Impact of U.S. Quantitative Easing on Global Finance

VerifiedAdded on 2020/07/23

|12

|3084

|303

AI Summary

Quantitative Easing (QE) is a monetary policy tool used by central banks to stimulate economic activity by increasing the money supply and lowering interest rates. This assignment provides an in-depth analysis of QE’s global impacts on financial markets, particularly focusing on bond and equity funds. By examining historical data and scholarly resources, we assess how QE influences market volatility, investment strategies, and portfolio performance. Key aspects include understanding the correlation between QE policies and shifts in asset prices, evaluating risk measures such as standard deviation and Sharpe ratios, and discussing strategic adjustments for investors. The analysis is supported by financial models that compute expected returns, variances, and covariances to guide investment decisions under different economic conditions shaped by QE initiatives.

PORTFOLIO

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Expected return and standard deviation of portfolio.......................................................................1

Difference between growth and value fund.....................................................................................1

Advantage and disadvantage of value and growth investing...........................................................2

Characteristics need to be coverd by bond......................................................................................3

Portfolio measurement.....................................................................................................................3

Implications of going for balanced portfolio in 50:50 portion for bond and equity........................4

Quantitative easing program and possibilities to halt it...................................................................4

Future possibilities for QE program and Fed balance sheet............................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

Calculations.................................................................................................................................8

Table 1Computation of return and standard deviation....................................................................1

Table 2Portoflio risk measurement..................................................................................................4

INTRODUCTION...........................................................................................................................1

Expected return and standard deviation of portfolio.......................................................................1

Difference between growth and value fund.....................................................................................1

Advantage and disadvantage of value and growth investing...........................................................2

Characteristics need to be coverd by bond......................................................................................3

Portfolio measurement.....................................................................................................................3

Implications of going for balanced portfolio in 50:50 portion for bond and equity........................4

Quantitative easing program and possibilities to halt it...................................................................4

Future possibilities for QE program and Fed balance sheet............................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

Calculations.................................................................................................................................8

Table 1Computation of return and standard deviation....................................................................1

Table 2Portoflio risk measurement..................................................................................................4

INTRODUCTION

Portfolio creation is an art because while preparing it one need to consider number of

factors and on that basis same is prepared. In the current report expected return and standard

deviation of portfolio is computed. Apart from this, in the report Sharpe and Trenyor ratios are

also computed. In second part of the research report, detail discussion is carried out on

quantitative easing programs and chances that same can be closed by the firm in the market. atn

end of the report finally, conclusion section is prepared in which in detail after analysi of entire

facts summary is formed in respect to entire work that is done in report.

