Financial Management: Decision-Making Techniques and Strategies

VerifiedAdded on 2023/01/13

|15

|4656

|40

Report

AI Summary

This report delves into the principles of financial management, focusing on decision-making processes within a business context. It begins by outlining various approaches and techniques contributing to effective decision-making, including formal and informal approaches, alongside tools like T-charts, Pareto analysis, and decision matrices. The report emphasizes the importance of stakeholder management, addressing conflicting objectives and exploring management accounting techniques for cost control and maximizing shareholder value. It further examines techniques for fraud detection and ethical decision-making, including auditing and corporate governance. Task 2 analyzes how financial data informs strategic and operational decisions, comparing and contrasting investment appraisal techniques to maximize ROI, and financial decision-making for long-term business sustainability, offering recommendations for improving financial sustainability through management accounting. The report uses Persimmon plc, a real estate company, as a case study throughout.

PRINCIPLE OF FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Approaches and techniques contributing to effective decision making. .....................................1

Stakeholders management and of conflicting objectives of different stakeholders ....................3

Management accounting techniques in cost control and maximising shareholder value............3

Techniques for fraud detection and ethical decision making. .....................................................4

Reflection.....................................................................................................................................5

TASK 2 ..........................................................................................................................................6

Financial data helping in making strategic and operational decisions. .......................................6

Comparing and contrasting investment appraisals techniques and its effectiveness in

maximising ROI. .........................................................................................................................6

Value of techniques used in financial decision-making..............................................................7

Financial decision making in long term sustainability of business. ............................................8

Recommendations in relation to the way in which management accounting could be used for

improving the financial sustainability .......................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Approaches and techniques contributing to effective decision making. .....................................1

Stakeholders management and of conflicting objectives of different stakeholders ....................3

Management accounting techniques in cost control and maximising shareholder value............3

Techniques for fraud detection and ethical decision making. .....................................................4

Reflection.....................................................................................................................................5

TASK 2 ..........................................................................................................................................6

Financial data helping in making strategic and operational decisions. .......................................6

Comparing and contrasting investment appraisals techniques and its effectiveness in

maximising ROI. .........................................................................................................................6

Value of techniques used in financial decision-making..............................................................7

Financial decision making in long term sustainability of business. ............................................8

Recommendations in relation to the way in which management accounting could be used for

improving the financial sustainability .......................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial management deals with management of financial resources in the best possible

manner. It refers to allocating the financial resources of company to the most productive

operations. Present study is about the financial decision-making and its importance for the

business enterprise. The research is based on Persimmon plc that is a real estate company. The

report will cover the decision making approaches, techniques and factors influencing. This will

also cover the stakeholder management and cost accounting for minimising the costs. Study

provides and understanding about information essential for strategic and operational decisions.

This covers the investment appraisal techniques in in decision-making and the financial decision

for long term sustainability of business enterprise.

TASK 1

Approaches and techniques contributing to effective decision making.

Formal Approach

It is the approach comprising of structures, systems and processes which helps

management in decision-making. In this approach step by step format is followed by

organisation for the purpose of making acceptable and viable decisions. The structure defines the

information that defines the alternatives. It is used by organisations for formalizing the

relationship among the staff and processes of company. The formal approach helps organisation

in establishing coordinated environment through effective decisions. Organisations can solve

different types of business problems using subjective approach of decision-making. The

approach is very useful for organisations to make decisions in organisation with big amount of

data and information and also they have to make repetitive decisions in the stable environment

(Hemmer and Labro,2019). It also helps company in accurate and efficient transmissions of

decisions in the business environment. It is highly used approach for planning , allocating the

resources and for setting targets. The advantage of the approach is that it helps in effective

collaboration and organising the structure of business activities.

Informal Approach

This could be defined as approach consisting of unwritten rules, networks and the

relationship building for decision making purposes. There should be a strong relationship

between the senior and lower level management for getting correct and reliable data and

1

Financial management deals with management of financial resources in the best possible

manner. It refers to allocating the financial resources of company to the most productive

operations. Present study is about the financial decision-making and its importance for the

business enterprise. The research is based on Persimmon plc that is a real estate company. The

report will cover the decision making approaches, techniques and factors influencing. This will

also cover the stakeholder management and cost accounting for minimising the costs. Study

provides and understanding about information essential for strategic and operational decisions.

This covers the investment appraisal techniques in in decision-making and the financial decision

for long term sustainability of business enterprise.

TASK 1

Approaches and techniques contributing to effective decision making.

Formal Approach

It is the approach comprising of structures, systems and processes which helps

management in decision-making. In this approach step by step format is followed by

organisation for the purpose of making acceptable and viable decisions. The structure defines the

information that defines the alternatives. It is used by organisations for formalizing the

relationship among the staff and processes of company. The formal approach helps organisation

in establishing coordinated environment through effective decisions. Organisations can solve

different types of business problems using subjective approach of decision-making. The

approach is very useful for organisations to make decisions in organisation with big amount of

data and information and also they have to make repetitive decisions in the stable environment

(Hemmer and Labro,2019). It also helps company in accurate and efficient transmissions of

decisions in the business environment. It is highly used approach for planning , allocating the

resources and for setting targets. The advantage of the approach is that it helps in effective

collaboration and organising the structure of business activities.

