Principles and Practice of Financial Accounting Assignment Solution

VerifiedAdded on 2023/01/07

|11

|1676

|63

Homework Assignment

AI Summary

This document provides a complete solution to a financial accounting assignment. The solution includes a statement of comprehensive income, a statement of changes in equity, and a statement of financial position. It also includes working notes detailing the calculations. The assignment covers the purpose of accounting standards, ratio analysis for two companies (Ruislip plc and Hayes plc), and the limitations of ratio analysis. Furthermore, the solution distinguishes between finance and operating leases, explains factors indicating a finance lease, and discusses disclosure requirements for lessors and presentation/disclosure requirements for lessees related to both lease types. The assignment offers a detailed analysis of financial accounting principles and practices.

Principles and Practice of

Financial Accounting

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section A

Question 1

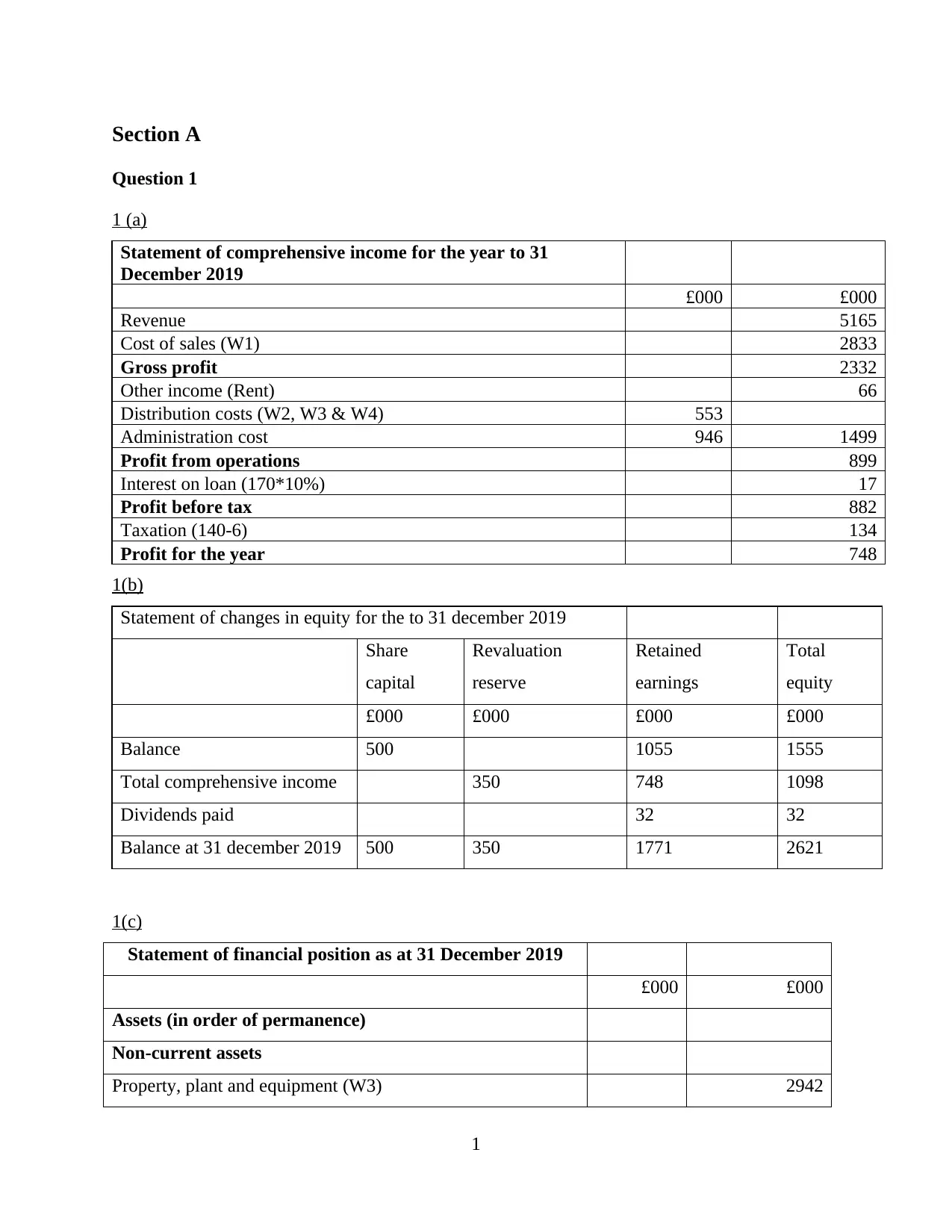

1 (a)

Statement of comprehensive income for the year to 31

December 2019

£000 £000

Revenue 5165

Cost of sales (W1) 2833

Gross profit 2332

Other income (Rent) 66

Distribution costs (W2, W3 & W4) 553

Administration cost 946 1499

Profit from operations 899

Interest on loan (170*10%) 17

Profit before tax 882

Taxation (140-6) 134

Profit for the year 748

1(b)

