Consolidated Financial Statements: Case Study and Analysis - BAP32

VerifiedAdded on 2023/01/09

|20

|2472

|77

Project

AI Summary

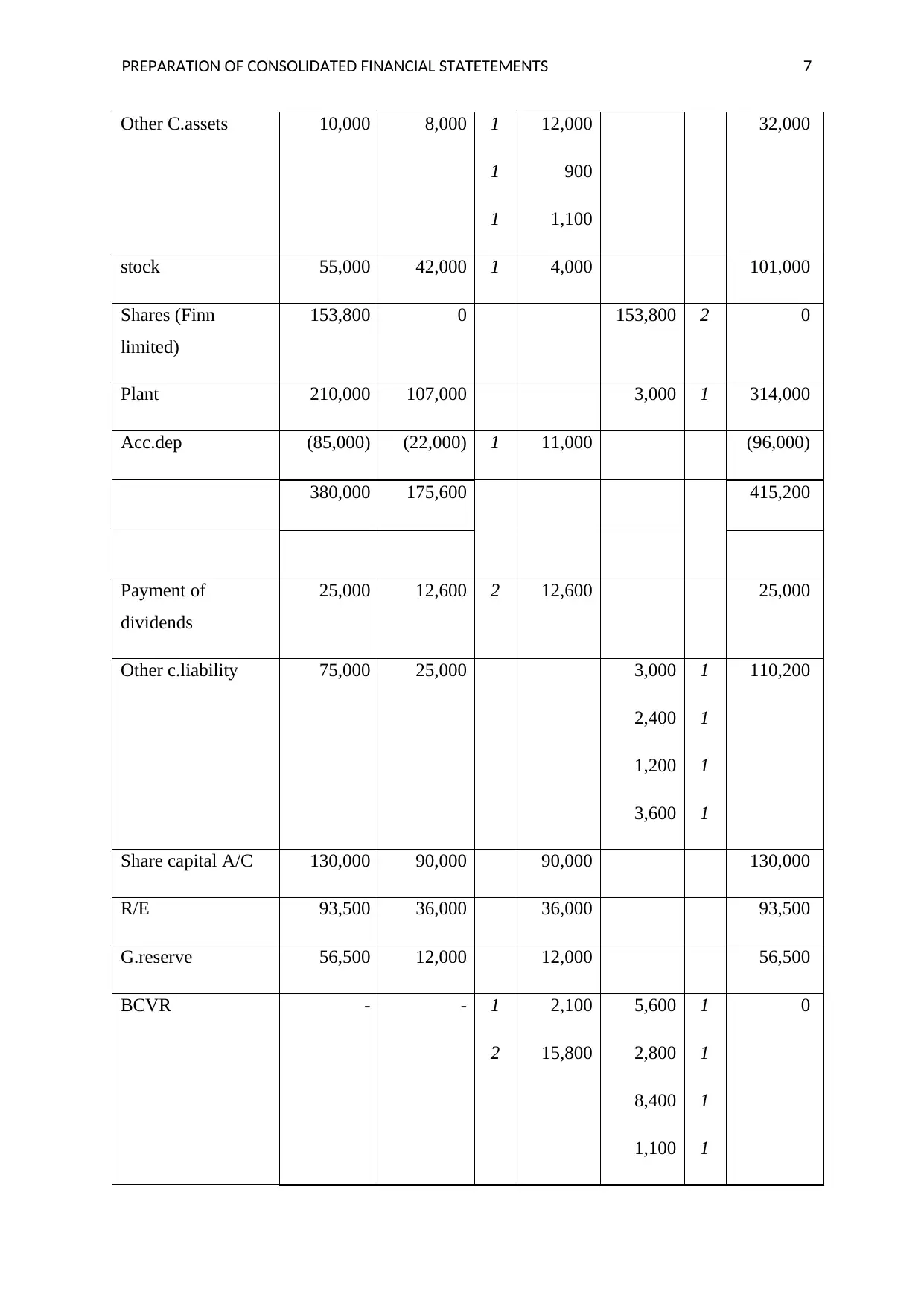

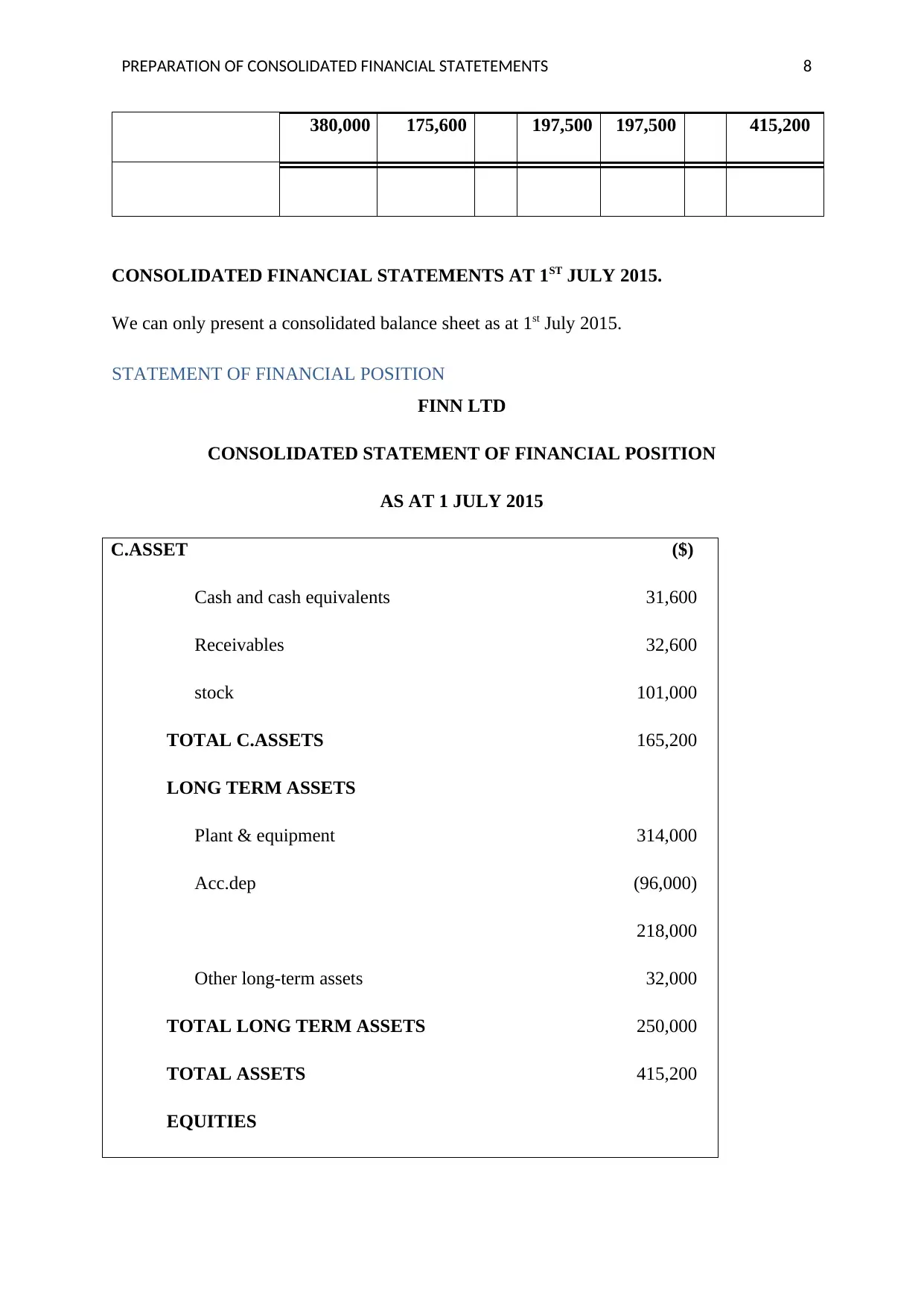

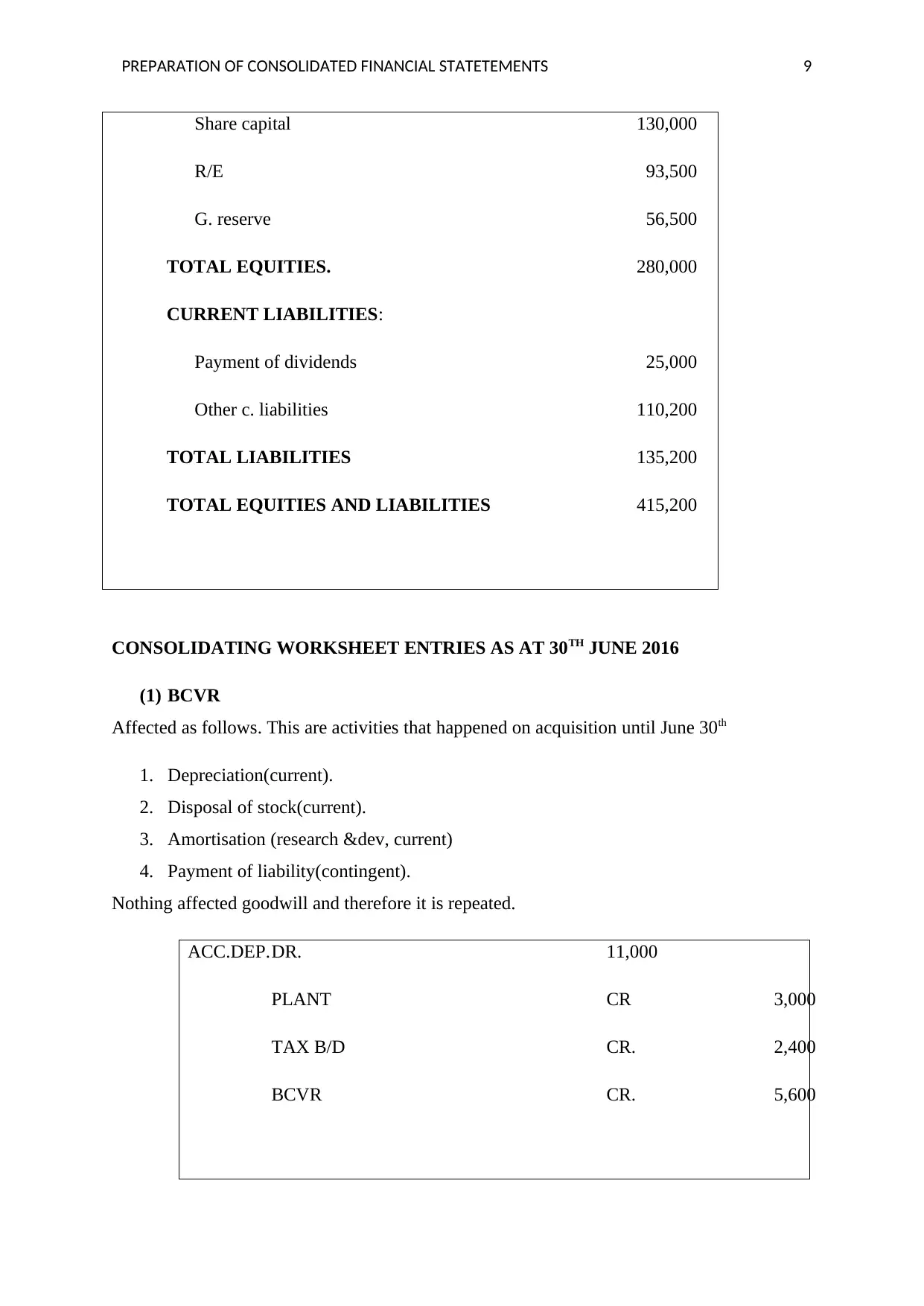

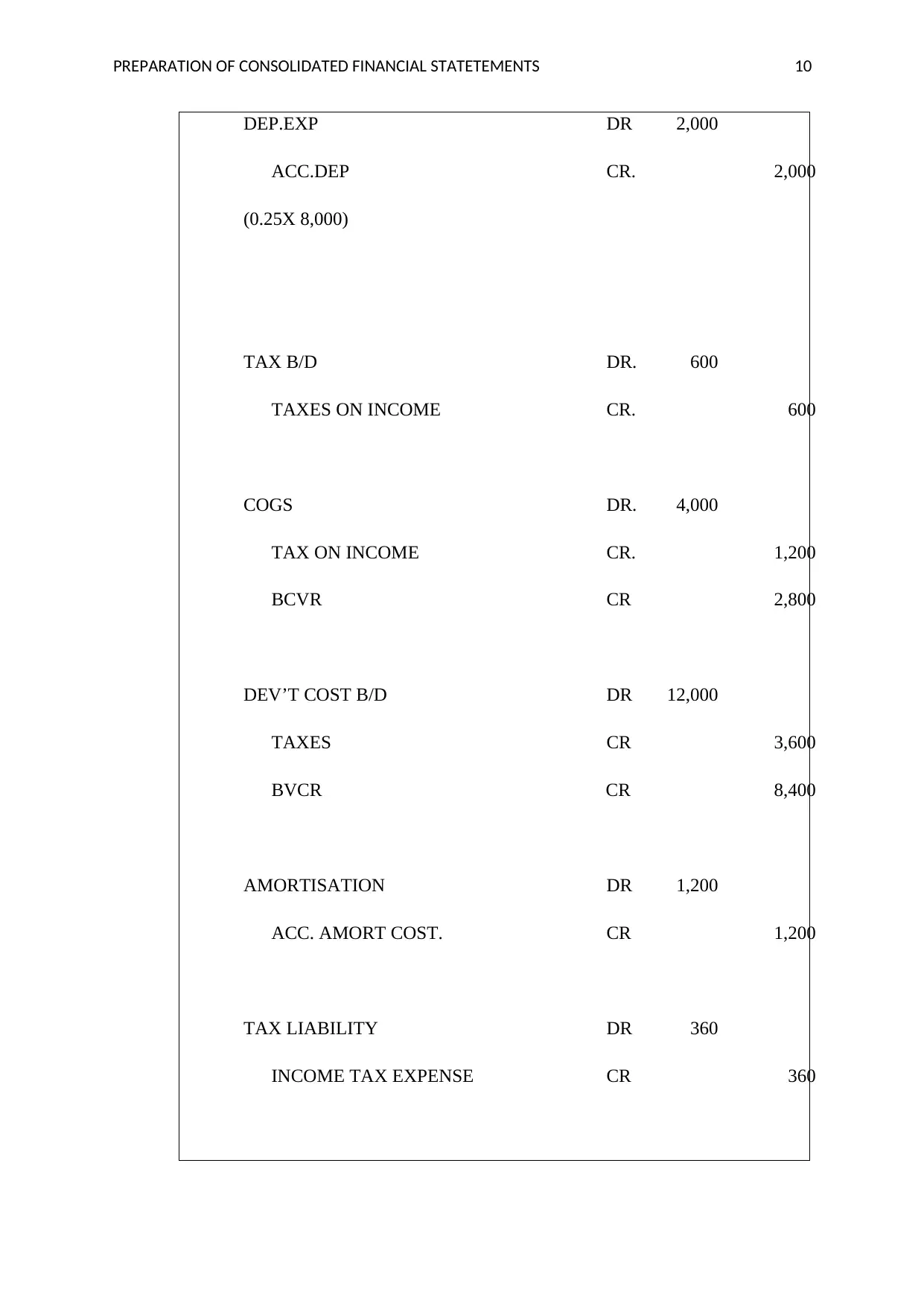

