ACCG224: Analysis of Accounting Policies and PPE of AGL Energy

VerifiedAdded on 2022/10/09

|10

|1629

|408

Report

AI Summary

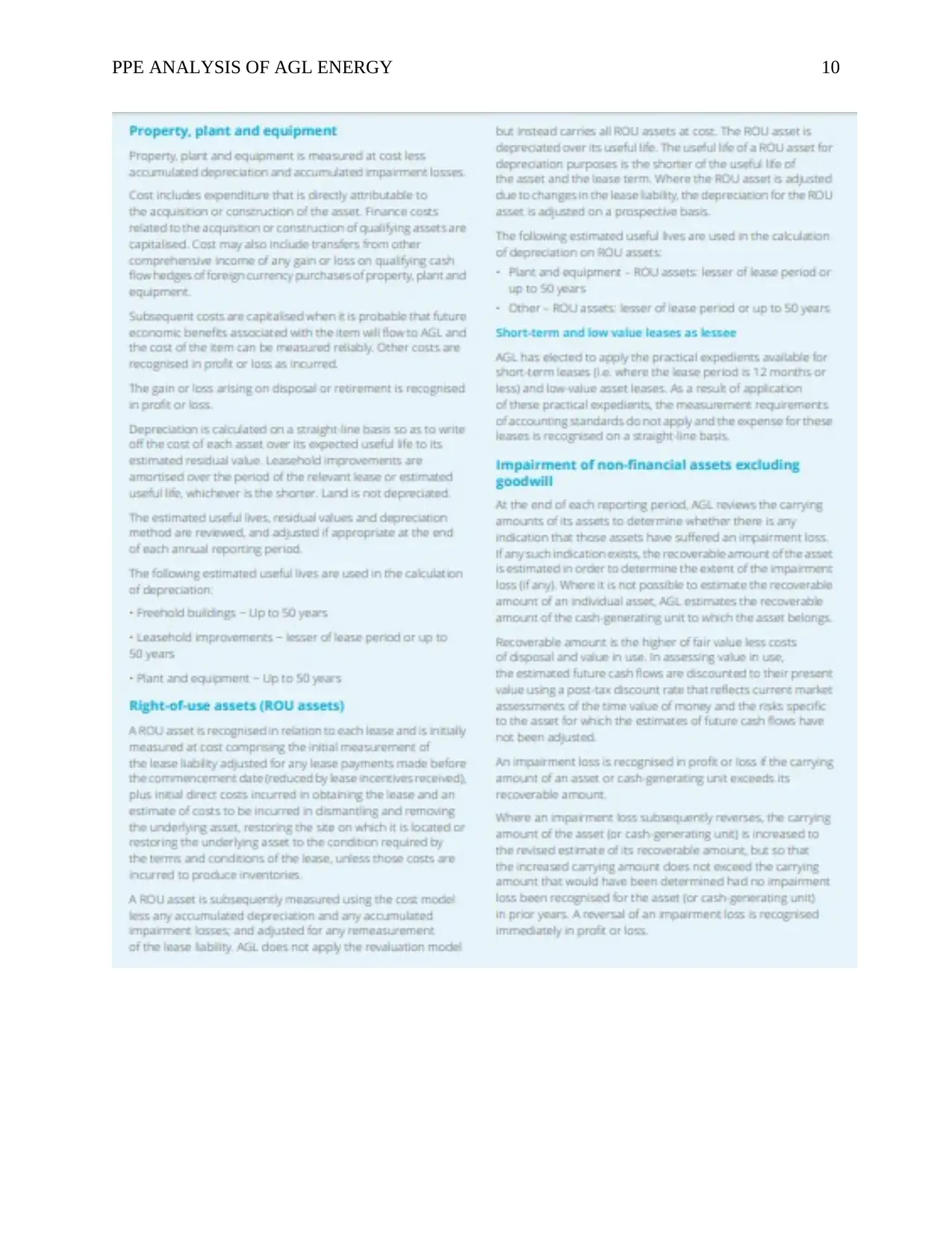

This report provides a detailed analysis of the accounting policies and estimates related to Plant, Property, and Equipment (PPE) for AGL Energy Limited. The report begins with an executive summary and an introduction to AGL Energy, an ASX-listed company in the energy sector. It then delves into the criteria for selecting and changing accounting policies, referencing AASB 108. The core of the report examines AGL Energy's specific accounting policies and estimates for PPE, including cost measurement, depreciation methods, and impairment reviews. The analysis includes an evaluation of the professional judgment applied in these policies, assessing their appropriateness and reasonableness. Furthermore, the report suggests improvements to these policies, such as conducting technical analysis of asset useful lives. The report concludes with a summary of the findings and references relevant sources, including AGL Energy's and Origin Energy's annual reports, and the Australian Accounting Standards Board. An appendix containing AGL Energy's accounting policy for PPE is also included.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.