Project Plan Template: Primary Health Facility for Elderly Care

VerifiedAdded on 2023/06/12

|14

|4035

|116

Project

AI Summary

This project plan details the establishment of a primary health care facility in Mount Pleasant to address the needs of its growing elderly population. The plan includes a problem statement, project mission, goals, objectives (Specific, Measurable, Achievable, Realistic, Time-bound), and strategies focuse...

Project Plan Template for Primary Health Care Facility

1. Problem statement

In the recent times it has been observed that there has been a significant rise in the

ageing population of Mount Pleasant. The ageing population of the area demands more

accessible and the affordable, integrated and quality care. A facility related to health

care has to be opened up for the purpose of addressing the issues. The issues must be

addressed on an immediate basis so as to ensure the aged people of the area of basic

and quality health care (Todini et al., 2018).

2. Project mission statement

The overall project is concerned with the provision of affordable, accessible, integrated

and quality health care facility to the aged population of Mount Pleasant area.

Providing information for two main questions:

o For the purpose of addressing the issues related to the provision of quality and

affordable health care in the area a primary health care facility will be opened up.

o The facility will mainly cater to the needs of the elderly people of the area

(O'Neill&Ensle, 2015).

3. Project goals, objectives and strategies

Project goal

The goal of the project is to establish and commence the operations of a health care

facility that is capable of catering to the medical needs of the ageing population of

Mount Pleasant area.

All the ancillary actions to the construction of the health care facility will also have to be

taken actively. These will encompass activities like the promotion of the facility.

Arranging for the adequate amount of transport facility for the elderly people, to make

the bring the facility even closer to them (Carroll& Smith, 2016).

Project Objectives

Specific:

The specific objective of the entire program is to ensure that the adequate medical

facility reaches the elderly people in the right time and in the most appropriate manner.

Measurable:

One of the most important thing that needs to be measured objectively is the proportion

of the ageingpopulation that is going to be present in the total patient footprint to be

recorded by the new primary health centre. This would further enhance the calculation

in respect of the type of medicine that is going to be required, the number of doctors

1. Problem statement

In the recent times it has been observed that there has been a significant rise in the

ageing population of Mount Pleasant. The ageing population of the area demands more

accessible and the affordable, integrated and quality care. A facility related to health

care has to be opened up for the purpose of addressing the issues. The issues must be

addressed on an immediate basis so as to ensure the aged people of the area of basic

and quality health care (Todini et al., 2018).

2. Project mission statement

The overall project is concerned with the provision of affordable, accessible, integrated

and quality health care facility to the aged population of Mount Pleasant area.

Providing information for two main questions:

o For the purpose of addressing the issues related to the provision of quality and

affordable health care in the area a primary health care facility will be opened up.

o The facility will mainly cater to the needs of the elderly people of the area

(O'Neill&Ensle, 2015).

3. Project goals, objectives and strategies

Project goal

The goal of the project is to establish and commence the operations of a health care

facility that is capable of catering to the medical needs of the ageing population of

Mount Pleasant area.

All the ancillary actions to the construction of the health care facility will also have to be

taken actively. These will encompass activities like the promotion of the facility.

Arranging for the adequate amount of transport facility for the elderly people, to make

the bring the facility even closer to them (Carroll& Smith, 2016).

Project Objectives

Specific:

The specific objective of the entire program is to ensure that the adequate medical

facility reaches the elderly people in the right time and in the most appropriate manner.

Measurable:

One of the most important thing that needs to be measured objectively is the proportion

of the ageingpopulation that is going to be present in the total patient footprint to be

recorded by the new primary health centre. This would further enhance the calculation

in respect of the type of medicine that is going to be required, the number of doctors

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

specialising in certain common diseases and the number of support staff that is going to

be needed in the hospital for the purpose of helping the elderly people (Wright, 2017).

Achievable:

The target that has been set up is very much achievable. The reason being that the

infrastructure that is needed for the better and effective implementation and

commencement of the primary health care facility is readily available in the market. The

only requirement is to utilise the same for the purpose of delivery of quality and

affordable care that is directed towards the elderly population of the area

(Stiglitz&Rosengard, 2015).

Realistic:

The goal that has been ascertained is very realistic in nature. The reason being that the

service that is to be provided to the patients is directed towards a niche of patients. The

niche is comprised of elderly patients. Due to this the design of the operational structure

of the hospital will be way better than the other facilities present around the area. The

specific design of operations and the availability of the requisite facility for the elderly

will realistically ensure that the quality of service that is provided to the patients meet all

the standard requirements and the expectations of the patients.

Time limited:

For the purpose of effective and efficient implementation and commencement of the

primary health care facility it is an absolute necessity that a particular time is being fixed

within which the entire project will be completed and the operations will commence.

The timeliness in completion and the starting of the operations of the primary health

care facility will ensure that adequate services and care reaches the elderly at the

earliest possible time (Baker&Dworkin, 2017).

Project strategies (what is actually going to be done)

Based on evidence of “what works”

For the purpose of ensuring that the safety component of the project planning is taken

care of, the strategies will be based on the result that had been previously obtained by

several centres that have completed their construction and have started their operations

too.

Actionable:

The process of starting the centre will have to be commenced immediately.

Feasible:

The revenue that is going to be generated by the project corresponding to the costs that

are being incurred in its respect must be ascertained and fixed objectively.

Sustainable:

The operations of the hospital must be conducted in such a manner that it ensures that

the services and the care that is being delivered to the elderly patients are sustainable in

nature. The reason being sustainable and consistent in delivery of the service to the

patients will ensure the long term existence and the viability of the operations of the

medical centres (Lewis et al., 2016).

be needed in the hospital for the purpose of helping the elderly people (Wright, 2017).

Achievable:

The target that has been set up is very much achievable. The reason being that the

infrastructure that is needed for the better and effective implementation and

commencement of the primary health care facility is readily available in the market. The

only requirement is to utilise the same for the purpose of delivery of quality and

affordable care that is directed towards the elderly population of the area

(Stiglitz&Rosengard, 2015).

Realistic:

The goal that has been ascertained is very realistic in nature. The reason being that the

service that is to be provided to the patients is directed towards a niche of patients. The

niche is comprised of elderly patients. Due to this the design of the operational structure

of the hospital will be way better than the other facilities present around the area. The

specific design of operations and the availability of the requisite facility for the elderly

will realistically ensure that the quality of service that is provided to the patients meet all

the standard requirements and the expectations of the patients.

Time limited:

For the purpose of effective and efficient implementation and commencement of the

primary health care facility it is an absolute necessity that a particular time is being fixed

within which the entire project will be completed and the operations will commence.

The timeliness in completion and the starting of the operations of the primary health

care facility will ensure that adequate services and care reaches the elderly at the

earliest possible time (Baker&Dworkin, 2017).

Project strategies (what is actually going to be done)

Based on evidence of “what works”

For the purpose of ensuring that the safety component of the project planning is taken

care of, the strategies will be based on the result that had been previously obtained by

several centres that have completed their construction and have started their operations

too.

Actionable:

The process of starting the centre will have to be commenced immediately.

Feasible:

The revenue that is going to be generated by the project corresponding to the costs that

are being incurred in its respect must be ascertained and fixed objectively.

Sustainable:

The operations of the hospital must be conducted in such a manner that it ensures that

the services and the care that is being delivered to the elderly patients are sustainable in

nature. The reason being sustainable and consistent in delivery of the service to the

patients will ensure the long term existence and the viability of the operations of the

medical centres (Lewis et al., 2016).