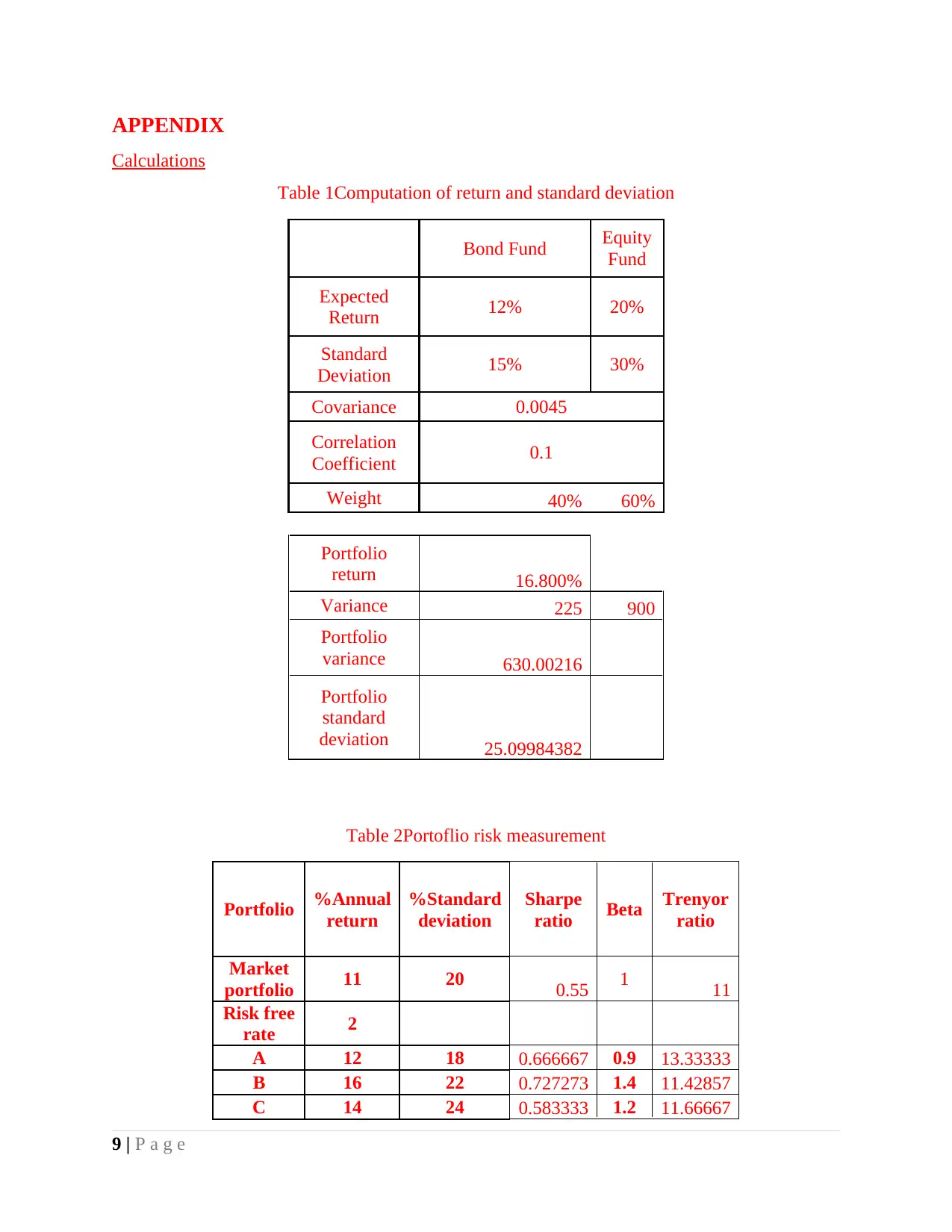

Expected return and standard deviation of portfolio

Portfolio return is computed and its value is 16.80% as well as standard deviation value is

25.09 which means that if weights are taken in to account for each security alongwith return

percentage then overall portfolio return percentage will be 16.80%. Standard deviation reflect the

deviation that comes in values of the variable from mean value or distance that is between mean

and data points of variable. Higher standard deviation reflect that there is very high gap between

mean value and data points which means that stock is volatile in nature. On other hand, low

standard deviation value reflect that there is low gap between mean value and data points which

means that most of times data points are moving around mean value (Brealey and et.al., 2012). It

can be said that low standard deviation value reflect there is less fluctuation in variable values.

Hence, it can be assumed that low standard deviation is better for the firm then high standard

deviation. From table it can be seen that standard deviation value is 25.09 which means that

portfolio return is moving at very slow rate. Hence, it can be said that portfolio is giving stable

and good amount of return to the investors. Due to this reason further investment can be made on

the mentioned portfolio.

Difference between growth and value fund

Particulars Growth fund Value fund

Higher price In case of growth fund there

is very high price of the

product and investor try to

take advantage of this high

product price. Hence, it can

be said that higher price

In case of value fund thing is

inverse as it can be observed

that in case of value fund

most of stocks are

undervalued but they have

huge growth potential. Hence,

1 | P a g e

Portfolio creation is an art because while preparing it one need to consider number of

factors and on that basis same is prepared. In the current report expected return and standard

deviation of portfolio is computed. Apart from this, in the report Sharpe and Trenyor ratios are

also computed. In second part of the research report, detail discussion is carried out on

quantitative easing programs and chances that same can be closed by the firm in the market. atn

end of the report finally, conclusion section is prepared in which in detail after analysi of entire

facts summary is formed in respect to entire work that is done in report.

Expected return and standard deviation of portfolio

Portfolio return is computed and its value is 16.80% as well as standard deviation value is

25.09 which means that if weights are taken in to account for each security alongwith return

percentage then overall portfolio return percentage will be 16.80%. Standard deviation reflect the

deviation that comes in values of the variable from mean value or distance that is between mean

and data points of variable. Higher standard deviation reflect that there is very high gap between

mean value and data points which means that stock is volatile in nature. On other hand, low

standard deviation value reflect that there is low gap between mean value and data points which

means that most of times data points are moving around mean value (Brealey and et.al., 2012). It

can be said that low standard deviation value reflect there is less fluctuation in variable values.

Hence, it can be assumed that low standard deviation is better for the firm then high standard

deviation. From table it can be seen that standard deviation value is 25.09 which means that

portfolio return is moving at very slow rate. Hence, it can be said that portfolio is giving stable

and good amount of return to the investors. Due to this reason further investment can be made on

the mentioned portfolio.

Difference between growth and value fund

Particulars Growth fund Value fund

Higher price In case of growth fund there

is very high price of the

product and investor try to

take advantage of this high

product price. Hence, it can

be said that higher price

In case of value fund thing is

inverse as it can be observed

that in case of value fund

most of stocks are

undervalued but they have

huge growth potential. Hence,

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

benefit an invstor in terms of

high growth in shares value

or earning of huge amount of

capital gain (Tirole, 2010).

value fund also have huge

significence for the investors.

