Preparation of Consolidated Worksheet for Sisters Ltd and Brothers Ltd

VerifiedAdded on 2021/06/17

|4

|861

|518

Homework Assignment

AI Summary

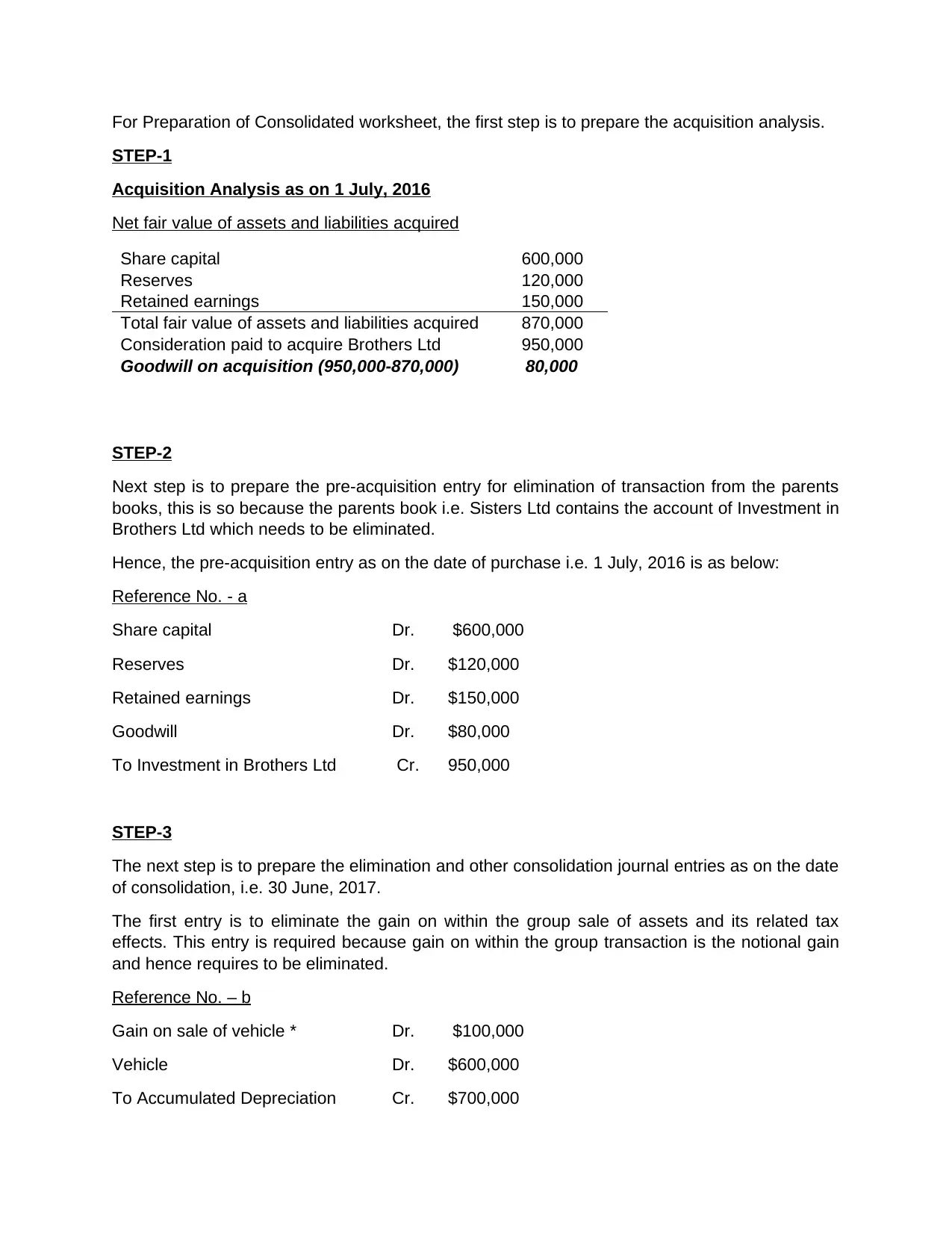

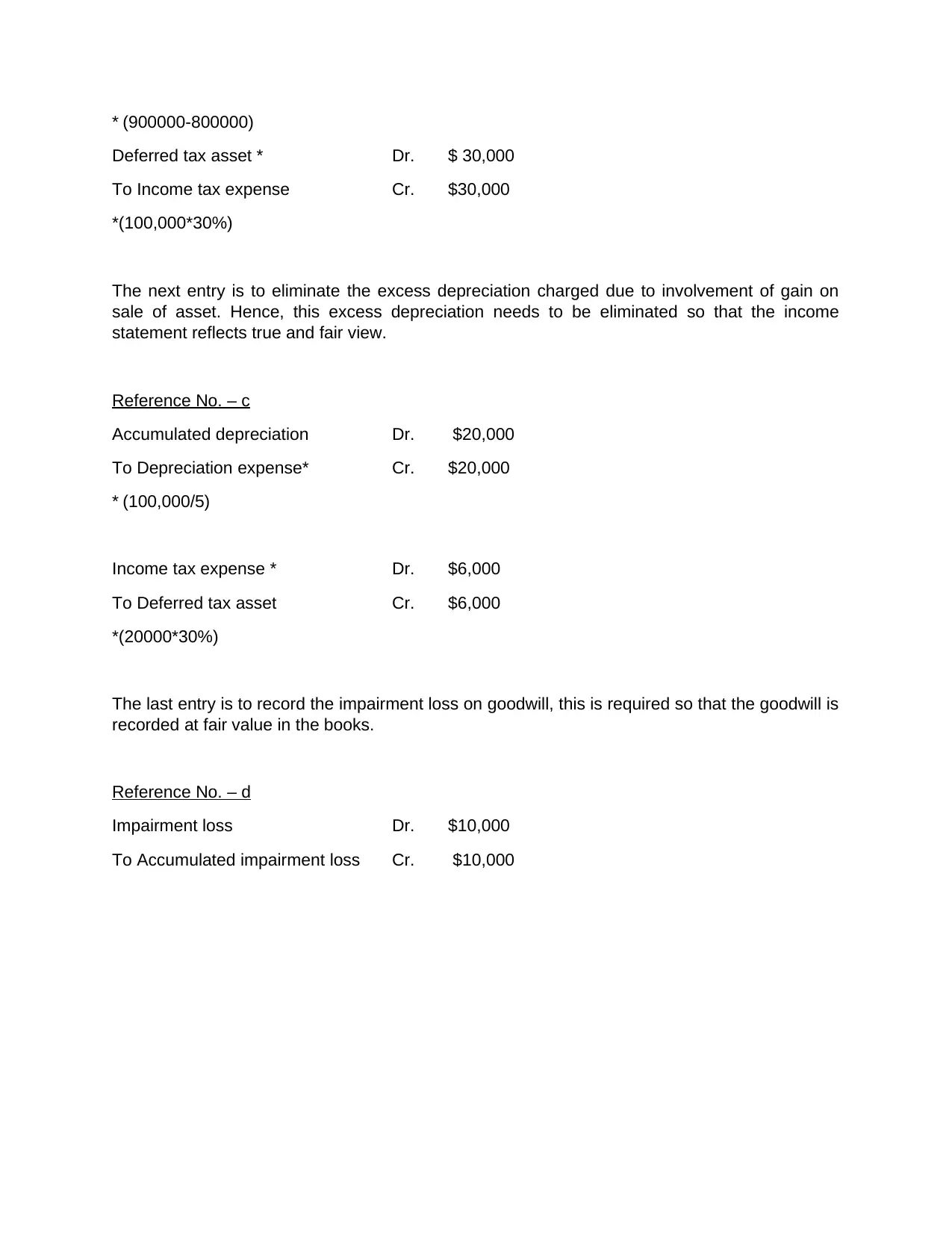

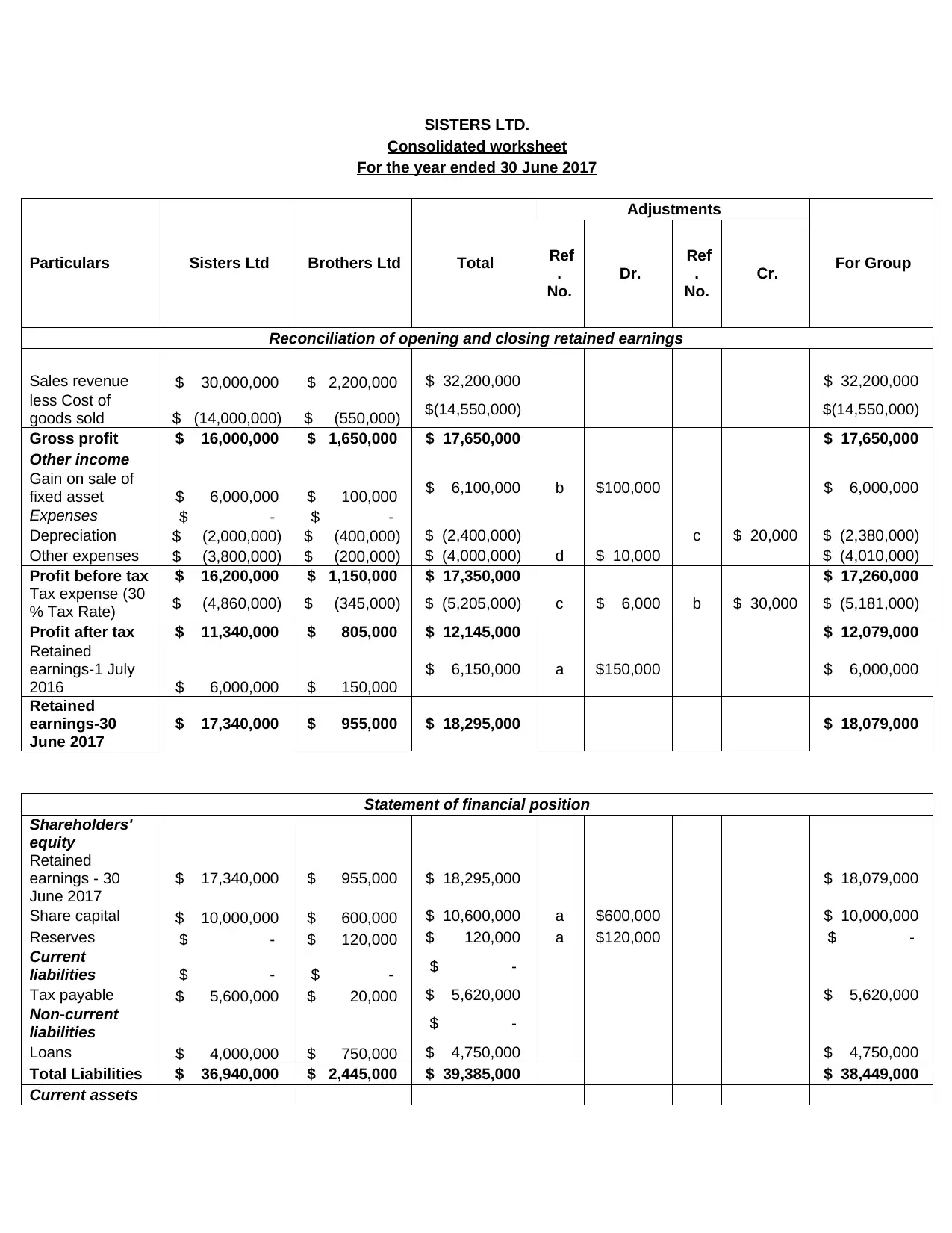

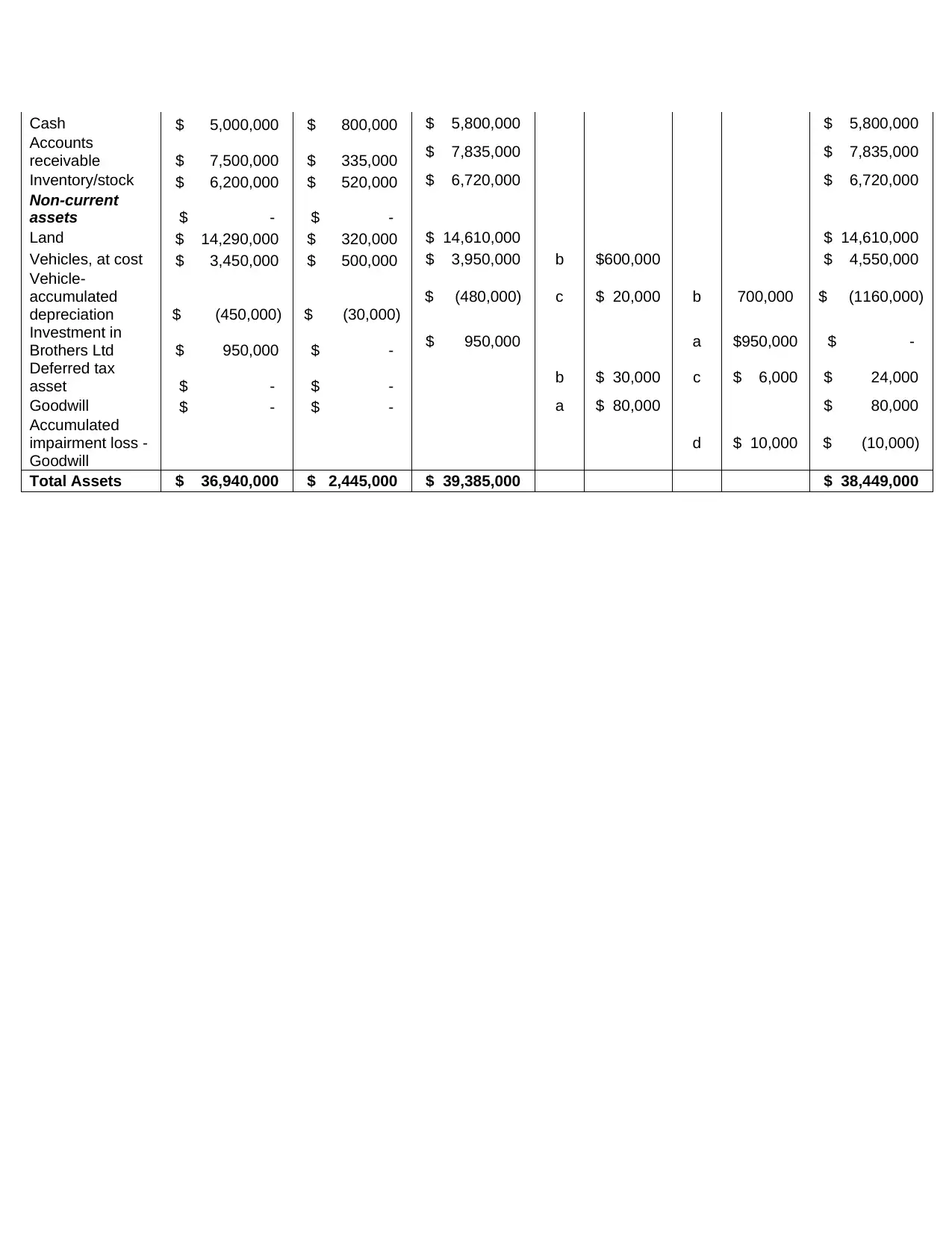

This assignment provides a detailed solution for preparing a consolidated worksheet for Sisters Ltd and Brothers Ltd. The solution begins with an acquisition analysis, calculating the net fair value of assets and liabilities, and determining goodwill. It then presents the pre-acquisition entry to eliminate the investment in Brothers Ltd from Sisters Ltd's books. Subsequent steps involve preparing elimination and consolidation journal entries, including entries to eliminate the gain on the within-group sale of assets and its related tax effects, excess depreciation, and impairment loss on goodwill. The solution includes a complete consolidated worksheet for the year ended June 30, 2017, with adjustments, and reconciliations of retained earnings and the statement of financial position. The worksheet reflects the consolidated financial performance and position of the two companies, after eliminating intercompany transactions and adjusting for fair value differences.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.