Able to address political and stakeholder issues:

The hospital must ensure that no mal practices in pursuance of delivery of the care and

service to the elderly patients be adopted by the health centre. The reason for this is

that the same would attract a levy of heavy interference from the government.

Ethical :

The strategies for the purpose of delivery of care and service to the elderly patients must

be conducted in accordance with the ethical practices that are applicable and relevant in

the case of the health care (Scheffler et al., 2018).

Selected because they have the highest impact:

Only such strategies are being selected that will yield the best results in the least amount

of time.

4. Deliverables

On the completion of the project the elderly people around the area. This will ensure

that quality, affordable, accessible and reliable service and care is being provided to

them in the most appropriate manner possible.

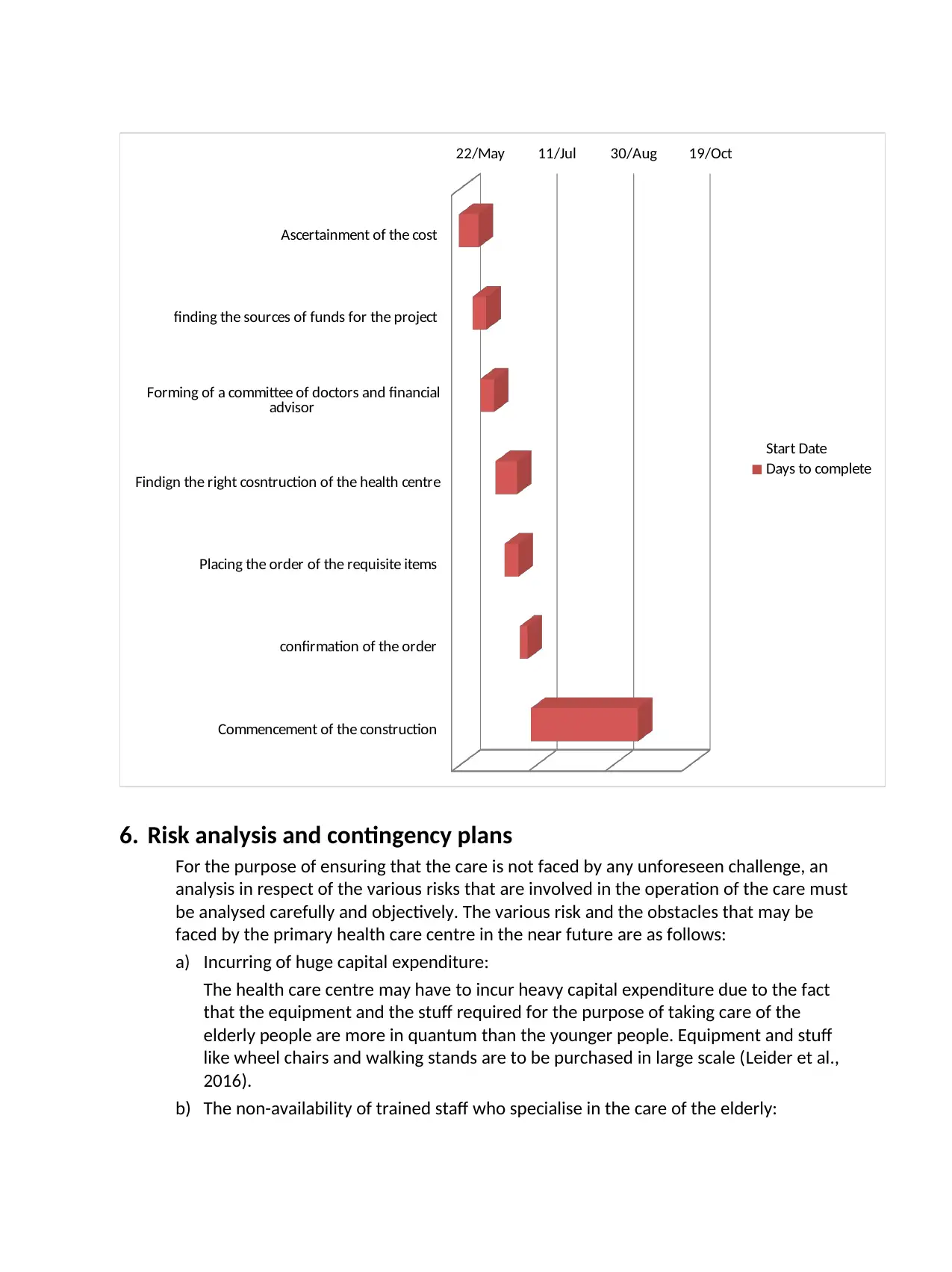

5. Work breakdown structure to detail tasks; schedule, sequencing

and timeframe

The hospital must ensure that no mal practices in pursuance of delivery of the care and

service to the elderly patients be adopted by the health centre. The reason for this is

that the same would attract a levy of heavy interference from the government.

Ethical :

The strategies for the purpose of delivery of care and service to the elderly patients must

be conducted in accordance with the ethical practices that are applicable and relevant in

the case of the health care (Scheffler et al., 2018).

Selected because they have the highest impact:

Only such strategies are being selected that will yield the best results in the least amount

of time.

4. Deliverables

On the completion of the project the elderly people around the area. This will ensure

that quality, affordable, accessible and reliable service and care is being provided to

them in the most appropriate manner possible.

5. Work breakdown structure to detail tasks; schedule, sequencing

and timeframe

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ascertainment of the cost

finding the sources of funds for the project

Forming of a committee of doctors and financial

advisor

Findign the right cosntruction of the health centre

Placing the order of the requisite items

confirmation of the order

Commencement of the construction

22/May 11/Jul 30/Aug 19/Oct

Start Date

Days to complete

6. Risk analysis and contingency plans

For the purpose of ensuring that the care is not faced by any unforeseen challenge, an

analysis in respect of the various risks that are involved in the operation of the care must

be analysed carefully and objectively. The various risk and the obstacles that may be

faced by the primary health care centre in the near future are as follows:

a) Incurring of huge capital expenditure:

The health care centre may have to incur heavy capital expenditure due to the fact

that the equipment and the stuff required for the purpose of taking care of the

elderly people are more in quantum than the younger people. Equipment and stuff

like wheel chairs and walking stands are to be purchased in large scale (Leider et al.,

2016).

b) The non-availability of trained staff who specialise in the care of the elderly:

finding the sources of funds for the project

Forming of a committee of doctors and financial

advisor

Findign the right cosntruction of the health centre

Placing the order of the requisite items

confirmation of the order

Commencement of the construction

22/May 11/Jul 30/Aug 19/Oct

Start Date

Days to complete

6. Risk analysis and contingency plans

For the purpose of ensuring that the care is not faced by any unforeseen challenge, an

analysis in respect of the various risks that are involved in the operation of the care must

be analysed carefully and objectively. The various risk and the obstacles that may be

faced by the primary health care centre in the near future are as follows:

a) Incurring of huge capital expenditure:

The health care centre may have to incur heavy capital expenditure due to the fact

that the equipment and the stuff required for the purpose of taking care of the

elderly people are more in quantum than the younger people. Equipment and stuff

like wheel chairs and walking stands are to be purchased in large scale (Leider et al.,

2016).

b) The non-availability of trained staff who specialise in the care of the elderly:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The care that has to be given to the elderly people is way more intensive and time

consuming than demanded by the younger people. Hence for the purpose of delivery

of the same it is required that the primary health care facility ensures that the

services in this regard are provided by trained professionals (Kaiser et al., 2016).

c) Increase in the death rate registered by the health care centre:

The people who are admitted in the health care facility are of advanced age, this

means the chance of their death are high. Irrespective of the quality of the service

provided by the health care facility the death rate among the elderly patient will

always remain high.

