Analysis of Management Accounting Systems, Methods, and Benefits

VerifiedAdded on 2023/01/11

|22

|5460

|52

Homework Assignment

AI Summary

This assignment delves into the core principles and practices of management accounting, focusing on the application of these principles within a manufacturing entity, Alpha Limited. The study initiates with an introduction to management accounting, highlighting its role in providing crucial information for decision-making. It then proceeds to examine different types of management accounting (MA) systems, including inventory management, cost accounting, job costing, and price optimization systems, emphasizing their importance and operational mechanics. The assignment also explores various MA reporting methods, such as inventory reports, performance reports, budget reports, and accounts receivable aging reports. Furthermore, it discusses the benefits of implementing MA systems, like cost control, inventory optimization, and competitive pricing. The paper also includes an income statement analysis under absorption and marginal costing, providing a practical application of the concepts discussed. Overall, the assignment provides a comprehensive overview of management accounting, its systems, reporting, and their practical applications, providing a solid foundation for understanding how these tools are used in business operations.

Principles and Practice of

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

P1 Different kind of MA system............................................................................................3

P2. Different methods of MA reports:....................................................................................5

M1. Benefits of MASs:...........................................................................................................6

TASK 3..........................................................................................................................................14

P4. Advantages and disadvantages of different types of planning tools..............................14

Advantages.....................................................................................................................................15

M3. Planning tools role to make accurate forecasting and preparing the budgets...............16

TASK 4..........................................................................................................................................16

P5. Comparison of enterprise to use MAS and techniques to overcome financial issues....16

M4. Importance of MAS in the context of solving financial problems................................18

D3. Role of planning tools in overcoming from monetary issues........................................18

CONCLUSION..............................................................................................................................19

REEFRENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

P1 Different kind of MA system............................................................................................3

P2. Different methods of MA reports:....................................................................................5

M1. Benefits of MASs:...........................................................................................................6

TASK 3..........................................................................................................................................14

P4. Advantages and disadvantages of different types of planning tools..............................14

Advantages.....................................................................................................................................15

M3. Planning tools role to make accurate forecasting and preparing the budgets...............16

TASK 4..........................................................................................................................................16

P5. Comparison of enterprise to use MAS and techniques to overcome financial issues....16

M4. Importance of MAS in the context of solving financial problems................................18

D3. Role of planning tools in overcoming from monetary issues........................................18

CONCLUSION..............................................................................................................................19

REEFRENCES..............................................................................................................................20

INTRODUCTION

Management accounting involves the framework and guidelines for the compilation of

documents and statements to help management executives in decision-making processes of the

organization. This is a larger and more diverse area which also contains managerial reporting and

accounting procedures supporting organizational practices and strategies (Chandar, Collier and

Miranti, 2012).The study discusses about each crucial aspect of managerial accounting and its

core requisites/requirements of its concerned systems in context of enterprise named Alpha

Limited, manufacturing entity and has only just 50 staff members. Alpha’s turnover per year is

around GBP500,000. Corporation has expertise in making local-made pizzas and founded in year

2001 as a small pizza corporation. With rapid growth in business company now is focusing to

open its franchising business.

TASK

P1 Different kind of MA system.

Managerial accounting, which is sometimes recognized as the management accounting,

is defined as the provision and use of accounting information supplied by a company's

executives, bookkeepers and accountants. This enables them to start taking the feasible decisions

about any ongoing problem that arises within the entity (Fiondella, Macchioni, Maffei, and

Spanò, 2016). This also helps them ingratiate themselves with the management regulation

processes that prohibit them from making any incorrect decisions that may impact the

corporation's functions. This opts for a forward-looking strategy that anticipates future from the

corporation's previous performance. Accordingly, managerial accounting lets a leader in a

company or the company as a whole make the correct decisions in areas of concern.

It is crucial to discuss about systems of MA which offers defined structures to convert raw

data and details into management relevant information. MA system may be defined as vital

mechanism which is implement by managers in organisation to generate and obtain major and

accurate information for supporting their managerial decision-making tasks. Alpha has also

implemented several major systems of MA within premises, as discussed below:

Inventory management system: Holding inventories/stock is never attractive, since excessive

inventory often amounts to increased operational expenditures. Modern manufacturing

corporations like Alpha also use the inventory management systems to assure they simply keep

Management accounting involves the framework and guidelines for the compilation of

documents and statements to help management executives in decision-making processes of the

organization. This is a larger and more diverse area which also contains managerial reporting and

accounting procedures supporting organizational practices and strategies (Chandar, Collier and

Miranti, 2012).The study discusses about each crucial aspect of managerial accounting and its

core requisites/requirements of its concerned systems in context of enterprise named Alpha

Limited, manufacturing entity and has only just 50 staff members. Alpha’s turnover per year is

around GBP500,000. Corporation has expertise in making local-made pizzas and founded in year

2001 as a small pizza corporation. With rapid growth in business company now is focusing to

open its franchising business.

