Property Plant and Equipment Valuation

VerifiedAdded on 2023/06/05

|10

|590

|354

AI Summary

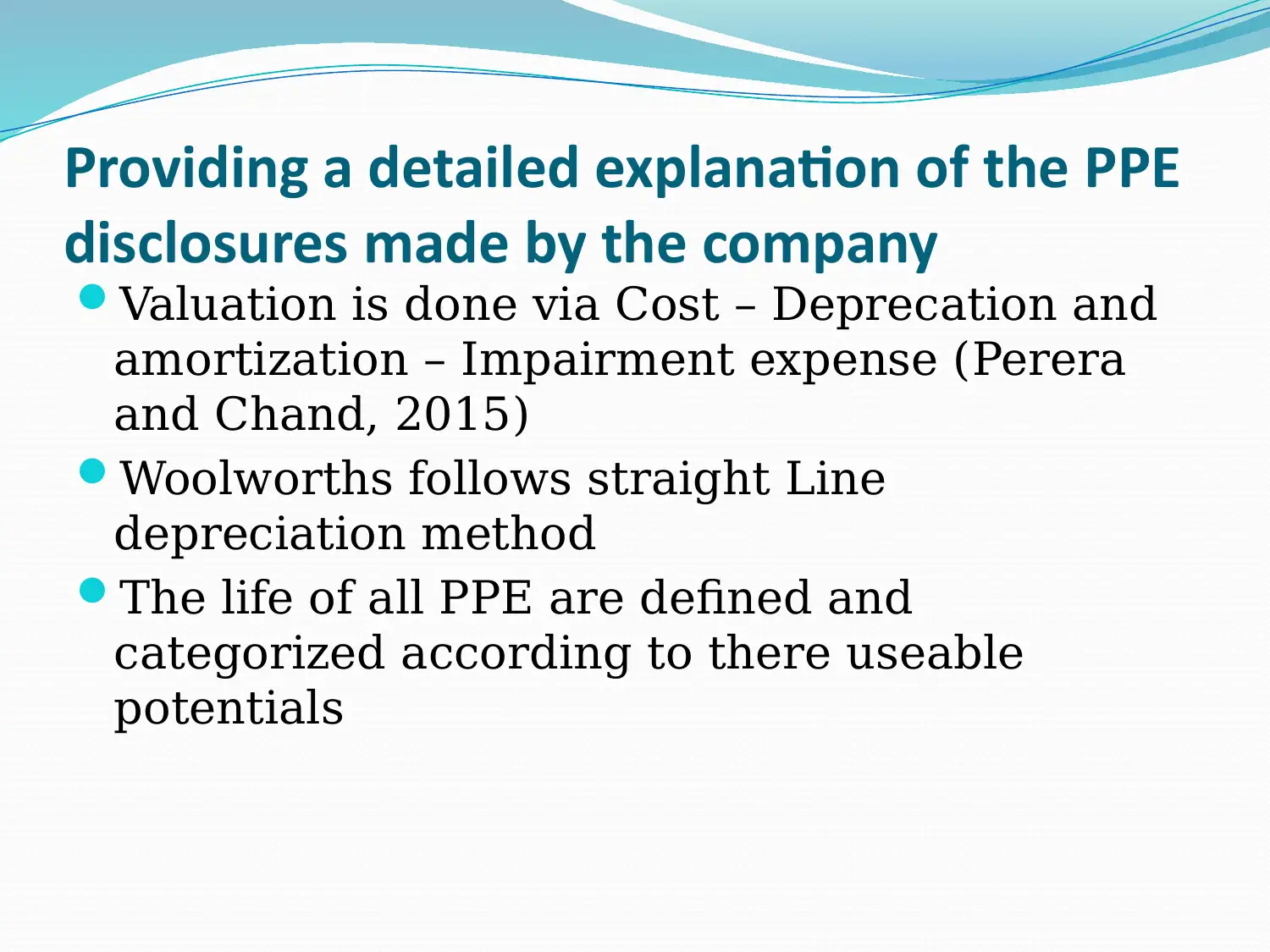

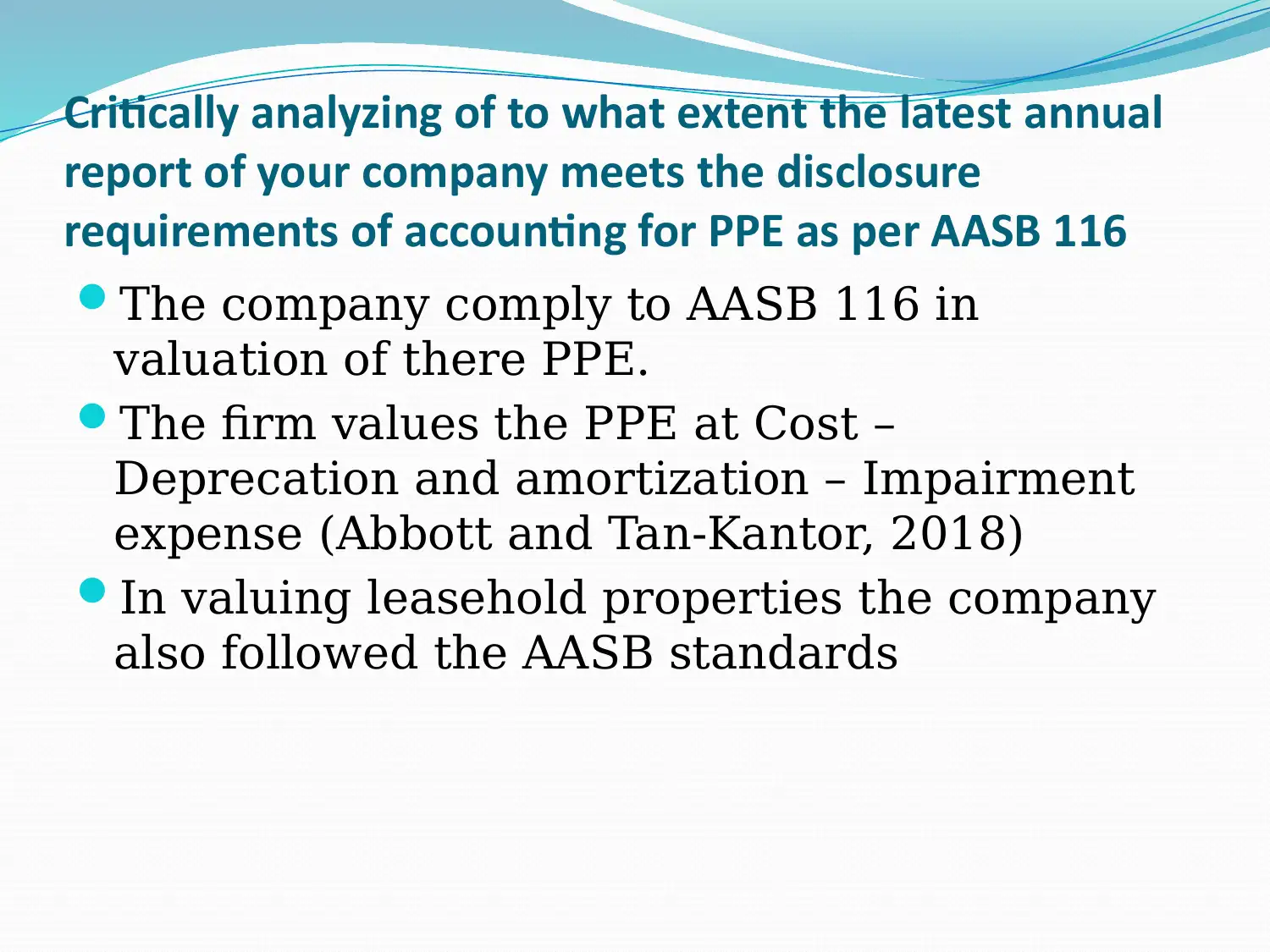

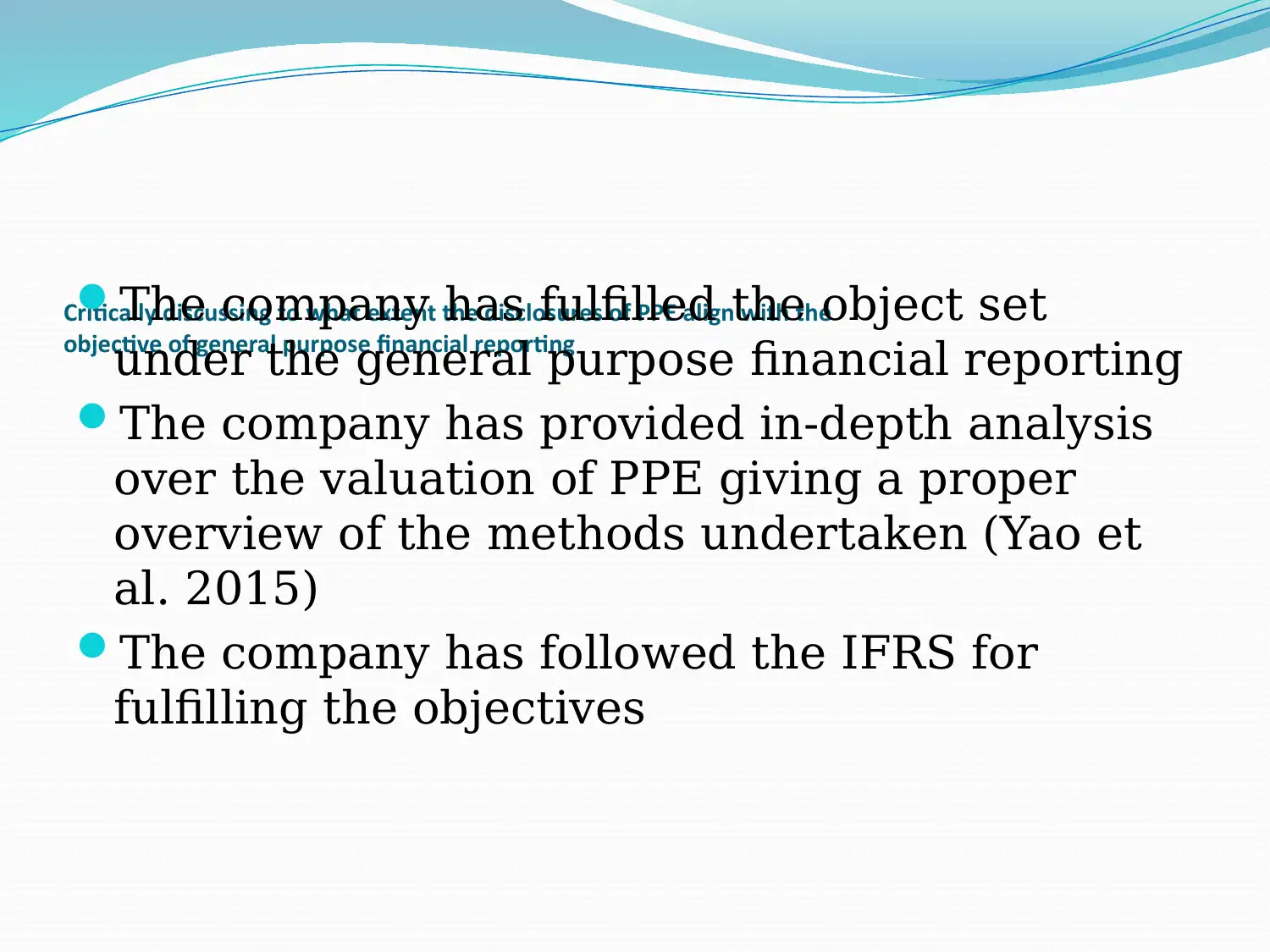

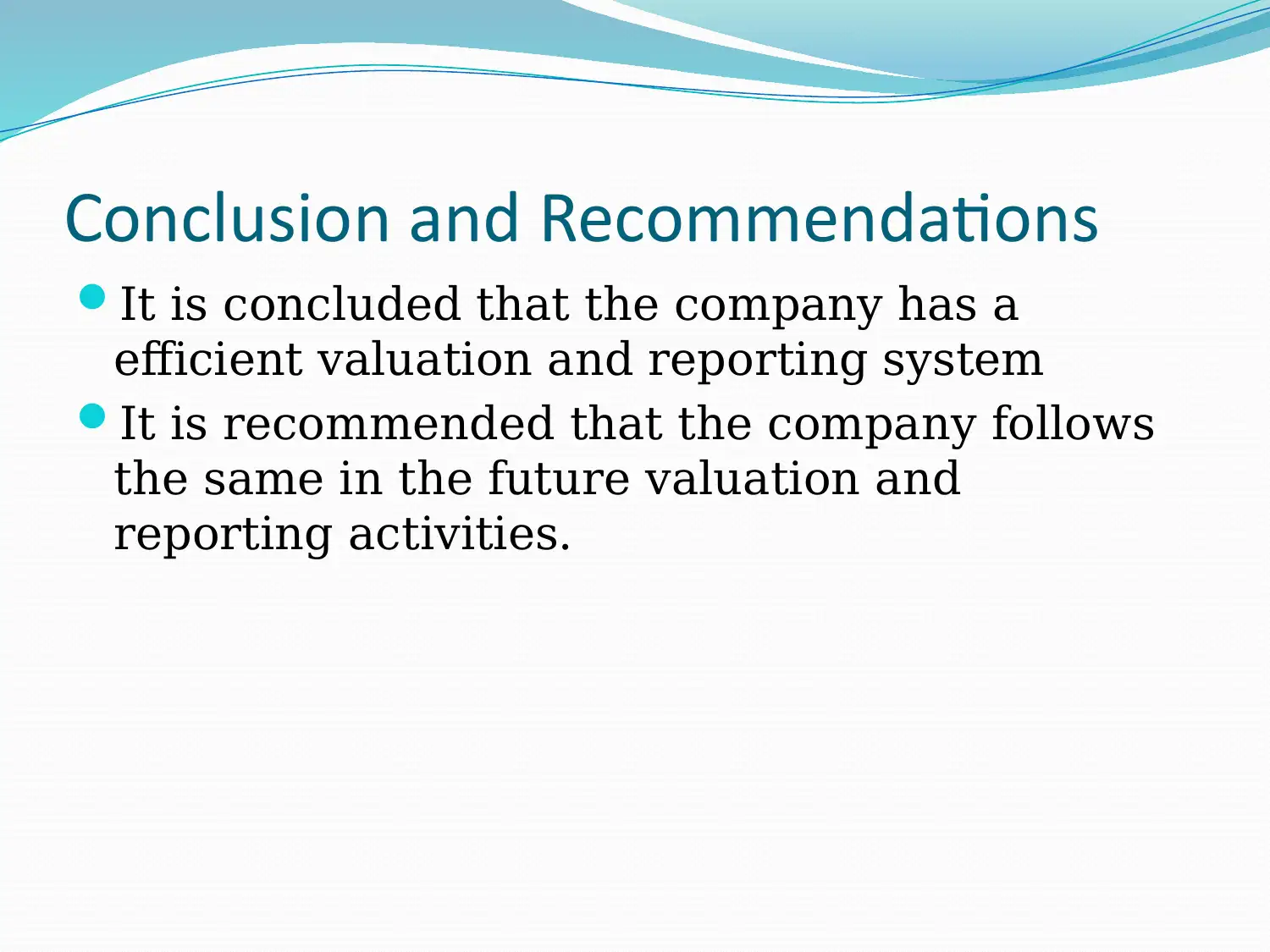

This presentation discusses the importance of valuing physical and tangible assets, specifically Property, Plant and Equipment (PPE), in order to report fair values to stakeholders. It analyzes the complexities and key issues involved in accounting for PPE, provides a detailed explanation of the PPE disclosures made by the company, and critically analyzes to what extent the latest annual report of the company meets the disclosure requirements of accounting for PPE as per AASB 116. The presentation concludes that the company has an efficient valuation and reporting system and recommends that the company follows the same in the future valuation and reporting activities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.