Statement of changes in equity for the to 31 december 2019

Share

capital

Revaluation

reserve

Retained

earnings

Total

equity

£000 £000 £000 £000

Balance 500 1055 1555

Total comprehensive income 350 748 1098

Dividends paid 32 32

Balance at 31 december 2019 500 350 1771 2621

1(c)

Statement of financial position as at 31 December 2019

£000 £000

Assets (in order of permanence)

Non-current assets

Property, plant and equipment (W3) 2942

1

Question 1

1 (a)

Statement of comprehensive income for the year to 31

December 2019

£000 £000

Revenue 5165

Cost of sales (W1) 2833

Gross profit 2332

Other income (Rent) 66

Distribution costs (W2, W3 & W4) 553

Administration cost 946 1499

Profit from operations 899

Interest on loan (170*10%) 17

Profit before tax 882

Taxation (140-6) 134

Profit for the year 748

1(b)

Statement of changes in equity for the to 31 december 2019

Share

capital

Revaluation

reserve

Retained

earnings

Total

equity

£000 £000 £000 £000

Balance 500 1055 1555

Total comprehensive income 350 748 1098

Dividends paid 32 32

Balance at 31 december 2019 500 350 1771 2621

1(c)

Statement of financial position as at 31 December 2019

£000 £000

Assets (in order of permanence)

Non-current assets

Property, plant and equipment (W3) 2942

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

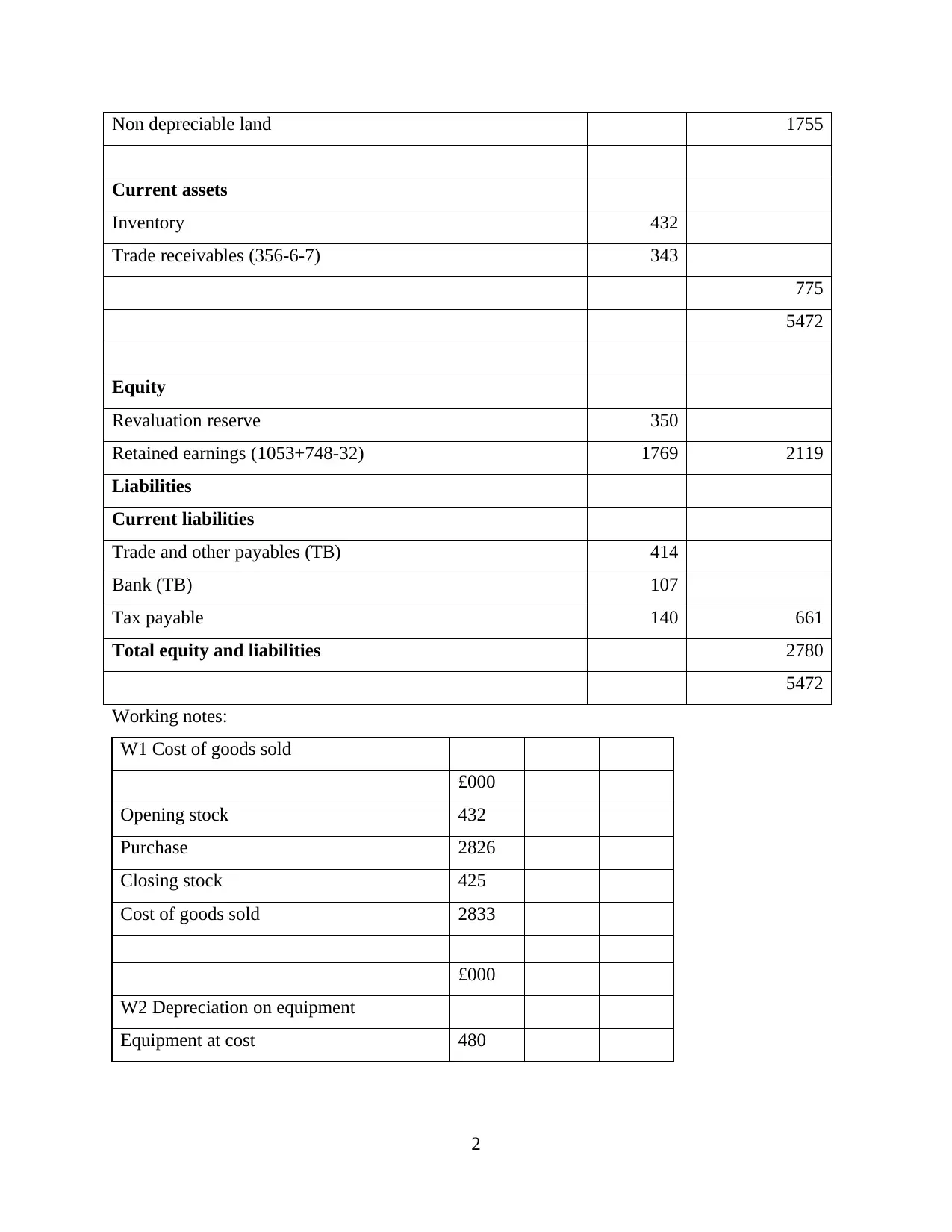

Non depreciable land 1755

Current assets

Inventory 432

Trade receivables (356-6-7) 343

775

5472

Equity

Revaluation reserve 350

Retained earnings (1053+748-32) 1769 2119

Liabilities

Current liabilities

Trade and other payables (TB) 414

Bank (TB) 107

Tax payable 140 661

Total equity and liabilities 2780

5472

Working notes:

W1 Cost of goods sold

£000

Opening stock 432

Purchase 2826

Closing stock 425

Cost of goods sold 2833

£000

W2 Depreciation on equipment

Equipment at cost 480

2

Current assets

Inventory 432

Trade receivables (356-6-7) 343

775

5472

Equity

Revaluation reserve 350

Retained earnings (1053+748-32) 1769 2119

Liabilities

Current liabilities

Trade and other payables (TB) 414

Bank (TB) 107

Tax payable 140 661

Total equity and liabilities 2780

5472

Working notes:

W1 Cost of goods sold

£000

Opening stock 432

Purchase 2826

Closing stock 425

Cost of goods sold 2833

£000

W2 Depreciation on equipment

Equipment at cost 480

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

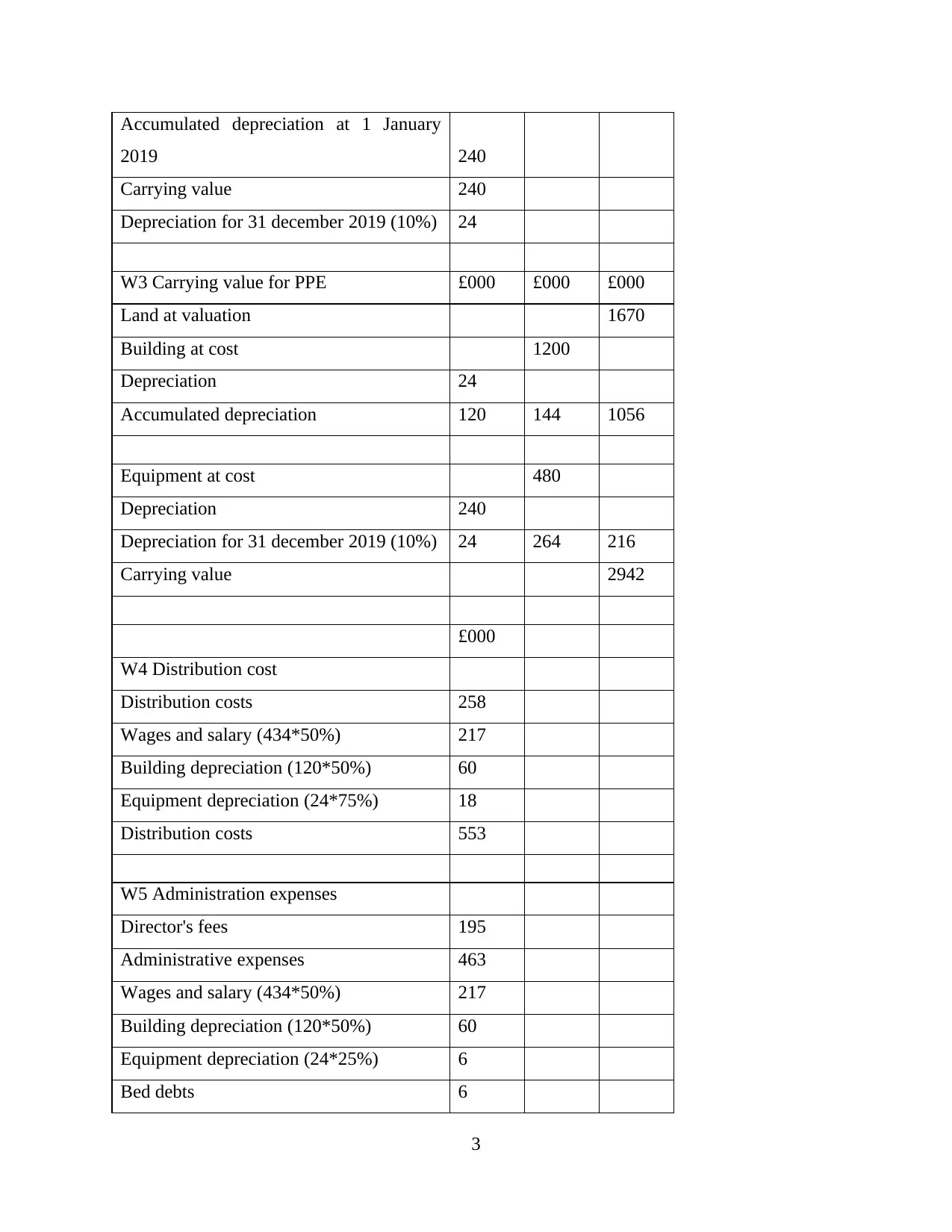

Accumulated depreciation at 1 January

2019 240

Carrying value 240

Depreciation for 31 december 2019 (10%) 24

W3 Carrying value for PPE £000 £000 £000

Land at valuation 1670

Building at cost 1200

Depreciation 24

Accumulated depreciation 120 144 1056

Equipment at cost 480

Depreciation 240

Depreciation for 31 december 2019 (10%) 24 264 216

Carrying value 2942

£000

W4 Distribution cost

Distribution costs 258

Wages and salary (434*50%) 217

Building depreciation (120*50%) 60

Equipment depreciation (24*75%) 18

Distribution costs 553

W5 Administration expenses

Director's fees 195

Administrative expenses 463

Wages and salary (434*50%) 217

Building depreciation (120*50%) 60