Higher earning It is observed that for growth

fund firms higher amount of

earning is observed. Means

that firms which comes in

growth fund earn a good

amount of revenue in

business and it is its major

characteristics.

On other hand, in case of

value fund it is observed that

firms earn very low amount

of return and due to this

reason its shares remain

undervalued in the market.

More volatility High growth stocks are more

volatile and good amount of

return is made in it. On other

hand, if market is not moving

in positive direction then in

that case share price decline

at fast rate (Damodaran,

2016).

In case of value fund less

amount of volatility is

observed as with change in

market slight increase or

decrease in observed in

stocks.

Price below similar

companies in industry

In case of growth stocks share

price is relatively higher then

competitors in the market.

On other hand, in case of

value stocks price is below

the similar companies in

industry.

Return Return percentage is high in

case of growth stocks as stock

price plunged at fast rate.

In case of value stock return

percentage is very low as

stocks are less volatile in

nature.

Advantage and disadvantage of value and growth investing

Advantage of growth investing

2 | P a g e

high growth in shares value

or earning of huge amount of

capital gain (Tirole, 2010).

value fund also have huge

significence for the investors.

Higher earning It is observed that for growth

fund firms higher amount of

earning is observed. Means

that firms which comes in

growth fund earn a good

amount of revenue in

business and it is its major

characteristics.

On other hand, in case of

value fund it is observed that

firms earn very low amount

of return and due to this

reason its shares remain

undervalued in the market.

More volatility High growth stocks are more

volatile and good amount of

return is made in it. On other

hand, if market is not moving

in positive direction then in

that case share price decline

at fast rate (Damodaran,

2016).

In case of value fund less

amount of volatility is

observed as with change in

market slight increase or

decrease in observed in

stocks.

Price below similar

companies in industry

In case of growth stocks share

price is relatively higher then

competitors in the market.

On other hand, in case of

value stocks price is below

the similar companies in

industry.

Return Return percentage is high in

case of growth stocks as stock

price plunged at fast rate.

In case of value stock return

percentage is very low as

stocks are less volatile in

nature.

Advantage and disadvantage of value and growth investing

Advantage of growth investing

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Major advantage of growth investing is that good amount of gain can be made on stock if

investment isn made in it.

Disadvantage of growth investing

Major disadvantage is that in case stock market decline huge loss can be faced on

investment that is made on growth stocks (Damodaran, 2010).

Advantage of value stock

In case of value stock major advantage is that risk is less and there is less volatility in the

market.

Disadvantage of value stock

Major disadvantage of value stock is that one can not expect to earn good amount of

profit earning from value investing.

Characteristics need to be coverd by bond

As per case it can be observed that base rate get increased which will lead to increase in

interest rate. In such situation it is very important to take high coupon rate bond. This is because

in bond interest rate is locked and in comparison to market interest rate if it is low then it means

that low return is earned on investment. Hence, bond with high yield and coupon rate is required

but with short duration (Hillier and et.al., 2013). This is because short duration bonds are less

volatile in nature in comparison to long duration bond. Thus, in order to earn profit even base

rate increase there is need to take open position on bond whose duration is low and yield

percentage as well as coupon rate is less.

Portfolio measurement

Standard deviation reflect the distance that is between mean value and final value of the

variable. Sharpe ratio reflect the return that is gained on each unit of risk that is taken in the

business in form of standard deviation. On other hand, Trenyor ratio reflect the return that is

earned on each unit of risk that is taken on investment and measured in form of beta. On analysis

of facts it can be observed that for portfolio A Sharpe ratio value is 0.66 and same is 0.72 for

portfolio B and 0.58 for portfolio C. It can be said that on this front there is high return for risk in

case of portfolio B. On other hand, there is Trenyor ratio wherein higher return is observed in

case of portfolio A where return percentage is 13.33 which is very high. Hence, it can be said

3 | P a g e

investment isn made in it.

Disadvantage of growth investing

Major disadvantage is that in case stock market decline huge loss can be faced on

investment that is made on growth stocks (Damodaran, 2010).

Advantage of value stock

In case of value stock major advantage is that risk is less and there is less volatility in the

market.

Disadvantage of value stock

Major disadvantage of value stock is that one can not expect to earn good amount of

profit earning from value investing.

Characteristics need to be coverd by bond

As per case it can be observed that base rate get increased which will lead to increase in

interest rate. In such situation it is very important to take high coupon rate bond. This is because

in bond interest rate is locked and in comparison to market interest rate if it is low then it means

that low return is earned on investment. Hence, bond with high yield and coupon rate is required

but with short duration (Hillier and et.al., 2013). This is because short duration bonds are less

volatile in nature in comparison to long duration bond. Thus, in order to earn profit even base

rate increase there is need to take open position on bond whose duration is low and yield

percentage as well as coupon rate is less.