Informal Approach

This could be defined as approach consisting of unwritten rules, networks and the

relationship building for decision making purposes. There should be a strong relationship

between the senior and lower level management for getting correct and reliable data and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

informations from all the departments on which the decisions of management will be based. This

approach requires company to consider the rules and regulation, values, beliefs and the history of

organisation in its decisions. The informal approach of decision making is not based on a set

criteria but on considering the results that would be most beneficial for company (Moreno and

et.al., 2019).

Techniques used in Decision-making.

Decisions are taken at various level of the organisation. These decisions define the future

performance of company. The accuracy of the decisions is dependent on the techniques use by

organisation for responding them.

T-Chart : This chart is used for assessing the positive and negative points of a decision. This

enables company in taking decisions with maximum positive points.

Pareto Analysis : The technique is useful in case of multiple options are available with the

company for making the decisions. In this technique options are ranked and the one with highest

rank is chosen.

Decision matrix : This is used for evaluating options to make decisions (Devi and Devaki,

2019). It places option in 1st column and factors affecting in 1st row. Options are than scored and

weighed on the basis of importance.

Factor contributing in decision-making.

Nature of business

It is the major factor to be considered by the organisation in making decisions. The nature

of business defined the viability of choices available to company. For instance manufacturing

concerns decision are taken considering their production capacity.

Capital Structure

This refers to sources of funds available to company. The business is available with

enough funds or not for making any decisions is important.

Economic State

The economic conditions have great influence over decisions to be taken. The managers

of company take decision analysing the economic conditions of market. The market and

consumer behaviours play an important role in any organisation (Güler, Mukul and

Büyüközkan, 2019).

2

approach requires company to consider the rules and regulation, values, beliefs and the history of

organisation in its decisions. The informal approach of decision making is not based on a set

criteria but on considering the results that would be most beneficial for company (Moreno and

et.al., 2019).

Techniques used in Decision-making.

Decisions are taken at various level of the organisation. These decisions define the future

performance of company. The accuracy of the decisions is dependent on the techniques use by

organisation for responding them.

T-Chart : This chart is used for assessing the positive and negative points of a decision. This

enables company in taking decisions with maximum positive points.

Pareto Analysis : The technique is useful in case of multiple options are available with the

company for making the decisions. In this technique options are ranked and the one with highest

rank is chosen.

Decision matrix : This is used for evaluating options to make decisions (Devi and Devaki,

2019). It places option in 1st column and factors affecting in 1st row. Options are than scored and

weighed on the basis of importance.

Factor contributing in decision-making.

Nature of business

It is the major factor to be considered by the organisation in making decisions. The nature

of business defined the viability of choices available to company. For instance manufacturing

concerns decision are taken considering their production capacity.

Capital Structure

This refers to sources of funds available to company. The business is available with

enough funds or not for making any decisions is important.

Economic State

The economic conditions have great influence over decisions to be taken. The managers

of company take decision analysing the economic conditions of market. The market and

consumer behaviours play an important role in any organisation (Güler, Mukul and

Büyüközkan, 2019).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stakeholders management and of conflicting objectives of different stakeholders

Stakeholders refers to the parties having interest in the company and it operations. They

are the individuals or group having interests in business portfolios, projects and projects as they

are also affected with their decisions. Every business enterprise is having stakeholders whose

interest are required to be considered by organisation. They play an important role for the

business in decision-making. The business organisation is concerned with making decisions

related to planning, analysing, interpreting and implementing the actions related to stakeholder

management (Cheraghi, Choobchian and Abbasi, 2019). It is concerned with engaging people by

considering their interests for maximising the stakeholders value.

Managing conflicting stakeholder objectives

There is a great importance of managing the interests of different stakeholder. These

stakeholders are concerned with maximising their values. The suppliers of the company are

concerned with the payments schedules for their supplies, customers are concerned with

receiving high quality goods at low costs. The shareholders of company are concerned with

receiving high returns over their investments maximising their wealth. Decisions are taken by

management considering concerns of all the stakeholders. Conflicts arise when one is given

priority by the business over the other. The policies and procedures adopted by the management

should be for the benefit of all stakeholders. This could be better managed by identifying the

different stakeholders and their interests.

Management accounting techniques in cost control and maximising shareholder value.

Management accounting is concerned with the management of business resources and

cost control strategies. It is of great importance for company in achieving its defined goals and

objectives. Management accountants perform their roles by ensuring that the resources are used

in best possible way and processes are being run the most cost effective manner (Garcia‐Castro

and Francoeur, 2016).

