Portfolio Management: Investment Strategy, Risk & Return Analysis

VerifiedAdded on 2023/06/12

|28

|6460

|199

Report

AI Summary

This report provides a detailed analysis of portfolio management and theory, focusing on developing an optimal portfolio for Jack and Gloria to support their retirement expenses. It includes an investment policy statement, evaluating their risk and return objectives, and considering investment constrai...

Running head: PORTFOLIO MANAGEMENT AND THEORY

Portfolio Management and Theory

Name of the Student:

Name of the University:

Authors Note:

Portfolio Management and Theory

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

1

Table of Contents

Executive Summary:..................................................................................................................3

Introduction:...............................................................................................................................4

Part 1 Investment policy Statement:..........................................................................................4

1.1 Return objective:..................................................................................................................4

1.2 Risk objective:......................................................................................................................5

1.3 Investment constraints:.........................................................................................................5

1.4 Standards for performance evaluation:................................................................................6

1.5 Analysis of market indices:..................................................................................................6

1.5.1 Providing summary statistics and analysing the performance, while discussing the role

of each asset class:.....................................................................................................................6

1.5.2 Evaluating the risk and return provisions of the security market indices:........................7

1.6 Recommendations:...............................................................................................................9

Part 2 Active Portfolio:..............................................................................................................9

2.1 Research on momentum strategies:......................................................................................9

2.2 Portfolio construction:........................................................................................................11

2.3 Analysis of the portfolio performance:..............................................................................14

2.3.1 Identifying whether winner stock outperform past loser stocks on average:..................14

2.3.2 Stating whether winner stock outperform average return of the 100 stocks:..................14

2.3.3 Recommending whether momentum strategy is good based on the analysis:................15

2.3.4 Changing he weightage calculation for detecting the change in performance of the

portfolio:...................................................................................................................................15

Part 3 Top-Down Analysis:......................................................................................................17

3.1 Economic Analysis:...........................................................................................................17

3.2 Industry Analysis:..............................................................................................................19

1

Table of Contents

Executive Summary:..................................................................................................................3

Introduction:...............................................................................................................................4

Part 1 Investment policy Statement:..........................................................................................4

1.1 Return objective:..................................................................................................................4

1.2 Risk objective:......................................................................................................................5

1.3 Investment constraints:.........................................................................................................5

1.4 Standards for performance evaluation:................................................................................6

1.5 Analysis of market indices:..................................................................................................6

1.5.1 Providing summary statistics and analysing the performance, while discussing the role

of each asset class:.....................................................................................................................6

1.5.2 Evaluating the risk and return provisions of the security market indices:........................7

1.6 Recommendations:...............................................................................................................9

Part 2 Active Portfolio:..............................................................................................................9

2.1 Research on momentum strategies:......................................................................................9

2.2 Portfolio construction:........................................................................................................11

2.3 Analysis of the portfolio performance:..............................................................................14

2.3.1 Identifying whether winner stock outperform past loser stocks on average:..................14

2.3.2 Stating whether winner stock outperform average return of the 100 stocks:..................14

2.3.3 Recommending whether momentum strategy is good based on the analysis:................15

2.3.4 Changing he weightage calculation for detecting the change in performance of the

portfolio:...................................................................................................................................15

Part 3 Top-Down Analysis:......................................................................................................17

3.1 Economic Analysis:...........................................................................................................17

3.2 Industry Analysis:..............................................................................................................19

PORTFOLIO MANAGEMENT AND THEORY

2

3.3 Security Outlook:...............................................................................................................21

Conclusion:..............................................................................................................................22

Reference and Bibliography:....................................................................................................24

2

3.3 Security Outlook:...............................................................................................................21

Conclusion:..............................................................................................................................22

Reference and Bibliography:....................................................................................................24

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

3

Executive Summary:

The report directly focuses on detecting the adequate portfolio for Jack and Gloria, which

could eventually help them to generate higher rate of returns from investment to support their

retirement expenses. the relevant evaluation is conducted on different risk and return

attributes of Gloria and Jack to identify the minimum returns requirement and risk viability to

support the investment scope. the analysis of different sectors of ASX index is conducted,

which relatively helps in identifying the stocks that could be taken into consideration for

improving profitability of the superannuation fund. The advantages and disadvantages of

momentum analysis is also conducted to identify the minimum level of returns that could be

generated from an investment. however, the analysis of momentum trading strategy depicted

a negative Outlook, which relatively indicates that the ignorance of the trading strategy is

much more profitable for the investors, as it does not evaluate the stocks on the basis of

value. The different significant valuation of the momentum analysis is being conducted by

deriving different portfolios, which could support the recommendations for Jack and Gloria.

Furthermore, the evaluation of Telstra and AGL with the industry and country analysis

relatively indicate a low investment opportunity for the investors on the companies due to the

high volatility in effective. This relatively represents that ignoring the current investments

and energy and telecommunication sector would eventually allow the investors to generate

higher rate of returns from investment.

3

Executive Summary:

The report directly focuses on detecting the adequate portfolio for Jack and Gloria, which

could eventually help them to generate higher rate of returns from investment to support their

retirement expenses. the relevant evaluation is conducted on different risk and return

attributes of Gloria and Jack to identify the minimum returns requirement and risk viability to

support the investment scope. the analysis of different sectors of ASX index is conducted,

which relatively helps in identifying the stocks that could be taken into consideration for

improving profitability of the superannuation fund. The advantages and disadvantages of

momentum analysis is also conducted to identify the minimum level of returns that could be

generated from an investment. however, the analysis of momentum trading strategy depicted

a negative Outlook, which relatively indicates that the ignorance of the trading strategy is

much more profitable for the investors, as it does not evaluate the stocks on the basis of

value. The different significant valuation of the momentum analysis is being conducted by

deriving different portfolios, which could support the recommendations for Jack and Gloria.

Furthermore, the evaluation of Telstra and AGL with the industry and country analysis

relatively indicate a low investment opportunity for the investors on the companies due to the

high volatility in effective. This relatively represents that ignoring the current investments

and energy and telecommunication sector would eventually allow the investors to generate

higher rate of returns from investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

4

Introduction:

The overall assessment focuses on identifying the overall portfolio for Jack and

Gloria, which could help them through the superannuation period. In addition, the investment

policy statement of Jack and Gloria is mainly conducted in the assessment to identify the

return and risk attributes of the individuals. In addition, the evaluation of investment return is

conducted while identifying the standard got performance evaluation. Moreover, analysis of

the market indices is conducted to identify the performance of different asset classes listed in

ASX index. The portfolio construction is also conducted with the help of momentum analysis

to identify the best possible investment stocks for Jack and Gloria. Lastly, the security

analysis is mainly conducted on Telstra and AGL, while evaluating the economic and sundry

conduction in which the organisation was operating.

Part 1 Investment policy Statement:

1.1 Return objective:

The main objective of the investment policy statement is to generate adequate return

for supporting the retirement fund of Jack and Gloria. In addition, Jack and Gloria wants to

grow their current superannuation fund by inputting new financial instruments that is present

within the Australian stock market. The return needs to be calculated based on expenses,

which will Jack and Gloria incur after the retirement. The main retirement age for both the

couples is at the age of 65 years, where there will be no expenses regarding Mortgage

payments, as the loan would eventually mature in 30 years. The minimum return of $18,000

needs to be earned by the couple for supporting their expenses after retirement.

4

Introduction:

The overall assessment focuses on identifying the overall portfolio for Jack and

Gloria, which could help them through the superannuation period. In addition, the investment

policy statement of Jack and Gloria is mainly conducted in the assessment to identify the

return and risk attributes of the individuals. In addition, the evaluation of investment return is

conducted while identifying the standard got performance evaluation. Moreover, analysis of

the market indices is conducted to identify the performance of different asset classes listed in

ASX index. The portfolio construction is also conducted with the help of momentum analysis

to identify the best possible investment stocks for Jack and Gloria. Lastly, the security

analysis is mainly conducted on Telstra and AGL, while evaluating the economic and sundry

conduction in which the organisation was operating.

Part 1 Investment policy Statement:

1.1 Return objective:

The main objective of the investment policy statement is to generate adequate return

for supporting the retirement fund of Jack and Gloria. In addition, Jack and Gloria wants to

grow their current superannuation fund by inputting new financial instruments that is present

within the Australian stock market. The return needs to be calculated based on expenses,

which will Jack and Gloria incur after the retirement. The main retirement age for both the

couples is at the age of 65 years, where there will be no expenses regarding Mortgage

payments, as the loan would eventually mature in 30 years. The minimum return of $18,000

needs to be earned by the couple for supporting their expenses after retirement.

PORTFOLIO MANAGEMENT AND THEORY

5

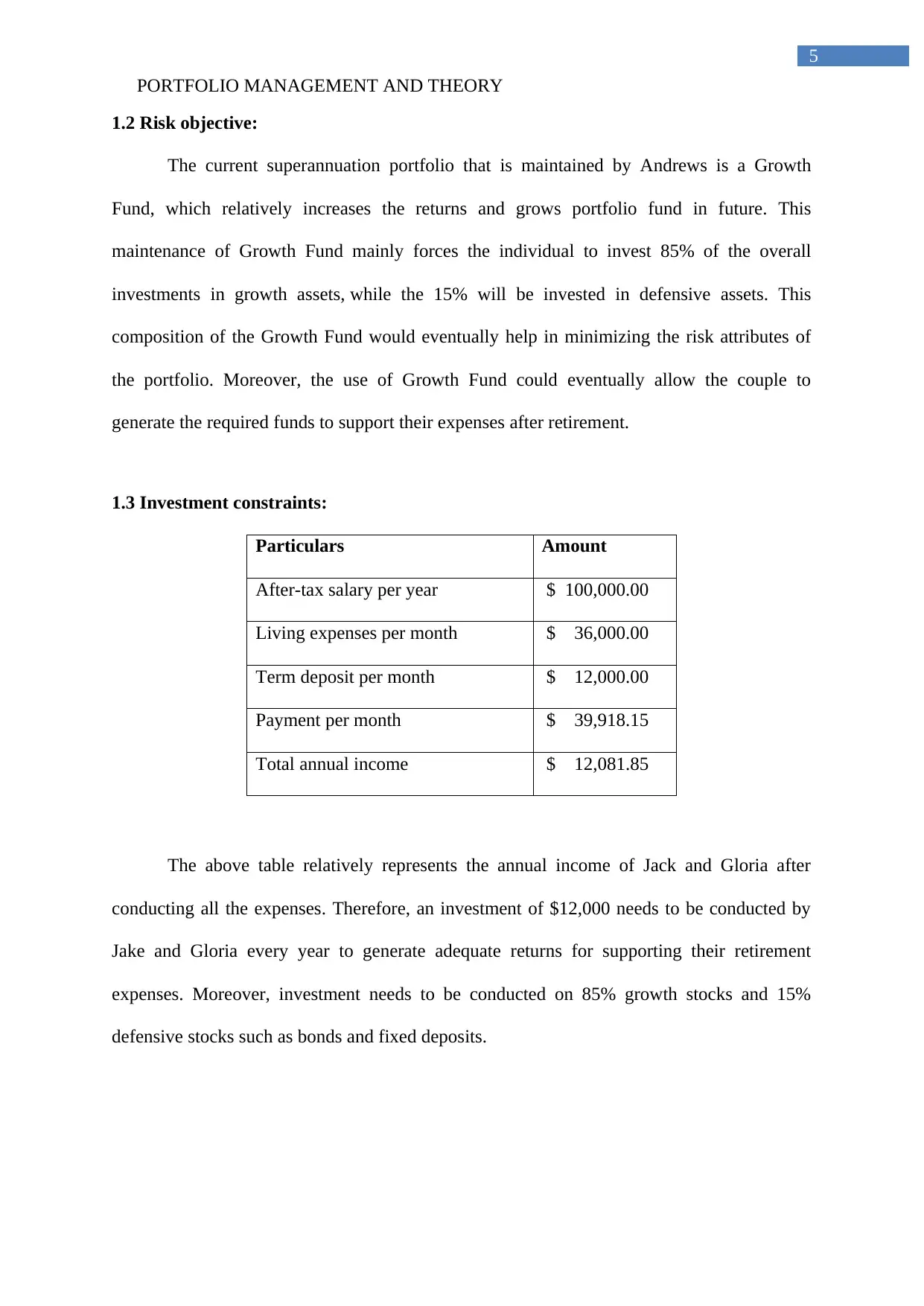

1.2 Risk objective:

The current superannuation portfolio that is maintained by Andrews is a Growth

Fund, which relatively increases the returns and grows portfolio fund in future. This

maintenance of Growth Fund mainly forces the individual to invest 85% of the overall

investments in growth assets, while the 15% will be invested in defensive assets. This

composition of the Growth Fund would eventually help in minimizing the risk attributes of

the portfolio. Moreover, the use of Growth Fund could eventually allow the couple to

generate the required funds to support their expenses after retirement.

