FNCE4036EL-12 Risk Management Assignment: Problems and Solutions

VerifiedAdded on 2022/08/23

|9

|1247

|15

Homework Assignment

AI Summary

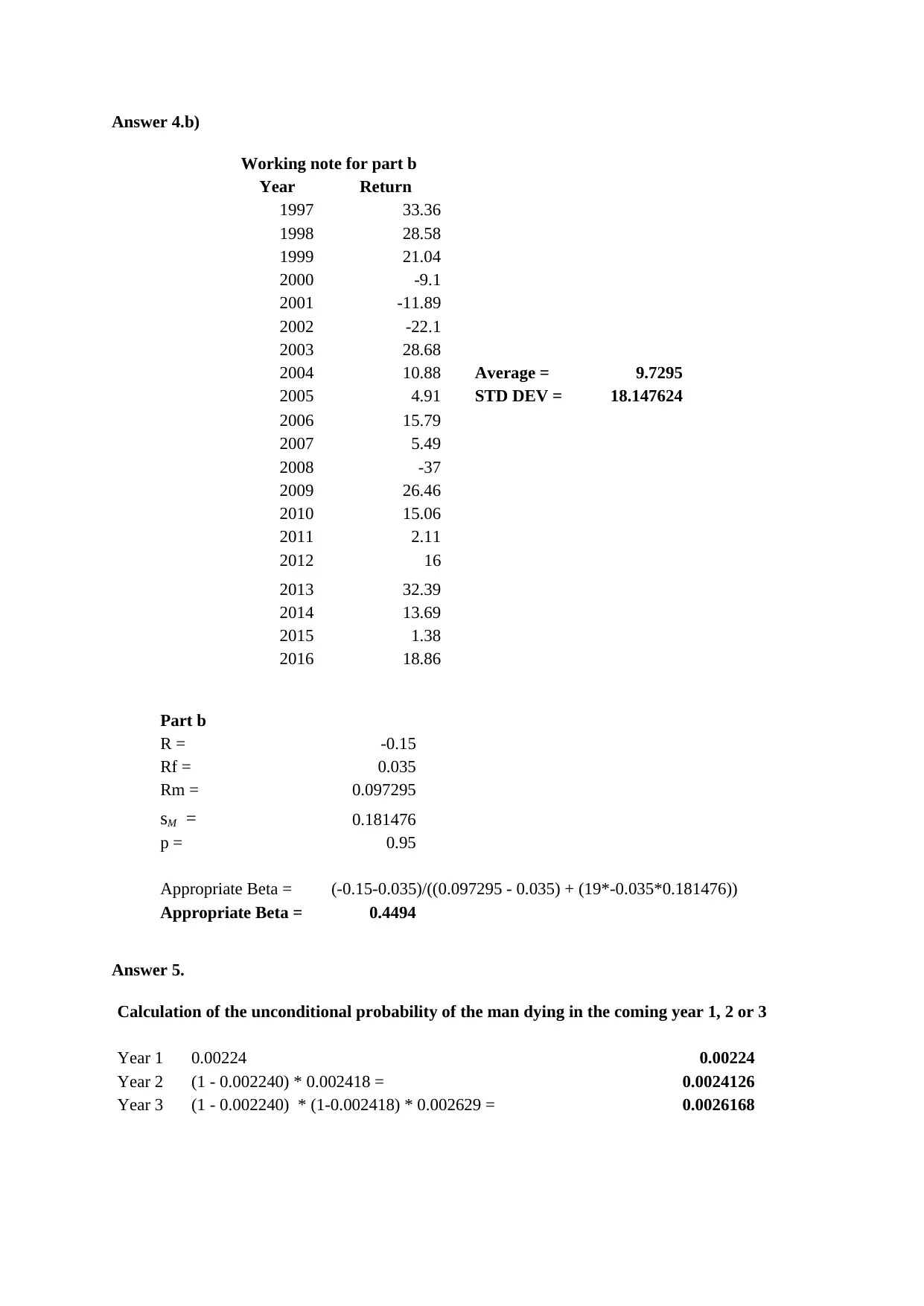

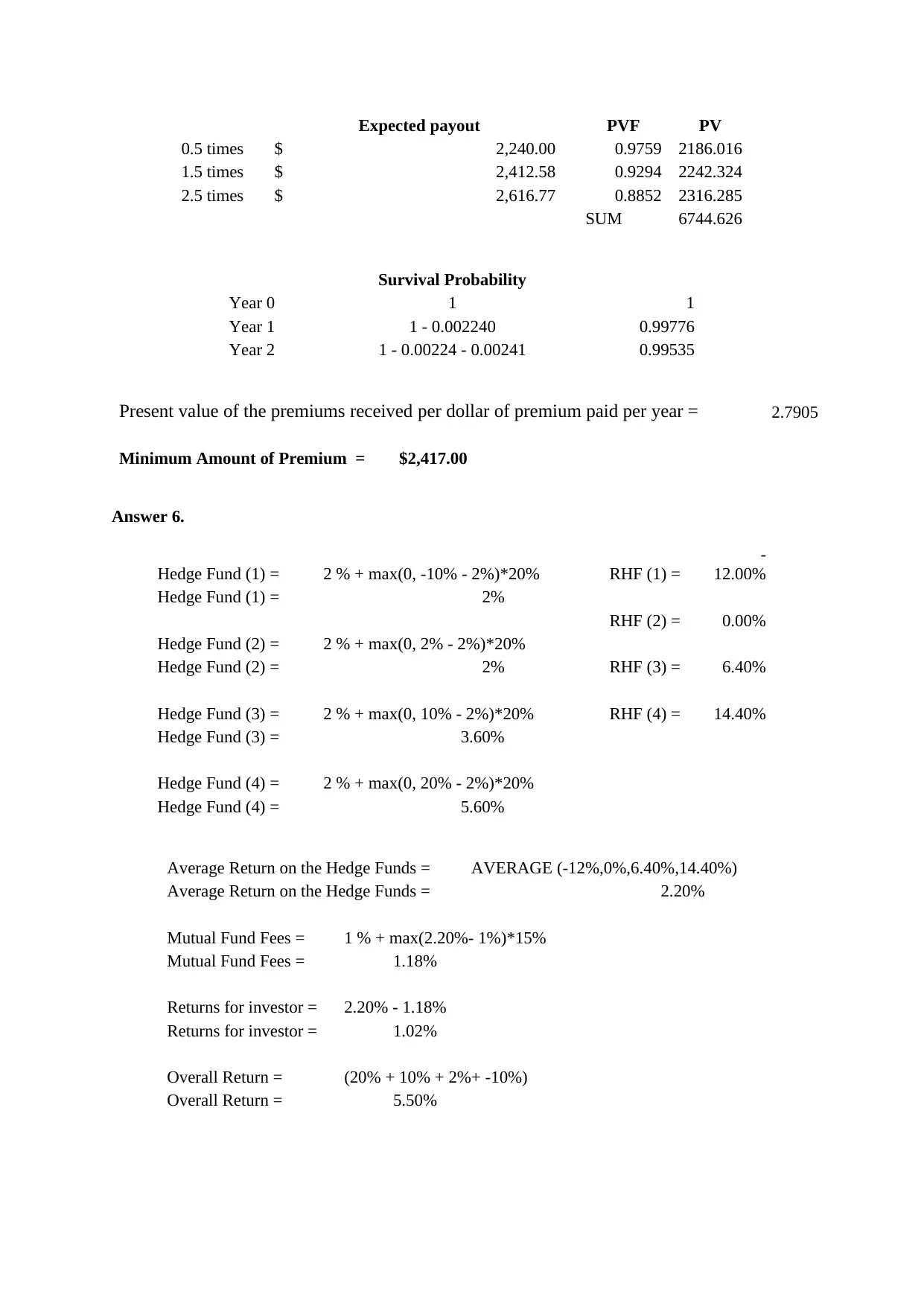

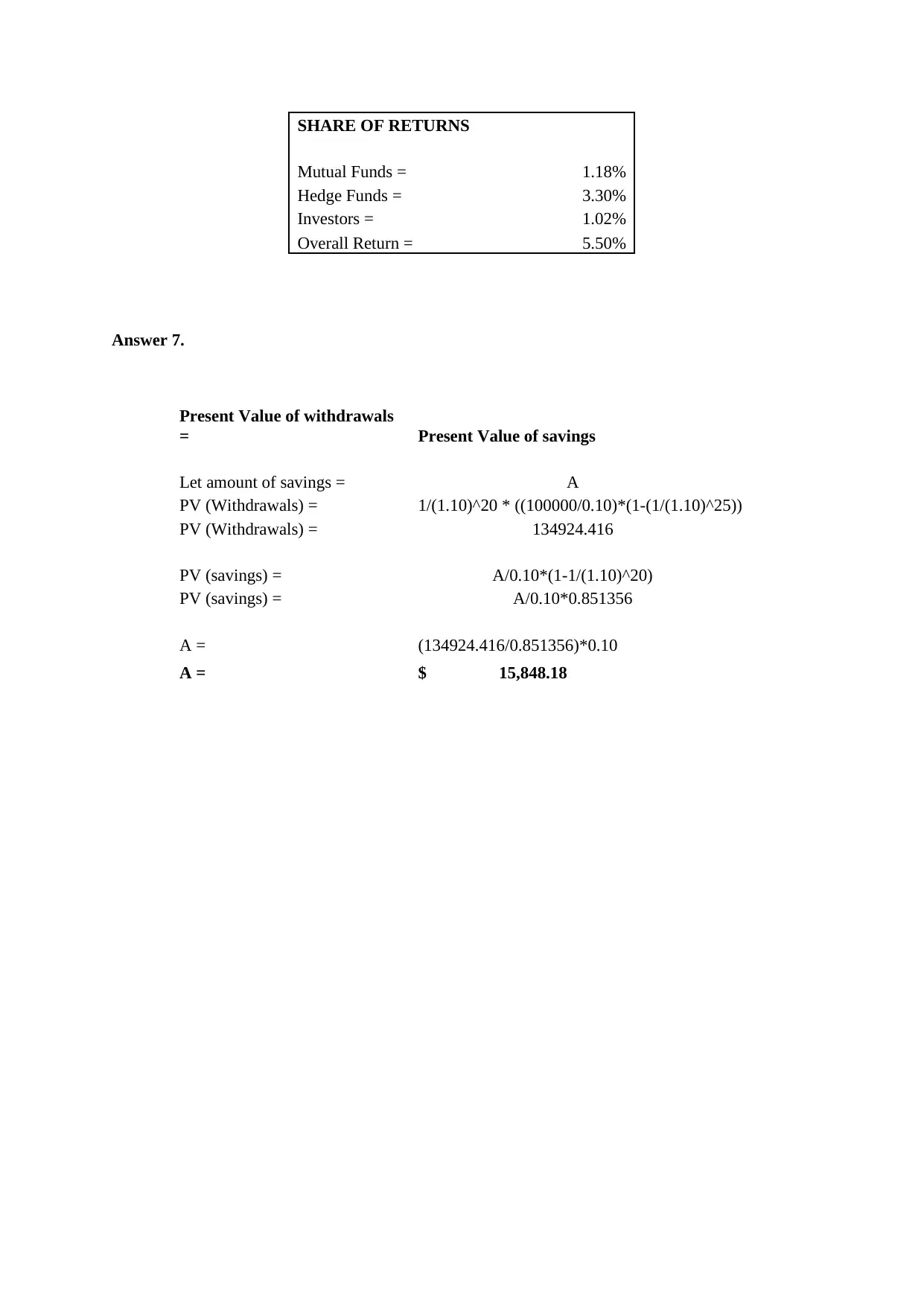

This document contains the solutions to a Finance assignment (FNCE4036) from Laurentian University, focusing on risk management. The assignment is divided into two parts: Part A consists of multiple-choice questions covering topics related to risk management, while Part B involves problem-solving and short answer questions. The solutions address concepts such as prepayment risk, operational risk, portfolio diversification, Dutch auctions, operational risk capital, beta calculation, probability and expected payouts, and hedge fund and mutual fund returns, as well as present value calculations. The solutions are comprehensive, including detailed calculations and explanations to help students understand the concepts and solve the problems effectively.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.