Portfolio measurement

Standard deviation reflect the distance that is between mean value and final value of the

variable. Sharpe ratio reflect the return that is gained on each unit of risk that is taken in the

business in form of standard deviation. On other hand, Trenyor ratio reflect the return that is

earned on each unit of risk that is taken on investment and measured in form of beta. On analysis

of facts it can be observed that for portfolio A Sharpe ratio value is 0.66 and same is 0.72 for

portfolio B and 0.58 for portfolio C. It can be said that on this front there is high return for risk in

case of portfolio B. On other hand, there is Trenyor ratio wherein higher return is observed in

case of portfolio A where return percentage is 13.33 which is very high. Hence, it can be said

3 | P a g e

that is the reason due to which in case of Sharpe ratio portfolio B have high return and in case of

Trenyor ratio portfolio A have high return.

Implications of going for balanced portfolio in 50:50 portion for bond and

equity

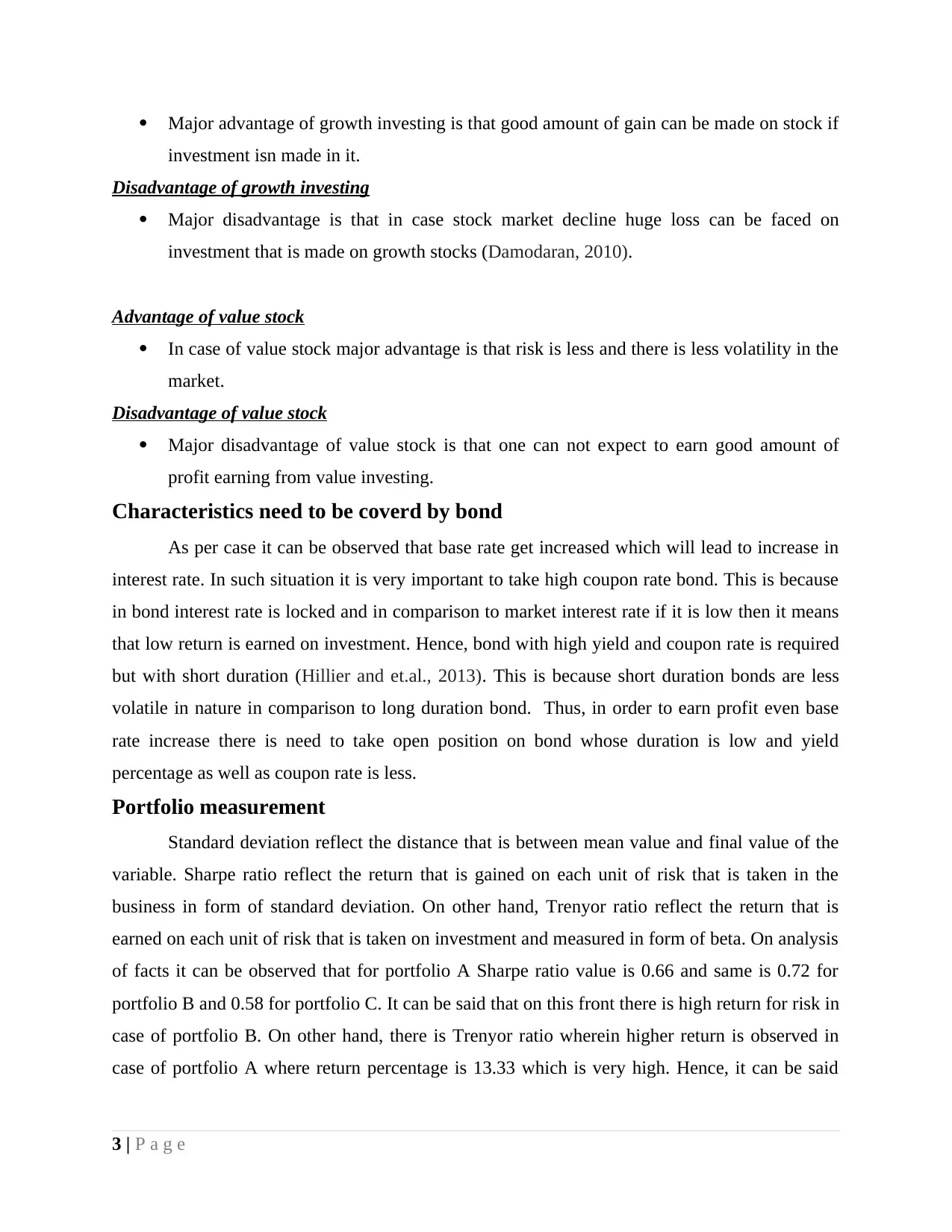

On analysis of charts it can be observed that most of times S&P 500 index moved in

specific range and interest rate is declining consistently.