1.3 Investment constraints:

Particulars Amount

After-tax salary per year $ 100,000.00

Living expenses per month $ 36,000.00

Term deposit per month $ 12,000.00

Payment per month $ 39,918.15

Total annual income $ 12,081.85

The above table relatively represents the annual income of Jack and Gloria after

conducting all the expenses. Therefore, an investment of $12,000 needs to be conducted by

Jake and Gloria every year to generate adequate returns for supporting their retirement

expenses. Moreover, investment needs to be conducted on 85% growth stocks and 15%

defensive stocks such as bonds and fixed deposits.

5

1.2 Risk objective:

The current superannuation portfolio that is maintained by Andrews is a Growth

Fund, which relatively increases the returns and grows portfolio fund in future. This

maintenance of Growth Fund mainly forces the individual to invest 85% of the overall

investments in growth assets, while the 15% will be invested in defensive assets. This

composition of the Growth Fund would eventually help in minimizing the risk attributes of

the portfolio. Moreover, the use of Growth Fund could eventually allow the couple to

generate the required funds to support their expenses after retirement.

1.3 Investment constraints:

Particulars Amount

After-tax salary per year $ 100,000.00

Living expenses per month $ 36,000.00

Term deposit per month $ 12,000.00

Payment per month $ 39,918.15

Total annual income $ 12,081.85

The above table relatively represents the annual income of Jack and Gloria after

conducting all the expenses. Therefore, an investment of $12,000 needs to be conducted by

Jake and Gloria every year to generate adequate returns for supporting their retirement

expenses. Moreover, investment needs to be conducted on 85% growth stocks and 15%

defensive stocks such as bonds and fixed deposits.

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

6

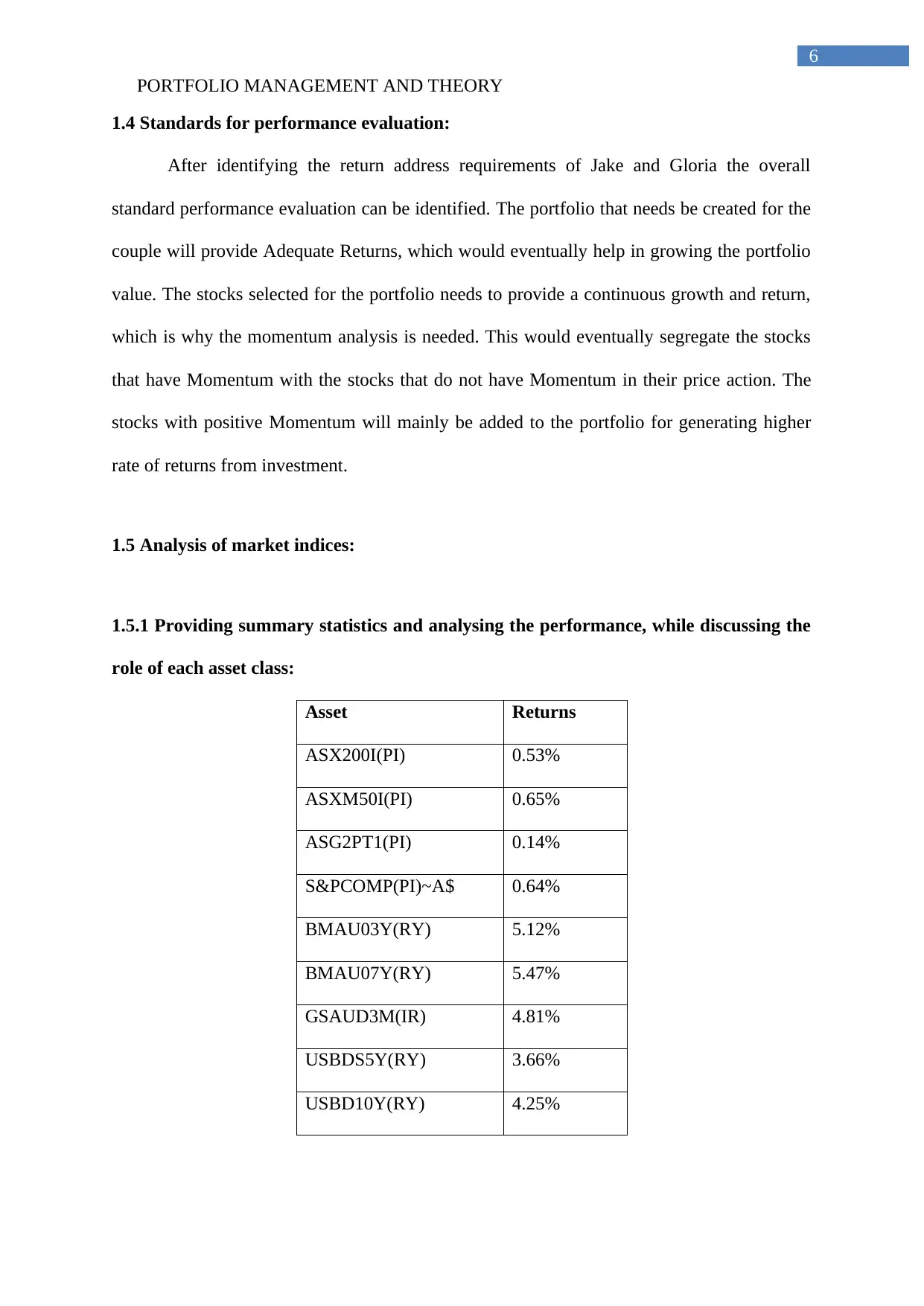

1.4 Standards for performance evaluation:

After identifying the return address requirements of Jake and Gloria the overall

standard performance evaluation can be identified. The portfolio that needs be created for the

couple will provide Adequate Returns, which would eventually help in growing the portfolio

value. The stocks selected for the portfolio needs to provide a continuous growth and return,

which is why the momentum analysis is needed. This would eventually segregate the stocks

that have Momentum with the stocks that do not have Momentum in their price action. The

stocks with positive Momentum will mainly be added to the portfolio for generating higher

rate of returns from investment.

1.5 Analysis of market indices:

1.5.1 Providing summary statistics and analysing the performance, while discussing the

role of each asset class:

Asset Returns

ASX200I(PI) 0.53%

ASXM50I(PI) 0.65%

ASG2PT1(PI) 0.14%

S&PCOMP(PI)~A$ 0.64%

BMAU03Y(RY) 5.12%

BMAU07Y(RY) 5.47%

GSAUD3M(IR) 4.81%

USBDS5Y(RY) 3.66%

USBD10Y(RY) 4.25%

6

1.4 Standards for performance evaluation:

After identifying the return address requirements of Jake and Gloria the overall

standard performance evaluation can be identified. The portfolio that needs be created for the

couple will provide Adequate Returns, which would eventually help in growing the portfolio

value. The stocks selected for the portfolio needs to provide a continuous growth and return,

which is why the momentum analysis is needed. This would eventually segregate the stocks

that have Momentum with the stocks that do not have Momentum in their price action. The

stocks with positive Momentum will mainly be added to the portfolio for generating higher

rate of returns from investment.

1.5 Analysis of market indices:

1.5.1 Providing summary statistics and analysing the performance, while discussing the

role of each asset class:

Asset Returns

ASX200I(PI) 0.53%

ASXM50I(PI) 0.65%

ASG2PT1(PI) 0.14%

S&PCOMP(PI)~A$ 0.64%

BMAU03Y(RY) 5.12%

BMAU07Y(RY) 5.47%

GSAUD3M(IR) 4.81%

USBDS5Y(RY) 3.66%

USBD10Y(RY) 4.25%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

7

And the overall evaluation performance of S&PCOMP(PI)~A$, ASXM50I(PI) and

ASX200I(PI) is identified to be the highest among the Asset class. However, the equity

section and bond section are a relevant part of the portfolio, as it helps in divesting the risky

stocks, while improving the returns from investment. Equity class a relatively provides high

growth and return generation capacity to the investors while having higher risk involvement

in Investments. However, the bond and treasury class a relatively provide a stable returns

with no risk, which in turn helps the investors to minimize the risk in their portfolio while

generating higher returns from investment (Szego, 2014).

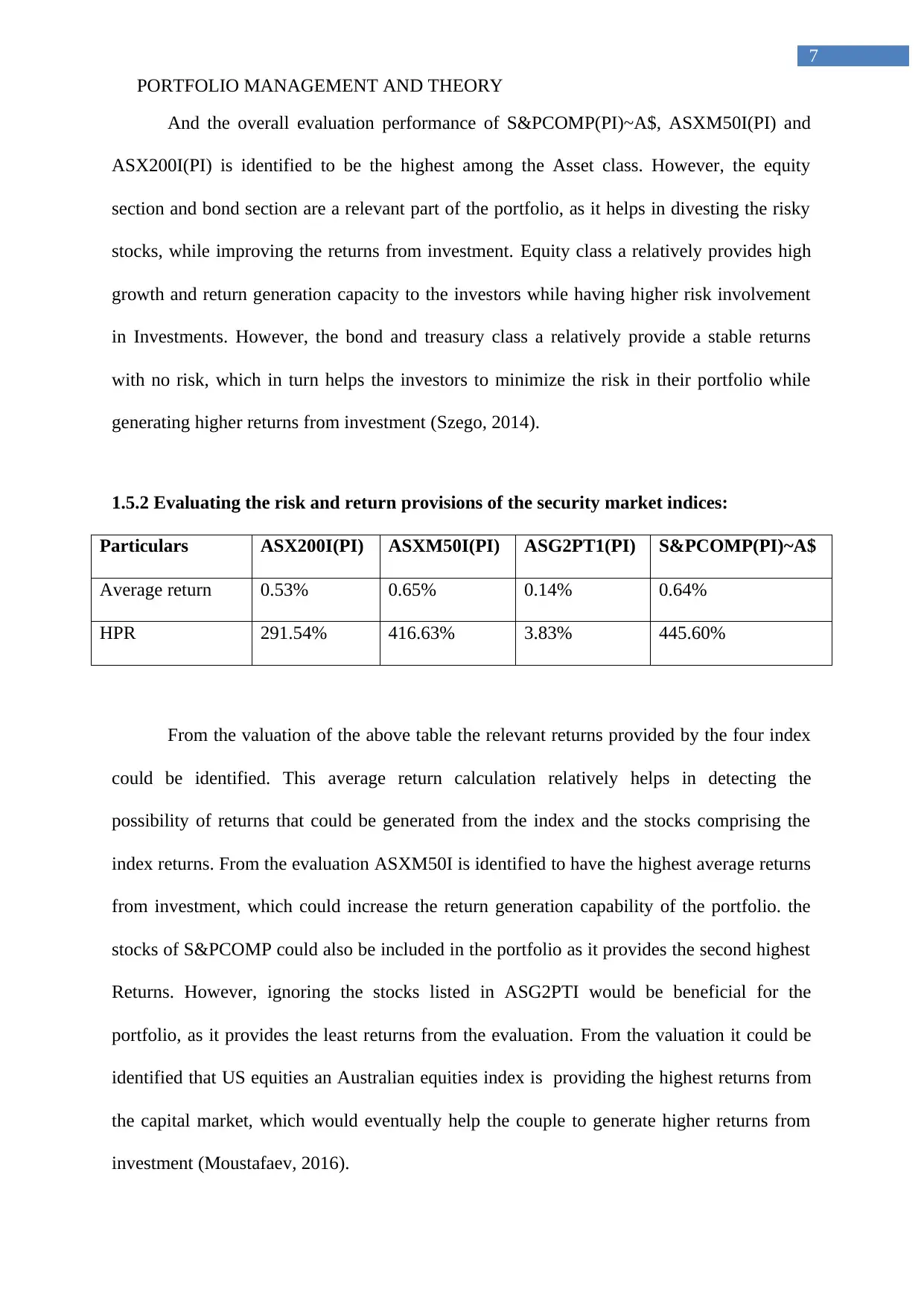

1.5.2 Evaluating the risk and return provisions of the security market indices:

Particulars ASX200I(PI) ASXM50I(PI) ASG2PT1(PI) S&PCOMP(PI)~A$

Average return 0.53% 0.65% 0.14% 0.64%

HPR 291.54% 416.63% 3.83% 445.60%

From the valuation of the above table the relevant returns provided by the four index

could be identified. This average return calculation relatively helps in detecting the

possibility of returns that could be generated from the index and the stocks comprising the

index returns. From the evaluation ASXM50I is identified to have the highest average returns

from investment, which could increase the return generation capability of the portfolio. the

stocks of S&PCOMP could also be included in the portfolio as it provides the second highest

Returns. However, ignoring the stocks listed in ASG2PTI would be beneficial for the

portfolio, as it provides the least returns from the evaluation. From the valuation it could be

identified that US equities an Australian equities index is providing the highest returns from

the capital market, which would eventually help the couple to generate higher returns from

investment (Moustafaev, 2016).

