Investment Portfolio Analysis: Performance, Selection, and Allocation

VerifiedAdded on 2023/06/10

|7

|1346

|383

Homework Assignment

AI Summary

This assignment provides detailed answers to questions related to portfolio performance analysis and investment decisions. It covers topics such as the significance of alpha value, asset allocation, security selection, and the Capital Asset Pricing Model (CAPM). The analysis includes calculations for expected returns, risk assessments using standard deviation, and the impact of market conditions on portfolio management strategies. The assignment also evaluates whether a manager's ability to generate alpha changes during the business cycle and provides relevant references for further study. It concludes with practical recommendations for investors based on quantitative analysis and risk-adjusted return metrics.

Questions and Answers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

QUESTION 1..................................................................................................................................3

Do you agree? Why or why not?.................................................................................................3

Could a positive alpha be associated with inferior performance? Explain..................................3

QUESTION 2..................................................................................................................................3

Question 3........................................................................................................................................3

Question 4........................................................................................................................................3

If you currently hold a market index portfolio, would you choose to add either of these

portfolios to your holdings? Explain...........................................................................................3

If, instead, you could invest only in T-Notes and one of these portfolios, which would you

choose?........................................................................................................................................4

Question 5........................................................................................................................................4

What was the manager’s return in the month? What was her over- or underperformance?........4

What was the contribution of security selection to relative performance?..................................5

What was the contribution of asset allocation to relative performance?.....................................5

Confirm that the sum of selection and allocation contributions equals her total excess return

relative to the bogey.....................................................................................................................5

Question 6........................................................................................................................................5

Question 7........................................................................................................................................6

REFERENCES................................................................................................................................7

QUESTION 1..................................................................................................................................3

Do you agree? Why or why not?.................................................................................................3

Could a positive alpha be associated with inferior performance? Explain..................................3

QUESTION 2..................................................................................................................................3

Question 3........................................................................................................................................3

Question 4........................................................................................................................................3

If you currently hold a market index portfolio, would you choose to add either of these

portfolios to your holdings? Explain...........................................................................................3

If, instead, you could invest only in T-Notes and one of these portfolios, which would you

choose?........................................................................................................................................4

Question 5........................................................................................................................................4

What was the manager’s return in the month? What was her over- or underperformance?........4

What was the contribution of security selection to relative performance?..................................5

What was the contribution of asset allocation to relative performance?.....................................5

Confirm that the sum of selection and allocation contributions equals her total excess return

relative to the bogey.....................................................................................................................5

Question 6........................................................................................................................................5

Question 7........................................................................................................................................6

REFERENCES................................................................................................................................7

QUESTION 1

Do you agree? Why or why not?

Alpha value denotes the expected performance of the portfolio which denoted the

benchmark for the company. The greater the value of alpha is means the it is better for the

investment purpose, So, the client which wants to shift to the portfolio having greater alpha value

is good for the client.

Could a positive alpha be associated with inferior performance? Explain.

Yes, the positive value of alpha can exist in the market portfolio. But if taken the Sharpe

ratio in consideration, it will not be able to show the inferior performance of the portfolio.

QUESTION 2

It is recommended to the client to increase the allocation of the manager’s fund, as the aloha

value is increased it will enable the investor to earn more return than expected.

Question 3

The larger value of alpha denoted that the portfolio is overpriced. In the Fama French index

model, the larger alpha value means that the market size, risk and value of the portfolio way

higher than the expectation of investment.

Question 4

If you currently hold a market index portfolio, would you choose to add either of these portfolios

to your holdings? Explain.

Capital assets pricing model = Rf + β * (Rm – Rf)

A = 3.5% + 0.8 *(5% - 3.5%)

= 3.5% + 0.8* 1.5%

= 3.5% + 1.2%

= 4.7%

B = 3.5% + 1.5 *(5% - 3.5%)

Do you agree? Why or why not?

Alpha value denotes the expected performance of the portfolio which denoted the

benchmark for the company. The greater the value of alpha is means the it is better for the

investment purpose, So, the client which wants to shift to the portfolio having greater alpha value

is good for the client.

Could a positive alpha be associated with inferior performance? Explain.

Yes, the positive value of alpha can exist in the market portfolio. But if taken the Sharpe

ratio in consideration, it will not be able to show the inferior performance of the portfolio.

