Principles of Finance Assignment: Solutions for Finance Problems

VerifiedAdded on 2022/10/14

|13

|2767

|14

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Principles of Finance assignment, addressing key concepts in financial management. The assignment covers a range of topics including capital budgeting, security valuation, and project evaluation. Problem 1 explores miscellaneous topics like project ranking based on IRR and NPV, and accelerated depreciation. Problem 2 focuses on security valuation, bond yields, and stock prices, including calculations of YTM and intrinsic value. Problem 3 delves into investment analysis and project evaluation, determining the viability of a project through NPV and IRR analysis. Problem 4 addresses topics like share buybacks, cost of capital, and the impact of financial leverage. Finally, Problem 5 examines financial statements and cost of capital calculations. The solutions include detailed calculations, explanations, and interpretations, providing a thorough understanding of the principles discussed.

Running Head: Principles of Finance

Principles of Finance

Name of the Student:

Name of the University:

Author’s Note:

Principles of Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1Principles of Finance

Table of Contents

Problem 1 ..………………………………………………………………………………………………………... 2

Problem 2…………….………………………………………………………………………………………….... 3

Problem 3 ……………………………………………………………………………………………………….…. 6

Problem 4 ……………………………………………..……………………………………………………….….. 7

Problem 5 ………………………………………………………………………………………………………….. 9

References ………………………………………………………………………………………..………………12

Table of Contents

Problem 1 ..………………………………………………………………………………………………………... 2

Problem 2…………….………………………………………………………………………………………….... 3

Problem 3 ……………………………………………………………………………………………………….…. 6

Problem 4 ……………………………………………..……………………………………………………….….. 7

Problem 5 ………………………………………………………………………………………………………….. 9

References ………………………………………………………………………………………..………………12

2Principles of Finance

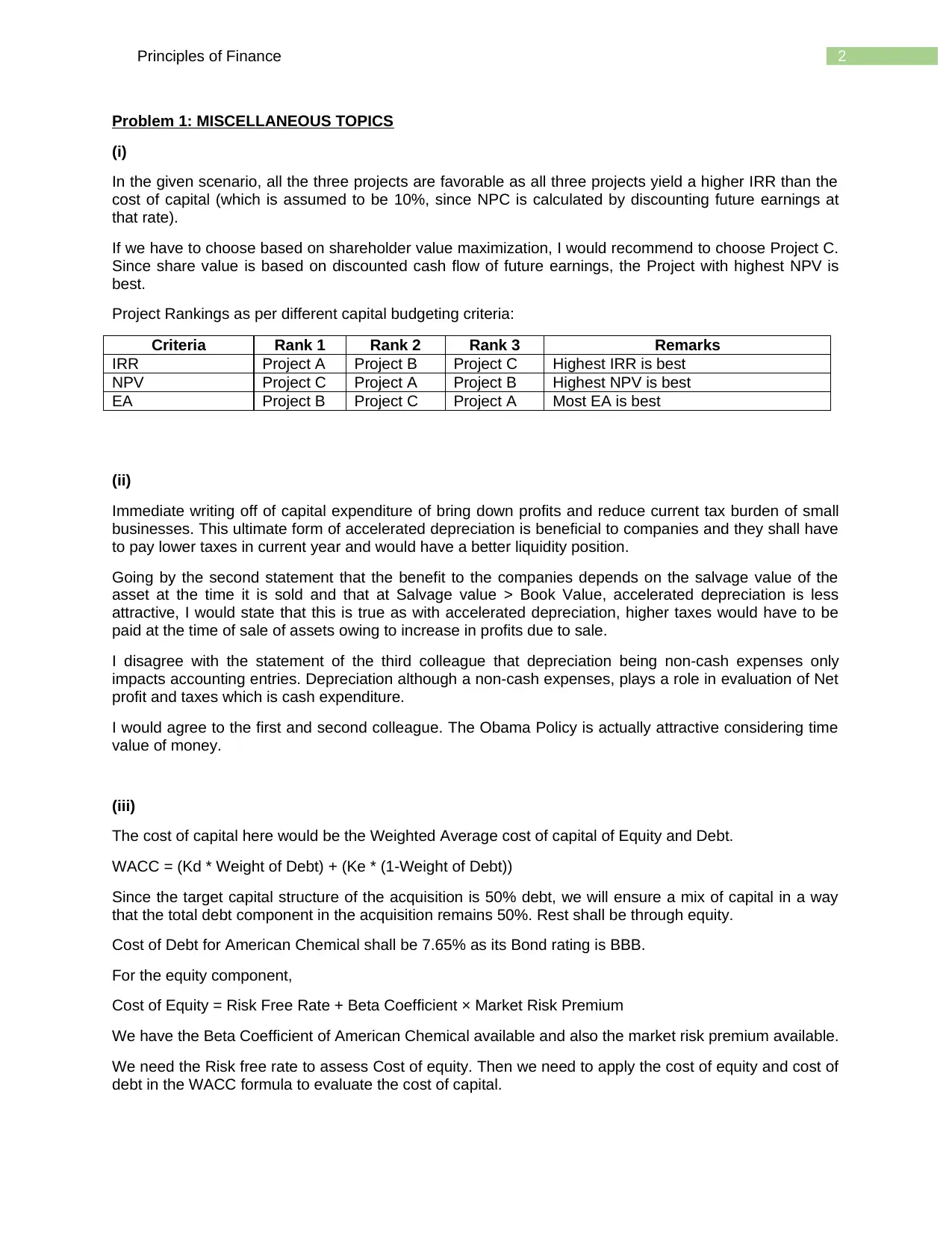

Problem 1: MISCELLANEOUS TOPICS

(i)

In the given scenario, all the three projects are favorable as all three projects yield a higher IRR than the

cost of capital (which is assumed to be 10%, since NPC is calculated by discounting future earnings at

that rate).

