Managerial Finance Report: Ratio Analysis of Tesco and Sainsbury

VerifiedAdded on 2022/12/30

|19

|4170

|5

Report

AI Summary

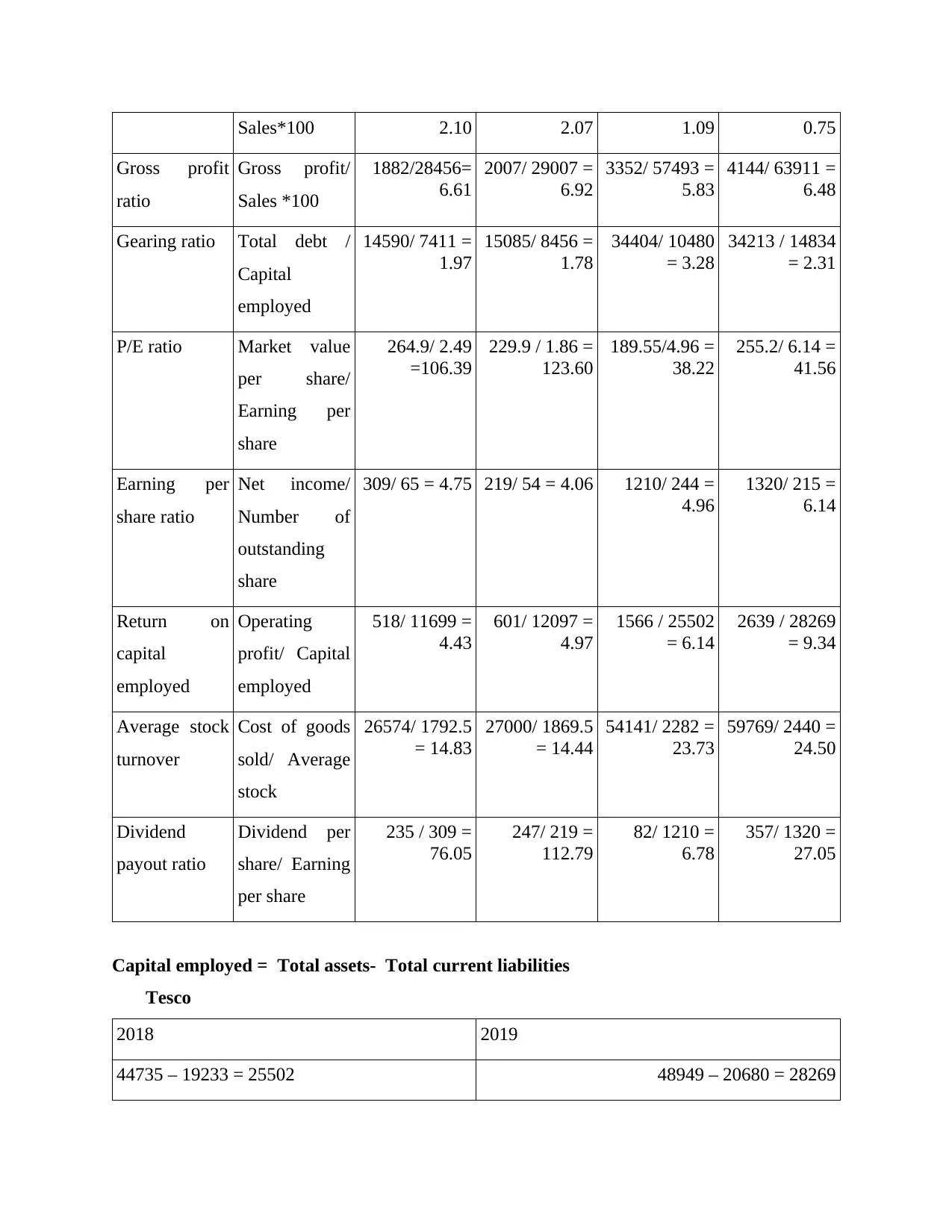

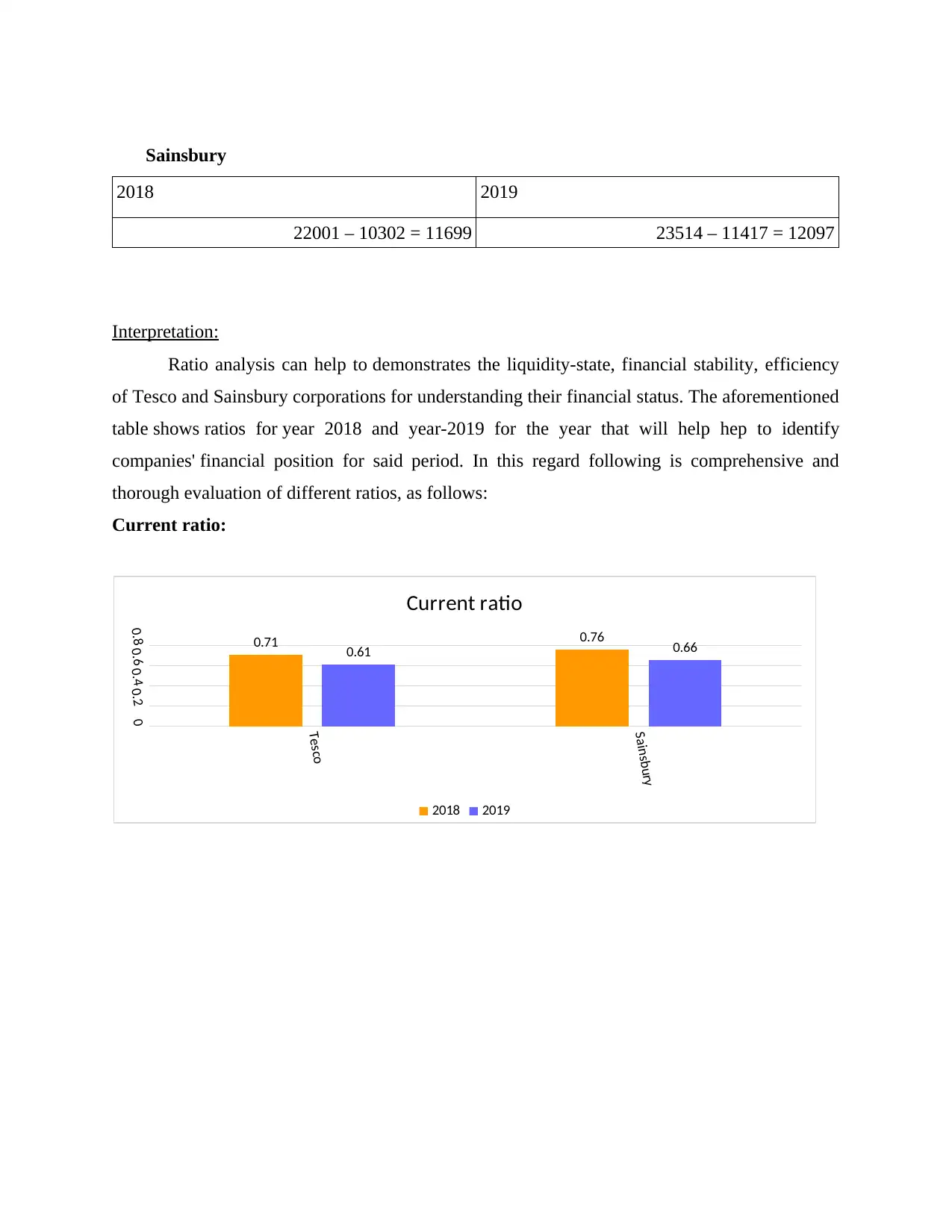

