Financial Analysis of Poundland Group PLC: Debt, Equity, Cash Flow

VerifiedAdded on 2019/12/03

|13

|3811

|186

Report

AI Summary

This report offers a financial analysis of Poundland Group PLC, examining its debt and equity structure, gearing ratios, and cash flow statements. The introduction provides a business overview and outlines the report's objectives. Task 1 delves into the distinctions between debt and equity, the gearing ratio's significance for investors and creditors, and relevant accounting standards like AS 13, AS 16, AS 22, and AS 21. The report also discusses the impact of the credit crunch. Task 2 focuses on cash flow statements, their objectives, and the difference between cash flow and profitability. The analysis includes financial data from 2013 to 2015, illustrating the company's financial performance and capital structure changes, concluding with references for further study.

Poundland Group PLC-

Accounts

Accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................1

TASK 1......................................................................................................................................1

Debt and equity......................................................................................................................1

Gearing ratio..........................................................................................................................4

Accounting standard..............................................................................................................5

Credit crunch crisis................................................................................................................6

TASK 2......................................................................................................................................6

Cash flow statement...............................................................................................................6

Objectives of cash flow statements.......................................................................................6

Difference between cash flow and profitability....................................................................7

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................10

Introduction................................................................................................................................1

TASK 1......................................................................................................................................1

Debt and equity......................................................................................................................1

Gearing ratio..........................................................................................................................4

Accounting standard..............................................................................................................5

Credit crunch crisis................................................................................................................6

TASK 2......................................................................................................................................6

Cash flow statement...............................................................................................................6

Objectives of cash flow statements.......................................................................................6

Difference between cash flow and profitability....................................................................7

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................10

INTRODUCTION

Each and every business organization prepares financial statements in order to

identify their business results. Moreover, business can take necessary decisions through

evaluating these statements. Poundland is a British Variety store chain that is headquartered

in Wilenhall. Company was established in the year 1990 that sells most of the items to stores.

The firm is providing large number of branded and own label products to the stores. It

decided a clear business growth strategy through paying focus on delivering qualified

products to the customers and planned for business expansions. The long term target of

company is to operate over 1000 stores in United Kingdom. This report will help us in

identifying the role of debt and equity in the business capital structure. Further, report

analyzes the importance of cash flow statement to get higher amount of profitability.

TASK 1

Every business organization requires collecting necessary amount of funds through

different finance sources. Both debt and equity used by every enterprise to fulfil long term

finance requirements. It helps to compare the business opportunities and risk with the other

firm that operates in the same industry. The distinction between debt and equity are explained

as under:

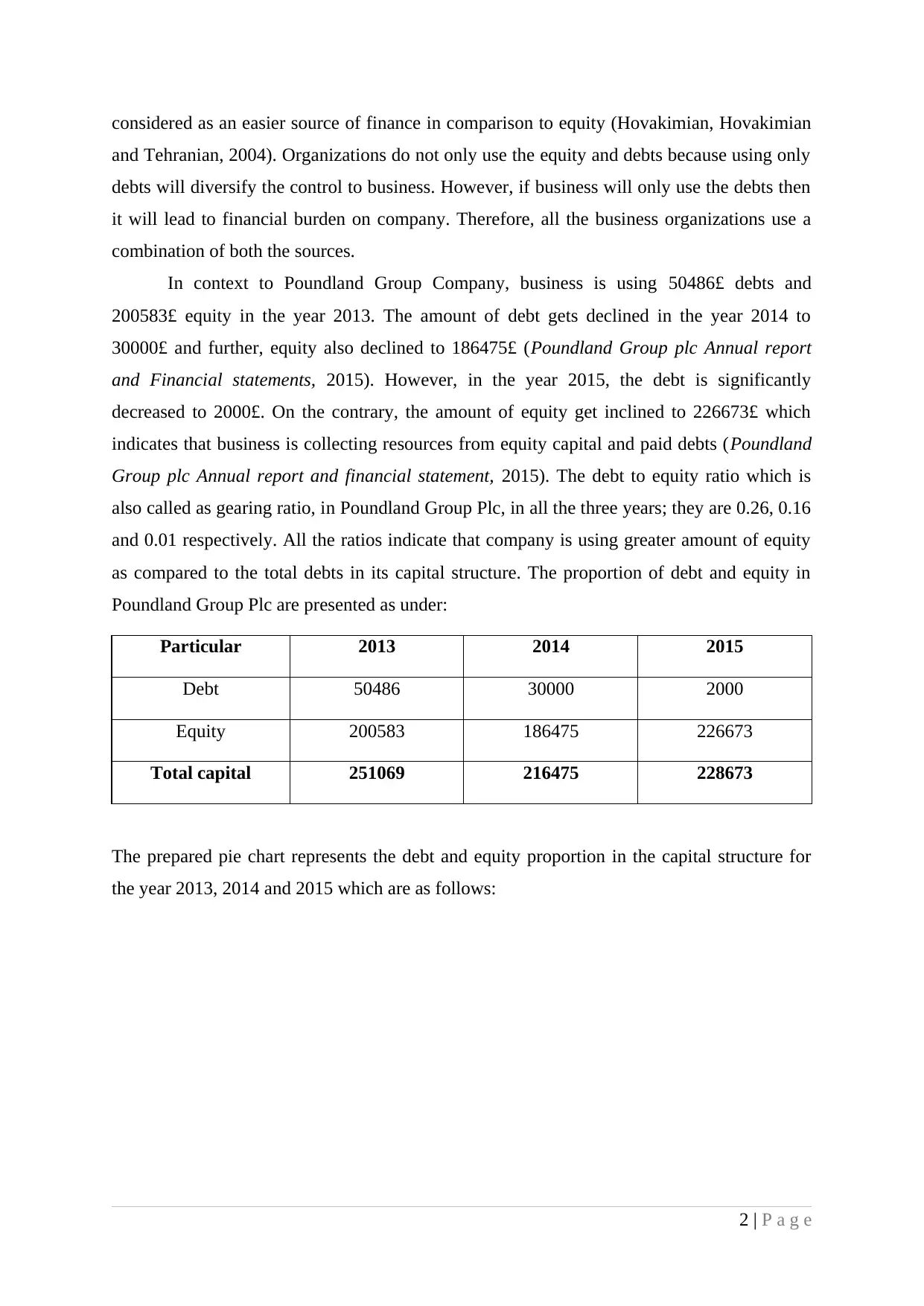

Debt and equity

Both are external finance sources as available outside from the market. Poundland