7

And the overall evaluation performance of S&PCOMP(PI)~A$, ASXM50I(PI) and

ASX200I(PI) is identified to be the highest among the Asset class. However, the equity

section and bond section are a relevant part of the portfolio, as it helps in divesting the risky

stocks, while improving the returns from investment. Equity class a relatively provides high

growth and return generation capacity to the investors while having higher risk involvement

in Investments. However, the bond and treasury class a relatively provide a stable returns

with no risk, which in turn helps the investors to minimize the risk in their portfolio while

generating higher returns from investment (Szego, 2014).

1.5.2 Evaluating the risk and return provisions of the security market indices:

Particulars ASX200I(PI) ASXM50I(PI) ASG2PT1(PI) S&PCOMP(PI)~A$

Average return 0.53% 0.65% 0.14% 0.64%

HPR 291.54% 416.63% 3.83% 445.60%

From the valuation of the above table the relevant returns provided by the four index

could be identified. This average return calculation relatively helps in detecting the

possibility of returns that could be generated from the index and the stocks comprising the

index returns. From the evaluation ASXM50I is identified to have the highest average returns

from investment, which could increase the return generation capability of the portfolio. the

stocks of S&PCOMP could also be included in the portfolio as it provides the second highest

Returns. However, ignoring the stocks listed in ASG2PTI would be beneficial for the

portfolio, as it provides the least returns from the evaluation. From the valuation it could be

identified that US equities an Australian equities index is providing the highest returns from

the capital market, which would eventually help the couple to generate higher returns from

investment (Moustafaev, 2016).

PORTFOLIO MANAGEMENT AND THEORY

8

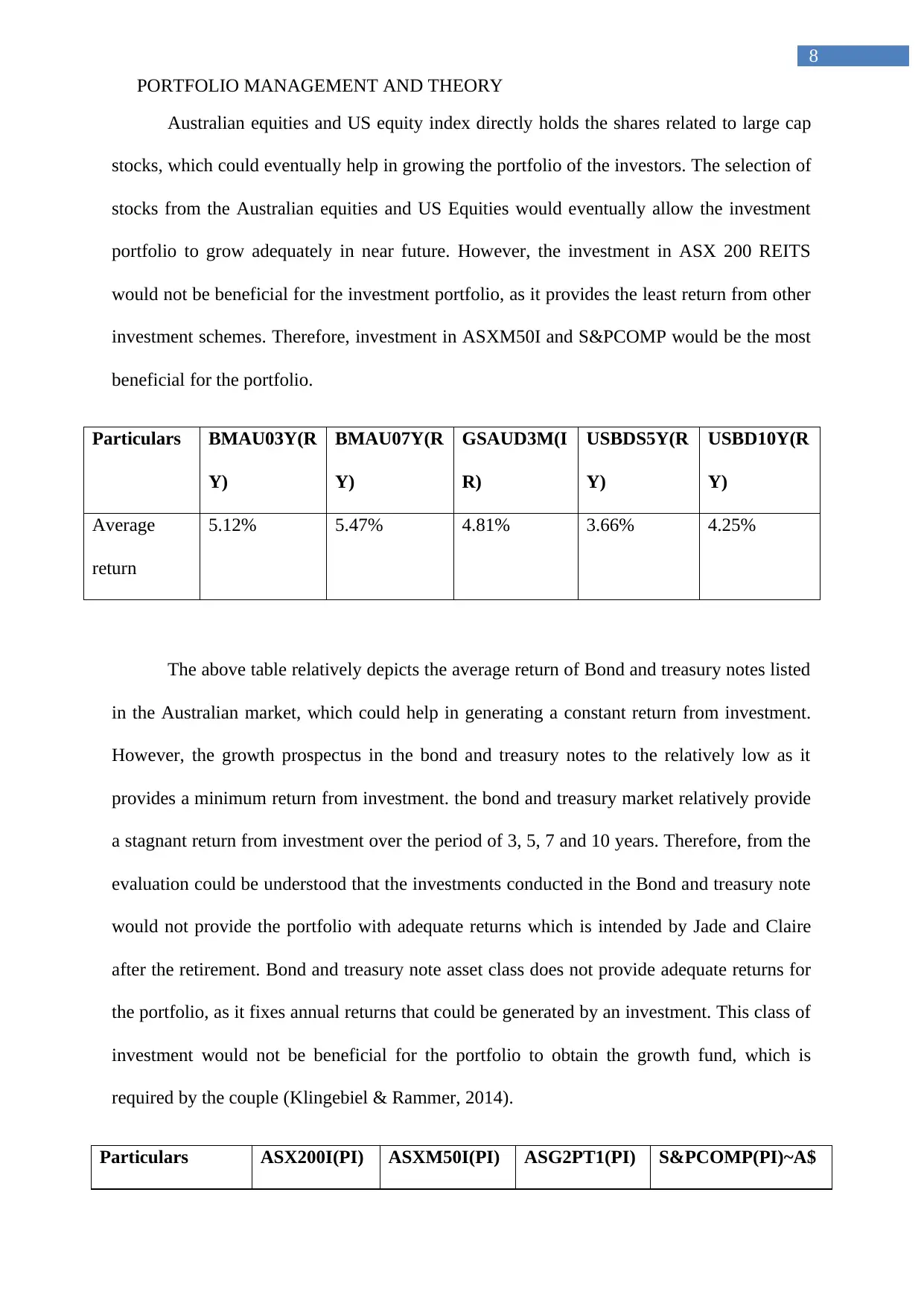

Australian equities and US equity index directly holds the shares related to large cap

stocks, which could eventually help in growing the portfolio of the investors. The selection of

stocks from the Australian equities and US Equities would eventually allow the investment

portfolio to grow adequately in near future. However, the investment in ASX 200 REITS

would not be beneficial for the investment portfolio, as it provides the least return from other

investment schemes. Therefore, investment in ASXM50I and S&PCOMP would be the most

beneficial for the portfolio.

Particulars BMAU03Y(R

Y)

BMAU07Y(R

Y)

GSAUD3M(I

R)

USBDS5Y(R

Y)

USBD10Y(R

Y)

Average

return

5.12% 5.47% 4.81% 3.66% 4.25%

The above table relatively depicts the average return of Bond and treasury notes listed

in the Australian market, which could help in generating a constant return from investment.

However, the growth prospectus in the bond and treasury notes to the relatively low as it

provides a minimum return from investment. the bond and treasury market relatively provide

a stagnant return from investment over the period of 3, 5, 7 and 10 years. Therefore, from the

evaluation could be understood that the investments conducted in the Bond and treasury note

would not provide the portfolio with adequate returns which is intended by Jade and Claire

after the retirement. Bond and treasury note asset class does not provide adequate returns for

the portfolio, as it fixes annual returns that could be generated by an investment. This class of

investment would not be beneficial for the portfolio to obtain the growth fund, which is

required by the couple (Klingebiel & Rammer, 2014).

Particulars ASX200I(PI) ASXM50I(PI) ASG2PT1(PI) S&PCOMP(PI)~A$

8

Australian equities and US equity index directly holds the shares related to large cap

stocks, which could eventually help in growing the portfolio of the investors. The selection of

stocks from the Australian equities and US Equities would eventually allow the investment

portfolio to grow adequately in near future. However, the investment in ASX 200 REITS

would not be beneficial for the investment portfolio, as it provides the least return from other

investment schemes. Therefore, investment in ASXM50I and S&PCOMP would be the most

beneficial for the portfolio.

Particulars BMAU03Y(R

Y)

BMAU07Y(R

Y)

GSAUD3M(I

R)

USBDS5Y(R

Y)

USBD10Y(R

Y)

Average

return

5.12% 5.47% 4.81% 3.66% 4.25%

The above table relatively depicts the average return of Bond and treasury notes listed

in the Australian market, which could help in generating a constant return from investment.

However, the growth prospectus in the bond and treasury notes to the relatively low as it

provides a minimum return from investment. the bond and treasury market relatively provide

a stagnant return from investment over the period of 3, 5, 7 and 10 years. Therefore, from the

evaluation could be understood that the investments conducted in the Bond and treasury note

would not provide the portfolio with adequate returns which is intended by Jade and Claire

after the retirement. Bond and treasury note asset class does not provide adequate returns for

the portfolio, as it fixes annual returns that could be generated by an investment. This class of

investment would not be beneficial for the portfolio to obtain the growth fund, which is

required by the couple (Klingebiel & Rammer, 2014).

Particulars ASX200I(PI) ASXM50I(PI) ASG2PT1(PI) S&PCOMP(PI)~A$

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

9

Standard deviation 3.93% 4.42% 4.77% 3.91%

The above table collectively represents the standard deviation of the four-different

asset class that could be used in formulating the portfolio of Jake and Claire. the overall risk

assessment relatively indicates that S&PCOMP has the lowest risk attributes from investment

following the ASX200I and ASXM50I, which could be used to formulate the portfolio that

would obtain high growth rate in future. However, ASG2PTI has the highest risk attributes

from investment, which needs to be ignored during the formulation of the portfolio.

Therefore, the use of stocks from ASX200I and ASXM50I and S&PCOMP would eventually

allow Jake and Claire to generate the adequate returns from investment to support the Growth

Fund. The bond and treasury section does not have any kind of risk involved in investment,

as it is the risk-free investment (Lynn & Hao, 2015).

1.6 Recommendations:

Therefore, with the combination of ASX200I and ASXM50I and S&PCOMP

comprising 85% of the portfolio with ASXM50I(PI) and ASG2PTI(PI) comprising the rest

15% Jake and Clare to get their growth fund, which might generate exponential returns. This

comprised portfolio could allow Jake and Clair to generate adequate returns to support their

expenses after the retirement.

Part 2 Active Portfolio:

2.1 Research on momentum strategies:

Investors use the investment strategy to detect the overall trend of the market, which

might eventually help in improving the returns that could be generated from investment.

9

Standard deviation 3.93% 4.42% 4.77% 3.91%

The above table collectively represents the standard deviation of the four-different

asset class that could be used in formulating the portfolio of Jake and Claire. the overall risk

assessment relatively indicates that S&PCOMP has the lowest risk attributes from investment

following the ASX200I and ASXM50I, which could be used to formulate the portfolio that

would obtain high growth rate in future. However, ASG2PTI has the highest risk attributes

from investment, which needs to be ignored during the formulation of the portfolio.

Therefore, the use of stocks from ASX200I and ASXM50I and S&PCOMP would eventually

allow Jake and Claire to generate the adequate returns from investment to support the Growth

Fund. The bond and treasury section does not have any kind of risk involved in investment,

as it is the risk-free investment (Lynn & Hao, 2015).

1.6 Recommendations:

Therefore, with the combination of ASX200I and ASXM50I and S&PCOMP

comprising 85% of the portfolio with ASXM50I(PI) and ASG2PTI(PI) comprising the rest

15% Jake and Clare to get their growth fund, which might generate exponential returns. This

comprised portfolio could allow Jake and Clair to generate adequate returns to support their

expenses after the retirement.

Part 2 Active Portfolio:

2.1 Research on momentum strategies:

Investors use the investment strategy to detect the overall trend of the market, which

might eventually help in improving the returns that could be generated from investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

10

Moreover, the momentum investing strategy directly involve long term trading provisions,

which needs to be conducted by individuals to generate higher rate of return from investment.

The strategy relatively focuses on identifying the upper trending stocks, which could be used

during the portfolio creation. However, the momentum strategy does not provide adequate

knowledge regarding the risk and return attributes of the stock, which can be identified as its

major disadvantage. Moreover, the investment strategy Relatively focuses on establishing or

detecting a relevant Trend which could be used in maximizing the profits of the investors

(Asparouhova et al., 2014).