From image given above it can be seen that S&P 500 index almost move in specific pattern as

organge lines are highlighting same. At top and bottom these lines are given. It can be seen from

chart that past trend is break and index value is consistently rising. From this level either new

level can be developed or market may tumbeled at fast rate (Coles, Lemmon and Meschke,

2012). All these things lead to decline in return on equity. On other hand, in case of interest rate

bond interest rate declined sharply in past 5 years. In future further interet rate may move in

positive direction. Hence, it can be said that risk that is on stock market can be compensated by

safen heavn bond. Hence, it can be said that this proportion of 50:50 will have positive impact on

the portfolio return.

Quantitative easing program and possibilities to halt it

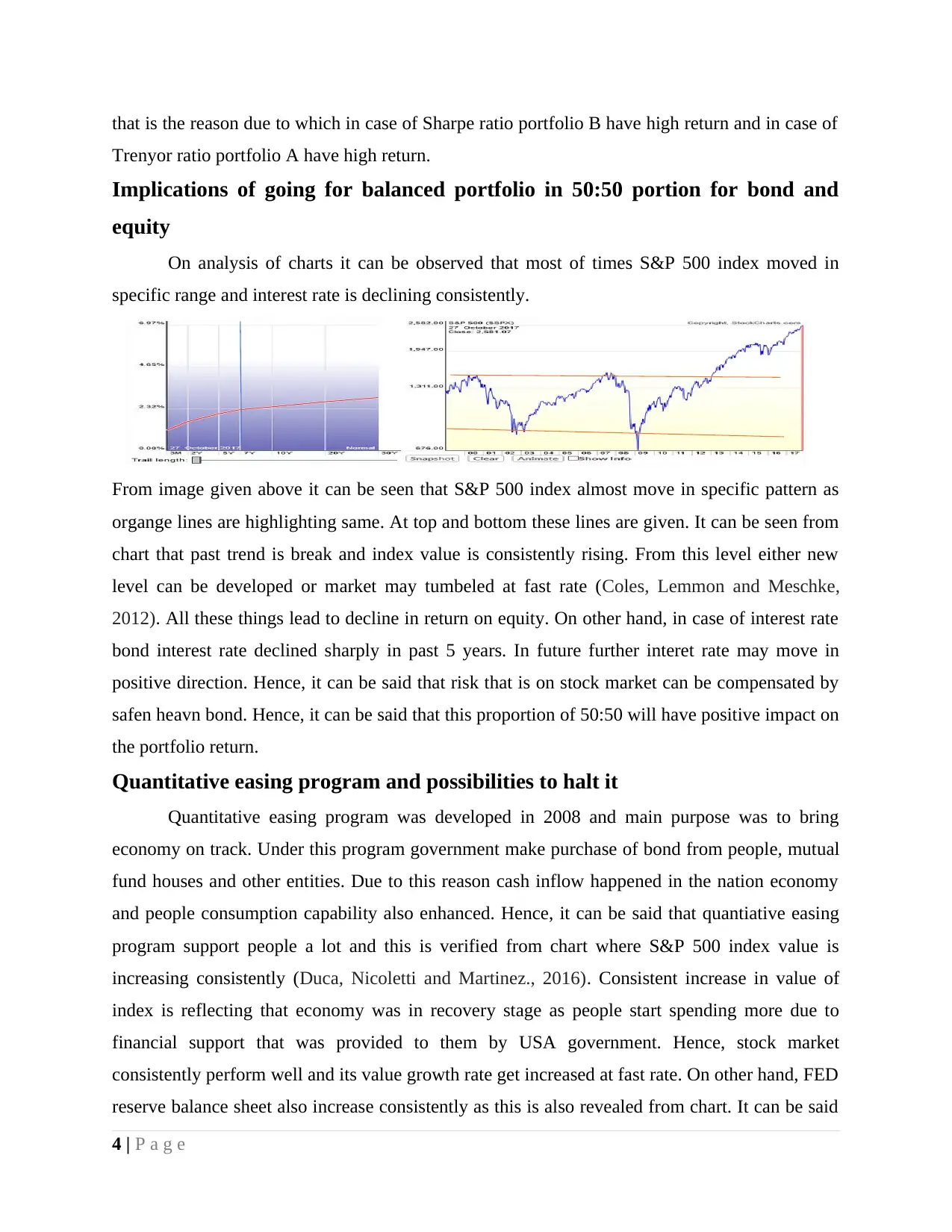

Quantitative easing program was developed in 2008 and main purpose was to bring

economy on track. Under this program government make purchase of bond from people, mutual

fund houses and other entities. Due to this reason cash inflow happened in the nation economy

and people consumption capability also enhanced. Hence, it can be said that quantiative easing

program support people a lot and this is verified from chart where S&P 500 index value is

increasing consistently (Duca, Nicoletti and Martinez., 2016). Consistent increase in value of

index is reflecting that economy was in recovery stage as people start spending more due to

financial support that was provided to them by USA government. Hence, stock market

consistently perform well and its value growth rate get increased at fast rate. On other hand, FED

reserve balance sheet also increase consistently as this is also revealed from chart. It can be said

4 | P a g e

Trenyor ratio portfolio A have high return.