If we have to choose based on shareholder value maximization, I would recommend to choose Project C.

Since share value is based on discounted cash flow of future earnings, the Project with highest NPV is

best.

Project Rankings as per different capital budgeting criteria:

Criteria Rank 1 Rank 2 Rank 3 Remarks

IRR Project A Project B Project C Highest IRR is best

NPV Project C Project A Project B Highest NPV is best

EA Project B Project C Project A Most EA is best

(ii)

Immediate writing off of capital expenditure of bring down profits and reduce current tax burden of small

businesses. This ultimate form of accelerated depreciation is beneficial to companies and they shall have

to pay lower taxes in current year and would have a better liquidity position.

Going by the second statement that the benefit to the companies depends on the salvage value of the

asset at the time it is sold and that at Salvage value > Book Value, accelerated depreciation is less

attractive, I would state that this is true as with accelerated depreciation, higher taxes would have to be

paid at the time of sale of assets owing to increase in profits due to sale.

I disagree with the statement of the third colleague that depreciation being non-cash expenses only

impacts accounting entries. Depreciation although a non-cash expenses, plays a role in evaluation of Net

profit and taxes which is cash expenditure.

I would agree to the first and second colleague. The Obama Policy is actually attractive considering time

value of money.

(iii)

The cost of capital here would be the Weighted Average cost of capital of Equity and Debt.

WACC = (Kd * Weight of Debt) + (Ke * (1-Weight of Debt))

Since the target capital structure of the acquisition is 50% debt, we will ensure a mix of capital in a way

that the total debt component in the acquisition remains 50%. Rest shall be through equity.

Cost of Debt for American Chemical shall be 7.65% as its Bond rating is BBB.

For the equity component,

Cost of Equity = Risk Free Rate + Beta Coefficient × Market Risk Premium

We have the Beta Coefficient of American Chemical available and also the market risk premium available.

We need the Risk free rate to assess Cost of equity. Then we need to apply the cost of equity and cost of

debt in the WACC formula to evaluate the cost of capital.

Problem 1: MISCELLANEOUS TOPICS

(i)

In the given scenario, all the three projects are favorable as all three projects yield a higher IRR than the

cost of capital (which is assumed to be 10%, since NPC is calculated by discounting future earnings at

that rate).

If we have to choose based on shareholder value maximization, I would recommend to choose Project C.

Since share value is based on discounted cash flow of future earnings, the Project with highest NPV is

best.

Project Rankings as per different capital budgeting criteria:

Criteria Rank 1 Rank 2 Rank 3 Remarks

IRR Project A Project B Project C Highest IRR is best

NPV Project C Project A Project B Highest NPV is best

EA Project B Project C Project A Most EA is best

(ii)

Immediate writing off of capital expenditure of bring down profits and reduce current tax burden of small

businesses. This ultimate form of accelerated depreciation is beneficial to companies and they shall have

to pay lower taxes in current year and would have a better liquidity position.

Going by the second statement that the benefit to the companies depends on the salvage value of the

asset at the time it is sold and that at Salvage value > Book Value, accelerated depreciation is less

attractive, I would state that this is true as with accelerated depreciation, higher taxes would have to be

paid at the time of sale of assets owing to increase in profits due to sale.

I disagree with the statement of the third colleague that depreciation being non-cash expenses only

impacts accounting entries. Depreciation although a non-cash expenses, plays a role in evaluation of Net

profit and taxes which is cash expenditure.

I would agree to the first and second colleague. The Obama Policy is actually attractive considering time

value of money.

(iii)

The cost of capital here would be the Weighted Average cost of capital of Equity and Debt.

WACC = (Kd * Weight of Debt) + (Ke * (1-Weight of Debt))

Since the target capital structure of the acquisition is 50% debt, we will ensure a mix of capital in a way

that the total debt component in the acquisition remains 50%. Rest shall be through equity.

Cost of Debt for American Chemical shall be 7.65% as its Bond rating is BBB.

For the equity component,

Cost of Equity = Risk Free Rate + Beta Coefficient × Market Risk Premium

We have the Beta Coefficient of American Chemical available and also the market risk premium available.

We need the Risk free rate to assess Cost of equity. Then we need to apply the cost of equity and cost of

debt in the WACC formula to evaluate the cost of capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3Principles of Finance