Group can issue equity shares in the market for collecting the funds. The cost of the share

capital is that company has to pay return to the shareholders. Further, it is not obligatory to

the firm to provide regular return. In case of loss, it does not require to pay dividend to the

shareholders. Further, shareholders are the owners of company so they have voting rights to

manage and control the business operations. Therefore, dilution of control exists in this case.

Before implementing any new policy or rules, company requires to communicate with their

shareholders. On the contrary, debt capital can be obtained through bank loans and issuing

debentures. Poundland Group requires paying timely interest and instalment to the

shareholders. Further, company requires keeping business assets as security towards the loans

(Hovakimian, Opler and Titman, 2001). They have to fulfil many legal formalities before

collecting funds. Further, the debenture holders and banks do not have any voting rights to

the organization. Therefore, dilution of control does not exist. Moreover, bank loans are

available at different time periods and at reasonable interest rates. On the other hand, interest

payment is considered as an allowable expenditure for the tax purpose. Hence, it is

1 | P a g e

Each and every business organization prepares financial statements in order to

identify their business results. Moreover, business can take necessary decisions through

evaluating these statements. Poundland is a British Variety store chain that is headquartered

in Wilenhall. Company was established in the year 1990 that sells most of the items to stores.

The firm is providing large number of branded and own label products to the stores. It

decided a clear business growth strategy through paying focus on delivering qualified

products to the customers and planned for business expansions. The long term target of

company is to operate over 1000 stores in United Kingdom. This report will help us in

identifying the role of debt and equity in the business capital structure. Further, report

analyzes the importance of cash flow statement to get higher amount of profitability.

TASK 1

Every business organization requires collecting necessary amount of funds through

different finance sources. Both debt and equity used by every enterprise to fulfil long term

finance requirements. It helps to compare the business opportunities and risk with the other

firm that operates in the same industry. The distinction between debt and equity are explained

as under:

Debt and equity

Both are external finance sources as available outside from the market. Poundland

Group can issue equity shares in the market for collecting the funds. The cost of the share

capital is that company has to pay return to the shareholders. Further, it is not obligatory to

the firm to provide regular return. In case of loss, it does not require to pay dividend to the

shareholders. Further, shareholders are the owners of company so they have voting rights to

manage and control the business operations. Therefore, dilution of control exists in this case.

Before implementing any new policy or rules, company requires to communicate with their

shareholders. On the contrary, debt capital can be obtained through bank loans and issuing

debentures. Poundland Group requires paying timely interest and instalment to the

shareholders. Further, company requires keeping business assets as security towards the loans

(Hovakimian, Opler and Titman, 2001). They have to fulfil many legal formalities before

collecting funds. Further, the debenture holders and banks do not have any voting rights to

the organization. Therefore, dilution of control does not exist. Moreover, bank loans are

available at different time periods and at reasonable interest rates. On the other hand, interest

payment is considered as an allowable expenditure for the tax purpose. Hence, it is

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considered as an easier source of finance in comparison to equity (Hovakimian, Hovakimian

and Tehranian, 2004). Organizations do not only use the equity and debts because using only

debts will diversify the control to business. However, if business will only use the debts then

it will lead to financial burden on company. Therefore, all the business organizations use a

combination of both the sources.