Moreover, with the help of momentum investing strategy investors can detect price

movement is for the trend moving gives the trend identified by the strategy. this relatively

close the investors to detect major reversals, which could reduce the losses from investment,

while providing an adequate investment opportunity to the investors. Moreover, Momentum

is identified to be a short-term strategy indicator, which relatively focuses on short duration

of historical price to determine the actual and current position of the stocks. Furthermore,

Momentum strategy is not concerned with the operational performance of the stock it directly

focuses on the changing trend value of a stock to determine the investment opportunity. In

addition, the momentum strategy can be identified as an indicator which thrives on investor

emotions, which would eventually help in detecting the investment opportunity for the

investors (Stettina & Horz, 2015).

The momentum trading utilizes changes in price which is conducted by stocks

overtime, while providing an adequate investment opportunity to the investors. the evaluation

of price change is derived by moving averages, which could eventually help investors in

detecting the trend of the stock. this trend detection is the momentum indicator which allows

investors to identify whether the trend is positive or negative. Investors utilize the

10

Moreover, the momentum investing strategy directly involve long term trading provisions,

which needs to be conducted by individuals to generate higher rate of return from investment.

The strategy relatively focuses on identifying the upper trending stocks, which could be used

during the portfolio creation. However, the momentum strategy does not provide adequate

knowledge regarding the risk and return attributes of the stock, which can be identified as its

major disadvantage. Moreover, the investment strategy Relatively focuses on establishing or

detecting a relevant Trend which could be used in maximizing the profits of the investors

(Asparouhova et al., 2014).

Moreover, with the help of momentum investing strategy investors can detect price

movement is for the trend moving gives the trend identified by the strategy. this relatively

close the investors to detect major reversals, which could reduce the losses from investment,

while providing an adequate investment opportunity to the investors. Moreover, Momentum

is identified to be a short-term strategy indicator, which relatively focuses on short duration

of historical price to determine the actual and current position of the stocks. Furthermore,

Momentum strategy is not concerned with the operational performance of the stock it directly

focuses on the changing trend value of a stock to determine the investment opportunity. In

addition, the momentum strategy can be identified as an indicator which thrives on investor

emotions, which would eventually help in detecting the investment opportunity for the

investors (Stettina & Horz, 2015).

The momentum trading utilizes changes in price which is conducted by stocks

overtime, while providing an adequate investment opportunity to the investors. the evaluation

of price change is derived by moving averages, which could eventually help investors in

detecting the trend of the stock. this trend detection is the momentum indicator which allows

investors to identify whether the trend is positive or negative. Investors utilize the

PORTFOLIO MANAGEMENT AND THEORY

11

information for short term trades and identify major reversals, which could provide the

maximum returns from their investment (Gutiérrez & Magnusson, 2014).

2.2 Portfolio construction:

Jun-06

Dec-06

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

Portfolio 1 Average Returns

Jun-06

Dec-06

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Portfolio 2 Average Returns

11

information for short term trades and identify major reversals, which could provide the

maximum returns from their investment (Gutiérrez & Magnusson, 2014).