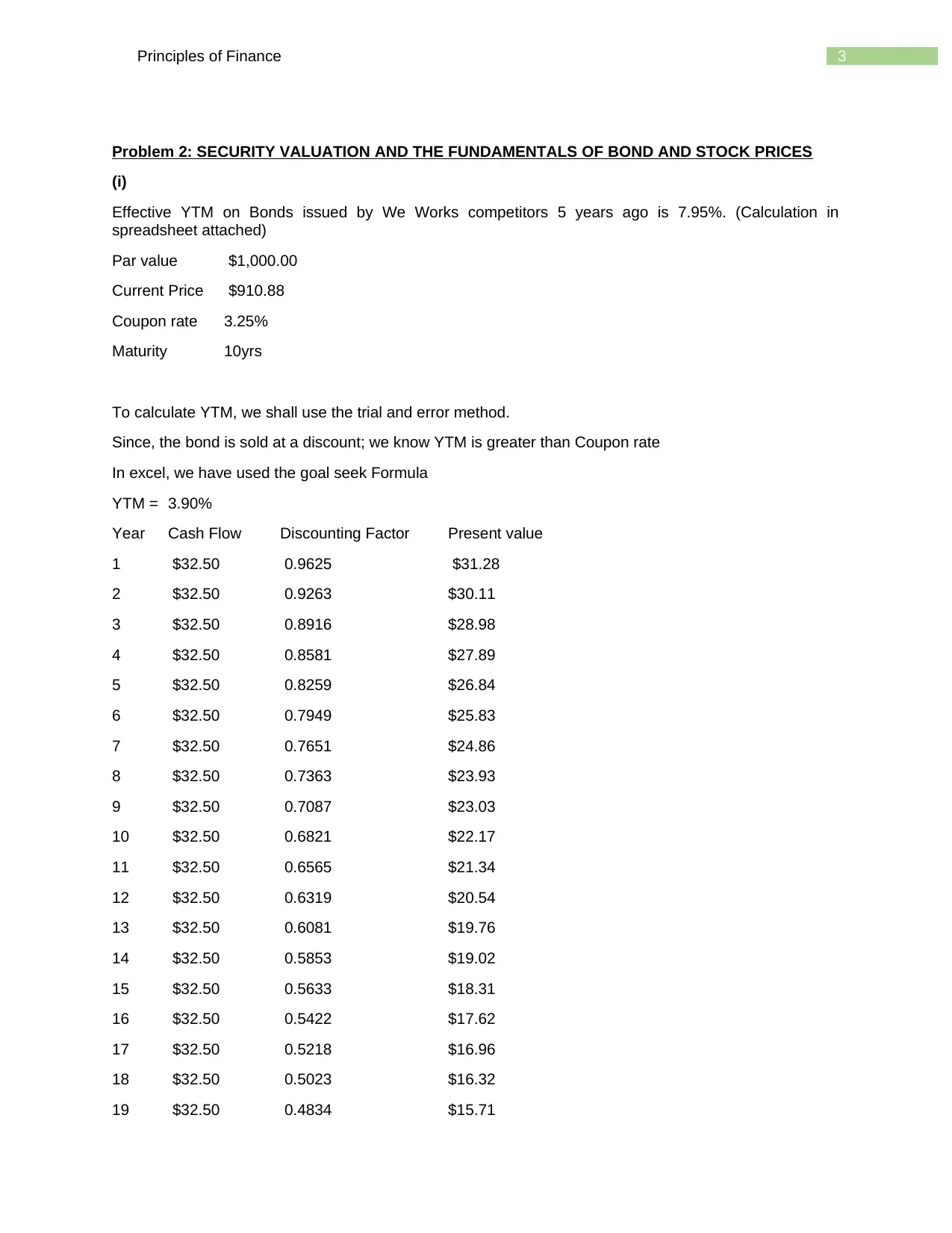

Problem 2: SECURITY VALUATION AND THE FUNDAMENTALS OF BOND AND STOCK PRICES

(i)

Effective YTM on Bonds issued by We Works competitors 5 years ago is 7.95%. (Calculation in

spreadsheet attached)

Par value $1,000.00

Current Price $910.88

Coupon rate 3.25%

Maturity 10yrs

To calculate YTM, we shall use the trial and error method.

Since, the bond is sold at a discount; we know YTM is greater than Coupon rate

In excel, we have used the goal seek Formula

YTM = 3.90%

Year Cash Flow Discounting Factor Present value

1 $32.50 0.9625 $31.28

2 $32.50 0.9263 $30.11

3 $32.50 0.8916 $28.98

4 $32.50 0.8581 $27.89

5 $32.50 0.8259 $26.84

6 $32.50 0.7949 $25.83

7 $32.50 0.7651 $24.86

8 $32.50 0.7363 $23.93

9 $32.50 0.7087 $23.03

10 $32.50 0.6821 $22.17

11 $32.50 0.6565 $21.34

12 $32.50 0.6319 $20.54

13 $32.50 0.6081 $19.76

14 $32.50 0.5853 $19.02

15 $32.50 0.5633 $18.31

16 $32.50 0.5422 $17.62

17 $32.50 0.5218 $16.96

18 $32.50 0.5023 $16.32

19 $32.50 0.4834 $15.71

Problem 2: SECURITY VALUATION AND THE FUNDAMENTALS OF BOND AND STOCK PRICES

(i)

Effective YTM on Bonds issued by We Works competitors 5 years ago is 7.95%. (Calculation in

spreadsheet attached)

Par value $1,000.00

Current Price $910.88

Coupon rate 3.25%

Maturity 10yrs

To calculate YTM, we shall use the trial and error method.