Management accounting cost control techniques

Cost accounting

This is concerned with analysing the cost associated with the manufacturing of each

product. It provides important information about the variable and fixed costs incurred by

organisation. The cost accounting uses various concepts and tools for minimising the costs of

3

Stakeholders refers to the parties having interest in the company and it operations. They

are the individuals or group having interests in business portfolios, projects and projects as they

are also affected with their decisions. Every business enterprise is having stakeholders whose

interest are required to be considered by organisation. They play an important role for the

business in decision-making. The business organisation is concerned with making decisions

related to planning, analysing, interpreting and implementing the actions related to stakeholder

management (Cheraghi, Choobchian and Abbasi, 2019). It is concerned with engaging people by

considering their interests for maximising the stakeholders value.

Managing conflicting stakeholder objectives

There is a great importance of managing the interests of different stakeholder. These

stakeholders are concerned with maximising their values. The suppliers of the company are

concerned with the payments schedules for their supplies, customers are concerned with

receiving high quality goods at low costs. The shareholders of company are concerned with

receiving high returns over their investments maximising their wealth. Decisions are taken by

management considering concerns of all the stakeholders. Conflicts arise when one is given

priority by the business over the other. The policies and procedures adopted by the management

should be for the benefit of all stakeholders. This could be better managed by identifying the

different stakeholders and their interests.

Management accounting techniques in cost control and maximising shareholder value.

Management accounting is concerned with the management of business resources and

cost control strategies. It is of great importance for company in achieving its defined goals and

objectives. Management accountants perform their roles by ensuring that the resources are used

in best possible way and processes are being run the most cost effective manner (Garcia‐Castro

and Francoeur, 2016).

Management accounting cost control techniques

Cost accounting

This is concerned with analysing the cost associated with the manufacturing of each

product. It provides important information about the variable and fixed costs incurred by

organisation. The cost accounting uses various concepts and tools for minimising the costs of

3

production. Cost accounting involves break-even analysis that helps company in identifying the

required level of outputs for covering its production costs.

Financial planning

The objective of company is to achieve maximum returns reducing the costs and its

operations. Financial planning helps business in having a defined business plans for the future

activities. This provides company a structured path to follow. Majority of the costs control issue

arises due to inefficient planning of management.

Budgetary Control

It is an effective tool used by organisation in decision making. It involves making

forecast about the future income and expenditures of company. This requires company to make

in depth analysis of the market conditions, inflations and all the other factors for making budgets.

Company make comparison between the actual and budgeted outputs (Epstein and et.al., 2017.).

On the basis of this company identifies the reasons behind variations and take corrective

measures for having the cost under control.

Margin analysis

This refers to measuring the the break-even points so that company can have an optimum

sales mix with minimal costs. It is an essential technique of management accounting for keeping

the costs under control. Company adopt effective strategies and policies for reducing the costs of

production.

Techniques for fraud detection and ethical decision making.

Companies are nowadays having serious considerations for detecting the frauds carried

out within their organisation. Businesses are using different fraud detection techniques such as

Auditing

This refers to inspection and checking of all the business transactions carried within

organisation. Majority of the frauds are incurred in the financial transactions. Auditing is

conducted by professionals of all the financials. This enables them to identify any frauds being

conducted so that they can be identified at their initial stage. Any errors or misstatements in the

financial statements, fake invoices and irregular transactions are inspected by the auditors for

preventing any defaults or frauds.

Corporate Governance

4

required level of outputs for covering its production costs.

Financial planning

The objective of company is to achieve maximum returns reducing the costs and its

operations. Financial planning helps business in having a defined business plans for the future

activities. This provides company a structured path to follow. Majority of the costs control issue

arises due to inefficient planning of management.

Budgetary Control

It is an effective tool used by organisation in decision making. It involves making

forecast about the future income and expenditures of company. This requires company to make

in depth analysis of the market conditions, inflations and all the other factors for making budgets.

Company make comparison between the actual and budgeted outputs (Epstein and et.al., 2017.).

On the basis of this company identifies the reasons behind variations and take corrective

measures for having the cost under control.

Margin analysis

This refers to measuring the the break-even points so that company can have an optimum

sales mix with minimal costs. It is an essential technique of management accounting for keeping

the costs under control. Company adopt effective strategies and policies for reducing the costs of

production.

Techniques for fraud detection and ethical decision making.

Companies are nowadays having serious considerations for detecting the frauds carried

out within their organisation. Businesses are using different fraud detection techniques such as

Auditing

This refers to inspection and checking of all the business transactions carried within

organisation. Majority of the frauds are incurred in the financial transactions. Auditing is

conducted by professionals of all the financials. This enables them to identify any frauds being

conducted so that they can be identified at their initial stage. Any errors or misstatements in the

financial statements, fake invoices and irregular transactions are inspected by the auditors for

preventing any defaults or frauds.

Corporate Governance

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The corporate governance refers to establishing proper control and monitoring procedures

of all the business transactions. This involves keeping adequate checks in the enterprise for

preventing the frauds. Company should have checking of all the inventory moving in and out of

the organisations. The material purchase orders, consumption of materials in the given process,

wastages and like other activities carried within business (Marota and et.al., 2017). All the

invoices and other transactions should be carried out by employees with proper authority and

inspection by the managers and seniors executives of business.

Ethical Decision-making

It refers to practising ethics in decisions taken. It deals with the establishment of ethical

values in the business. Decisions should not be taken considering the interest of single party.