2.2 Portfolio construction:

Jun-06

Dec-06

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

Portfolio 1 Average Returns

Jun-06

Dec-06

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Portfolio 2 Average Returns

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

12

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Portfolio 3 Average Returns

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Portfolio 4 Average Returns

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Portfolio 5 Average Returns

12

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Portfolio 3 Average Returns

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Portfolio 4 Average Returns

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Portfolio 5 Average Returns

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

13

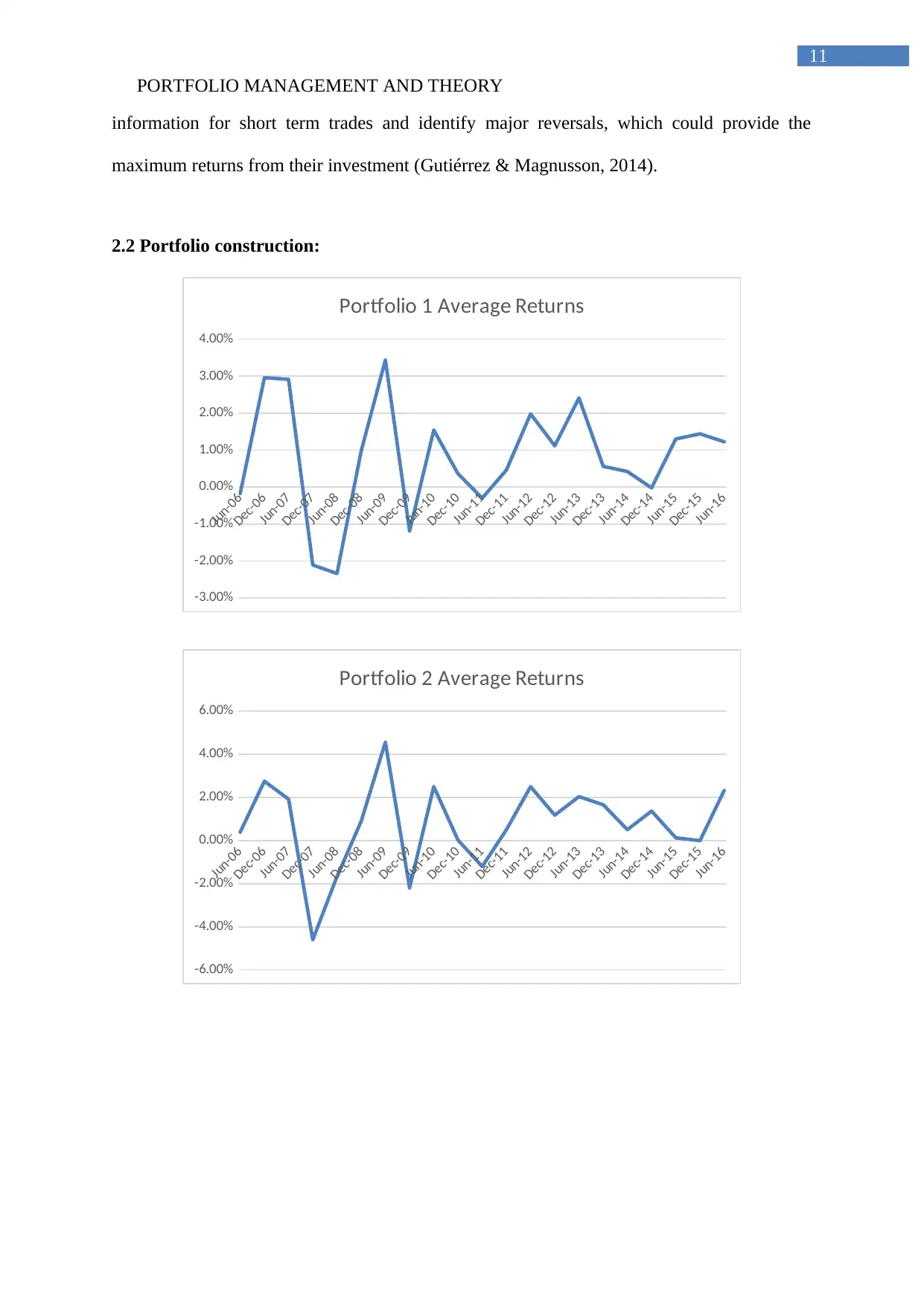

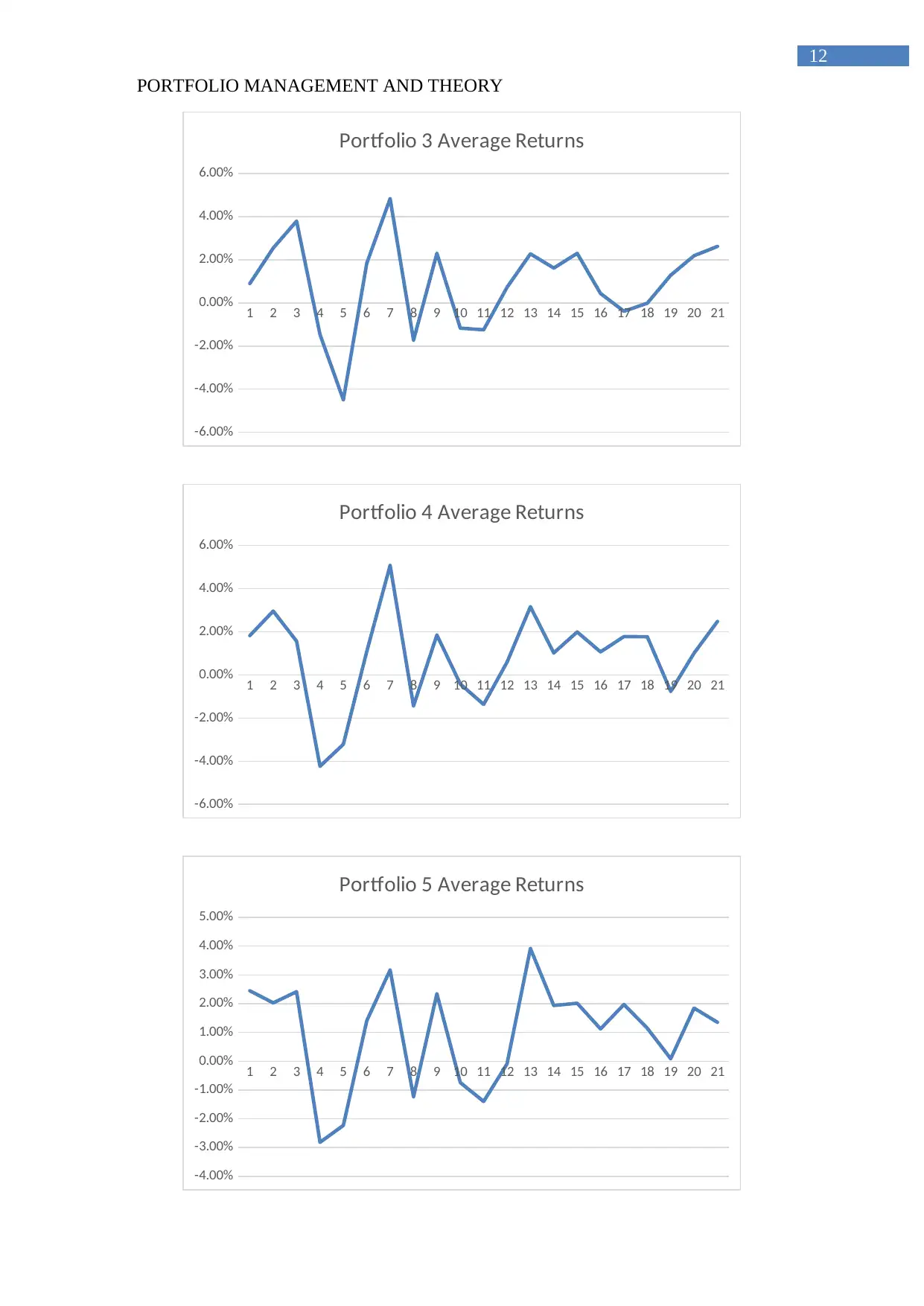

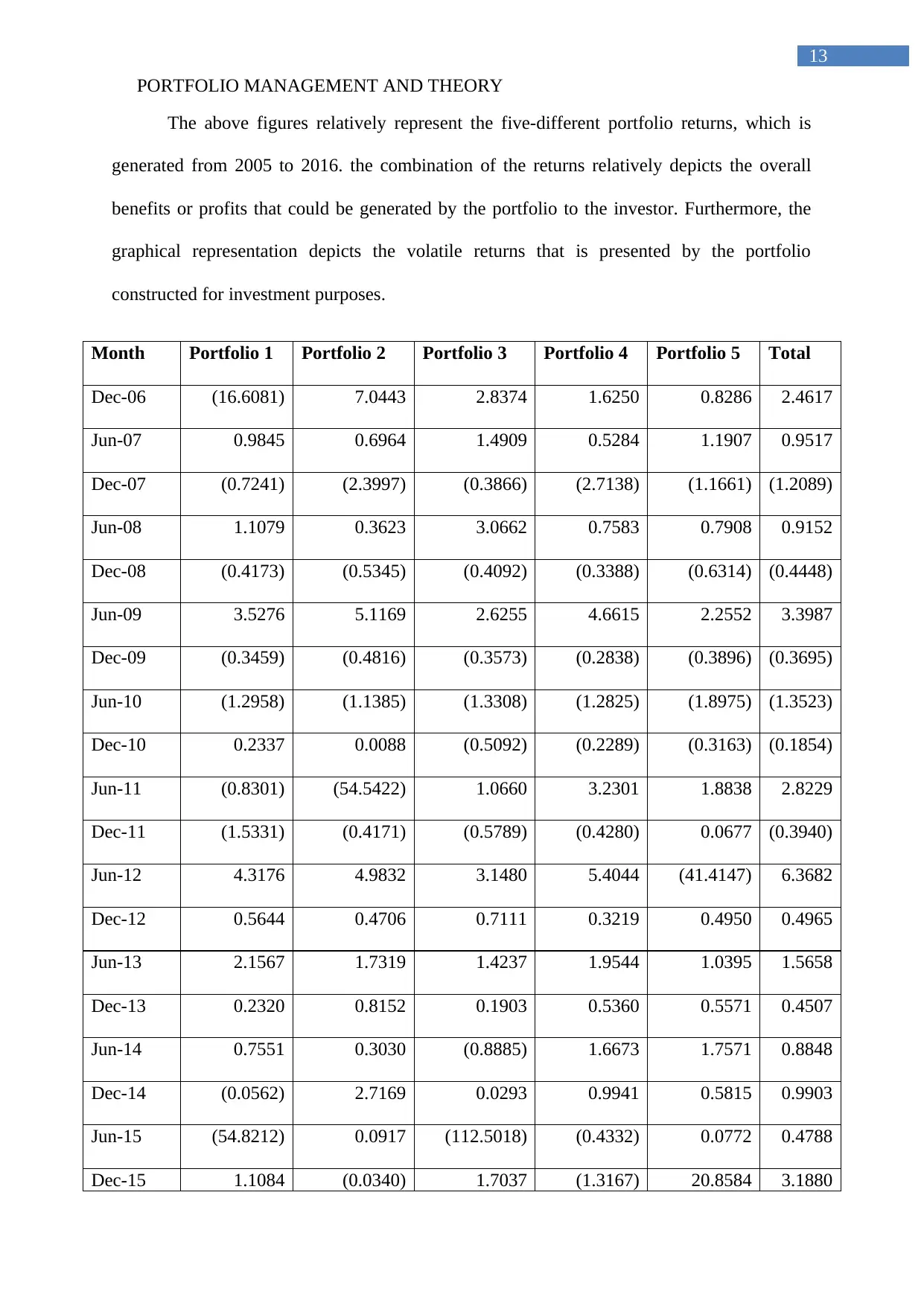

The above figures relatively represent the five-different portfolio returns, which is

generated from 2005 to 2016. the combination of the returns relatively depicts the overall

benefits or profits that could be generated by the portfolio to the investor. Furthermore, the

graphical representation depicts the volatile returns that is presented by the portfolio

constructed for investment purposes.

Month Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5 Total

Dec-06 (16.6081) 7.0443 2.8374 1.6250 0.8286 2.4617

Jun-07 0.9845 0.6964 1.4909 0.5284 1.1907 0.9517

Dec-07 (0.7241) (2.3997) (0.3866) (2.7138) (1.1661) (1.2089)

Jun-08 1.1079 0.3623 3.0662 0.7583 0.7908 0.9152

Dec-08 (0.4173) (0.5345) (0.4092) (0.3388) (0.6314) (0.4448)

Jun-09 3.5276 5.1169 2.6255 4.6615 2.2552 3.3987

Dec-09 (0.3459) (0.4816) (0.3573) (0.2838) (0.3896) (0.3695)

Jun-10 (1.2958) (1.1385) (1.3308) (1.2825) (1.8975) (1.3523)

Dec-10 0.2337 0.0088 (0.5092) (0.2289) (0.3163) (0.1854)

Jun-11 (0.8301) (54.5422) 1.0660 3.2301 1.8838 2.8229

Dec-11 (1.5331) (0.4171) (0.5789) (0.4280) 0.0677 (0.3940)

Jun-12 4.3176 4.9832 3.1480 5.4044 (41.4147) 6.3682

Dec-12 0.5644 0.4706 0.7111 0.3219 0.4950 0.4965

Jun-13 2.1567 1.7319 1.4237 1.9544 1.0395 1.5658

Dec-13 0.2320 0.8152 0.1903 0.5360 0.5571 0.4507

Jun-14 0.7551 0.3030 (0.8885) 1.6673 1.7571 0.8848

Dec-14 (0.0562) 2.7169 0.0293 0.9941 0.5815 0.9903

Jun-15 (54.8212) 0.0917 (112.5018) (0.4332) 0.0772 0.4788

Dec-15 1.1084 (0.0340) 1.7037 (1.3167) 20.8584 3.1880

13

The above figures relatively represent the five-different portfolio returns, which is

generated from 2005 to 2016. the combination of the returns relatively depicts the overall

benefits or profits that could be generated by the portfolio to the investor. Furthermore, the

graphical representation depicts the volatile returns that is presented by the portfolio

constructed for investment purposes.

Month Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5 Total

Dec-06 (16.6081) 7.0443 2.8374 1.6250 0.8286 2.4617

Jun-07 0.9845 0.6964 1.4909 0.5284 1.1907 0.9517

Dec-07 (0.7241) (2.3997) (0.3866) (2.7138) (1.1661) (1.2089)

Jun-08 1.1079 0.3623 3.0662 0.7583 0.7908 0.9152

Dec-08 (0.4173) (0.5345) (0.4092) (0.3388) (0.6314) (0.4448)

Jun-09 3.5276 5.1169 2.6255 4.6615 2.2552 3.3987

Dec-09 (0.3459) (0.4816) (0.3573) (0.2838) (0.3896) (0.3695)

Jun-10 (1.2958) (1.1385) (1.3308) (1.2825) (1.8975) (1.3523)

Dec-10 0.2337 0.0088 (0.5092) (0.2289) (0.3163) (0.1854)

Jun-11 (0.8301) (54.5422) 1.0660 3.2301 1.8838 2.8229

Dec-11 (1.5331) (0.4171) (0.5789) (0.4280) 0.0677 (0.3940)

Jun-12 4.3176 4.9832 3.1480 5.4044 (41.4147) 6.3682

Dec-12 0.5644 0.4706 0.7111 0.3219 0.4950 0.4965

Jun-13 2.1567 1.7319 1.4237 1.9544 1.0395 1.5658

Dec-13 0.2320 0.8152 0.1903 0.5360 0.5571 0.4507

Jun-14 0.7551 0.3030 (0.8885) 1.6673 1.7571 0.8848

Dec-14 (0.0562) 2.7169 0.0293 0.9941 0.5815 0.9903

Jun-15 (54.8212) 0.0917 (112.5018) (0.4332) 0.0772 0.4788

Dec-15 1.1084 (0.0340) 1.7037 (1.3167) 20.8584 3.1880

PORTFOLIO MANAGEMENT AND THEORY

14

Jun-16 0.8491 (545.7905) 1.1969 2.4623 0.7326 1.5435

2.3 Analysis of the portfolio performance:

2.3.1 Identifying whether winner stock outperform past loser stocks on average:

From the overall evaluation the winner’s stocks did not outperform the losers stock

during the fading period of 10 years, which could eventually indicate the low reliability of the

momentum indicator. Moreover, the ending value of loser stocks was at the levels of 0.8491

while the winner stock value was at the levels of 0.732, which is relatively lower and

indicates the loopholes in momentum strategy. Furthermore, the analysis also indicates that

the relevant profitability of both the strategy was not adequate to generate a higher return

from the investment of $1. Therefore, both the strategy would provide losses to the investor,

which hampering the investment capital. In this context, Rank, Unger & Gemunden (2015)

stated that investors utilize the trading indicators to identify trends, which could eventually

help in improving their trading profitability for short duration.

2.3.2 Stating whether winner stock outperform average return of the 100 stocks:

The evaluation of the calculations also indicates that the winner’s talks did not

outperform the 100 stocks portfolio, as the returns provided by the hundred-stock portfolio is

relatively higher. the hundred-stock portfolio mainly provides the last return of 1.5425, while

the winner stocks provided or return of 0.8491, which is a relatively lower and would not

provide investors with higher rate of return. Therefore, it could be said that the hundred

stocks would eventually provide a higher rate of return due to the diversification of the

stocks. Kock, Heising & Gemünden (2015) argued that without adequate investigation and

14

Jun-16 0.8491 (545.7905) 1.1969 2.4623 0.7326 1.5435

2.3 Analysis of the portfolio performance:

2.3.1 Identifying whether winner stock outperform past loser stocks on average:

From the overall evaluation the winner’s stocks did not outperform the losers stock

during the fading period of 10 years, which could eventually indicate the low reliability of the

momentum indicator. Moreover, the ending value of loser stocks was at the levels of 0.8491

while the winner stock value was at the levels of 0.732, which is relatively lower and

indicates the loopholes in momentum strategy. Furthermore, the analysis also indicates that

the relevant profitability of both the strategy was not adequate to generate a higher return

from the investment of $1. Therefore, both the strategy would provide losses to the investor,

which hampering the investment capital. In this context, Rank, Unger & Gemunden (2015)

stated that investors utilize the trading indicators to identify trends, which could eventually

help in improving their trading profitability for short duration.

2.3.2 Stating whether winner stock outperform average return of the 100 stocks:

The evaluation of the calculations also indicates that the winner’s talks did not

outperform the 100 stocks portfolio, as the returns provided by the hundred-stock portfolio is

relatively higher. the hundred-stock portfolio mainly provides the last return of 1.5425, while

the winner stocks provided or return of 0.8491, which is a relatively lower and would not

provide investors with higher rate of return. Therefore, it could be said that the hundred

stocks would eventually provide a higher rate of return due to the diversification of the

stocks. Kock, Heising & Gemünden (2015) argued that without adequate investigation and

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

15

research investors are not able to Improve the level of returns that could be generated from

investment, while anticipating the risk from an investment.

2.3.3 Recommending whether momentum strategy is good based on the analysis:

From the overall evaluation that could be identified that Momentum strategy is not the

best possible way for creating a Portfolio and maintaining it throughout the long-term

phase. Moreover, the momentum strategy was not able to identify stocks that could generate a

relevant return from investment on a constant basis, while it only provided stocks that have a

relevant Trend. Therefore, investing reboot full you based on momentum strategy would not

be feasible for the investors, as relevant changes in the portfolio needs to be conducted for the

period due to the change in momentum trend of stocks. This would eventually increase

problems for investor while raising the level of transaction charges for the individual.

Therefore, Momentum strategy needs to be ignored by the investors as it is an indicator

which only focuses on trend analysis and does not provide the actual value of the stock. On

the other hand, if investors use value analysis such as dividend discount model or Fama

French model, then the return generation capability of the portfolio relatively increases.

2.3.4 Changing he weightage calculation for detecting the change in performance of the

portfolio:

Month Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

Dec-06 6.9040 1.3805 1.9678 0.5956 0.7537

Jun-07 0.4438 1.0201 1.3980 0.5612 0.8771

Dec-07 (1.5699) (1.1435) 0.3959 (2.2479) (1.8459)

Jun-08 0.1851 0.6686 (5.0540) 0.7491 0.4166

Dec-08 (3.0711) (0.4350) (0.2906) (1.0312) (0.6771)

15

research investors are not able to Improve the level of returns that could be generated from

investment, while anticipating the risk from an investment.

2.3.3 Recommending whether momentum strategy is good based on the analysis:

From the overall evaluation that could be identified that Momentum strategy is not the

best possible way for creating a Portfolio and maintaining it throughout the long-term

phase. Moreover, the momentum strategy was not able to identify stocks that could generate a

relevant return from investment on a constant basis, while it only provided stocks that have a

relevant Trend. Therefore, investing reboot full you based on momentum strategy would not

be feasible for the investors, as relevant changes in the portfolio needs to be conducted for the

period due to the change in momentum trend of stocks. This would eventually increase

problems for investor while raising the level of transaction charges for the individual.

Therefore, Momentum strategy needs to be ignored by the investors as it is an indicator

which only focuses on trend analysis and does not provide the actual value of the stock. On

the other hand, if investors use value analysis such as dividend discount model or Fama

French model, then the return generation capability of the portfolio relatively increases.