Implications of going for balanced portfolio in 50:50 portion for bond and

equity

On analysis of charts it can be observed that most of times S&P 500 index moved in

specific range and interest rate is declining consistently.

From image given above it can be seen that S&P 500 index almost move in specific pattern as

organge lines are highlighting same. At top and bottom these lines are given. It can be seen from

chart that past trend is break and index value is consistently rising. From this level either new

level can be developed or market may tumbeled at fast rate (Coles, Lemmon and Meschke,

2012). All these things lead to decline in return on equity. On other hand, in case of interest rate

bond interest rate declined sharply in past 5 years. In future further interet rate may move in

positive direction. Hence, it can be said that risk that is on stock market can be compensated by

safen heavn bond. Hence, it can be said that this proportion of 50:50 will have positive impact on

the portfolio return.

Quantitative easing program and possibilities to halt it

Quantitative easing program was developed in 2008 and main purpose was to bring

economy on track. Under this program government make purchase of bond from people, mutual

fund houses and other entities. Due to this reason cash inflow happened in the nation economy

and people consumption capability also enhanced. Hence, it can be said that quantiative easing

program support people a lot and this is verified from chart where S&P 500 index value is

increasing consistently (Duca, Nicoletti and Martinez., 2016). Consistent increase in value of

index is reflecting that economy was in recovery stage as people start spending more due to

financial support that was provided to them by USA government. Hence, stock market

consistently perform well and its value growth rate get increased at fast rate. On other hand, FED

reserve balance sheet also increase consistently as this is also revealed from chart. It can be said

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that launch of quantitative easing program lead to increase in spending capacity of people but at

same time due to this reason balance sheet also increased at rapid rate. It is the full support to the

general public due to which to some extent recovery start in an economy and index value

increased at very fast rate from 2008 to 2015.

Goal: On basis of entire discussion that is done above it can be said that major goal

behind quantitative easing program was to increase expenditure from side of people so

that economy can be bring back on growth track.

Consequences: Major consequence of quantitative easing program was that balance sheet

of FED reserve increase at fast rate as some of economist had view that as expected

results are not obtained from QE program (Jarrow and Li, 2014).

Outcome: Economy of USA gradually comes on track and as government give support to

people to meet their educational and health expenses. Thus, outcome was positive for

nation economy.

Future possibilities for QE program and Fed balance sheet

There is future possibility that in future time period quantitative easing program will be

stopped by the USA FED reserve. This is because now USA economy is on growth track and

labour market condition get improved to great extent. Hence, it can be said that things are going

well to some extent in the nation economy and due to this reason quantitative easing program can

be stopped by the USA central bank. USA central bank state that substantive improvement

comes in the nation economy in terms of outlook that is towards labour market of the nation. In

other words it can be said that since starting of quantitative easing program whatever was

condition of nation now get improveed to large extent (Barroso, da Silva and Sales, 2016).

Economy become more broader then before and there is high potential in its growth. Hence, in

future time period economy itself will be able to handle itself in complex condition and soon it

will come on track. It can be said that this is the right time for the USA government to close its

quantitative easing program. All these things will have huge impact on the assets and liability. It

must be noted that when FED program was launched it was operated in specific manner under

which assets were purchased in terms of bond from the market and in this way cash inflow

happened in the nation economy. It can be said that due to consistent purchase of bond FED

balance sheet increased regularly (Cobham and Kang, 2012). Hence, it can be said that in future

time period there is possibility that quantitative easing program can be halted and due to this

5 | P a g e

same time due to this reason balance sheet also increased at rapid rate. It is the full support to the

general public due to which to some extent recovery start in an economy and index value

increased at very fast rate from 2008 to 2015.

Goal: On basis of entire discussion that is done above it can be said that major goal

behind quantitative easing program was to increase expenditure from side of people so

that economy can be bring back on growth track.

Consequences: Major consequence of quantitative easing program was that balance sheet

of FED reserve increase at fast rate as some of economist had view that as expected

results are not obtained from QE program (Jarrow and Li, 2014).

Outcome: Economy of USA gradually comes on track and as government give support to

people to meet their educational and health expenses. Thus, outcome was positive for

nation economy.

Future possibilities for QE program and Fed balance sheet

There is future possibility that in future time period quantitative easing program will be

stopped by the USA FED reserve. This is because now USA economy is on growth track and

labour market condition get improved to great extent. Hence, it can be said that things are going

well to some extent in the nation economy and due to this reason quantitative easing program can

be stopped by the USA central bank. USA central bank state that substantive improvement

comes in the nation economy in terms of outlook that is towards labour market of the nation. In

other words it can be said that since starting of quantitative easing program whatever was

condition of nation now get improveed to large extent (Barroso, da Silva and Sales, 2016).