Since, the bond is sold at a discount; we know YTM is greater than Coupon rate

In excel, we have used the goal seek Formula

YTM = 3.90%

Year Cash Flow Discounting Factor Present value

1 $32.50 0.9625 $31.28

2 $32.50 0.9263 $30.11

3 $32.50 0.8916 $28.98

4 $32.50 0.8581 $27.89

5 $32.50 0.8259 $26.84

6 $32.50 0.7949 $25.83

7 $32.50 0.7651 $24.86

8 $32.50 0.7363 $23.93

9 $32.50 0.7087 $23.03

10 $32.50 0.6821 $22.17

11 $32.50 0.6565 $21.34

12 $32.50 0.6319 $20.54

13 $32.50 0.6081 $19.76

14 $32.50 0.5853 $19.02

15 $32.50 0.5633 $18.31

16 $32.50 0.5422 $17.62

17 $32.50 0.5218 $16.96

18 $32.50 0.5023 $16.32

19 $32.50 0.4834 $15.71

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4Principles of Finance

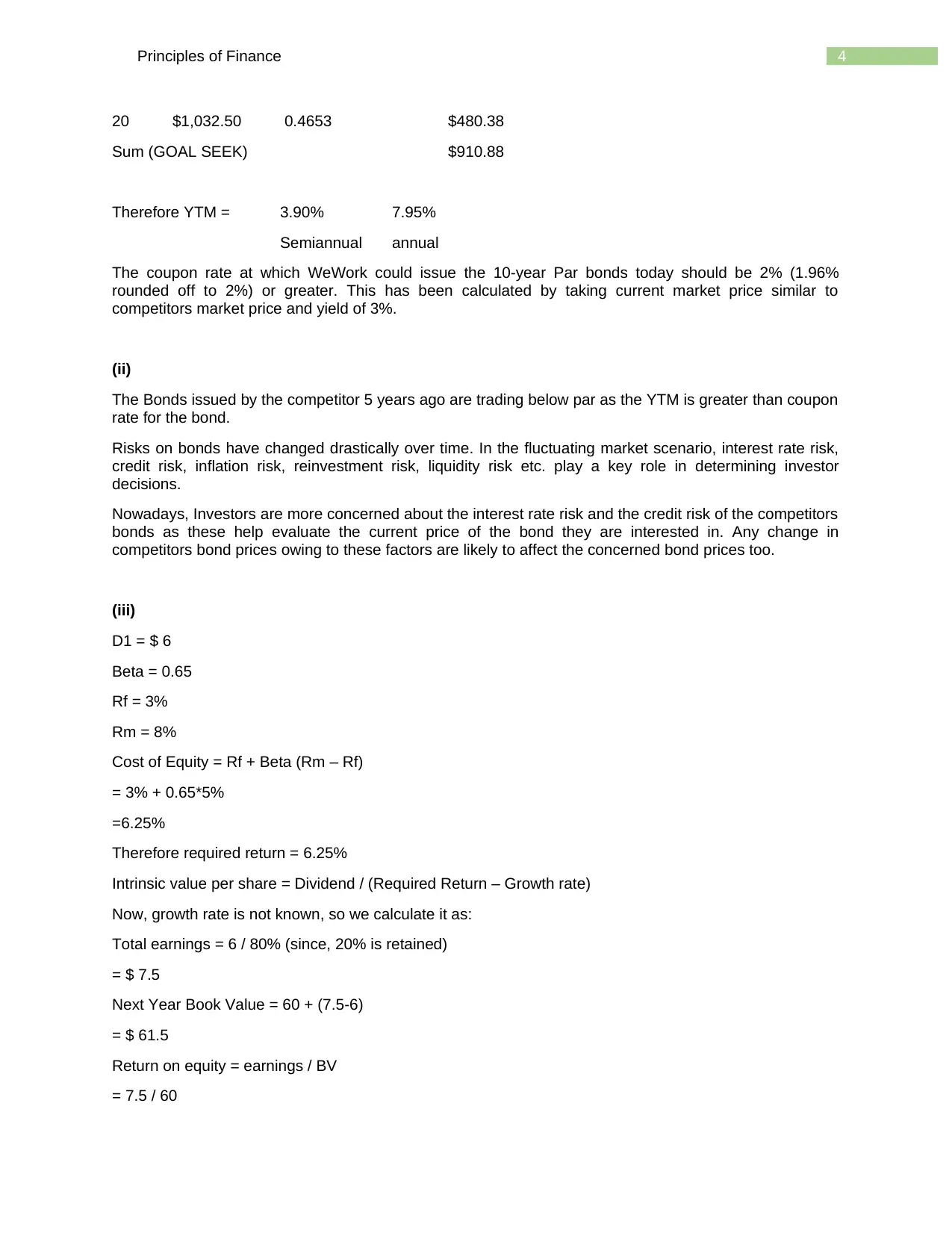

20 $1,032.50 0.4653 $480.38

Sum (GOAL SEEK) $910.88

Therefore YTM = 3.90% 7.95%

Semiannual annual

The coupon rate at which WeWork could issue the 10-year Par bonds today should be 2% (1.96%

rounded off to 2%) or greater. This has been calculated by taking current market price similar to

competitors market price and yield of 3%.

(ii)

The Bonds issued by the competitor 5 years ago are trading below par as the YTM is greater than coupon

rate for the bond.

Risks on bonds have changed drastically over time. In the fluctuating market scenario, interest rate risk,

credit risk, inflation risk, reinvestment risk, liquidity risk etc. play a key role in determining investor

decisions.

Nowadays, Investors are more concerned about the interest rate risk and the credit risk of the competitors

bonds as these help evaluate the current price of the bond they are interested in. Any change in

competitors bond prices owing to these factors are likely to affect the concerned bond prices too.

(iii)

D1 = $ 6

Beta = 0.65

Rf = 3%

Rm = 8%

Cost of Equity = Rf + Beta (Rm – Rf)

= 3% + 0.65*5%

=6.25%

Therefore required return = 6.25%

Intrinsic value per share = Dividend / (Required Return – Growth rate)

Now, growth rate is not known, so we calculate it as:

Total earnings = 6 / 80% (since, 20% is retained)

= $ 7.5

Next Year Book Value = 60 + (7.5-6)

= $ 61.5

Return on equity = earnings / BV

= 7.5 / 60

20 $1,032.50 0.4653 $480.38

Sum (GOAL SEEK) $910.88

Therefore YTM = 3.90% 7.95%

Semiannual annual

The coupon rate at which WeWork could issue the 10-year Par bonds today should be 2% (1.96%

rounded off to 2%) or greater. This has been calculated by taking current market price similar to

competitors market price and yield of 3%.