7. Project resources required

Some of the most important resources that are going to be needed for the establishment

and the commencement of the operations of the primary health care facility include the

following:

a) Building:

It is one of the most basic needs of the primary health care centre. A building will be

needed for the purpose of conducting all the services that are to be provided to the

patients. It is the structure that will house the beds for the patients and the will have

chambers for the doctors (Dalton& Holland, 2017).

b) Equipment:

There is medical equipment that will have to be acquired for the purpose of delivery

of the quality care to the elderly people of the area. These equipment include wheel

chair, various radiological equipment and beds for the patients.

c) Consumables:

The consumables refer to the one time use items that are required for conducting

the operations of the clinic on a daily basis. The consumables of the entity include

detergents, disposable gloves and disinfecting agents (Asquith& Weiss, 2016).

d) Electricity:

For the purpose of ensuring that the equipment and the other appliances of the

centre operate properly the availability of the regular flow of electricity is required in

the medical centre.

e) Water supply:

The water supply must be ensured in the centre. It is one of the most important and

basic requirement of any establishment especially in case of a medical centre.

f) Waste disposal:

Being a medical health care centre the same will generate huge amount of bio-

chemical waste. The same should be disposed of with utmost care by the

establishment.

The presence of all these resources will ensure that the medical centre doesn’t face any

difficulty in operating in the future,

consuming than demanded by the younger people. Hence for the purpose of delivery

of the same it is required that the primary health care facility ensures that the

services in this regard are provided by trained professionals (Kaiser et al., 2016).

c) Increase in the death rate registered by the health care centre:

The people who are admitted in the health care facility are of advanced age, this

means the chance of their death are high. Irrespective of the quality of the service

provided by the health care facility the death rate among the elderly patient will

always remain high.

7. Project resources required

Some of the most important resources that are going to be needed for the establishment

and the commencement of the operations of the primary health care facility include the

following:

a) Building:

It is one of the most basic needs of the primary health care centre. A building will be

needed for the purpose of conducting all the services that are to be provided to the

patients. It is the structure that will house the beds for the patients and the will have

chambers for the doctors (Dalton& Holland, 2017).

b) Equipment:

There is medical equipment that will have to be acquired for the purpose of delivery

of the quality care to the elderly people of the area. These equipment include wheel

chair, various radiological equipment and beds for the patients.

c) Consumables:

The consumables refer to the one time use items that are required for conducting

the operations of the clinic on a daily basis. The consumables of the entity include

detergents, disposable gloves and disinfecting agents (Asquith& Weiss, 2016).

d) Electricity:

For the purpose of ensuring that the equipment and the other appliances of the

centre operate properly the availability of the regular flow of electricity is required in

the medical centre.

e) Water supply:

The water supply must be ensured in the centre. It is one of the most important and

basic requirement of any establishment especially in case of a medical centre.

f) Waste disposal:

Being a medical health care centre the same will generate huge amount of bio-

chemical waste. The same should be disposed of with utmost care by the

establishment.

The presence of all these resources will ensure that the medical centre doesn’t face any

difficulty in operating in the future,

8. Project management structure

For the implementation of the project a team of quality doctors and the will be formed

who will overlook and monitor the activities related to the proposed project. For the

purpose of getting the sponsorship the various government entities and the charitable

institutions and the donors will be approached. Any additional requirement will be

fulfilled with the help of the funds that are being arranged by way of loans and

borrowings (Connor, 2015).

9. Budget

For the purpose of detailed analysis of the various costs and the revenue that are going

to be generated from the application and the implementation of the project and effort

has been made to prepare and present a complete budget that will list out all the costs

and the revenue to be incurred or generated from the project.

In addition to that the complete analysis of the cash flow statement of the company, the

start-up costs that are required to be incurred, the projected income statement of the

company determining the profitability of the proposed project, the balance sheet of the

company reflecting the financial position of the company, the breakeven analysis of the

project and the net present value of the entire project has been calculated. In addition to

that for the purpose of ensuring that the timeliness of the project is being maintained a

proper gnat chart has been produced in respect of the project ().

10. Communications and reporting

For the purpose of making it absolutely sure that all the project specifications are adequately

met, establishment of effective communication and reporting has to be undertaken between all

the members who are going to monitor and overlook the execution of the project in the near

future. For this the adequate documentation in respect of the project has to be maintained and

the same has to be presented before the team responsible in the meetings that are going to be

held regularly (Kieny&Dovlo, 2015).

For the purpose of conducting effective and efficient management and monitoring of the project

the meeting will be held after every week. The documentation that are going to be presented

include the costs invoices regarding the payment that are being paid to the labourers and the

workers who are engaged in the construction work of the centre, the cop[y of the agreement

that has been entered into with the suppliers and the contractors (Al-Hanawi et al., 2018).

The keeping of the proper records and the presentation of the same in the meeting will ensure

that the entire project is being supervised very diligently and all the requisite objectives are duel met.

For the implementation of the project a team of quality doctors and the will be formed

who will overlook and monitor the activities related to the proposed project. For the

purpose of getting the sponsorship the various government entities and the charitable

institutions and the donors will be approached. Any additional requirement will be

fulfilled with the help of the funds that are being arranged by way of loans and

borrowings (Connor, 2015).

9. Budget

For the purpose of detailed analysis of the various costs and the revenue that are going

to be generated from the application and the implementation of the project and effort

has been made to prepare and present a complete budget that will list out all the costs

and the revenue to be incurred or generated from the project.

In addition to that the complete analysis of the cash flow statement of the company, the

start-up costs that are required to be incurred, the projected income statement of the

company determining the profitability of the proposed project, the balance sheet of the

company reflecting the financial position of the company, the breakeven analysis of the

project and the net present value of the entire project has been calculated. In addition to

that for the purpose of ensuring that the timeliness of the project is being maintained a

proper gnat chart has been produced in respect of the project ().

10. Communications and reporting

For the purpose of making it absolutely sure that all the project specifications are adequately

met, establishment of effective communication and reporting has to be undertaken between all

the members who are going to monitor and overlook the execution of the project in the near

future. For this the adequate documentation in respect of the project has to be maintained and

the same has to be presented before the team responsible in the meetings that are going to be

held regularly (Kieny&Dovlo, 2015).

For the purpose of conducting effective and efficient management and monitoring of the project

the meeting will be held after every week. The documentation that are going to be presented

include the costs invoices regarding the payment that are being paid to the labourers and the

workers who are engaged in the construction work of the centre, the cop[y of the agreement

that has been entered into with the suppliers and the contractors (Al-Hanawi et al., 2018).

The keeping of the proper records and the presentation of the same in the meeting will ensure

that the entire project is being supervised very diligently and all the requisite objectives are duel met.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference

Al-Hanawi, M. K., Alsharqi, O., Almazrou, S., & Vaidya, K. (2018). Healthcare Finance in the Kingdom of

Saudi Arabia: a qualitative study of householders’ attitudes. Applied health economics and health

policy, 16(1), 55-64. (Accessed from: https://link.springer.com/article/10.1007/s40258-017-

0353-7)

Asquith, P., & Weiss, L. A. (2016). Determining a Firm's Financial Health (PIPES A). Lessons in Corporate‐

Finance: A Case Studies Approach to Financial Tools, Financial Policies, and Valuation, 7-25.