TASK

P1 Different kind of MA system.

Managerial accounting, which is sometimes recognized as the management accounting,

is defined as the provision and use of accounting information supplied by a company's

executives, bookkeepers and accountants. This enables them to start taking the feasible decisions

about any ongoing problem that arises within the entity (Fiondella, Macchioni, Maffei, and

Spanò, 2016). This also helps them ingratiate themselves with the management regulation

processes that prohibit them from making any incorrect decisions that may impact the

corporation's functions. This opts for a forward-looking strategy that anticipates future from the

corporation's previous performance. Accordingly, managerial accounting lets a leader in a

company or the company as a whole make the correct decisions in areas of concern.

It is crucial to discuss about systems of MA which offers defined structures to convert raw

data and details into management relevant information. MA system may be defined as vital

mechanism which is implement by managers in organisation to generate and obtain major and

accurate information for supporting their managerial decision-making tasks. Alpha has also

implemented several major systems of MA within premises, as discussed below:

Inventory management system: Holding inventories/stock is never attractive, since excessive

inventory often amounts to increased operational expenditures. Modern manufacturing

corporations like Alpha also use the inventory management systems to assure they simply keep

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the necessary volume of inventories that will support their processes without dealing with the

unnecessary costs of keeping additional inventory (Granlund and Lukka, 2017). Adoption

of inventory management systems is essential drivers of productivity for operations. Cost

reduction is one of ways of measuring the organisation's performance. The company's inventory

management techniques like LIFO, FIFO and Average cost method allow them to minimize costs

related to inventories. This system requires thorough information of inventories and methods

used in recording inventories. Following are several methods used by organisation for valuing

inventories, as follows:

LIFO: LIFO presumes that items which have created their manner to stock (after buy, produce,

etc.) will later be first sold while those that are early produced or purchased will be last sold.

Consequently, LIFO allocates cost of new stock to costs of sold commodities and costs of older

stocks to end of inventory (Hirsch, Seubert and Sohn, 2015).

FIFO: This method assumes that first bought stock is presumed to be first sold. This approach is

just opposite to LIFO method. Here first items sold are assumed to purchased first in particular

sequence.

Average Cost: This method employs a simple average rate to value closing stock. Here average

cost is assessed by use of weights. Here no assumption required to be taken like LIFO and FIFO

method.

Cost Accounting System: This system act as vital framework which concentrates on the

managing costs and allocates costs. Various costs and expenditures are elements that define

profit estimation. Especially manufacturing entity such as Alpha often tries to minimize the cost

per pizza in order to accomplish more profitability. Such system requires thorough analysis and

evaluation of different costs incurred within organisation (Horton and de Araujo Wanderley,

2018).

Job costing system: The accountability and administration of products and processes that are by

essence or in other aspects entirely different is challenging but the deployment of a system of job

costing may ensure that tasks linked to these goods are reported and handled smoothly. This

framework is beneficial for manufacturing firms such as Alpha which have wide range of

processes and product items. For eg, in Alpha limited corporation, their management are

enforcing such accounting system with intention of maintaining control over costs of jobs

associated with the varying activities and procedures. This system requires effective

unnecessary costs of keeping additional inventory (Granlund and Lukka, 2017). Adoption

of inventory management systems is essential drivers of productivity for operations. Cost

reduction is one of ways of measuring the organisation's performance. The company's inventory

management techniques like LIFO, FIFO and Average cost method allow them to minimize costs

related to inventories. This system requires thorough information of inventories and methods

used in recording inventories. Following are several methods used by organisation for valuing

inventories, as follows:

LIFO: LIFO presumes that items which have created their manner to stock (after buy, produce,

etc.) will later be first sold while those that are early produced or purchased will be last sold.

Consequently, LIFO allocates cost of new stock to costs of sold commodities and costs of older

stocks to end of inventory (Hirsch, Seubert and Sohn, 2015).

FIFO: This method assumes that first bought stock is presumed to be first sold. This approach is

just opposite to LIFO method. Here first items sold are assumed to purchased first in particular

sequence.

Average Cost: This method employs a simple average rate to value closing stock. Here average

cost is assessed by use of weights. Here no assumption required to be taken like LIFO and FIFO

method.