(ii)

The Bonds issued by the competitor 5 years ago are trading below par as the YTM is greater than coupon

rate for the bond.

Risks on bonds have changed drastically over time. In the fluctuating market scenario, interest rate risk,

credit risk, inflation risk, reinvestment risk, liquidity risk etc. play a key role in determining investor

decisions.

Nowadays, Investors are more concerned about the interest rate risk and the credit risk of the competitors

bonds as these help evaluate the current price of the bond they are interested in. Any change in

competitors bond prices owing to these factors are likely to affect the concerned bond prices too.

(iii)

D1 = $ 6

Beta = 0.65

Rf = 3%

Rm = 8%

Cost of Equity = Rf + Beta (Rm – Rf)

= 3% + 0.65*5%

=6.25%

Therefore required return = 6.25%

Intrinsic value per share = Dividend / (Required Return – Growth rate)

Now, growth rate is not known, so we calculate it as:

Total earnings = 6 / 80% (since, 20% is retained)

= $ 7.5

Next Year Book Value = 60 + (7.5-6)

= $ 61.5

Return on equity = earnings / BV

= 7.5 / 60

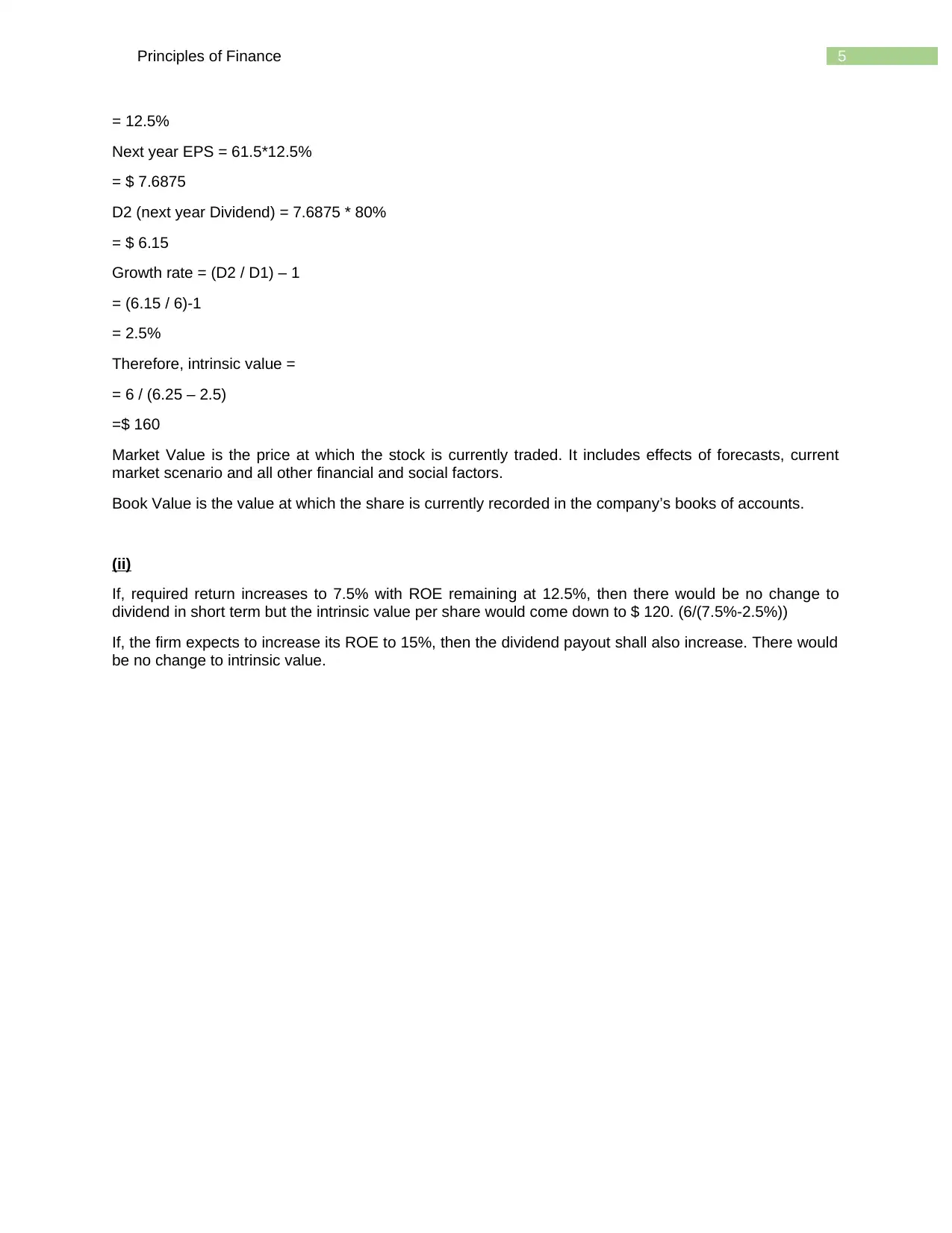

5Principles of Finance

= 12.5%

Next year EPS = 61.5*12.5%

= $ 7.6875

D2 (next year Dividend) = 7.6875 * 80%

= $ 6.15

Growth rate = (D2 / D1) – 1

= (6.15 / 6)-1

= 2.5%

Therefore, intrinsic value =

= 6 / (6.25 – 2.5)

=$ 160

Market Value is the price at which the stock is currently traded. It includes effects of forecasts, current

market scenario and all other financial and social factors.