(Accessed from: https://onlinelibrary.wiley.com/doi/10.1002/9781119228899.ch2)

Baker, R. W., &Dworkin, N. R. (2017). Health care finance. Jones & Bartlett Learning. (Accessed from:

https://books.google.co.in/books?hl=en&lr=&id=tObXDQAAQBAJ&oi=fnd&pg=PP1&dq=Baker,

+R.+W.,+%26+Dworkin,+N.+R.+(2017).+Health+care+finance.+Jones+

%26+Bartlett+Learning.&ots=m_wJ1W2nPb&sig=H3Ee_lS0cTqV89v8cbWZIKf1Mlo#v=onepage&q

&f=false)

Carroll, N. W., & Smith, D. G. (2016). Addressing the healthcare finance faculty shortage: Perspectives

and paths forward. Journal of Health Administration Education, 33(2), 311-319. (Accessed from:

http://www.ingentaconnect.com/content/aupha/jhae/2016/00000033/00000002/art00008)

Connor, E. (2015). Healthcare Finance and Financial Management: Essentials for Advanced Practice

Nurses and Interdisciplinary Care Teams. Journal of the Medical Library Association: JMLA,

103(2), 111. (Accessed from: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4404853/)

Dalton, C. M., & Holland, S. B. (2017). Why Do Firms Use Insurance to Fund Worker Health Benefits? The

Role of Corporate Finance. Journal of Risk and Insurance. (Accessed from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/jori.12207)

Kaiser, K., Bredenkamp, C., & Iglesias, R. (2016). Sin Tax Reform in the Philippines: Transforming Public

Finance, Health, and Governance for More Inclusive Development. Directions in Development—

Countries and Regions. Washington, DC: World Bank. Available at: https://openknowledge.

worldbank. org/handle/10986/24617. (Accessed from: https://books.google.co.in/books?

hl=en&lr=&id=eObCDAAAQBAJ&oi=fnd&pg=PT10&dq=Kaiser,+K.,+Bredenkamp,+C.,+

%26+Iglesias,+R.+(2016).+Sin+Tax+Reform+in+the+Philippines:+Transforming+Public+Finance,

+Health,+and+Governance+for+More+Inclusive+Development.+Directions+in+Development

%E2%80%94Countries+and+Regions.+Washington,+DC:+World+Bank.

+Availab&ots=PXNIpA_zwE&sig=mV2Hf3q5ThKgzdjlPhppgv-IoGE)

Kieny, M. P., &Dovlo, D. (2015). Beyond Ebola: a new agenda for resilient health systems. Lancet

(London, England), 385(9963), 91. (Accessed from:

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5513100/)

Leider, J. P., Resnick, B. A., Sensenig, A. L., Alfonso, N., Brady, E., &Bishai, D. M. (2016). Assessing the

public health activity estimate from the National Health Expenditure Accounts: why public health

Al-Hanawi, M. K., Alsharqi, O., Almazrou, S., & Vaidya, K. (2018). Healthcare Finance in the Kingdom of

Saudi Arabia: a qualitative study of householders’ attitudes. Applied health economics and health

policy, 16(1), 55-64. (Accessed from: https://link.springer.com/article/10.1007/s40258-017-

0353-7)

Asquith, P., & Weiss, L. A. (2016). Determining a Firm's Financial Health (PIPES A). Lessons in Corporate‐

Finance: A Case Studies Approach to Financial Tools, Financial Policies, and Valuation, 7-25.

(Accessed from: https://onlinelibrary.wiley.com/doi/10.1002/9781119228899.ch2)

Baker, R. W., &Dworkin, N. R. (2017). Health care finance. Jones & Bartlett Learning. (Accessed from:

https://books.google.co.in/books?hl=en&lr=&id=tObXDQAAQBAJ&oi=fnd&pg=PP1&dq=Baker,

+R.+W.,+%26+Dworkin,+N.+R.+(2017).+Health+care+finance.+Jones+

%26+Bartlett+Learning.&ots=m_wJ1W2nPb&sig=H3Ee_lS0cTqV89v8cbWZIKf1Mlo#v=onepage&q

&f=false)

Carroll, N. W., & Smith, D. G. (2016). Addressing the healthcare finance faculty shortage: Perspectives

and paths forward. Journal of Health Administration Education, 33(2), 311-319. (Accessed from:

http://www.ingentaconnect.com/content/aupha/jhae/2016/00000033/00000002/art00008)

Connor, E. (2015). Healthcare Finance and Financial Management: Essentials for Advanced Practice

Nurses and Interdisciplinary Care Teams. Journal of the Medical Library Association: JMLA,

103(2), 111. (Accessed from: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4404853/)

Dalton, C. M., & Holland, S. B. (2017). Why Do Firms Use Insurance to Fund Worker Health Benefits? The

Role of Corporate Finance. Journal of Risk and Insurance. (Accessed from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/jori.12207)

Kaiser, K., Bredenkamp, C., & Iglesias, R. (2016). Sin Tax Reform in the Philippines: Transforming Public

Finance, Health, and Governance for More Inclusive Development. Directions in Development—

Countries and Regions. Washington, DC: World Bank. Available at: https://openknowledge.

worldbank. org/handle/10986/24617. (Accessed from: https://books.google.co.in/books?

hl=en&lr=&id=eObCDAAAQBAJ&oi=fnd&pg=PT10&dq=Kaiser,+K.,+Bredenkamp,+C.,+

%26+Iglesias,+R.+(2016).+Sin+Tax+Reform+in+the+Philippines:+Transforming+Public+Finance,

+Health,+and+Governance+for+More+Inclusive+Development.+Directions+in+Development

%E2%80%94Countries+and+Regions.+Washington,+DC:+World+Bank.

+Availab&ots=PXNIpA_zwE&sig=mV2Hf3q5ThKgzdjlPhppgv-IoGE)

Kieny, M. P., &Dovlo, D. (2015). Beyond Ebola: a new agenda for resilient health systems. Lancet

(London, England), 385(9963), 91. (Accessed from:

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5513100/)

Leider, J. P., Resnick, B. A., Sensenig, A. L., Alfonso, N., Brady, E., &Bishai, D. M. (2016). Assessing the

public health activity estimate from the National Health Expenditure Accounts: why public health

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenditure definitions matter. J Health Care Finance, 43(2), 225-240. (Accessed from:

http://www.healthfinancejournal.com/index.php/johcf/article/view/112)

Lewis, M. A., Lewis, C. E., Leake, B., King, B. H., &Lindemanne, R. (2016). The quality of health care for

adults with developmental disabilities. Public health reports. (Accessed from:

http://journals.sagepub.com/doi/full/10.1093/phr/117.2.174)

O'Neill, B., &Ensle, K. (2015). Personal Health and Finance Quiz&58; A Tool for Outreach, Research, and

Evaluation. Journal of Human Sciences and Extension, 3(1), 149-149. (Accessed from:

http://www.ingentaconnect.com/content/doaj/23255226/2015/00000003/00000001/art00011)

Scheffler, R. M., Hoang, D. D., &Shortell, S. M. (2018). Proposal to Use Three Initiatives to Lower

Healthcare Spending and Finance Universal Health Insurance Coverage in California. (Accessed

from: http://petris.org/wp-content/uploads/2018/03/Proposal-to-Lower-Spending-and-Finance-

Universal-Coverage-Full-Report.pdf)

Stiglitz, J. E., &Rosengard, J. K. (2015). Economics of the Public Sector: Fourth International Student

Edition. WW Norton & Company. (Accessed from: https://books.google.co.in/books?

hl=en&lr=&id=miPeCgAAQBAJ&oi=fnd&pg=PR24&dq=Stiglitz,+J.+E.,+%26Rosengard,+J.+K.