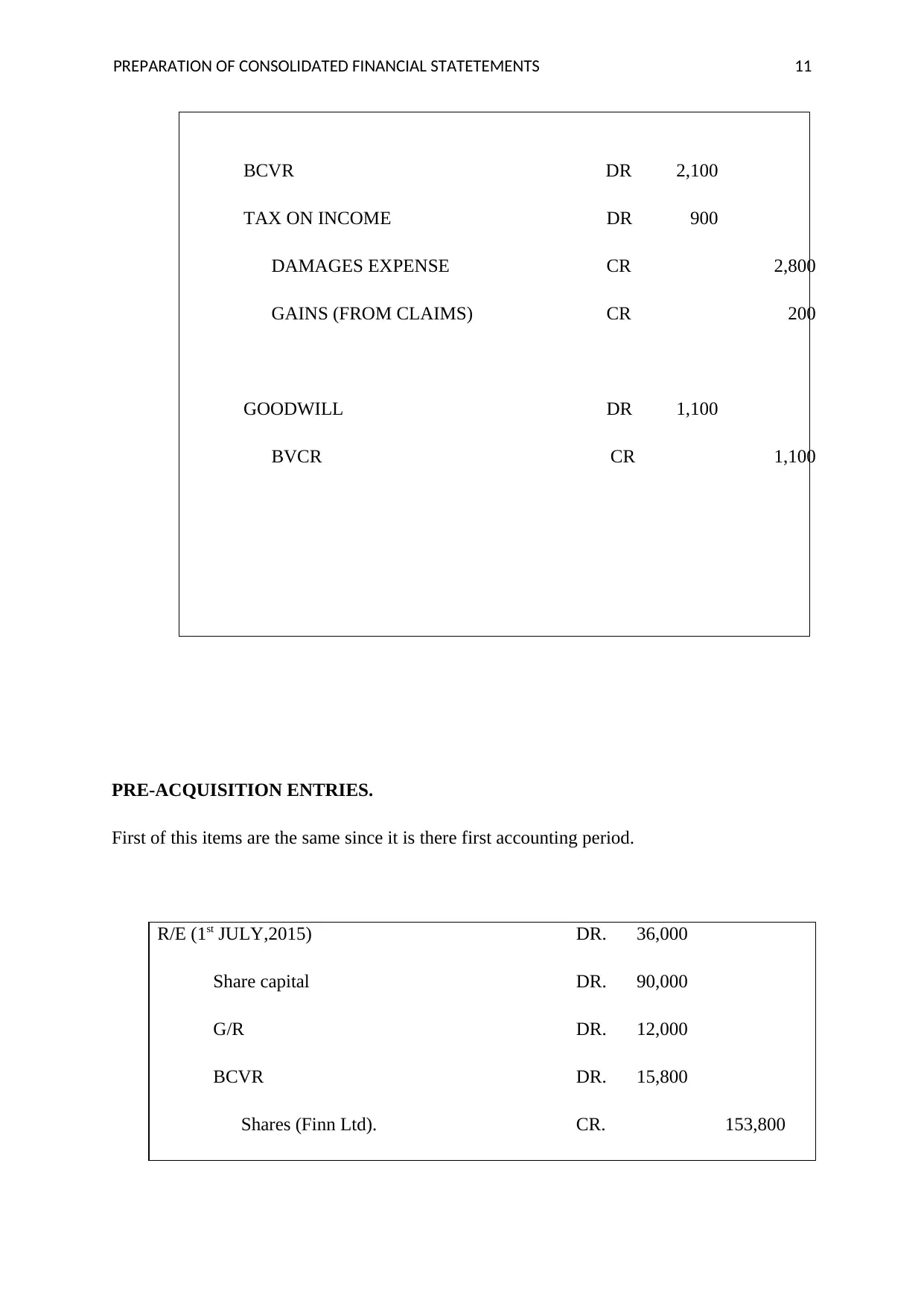

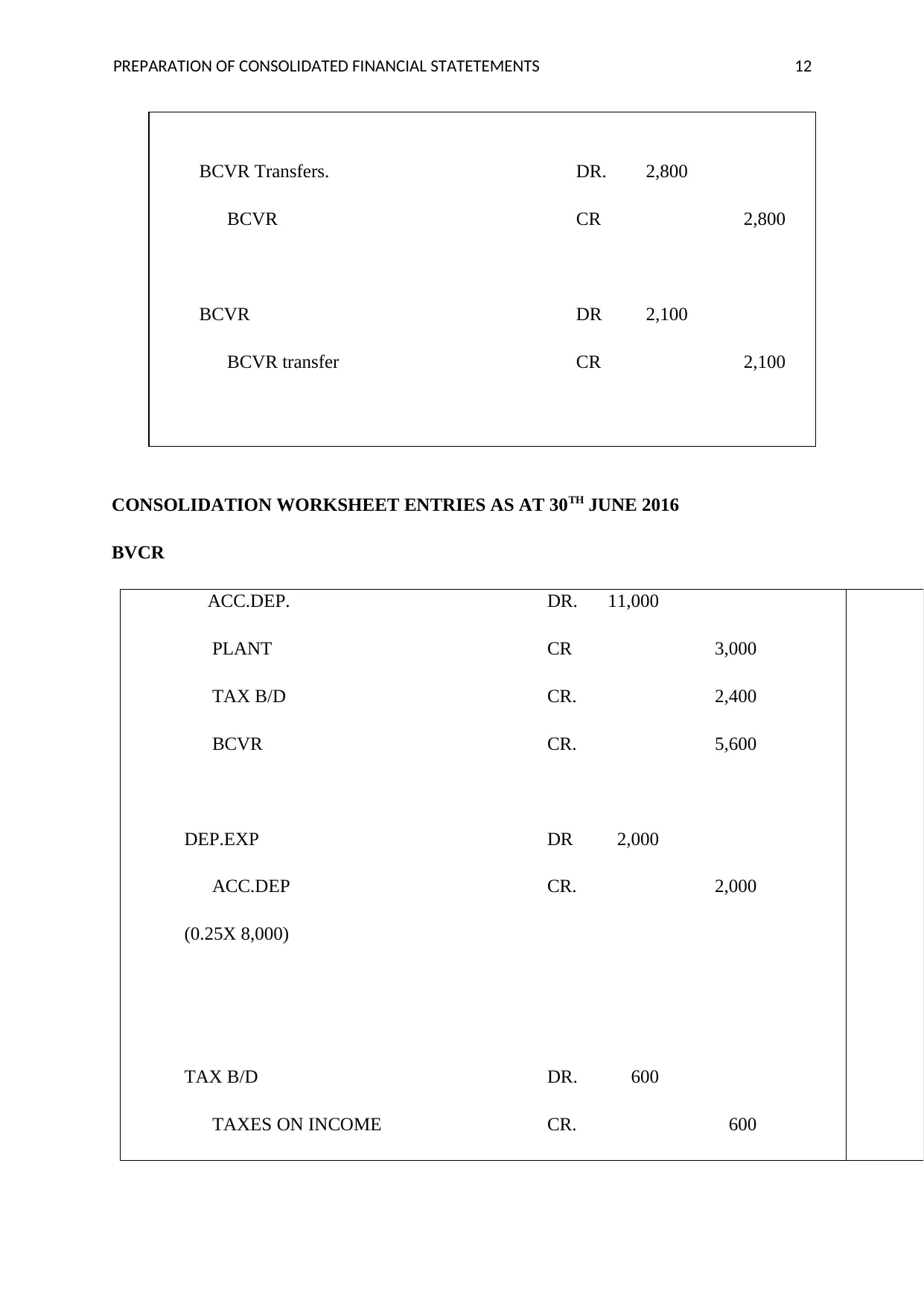

This project focuses on the preparation of consolidated financial statements, encompassing a detailed analysis of business combinations and the associated accounting procedures. The report meticulously outlines the consolidation process, including the creation and utilization of combination worksheet entries to prevent double-counting and ensure a coherent presentation of financial data. It examines the journal entries required when one business acquires another, specifically addressing pre-acquisition entries and business combination valuation entries. The analysis includes a case study involving Erik Ltd and Finn Ltd, demonstrating the calculation of goodwill, the preparation of a consolidated statement of financial position, and the impact of subsequent events. The project also explores a second case study involving Bob Ltd's acquisition of Jack Ltd, highlighting the recording of assets, liabilities, and goodwill, along with the relevant journal entries in the books of Bob Ltd. Furthermore, the report elucidates the purposes of pre-acquisition and business combination valuation entries in the context of consolidated financial statements, emphasizing their role in accurate financial reporting and the elimination of potential errors.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.