Equipment depreciation (24*25%) 6

Bed debts 6

3

2019 240

Carrying value 240

Depreciation for 31 december 2019 (10%) 24

W3 Carrying value for PPE £000 £000 £000

Land at valuation 1670

Building at cost 1200

Depreciation 24

Accumulated depreciation 120 144 1056

Equipment at cost 480

Depreciation 240

Depreciation for 31 december 2019 (10%) 24 264 216

Carrying value 2942

£000

W4 Distribution cost

Distribution costs 258

Wages and salary (434*50%) 217

Building depreciation (120*50%) 60

Equipment depreciation (24*75%) 18

Distribution costs 553

W5 Administration expenses

Director's fees 195

Administrative expenses 463

Wages and salary (434*50%) 217

Building depreciation (120*50%) 60

Equipment depreciation (24*25%) 6

Bed debts 6

3

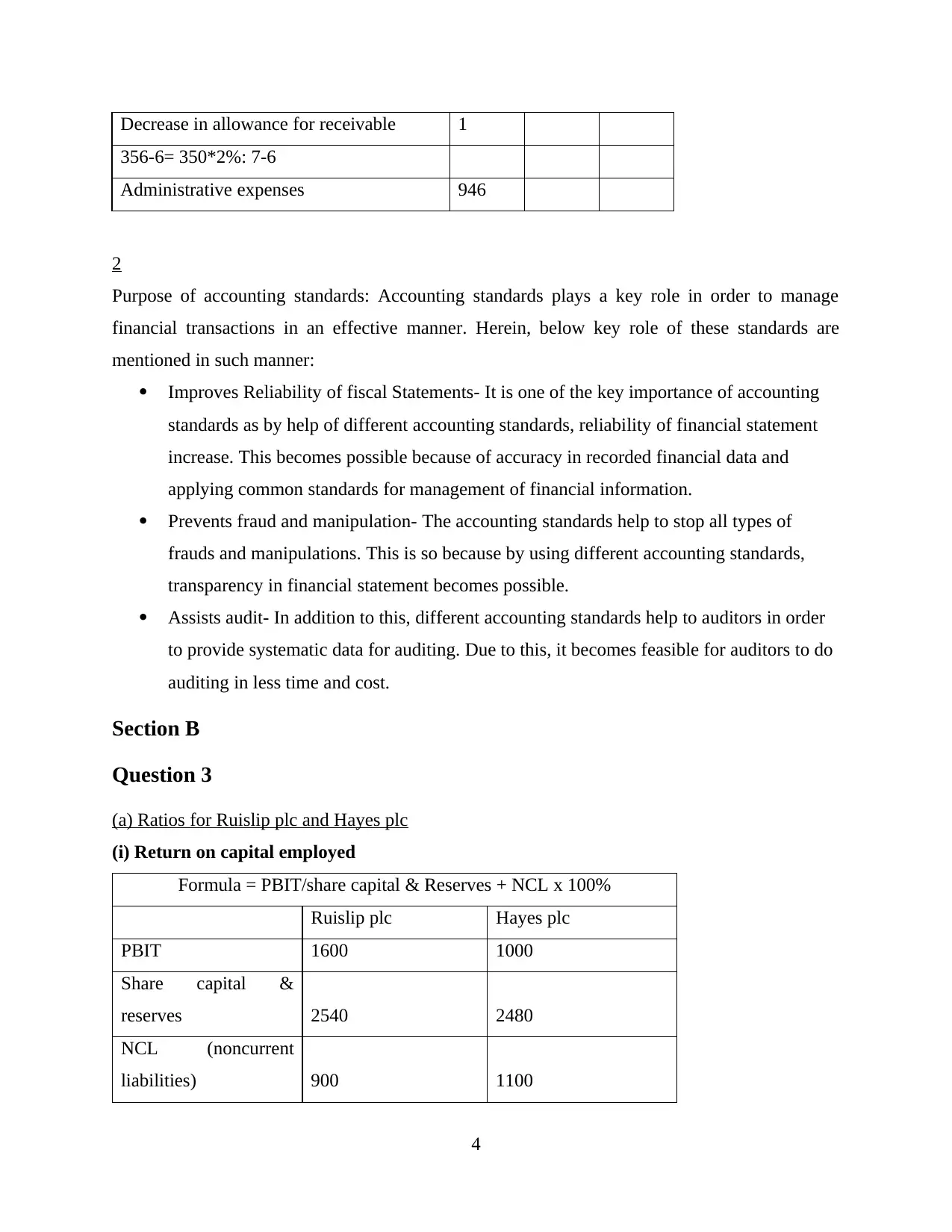

Decrease in allowance for receivable 1

356-6= 350*2%: 7-6

Administrative expenses 946

2

Purpose of accounting standards: Accounting standards plays a key role in order to manage

financial transactions in an effective manner. Herein, below key role of these standards are

mentioned in such manner:

Improves Reliability of fiscal Statements- It is one of the key importance of accounting

standards as by help of different accounting standards, reliability of financial statement

increase. This becomes possible because of accuracy in recorded financial data and

applying common standards for management of financial information.