Book Value is the value at which the share is currently recorded in the company’s books of accounts.

(ii)

If, required return increases to 7.5% with ROE remaining at 12.5%, then there would be no change to

dividend in short term but the intrinsic value per share would come down to $ 120. (6/(7.5%-2.5%))

If, the firm expects to increase its ROE to 15%, then the dividend payout shall also increase. There would

be no change to intrinsic value.

= 12.5%

Next year EPS = 61.5*12.5%

= $ 7.6875

D2 (next year Dividend) = 7.6875 * 80%

= $ 6.15

Growth rate = (D2 / D1) – 1

= (6.15 / 6)-1

= 2.5%

Therefore, intrinsic value =

= 6 / (6.25 – 2.5)

=$ 160

Market Value is the price at which the stock is currently traded. It includes effects of forecasts, current

market scenario and all other financial and social factors.

Book Value is the value at which the share is currently recorded in the company’s books of accounts.

(ii)

If, required return increases to 7.5% with ROE remaining at 12.5%, then there would be no change to

dividend in short term but the intrinsic value per share would come down to $ 120. (6/(7.5%-2.5%))

If, the firm expects to increase its ROE to 15%, then the dividend payout shall also increase. There would

be no change to intrinsic value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6Principles of Finance

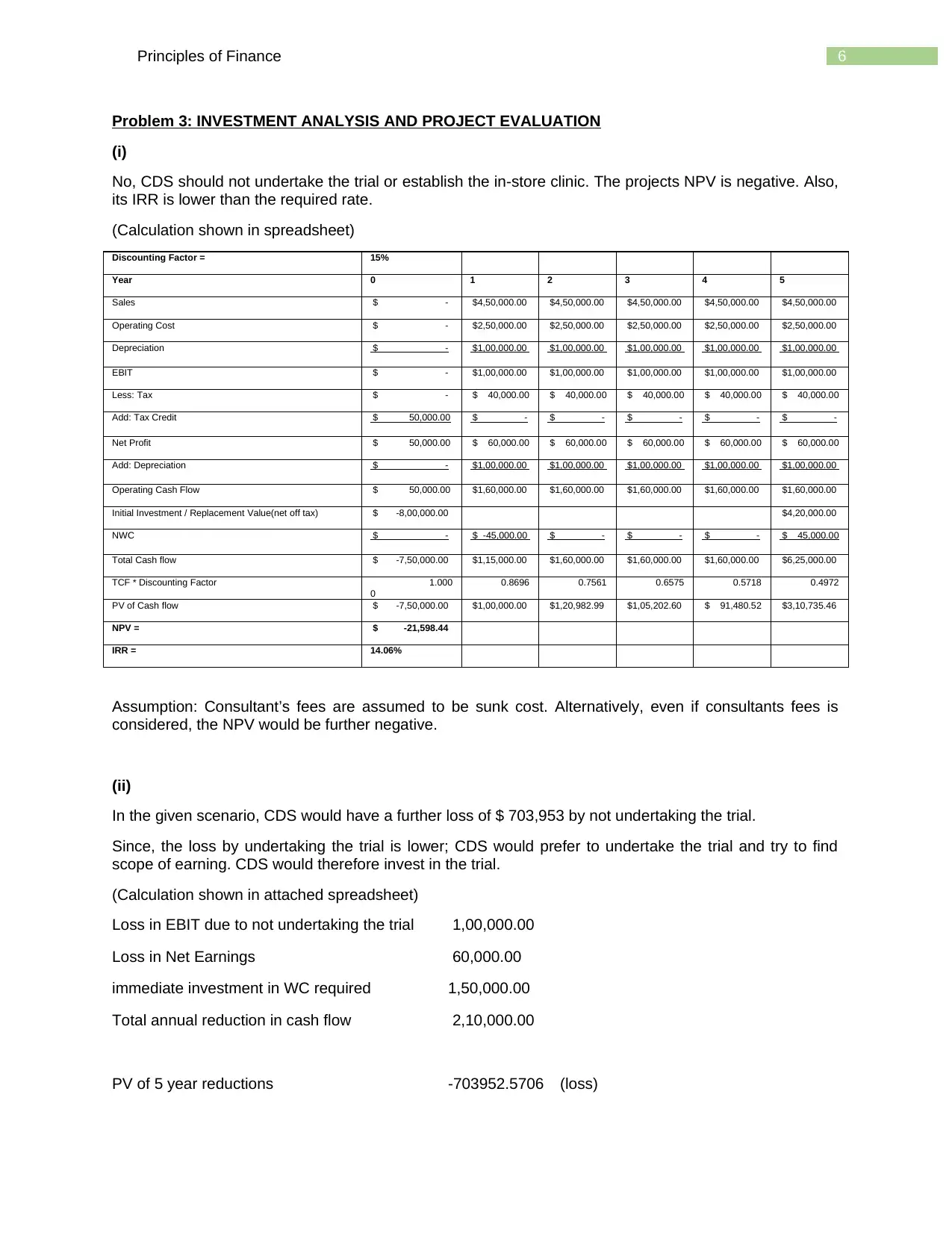

Problem 3: INVESTMENT ANALYSIS AND PROJECT EVALUATION

(i)

No, CDS should not undertake the trial or establish the in-store clinic. The projects NPV is negative. Also,

its IRR is lower than the required rate.