Economy become more broader then before and there is high potential in its growth. Hence, in

future time period economy itself will be able to handle itself in complex condition and soon it

will come on track. It can be said that this is the right time for the USA government to close its

quantitative easing program. All these things will have huge impact on the assets and liability. It

must be noted that when FED program was launched it was operated in specific manner under

which assets were purchased in terms of bond from the market and in this way cash inflow

happened in the nation economy. It can be said that due to consistent purchase of bond FED

balance sheet increased regularly (Cobham and Kang, 2012). Hence, it can be said that in future

time period there is possibility that quantitative easing program can be halted and due to this

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reason both assets and liabilities will be reduced in the central bank balance sheet. It can be said

that with consistent recovery in the economy in future time period quantitative easing program

soon can be closed by the central bank of the nation. However, in case any downturn is observed

in the USA economy due to any reason then in that case this program can be extended to the

some extent by the central bank of USA. However, till the time chances are developed that

quantitative easing program can be shut down as global economy is also observing recovery.

USA government or FED decision to stop quantitative easing program will depend on number of

factors like growth rate of world major economies like China, India, Japan and some of

European nations. If economic condition of these nations will not be good then in that case

global economy can derail from growth track (Cho and Rhee, 2014). Hence, it solely depend on

internation level economic conditions whether central bank close its policy. In current time

period many new reforms are launched in multiple nations of the world and due to this reason

there are chances that economic growth of nations will accelerate and this will bring stability in

international market. If all these happened then in that case there are full chances that central

bank may close its qunaitative easing program. All these things will lead to decline in assets and

liability of central bank which will made it stronger. Currently, also many countries governments

are working together to handle the situation through common platform like BRICS and EU etc.

Collective efforts of the varied nations government will ensure that now global economy

consistently grow (Monaghan., 2014). It is regional cooperation that help nations to come on

recovery track. Thus, it can be said that all these things if gone well then in that case in future

time period government of USA and central bank will stop implementation of quantitative

easing program in the nation and this will lead to decline in assets and liability in balance sheet

of central bank as well as it become more balanced then before. Market will continue to perform

well as it is expected that in future time period USA economy will be more stronger then current

time period.

CONCLUSION

On the basis of above discussion and analysis it is concluded that there is significent

importance of methods like Sharpe ratio and Trenyor ratio for the firms. This is because by using

these approaches in systematic manner return that is earned on unit of risk is identified. It is also

concluded that central bank of USA can close its quantitative easing program soon. Bonds that

6 | P a g e

that with consistent recovery in the economy in future time period quantitative easing program

soon can be closed by the central bank of the nation. However, in case any downturn is observed

in the USA economy due to any reason then in that case this program can be extended to the

some extent by the central bank of USA. However, till the time chances are developed that

quantitative easing program can be shut down as global economy is also observing recovery.

USA government or FED decision to stop quantitative easing program will depend on number of

factors like growth rate of world major economies like China, India, Japan and some of

European nations. If economic condition of these nations will not be good then in that case

global economy can derail from growth track (Cho and Rhee, 2014). Hence, it solely depend on

internation level economic conditions whether central bank close its policy. In current time

period many new reforms are launched in multiple nations of the world and due to this reason

there are chances that economic growth of nations will accelerate and this will bring stability in

international market. If all these happened then in that case there are full chances that central

bank may close its qunaitative easing program. All these things will lead to decline in assets and

liability of central bank which will made it stronger. Currently, also many countries governments

are working together to handle the situation through common platform like BRICS and EU etc.

Collective efforts of the varied nations government will ensure that now global economy

consistently grow (Monaghan., 2014). It is regional cooperation that help nations to come on

recovery track. Thus, it can be said that all these things if gone well then in that case in future

time period government of USA and central bank will stop implementation of quantitative

easing program in the nation and this will lead to decline in assets and liability in balance sheet

of central bank as well as it become more balanced then before. Market will continue to perform

well as it is expected that in future time period USA economy will be more stronger then current

time period.

CONCLUSION

On the basis of above discussion and analysis it is concluded that there is significent

importance of methods like Sharpe ratio and Trenyor ratio for the firms. This is because by using

these approaches in systematic manner return that is earned on unit of risk is identified. It is also

concluded that central bank of USA can close its quantitative easing program soon. Bonds that

6 | P a g e

have short durtation are less risky and coupon percentage is also high on them. Hence, according

to changes that are made in the base rate specific bond need to be pick for the portfolio.

7 | P a g e

to changes that are made in the base rate specific bond need to be pick for the portfolio.

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Barroso, J.B.R., da Silva, L.A.P. and Sales, A.S., 2016. Quantitative Easing and Related Capital

Flows into Brazil: measuring its effects and transmission channels through a rigorous

counterfactual evaluation. Journal of International Money and Finance. 67. pp.102-122.