+(2015).+Economics+of+the+Public+Sector:+Fourth+International+Student+Edition.

+WW+Norton+

%26+Company.&ots=VS3NQ4jZdy&sig=oGdd8g4qqeNw_MsvZubB1ZbGKlk#v=onepage&q&f=fals

e)

Todini, N., Hammett, T. M., &Fryatt, B. (2018). Integrating HIV/AIDS in Vietnam's Social Health Insurance

Scheme: Experience and Lessons from the Health Finance and Governance Project, 2014–2017.

Health Systems & Reform, (just-accepted), 1-28. (Accessed from:

https://www.tandfonline.com/doi/abs/10.1080/23288604.2018.1440346)

World Health Organization. (2015). WHO report on the global tobacco epidemic 2015: raising taxes on

tobacco. World Health Organization. (Accessed from: https://books.google.co.in/books?

hl=en&lr=&id=3k80DgAAQBAJ&oi=fnd&pg=PP1&dq=World+Health+Organization.+(2015).

+WHO+report+on+the+global+tobacco+epidemic+2015:+raising+taxes+on+tobacco.

+World+Health+Organization.&ots=EcZ5K86Clx&sig=L93oOPHIgm5CtjWIkAn6UVA97ws#v=onepa

ge&q=World%20Health%20Organization.%20(2015).%20WHO%20report%20on%20the

%20global%20tobacco%20epidemic%202015%3A%20raising%20taxes%20on%20tobacco.

%20World%20Health%20Organization.&f=false)

Wright, J. (2017). The link between provider payment and quality of maternal health services: a

framework and literature review. (Accessed from: https://www.popline.org/node/662075)

http://www.healthfinancejournal.com/index.php/johcf/article/view/112)

Lewis, M. A., Lewis, C. E., Leake, B., King, B. H., &Lindemanne, R. (2016). The quality of health care for

adults with developmental disabilities. Public health reports. (Accessed from:

http://journals.sagepub.com/doi/full/10.1093/phr/117.2.174)

O'Neill, B., &Ensle, K. (2015). Personal Health and Finance Quiz&58; A Tool for Outreach, Research, and

Evaluation. Journal of Human Sciences and Extension, 3(1), 149-149. (Accessed from:

http://www.ingentaconnect.com/content/doaj/23255226/2015/00000003/00000001/art00011)

Scheffler, R. M., Hoang, D. D., &Shortell, S. M. (2018). Proposal to Use Three Initiatives to Lower

Healthcare Spending and Finance Universal Health Insurance Coverage in California. (Accessed

from: http://petris.org/wp-content/uploads/2018/03/Proposal-to-Lower-Spending-and-Finance-

Universal-Coverage-Full-Report.pdf)

Stiglitz, J. E., &Rosengard, J. K. (2015). Economics of the Public Sector: Fourth International Student

Edition. WW Norton & Company. (Accessed from: https://books.google.co.in/books?

hl=en&lr=&id=miPeCgAAQBAJ&oi=fnd&pg=PR24&dq=Stiglitz,+J.+E.,+%26Rosengard,+J.+K.

+(2015).+Economics+of+the+Public+Sector:+Fourth+International+Student+Edition.

+WW+Norton+

%26+Company.&ots=VS3NQ4jZdy&sig=oGdd8g4qqeNw_MsvZubB1ZbGKlk#v=onepage&q&f=fals

e)

Todini, N., Hammett, T. M., &Fryatt, B. (2018). Integrating HIV/AIDS in Vietnam's Social Health Insurance

Scheme: Experience and Lessons from the Health Finance and Governance Project, 2014–2017.

Health Systems & Reform, (just-accepted), 1-28. (Accessed from:

https://www.tandfonline.com/doi/abs/10.1080/23288604.2018.1440346)

World Health Organization. (2015). WHO report on the global tobacco epidemic 2015: raising taxes on

tobacco. World Health Organization. (Accessed from: https://books.google.co.in/books?

hl=en&lr=&id=3k80DgAAQBAJ&oi=fnd&pg=PP1&dq=World+Health+Organization.+(2015).

+WHO+report+on+the+global+tobacco+epidemic+2015:+raising+taxes+on+tobacco.

+World+Health+Organization.&ots=EcZ5K86Clx&sig=L93oOPHIgm5CtjWIkAn6UVA97ws#v=onepa

ge&q=World%20Health%20Organization.%20(2015).%20WHO%20report%20on%20the

%20global%20tobacco%20epidemic%202015%3A%20raising%20taxes%20on%20tobacco.

%20World%20Health%20Organization.&f=false)

Wright, J. (2017). The link between provider payment and quality of maternal health services: a

framework and literature review. (Accessed from: https://www.popline.org/node/662075)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