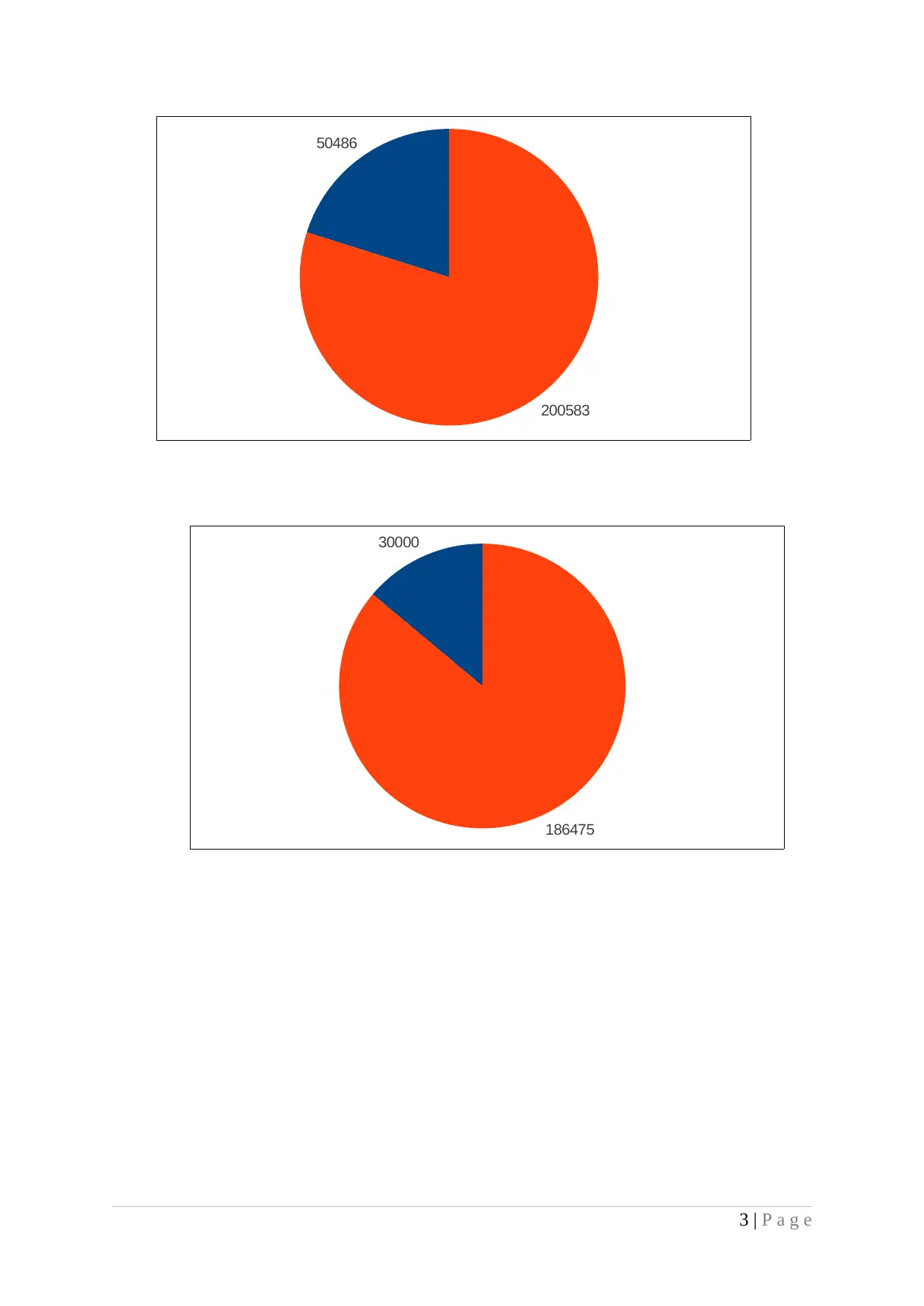

In context to Poundland Group Company, business is using 50486£ debts and

200583£ equity in the year 2013. The amount of debt gets declined in the year 2014 to

30000£ and further, equity also declined to 186475£ (Poundland Group plc Annual report

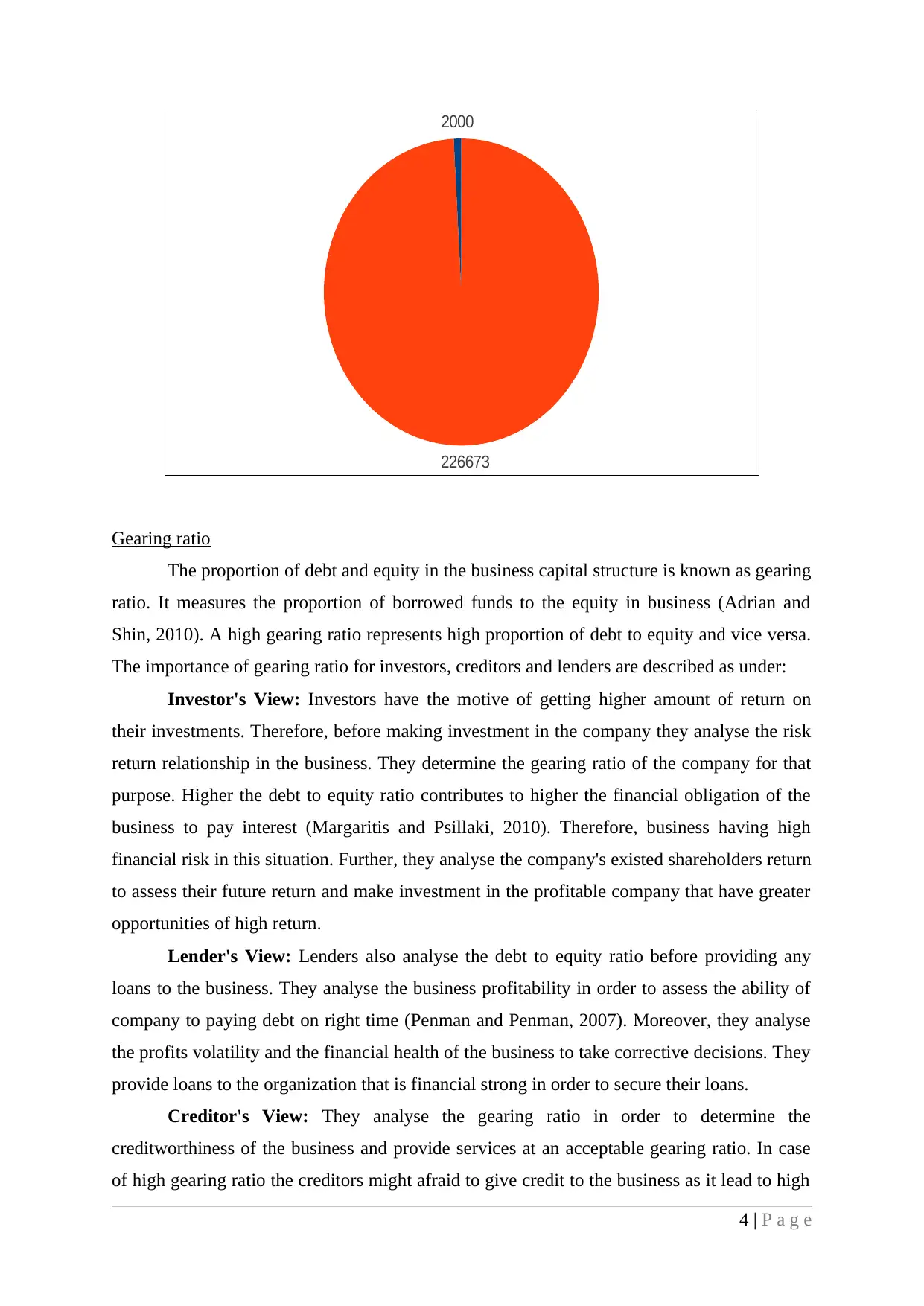

and Financial statements, 2015). However, in the year 2015, the debt is significantly

decreased to 2000£. On the contrary, the amount of equity get inclined to 226673£ which

indicates that business is collecting resources from equity capital and paid debts (Poundland