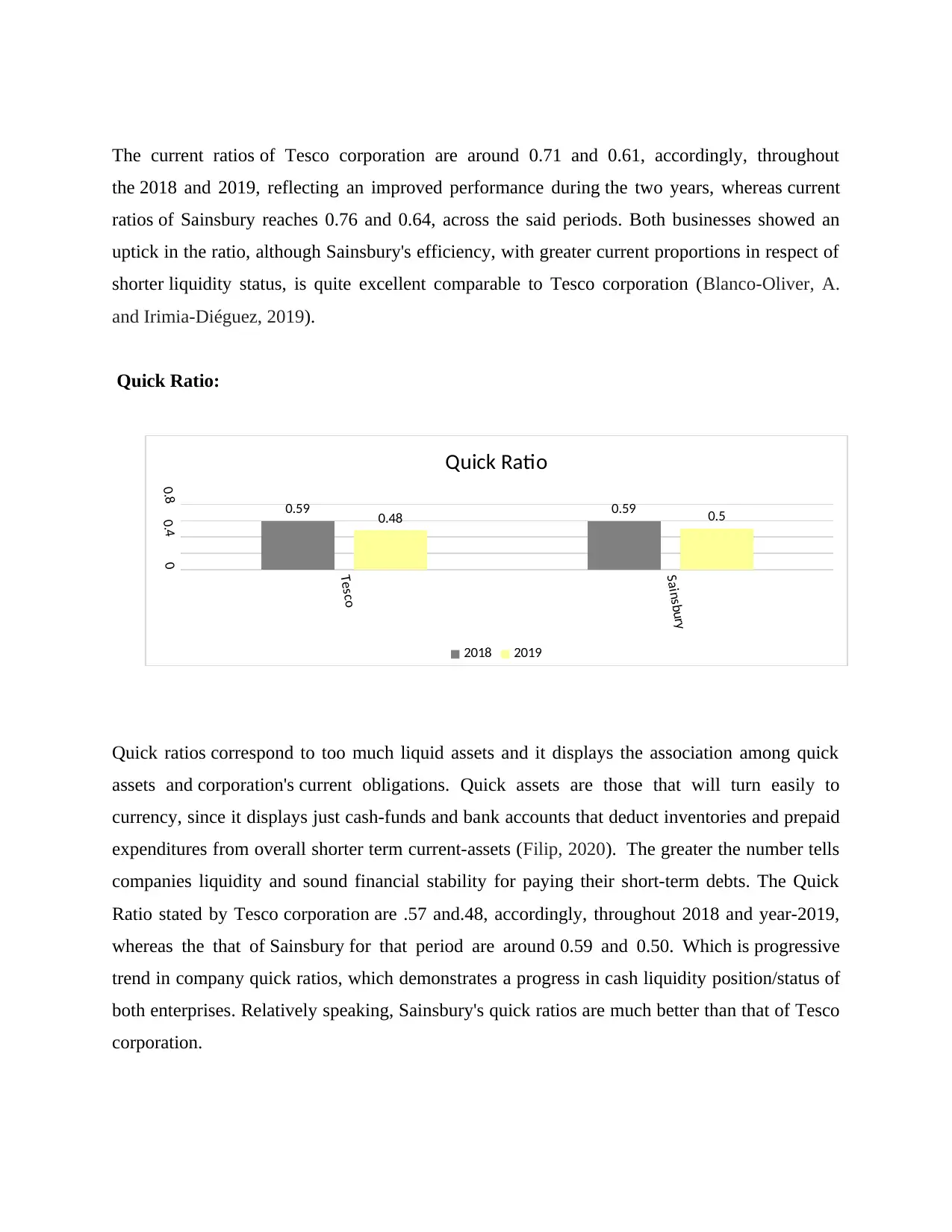

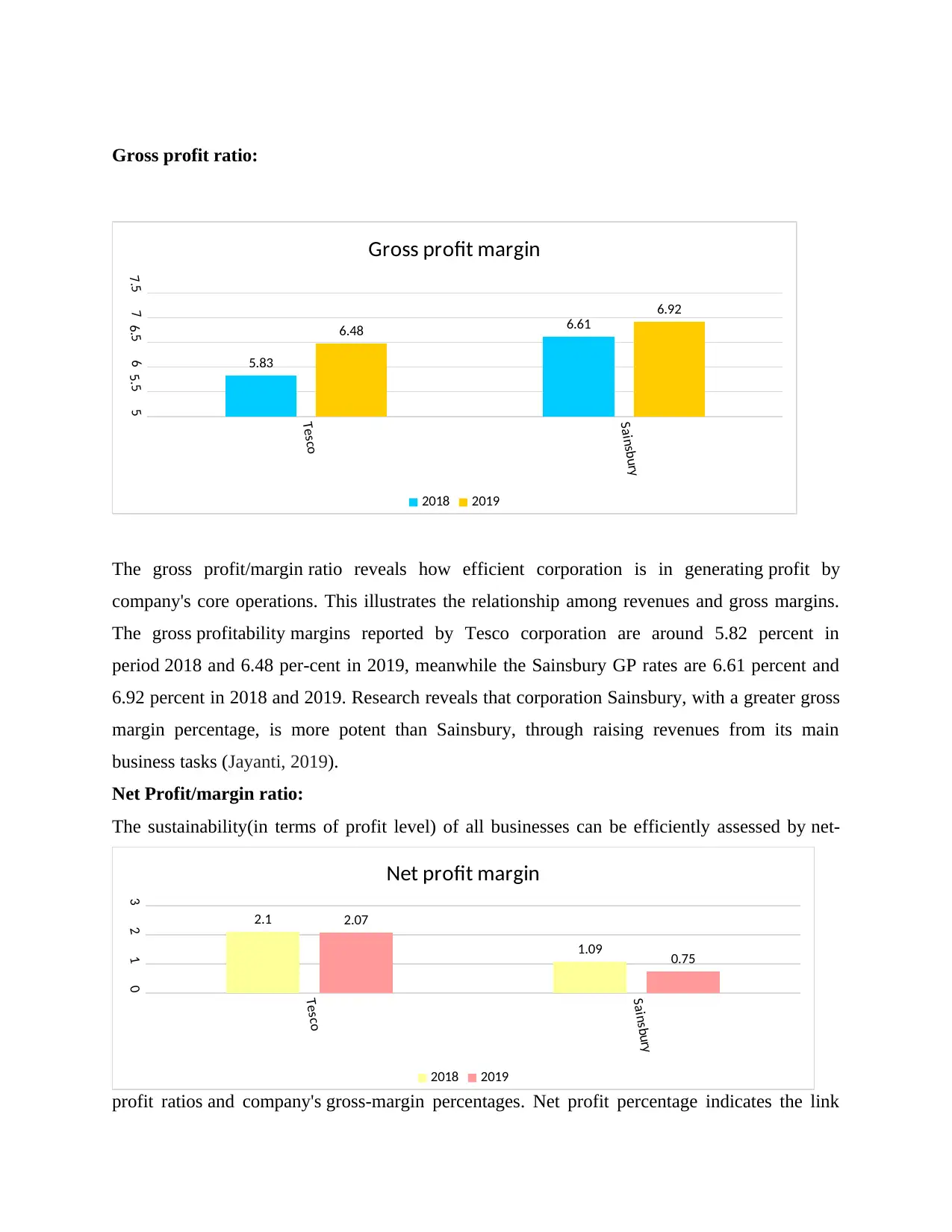

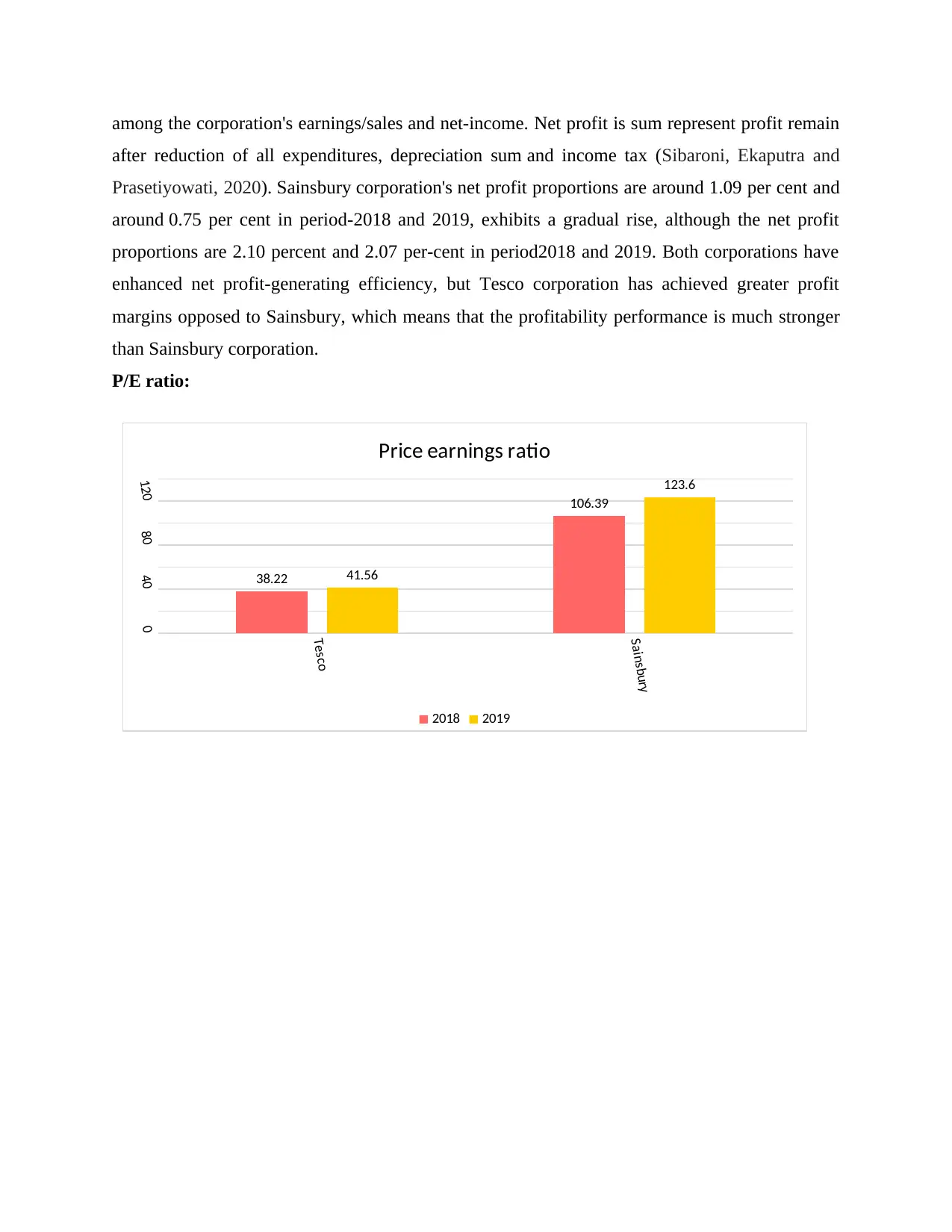

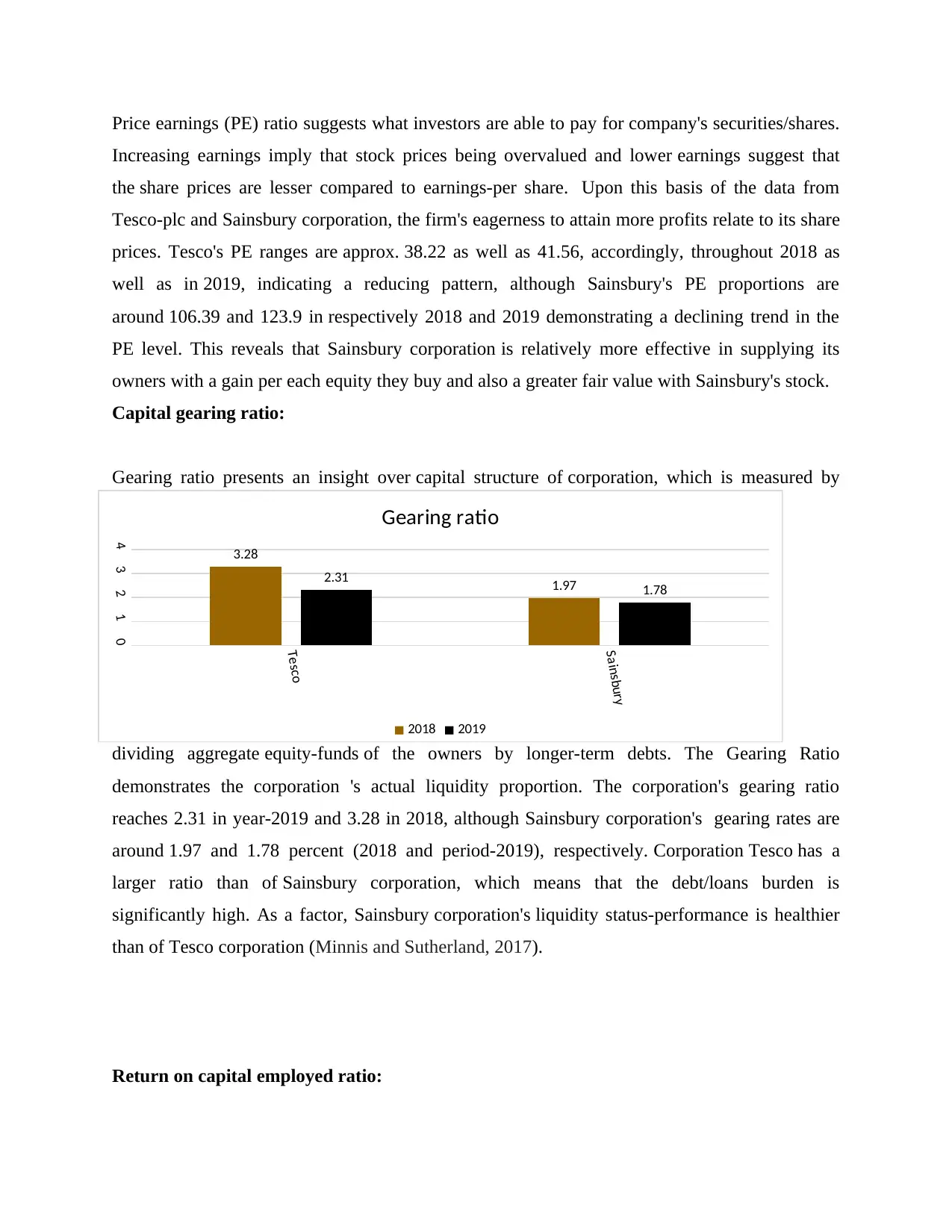

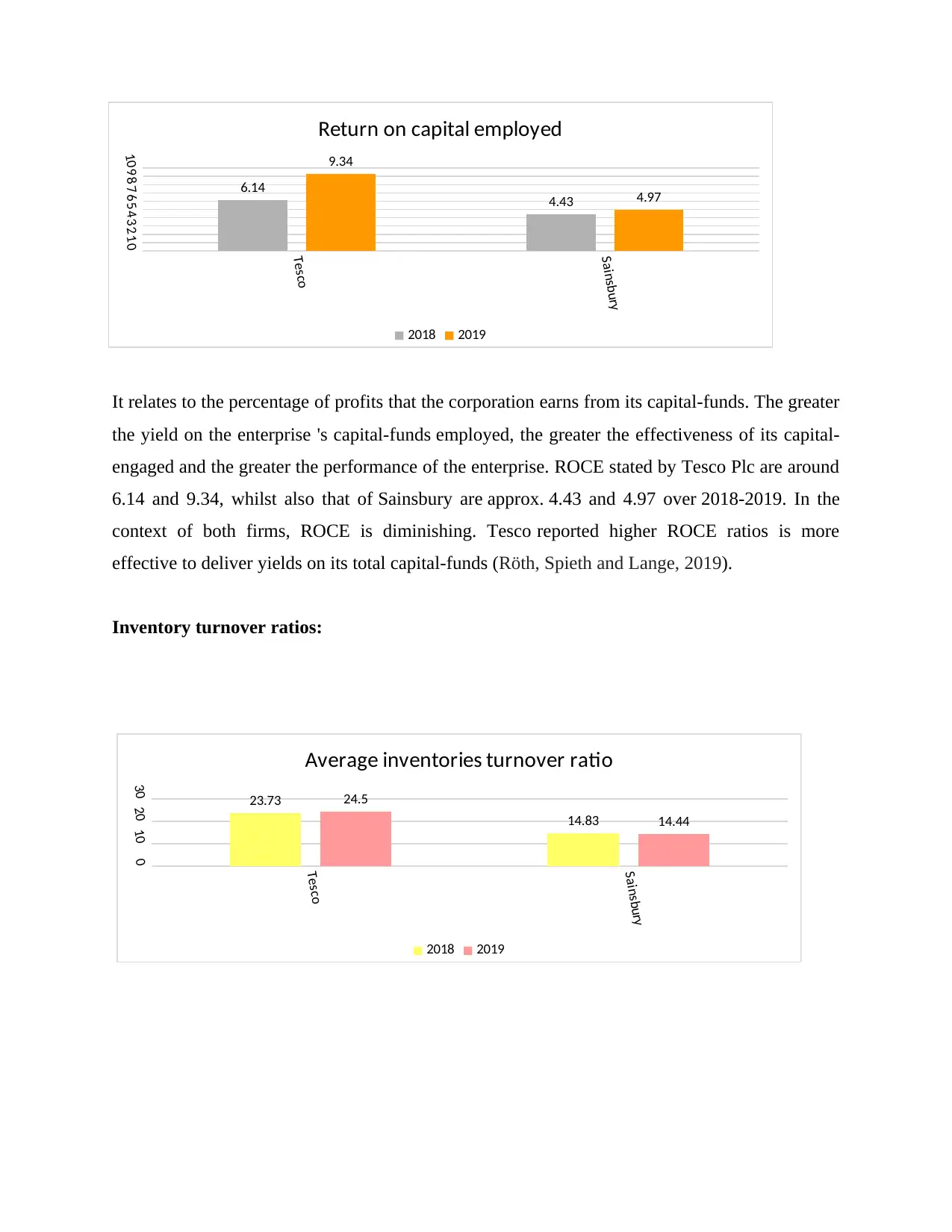

