.8 2.20% 1665.71 2.76%

11/30/2015 4.38 -0.45% 15.9 0.63% 1672.16 0.39%

12/31/2015 4.47 2.05% 16.58 4.28% 1692.51 1.22%

1/31/2016 4.13 -7.61% 16 -3.50% 1667.8 -1.46%

2/29/2016 4.54 9.93% 16.70 4.38% 1654.75 -0.78%

3/31/2016 4.47 -1.54% 16.18 -3.11% 1717.58 3.80%

4/30/2016 4.41 -1.34% 16.32 0.87% 1672.72 -2.61%

5/31/2016 4.45 0.91% 16.5 1.10% 1626 -2.79%

6/30/2016 4.31 -3.15% 16 -3.03% 1654.08 1.73%

Average

return 0.39%

Average

return 0.59%

Average

return -0.40%

Standard

deviation 0.480

Standard

deviation 0.030149

Calculation of expected return

CAPM acronym for capital Assets Pricing model is helps to determine the expected rate

of return on the stock in which investor is considering to undertake any investment (Kock and

Georg Gemünden, 2016). It is an equilibrium model that assists investors to examine the

relationship between risk and return of various stocks.

E(r) = Risk free rate + beta (market return-risk free rate)

Genting Malaysia Berhad:

Risk-free rate: Coupon rate on 10-Year Malaysian Government Bond 4.00% (Bank

Negara Malaysia, 2017)

Beta: It is a volatility measure which helps to examine systematic risk by measuring the

risk of a security with subject to the change in market return (Magazzini and., et.al., 2016). It is

used in CAPM model and depicts the security’s expected return tendency with respect to the

change in stock return also called as beta coefficient computed through as follows:

Slope (Monthly return of Genting Malaysia Bhd, Monthly return of FTSE Bursa Malaysia KLCI)

Slope: -0.067

Annualized return: (1+Monthly return)^12 – 1

(1 + 0.39%)^12-1

= 4.77%

E(r) = Rf + beta (Rm-Rf)

3

8/31/2015 4.01 3.35% 15.2 3.12% 1612.74 -6.41%

9/30/2015 4.3 7.23% 15.46 1.71% 1621.04 0.51%

10/31/2015 4.4 2.33% 15.8 2.20% 1665.71 2.76%

11/30/2015 4.38 -0.45% 15.9 0.63% 1672.16 0.39%

12/31/2015 4.47 2.05% 16.58 4.28% 1692.51 1.22%

1/31/2016 4.13 -7.61% 16 -3.50% 1667.8 -1.46%

2/29/2016 4.54 9.93% 16.70 4.38% 1654.75 -0.78%

3/31/2016 4.47 -1.54% 16.18 -3.11% 1717.58 3.80%

4/30/2016 4.41 -1.34% 16.32 0.87% 1672.72 -2.61%

5/31/2016 4.45 0.91% 16.5 1.10% 1626 -2.79%

6/30/2016 4.31 -3.15% 16 -3.03% 1654.08 1.73%

Average

return 0.39%

Average

return 0.59%

Average

return -0.40%

Standard

deviation 0.480

Standard

deviation 0.030149

Calculation of expected return

CAPM acronym for capital Assets Pricing model is helps to determine the expected rate

of return on the stock in which investor is considering to undertake any investment (Kock and

Georg Gemünden, 2016). It is an equilibrium model that assists investors to examine the

relationship between risk and return of various stocks.

E(r) = Risk free rate + beta (market return-risk free rate)

Genting Malaysia Berhad:

Risk-free rate: Coupon rate on 10-Year Malaysian Government Bond 4.00% (Bank

Negara Malaysia, 2017)

Beta: It is a volatility measure which helps to examine systematic risk by measuring the

risk of a security with subject to the change in market return (Magazzini and., et.al., 2016). It is

used in CAPM model and depicts the security’s expected return tendency with respect to the

change in stock return also called as beta coefficient computed through as follows:

Slope (Monthly return of Genting Malaysia Bhd, Monthly return of FTSE Bursa Malaysia KLCI)