QUESTION 2

It is recommended to the client to increase the allocation of the manager’s fund, as the aloha

value is increased it will enable the investor to earn more return than expected.

Question 3

The larger value of alpha denoted that the portfolio is overpriced. In the Fama French index

model, the larger alpha value means that the market size, risk and value of the portfolio way

higher than the expectation of investment.

Question 4

If you currently hold a market index portfolio, would you choose to add either of these portfolios

to your holdings? Explain.

Capital assets pricing model = Rf + β * (Rm – Rf)

A = 3.5% + 0.8 *(5% - 3.5%)

= 3.5% + 0.8* 1.5%

= 3.5% + 1.2%

= 4.7%

B = 3.5% + 1.5 *(5% - 3.5%)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 3.5% + 1.5 * 1.5%

= 3.5% + 2.25%

= 5.75%

Value of Alpha = Estimated return - Required Return

Alpha value of A = 11 – 4.7 = 6.3%

Alpha value of B = 31 – 5.75 = 25.25%

The investment should be done in portfolio B as it has more value of alpha with 25.25%

If, instead, you could invest only in T-Notes and one of these portfolios, which would you

choose?

Relevant risk measure concept will be used in this of reverse viability risk.

Portfolio A = (Expected return of A– Rf) / S.D of A

= (11 – 3.5) / 10 = 0.75%

Portfolio B = (Expected return of B– Rf) / S.D of B

= (14 – 3.5) / 31 = 0.33%

Portfolio Index = (Expected return of index– Rf) / S.D of Index

(5 – 3.5) / 20 = 0.075%

So, according to the above calculation, the investor should invest in portfolio A.

Question 5

What was the manager’s return in the month? What was her over- or underperformance?

Actual = (Actual weight of Equity * Actual return of Equity) + (Actual weight of bond * Actual

return of bond) + (Actual weight of cash * Actual return of cash)

= (0.60 * 2%) + (0.3 * 1%) + (0.1 * 0.5%) = 1.55 %

Benchmark = (Benchmark weight of Equity * Index return of Equity) + (Benchmark

weight of bond * Index return of bond) + (Benchmark weight of cash * Index return of

cash)

= (0.5 * 2.5%) + (0.4 * 1.2%) + (0.1 * 0.5%) = 1.78%

= 3.5% + 2.25%

= 5.75%

Value of Alpha = Estimated return - Required Return

Alpha value of A = 11 – 4.7 = 6.3%

Alpha value of B = 31 – 5.75 = 25.25%

The investment should be done in portfolio B as it has more value of alpha with 25.25%

If, instead, you could invest only in T-Notes and one of these portfolios, which would you

choose?

Relevant risk measure concept will be used in this of reverse viability risk.

Portfolio A = (Expected return of A– Rf) / S.D of A

= (11 – 3.5) / 10 = 0.75%

Portfolio B = (Expected return of B– Rf) / S.D of B

= (14 – 3.5) / 31 = 0.33%

Portfolio Index = (Expected return of index– Rf) / S.D of Index

(5 – 3.5) / 20 = 0.075%

So, according to the above calculation, the investor should invest in portfolio A.

Question 5

What was the manager’s return in the month? What was her over- or underperformance?

Actual = (Actual weight of Equity * Actual return of Equity) + (Actual weight of bond * Actual

return of bond) + (Actual weight of cash * Actual return of cash)

= (0.60 * 2%) + (0.3 * 1%) + (0.1 * 0.5%) = 1.55 %

Benchmark = (Benchmark weight of Equity * Index return of Equity) + (Benchmark

weight of bond * Index return of bond) + (Benchmark weight of cash * Index return of

cash)

= (0.5 * 2.5%) + (0.4 * 1.2%) + (0.1 * 0.5%) = 1.78%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