They should not be taken to deceive and person or party. Operations of the business should be

carried out using ethical standards.

Reflection

The above study was an interesting part as it deals with financial sector. This study has

helped in getting the understanding and knowledge about the approaches of the business

decision-making. Decisions decide the future operations of business. I have learned that the

major business decision are taken considering the decisions techniques like t-chart, pareto

analysis, decision matrix so that they are much accurate and reliable. Also there are other factors

to be considered that are influencing the business decisions like economic factor, nature of

business and like other. The business not runs all alone it is associated with different parties

known as its stakeholders. They are concerned with every business decisions that have effect

over them. Organisations are required to ensure that the business decisions are not depriving the

interest of any one stakeholder as it will be giving rise to conflicts between the stakeholders.

Further it has also provided an understanding about the different management accounting

techniques used for controlling the costs and reducing them to minimum. Companies are using

different steps like auditing and strong governance for fraud detection and following ethical

approach for decision making.

5

of all the business transactions. This involves keeping adequate checks in the enterprise for

preventing the frauds. Company should have checking of all the inventory moving in and out of

the organisations. The material purchase orders, consumption of materials in the given process,

wastages and like other activities carried within business (Marota and et.al., 2017). All the

invoices and other transactions should be carried out by employees with proper authority and

inspection by the managers and seniors executives of business.

Ethical Decision-making

It refers to practising ethics in decisions taken. It deals with the establishment of ethical

values in the business. Decisions should not be taken considering the interest of single party.

They should not be taken to deceive and person or party. Operations of the business should be

carried out using ethical standards.

Reflection

The above study was an interesting part as it deals with financial sector. This study has

helped in getting the understanding and knowledge about the approaches of the business

decision-making. Decisions decide the future operations of business. I have learned that the

major business decision are taken considering the decisions techniques like t-chart, pareto

analysis, decision matrix so that they are much accurate and reliable. Also there are other factors

to be considered that are influencing the business decisions like economic factor, nature of

business and like other. The business not runs all alone it is associated with different parties

known as its stakeholders. They are concerned with every business decisions that have effect

over them. Organisations are required to ensure that the business decisions are not depriving the

interest of any one stakeholder as it will be giving rise to conflicts between the stakeholders.

Further it has also provided an understanding about the different management accounting

techniques used for controlling the costs and reducing them to minimum. Companies are using

different steps like auditing and strong governance for fraud detection and following ethical

approach for decision making.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Financial data helping in making strategic and operational decisions.

Annual reports give both financial and non financial information relevant for the business

to make decisions. The information helps in assessing the health and position in the market.

Financial information consists of quantitative figures stated in financial statement like income

statement, balance sheet and cash flow statements. They provide important information related to

efficiency of business in carrying out its operations using the existing resources. This provide the

management with information about whether the required returns have been earned by the

company or not. The information is used by organisation for making informed strategic

decisions for improving the productivity and efficiency.

Non financial information includes the business structures, policies and procedures,

corporate governance, political and economic influence. These factors are often ignore by the

viewers of financial statements but many of times affect the business operations. There are

organisations who are performing well but are not able to generate adequate returns (D'Onza,

Greco and Allegrini, 2016). The reports provide the information about the corporate governance,

leadership of business. The CSR practices being followed by organisations. This provides

information for making decision for improving the strategies and operational performance.

Comparing and contrasting investment appraisals techniques and its effectiveness in maximising

ROI.

A business decision-making process involves considering all the negative and positive

aspects before taking decisions. Business takes various financial decisions that includes

investments of huge business funds. These decisions are taken considering various investment

appraisal techniques like NPV, ARR and payback period. They are also known as capital

budgeting techniques for making capital decisions.,

Net Present Value

This is an investment appraisal techniques used in assessing the feasibility of projects that

company is considering to adopt. This method involves measuring the present value of cash

flows generated by the project. Projects with positive NPV are considered as profitable by the

business. This enables company to identify whether the future cash flows generated by project

will be enough for earning profits after recovering its investments costs. The method is an easy

6

Financial data helping in making strategic and operational decisions.

Annual reports give both financial and non financial information relevant for the business

to make decisions. The information helps in assessing the health and position in the market.

Financial information consists of quantitative figures stated in financial statement like income

statement, balance sheet and cash flow statements. They provide important information related to

efficiency of business in carrying out its operations using the existing resources. This provide the

management with information about whether the required returns have been earned by the

company or not. The information is used by organisation for making informed strategic

decisions for improving the productivity and efficiency.

Non financial information includes the business structures, policies and procedures,

corporate governance, political and economic influence. These factors are often ignore by the

viewers of financial statements but many of times affect the business operations. There are

organisations who are performing well but are not able to generate adequate returns (D'Onza,

Greco and Allegrini, 2016). The reports provide the information about the corporate governance,

leadership of business. The CSR practices being followed by organisations. This provides

information for making decision for improving the strategies and operational performance.

Comparing and contrasting investment appraisals techniques and its effectiveness in maximising

ROI.