Prevents fraud and manipulation- The accounting standards help to stop all types of

frauds and manipulations. This is so because by using different accounting standards,

transparency in financial statement becomes possible.

Assists audit- In addition to this, different accounting standards help to auditors in order

to provide systematic data for auditing. Due to this, it becomes feasible for auditors to do

auditing in less time and cost.

Section B

Question 3

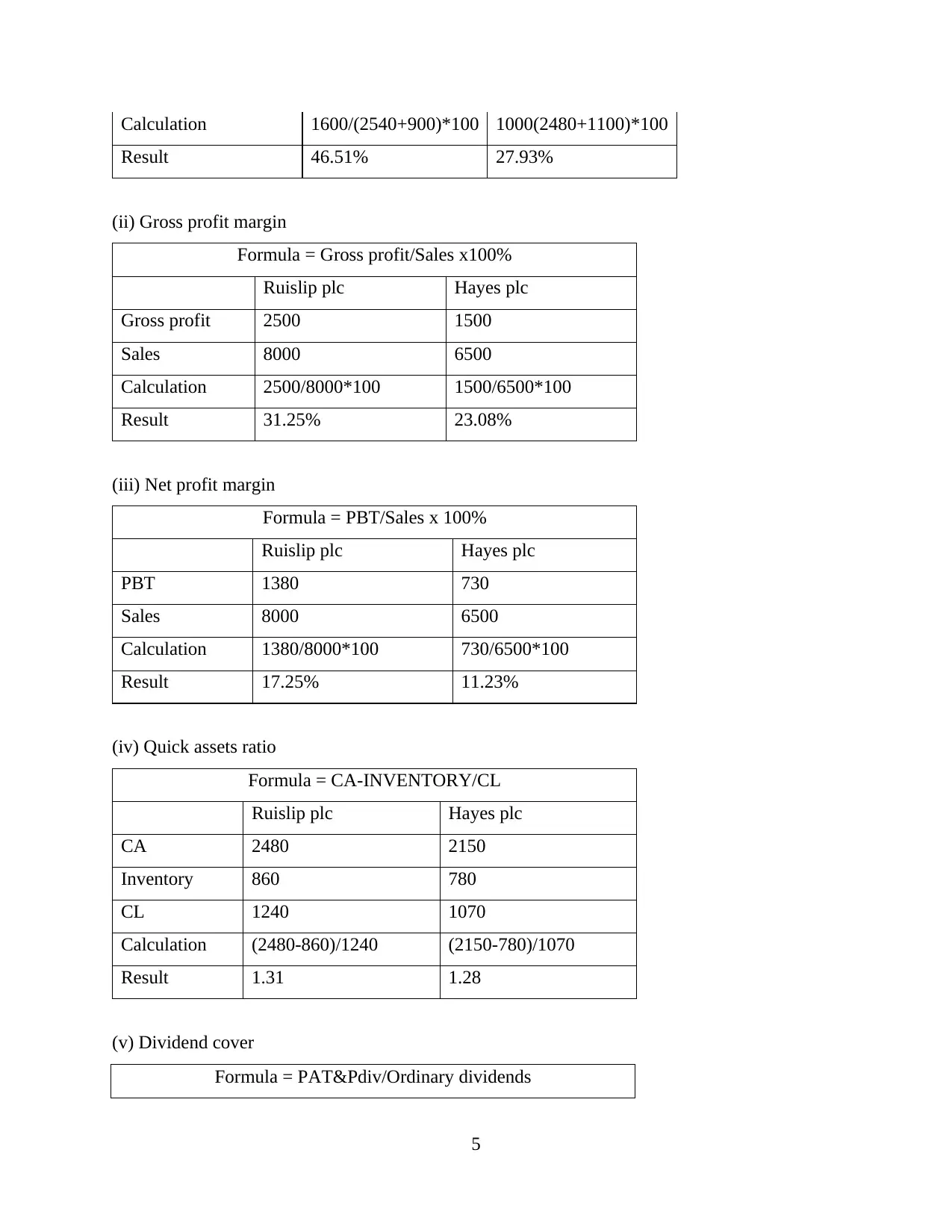

(a) Ratios for Ruislip plc and Hayes plc

(i) Return on capital employed

Formula = PBIT/share capital & Reserves + NCL x 100%

Ruislip plc Hayes plc

PBIT 1600 1000

Share capital &

reserves 2540 2480

NCL (noncurrent

liabilities) 900 1100

4

356-6= 350*2%: 7-6

Administrative expenses 946

2

Purpose of accounting standards: Accounting standards plays a key role in order to manage

financial transactions in an effective manner. Herein, below key role of these standards are

mentioned in such manner:

Improves Reliability of fiscal Statements- It is one of the key importance of accounting

standards as by help of different accounting standards, reliability of financial statement

increase. This becomes possible because of accuracy in recorded financial data and

applying common standards for management of financial information.