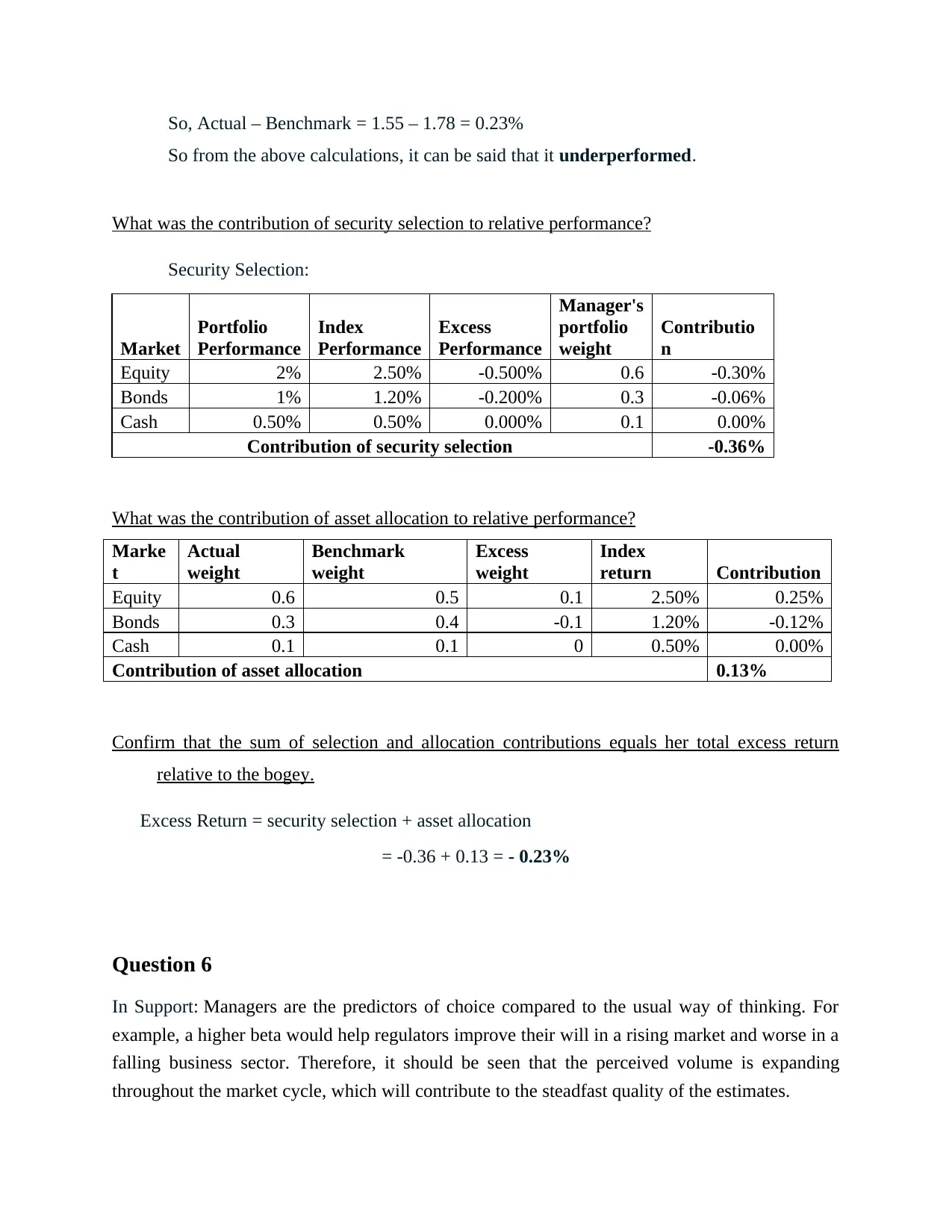

So, Actual – Benchmark = 1.55 – 1.78 = 0.23%

So from the above calculations, it can be said that it underperformed.

What was the contribution of security selection to relative performance?

Security Selection:

Market

Portfolio

Performance

Index

Performance

Excess

Performance

Manager's

portfolio

weight

Contributio

n

Equity 2% 2.50% -0.500% 0.6 -0.30%

Bonds 1% 1.20% -0.200% 0.3 -0.06%

Cash 0.50% 0.50% 0.000% 0.1 0.00%

Contribution of security selection -0.36%

What was the contribution of asset allocation to relative performance?

Marke

t

Actual

weight

Benchmark

weight

Excess

weight

Index

return Contribution

Equity 0.6 0.5 0.1 2.50% 0.25%

Bonds 0.3 0.4 -0.1 1.20% -0.12%

Cash 0.1 0.1 0 0.50% 0.00%

Contribution of asset allocation 0.13%

Confirm that the sum of selection and allocation contributions equals her total excess return

relative to the bogey.