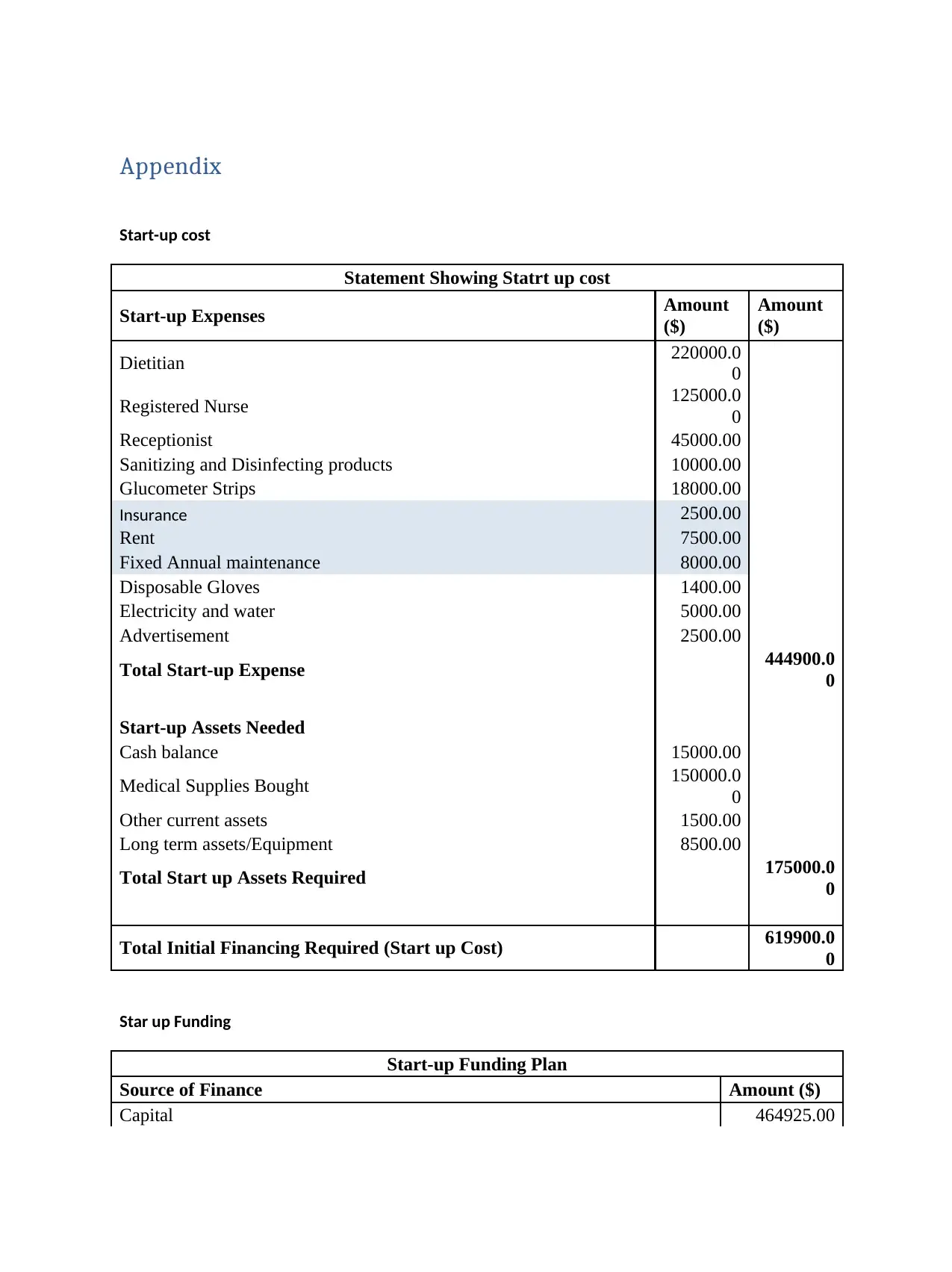

Appendix

Start-up cost

Statement Showing Statrt up cost

Start-up Expenses Amount

($)

Amount

($)

Dietitian 220000.0

0

Registered Nurse 125000.0

0

Receptionist 45000.00

Sanitizing and Disinfecting products 10000.00

Glucometer Strips 18000.00

Insurance 2500.00

Rent 7500.00

Fixed Annual maintenance 8000.00

Disposable Gloves 1400.00

Electricity and water 5000.00

Advertisement 2500.00

Total Start-up Expense 444900.0

0

Start-up Assets Needed

Cash balance 15000.00

Medical Supplies Bought 150000.0

0

Other current assets 1500.00

Long term assets/Equipment 8500.00

Total Start up Assets Required 175000.0

0

Total Initial Financing Required (Start up Cost) 619900.0

0

Star up Funding

Start-up Funding Plan

Source of Finance Amount ($)

Capital 464925.00

Start-up cost

Statement Showing Statrt up cost

Start-up Expenses Amount

($)

Amount

($)

Dietitian 220000.0

0

Registered Nurse 125000.0

0

Receptionist 45000.00

Sanitizing and Disinfecting products 10000.00

Glucometer Strips 18000.00

Insurance 2500.00

Rent 7500.00

Fixed Annual maintenance 8000.00

Disposable Gloves 1400.00

Electricity and water 5000.00

Advertisement 2500.00

Total Start-up Expense 444900.0

0

Start-up Assets Needed

Cash balance 15000.00

Medical Supplies Bought 150000.0

0

Other current assets 1500.00

Long term assets/Equipment 8500.00

Total Start up Assets Required 175000.0

0

Total Initial Financing Required (Start up Cost) 619900.0

0

Star up Funding

Start-up Funding Plan

Source of Finance Amount ($)

Capital 464925.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank Loans 154975.00

Total Investment 619900.00

Income Statement

Income Statement (All amounts in $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Income from Services

65720

0

72292

0

79521

2

87473

3 962207

Less:

Variable Cost

Dietitian

22000

0

24200

0

26620

0

29282

0 322102

Registered Nurse

12500

0

13750

0

15125

0

16637

5

183012.

5

Receptionist 45000 49500 54450 59895 65884.5

Sanitizing and Disinfecting products 10000 11000 12100 13310 14641

Glucometer Strips 18000 19800 21780 23958 26353.8

Disposable Gloves 2500 2750 3025 3327.5 3660.25

Electricity and water 7500 8250 9075 9982.5

10980.7

5

Advertisement 8000 8800 9680 10648 11712.8

Contribution

22120

0

24332

0

26765

2

29441

7 323859

Less:

Fixed Costs

Insurance 2500 2750 3025 3327.5 3660.25

Rent 7500 8250 9075 9982.5

10980.7

5

Fixed Annual maintenance 8000 8800 9680 10648 11712.8

Net Profit

20320

0

22352

0

24587

2

27045

9 297505

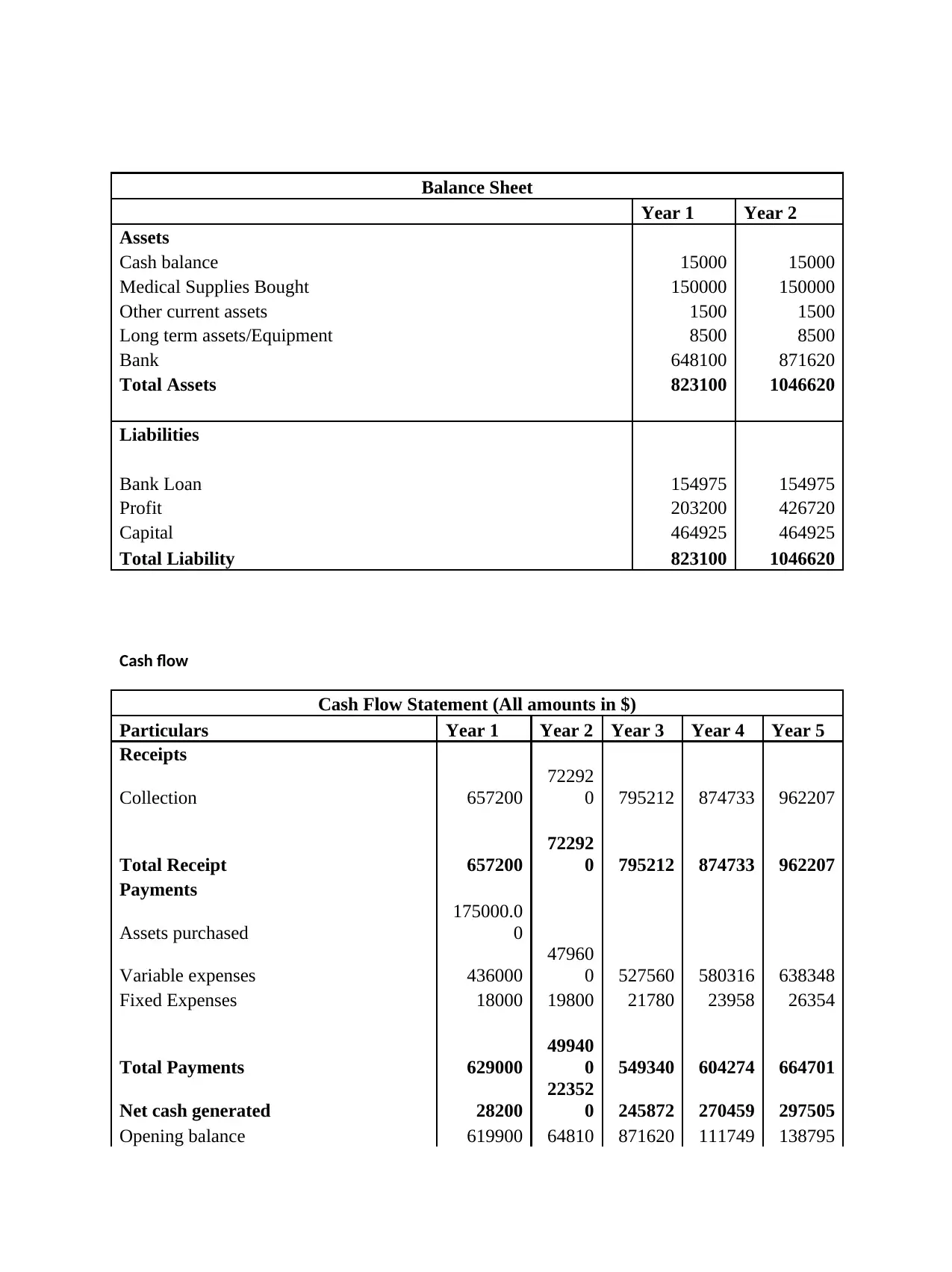

Balance sheet

Total Investment 619900.00

Income Statement

Income Statement (All amounts in $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Income from Services

65720

0

72292

0

79521

2

87473

3 962207

Less:

Variable Cost

Dietitian

22000

0

24200

0

26620

0

29282

0 322102

Registered Nurse

12500

0

13750

0

15125

0

16637

5

183012.