Slope: -0.067

Annualized return: (1+Monthly return)^12 – 1

(1 + 0.39%)^12-1

= 4.77%

E(r) = Rf + beta (Rm-Rf)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

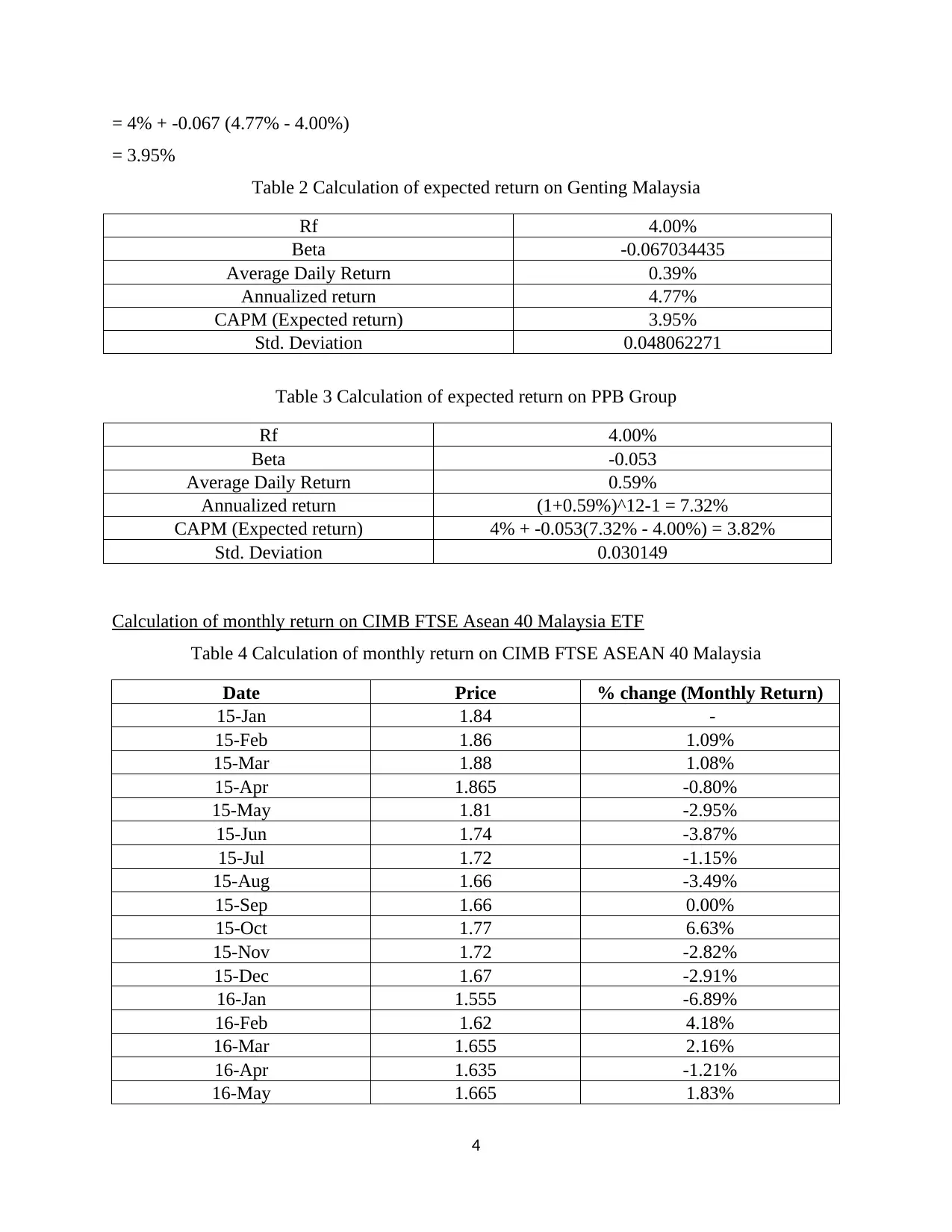

= 4% + -0.067 (4.77% - 4.00%)

= 3.95%

Table 2 Calculation of expected return on Genting Malaysia

Rf 4.00%

Beta -0.067034435

Average Daily Return 0.39%

Annualized return 4.77%

CAPM (Expected return) 3.95%

Std. Deviation 0.048062271

Table 3 Calculation of expected return on PPB Group

Rf 4.00%

Beta -0.053

Average Daily Return 0.59%

Annualized return (1+0.59%)^12-1 = 7.32%

CAPM (Expected return) 4% + -0.053(7.32% - 4.00%) = 3.82%

Std. Deviation 0.030149

Calculation of monthly return on CIMB FTSE Asean 40 Malaysia ETF

Table 4 Calculation of monthly return on CIMB FTSE ASEAN 40 Malaysia

Date Price % change (Monthly Return)

15-Jan 1.84 -

15-Feb 1.86 1.09%

15-Mar 1.88 1.08%

15-Apr 1.865 -0.80%

15-May 1.81 -2.95%

15-Jun 1.74 -3.87%

15-Jul 1.72 -1.15%

15-Aug 1.66 -3.49%

15-Sep 1.66 0.00%

15-Oct 1.77 6.63%

15-Nov 1.72 -2.82%

15-Dec 1.67 -2.91%

16-Jan 1.555 -6.89%

16-Feb 1.62 4.18%

16-Mar 1.655 2.16%

16-Apr 1.635 -1.21%

16-May 1.665 1.83%

4

= 3.95%

Table 2 Calculation of expected return on Genting Malaysia

Rf 4.00%

Beta -0.067034435

Average Daily Return 0.39%

Annualized return 4.77%

CAPM (Expected return) 3.95%

Std. Deviation 0.048062271

Table 3 Calculation of expected return on PPB Group

Rf 4.00%

Beta -0.053

Average Daily Return 0.59%

Annualized return (1+0.59%)^12-1 = 7.32%

CAPM (Expected return) 4% + -0.053(7.32% - 4.00%) = 3.82%

Std. Deviation 0.030149

Calculation of monthly return on CIMB FTSE Asean 40 Malaysia ETF

Table 4 Calculation of monthly return on CIMB FTSE ASEAN 40 Malaysia

Date Price % change (Monthly Return)