Excess Return = security selection + asset allocation

= -0.36 + 0.13 = - 0.23%

Question 6

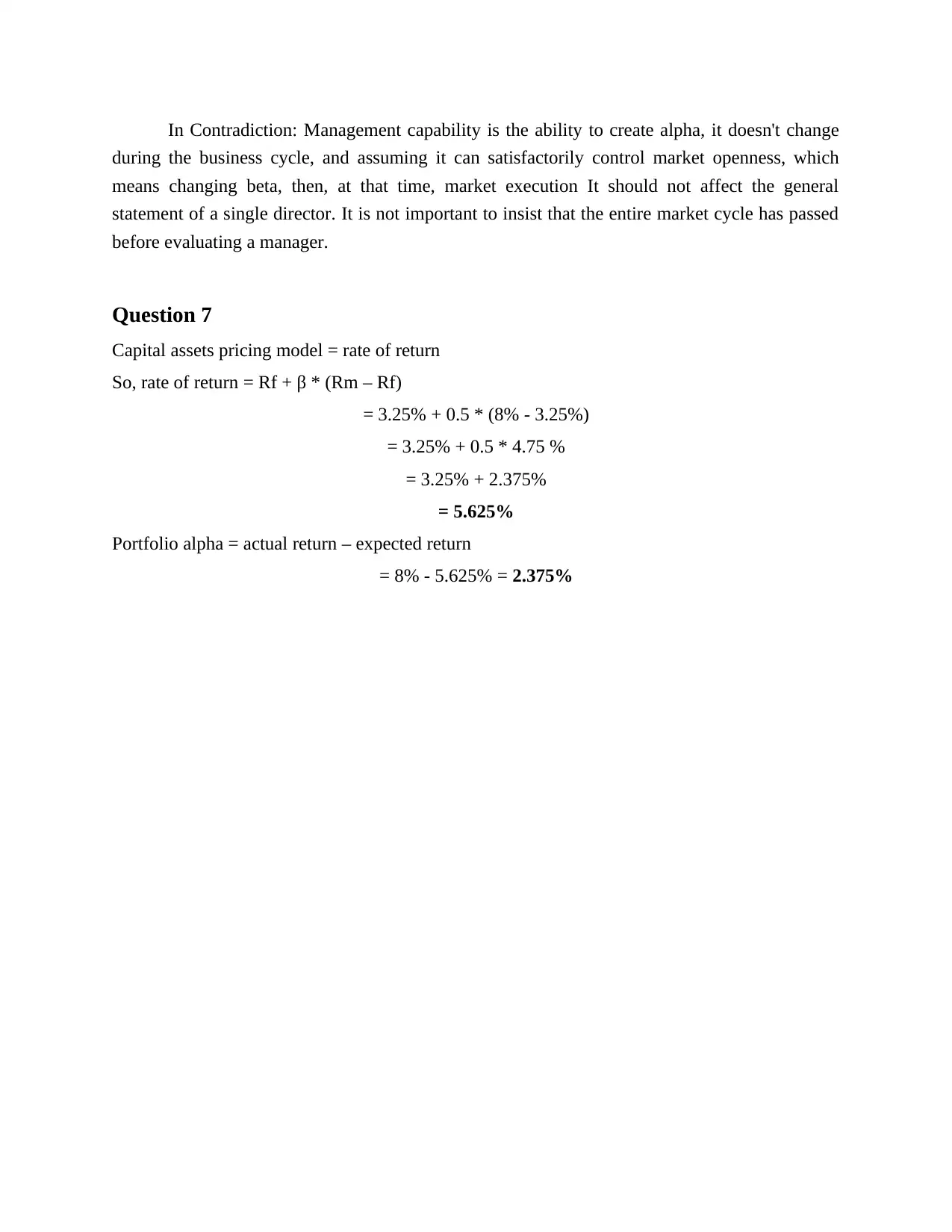

In Support: Managers are the predictors of choice compared to the usual way of thinking. For

example, a higher beta would help regulators improve their will in a rising market and worse in a

falling business sector. Therefore, it should be seen that the perceived volume is expanding

throughout the market cycle, which will contribute to the steadfast quality of the estimates.

So from the above calculations, it can be said that it underperformed.

What was the contribution of security selection to relative performance?