A business decision-making process involves considering all the negative and positive

aspects before taking decisions. Business takes various financial decisions that includes

investments of huge business funds. These decisions are taken considering various investment

appraisal techniques like NPV, ARR and payback period. They are also known as capital

budgeting techniques for making capital decisions.,

Net Present Value

This is an investment appraisal techniques used in assessing the feasibility of projects that

company is considering to adopt. This method involves measuring the present value of cash

flows generated by the project. Projects with positive NPV are considered as profitable by the

business. This enables company to identify whether the future cash flows generated by project

will be enough for earning profits after recovering its investments costs. The method is an easy

6

and simple to understand and is used by experts for making choices between the projects. This

investment technique involves time value of money.

Accounting Rate of Return

It refers to the rate of return that will be generated by the business from the investments

or projects it is proposing to make. Accounting rate of return considers the accounting returns

that are not considered by any other investment technique. Investments should be generating

adequate rate of returns so that the cost of investments could be recovered by the project. This

enables company in identifying whether the project will be generating enough returns or not

(Hirshleifer, Jian and Zhang, 2018). The method is a capital budgeting technique used by

experts for making comparisons between the projects. This identifies return in percentage terms

from the proposed investments.

Payback Period

It is also an investment appraisal technique used by organisation to identify the time

taken by the investments to recover its costs. The companies should make investments if it is

able to recover its cost. This enables company in identifying the time after which company will

start making profits. This approach says, shorter the payback period more profitable is the

project. Between the two projects on with shorter payback should be selected. The disadvantage

of using this technique is that it do not consider time value of money in its calculations.

Value of techniques used in financial decision-making.

There are various techniques used by management of enterprise for making decisions. It

ensures that the business organisations are having effective control procedures and effective

strategies for the long term success of the business organisation. These techniques include cash

flow statements, balance sheet, income statements and break even analysis.

Income Statement

These are the statements prepared by the organisation for assessing the profitability of

business. This statement reflects all the incomes and expenditures incurred by the organisation

during the year such as revenues, cost of sales, operational costs, finance costa and other income

earned by the company. This is used for assessing whether the the required returns are generated

by the company or not. This also provides the efficiency in carrying out the business

7

investment technique involves time value of money.

Accounting Rate of Return

It refers to the rate of return that will be generated by the business from the investments

or projects it is proposing to make. Accounting rate of return considers the accounting returns

that are not considered by any other investment technique. Investments should be generating

adequate rate of returns so that the cost of investments could be recovered by the project. This

enables company in identifying whether the project will be generating enough returns or not

(Hirshleifer, Jian and Zhang, 2018). The method is a capital budgeting technique used by

experts for making comparisons between the projects. This identifies return in percentage terms

from the proposed investments.

Payback Period

It is also an investment appraisal technique used by organisation to identify the time

taken by the investments to recover its costs. The companies should make investments if it is

able to recover its cost. This enables company in identifying the time after which company will

start making profits. This approach says, shorter the payback period more profitable is the

project. Between the two projects on with shorter payback should be selected. The disadvantage

of using this technique is that it do not consider time value of money in its calculations.

Value of techniques used in financial decision-making.

There are various techniques used by management of enterprise for making decisions. It

ensures that the business organisations are having effective control procedures and effective

strategies for the long term success of the business organisation. These techniques include cash

flow statements, balance sheet, income statements and break even analysis.

Income Statement

These are the statements prepared by the organisation for assessing the profitability of

business. This statement reflects all the incomes and expenditures incurred by the organisation

during the year such as revenues, cost of sales, operational costs, finance costa and other income

earned by the company. This is used for assessing whether the the required returns are generated

by the company or not. This also provides the efficiency in carrying out the business

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

transactions so that the strategies and policies of company can be modified (Lu, Won and Cheng,

2016).

Balance sheet

It provides the details about the assets and liabilities of company. This shows the capital

structure being followed by the organisations for keeping its costs minimum. It provides the

business about the short and long term obligations and its investments. The statements is used for

assessing the over all health of the business enterprise.

Cash flow statements

The cash flow statements are the statement represents the inflow and outflow of cash in

business. The cash flow statements covers operating activities, financing activities and the

investing activities. Using this statements company can identify the flow of cash in different

activities. It could identify the areas that are unproductive so that the flow of cash towards them

could be stopped and focus could be given over productive areas (Stewart, and et.al., 2018).

Break-even Analysis

This is a technique used by the management in identifying the level of sales required for

covering its production costs. This enables company in identify the point where its cost and

revenues are equal. It helps company in deciding its marketing strategies and production outputs.

Financial decision making in long term sustainability of business.