Cost Accounting System: This system act as vital framework which concentrates on the

managing costs and allocates costs. Various costs and expenditures are elements that define

profit estimation. Especially manufacturing entity such as Alpha often tries to minimize the cost

per pizza in order to accomplish more profitability. Such system requires thorough analysis and

evaluation of different costs incurred within organisation (Horton and de Araujo Wanderley,

2018).

Job costing system: The accountability and administration of products and processes that are by

essence or in other aspects entirely different is challenging but the deployment of a system of job

costing may ensure that tasks linked to these goods are reported and handled smoothly. This

framework is beneficial for manufacturing firms such as Alpha which have wide range of

processes and product items. For eg, in Alpha limited corporation, their management are

enforcing such accounting system with intention of maintaining control over costs of jobs

associated with the varying activities and procedures. This system requires effective

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

categorisation of job processes and proper allocation of multiple costs to such prespecified job

processes.

Price optimisation system: This can be categorized as system of MA that is basically

connected to the products and services' pricing phase. It acts as supporting framework for

determining the prices of products in Alpha limited as it determine the prices by evaluating the

effect of suych price on demand as well as customer response. Corporations need to change the

commodity prices in accordance with marketing research. As in Alpha limited business, their

sales department has fix Pizzas prices as per market superiority and consumer requirements.

Essential Requirements of Management Accounting:

Accuracy: The information which is required for different management accounting

systems should be accurate. Vagueness and ambiguity in management accounting information

leads to inaccurate forecasts and interpretations which hinders the overall effectiveness of

management accounting.

Reliability: One of the most essential requirement of management accounting is that the

information which is being used by the management for decision-making related to everyday

operations is originating from a reliable source. Information from unauthentic and unreliable

sources is not significant for managers to make forecasts.

Relevancy: It is also very essential for the managers of an organisation to determine

which information is relevant and useful for making any conclusion or interpretation. A lot of

information is accumulated in the management accounting process which doesn’t have any

influence on the decisions and operations and such information should be ignored by the

managers.

Regularity: Irregularity and inconsistency in the information required by managers

hinders the effectiveness of management accounting systems and hence, it is imperative as an

essential requirement of management accounting to ensure that information is provided to the

managers regularly and timely.

Organisational structure: Structure of an organisation and channels of communication

within the company affects the flow of information which is essential for management

accounting. A strict chain of command and communication channel within the organisation

might stem the effectiveness in the flow of information which is not a desirable situation for

processes.

Price optimisation system: This can be categorized as system of MA that is basically

connected to the products and services' pricing phase. It acts as supporting framework for

determining the prices of products in Alpha limited as it determine the prices by evaluating the

effect of suych price on demand as well as customer response. Corporations need to change the

commodity prices in accordance with marketing research. As in Alpha limited business, their

sales department has fix Pizzas prices as per market superiority and consumer requirements.

Essential Requirements of Management Accounting:

Accuracy: The information which is required for different management accounting

systems should be accurate. Vagueness and ambiguity in management accounting information

leads to inaccurate forecasts and interpretations which hinders the overall effectiveness of

management accounting.

Reliability: One of the most essential requirement of management accounting is that the

information which is being used by the management for decision-making related to everyday

operations is originating from a reliable source. Information from unauthentic and unreliable

sources is not significant for managers to make forecasts.

Relevancy: It is also very essential for the managers of an organisation to determine

which information is relevant and useful for making any conclusion or interpretation. A lot of

information is accumulated in the management accounting process which doesn’t have any

influence on the decisions and operations and such information should be ignored by the

managers.

Regularity: Irregularity and inconsistency in the information required by managers

hinders the effectiveness of management accounting systems and hence, it is imperative as an

essential requirement of management accounting to ensure that information is provided to the

managers regularly and timely.

Organisational structure: Structure of an organisation and channels of communication

within the company affects the flow of information which is essential for management

accounting. A strict chain of command and communication channel within the organisation

might stem the effectiveness in the flow of information which is not a desirable situation for

management accounting. Hence, it is vital for managers to ensure that organisational structure

allows the exchange and free flow of information to the managers.

P2. Different methods of MA reports:

The word MA reporting method can be defined as reports which constitute valuable

information concerning to all facets of financing and management. This reporting method offers

quick analysis of organisation’s performance. Generally, unit managers within organisation use

these methods to report critical analysis and information to top level managing officials

(Kastberg and Siverbo, 2016). Managers in Alpha prepare various types of reports as a part of

entire management accounting mechanism, as follows:

Inventory report: It may be characterized as a style of reporting which involves essential

information relating to the opening and closing of the balances of different types of inventories

within Alpha, namely raw resources items, finished goods items etc. Such a report contains all

information of methods used for determining stock volumes like LIFO, FIFO and weighted

average system. In the aforementioned Alpha limited business, executives are using such report

to keep in contact about how much materials they have at end of a single day.