15-Jan 1.84 -

15-Feb 1.86 1.09%

15-Mar 1.88 1.08%

15-Apr 1.865 -0.80%

15-May 1.81 -2.95%

15-Jun 1.74 -3.87%

15-Jul 1.72 -1.15%

15-Aug 1.66 -3.49%

15-Sep 1.66 0.00%

15-Oct 1.77 6.63%

15-Nov 1.72 -2.82%

15-Dec 1.67 -2.91%

16-Jan 1.555 -6.89%

16-Feb 1.62 4.18%

16-Mar 1.655 2.16%

16-Apr 1.635 -1.21%

16-May 1.665 1.83%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

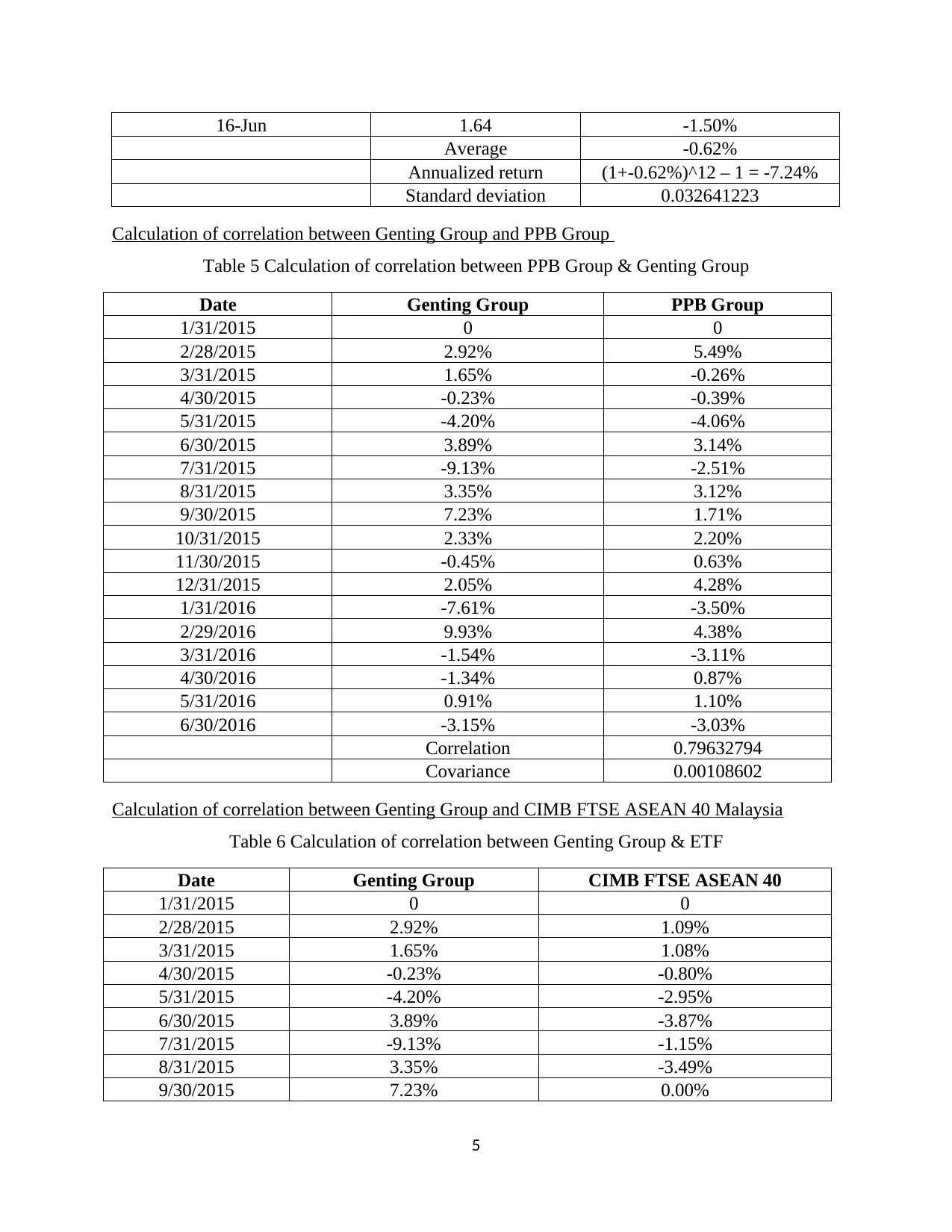

16-Jun 1.64 -1.50%

Average -0.62%

Annualized return (1+-0.62%)^12 – 1 = -7.24%

Standard deviation 0.032641223

Calculation of correlation between Genting Group and PPB Group

Table 5 Calculation of correlation between PPB Group & Genting Group

Date Genting Group PPB Group

1/31/2015 0 0

2/28/2015 2.92% 5.49%

3/31/2015 1.65% -0.26%

4/30/2015 -0.23% -0.39%

5/31/2015 -4.20% -4.06%

6/30/2015 3.89% 3.14%

7/31/2015 -9.13% -2.51%

8/31/2015 3.35% 3.12%

9/30/2015 7.23% 1.71%

10/31/2015 2.33% 2.20%

11/30/2015 -0.45% 0.63%

12/31/2015 2.05% 4.28%

1/31/2016 -7.61% -3.50%

2/29/2016 9.93% 4.38%

3/31/2016 -1.54% -3.11%

4/30/2016 -1.34% 0.87%

5/31/2016 0.91% 1.10%

6/30/2016 -3.15% -3.03%

Correlation 0.79632794

Covariance 0.00108602

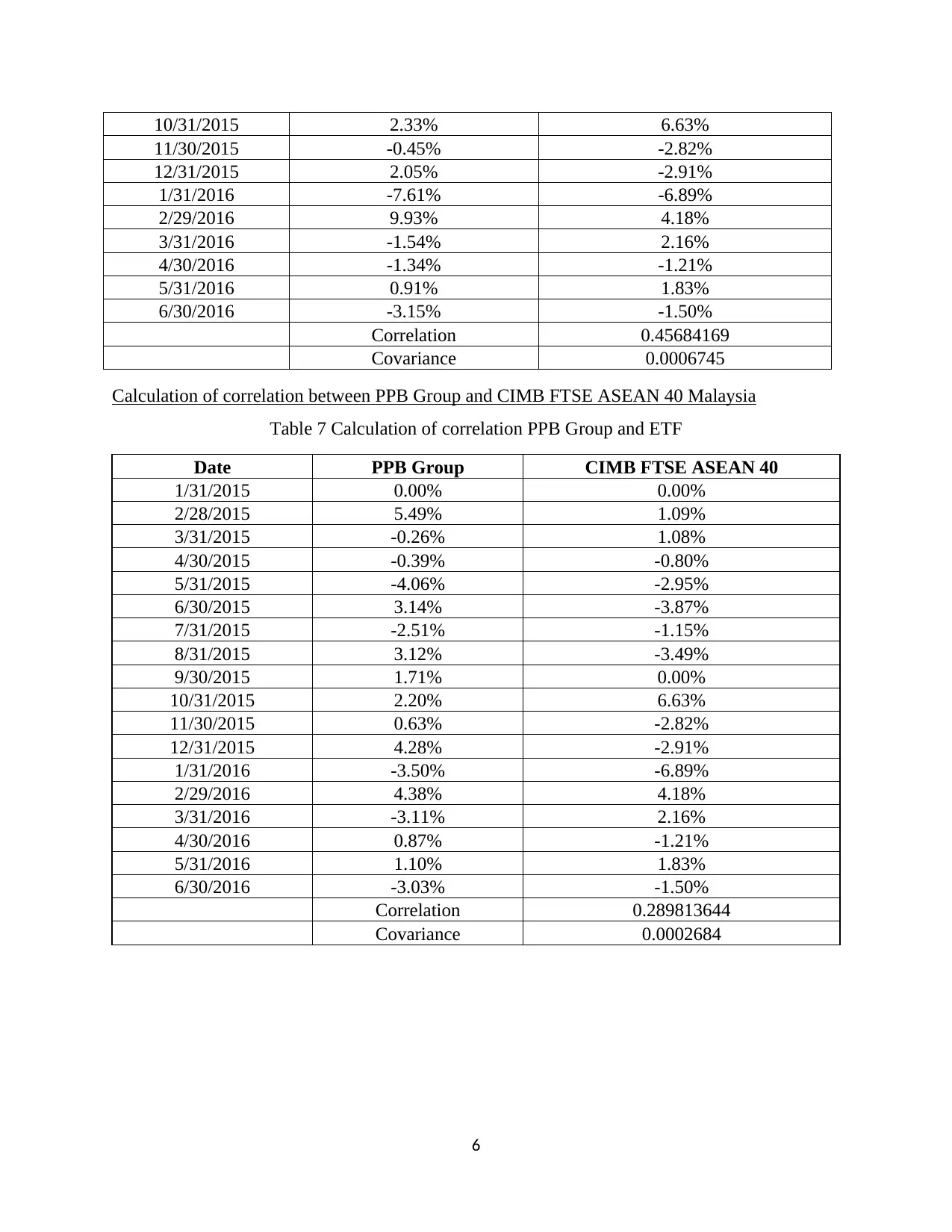

Calculation of correlation between Genting Group and CIMB FTSE ASEAN 40 Malaysia

Table 6 Calculation of correlation between Genting Group & ETF

Date Genting Group CIMB FTSE ASEAN 40

1/31/2015 0 0

2/28/2015 2.92% 1.09%

3/31/2015 1.65% 1.08%

4/30/2015 -0.23% -0.80%

5/31/2015 -4.20% -2.95%

6/30/2015 3.89% -3.87%

7/31/2015 -9.13% -1.15%

8/31/2015 3.35% -3.49%

9/30/2015 7.23% 0.00%

5

Average -0.62%

Annualized return (1+-0.62%)^12 – 1 = -7.24%

Standard deviation 0.032641223

Calculation of correlation between Genting Group and PPB Group