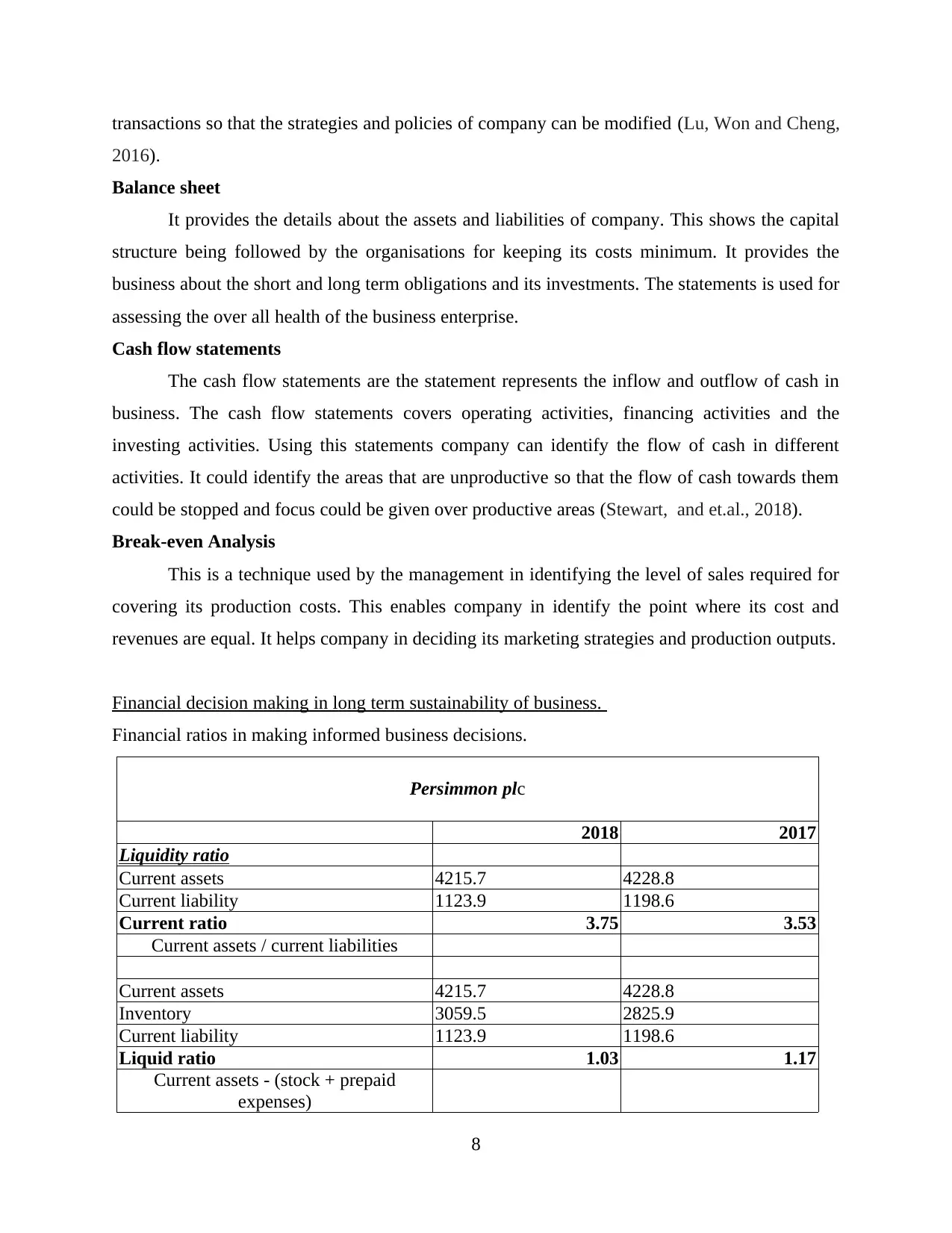

Financial ratios in making informed business decisions.

Persimmon plc

2018 2017

Liquidity ratio

Current assets 4215.7 4228.8

Current liability 1123.9 1198.6

Current ratio 3.75 3.53

Current assets / current liabilities

Current assets 4215.7 4228.8

Inventory 3059.5 2825.9

Current liability 1123.9 1198.6

Liquid ratio 1.03 1.17

Current assets - (stock + prepaid

expenses)

8

2016).

Balance sheet

It provides the details about the assets and liabilities of company. This shows the capital

structure being followed by the organisations for keeping its costs minimum. It provides the

business about the short and long term obligations and its investments. The statements is used for

assessing the over all health of the business enterprise.

Cash flow statements

The cash flow statements are the statement represents the inflow and outflow of cash in

business. The cash flow statements covers operating activities, financing activities and the

investing activities. Using this statements company can identify the flow of cash in different

activities. It could identify the areas that are unproductive so that the flow of cash towards them

could be stopped and focus could be given over productive areas (Stewart, and et.al., 2018).

Break-even Analysis

This is a technique used by the management in identifying the level of sales required for

covering its production costs. This enables company in identify the point where its cost and

revenues are equal. It helps company in deciding its marketing strategies and production outputs.

Financial decision making in long term sustainability of business.

Financial ratios in making informed business decisions.