Security Selection:

Market

Portfolio

Performance

Index

Performance

Excess

Performance

Manager's

portfolio

weight

Contributio

n

Equity 2% 2.50% -0.500% 0.6 -0.30%

Bonds 1% 1.20% -0.200% 0.3 -0.06%

Cash 0.50% 0.50% 0.000% 0.1 0.00%

Contribution of security selection -0.36%

What was the contribution of asset allocation to relative performance?

Marke

t

Actual

weight

Benchmark

weight

Excess

weight

Index

return Contribution

Equity 0.6 0.5 0.1 2.50% 0.25%

Bonds 0.3 0.4 -0.1 1.20% -0.12%

Cash 0.1 0.1 0 0.50% 0.00%

Contribution of asset allocation 0.13%

Confirm that the sum of selection and allocation contributions equals her total excess return

relative to the bogey.

Excess Return = security selection + asset allocation

= -0.36 + 0.13 = - 0.23%

Question 6

In Support: Managers are the predictors of choice compared to the usual way of thinking. For

example, a higher beta would help regulators improve their will in a rising market and worse in a

falling business sector. Therefore, it should be seen that the perceived volume is expanding

throughout the market cycle, which will contribute to the steadfast quality of the estimates.

In Contradiction: Management capability is the ability to create alpha, it doesn't change

during the business cycle, and assuming it can satisfactorily control market openness, which

means changing beta, then, at that time, market execution It should not affect the general

statement of a single director. It is not important to insist that the entire market cycle has passed

before evaluating a manager.

Question 7

Capital assets pricing model = rate of return

So, rate of return = Rf + β * (Rm – Rf)

= 3.25% + 0.5 * (8% - 3.25%)

= 3.25% + 0.5 * 4.75 %

= 3.25% + 2.375%

= 5.625%

Portfolio alpha = actual return – expected return

= 8% - 5.625% = 2.375%

during the business cycle, and assuming it can satisfactorily control market openness, which

means changing beta, then, at that time, market execution It should not affect the general

statement of a single director. It is not important to insist that the entire market cycle has passed

before evaluating a manager.

Question 7

Capital assets pricing model = rate of return

So, rate of return = Rf + β * (Rm – Rf)

= 3.25% + 0.5 * (8% - 3.25%)

= 3.25% + 0.5 * 4.75 %

= 3.25% + 2.375%

= 5.625%

Portfolio alpha = actual return – expected return

= 8% - 5.625% = 2.375%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Alam, R., Arnob, R.I. and Alam, A.E., 2020, August. An ARIMA-LSTM Correlation

Coefficient Based Hybrid Model for Portfolio Management of Dhaka Stock Exchange.

In International Conference for Emerging Technologies in Computing (pp. 214-226).

Springer. Cham.

Bouchey, P. and Pritamani, M., 2018. On the Benefits of Centralized Portfolio Management. The

Journal of Portfolio Management. 44(5). pp.68-77.

Dhankar, R.S., 2019. Single-Factor Model and Portfolio Management. In Risk-Return

Relationship and Portfolio Management. (pp. 79-93). Springer. New Delhi.

Edelman, D. and Goryagina, E., 2019. Quantifying the Maximum Worth of Portfolio

Management in a Multi-Period Setting. Available at SSRN 3330625.

Kobayashi, S. and Arai, T., 2019. A Characterization of Optimum Fee Schemes for Delegated

Portfolio Management (No. 1910).

Books and Journals

Alam, R., Arnob, R.I. and Alam, A.E., 2020, August. An ARIMA-LSTM Correlation

Coefficient Based Hybrid Model for Portfolio Management of Dhaka Stock Exchange.

In International Conference for Emerging Technologies in Computing (pp. 214-226).

Springer. Cham.

Bouchey, P. and Pritamani, M., 2018. On the Benefits of Centralized Portfolio Management. The

Journal of Portfolio Management. 44(5). pp.68-77.

Dhankar, R.S., 2019. Single-Factor Model and Portfolio Management. In Risk-Return

Relationship and Portfolio Management. (pp. 79-93). Springer. New Delhi.

Edelman, D. and Goryagina, E., 2019. Quantifying the Maximum Worth of Portfolio

Management in a Multi-Period Setting. Available at SSRN 3330625.

Kobayashi, S. and Arai, T., 2019. A Characterization of Optimum Fee Schemes for Delegated

Portfolio Management (No. 1910).

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.