Prevents fraud and manipulation- The accounting standards help to stop all types of

frauds and manipulations. This is so because by using different accounting standards,

transparency in financial statement becomes possible.

Assists audit- In addition to this, different accounting standards help to auditors in order

to provide systematic data for auditing. Due to this, it becomes feasible for auditors to do

auditing in less time and cost.

Section B

Question 3

(a) Ratios for Ruislip plc and Hayes plc

(i) Return on capital employed

Formula = PBIT/share capital & Reserves + NCL x 100%

Ruislip plc Hayes plc

PBIT 1600 1000

Share capital &

reserves 2540 2480

NCL (noncurrent

liabilities) 900 1100

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation 1600/(2540+900)*100 1000(2480+1100)*100

Result 46.51% 27.93%

(ii) Gross profit margin

Formula = Gross profit/Sales x100%

Ruislip plc Hayes plc

Gross profit 2500 1500

Sales 8000 6500

Calculation 2500/8000*100 1500/6500*100

Result 31.25% 23.08%

(iii) Net profit margin

Formula = PBT/Sales x 100%

Ruislip plc Hayes plc

PBT 1380 730

Sales 8000 6500

Calculation 1380/8000*100 730/6500*100

Result 17.25% 11.23%

(iv) Quick assets ratio

Formula = CA-INVENTORY/CL

Ruislip plc Hayes plc

CA 2480 2150

Inventory 860 780

CL 1240 1070

Calculation (2480-860)/1240 (2150-780)/1070

Result 1.31 1.28

(v) Dividend cover

Formula = PAT&Pdiv/Ordinary dividends

5

Result 46.51% 27.93%

(ii) Gross profit margin

Formula = Gross profit/Sales x100%

Ruislip plc Hayes plc

Gross profit 2500 1500

Sales 8000 6500

Calculation 2500/8000*100 1500/6500*100

Result 31.25% 23.08%

(iii) Net profit margin

Formula = PBT/Sales x 100%

Ruislip plc Hayes plc

PBT 1380 730

Sales 8000 6500

Calculation 1380/8000*100 730/6500*100

Result 17.25% 11.23%

(iv) Quick assets ratio

Formula = CA-INVENTORY/CL

Ruislip plc Hayes plc

CA 2480 2150

Inventory 860 780

CL 1240 1070

Calculation (2480-860)/1240 (2150-780)/1070

Result 1.31 1.28

(v) Dividend cover

Formula = PAT&Pdiv/Ordinary dividends

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ruislip plc Hayes plc

PAT 1035 550

Ordinary dividends 425 395

Calculation 1035/425 550/395

Result 2.435294118 1.392405063

(vi) Dividend yield

Formula = DPS/MPS

Ruislip plc Hayes plc

Total dividend 425000 395000

Number of ordinary

shares 1500000 1500000

Calculation 425000/1500000 395000/1500000

DPS 0.283333333 0.263333333

MPS 2.5 2.25

Calculation 0.28/2.5*100 0.26/2.25*100

Result 11.20% 11.20%

(vii) Capital gearing

Formula = Pref Share capital + NCL/ Total SC & Res + NCL x 100%

Ruislip plc Hayes plc

Pref share capital 0 0

NCL 900 1100

Total share capital

and reserves 2540 2480

Calculation 900/(2540+900)*100 1100/(2480+1100)*100

Result 26.16% 30.73%

(viii) Interest cover

Formula = PBIT/Interest payable

Ruislip plc Hayes plc