Table 5 Calculation of correlation between PPB Group & Genting Group

Date Genting Group PPB Group

1/31/2015 0 0

2/28/2015 2.92% 5.49%

3/31/2015 1.65% -0.26%

4/30/2015 -0.23% -0.39%

5/31/2015 -4.20% -4.06%

6/30/2015 3.89% 3.14%

7/31/2015 -9.13% -2.51%

8/31/2015 3.35% 3.12%

9/30/2015 7.23% 1.71%

10/31/2015 2.33% 2.20%

11/30/2015 -0.45% 0.63%

12/31/2015 2.05% 4.28%

1/31/2016 -7.61% -3.50%

2/29/2016 9.93% 4.38%

3/31/2016 -1.54% -3.11%

4/30/2016 -1.34% 0.87%

5/31/2016 0.91% 1.10%

6/30/2016 -3.15% -3.03%

Correlation 0.79632794

Covariance 0.00108602

Calculation of correlation between Genting Group and CIMB FTSE ASEAN 40 Malaysia

Table 6 Calculation of correlation between Genting Group & ETF

Date Genting Group CIMB FTSE ASEAN 40

1/31/2015 0 0

2/28/2015 2.92% 1.09%

3/31/2015 1.65% 1.08%

4/30/2015 -0.23% -0.80%

5/31/2015 -4.20% -2.95%

6/30/2015 3.89% -3.87%

7/31/2015 -9.13% -1.15%

8/31/2015 3.35% -3.49%

9/30/2015 7.23% 0.00%

5

10/31/2015 2.33% 6.63%

11/30/2015 -0.45% -2.82%

12/31/2015 2.05% -2.91%

1/31/2016 -7.61% -6.89%

2/29/2016 9.93% 4.18%

3/31/2016 -1.54% 2.16%

4/30/2016 -1.34% -1.21%

5/31/2016 0.91% 1.83%

6/30/2016 -3.15% -1.50%

Correlation 0.45684169

Covariance 0.0006745

Calculation of correlation between PPB Group and CIMB FTSE ASEAN 40 Malaysia

Table 7 Calculation of correlation PPB Group and ETF

Date PPB Group CIMB FTSE ASEAN 40

1/31/2015 0.00% 0.00%

2/28/2015 5.49% 1.09%

3/31/2015 -0.26% 1.08%

4/30/2015 -0.39% -0.80%

5/31/2015 -4.06% -2.95%

6/30/2015 3.14% -3.87%

7/31/2015 -2.51% -1.15%

8/31/2015 3.12% -3.49%

9/30/2015 1.71% 0.00%

10/31/2015 2.20% 6.63%

11/30/2015 0.63% -2.82%

12/31/2015 4.28% -2.91%

1/31/2016 -3.50% -6.89%

2/29/2016 4.38% 4.18%

3/31/2016 -3.11% 2.16%