2.3.4 Changing he weightage calculation for detecting the change in performance of the

portfolio:

Month Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

Dec-06 6.9040 1.3805 1.9678 0.5956 0.7537

Jun-07 0.4438 1.0201 1.3980 0.5612 0.8771

Dec-07 (1.5699) (1.1435) 0.3959 (2.2479) (1.8459)

Jun-08 0.1851 0.6686 (5.0540) 0.7491 0.4166

Dec-08 (3.0711) (0.4350) (0.2906) (1.0312) (0.6771)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

16

Jun-09 1.4661 4.2417 2.1695 2.0329 4.7321

Dec-09 0.0801 (0.0680) (0.5343) (0.0064) (0.2711)

Jun-10 2.9331 (10.7639) (0.9437) (71.1760) (4.3859)

Dec-10 2.3031 0.9130 (1.6346) (0.3070) 0.2027

Jun-11 (0.9084) 0.1321 1.3521 4.5767 0.1616

Dec-11 (0.7112) 6.2562 0.2482 0.4620 (0.5816)

Jun-12 3.6303 1.1770 (5.1986) (4.4246) (49.1243)

Dec-12 0.4446 0.8214 0.6059 0.4472 0.9436

Jun-13 1.1941 0.5378 0.8116 1.4369 0.5964

Dec-13 0.6641 2.1947 0.1475 1.0697 0.6560

Jun-14 0.5415 0.5060 2.3863 0.7284 2.1059

Dec-14 0.1980 1.8383 (2.9124) 0.4835 0.4572

Jun-15 6.5504 0.6173 (1.3056) (0.7472) 0.8904

Dec-15 2.6848 1.9824 0.9328 (3.7571) 2.0038

Jun-16 1.0612 0.8654 1.1512 1.2526 0.6722

After changing weights of the portfolio, the overall rate of return that could be

provided by the stocks has a relatively changed, which directly indicates the significance of

weights in formulating a Portfolio. The above table relatively represents the overall returns

that could be generated from portfolio 1 to portfolio 5 during the period of the analysis if

relevant changes in the weights can be conducted. therefore, it could be stated that with the

changes in be your all photo you can be created with the help of momentum trading to

improve the returns from investment. However, the determination of the ways is relatively

the main factor which might affect the profitability and reliability of the investment. Hence,

16

Jun-09 1.4661 4.2417 2.1695 2.0329 4.7321

Dec-09 0.0801 (0.0680) (0.5343) (0.0064) (0.2711)

Jun-10 2.9331 (10.7639) (0.9437) (71.1760) (4.3859)

Dec-10 2.3031 0.9130 (1.6346) (0.3070) 0.2027

Jun-11 (0.9084) 0.1321 1.3521 4.5767 0.1616

Dec-11 (0.7112) 6.2562 0.2482 0.4620 (0.5816)

Jun-12 3.6303 1.1770 (5.1986) (4.4246) (49.1243)

Dec-12 0.4446 0.8214 0.6059 0.4472 0.9436

Jun-13 1.1941 0.5378 0.8116 1.4369 0.5964

Dec-13 0.6641 2.1947 0.1475 1.0697 0.6560

Jun-14 0.5415 0.5060 2.3863 0.7284 2.1059

Dec-14 0.1980 1.8383 (2.9124) 0.4835 0.4572

Jun-15 6.5504 0.6173 (1.3056) (0.7472) 0.8904

Dec-15 2.6848 1.9824 0.9328 (3.7571) 2.0038

Jun-16 1.0612 0.8654 1.1512 1.2526 0.6722

After changing weights of the portfolio, the overall rate of return that could be

provided by the stocks has a relatively changed, which directly indicates the significance of

weights in formulating a Portfolio. The above table relatively represents the overall returns

that could be generated from portfolio 1 to portfolio 5 during the period of the analysis if

relevant changes in the weights can be conducted. therefore, it could be stated that with the

changes in be your all photo you can be created with the help of momentum trading to

improve the returns from investment. However, the determination of the ways is relatively

the main factor which might affect the profitability and reliability of the investment. Hence,

PORTFOLIO MANAGEMENT AND THEORY

17

the momentum strategy does not provide adequate returns from investment, while hampering

the profits, which could be generated overtime.

Part 3 Top-Down Analysis:

3.1 Economic Analysis:

The economic analysis of Australia is relatively positive as the overall GDP and

capital market of the country is relatively growing. The overall progress can be evaluated

from the following analysis of Australian index and GDP.

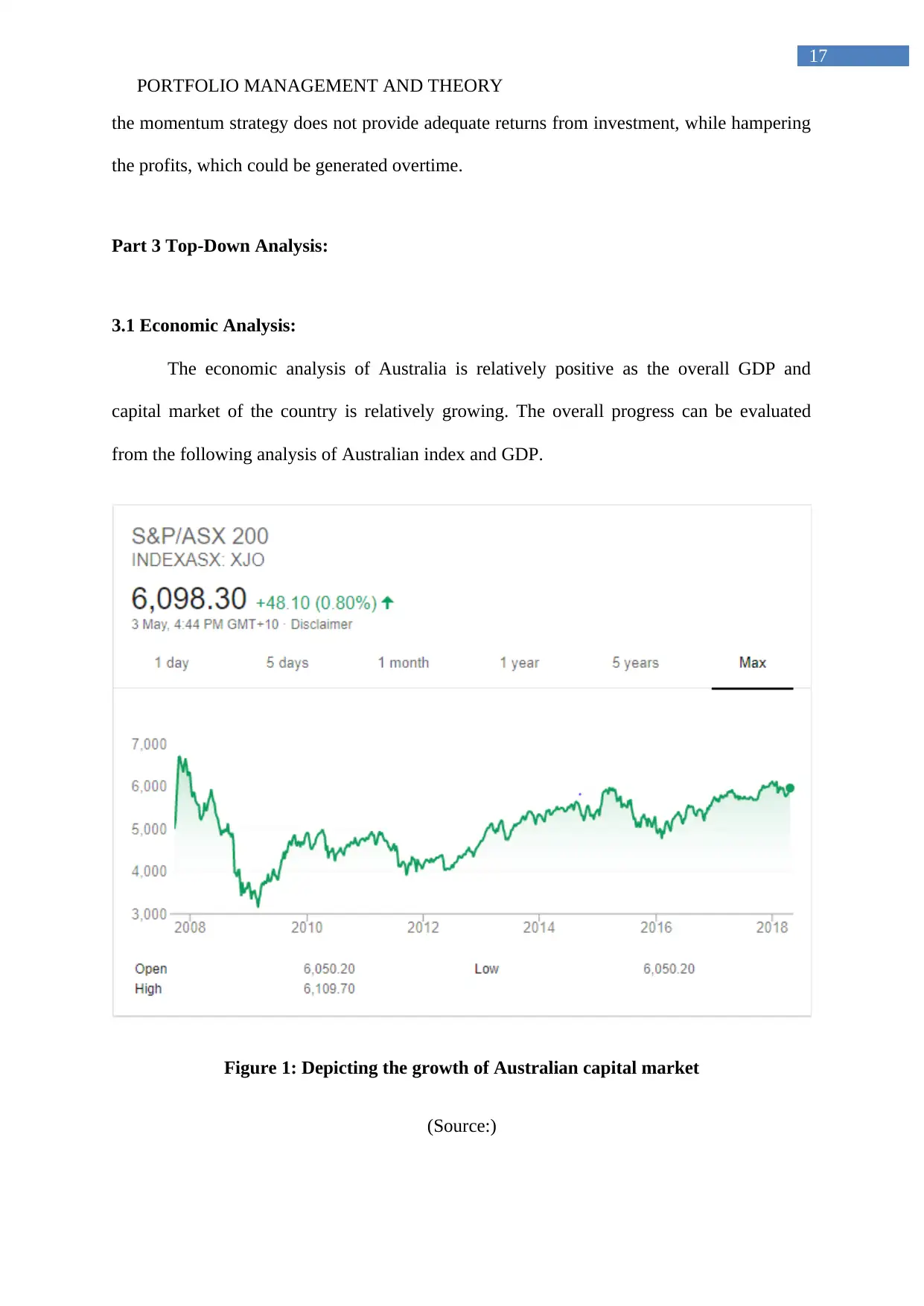

Figure 1: Depicting the growth of Australian capital market

(Source:)

17

the momentum strategy does not provide adequate returns from investment, while hampering

the profits, which could be generated overtime.

Part 3 Top-Down Analysis:

3.1 Economic Analysis:

The economic analysis of Australia is relatively positive as the overall GDP and

capital market of the country is relatively growing. The overall progress can be evaluated

from the following analysis of Australian index and GDP.

Figure 1: Depicting the growth of Australian capital market

(Source:)

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

18

From the valuation it could be identified that after 2009 new road progress of the

Australian market could be seen, which might eventually help the investors to generate higher

rate of returns from investment, Moreover the evaluation directly indicates growth in the

index for past 5 years, which relatively allowed the investors to generate higher rate of

returns from investment. Therefore, it could be understood that the current economic position

in Australia as a relatively positive, which would eventually benefit investors as the capital

market is generating higher value on each trading day.

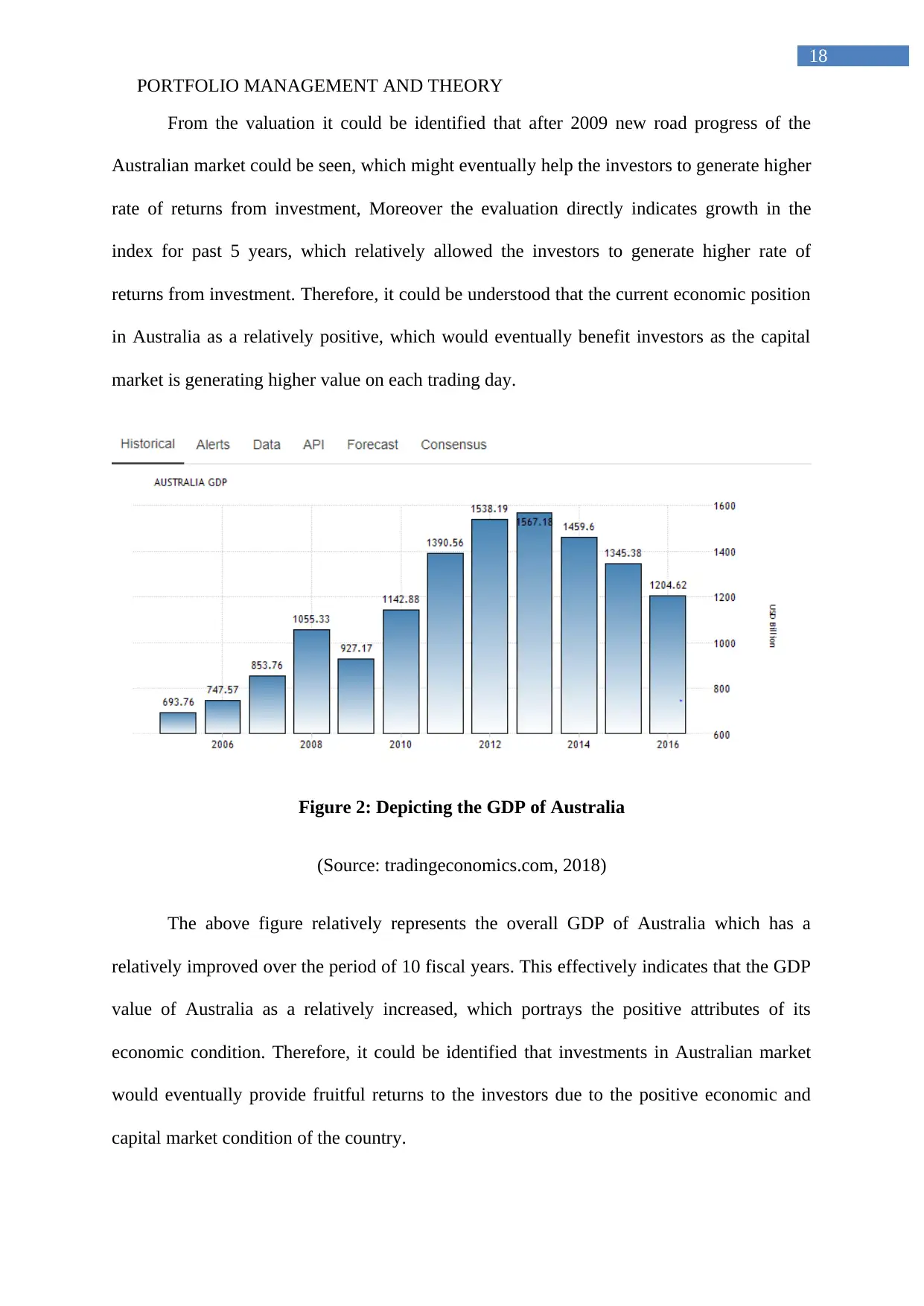

Figure 2: Depicting the GDP of Australia

(Source: tradingeconomics.com, 2018)

The above figure relatively represents the overall GDP of Australia which has a

relatively improved over the period of 10 fiscal years. This effectively indicates that the GDP

value of Australia as a relatively increased, which portrays the positive attributes of its

economic condition. Therefore, it could be identified that investments in Australian market

would eventually provide fruitful returns to the investors due to the positive economic and

capital market condition of the country.