(Calculation shown in spreadsheet)

Discounting Factor = 15%

Year 0 1 2 3 4 5

Sales $ - $4,50,000.00 $4,50,000.00 $4,50,000.00 $4,50,000.00 $4,50,000.00

Operating Cost $ - $2,50,000.00 $2,50,000.00 $2,50,000.00 $2,50,000.00 $2,50,000.00

Depreciation $ - $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00

EBIT $ - $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00

Less: Tax $ - $ 40,000.00 $ 40,000.00 $ 40,000.00 $ 40,000.00 $ 40,000.00

Add: Tax Credit $ 50,000.00 $ - $ - $ - $ - $ -

Net Profit $ 50,000.00 $ 60,000.00 $ 60,000.00 $ 60,000.00 $ 60,000.00 $ 60,000.00

Add: Depreciation $ - $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00

Operating Cash Flow $ 50,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00

Initial Investment / Replacement Value(net off tax) $ -8,00,000.00 $4,20,000.00

NWC $ - $ -45,000.00 $ - $ - $ - $ 45,000.00

Total Cash flow $ -7,50,000.00 $1,15,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00 $6,25,000.00

TCF * Discounting Factor 1.000

0

0.8696 0.7561 0.6575 0.5718 0.4972

PV of Cash flow $ -7,50,000.00 $1,00,000.00 $1,20,982.99 $1,05,202.60 $ 91,480.52 $3,10,735.46

NPV = $ -21,598.44

IRR = 14.06%

Assumption: Consultant’s fees are assumed to be sunk cost. Alternatively, even if consultants fees is

considered, the NPV would be further negative.

(ii)

In the given scenario, CDS would have a further loss of $ 703,953 by not undertaking the trial.

Since, the loss by undertaking the trial is lower; CDS would prefer to undertake the trial and try to find

scope of earning. CDS would therefore invest in the trial.

(Calculation shown in attached spreadsheet)

Loss in EBIT due to not undertaking the trial 1,00,000.00

Loss in Net Earnings 60,000.00

immediate investment in WC required 1,50,000.00

Total annual reduction in cash flow 2,10,000.00

PV of 5 year reductions -703952.5706 (loss)

Problem 3: INVESTMENT ANALYSIS AND PROJECT EVALUATION

(i)

No, CDS should not undertake the trial or establish the in-store clinic. The projects NPV is negative. Also,

its IRR is lower than the required rate.

(Calculation shown in spreadsheet)

Discounting Factor = 15%

Year 0 1 2 3 4 5

Sales $ - $4,50,000.00 $4,50,000.00 $4,50,000.00 $4,50,000.00 $4,50,000.00

Operating Cost $ - $2,50,000.00 $2,50,000.00 $2,50,000.00 $2,50,000.00 $2,50,000.00

Depreciation $ - $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00

EBIT $ - $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00

Less: Tax $ - $ 40,000.00 $ 40,000.00 $ 40,000.00 $ 40,000.00 $ 40,000.00

Add: Tax Credit $ 50,000.00 $ - $ - $ - $ - $ -

Net Profit $ 50,000.00 $ 60,000.00 $ 60,000.00 $ 60,000.00 $ 60,000.00 $ 60,000.00

Add: Depreciation $ - $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00 $1,00,000.00

Operating Cash Flow $ 50,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00

Initial Investment / Replacement Value(net off tax) $ -8,00,000.00 $4,20,000.00

NWC $ - $ -45,000.00 $ - $ - $ - $ 45,000.00

Total Cash flow $ -7,50,000.00 $1,15,000.00 $1,60,000.00 $1,60,000.00 $1,60,000.00 $6,25,000.00

TCF * Discounting Factor 1.000

0

0.8696 0.7561 0.6575 0.5718 0.4972

PV of Cash flow $ -7,50,000.00 $1,00,000.00 $1,20,982.99 $1,05,202.60 $ 91,480.52 $3,10,735.46

NPV = $ -21,598.44

IRR = 14.06%

Assumption: Consultant’s fees are assumed to be sunk cost. Alternatively, even if consultants fees is

considered, the NPV would be further negative.

(ii)

In the given scenario, CDS would have a further loss of $ 703,953 by not undertaking the trial.

Since, the loss by undertaking the trial is lower; CDS would prefer to undertake the trial and try to find

scope of earning. CDS would therefore invest in the trial.

(Calculation shown in attached spreadsheet)

Loss in EBIT due to not undertaking the trial 1,00,000.00

Loss in Net Earnings 60,000.00

immediate investment in WC required 1,50,000.00

Total annual reduction in cash flow 2,10,000.00

PV of 5 year reductions -703952.5706 (loss)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7Principles of Finance

Problem 4:

(i)

Calculation shown in attached spreadsheet.

no. of shares outstanding 40000000

Price per share $75

Value of Equity 3000000000

Cost of Capital (K0) 7.50%

Value of Buyback 40,00,00,000.00

Revised Value of Equity 2,60,00,00,000.00 87% Proportion of equity

Value of Bonds issued 40,00,00,000.00 13% Proportion of Debt

Cost of Debt 4.50%

tax rate 25%

Net Cost of Debt (after tax) 3.375%

Say, 5333333.333 shares were brought at a share price of 75 (assumption)

EPS = MP * Ke

$5.63

Current P/E = 75/5.625

13.33333333

Assuming constant earnings in the current year, i.e.:

EAT = EPS * no. of shares O/s $22,50,00,000.00

EBIT (initially) = $30,00,00,000.00

Interest = $1,80,00,000.00

EBT (now) $28,20,00,000.00

Tax $7,05,00,000.00

EAT $21,15,00,000.00

Problem 4:

(i)

Calculation shown in attached spreadsheet.