Persimmon plc

2018 2017

Liquidity ratio

Current assets 4215.7 4228.8

Current liability 1123.9 1198.6

Current ratio 3.75 3.53

Current assets / current liabilities

Current assets 4215.7 4228.8

Inventory 3059.5 2825.9

Current liability 1123.9 1198.6

Liquid ratio 1.03 1.17

Current assets - (stock + prepaid

expenses)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

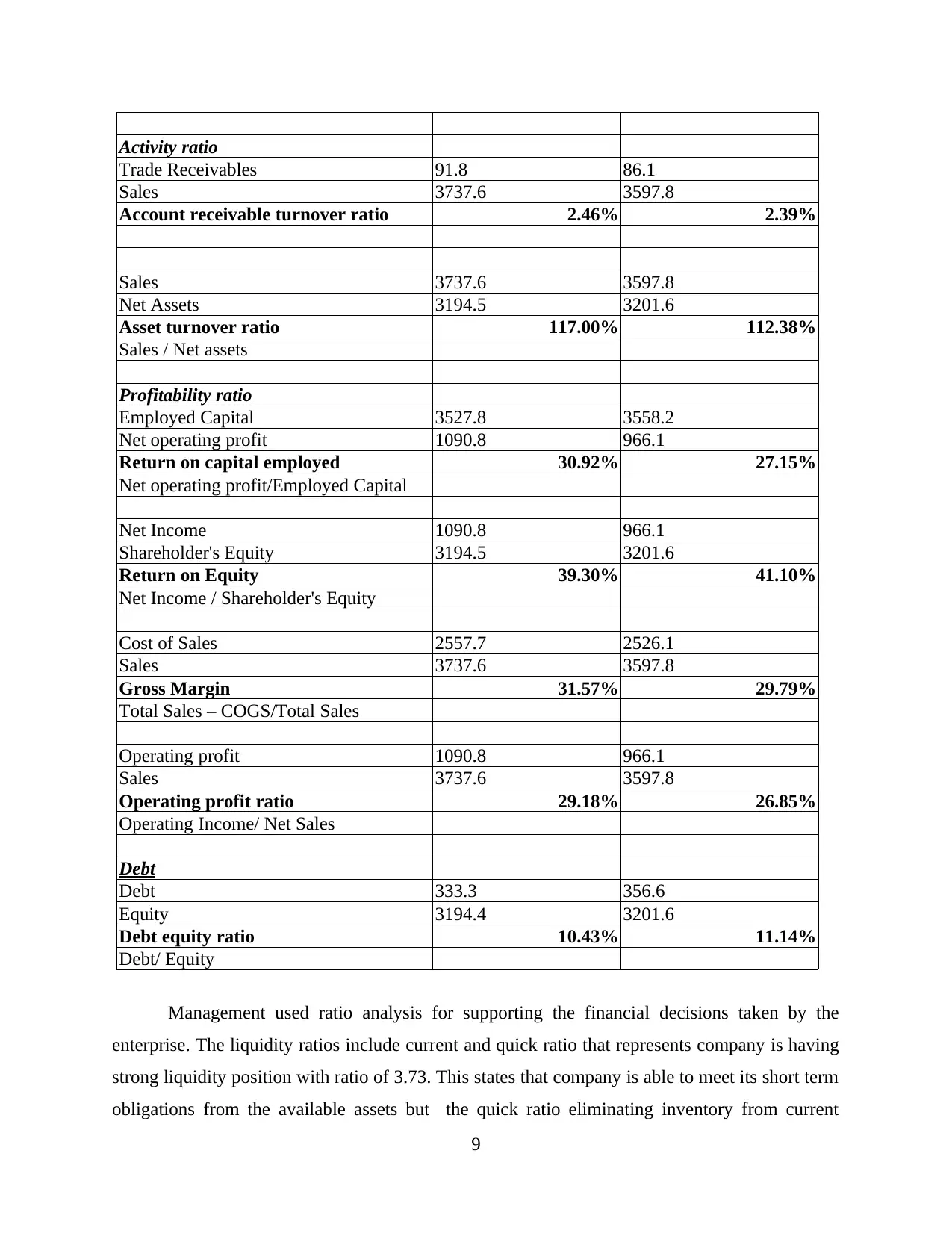

Activity ratio

Trade Receivables 91.8 86.1

Sales 3737.6 3597.8

Account receivable turnover ratio 2.46% 2.39%

Sales 3737.6 3597.8

Net Assets 3194.5 3201.6

Asset turnover ratio 117.00% 112.38%

Sales / Net assets

Profitability ratio

Employed Capital 3527.8 3558.2

Net operating profit 1090.8 966.1

Return on capital employed 30.92% 27.15%

Net operating profit/Employed Capital

Net Income 1090.8 966.1

Shareholder's Equity 3194.5 3201.6

Return on Equity 39.30% 41.10%

Net Income / Shareholder's Equity

Cost of Sales 2557.7 2526.1

Sales 3737.6 3597.8

Gross Margin 31.57% 29.79%

Total Sales – COGS/Total Sales

Operating profit 1090.8 966.1

Sales 3737.6 3597.8

Operating profit ratio 29.18% 26.85%

Operating Income/ Net Sales

Debt

Debt 333.3 356.6

Equity 3194.4 3201.6

Debt equity ratio 10.43% 11.14%

Debt/ Equity

Management used ratio analysis for supporting the financial decisions taken by the

enterprise. The liquidity ratios include current and quick ratio that represents company is having

strong liquidity position with ratio of 3.73. This states that company is able to meet its short term

obligations from the available assets but the quick ratio eliminating inventory from current