18

From the valuation it could be identified that after 2009 new road progress of the

Australian market could be seen, which might eventually help the investors to generate higher

rate of returns from investment, Moreover the evaluation directly indicates growth in the

index for past 5 years, which relatively allowed the investors to generate higher rate of

returns from investment. Therefore, it could be understood that the current economic position

in Australia as a relatively positive, which would eventually benefit investors as the capital

market is generating higher value on each trading day.

Figure 2: Depicting the GDP of Australia

(Source: tradingeconomics.com, 2018)

The above figure relatively represents the overall GDP of Australia which has a

relatively improved over the period of 10 fiscal years. This effectively indicates that the GDP

value of Australia as a relatively increased, which portrays the positive attributes of its

economic condition. Therefore, it could be identified that investments in Australian market

would eventually provide fruitful returns to the investors due to the positive economic and

capital market condition of the country.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

19

3.2 Industry Analysis:

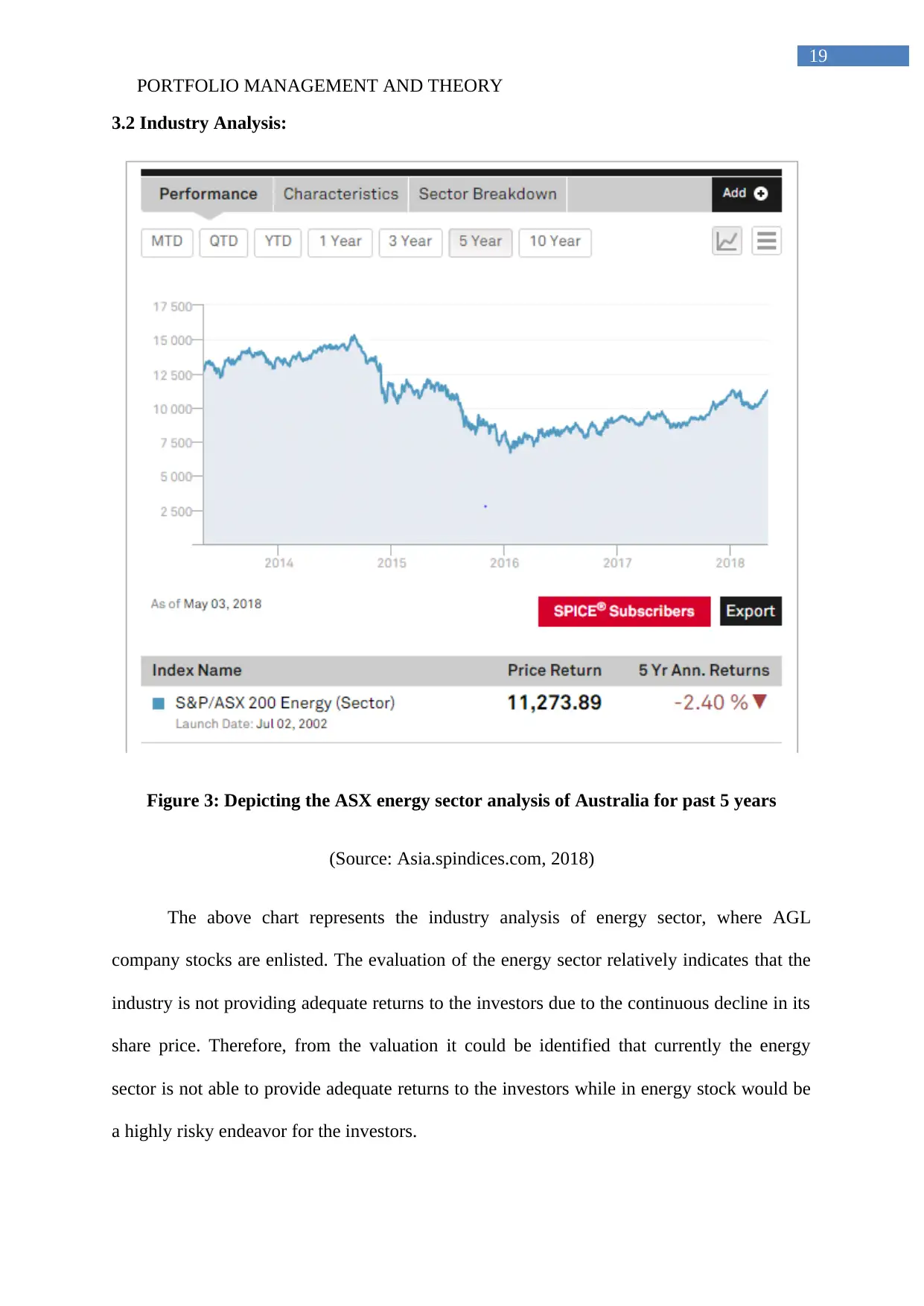

Figure 3: Depicting the ASX energy sector analysis of Australia for past 5 years

(Source: Asia.spindices.com, 2018)

The above chart represents the industry analysis of energy sector, where AGL

company stocks are enlisted. The evaluation of the energy sector relatively indicates that the

industry is not providing adequate returns to the investors due to the continuous decline in its

share price. Therefore, from the valuation it could be identified that currently the energy

sector is not able to provide adequate returns to the investors while in energy stock would be

a highly risky endeavor for the investors.

19

3.2 Industry Analysis:

Figure 3: Depicting the ASX energy sector analysis of Australia for past 5 years

(Source: Asia.spindices.com, 2018)

The above chart represents the industry analysis of energy sector, where AGL

company stocks are enlisted. The evaluation of the energy sector relatively indicates that the

industry is not providing adequate returns to the investors due to the continuous decline in its

share price. Therefore, from the valuation it could be identified that currently the energy

sector is not able to provide adequate returns to the investors while in energy stock would be

a highly risky endeavor for the investors.

PORTFOLIO MANAGEMENT AND THEORY

20

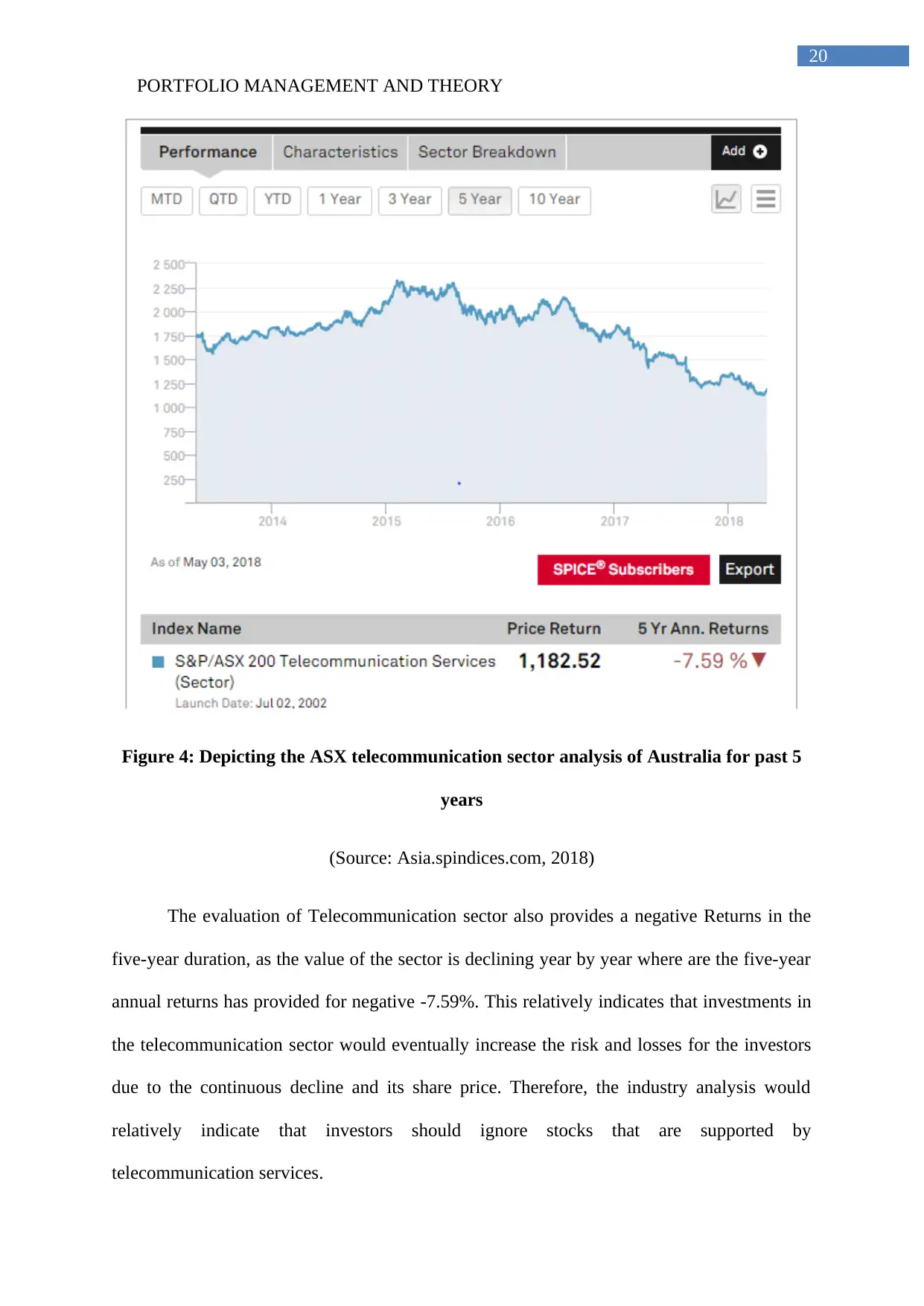

Figure 4: Depicting the ASX telecommunication sector analysis of Australia for past 5

years

(Source: Asia.spindices.com, 2018)

The evaluation of Telecommunication sector also provides a negative Returns in the

five-year duration, as the value of the sector is declining year by year where are the five-year

annual returns has provided for negative -7.59%. This relatively indicates that investments in

the telecommunication sector would eventually increase the risk and losses for the investors

due to the continuous decline and its share price. Therefore, the industry analysis would

relatively indicate that investors should ignore stocks that are supported by

telecommunication services.

20

Figure 4: Depicting the ASX telecommunication sector analysis of Australia for past 5

years

(Source: Asia.spindices.com, 2018)

The evaluation of Telecommunication sector also provides a negative Returns in the

five-year duration, as the value of the sector is declining year by year where are the five-year

annual returns has provided for negative -7.59%. This relatively indicates that investments in

the telecommunication sector would eventually increase the risk and losses for the investors

due to the continuous decline and its share price. Therefore, the industry analysis would

relatively indicate that investors should ignore stocks that are supported by

telecommunication services.

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

21

And from the evaluation of both the energy sector and telecommunication sector it

could be identified that investment in both the category would directly increase the score of

the investors. In addition, the losses that could in by the investor would eventually increase

adequate investments are conducted in telecommunication and energy sector therefore

investors should ignore the stocks related to the Sector to improve its return and reduce the

risk from the portfolio.

3.3 Security Outlook:

Particulars Telstra AGL

Average return 5.1406 18.7602

Dividend yield 6.87 4.76

PE 10.4 17.2

The above table represents the average Returns, dividend yield, and the ratio of

Telstra and AGL, which could help in identifying the current position of the company. From

the overall evaluation it could be detected that Telstra does not provide an adequate higher

rate of returns from investment, while its dividend yield is relevantly high with a lower

period. This indicates that Telstra is able to provide a higher rate of dividend to its investors

on yearly basis, which would eventually allow investors to increase the returns from

investment. Moreover, the PE ratio of 10 star is a relatively lower which directly indicates

that there is possibility of higher growth in the share price. However, the average returns

provided by Telstra from its price movement is relatively at the levels of 5.1406, which can

be considered an adequate investment opportunity that could generate higher rate of returns

from investment (Kaiser, Arbi & Ahlemann, 2015).

21

And from the evaluation of both the energy sector and telecommunication sector it

could be identified that investment in both the category would directly increase the score of

the investors. In addition, the losses that could in by the investor would eventually increase

adequate investments are conducted in telecommunication and energy sector therefore

investors should ignore the stocks related to the Sector to improve its return and reduce the

risk from the portfolio.