Performance report: This report method that includes the main performance-related details for

each employee in detail. This is required by managers in companies to make rational judgments

about growth of the employees. The absence of this report will mask the overall output of staff.

Besides employee performance records, it also provides key information such as output of

different functions and activities performed, etc. In case of the aforementioned Alpha limited

corporation, the managers prepare this report in attempt to maintain and improve performance of

employees and set policies for them.

Budget report: This is a report which contains precise detail about budget success and actual

outcomes. through this report, the Financing division would be enabled to determine the

discrepancy between real and estimated efficiency. The managers produce this report towards

tracking deviations and keeping an additional finger on final results within the framework

of above-mentioned Alpha limited corporation. Information of this report act as basic foundation

of entire established budgetary system and managerial control as it allocates areas of deficiency

in system (Prencipe, Bar-Yosef and Dekker, 2014).

Accounts receivable ageing report: It can be represented as a report which offers extensive

figures on overall account receivable balance that is to be collected by enterprise and how much

allows the exchange and free flow of information to the managers.

P2. Different methods of MA reports:

The word MA reporting method can be defined as reports which constitute valuable

information concerning to all facets of financing and management. This reporting method offers

quick analysis of organisation’s performance. Generally, unit managers within organisation use

these methods to report critical analysis and information to top level managing officials

(Kastberg and Siverbo, 2016). Managers in Alpha prepare various types of reports as a part of

entire management accounting mechanism, as follows:

Inventory report: It may be characterized as a style of reporting which involves essential

information relating to the opening and closing of the balances of different types of inventories

within Alpha, namely raw resources items, finished goods items etc. Such a report contains all

information of methods used for determining stock volumes like LIFO, FIFO and weighted

average system. In the aforementioned Alpha limited business, executives are using such report

to keep in contact about how much materials they have at end of a single day.

Performance report: This report method that includes the main performance-related details for

each employee in detail. This is required by managers in companies to make rational judgments

about growth of the employees. The absence of this report will mask the overall output of staff.

Besides employee performance records, it also provides key information such as output of

different functions and activities performed, etc. In case of the aforementioned Alpha limited

corporation, the managers prepare this report in attempt to maintain and improve performance of

employees and set policies for them.

Budget report: This is a report which contains precise detail about budget success and actual

outcomes. through this report, the Financing division would be enabled to determine the

discrepancy between real and estimated efficiency. The managers produce this report towards

tracking deviations and keeping an additional finger on final results within the framework

of above-mentioned Alpha limited corporation. Information of this report act as basic foundation

of entire established budgetary system and managerial control as it allocates areas of deficiency

in system (Prencipe, Bar-Yosef and Dekker, 2014).

Accounts receivable ageing report: It can be represented as a report which offers extensive

figures on overall account receivable balance that is to be collected by enterprise and how much

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

average time it takes to generate cash through accounts receivables. In Alpha, managing

personnel and accounting officials use this report to recognise all the existing and possible

debtors who are or may be bankrupt. It also helps to determine the policies for providing credit

limits.

