Acquisition Analysis of Y-s Ltd

This is the second part of assessment task 2. You can choose to do Part B either as an individual or you can pair up with another student who is currently enrolled in the unit.

6 Pages684 Words432 Views

Added on 2022-10-19

About This Document

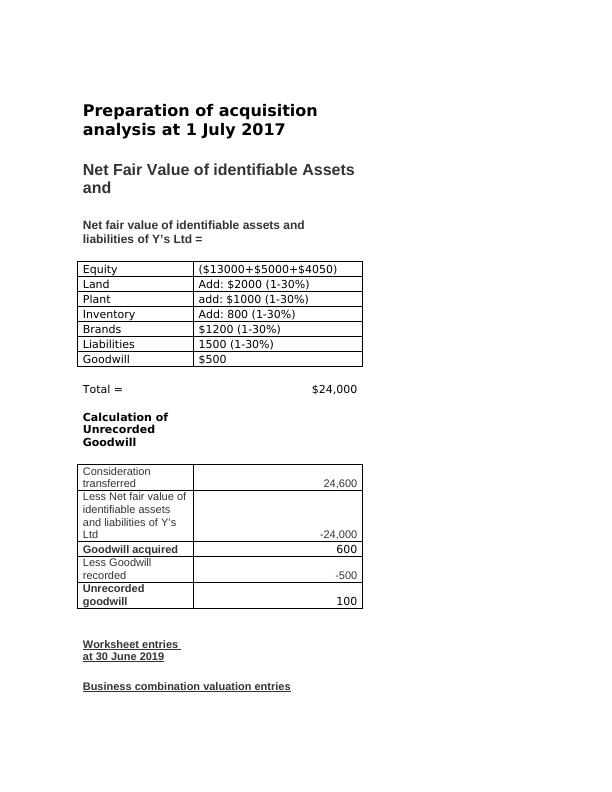

Preparation of acquisition analysis at 1 July 2017 Net Fair Value of identifiable Assets and Net fair value of identifiable assets and liabilities of Y’s Ltd = Equity ($13000+$5000+$4050) Land Add: $2000 (1-30%) Plant add: $1000 (1-30%) Inventory Add: 800 (1-30%) Brands $1200 (1-30%) Liabilities 1500 (1-30%) Goodwill $500 Total = 1050 Calculation of Unrecorded Goodwill Consideration transferred 24,600 Less Net fair value of identifiable assets and liabilities

Acquisition Analysis of Y-s Ltd

This is the second part of assessment task 2. You can choose to do Part B either as an individual or you can pair up with another student who is currently enrolled in the unit.

Added on 2022-10-19

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Acquisition Analysis and Consolidation Worksheet for Desklib

|5

|696

|193

1.Acquisition analysis At 30 June 2018:.

|3

|456

|68

Company Accounting: Acquisition Analysis, Consolidation Worksheet and Statement

|11

|1178

|437

Company Accounting: Acquisition Analysis, Consolidation Worksheet and Statement

|11

|1137

|292

Financial Accounting | Document

|11

|1543

|38

Financial Accounting: Assignment

|11

|1544

|183