3.3 Security Outlook:

Particulars Telstra AGL

Average return 5.1406 18.7602

Dividend yield 6.87 4.76

PE 10.4 17.2

The above table represents the average Returns, dividend yield, and the ratio of

Telstra and AGL, which could help in identifying the current position of the company. From

the overall evaluation it could be detected that Telstra does not provide an adequate higher

rate of returns from investment, while its dividend yield is relevantly high with a lower

period. This indicates that Telstra is able to provide a higher rate of dividend to its investors

on yearly basis, which would eventually allow investors to increase the returns from

investment. Moreover, the PE ratio of 10 star is a relatively lower which directly indicates

that there is possibility of higher growth in the share price. However, the average returns

provided by Telstra from its price movement is relatively at the levels of 5.1406, which can

be considered an adequate investment opportunity that could generate higher rate of returns

from investment (Kaiser, Arbi & Ahlemann, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

22

The above calculation also evaluates the performance of AGL, which could help in

generating higher rate of returns from investment. The average returns provided by the

company is at the levels of 18.7602, which is relatively higher for the investors who is willing

to increase value of its Portfolio. Furthermore, the dividend yield of the company is relatively

at the levels of 4.76 which indicate a profitable position for the investors who can generate

higher rate of returns from investment. However, PE ratio of the company is relatively high,

which indicates a short-term decline in share value, which could directly hamper the overall

portfolio value due to the declining share value of the company (Chandra, 2017).

The declining outlook of the industry can be witnessed in which Telstra and AGL is

operating, which relatively indicates the overall unstable position of the companies over the

period of 4 years. The industry analysis relatively indicates a negative trend where the sector

index is relatively losing value over the period, while increasing the risk reducing the overall

returns from investment. on the other hand, the country analysis represents a positive attribute

of Australia, which would eventually help investors in generating higher rate of returns from

investment. the current ASX index Is trending positive while providing hair growth in current

year after the recession, while the overall GDP of the country is a relatively improving over

the period of 10 fiscal years. this relatively indicates the positive attributes of investing in

Australian stock market, which could all investors to generate higher rate of returns from

investment. However, the current industry analysis depicts a negative trend, which might

hamper the overall profitability of the investors if investing is conducted in Energy sector and

Telecommunication service sector (Heding, Knudtzen & Bjerre, 2015).

Conclusion:

The overall assessment focuses on identifying the significance of trading and the

measures, which could be used for minimizing the risk from return. However, the output

22

The above calculation also evaluates the performance of AGL, which could help in

generating higher rate of returns from investment. The average returns provided by the

company is at the levels of 18.7602, which is relatively higher for the investors who is willing

to increase value of its Portfolio. Furthermore, the dividend yield of the company is relatively

at the levels of 4.76 which indicate a profitable position for the investors who can generate

higher rate of returns from investment. However, PE ratio of the company is relatively high,

which indicates a short-term decline in share value, which could directly hamper the overall

portfolio value due to the declining share value of the company (Chandra, 2017).

The declining outlook of the industry can be witnessed in which Telstra and AGL is

operating, which relatively indicates the overall unstable position of the companies over the

period of 4 years. The industry analysis relatively indicates a negative trend where the sector

index is relatively losing value over the period, while increasing the risk reducing the overall

returns from investment. on the other hand, the country analysis represents a positive attribute

of Australia, which would eventually help investors in generating higher rate of returns from

investment. the current ASX index Is trending positive while providing hair growth in current

year after the recession, while the overall GDP of the country is a relatively improving over

the period of 10 fiscal years. this relatively indicates the positive attributes of investing in

Australian stock market, which could all investors to generate higher rate of returns from

investment. However, the current industry analysis depicts a negative trend, which might

hamper the overall profitability of the investors if investing is conducted in Energy sector and

Telecommunication service sector (Heding, Knudtzen & Bjerre, 2015).

Conclusion:

The overall assessment focuses on identifying the significance of trading and the

measures, which could be used for minimizing the risk from return. However, the output

PORTFOLIO MANAGEMENT AND THEORY

23

identified from the above the assessment relatively indicates the problems that is situated

with Momentum investment strategy, which does not provide adequate leverage to the

investors. Moreover, the portfolio created for the evaluation depicted the losses, which would

be incurred by the investor due to the high volatility in investment. This evaluation relatively

indicate that investors needs to conduct different level of analysis before conducting

investment in stock market, as the investment could provide high risk and low returns from

investment. the economic analysis, industry analysis, and company analysis is conducted to

identify the viability of the investments in Australia. This macro analysis would eventually

help in identifying the current investment position of the market, which could generate a

higher rate of returns from investment.

23

identified from the above the assessment relatively indicates the problems that is situated

with Momentum investment strategy, which does not provide adequate leverage to the

investors. Moreover, the portfolio created for the evaluation depicted the losses, which would

be incurred by the investor due to the high volatility in investment. This evaluation relatively

indicate that investors needs to conduct different level of analysis before conducting

investment in stock market, as the investment could provide high risk and low returns from

investment. the economic analysis, industry analysis, and company analysis is conducted to

identify the viability of the investments in Australia. This macro analysis would eventually

help in identifying the current investment position of the market, which could generate a

higher rate of returns from investment.

You're viewing a preview

Unlock full access by subscribing today!

PORTFOLIO MANAGEMENT AND THEORY

24

Reference and Bibliography:

Adabi, F., Mozafari, B., Ranjbar, A. M., & Soleymani, S. (2017). Policy Making for

Generation Expansion Planning by means of Portfolio Theory; Case Study of

Iran. International Journal of Renewable Energy Research (IJRER), 7(3), 1426-1435.

Aouni, B., Colapinto, C., & La Torre, D. (2014). Financial portfolio management through the

goal programming model: Current state-of-the-art. European Journal of Operational

Research, 234(2), 536-545.

Archibald, R. D., & Archibald, S. (2016). Leading and Managing Innovation: What Every

Executive Team Must Know about Project, Program, and Portfolio Management.

Auerbach Publications.

Asparouhova, E., Bossaerts, P., Čopič, J., Cornell, B., Cvitanić, J., & Meloso, D. (2014).

Competition in portfolio management: theory and experiment. Management

Science, 61(8), 1868-1888.

Australia GDP Growth Rate | 1959-2018 | Data | Chart | Calendar | Forecast.

(2018). Tradingeconomics.com. Retrieved 6 May 2018, from

https://tradingeconomics.com/australia/gdp-growth

Baldi, F., & Trigeorgis, L. (2015). Toward a Real Options Theory of Strategic Human

Resource Management. In Academy of Management Proceedings (Vol. 2015, No. 1,

p. 14862). Briarcliff Manor, NY 10510: Academy of Management.

Behrens, J. (2016). A Lack of insight: An experimental analysis of R&D managers’ decision

making in innovation portfolio management. Creativity and Innovation

Management, 25(2), 239-250.

24

Reference and Bibliography:

Adabi, F., Mozafari, B., Ranjbar, A. M., & Soleymani, S. (2017). Policy Making for

Generation Expansion Planning by means of Portfolio Theory; Case Study of

Iran. International Journal of Renewable Energy Research (IJRER), 7(3), 1426-1435.

Aouni, B., Colapinto, C., & La Torre, D. (2014). Financial portfolio management through the

goal programming model: Current state-of-the-art. European Journal of Operational

Research, 234(2), 536-545.

Archibald, R. D., & Archibald, S. (2016). Leading and Managing Innovation: What Every

Executive Team Must Know about Project, Program, and Portfolio Management.

Auerbach Publications.

Asparouhova, E., Bossaerts, P., Čopič, J., Cornell, B., Cvitanić, J., & Meloso, D. (2014).

Competition in portfolio management: theory and experiment. Management

Science, 61(8), 1868-1888.

Australia GDP Growth Rate | 1959-2018 | Data | Chart | Calendar | Forecast.

(2018). Tradingeconomics.com. Retrieved 6 May 2018, from

https://tradingeconomics.com/australia/gdp-growth

Baldi, F., & Trigeorgis, L. (2015). Toward a Real Options Theory of Strategic Human

Resource Management. In Academy of Management Proceedings (Vol. 2015, No. 1,

p. 14862). Briarcliff Manor, NY 10510: Academy of Management.

Behrens, J. (2016). A Lack of insight: An experimental analysis of R&D managers’ decision

making in innovation portfolio management. Creativity and Innovation

Management, 25(2), 239-250.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PORTFOLIO MANAGEMENT AND THEORY

25

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education.

Gerber, S., Markowitz, H., & Pujara, P. (2015). Enhancing Multi-Asset Portfolio

Construction Under Modern Portfolio Theory with a Robust Co-Movement Measure.

Gutiérrez, E., & Magnusson, M. (2014). Dealing with legitimacy: A key challenge for Project

Portfolio Management decision makers. International Journal of Project

Management, 32(1), 30-39.

Heding, T., Knudtzen, C. F., & Bjerre, M. (2015). Brand management: Research, theory and

practice. Routledge.

Hill, C. W., Jones, G. R., & Schilling, M. A. (2014). Strategic management: theory: an

integrated approach. Cengage Learning.

Kaiser, M. G., El Arbi, F., & Ahlemann, F. (2015). Successful project portfolio management

beyond project selection techniques: Understanding the role of structural

alignment. International Journal of Project Management, 33(1), 126-139.

Kevin, S. (2015). Security analysis and portfolio management. PHI Learning Pvt. Ltd.

Klingebiel, R., & Rammer, C. (2014). Resource allocation strategy for innovation portfolio

management. Strategic Management Journal, 35(2), 246-268.

Kock, A., Heising, W., & Gemünden, H. G. (2015). How ideation portfolio management

influences front‐end success. Journal of Product Innovation Management, 32(4), 539-

555.

Lynn, D., & Hao, Y. (2015). Active Portfolio Management Using Modern Portfolio

Theory. Active Private Equity Real Estate Strategy, 187-215.

25

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education.

Gerber, S., Markowitz, H., & Pujara, P. (2015). Enhancing Multi-Asset Portfolio

Construction Under Modern Portfolio Theory with a Robust Co-Movement Measure.

Gutiérrez, E., & Magnusson, M. (2014). Dealing with legitimacy: A key challenge for Project

Portfolio Management decision makers. International Journal of Project

Management, 32(1), 30-39.

Heding, T., Knudtzen, C. F., & Bjerre, M. (2015). Brand management: Research, theory and

practice. Routledge.

Hill, C. W., Jones, G. R., & Schilling, M. A. (2014). Strategic management: theory: an

integrated approach. Cengage Learning.

Kaiser, M. G., El Arbi, F., & Ahlemann, F. (2015). Successful project portfolio management

beyond project selection techniques: Understanding the role of structural

alignment. International Journal of Project Management, 33(1), 126-139.

Kevin, S. (2015). Security analysis and portfolio management. PHI Learning Pvt. Ltd.

Klingebiel, R., & Rammer, C. (2014). Resource allocation strategy for innovation portfolio

management. Strategic Management Journal, 35(2), 246-268.

Kock, A., Heising, W., & Gemünden, H. G. (2015). How ideation portfolio management

influences front‐end success. Journal of Product Innovation Management, 32(4), 539-

555.

Lynn, D., & Hao, Y. (2015). Active Portfolio Management Using Modern Portfolio

Theory. Active Private Equity Real Estate Strategy, 187-215.

PORTFOLIO MANAGEMENT AND THEORY

26

Marti, E., & Scherer, A. G. (2016). Financial regulation and social welfare: The critical

contribution of management theory. Academy of Management Review, 41(2), 298-

323.

Moustafaev, J. (2016). Project Portfolio Management in Theory and Practice: Thirty Case

Studies from Around the World. CRC Press.

Muller, R. (2017). Project governance. Routledge.

Nematollahi, S., & Manzi, G. (2018). Portfolio Management Using Prospect Theory:

Comparing Genetic Algorithms and Particle Swarm Optimization (No. 2018-03).

Rank, J., Unger, B. N., & Gemünden, H. G. (2015). Preparedness for the future in project

portfolio management: The roles of proactiveness, riskiness and willingness to

cannibalize. International Journal of Project Management, 33(8), 1730-1743.

Rank, J., Unger, B. N., & Gemünden, H. G. (2015). Preparedness for the future in project

portfolio management: The roles of proactiveness, riskiness and willingness to

cannibalize. International Journal of Project Management, 33(8), 1730-1743.

S&P/ASX 200 Energy (AUD) - S&P Dow Jones Indices. (2018). Asia.spindices.com.

Retrieved 6 May 2018, from https://asia.spindices.com/indices/equity/sp-asx-200-

energy-sector

S&P/ASX 200 Telecommunication Services (AUD) - S&P Dow Jones Indices.

(2018). Asia.spindices.com. Retrieved 6 May 2018, from

https://asia.spindices.com/indices/equity/sp-asx-200-telecommunication-services-

sector

26

Marti, E., & Scherer, A. G. (2016). Financial regulation and social welfare: The critical

contribution of management theory. Academy of Management Review, 41(2), 298-

323.

Moustafaev, J. (2016). Project Portfolio Management in Theory and Practice: Thirty Case

Studies from Around the World. CRC Press.