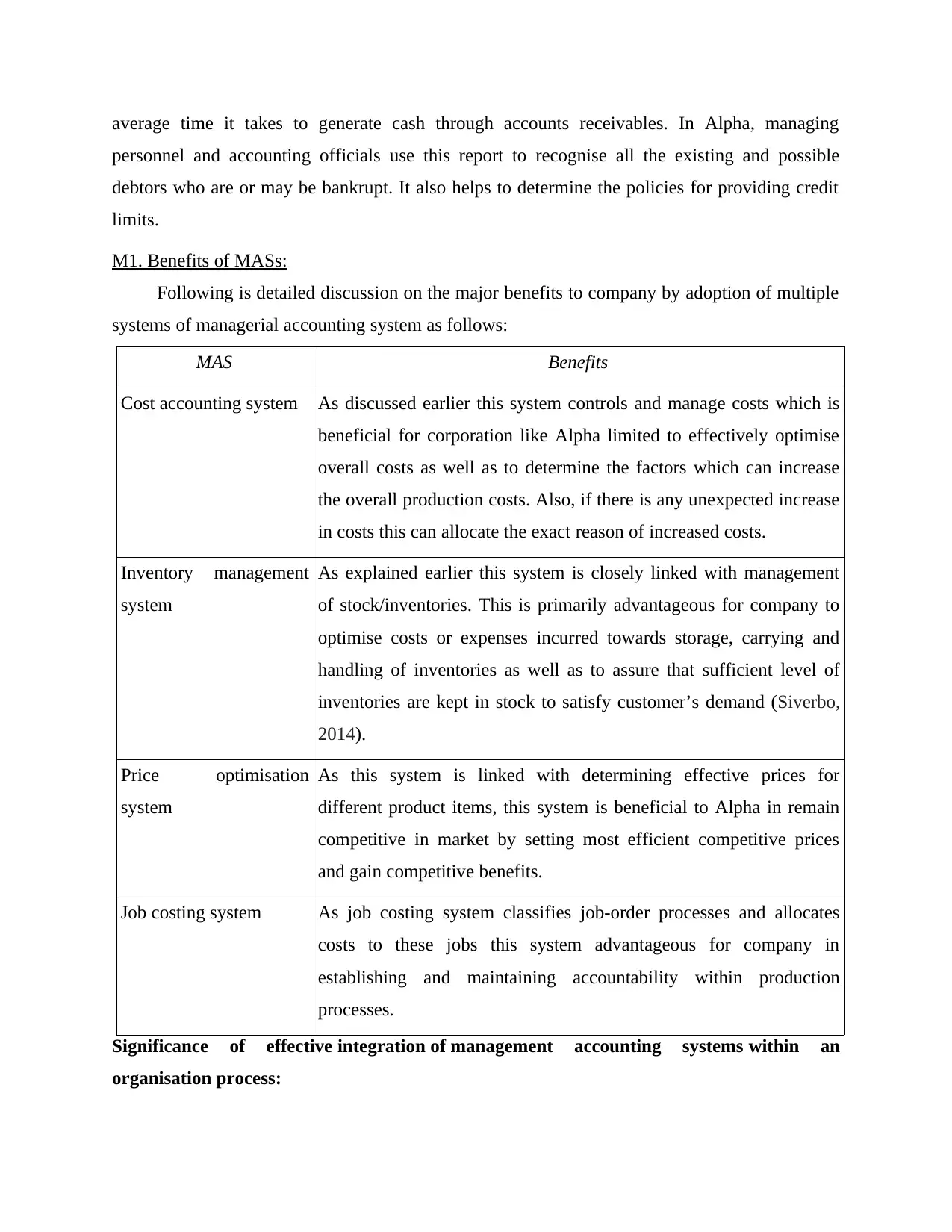

M1. Benefits of MASs:

Following is detailed discussion on the major benefits to company by adoption of multiple

systems of managerial accounting system as follows:

MAS Benefits

Cost accounting system As discussed earlier this system controls and manage costs which is

beneficial for corporation like Alpha limited to effectively optimise

overall costs as well as to determine the factors which can increase

the overall production costs. Also, if there is any unexpected increase

in costs this can allocate the exact reason of increased costs.

Inventory management

system

As explained earlier this system is closely linked with management

of stock/inventories. This is primarily advantageous for company to

optimise costs or expenses incurred towards storage, carrying and

handling of inventories as well as to assure that sufficient level of

inventories are kept in stock to satisfy customer’s demand (Siverbo,

2014).

Price optimisation

system

As this system is linked with determining effective prices for

different product items, this system is beneficial to Alpha in remain

competitive in market by setting most efficient competitive prices

and gain competitive benefits.

Job costing system As job costing system classifies job-order processes and allocates

costs to these jobs this system advantageous for company in

establishing and maintaining accountability within production

processes.

Significance of effective integration of management accounting systems within an

organisation process:

personnel and accounting officials use this report to recognise all the existing and possible

debtors who are or may be bankrupt. It also helps to determine the policies for providing credit

limits.

M1. Benefits of MASs:

Following is detailed discussion on the major benefits to company by adoption of multiple

systems of managerial accounting system as follows:

MAS Benefits

Cost accounting system As discussed earlier this system controls and manage costs which is

beneficial for corporation like Alpha limited to effectively optimise

overall costs as well as to determine the factors which can increase

the overall production costs. Also, if there is any unexpected increase

in costs this can allocate the exact reason of increased costs.

Inventory management

system

As explained earlier this system is closely linked with management

of stock/inventories. This is primarily advantageous for company to

optimise costs or expenses incurred towards storage, carrying and

handling of inventories as well as to assure that sufficient level of

inventories are kept in stock to satisfy customer’s demand (Siverbo,

2014).