5

Receptionist 45000 49500 54450 59895 65884.5

Sanitizing and Disinfecting products 10000 11000 12100 13310 14641

Glucometer Strips 18000 19800 21780 23958 26353.8

Disposable Gloves 2500 2750 3025 3327.5 3660.25

Electricity and water 7500 8250 9075 9982.5

10980.7

5

Advertisement 8000 8800 9680 10648 11712.8

Contribution

22120

0

24332

0

26765

2

29441

7 323859

Less:

Fixed Costs

Insurance 2500 2750 3025 3327.5 3660.25

Rent 7500 8250 9075 9982.5

10980.7

5

Fixed Annual maintenance 8000 8800 9680 10648 11712.8

Net Profit

20320

0

22352

0

24587

2

27045

9 297505

Balance sheet

Balance Sheet

Year 1 Year 2

Assets

Cash balance 15000 15000

Medical Supplies Bought 150000 150000

Other current assets 1500 1500

Long term assets/Equipment 8500 8500

Bank 648100 871620

Total Assets 823100 1046620

Liabilities

Bank Loan 154975 154975

Profit 203200 426720

Capital 464925 464925

Total Liability 823100 1046620

Cash flow

Cash Flow Statement (All amounts in $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Receipts

Collection 657200

72292

0 795212 874733 962207

Total Receipt 657200

72292

0 795212 874733 962207

Payments

Assets purchased

175000.0

0

Variable expenses 436000

47960

0 527560 580316 638348

Fixed Expenses 18000 19800 21780 23958 26354

Total Payments 629000

49940

0 549340 604274 664701

Net cash generated 28200

22352

0 245872 270459 297505

Opening balance 619900 64810 871620 111749 138795

Year 1 Year 2

Assets

Cash balance 15000 15000

Medical Supplies Bought 150000 150000

Other current assets 1500 1500

Long term assets/Equipment 8500 8500

Bank 648100 871620

Total Assets 823100 1046620

Liabilities

Bank Loan 154975 154975

Profit 203200 426720

Capital 464925 464925

Total Liability 823100 1046620

Cash flow

Cash Flow Statement (All amounts in $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Receipts

Collection 657200

72292

0 795212 874733 962207

Total Receipt 657200

72292

0 795212 874733 962207

Payments

Assets purchased

175000.0

0

Variable expenses 436000

47960

0 527560 580316 638348

Fixed Expenses 18000 19800 21780 23958 26354

Total Payments 629000

49940

0 549340 604274 664701

Net cash generated 28200

22352

0 245872 270459 297505

Opening balance 619900 64810 871620 111749 138795

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0 2 1

Closing 648100

87162

0

111749

2

138795

1

168545

6

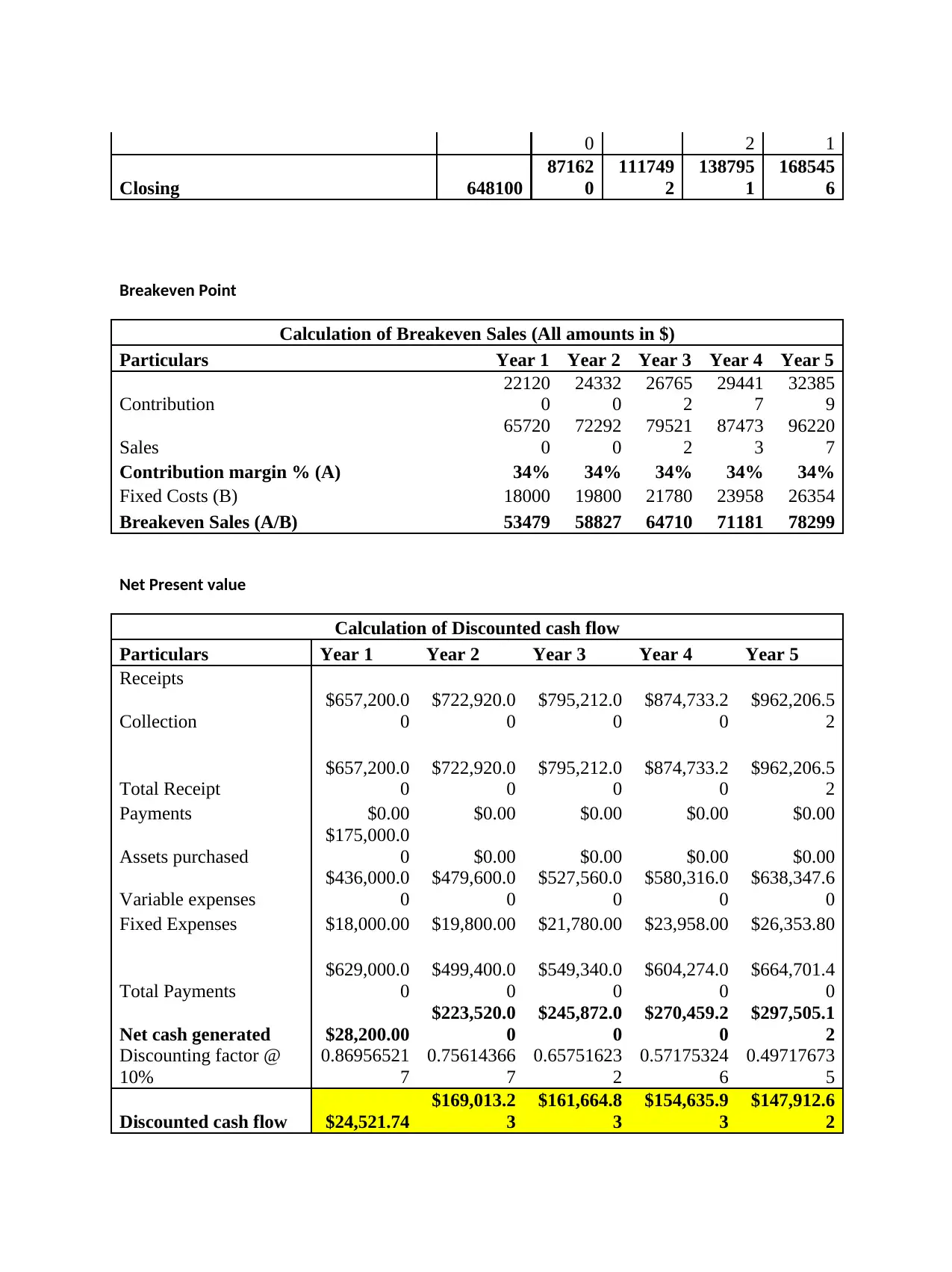

Breakeven Point

Calculation of Breakeven Sales (All amounts in $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Contribution