Brealey, R.A., Myers, S.C., Allen, F. and Mohanty, P., 2012. Principles of corporate finance.

Tata McGraw-Hill Education.

Cho, D. and Rhee, C., 2014. Effects of quantitative easing on asia: capital flows and financial

markets. The Singapore Economic Review. 59(03). p.1450018.

Cobham, D. and Kang, Y., 2012. Financial crisis and quantitative easing: can broad money tell

us anything?. The Manchester School. 80(s1). pp.54-76.

Coles, J.L., Lemmon, M.L. and Meschke, J.F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate

performance. Journal of Financial Economics. 103(1). pp.149-168.

Damodaran, A., 2010. Applied corporate finance. John Wiley & Sons.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance. John Wiley & Sons.

Duca, M.L., Nicoletti, G. and Martinez, A.V., 2016. Global corporate bond issuance: what role

for US quantitative easing?. Journal of International Money and Finance. 60. pp.114-150.

Hillier, D. and et.al., 2013. Corporate finance. McGraw Hill.

Jarrow, R. and Li, H., 2014. The impact of quantitative easing on the US term structure of

interest rates. Review of Derivatives Research. 17(3). pp.287-321.

Tirole, J., 2010. The theory of corporate finance. Princeton University Press.

Online

Monaghan., A., 2014. [Online]. US Federal reserve to end quantitative easing program.

Available through:<https://www.theguardian.com/business/2014/oct/29/us-federal-reserve-

end-quantitative-easing-programme>.

8 | P a g e

Books and Journals

Barroso, J.B.R., da Silva, L.A.P. and Sales, A.S., 2016. Quantitative Easing and Related Capital

Flows into Brazil: measuring its effects and transmission channels through a rigorous

counterfactual evaluation. Journal of International Money and Finance. 67. pp.102-122.

Brealey, R.A., Myers, S.C., Allen, F. and Mohanty, P., 2012. Principles of corporate finance.

Tata McGraw-Hill Education.

Cho, D. and Rhee, C., 2014. Effects of quantitative easing on asia: capital flows and financial

markets. The Singapore Economic Review. 59(03). p.1450018.

Cobham, D. and Kang, Y., 2012. Financial crisis and quantitative easing: can broad money tell

us anything?. The Manchester School. 80(s1). pp.54-76.

Coles, J.L., Lemmon, M.L. and Meschke, J.F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate

performance. Journal of Financial Economics. 103(1). pp.149-168.

Damodaran, A., 2010. Applied corporate finance. John Wiley & Sons.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance. John Wiley & Sons.

Duca, M.L., Nicoletti, G. and Martinez, A.V., 2016. Global corporate bond issuance: what role

for US quantitative easing?. Journal of International Money and Finance. 60. pp.114-150.

Hillier, D. and et.al., 2013. Corporate finance. McGraw Hill.

Jarrow, R. and Li, H., 2014. The impact of quantitative easing on the US term structure of

interest rates. Review of Derivatives Research. 17(3). pp.287-321.

Tirole, J., 2010. The theory of corporate finance. Princeton University Press.

Online

Monaghan., A., 2014. [Online]. US Federal reserve to end quantitative easing program.

Available through:<https://www.theguardian.com/business/2014/oct/29/us-federal-reserve-

end-quantitative-easing-programme>.

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Calculations

Table 1Computation of return and standard deviation

Bond Fund Equity

Fund

Expected

Return 12% 20%

Standard

Deviation 15% 30%

Covariance 0.0045

Correlation

Coefficient 0.1

Weight 40% 60%

Portfolio

return 16.800%

Variance 225 900

Portfolio

variance 630.00216

Portfolio

standard

deviation 25.09984382

Table 2Portoflio risk measurement

Portfolio %Annual

return

%Standard

deviation

Sharpe

ratio Beta Trenyor

ratio

Market

portfolio 11 20 0.55 1 11

Risk free

rate 2

A 12 18 0.666667 0.9 13.33333

B 16 22 0.727273 1.4 11.42857

C 14 24 0.583333 1.2 11.66667

9 | P a g e

Calculations

Table 1Computation of return and standard deviation

Bond Fund Equity

Fund

Expected

Return 12% 20%

Standard

Deviation 15% 30%

Covariance 0.0045

Correlation

Coefficient 0.1

Weight 40% 60%

Portfolio

return 16.800%

Variance 225 900

Portfolio

variance 630.00216

Portfolio

standard

deviation 25.09984382

Table 2Portoflio risk measurement

Portfolio %Annual

return

%Standard

deviation

Sharpe

ratio Beta Trenyor

ratio

Market

portfolio 11 20 0.55 1 11

Risk free

rate 2

A 12 18 0.666667 0.9 13.33333

B 16 22 0.727273 1.4 11.42857

C 14 24 0.583333 1.2 11.66667

9 | P a g e

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.