4/30/2016 0.87% -1.21%

5/31/2016 1.10% 1.83%

6/30/2016 -3.03% -1.50%

Correlation 0.289813644

Covariance 0.0002684

6

11/30/2015 -0.45% -2.82%

12/31/2015 2.05% -2.91%

1/31/2016 -7.61% -6.89%

2/29/2016 9.93% 4.18%

3/31/2016 -1.54% 2.16%

4/30/2016 -1.34% -1.21%

5/31/2016 0.91% 1.83%

6/30/2016 -3.15% -1.50%

Correlation 0.45684169

Covariance 0.0006745

Calculation of correlation between PPB Group and CIMB FTSE ASEAN 40 Malaysia

Table 7 Calculation of correlation PPB Group and ETF

Date PPB Group CIMB FTSE ASEAN 40

1/31/2015 0.00% 0.00%

2/28/2015 5.49% 1.09%

3/31/2015 -0.26% 1.08%

4/30/2015 -0.39% -0.80%

5/31/2015 -4.06% -2.95%

6/30/2015 3.14% -3.87%

7/31/2015 -2.51% -1.15%

8/31/2015 3.12% -3.49%

9/30/2015 1.71% 0.00%

10/31/2015 2.20% 6.63%

11/30/2015 0.63% -2.82%

12/31/2015 4.28% -2.91%

1/31/2016 -3.50% -6.89%

2/29/2016 4.38% 4.18%

3/31/2016 -3.11% 2.16%

4/30/2016 0.87% -1.21%

5/31/2016 1.10% 1.83%

6/30/2016 -3.03% -1.50%

Correlation 0.289813644

Covariance 0.0002684

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

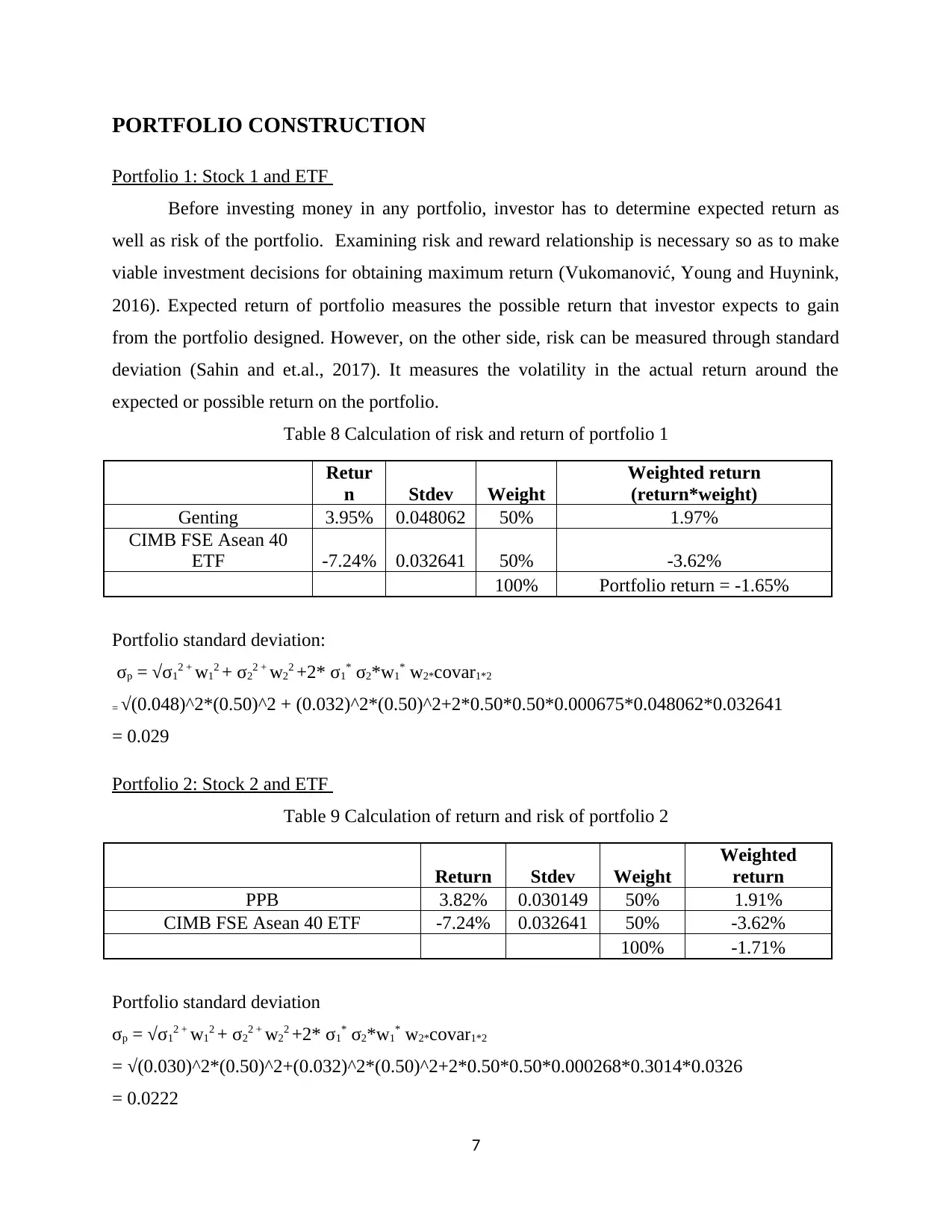

PORTFOLIO CONSTRUCTION

Portfolio 1: Stock 1 and ETF

Before investing money in any portfolio, investor has to determine expected return as

well as risk of the portfolio. Examining risk and reward relationship is necessary so as to make

viable investment decisions for obtaining maximum return (Vukomanović, Young and Huynink,

2016). Expected return of portfolio measures the possible return that investor expects to gain

from the portfolio designed. However, on the other side, risk can be measured through standard

deviation (Sahin and et.al., 2017). It measures the volatility in the actual return around the

expected or possible return on the portfolio.