Group plc Annual report and financial statement, 2015). The debt to equity ratio which is

also called as gearing ratio, in Poundland Group Plc, in all the three years; they are 0.26, 0.16

and 0.01 respectively. All the ratios indicate that company is using greater amount of equity

as compared to the total debts in its capital structure. The proportion of debt and equity in

Poundland Group Plc are presented as under:

Particular 2013 2014 2015

Debt 50486 30000 2000

Equity 200583 186475 226673

Total capital 251069 216475 228673

The prepared pie chart represents the debt and equity proportion in the capital structure for

the year 2013, 2014 and 2015 which are as follows:

2 | P a g e

and Tehranian, 2004). Organizations do not only use the equity and debts because using only

debts will diversify the control to business. However, if business will only use the debts then

it will lead to financial burden on company. Therefore, all the business organizations use a

combination of both the sources.

In context to Poundland Group Company, business is using 50486£ debts and

200583£ equity in the year 2013. The amount of debt gets declined in the year 2014 to

30000£ and further, equity also declined to 186475£ (Poundland Group plc Annual report

and Financial statements, 2015). However, in the year 2015, the debt is significantly

decreased to 2000£. On the contrary, the amount of equity get inclined to 226673£ which

indicates that business is collecting resources from equity capital and paid debts (Poundland

Group plc Annual report and financial statement, 2015). The debt to equity ratio which is

also called as gearing ratio, in Poundland Group Plc, in all the three years; they are 0.26, 0.16

and 0.01 respectively. All the ratios indicate that company is using greater amount of equity

as compared to the total debts in its capital structure. The proportion of debt and equity in

Poundland Group Plc are presented as under:

Particular 2013 2014 2015

Debt 50486 30000 2000

Equity 200583 186475 226673

Total capital 251069 216475 228673

The prepared pie chart represents the debt and equity proportion in the capital structure for

the year 2013, 2014 and 2015 which are as follows:

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 | P a g e

50486

200583

30000

186475

50486

200583

30000

186475

Gearing ratio

The proportion of debt and equity in the business capital structure is known as gearing

ratio. It measures the proportion of borrowed funds to the equity in business (Adrian and

Shin, 2010). A high gearing ratio represents high proportion of debt to equity and vice versa.

The importance of gearing ratio for investors, creditors and lenders are described as under:

Investor's View: Investors have the motive of getting higher amount of return on

their investments. Therefore, before making investment in the company they analyse the risk

return relationship in the business. They determine the gearing ratio of the company for that

purpose. Higher the debt to equity ratio contributes to higher the financial obligation of the

business to pay interest (Margaritis and Psillaki, 2010). Therefore, business having high

financial risk in this situation. Further, they analyse the company's existed shareholders return

to assess their future return and make investment in the profitable company that have greater

opportunities of high return.

Lender's View: Lenders also analyse the debt to equity ratio before providing any

loans to the business. They analyse the business profitability in order to assess the ability of

company to paying debt on right time (Penman and Penman, 2007). Moreover, they analyse

the profits volatility and the financial health of the business to take corrective decisions. They

provide loans to the organization that is financial strong in order to secure their loans.

Creditor's View: They analyse the gearing ratio in order to determine the

creditworthiness of the business and provide services at an acceptable gearing ratio. In case

of high gearing ratio the creditors might afraid to give credit to the business as it lead to high

4 | P a g e

2000

226673

The proportion of debt and equity in the business capital structure is known as gearing

ratio. It measures the proportion of borrowed funds to the equity in business (Adrian and

Shin, 2010). A high gearing ratio represents high proportion of debt to equity and vice versa.

The importance of gearing ratio for investors, creditors and lenders are described as under:

Investor's View: Investors have the motive of getting higher amount of return on

their investments. Therefore, before making investment in the company they analyse the risk

return relationship in the business. They determine the gearing ratio of the company for that

purpose. Higher the debt to equity ratio contributes to higher the financial obligation of the

business to pay interest (Margaritis and Psillaki, 2010). Therefore, business having high

financial risk in this situation. Further, they analyse the company's existed shareholders return

to assess their future return and make investment in the profitable company that have greater

opportunities of high return.

Lender's View: Lenders also analyse the debt to equity ratio before providing any

loans to the business. They analyse the business profitability in order to assess the ability of

company to paying debt on right time (Penman and Penman, 2007). Moreover, they analyse

the profits volatility and the financial health of the business to take corrective decisions. They

provide loans to the organization that is financial strong in order to secure their loans.

Creditor's View: They analyse the gearing ratio in order to determine the

creditworthiness of the business and provide services at an acceptable gearing ratio. In case

of high gearing ratio the creditors might afraid to give credit to the business as it lead to high

4 | P a g e

2000

226673

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial obligation to the business (Welch, 2011). However, low gearing ratio or maintained

gearing ratio would be preferable by them. Therefore, the businesses require maintaining an

appropriate ratio between the business debt and equity.