22120

0

24332

0

26765

2

29441

7

32385

9

Sales

65720

0

72292

0

79521

2

87473

3

96220

7

Contribution margin % (A) 34% 34% 34% 34% 34%

Fixed Costs (B) 18000 19800 21780 23958 26354

Breakeven Sales (A/B) 53479 58827 64710 71181 78299

Net Present value

Calculation of Discounted cash flow

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Receipts

Collection

$657,200.0

0

$722,920.0

0

$795,212.0

0

$874,733.2

0

$962,206.5

2

Total Receipt

$657,200.0

0

$722,920.0

0

$795,212.0

0

$874,733.2

0

$962,206.5

2

Payments $0.00 $0.00 $0.00 $0.00 $0.00

Assets purchased

$175,000.0

0 $0.00 $0.00 $0.00 $0.00

Variable expenses

$436,000.0

0

$479,600.0

0

$527,560.0

0

$580,316.0

0

$638,347.6

0

Fixed Expenses $18,000.00 $19,800.00 $21,780.00 $23,958.00 $26,353.80

Total Payments

$629,000.0

0

$499,400.0

0

$549,340.0

0

$604,274.0

0

$664,701.4

0

Net cash generated $28,200.00

$223,520.0

0

$245,872.0

0

$270,459.2

0

$297,505.1

2

Discounting factor @

10%

0.86956521

7

0.75614366

7

0.65751623

2

0.57175324

6

0.49717673

5

Discounted cash flow $24,521.74

$169,013.2

3

$161,664.8

3

$154,635.9

3

$147,912.6

2

Closing 648100

87162

0

111749

2

138795

1

168545

6

Breakeven Point

Calculation of Breakeven Sales (All amounts in $)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Contribution

22120

0

24332

0

26765

2

29441

7

32385

9

Sales

65720

0

72292

0

79521

2

87473

3

96220

7

Contribution margin % (A) 34% 34% 34% 34% 34%

Fixed Costs (B) 18000 19800 21780 23958 26354

Breakeven Sales (A/B) 53479 58827 64710 71181 78299

Net Present value

Calculation of Discounted cash flow

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Receipts

Collection

$657,200.0

0

$722,920.0

0

$795,212.0

0

$874,733.2

0

$962,206.5

2

Total Receipt

$657,200.0

0

$722,920.0

0

$795,212.0

0

$874,733.2

0

$962,206.5

2

Payments $0.00 $0.00 $0.00 $0.00 $0.00

Assets purchased

$175,000.0

0 $0.00 $0.00 $0.00 $0.00

Variable expenses

$436,000.0

0

$479,600.0

0

$527,560.0

0

$580,316.0

0

$638,347.6

0

Fixed Expenses $18,000.00 $19,800.00 $21,780.00 $23,958.00 $26,353.80

Total Payments

$629,000.0

0

$499,400.0

0

$549,340.0

0

$604,274.0

0

$664,701.4

0

Net cash generated $28,200.00

$223,520.0

0

$245,872.0

0

$270,459.2

0

$297,505.1

2

Discounting factor @

10%

0.86956521

7

0.75614366

7

0.65751623

2

0.57175324

6

0.49717673

5

Discounted cash flow $24,521.74

$169,013.2

3

$161,664.8

3

$154,635.9

3

$147,912.6

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

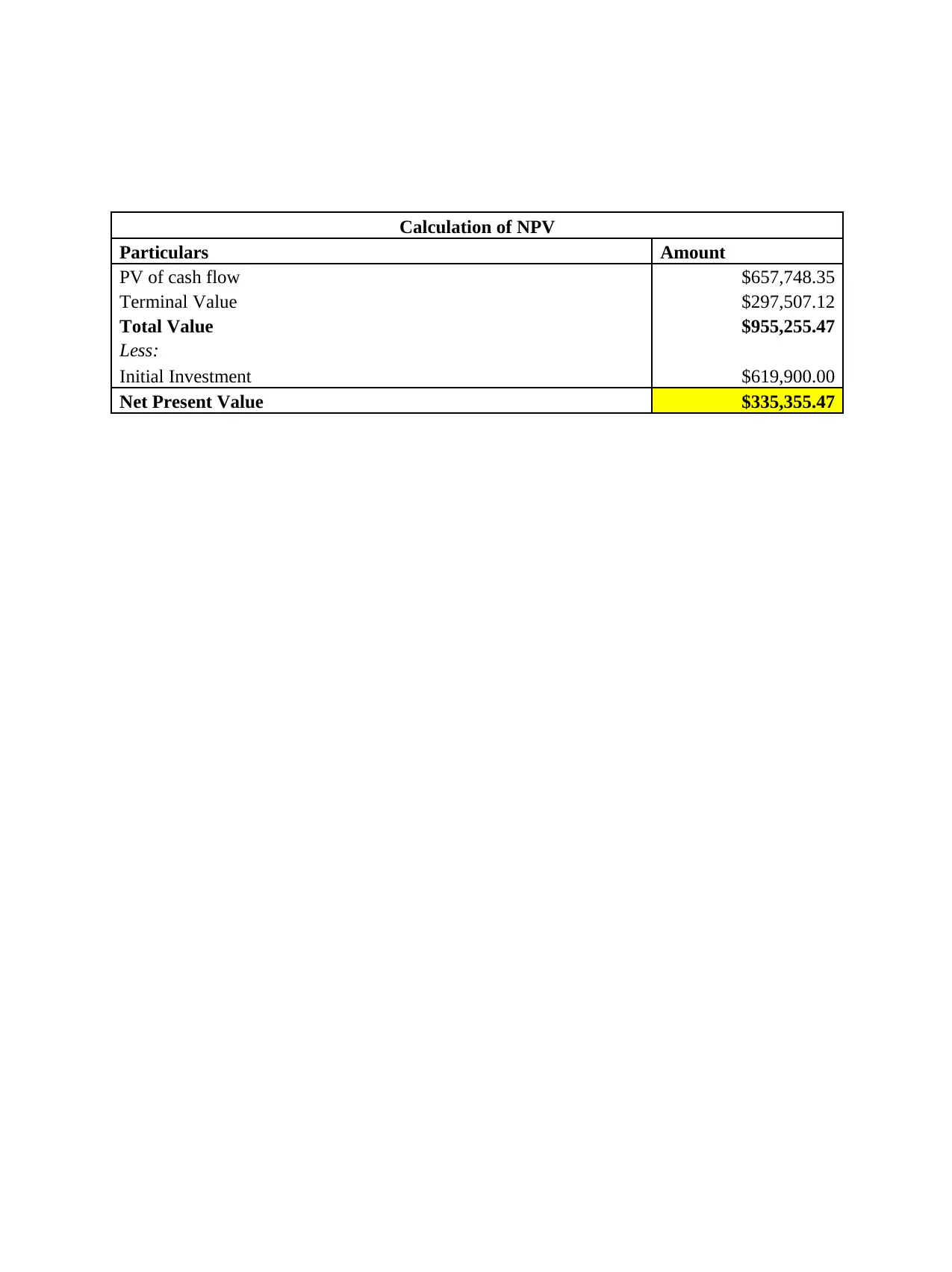

Calculation of NPV

Particulars Amount

PV of cash flow $657,748.35

Terminal Value $297,507.12

Total Value $955,255.47

Less:

Initial Investment $619,900.00

Net Present Value $335,355.47

Particulars Amount

PV of cash flow $657,748.35

Terminal Value $297,507.12

Total Value $955,255.47

Less:

Initial Investment $619,900.00

Net Present Value $335,355.47

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.