Table 8 Calculation of risk and return of portfolio 1

Retur

n Stdev Weight

Weighted return

(return*weight)

Genting 3.95% 0.048062 50% 1.97%

CIMB FSE Asean 40

ETF -7.24% 0.032641 50% -3.62%

100% Portfolio return = -1.65%

Portfolio standard deviation:

σp = √σ12 + w12 + σ22 + w22 +2* σ1* σ2*w1* w2*covar1*2

= √(0.048)^2*(0.50)^2 + (0.032)^2*(0.50)^2+2*0.50*0.50*0.000675*0.048062*0.032641

= 0.029

Portfolio 2: Stock 2 and ETF

Table 9 Calculation of return and risk of portfolio 2

Return Stdev Weight

Weighted

return

PPB 3.82% 0.030149 50% 1.91%

CIMB FSE Asean 40 ETF -7.24% 0.032641 50% -3.62%

100% -1.71%

Portfolio standard deviation

σp = √σ12 + w12 + σ22 + w22 +2* σ1* σ2*w1* w2*covar1*2

= √(0.030)^2*(0.50)^2+(0.032)^2*(0.50)^2+2*0.50*0.50*0.000268*0.3014*0.0326

= 0.0222

7

Portfolio 1: Stock 1 and ETF

Before investing money in any portfolio, investor has to determine expected return as

well as risk of the portfolio. Examining risk and reward relationship is necessary so as to make

viable investment decisions for obtaining maximum return (Vukomanović, Young and Huynink,

2016). Expected return of portfolio measures the possible return that investor expects to gain

from the portfolio designed. However, on the other side, risk can be measured through standard

deviation (Sahin and et.al., 2017). It measures the volatility in the actual return around the

expected or possible return on the portfolio.

Table 8 Calculation of risk and return of portfolio 1

Retur

n Stdev Weight

Weighted return

(return*weight)

Genting 3.95% 0.048062 50% 1.97%

CIMB FSE Asean 40

ETF -7.24% 0.032641 50% -3.62%

100% Portfolio return = -1.65%

Portfolio standard deviation:

σp = √σ12 + w12 + σ22 + w22 +2* σ1* σ2*w1* w2*covar1*2

= √(0.048)^2*(0.50)^2 + (0.032)^2*(0.50)^2+2*0.50*0.50*0.000675*0.048062*0.032641