Accounting standard

Business requires manipulating the composition of debt and equity proportion in order

to maintain its gearing ratio. Every organization requires preparing its financial statements

according to the Accounting standards. There are number of accounting standards that have

to follow by each and every corporation.

Accounting standard 13 that relates to accounting for investment require showing the

amount of all the investment in the financial statements of the company. According to this

standard, the companies have to disclose all the investments in the final accounts. Investment

is the assets that are held by enterprise for earning income includes dividend, interest and

other rentals. In context to Poundland Group financial statements the company disclosed the

amount of the share capital and the borrowings. Further, the accounting standard 16 that

applied to the borrowing cost. According to the standard the business should disclose the cost

of all the borrowings in the financial statements. The cost of the borrowing includes interest

and other commitment charges on borrowings, amortisation of discount or premium,

amortisation of ancillary cost and exchange difference arising from foreign currency

borrowings. With reference to Poundland Group Plc it disclosed the amount of finance

expenses in the income statement.

On contrary, Accounting standard 22 applied for accounting for taxes on the incomes.

Moreover, debt interest is deducted while calculating the business taxes. In context to Pound

land Group Plc the company disclosed the amount of taxes in its income statement.

Furthermore, accounting standard 21 that relates to preparation of consolidated financial

statements. As per the Accounting standard parent or holding company that has any

subsidiary requires to prepare consolidated financial statements. The standard is also applied

for investments that have taken place in subsidiary company by the parent company.

According to this standard the consolidated financial statements are such statements that

prepares through combining all the operations of the subsidiary company. Further, the

amount of equity share capital that is invested by the parent or holding company in subsidiary

also must be shown in the prepared accounts (Gill, Biger and Mathur, 2011). Poundland

Group Plc discloses the amount of invested share capital in the subsidiary company and also

the respective changes that have taken place in the accounting period in the consolidated

5 | P a g e

gearing ratio would be preferable by them. Therefore, the businesses require maintaining an

appropriate ratio between the business debt and equity.

Accounting standard

Business requires manipulating the composition of debt and equity proportion in order

to maintain its gearing ratio. Every organization requires preparing its financial statements

according to the Accounting standards. There are number of accounting standards that have

to follow by each and every corporation.

Accounting standard 13 that relates to accounting for investment require showing the

amount of all the investment in the financial statements of the company. According to this

standard, the companies have to disclose all the investments in the final accounts. Investment

is the assets that are held by enterprise for earning income includes dividend, interest and

other rentals. In context to Poundland Group financial statements the company disclosed the

amount of the share capital and the borrowings. Further, the accounting standard 16 that

applied to the borrowing cost. According to the standard the business should disclose the cost

of all the borrowings in the financial statements. The cost of the borrowing includes interest

and other commitment charges on borrowings, amortisation of discount or premium,

amortisation of ancillary cost and exchange difference arising from foreign currency

borrowings. With reference to Poundland Group Plc it disclosed the amount of finance

expenses in the income statement.

On contrary, Accounting standard 22 applied for accounting for taxes on the incomes.

Moreover, debt interest is deducted while calculating the business taxes. In context to Pound

land Group Plc the company disclosed the amount of taxes in its income statement.

Furthermore, accounting standard 21 that relates to preparation of consolidated financial

statements. As per the Accounting standard parent or holding company that has any

subsidiary requires to prepare consolidated financial statements. The standard is also applied

for investments that have taken place in subsidiary company by the parent company.

According to this standard the consolidated financial statements are such statements that

prepares through combining all the operations of the subsidiary company. Further, the

amount of equity share capital that is invested by the parent or holding company in subsidiary

also must be shown in the prepared accounts (Gill, Biger and Mathur, 2011). Poundland

Group Plc discloses the amount of invested share capital in the subsidiary company and also

the respective changes that have taken place in the accounting period in the consolidated

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statement of changes in equity. Therefore, on the basis of such accounting standard, it can be

said that it encouraged them to change its capital structure through changing the debt and

equity combination.

Credit crunch crisis

Due to the debt facilities that are available for the different time duration and also at

the reasonable rates business used it to a great extent. Excessive borrowings or lending by the

entities resulted in credit crunch crisis. Further, credit crunch crisis is the reason for global

financial meltdown in the year 2007. It has both negative and positive impact on both the

consumers and the businesses. It reduces the amount of loan availabilities from the banks due

to higher the interest rates (Kumar, 2009). Therefore, the business struggle to survive in the

market due to lack availability of funds through banks. Business may not have adequate

availability of required funds in this case as in this case banks refused to lend loans to the

business. Further, it create uncertainty for the future earnings that causes that large number

of investors can sell their stocks and make investment in other safer areas. However, it has

also some positive effects. For instance, using greater level of debts in the capital structure

resulted in enhancing the financial burden to them. This in turn the business financial position

can be weakened (Foster and Magdoff, 2009). Therefore, if the credit crunch arises than

business will not take any further loan and collect funds through equity. This in turn, the

financial position can be strengthened.

TASK 2

Cash flow statement

Cash flow statements measure the cash sources and its application in the business. It

is a financial statement that measures the cash generated or its implication or uses in the

company. It identifies the changes in the financial position of the business on cash flow basis.

Every business organization whether big or small needs to prepare cash flow statement in

order to determine the changes in the cash balance between two accounting period.

Objectives of cash flow statements

There are different objectives for preparing the cash flow statements. Some of the

most important objectives of these statements are described as under:

It identifies the cash earning capacity of the business. Moreover, it indicates the

amount of cash collected and also the purpose for which cash is being utilised in the business.

It helps in making effective cash planning and control in order to ensure adequate availability

6 | P a g e

said that it encouraged them to change its capital structure through changing the debt and

equity combination.