6

PAT 1035 550

Ordinary dividends 425 395

Calculation 1035/425 550/395

Result 2.435294118 1.392405063

(vi) Dividend yield

Formula = DPS/MPS

Ruislip plc Hayes plc

Total dividend 425000 395000

Number of ordinary

shares 1500000 1500000

Calculation 425000/1500000 395000/1500000

DPS 0.283333333 0.263333333

MPS 2.5 2.25

Calculation 0.28/2.5*100 0.26/2.25*100

Result 11.20% 11.20%

(vii) Capital gearing

Formula = Pref Share capital + NCL/ Total SC & Res + NCL x 100%

Ruislip plc Hayes plc

Pref share capital 0 0

NCL 900 1100

Total share capital

and reserves 2540 2480

Calculation 900/(2540+900)*100 1100/(2480+1100)*100

Result 26.16% 30.73%

(viii) Interest cover

Formula = PBIT/Interest payable

Ruislip plc Hayes plc

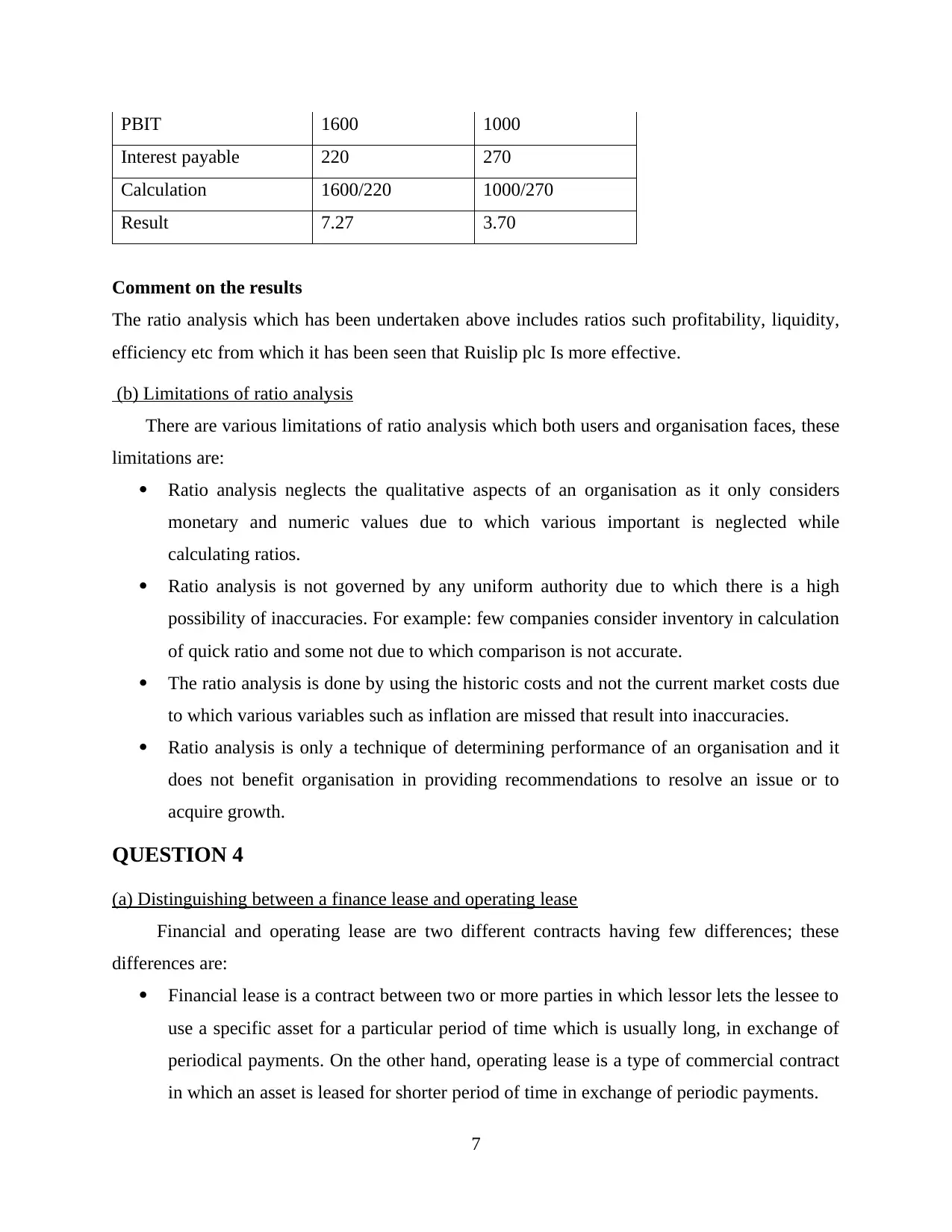

6

PBIT 1600 1000

Interest payable 220 270

Calculation 1600/220 1000/270

Result 7.27 3.70

Comment on the results

The ratio analysis which has been undertaken above includes ratios such profitability, liquidity,

efficiency etc from which it has been seen that Ruislip plc Is more effective.

(b) Limitations of ratio analysis

There are various limitations of ratio analysis which both users and organisation faces, these

limitations are:

Ratio analysis neglects the qualitative aspects of an organisation as it only considers

monetary and numeric values due to which various important is neglected while

calculating ratios.

Ratio analysis is not governed by any uniform authority due to which there is a high

possibility of inaccuracies. For example: few companies consider inventory in calculation

of quick ratio and some not due to which comparison is not accurate.

The ratio analysis is done by using the historic costs and not the current market costs due

to which various variables such as inflation are missed that result into inaccuracies.

Ratio analysis is only a technique of determining performance of an organisation and it

does not benefit organisation in providing recommendations to resolve an issue or to

acquire growth.

QUESTION 4

(a) Distinguishing between a finance lease and operating lease

Financial and operating lease are two different contracts having few differences; these

differences are:

Financial lease is a contract between two or more parties in which lessor lets the lessee to

use a specific asset for a particular period of time which is usually long, in exchange of

periodical payments. On the other hand, operating lease is a type of commercial contract

in which an asset is leased for shorter period of time in exchange of periodic payments.

7

Interest payable 220 270

Calculation 1600/220 1000/270

Result 7.27 3.70

Comment on the results

The ratio analysis which has been undertaken above includes ratios such profitability, liquidity,

efficiency etc from which it has been seen that Ruislip plc Is more effective.