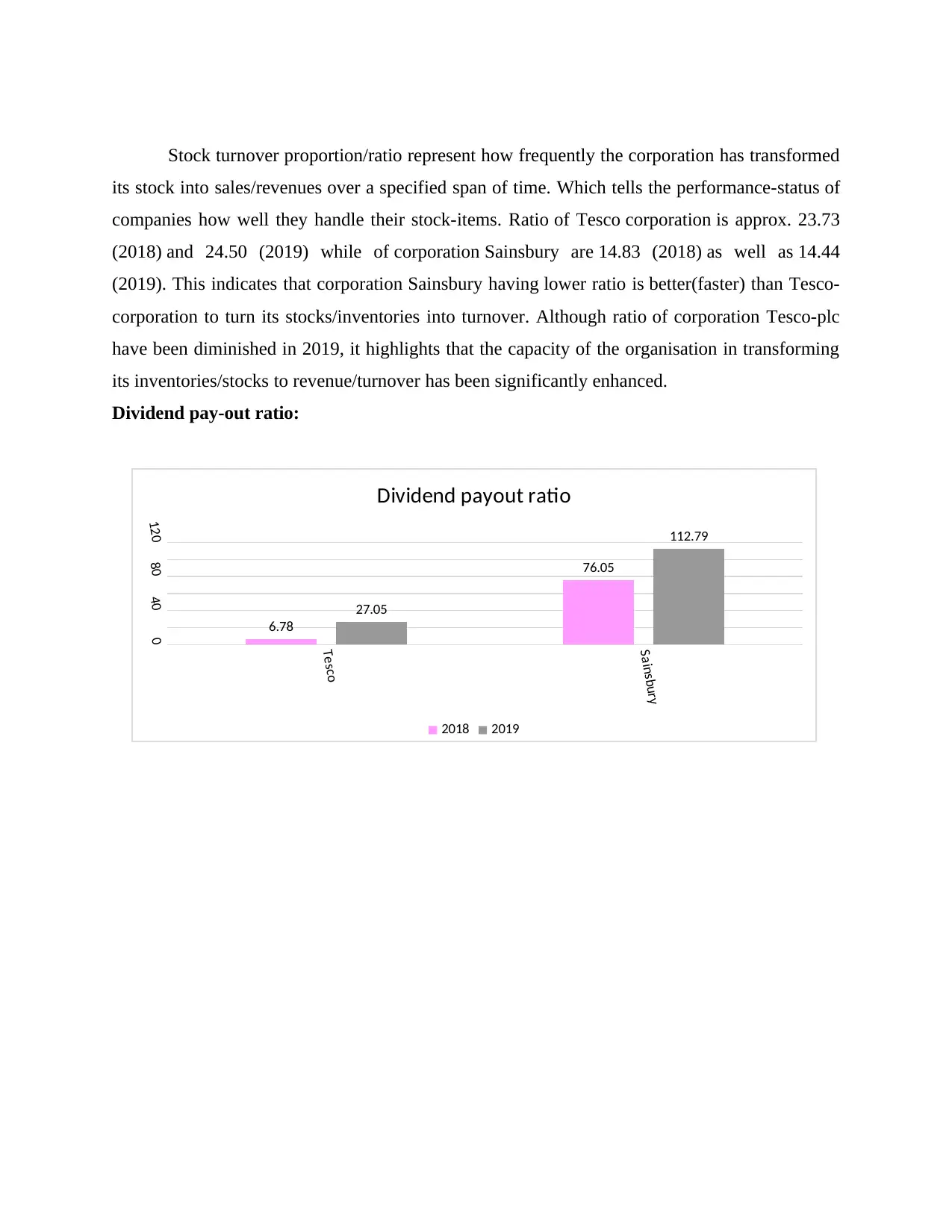

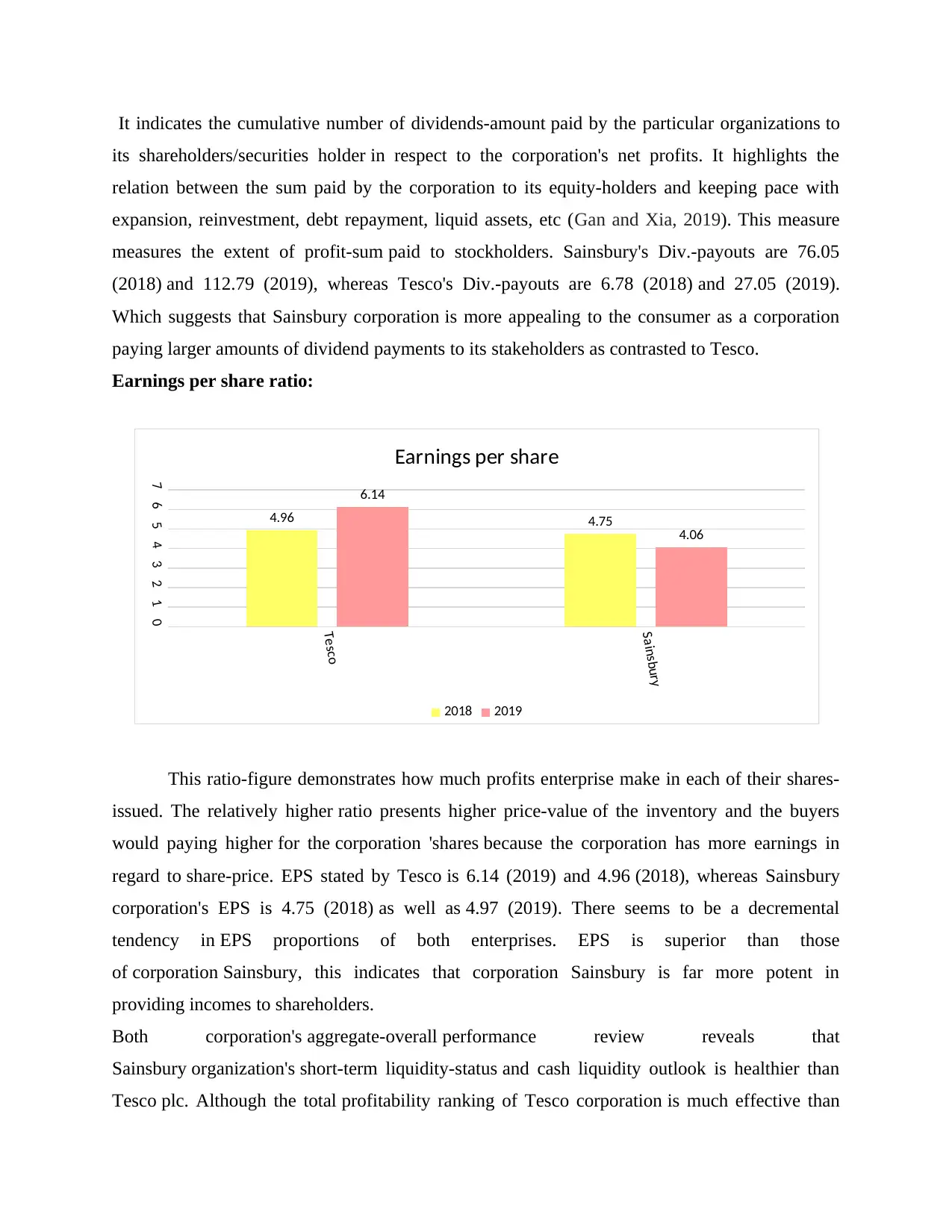

This report presents a comparative financial analysis of Tesco and Sainsbury, two prominent UK-based retail corporations. It begins with an introduction to managerial finance, defining key concepts and their importance in business operations. The core of the report focuses on ratio analysis, examining liquidity, profitability, and efficiency ratios for both companies over a two-year period. Detailed calculations and interpretations of current ratios, quick ratios, gross profit margins, net profit margins, price-to-earnings ratios, gearing ratios, return on capital employed, inventory turnover, dividend payout ratios, and earnings per share are provided. The analysis includes charts and tables to visually represent the financial performance of each company. Furthermore, the report explores investment appraisal techniques, although the specifics are not fully detailed in the provided text. It also addresses the limitations of using ratio analysis and investment appraisal techniques for long-term decision-making. The report concludes with a summary of findings and recommendations for each company, highlighting their strengths and weaknesses based on the financial data analyzed.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.