Credit crunch crisis

Due to the debt facilities that are available for the different time duration and also at

the reasonable rates business used it to a great extent. Excessive borrowings or lending by the

entities resulted in credit crunch crisis. Further, credit crunch crisis is the reason for global

financial meltdown in the year 2007. It has both negative and positive impact on both the

consumers and the businesses. It reduces the amount of loan availabilities from the banks due

to higher the interest rates (Kumar, 2009). Therefore, the business struggle to survive in the

market due to lack availability of funds through banks. Business may not have adequate

availability of required funds in this case as in this case banks refused to lend loans to the

business. Further, it create uncertainty for the future earnings that causes that large number

of investors can sell their stocks and make investment in other safer areas. However, it has

also some positive effects. For instance, using greater level of debts in the capital structure

resulted in enhancing the financial burden to them. This in turn the business financial position

can be weakened (Foster and Magdoff, 2009). Therefore, if the credit crunch arises than

business will not take any further loan and collect funds through equity. This in turn, the

financial position can be strengthened.

TASK 2

Cash flow statement

Cash flow statements measure the cash sources and its application in the business. It

is a financial statement that measures the cash generated or its implication or uses in the

company. It identifies the changes in the financial position of the business on cash flow basis.

Every business organization whether big or small needs to prepare cash flow statement in

order to determine the changes in the cash balance between two accounting period.

Objectives of cash flow statements

There are different objectives for preparing the cash flow statements. Some of the

most important objectives of these statements are described as under:

It identifies the cash earning capacity of the business. Moreover, it indicates the

amount of cash collected and also the purpose for which cash is being utilised in the business.

It helps in making effective cash planning and control in order to ensure adequate availability

6 | P a g e

of cash at any point of time (Hodder, Hopkins and Wood, 2008). Further, it measures the

business ability to pay the business obligations such as loan repayment, shareholder dividend

and taxes. Investors evaluate the cash flow statement to ensure the regular return on their

respective investment. It evaluates the cash inflows and outflows from operating, investing

and financing activities. Moreover, the statements helps to identify the reasons of the

difference between the businesses net income, its cash receipts and cash payments. It helps

the management in taking effective and strategic capital budgeting decisions. It ensures

optimum use of available funds for getting higher the benefits for the business.

In context to Poundland Group Plc the company prepare the cash flow statement for a

given period. It shows the cash flows from the business operating, investing and financing

activities. All the cash flows that relates to the business operation prevails under the operating

activities. It includes purchase and sales activities of the business. However, the purchase and

sales of capital assets reflect under the investing activities. It includes acquisition and

disposal of the fixed assets. Furthermore, cash flow from financing activities reflects the

changes in capital structure. It includes the company's purchase and sales of stock and

proceeds and payments on the debt financing. Poundland Group Plc cash flows from

operating, investing and financing activities are 33417£, (16438£) and (10034£) in the year

2013. However, in the year 2014, respective cash flows get inclined to 48202£, (17625£) and

(48170£). Operating activities cash flows get changed due to the adjustment for non cash

expenditures and increase the other operating expenses such as trade payable. On contrary,

the investing activity cash flows get changed due to acquisition of property, plant and

equipment and other non tangible assets. Further, the cash flows that results from financing

activities arises due to proceed from new loans, repayment to borrowers, redemption of

preference share in subsidiary company and new finance expenses. Therefore, the net cash

flows at the end of the year get decreased from 42861£ to 25268£ in the year 2014.

Difference between cash flow and profitability

Cash flow and profitability are distinct from each other. Income statements are

prepared in order to determine the business profitability. However, Cash flow statements are

prepared to determine the business cash inflows and cash outflows (Deegan, 2012).

Cash flow is the difference between the amount of business cash receipts and cash

payments. However, profitability is the difference between business revenues and

expenditures. A highly profitable entity may have adequate profit availability to 1000£

7 | P a g e

business ability to pay the business obligations such as loan repayment, shareholder dividend

and taxes. Investors evaluate the cash flow statement to ensure the regular return on their

respective investment. It evaluates the cash inflows and outflows from operating, investing

and financing activities. Moreover, the statements helps to identify the reasons of the

difference between the businesses net income, its cash receipts and cash payments. It helps

the management in taking effective and strategic capital budgeting decisions. It ensures

optimum use of available funds for getting higher the benefits for the business.

In context to Poundland Group Plc the company prepare the cash flow statement for a

given period. It shows the cash flows from the business operating, investing and financing

activities. All the cash flows that relates to the business operation prevails under the operating

activities. It includes purchase and sales activities of the business. However, the purchase and

sales of capital assets reflect under the investing activities. It includes acquisition and

disposal of the fixed assets. Furthermore, cash flow from financing activities reflects the

changes in capital structure. It includes the company's purchase and sales of stock and

proceeds and payments on the debt financing. Poundland Group Plc cash flows from

operating, investing and financing activities are 33417£, (16438£) and (10034£) in the year

2013. However, in the year 2014, respective cash flows get inclined to 48202£, (17625£) and

(48170£). Operating activities cash flows get changed due to the adjustment for non cash

expenditures and increase the other operating expenses such as trade payable. On contrary,

the investing activity cash flows get changed due to acquisition of property, plant and

equipment and other non tangible assets. Further, the cash flows that results from financing

activities arises due to proceed from new loans, repayment to borrowers, redemption of

preference share in subsidiary company and new finance expenses. Therefore, the net cash

flows at the end of the year get decreased from 42861£ to 25268£ in the year 2014.

Difference between cash flow and profitability

Cash flow and profitability are distinct from each other. Income statements are

prepared in order to determine the business profitability. However, Cash flow statements are

prepared to determine the business cash inflows and cash outflows (Deegan, 2012).