= 0.029

Portfolio 2: Stock 2 and ETF

Table 9 Calculation of return and risk of portfolio 2

Return Stdev Weight

Weighted

return

PPB 3.82% 0.030149 50% 1.91%

CIMB FSE Asean 40 ETF -7.24% 0.032641 50% -3.62%

100% -1.71%

Portfolio standard deviation

σp = √σ12 + w12 + σ22 + w22 +2* σ1* σ2*w1* w2*covar1*2

= √(0.030)^2*(0.50)^2+(0.032)^2*(0.50)^2+2*0.50*0.50*0.000268*0.3014*0.0326

= 0.0222

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

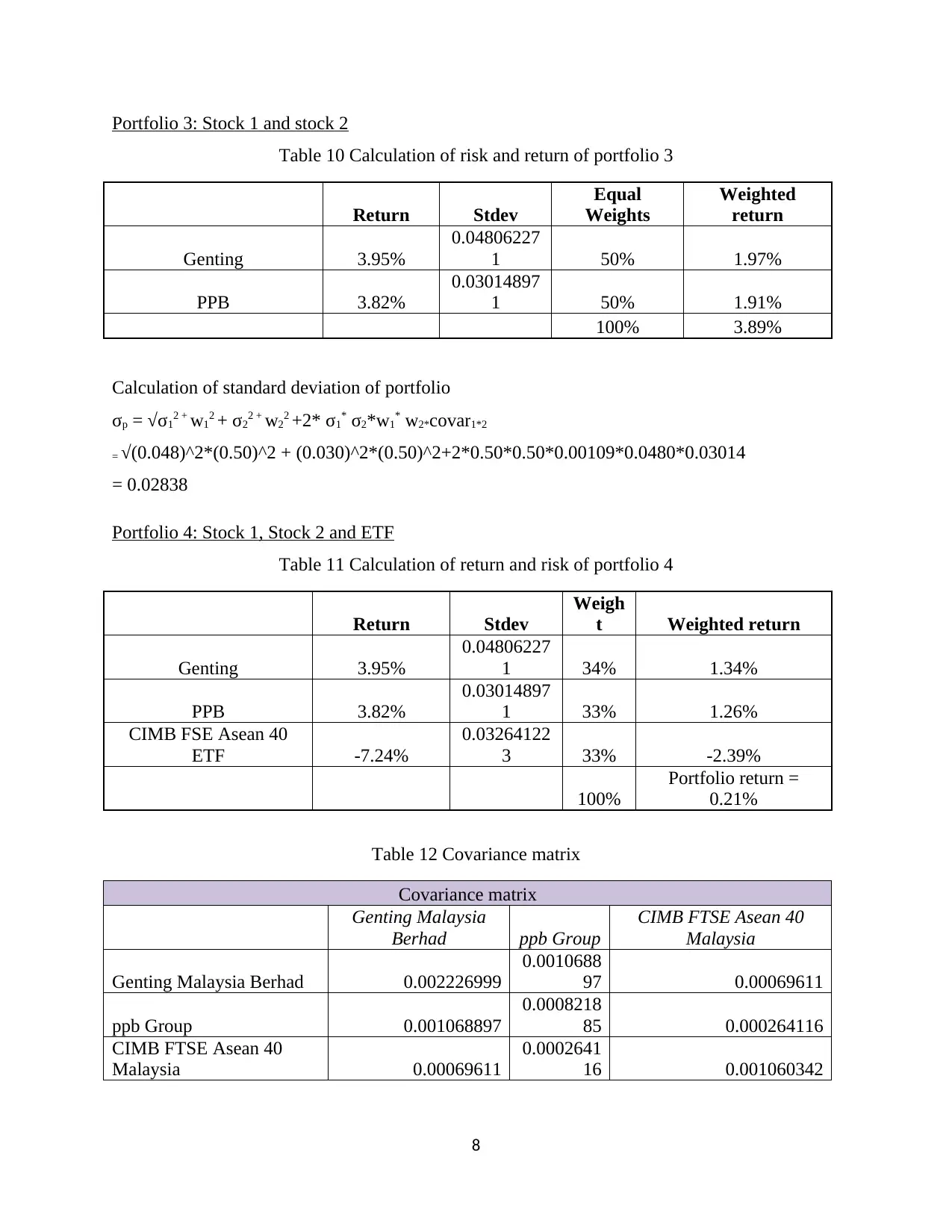

Portfolio 3: Stock 1 and stock 2

Table 10 Calculation of risk and return of portfolio 3

Return Stdev

Equal

Weights

Weighted

return

Genting 3.95%

0.04806227

1 50% 1.97%

PPB 3.82%

0.03014897

1 50% 1.91%

100% 3.89%

Calculation of standard deviation of portfolio

σp = √σ12 + w12 + σ22 + w22 +2* σ1* σ2*w1* w2*covar1*2

= √(0.048)^2*(0.50)^2 + (0.030)^2*(0.50)^2+2*0.50*0.50*0.00109*0.0480*0.03014

= 0.02838

Portfolio 4: Stock 1, Stock 2 and ETF

Table 11 Calculation of return and risk of portfolio 4

Return Stdev

Weigh

t Weighted return

Genting 3.95%

0.04806227

1 34% 1.34%

PPB 3.82%

0.03014897

1 33% 1.26%

CIMB FSE Asean 40

ETF -7.24%

0.03264122

3 33% -2.39%

100%

Portfolio return =

0.21%

Table 12 Covariance matrix

Covariance matrix

Genting Malaysia

Berhad ppb Group

CIMB FTSE Asean 40

Malaysia

Genting Malaysia Berhad 0.002226999

0.0010688

97 0.00069611

ppb Group 0.001068897

0.0008218

85 0.000264116

CIMB FTSE Asean 40

Malaysia 0.00069611

0.0002641

16 0.001060342

8

Table 10 Calculation of risk and return of portfolio 3

Return Stdev

Equal

Weights

Weighted

return

Genting 3.95%

0.04806227

1 50% 1.97%

PPB 3.82%

0.03014897

1 50% 1.91%

100% 3.89%

Calculation of standard deviation of portfolio

σp = √σ12 + w12 + σ22 + w22 +2* σ1* σ2*w1* w2*covar1*2

= √(0.048)^2*(0.50)^2 + (0.030)^2*(0.50)^2+2*0.50*0.50*0.00109*0.0480*0.03014

= 0.02838

Portfolio 4: Stock 1, Stock 2 and ETF

Table 11 Calculation of return and risk of portfolio 4

Return Stdev

Weigh

t Weighted return

Genting 3.95%

0.04806227

1 34% 1.34%

PPB 3.82%

0.03014897

1 33% 1.26%

CIMB FSE Asean 40

ETF -7.24%

0.03264122

3 33% -2.39%

100%

Portfolio return =

0.21%

Table 12 Covariance matrix

Covariance matrix

Genting Malaysia

Berhad ppb Group

CIMB FTSE Asean 40

Malaysia

Genting Malaysia Berhad 0.002226999

0.0010688

97 0.00069611

ppb Group 0.001068897

0.0008218

85 0.000264116

CIMB FTSE Asean 40

Malaysia 0.00069611

0.0002641

16 0.001060342

8

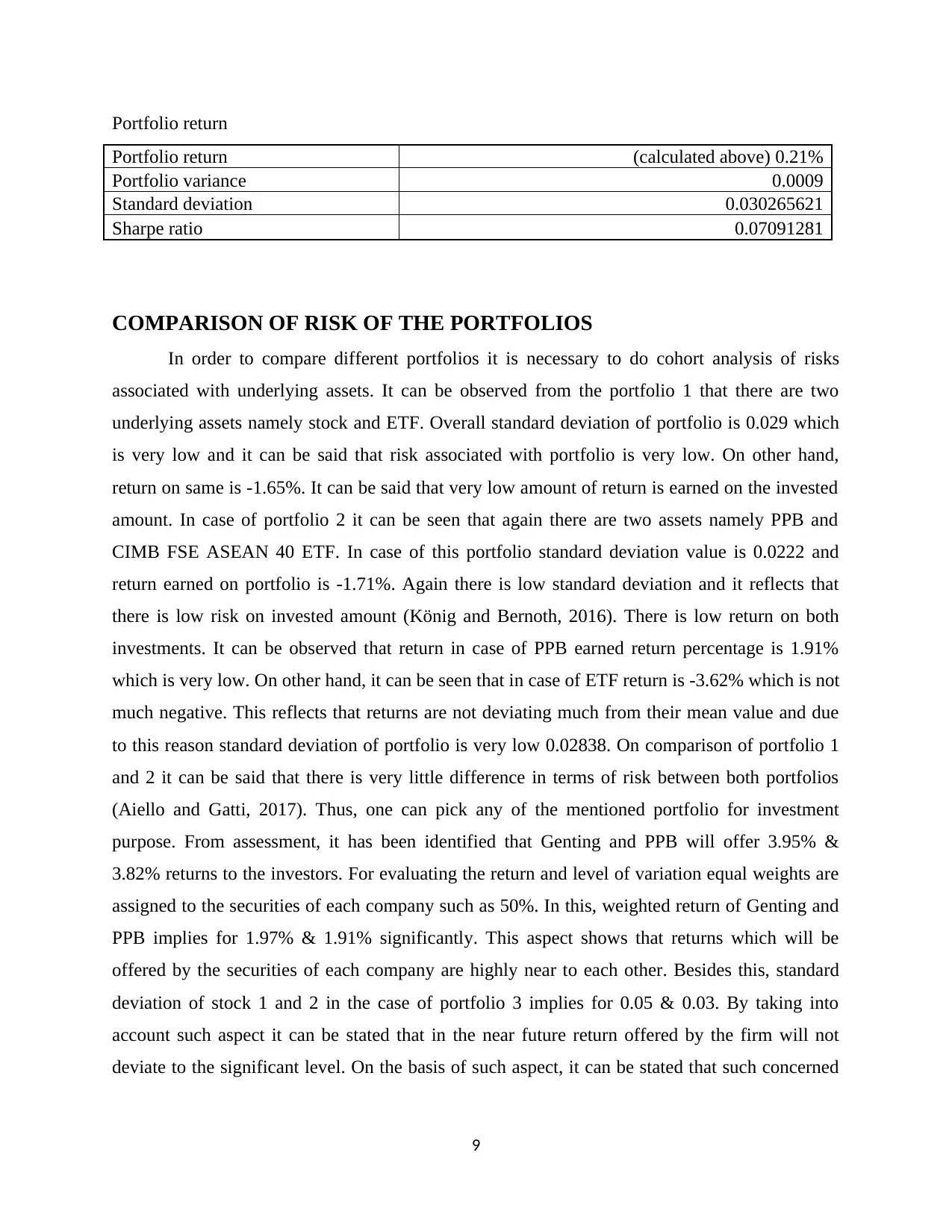

Portfolio return

Portfolio return (calculated above) 0.21%

Portfolio variance 0.0009

Standard deviation 0.030265621

Sharpe ratio 0.07091281

COMPARISON OF RISK OF THE PORTFOLIOS

In order to compare different portfolios it is necessary to do cohort analysis of risks

associated with underlying assets. It can be observed from the portfolio 1 that there are two

underlying assets namely stock and ETF. Overall standard deviation of portfolio is 0.029 which

is very low and it can be said that risk associated with portfolio is very low. On other hand,

return on same is -1.65%. It can be said that very low amount of return is earned on the invested

amount. In case of portfolio 2 it can be seen that again there are two assets namely PPB and

CIMB FSE ASEAN 40 ETF. In case of this portfolio standard deviation value is 0.0222 and

return earned on portfolio is -1.71%. Again there is low standard deviation and it reflects that

there is low risk on invested amount (König and Bernoth, 2016). There is low return on both

investments. It can be observed that return in case of PPB earned return percentage is 1.91%