Price optimisation

system

As this system is linked with determining effective prices for

different product items, this system is beneficial to Alpha in remain

competitive in market by setting most efficient competitive prices

and gain competitive benefits.

Job costing system As job costing system classifies job-order processes and allocates

costs to these jobs this system advantageous for company in

establishing and maintaining accountability within production

processes.

Significance of effective integration of management accounting systems within an

organisation process:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To accomplish smoother operating within an organization, a structured integration of the

above explained systems is usually required. all these specific systems enhance corporation

performance through the provision of crucial details. As in Alpha, Cost-accounting systems as

well as stock management system, aid in managing various processes within the enterprise such

as inventory control, cost sheet planning, process cost evaluation, etc. In Alpha limited,

company's sales and related processes are integrated with price optimization framework and

stock management framework (Teittinen, Pellinen and Järvenpää, 2013). There integration of

MA systems with process is needed for achievement of sustainable growth of organisation and

run business in smoother way.

above explained systems is usually required. all these specific systems enhance corporation

performance through the provision of crucial details. As in Alpha, Cost-accounting systems as

well as stock management system, aid in managing various processes within the enterprise such

as inventory control, cost sheet planning, process cost evaluation, etc. In Alpha limited,

company's sales and related processes are integrated with price optimization framework and

stock management framework (Teittinen, Pellinen and Järvenpää, 2013). There integration of

MA systems with process is needed for achievement of sustainable growth of organisation and

run business in smoother way.

Problem 1.

Income statement under absorption and marginal costing:

Absorption costing:

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19

01/09/

19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

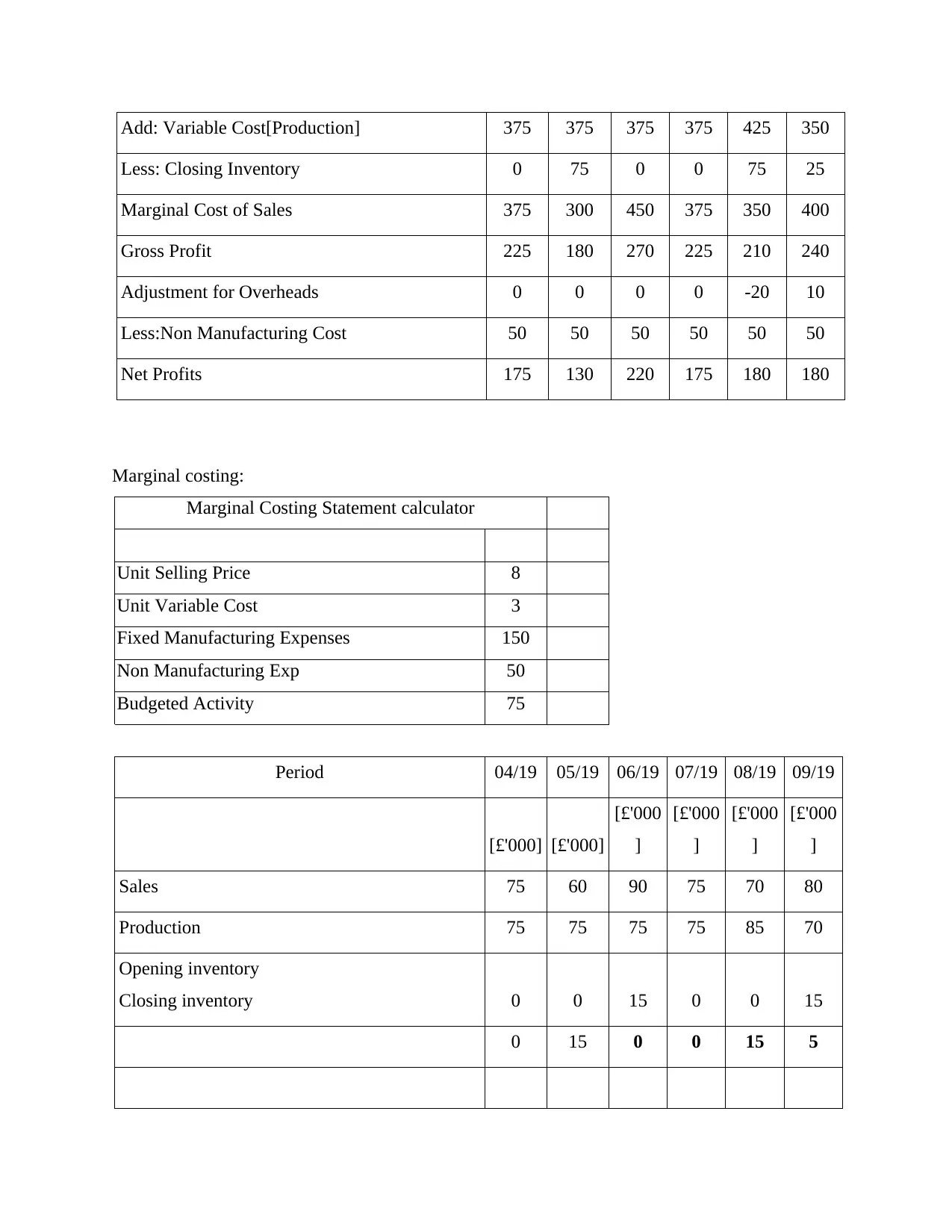

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Income statement under absorption and marginal costing:

Absorption costing:

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19

01/09/

19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Add: Variable Cost[Production] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Marginal costing:

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Marginal costing:

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufacturing Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

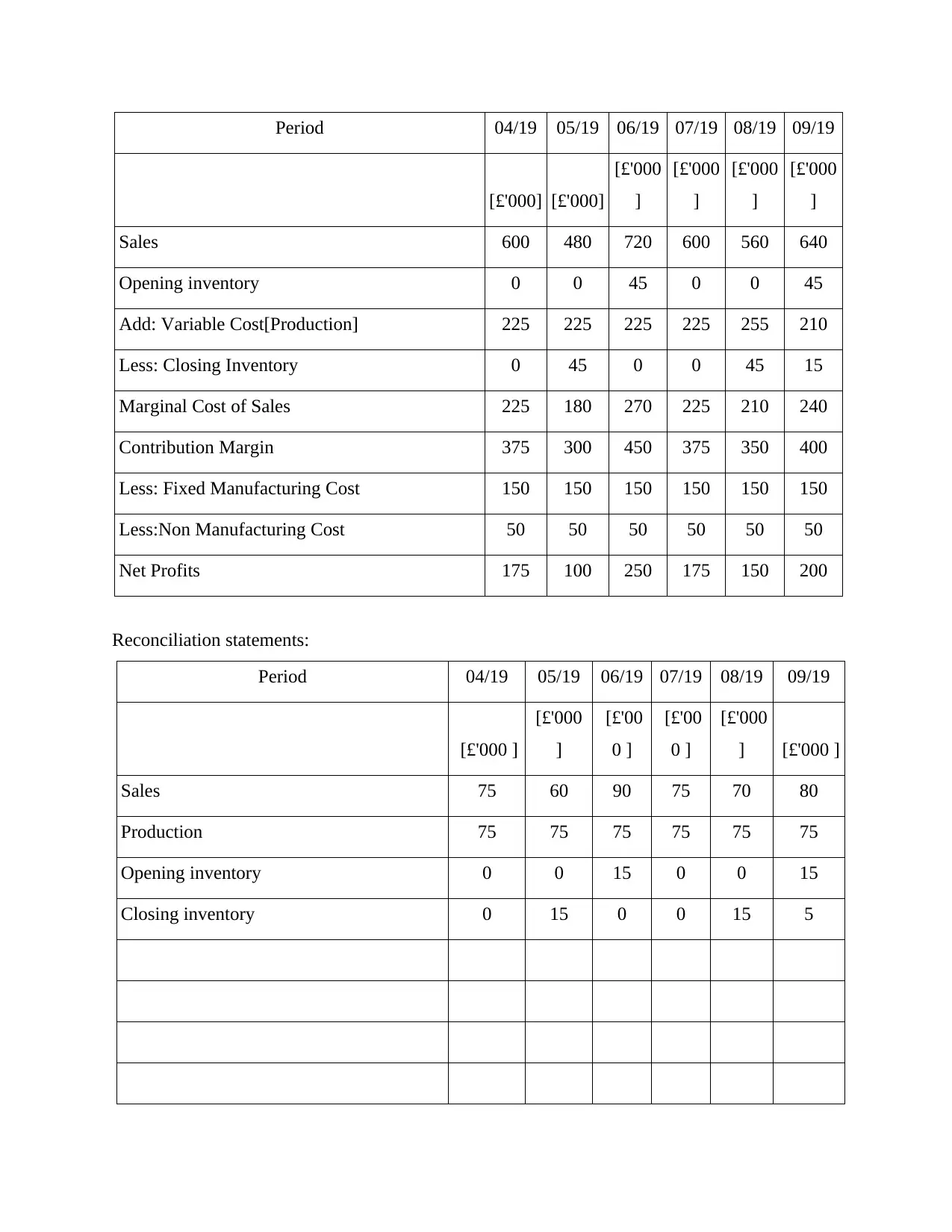

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Production] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufacturing Cost 150 150 150 150 150 150