Cash flow is the difference between the amount of business cash receipts and cash

payments. However, profitability is the difference between business revenues and

expenditures. A highly profitable entity may have adequate profit availability to 1000£

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

million and revenues to £1 Billion but the business trading is stopped in the market. There are

various reasons may be responsible for such occurrences described here as under:

Certain cash flows are not recorded as business revenues and expenses hence create a

reason for difference between profits and net cash flows. Moreover, certain cash flows that is

recorded as incomes or expenses but may not be a part of business operating activities. For

instance, if company make future payments in current period resulted in lowering the cash

flows without affecting the profitability. This in turn, results in different amount of cash

flows and the profitability. Moreover, the non cash transactions such as depreciation, loss on

sale of machinery are recorded in profit and loss statement. Hence, affect the business

profitability. However, cash flow statements do not includes any non cash transaction hence

it do not influenced the business cash flows resulted in difference between cash flows and

profitability (Orpurt and Zang, 2009). In the consolidated cash flow statement of Poundland

Group plc company adjust the amount of 15096£ of depreciation and amortisation in the

operating activities. On contrary, the non operating cash flows do not impact the business

profitability. For instance, expenditure and incomes that relates to the purchase and selling of

assets are not recorded in the profitability statement. Moreover, the payment to borrowers or

lend from borrowers and purchase and sales of company’s stock not present in the income

statement. This in turn the profitability will be unaffected (Carpenter and Guariglia, 2008).

Poundland Group income statement do not involve the expenditures that are incurred for

acquiring the property, plant and equipment amounted to 16563£ and other tangible assets

amounted to 1062£. Further the amount of loan taken of 29268£ increased the cash flows.

Moreover, repayment of borrowings to 54914£ and redemption of preference share capital to

20000£ lead to decrease the cash flows without impact the profits (Poundland Group plc

Annual report and Financial statements, 2014).

On the other hand, cash flow statement shows all kind of cash flows whether related

to operating activities or not. It shows all cash flows from operating, financing and investing

activities. In addition to it, non cash revenues may increase the business profits without

affecting the cash flows (Reinhart and Rogoff, 2010). The reason behind that is business

record its revenues on the basis of accrual concept. For instance, a credit sales made by the

enterprise may increase the overall profits at that time but at the same time it do not impact

the cash flows. However, when the business receive cash amount then it will be lead to

increase the cash flows without affecting the profits. Along with the non cash incomes, non

cash expenses also are a reason for having different cash flows and profitability (Crotty,

8 | P a g e

various reasons may be responsible for such occurrences described here as under:

Certain cash flows are not recorded as business revenues and expenses hence create a

reason for difference between profits and net cash flows. Moreover, certain cash flows that is

recorded as incomes or expenses but may not be a part of business operating activities. For

instance, if company make future payments in current period resulted in lowering the cash

flows without affecting the profitability. This in turn, results in different amount of cash

flows and the profitability. Moreover, the non cash transactions such as depreciation, loss on

sale of machinery are recorded in profit and loss statement. Hence, affect the business

profitability. However, cash flow statements do not includes any non cash transaction hence

it do not influenced the business cash flows resulted in difference between cash flows and

profitability (Orpurt and Zang, 2009). In the consolidated cash flow statement of Poundland

Group plc company adjust the amount of 15096£ of depreciation and amortisation in the

operating activities. On contrary, the non operating cash flows do not impact the business

profitability. For instance, expenditure and incomes that relates to the purchase and selling of

assets are not recorded in the profitability statement. Moreover, the payment to borrowers or

lend from borrowers and purchase and sales of company’s stock not present in the income

statement. This in turn the profitability will be unaffected (Carpenter and Guariglia, 2008).

Poundland Group income statement do not involve the expenditures that are incurred for

acquiring the property, plant and equipment amounted to 16563£ and other tangible assets

amounted to 1062£. Further the amount of loan taken of 29268£ increased the cash flows.

Moreover, repayment of borrowings to 54914£ and redemption of preference share capital to

20000£ lead to decrease the cash flows without impact the profits (Poundland Group plc

Annual report and Financial statements, 2014).

On the other hand, cash flow statement shows all kind of cash flows whether related

to operating activities or not. It shows all cash flows from operating, financing and investing

activities. In addition to it, non cash revenues may increase the business profits without

affecting the cash flows (Reinhart and Rogoff, 2010). The reason behind that is business

record its revenues on the basis of accrual concept. For instance, a credit sales made by the

enterprise may increase the overall profits at that time but at the same time it do not impact

the cash flows. However, when the business receive cash amount then it will be lead to

increase the cash flows without affecting the profits. Along with the non cash incomes, non

cash expenses also are a reason for having different cash flows and profitability (Crotty,

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2009). Companies may have less profitability due to non cash expenditures but such kind of

expenses will not affect the cash holdings. Therefore, it can be concluded that such business

that have higher amount of profitability but due to lack of cash business market trading

activities may be stopped. This in turn, affects the business growth, development and

sustainability for the future period.

CONCLUSION

From the presented report it becomes clear that the proportion of debt and equity that

is used by the enterprise in its capital structure plays a very important role in the organization

success. Further, the report described that higher level of debts as compared to the equity

contributes to higher level of risk for the business as it create financial burden to the business.

Moreover, the report explained that investor, lenders and creditors use the gearing ratio in

analysing the business risk and take effective decisions. In addition to it, cash flow statement

is significantly distinct from the profits of the business. It measures the business cash earning

capacity and identifies the cash sources and its application in the business.

9 | P a g e

expenses will not affect the cash holdings. Therefore, it can be concluded that such business

that have higher amount of profitability but due to lack of cash business market trading

activities may be stopped. This in turn, affects the business growth, development and

sustainability for the future period.