which is very low. On other hand, it can be seen that in case of ETF return is -3.62% which is not

much negative. This reflects that returns are not deviating much from their mean value and due

to this reason standard deviation of portfolio is very low 0.02838. On comparison of portfolio 1

and 2 it can be said that there is very little difference in terms of risk between both portfolios

(Aiello and Gatti, 2017). Thus, one can pick any of the mentioned portfolio for investment

purpose. From assessment, it has been identified that Genting and PPB will offer 3.95% &

3.82% returns to the investors. For evaluating the return and level of variation equal weights are

assigned to the securities of each company such as 50%. In this, weighted return of Genting and

PPB implies for 1.97% & 1.91% significantly. This aspect shows that returns which will be

offered by the securities of each company are highly near to each other. Besides this, standard

deviation of stock 1 and 2 in the case of portfolio 3 implies for 0.05 & 0.03. By taking into

account such aspect it can be stated that in the near future return offered by the firm will not

deviate to the significant level. On the basis of such aspect, it can be stated that such concerned

9

Portfolio return (calculated above) 0.21%

Portfolio variance 0.0009

Standard deviation 0.030265621

Sharpe ratio 0.07091281

COMPARISON OF RISK OF THE PORTFOLIOS

In order to compare different portfolios it is necessary to do cohort analysis of risks

associated with underlying assets. It can be observed from the portfolio 1 that there are two

underlying assets namely stock and ETF. Overall standard deviation of portfolio is 0.029 which

is very low and it can be said that risk associated with portfolio is very low. On other hand,

return on same is -1.65%. It can be said that very low amount of return is earned on the invested

amount. In case of portfolio 2 it can be seen that again there are two assets namely PPB and

CIMB FSE ASEAN 40 ETF. In case of this portfolio standard deviation value is 0.0222 and

return earned on portfolio is -1.71%. Again there is low standard deviation and it reflects that

there is low risk on invested amount (König and Bernoth, 2016). There is low return on both

investments. It can be observed that return in case of PPB earned return percentage is 1.91%

which is very low. On other hand, it can be seen that in case of ETF return is -3.62% which is not

much negative. This reflects that returns are not deviating much from their mean value and due

to this reason standard deviation of portfolio is very low 0.02838. On comparison of portfolio 1

and 2 it can be said that there is very little difference in terms of risk between both portfolios

(Aiello and Gatti, 2017). Thus, one can pick any of the mentioned portfolio for investment

purpose. From assessment, it has been identified that Genting and PPB will offer 3.95% &

3.82% returns to the investors. For evaluating the return and level of variation equal weights are

assigned to the securities of each company such as 50%. In this, weighted return of Genting and

PPB implies for 1.97% & 1.91% significantly. This aspect shows that returns which will be

offered by the securities of each company are highly near to each other. Besides this, standard

deviation of stock 1 and 2 in the case of portfolio 3 implies for 0.05 & 0.03. By taking into

account such aspect it can be stated that in the near future return offered by the firm will not

deviate to the significant level. On the basis of such aspect, it can be stated that such concerned

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.