9

Trade Receivables 91.8 86.1

Sales 3737.6 3597.8

Account receivable turnover ratio 2.46% 2.39%

Sales 3737.6 3597.8

Net Assets 3194.5 3201.6

Asset turnover ratio 117.00% 112.38%

Sales / Net assets

Profitability ratio

Employed Capital 3527.8 3558.2

Net operating profit 1090.8 966.1

Return on capital employed 30.92% 27.15%

Net operating profit/Employed Capital

Net Income 1090.8 966.1

Shareholder's Equity 3194.5 3201.6

Return on Equity 39.30% 41.10%

Net Income / Shareholder's Equity

Cost of Sales 2557.7 2526.1

Sales 3737.6 3597.8

Gross Margin 31.57% 29.79%

Total Sales – COGS/Total Sales

Operating profit 1090.8 966.1

Sales 3737.6 3597.8

Operating profit ratio 29.18% 26.85%

Operating Income/ Net Sales

Debt

Debt 333.3 356.6

Equity 3194.4 3201.6

Debt equity ratio 10.43% 11.14%

Debt/ Equity

Management used ratio analysis for supporting the financial decisions taken by the

enterprise. The liquidity ratios include current and quick ratio that represents company is having

strong liquidity position with ratio of 3.73. This states that company is able to meet its short term

obligations from the available assets but the quick ratio eliminating inventory from current

9

assets require company to take steps for the concerns related with liquidity. The Liquidity

position of company should be strong for long term sustainability.

Return on capital employed and return over equity are the investor profitability ratios

used for assessing the returns generated during the year. Company is having ROC of 30.92%

and ROE of 39.30%. The returns are high this presents that company is making efficient use of

its resources that is essential for attracting new investors and long term sustainability of business.

Gross profit and operating profit refers to the returns generated from the business. It

involves taking adequate decisions related with the business for increasing its revenues and

having effective control over the expenditures of business (D'Onza, Greco and Allegrini, 2016).

Cost control measures are essential for the long term success of organisation.

Solvency ratio or debt equity ratio is used for assessing the capital structure and financial

risks of company. They should take decisions regarding the capital analysing the current debt

structure of company. Current debt of company is 10%. Company should not raise more debts as

it will be increasing its finance costs.

Recommendations in relation to the way in which management accounting could be used for

improving the financial sustainability

There are various management accounting systems or tools that helps an organization in

attaining and improving the financial sustainability within the business that are as follows-

Organisation should make use of activity based costing tool that helps in ascertaining an

amount of the total funds and the resources allocated and dedicated to specific project or

the proposal. This in turn improves financial sustainability in the company.

An enterprise should adopt balanced scorecard technique as the model for evaluating

performance of the business which balances a measures of the financial performance,

internal operations, innovations and learning (Schaltegger, 2017). It helps the company

in viewing four major perspectives of the business that involves financial, customers,

growth and internal processes. These perspectives plays a crucial role in context of

increasing sustainability and the performance of the company.

Benchmarking is the other main MA technique that should be adopted by the firm for the

purpose of attaining suitable standards or the practice and thus establishing an attainable

standards through examining both external and an internal information. It might facilitate

10

position of company should be strong for long term sustainability.

Return on capital employed and return over equity are the investor profitability ratios

used for assessing the returns generated during the year. Company is having ROC of 30.92%

and ROE of 39.30%. The returns are high this presents that company is making efficient use of

its resources that is essential for attracting new investors and long term sustainability of business.

Gross profit and operating profit refers to the returns generated from the business. It

involves taking adequate decisions related with the business for increasing its revenues and

having effective control over the expenditures of business (D'Onza, Greco and Allegrini, 2016).

Cost control measures are essential for the long term success of organisation.

Solvency ratio or debt equity ratio is used for assessing the capital structure and financial

risks of company. They should take decisions regarding the capital analysing the current debt

structure of company. Current debt of company is 10%. Company should not raise more debts as

it will be increasing its finance costs.

Recommendations in relation to the way in which management accounting could be used for

improving the financial sustainability

There are various management accounting systems or tools that helps an organization in

attaining and improving the financial sustainability within the business that are as follows-

Organisation should make use of activity based costing tool that helps in ascertaining an

amount of the total funds and the resources allocated and dedicated to specific project or

the proposal. This in turn improves financial sustainability in the company.

An enterprise should adopt balanced scorecard technique as the model for evaluating

performance of the business which balances a measures of the financial performance,

internal operations, innovations and learning (Schaltegger, 2017). It helps the company

in viewing four major perspectives of the business that involves financial, customers,

growth and internal processes. These perspectives plays a crucial role in context of

increasing sustainability and the performance of the company.

Benchmarking is the other main MA technique that should be adopted by the firm for the

purpose of attaining suitable standards or the practice and thus establishing an attainable

standards through examining both external and an internal information. It might facilitate

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.