(b) Limitations of ratio analysis

There are various limitations of ratio analysis which both users and organisation faces, these

limitations are:

Ratio analysis neglects the qualitative aspects of an organisation as it only considers

monetary and numeric values due to which various important is neglected while

calculating ratios.

Ratio analysis is not governed by any uniform authority due to which there is a high

possibility of inaccuracies. For example: few companies consider inventory in calculation

of quick ratio and some not due to which comparison is not accurate.

The ratio analysis is done by using the historic costs and not the current market costs due

to which various variables such as inflation are missed that result into inaccuracies.

Ratio analysis is only a technique of determining performance of an organisation and it

does not benefit organisation in providing recommendations to resolve an issue or to

acquire growth.

QUESTION 4

(a) Distinguishing between a finance lease and operating lease

Financial and operating lease are two different contracts having few differences; these

differences are:

Financial lease is a contract between two or more parties in which lessor lets the lessee to

use a specific asset for a particular period of time which is usually long, in exchange of

periodical payments. On the other hand, operating lease is a type of commercial contract

in which an asset is leased for shorter period of time in exchange of periodic payments.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the case of financial lease, the ownership of the asset is transferred to the lessee but in

case of operating lease, the ownership remains in the hands of lessor.

Financial lease is referred as a loan agreement; on the other hand, operating lease is

regarded as a rental agreement.

The responsibility of maintenance and risk is transferred to lessee in financial lease but in

case of operating lease there is low responsibility and risk of assets in hands of lessee.

(b) Explaining the factors that which indicate a finance lease

There are various factors which indicate a lease as finance lease; such factors are stated

and explained below:

Time – A long term contract which usually more than a year indicates a lease as financial

lease and the payments are done in pre-determined periods.

Transferability – A contract which provides the transferability and ownership of an asset

indicates towards a financial lease.

Tax advantage – This is the major factor which indicates a financial lease as such lease

comes with allowance of depreciation and tax deduction.

Option to purchase – According this factor, a contract having a purchase option or an

option under which lessee can purchase the asset is a financial lease.

(c) Discussing the disclosure requirements for lessors in relation to the two types of leases

For finance and operating leases, the disclosure requirements for lessors include as

follows:

Operating lease disclosures:

Lessors are required to mention the minimum amount of each lease payment; these lease

payment periods include the next year and beyond five years.

Lessors are required to disclose all significant leasing arrangements.

The amount of contingent rent which is the income of lessor.

For finance lease:

All the requirements which are stated for operating lease are required to be disclosed

under finance lease as well.

The finance income which is unearned from the lease.

The residual values which are associated with finance lease but are unguaranteed.

8

case of operating lease, the ownership remains in the hands of lessor.

Financial lease is referred as a loan agreement; on the other hand, operating lease is

regarded as a rental agreement.

The responsibility of maintenance and risk is transferred to lessee in financial lease but in

case of operating lease there is low responsibility and risk of assets in hands of lessee.

(b) Explaining the factors that which indicate a finance lease

There are various factors which indicate a lease as finance lease; such factors are stated

and explained below:

Time – A long term contract which usually more than a year indicates a lease as financial

lease and the payments are done in pre-determined periods.

Transferability – A contract which provides the transferability and ownership of an asset

indicates towards a financial lease.

Tax advantage – This is the major factor which indicates a financial lease as such lease

comes with allowance of depreciation and tax deduction.

Option to purchase – According this factor, a contract having a purchase option or an

option under which lessee can purchase the asset is a financial lease.

(c) Discussing the disclosure requirements for lessors in relation to the two types of leases

For finance and operating leases, the disclosure requirements for lessors include as

follows:

Operating lease disclosures:

Lessors are required to mention the minimum amount of each lease payment; these lease

payment periods include the next year and beyond five years.

Lessors are required to disclose all significant leasing arrangements.

The amount of contingent rent which is the income of lessor.

For finance lease:

All the requirements which are stated for operating lease are required to be disclosed

under finance lease as well.

The finance income which is unearned from the lease.

The residual values which are associated with finance lease but are unguaranteed.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lessor required to disclose payments which are considered as accumulated allowance

for uncollectable lease payments.

(d) Briefly explain the presentation and disclosure requirements for lessees

Lessees are the parties who gains the leased assets and there are various presentation and

disclosure requirements for such parties which includes:

Lessees are required to present the carrying amount of an assets along with the minimum

lease payments.

Such parties are also required to disclose contingent rent which is considered as an

expense.

Amount of sub lease is also required to be disclosed along with all significant leasing

arrangements.

9

for uncollectable lease payments.

(d) Briefly explain the presentation and disclosure requirements for lessees

Lessees are the parties who gains the leased assets and there are various presentation and

disclosure requirements for such parties which includes:

Lessees are required to present the carrying amount of an assets along with the minimum

lease payments.

Such parties are also required to disclose contingent rent which is considered as an

expense.

Amount of sub lease is also required to be disclosed along with all significant leasing

arrangements.

9

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.