CONCLUSION

From the presented report it becomes clear that the proportion of debt and equity that

is used by the enterprise in its capital structure plays a very important role in the organization

success. Further, the report described that higher level of debts as compared to the equity

contributes to higher level of risk for the business as it create financial burden to the business.

Moreover, the report explained that investor, lenders and creditors use the gearing ratio in

analysing the business risk and take effective decisions. In addition to it, cash flow statement

is significantly distinct from the profits of the business. It measures the business cash earning

capacity and identifies the cash sources and its application in the business.

9 | P a g e

REFERENCES

Books and Journals

Adrian, T. and Shin, H.S., 2010. Liquidity and leverage. Journal of financial intermediation.

19(3). pp.418-437.

Carpenter, R.E. and Guariglia, A., 2008. Cash flow, investment, and investment

opportunities: New tests using UK panel data. Journal of Banking & Finance. 32(9).

pp. 1894-1906.

Crotty, J., 2009. Structural causes of the global financial crisis: a critical assessment of the

‘new financial architecture’. Cambridge Journal of Economics. 33(4). pp. 563-580.

Deegan, C., 2012. Australian financial accounting. McGraw-Hill Education Australia.

Foster, J.B. and Magdoff, F., 2009. The great financial crisis: Causes and consequences.

NYU Press.

Gill, A., Biger, N. and Mathur, N., 2011. The effect of capital structure on profitability:

Evidence from the United States. International Journal of Management. 28(4). p.3.

Hodder, L., Hopkins, P.E. and Wood, D.A., 2008. The effects of financial statement and

informational complexity on analysts' cash flow forecasts. The Accounting Review,

83(4), pp.915-956.

Hovakimian, A., Hovakimian, G. and Tehranian, H., 2004. Determinants of target capital

structure: The case of dual debt and equity issues. Journal of financial economics.

71(3). pp. 517-540.

Hovakimian, A., Opler, T. and Titman, S., 2001. The debt-equity choice. Journal of

Financial and Quantitative analysis. 36(01). pp.1-24.

Kumar, A., 2009. Global financial crisis and government intervention: surplus generation,

gearing ratio, asymmetry of financial multiplier and other considerations. Accountancy

Business and the Public Interest. 8(1). pp.1-24.

Margaritis, D. and Psillaki, M., 2010. Capital structure, equity ownership and firm

performance. Journal of Banking & Finance. 34(3). pp.621-632.

Orpurt, S.F. and Zang, Y., 2009. Do direct cash flow disclosures help predict future operating

cash flows and earnings?. The Accounting Review. 84(3). pp. 893-935.

Penman, S.H. and Penman, S.H., 2007. Financial statement analysis and security valuation

(p. 476). New York: McGraw-Hill.

Reinhart, C.M. and Rogoff, K.S., 2010. From financial crash to debt crisis (No. w15795).

National Bureau of Economic Research.

Welch, I., 2011. Two Common Problems in Capital Structure Research: The Financial‐Debt‐

To‐Asset Ratio and Issuing Activity Versus Leverage Changes. International Review of

Finance. 11(1). pp.1-17.

10 | P a g e

Books and Journals

Adrian, T. and Shin, H.S., 2010. Liquidity and leverage. Journal of financial intermediation.

19(3). pp.418-437.

Carpenter, R.E. and Guariglia, A., 2008. Cash flow, investment, and investment

opportunities: New tests using UK panel data. Journal of Banking & Finance. 32(9).

pp. 1894-1906.

Crotty, J., 2009. Structural causes of the global financial crisis: a critical assessment of the

‘new financial architecture’. Cambridge Journal of Economics. 33(4). pp. 563-580.

Deegan, C., 2012. Australian financial accounting. McGraw-Hill Education Australia.

Foster, J.B. and Magdoff, F., 2009. The great financial crisis: Causes and consequences.

NYU Press.

Gill, A., Biger, N. and Mathur, N., 2011. The effect of capital structure on profitability:

Evidence from the United States. International Journal of Management. 28(4). p.3.

Hodder, L., Hopkins, P.E. and Wood, D.A., 2008. The effects of financial statement and

informational complexity on analysts' cash flow forecasts. The Accounting Review,

83(4), pp.915-956.

Hovakimian, A., Hovakimian, G. and Tehranian, H., 2004. Determinants of target capital

structure: The case of dual debt and equity issues. Journal of financial economics.

71(3). pp. 517-540.

Hovakimian, A., Opler, T. and Titman, S., 2001. The debt-equity choice. Journal of

Financial and Quantitative analysis. 36(01). pp.1-24.

Kumar, A., 2009. Global financial crisis and government intervention: surplus generation,

gearing ratio, asymmetry of financial multiplier and other considerations. Accountancy

Business and the Public Interest. 8(1). pp.1-24.

Margaritis, D. and Psillaki, M., 2010. Capital structure, equity ownership and firm

performance. Journal of Banking & Finance. 34(3). pp.621-632.

Orpurt, S.F. and Zang, Y., 2009. Do direct cash flow disclosures help predict future operating

cash flows and earnings?. The Accounting Review. 84(3). pp. 893-935.

Penman, S.H. and Penman, S.H., 2007. Financial statement analysis and security valuation

(p. 476). New York: McGraw-Hill.

Reinhart, C.M. and Rogoff, K.S., 2010. From financial crash to debt crisis (No. w15795).

National Bureau of Economic Research.

Welch, I., 2011. Two Common Problems in Capital Structure Research: The Financial‐Debt‐

To‐Asset Ratio and Issuing Activity Versus Leverage Changes. International Review of

Finance. 11(1). pp.1-17.

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.