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Sales 75 60 90 75 70 80

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Production] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufacturing Cost 150 150 150 150 150 150

Less:Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Sales 75 60 90 75 70 80

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

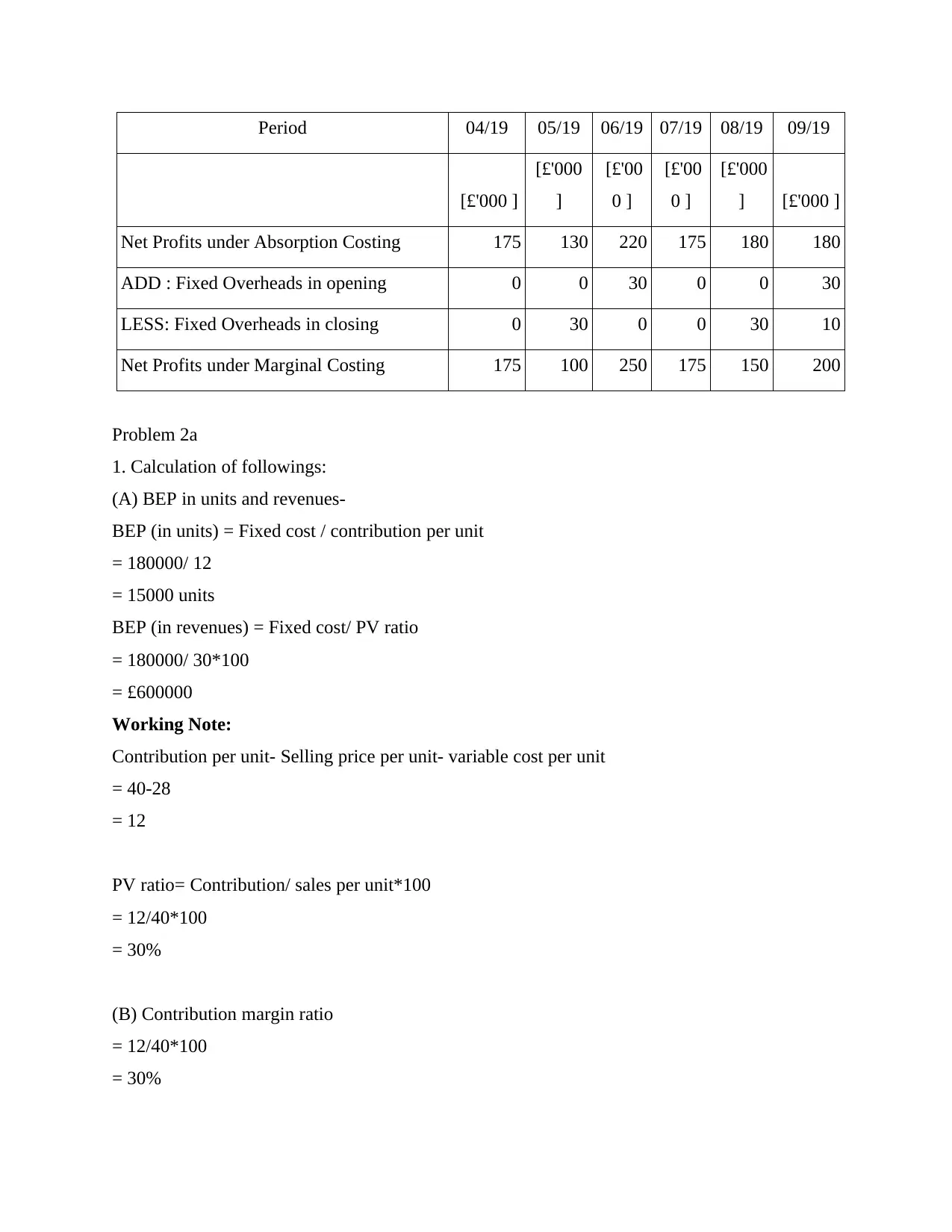

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units) = Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues) = Fixed cost/ PV ratio

= 180000/ 30*100

= £600000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

PV ratio= Contribution/ sales per unit*100

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units) = Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues) = Fixed cost/ PV ratio

= 180000/ 30*100

= £600000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

PV ratio= Contribution/ sales per unit*100

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.