no. of shares outstanding 40000000

Price per share $75

Value of Equity 3000000000

Cost of Capital (K0) 7.50%

Value of Buyback 40,00,00,000.00

Revised Value of Equity 2,60,00,00,000.00 87% Proportion of equity

Value of Bonds issued 40,00,00,000.00 13% Proportion of Debt

Cost of Debt 4.50%

tax rate 25%

Net Cost of Debt (after tax) 3.375%

Say, 5333333.333 shares were brought at a share price of 75 (assumption)

EPS = MP * Ke

$5.63

Current P/E = 75/5.625

13.33333333

Assuming constant earnings in the current year, i.e.:

EAT = EPS * no. of shares O/s $22,50,00,000.00

EBIT (initially) = $30,00,00,000.00

Interest = $1,80,00,000.00

EBT (now) $28,20,00,000.00

Tax $7,05,00,000.00

EAT $21,15,00,000.00

8Principles of Finance

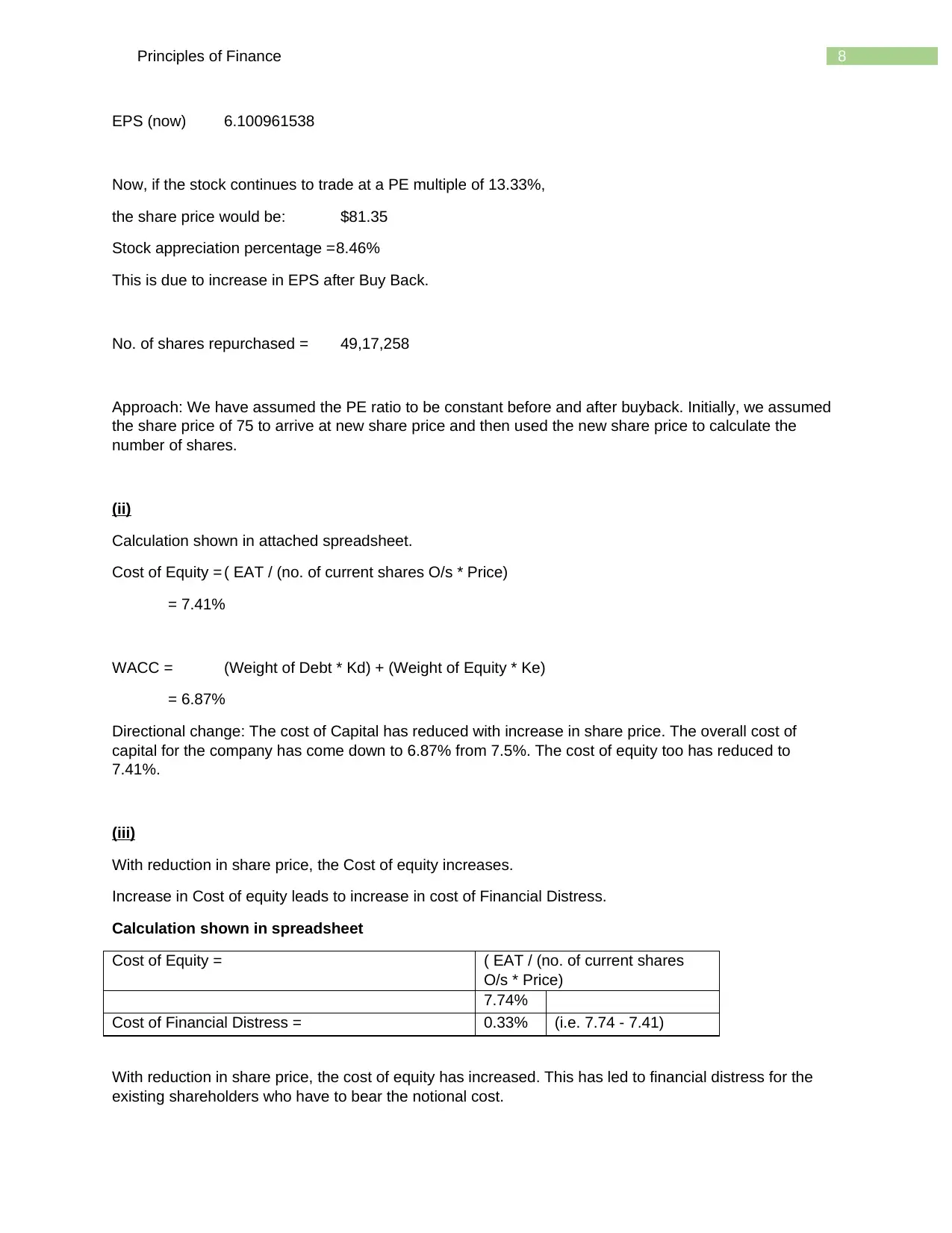

EPS (now) 6.100961538

Now, if the stock continues to trade at a PE multiple of 13.33%,

the share price would be: $81.35

Stock appreciation percentage =8.46%

This is due to increase in EPS after Buy Back.

No. of shares repurchased = 49,17,258

Approach: We have assumed the PE ratio to be constant before and after buyback. Initially, we assumed

the share price of 75 to arrive at new share price and then used the new share price to calculate the

number of shares.

(ii)

Calculation shown in attached spreadsheet.

Cost of Equity = ( EAT / (no. of current shares O/s * Price)

= 7.41%

WACC = (Weight of Debt * Kd) + (Weight of Equity * Ke)

= 6.87%

Directional change: The cost of Capital has reduced with increase in share price. The overall cost of

capital for the company has come down to 6.87% from 7.5%. The cost of equity too has reduced to

7.41%.

(iii)

With reduction in share price, the Cost of equity increases.

Increase in Cost of equity leads to increase in cost of Financial Distress.

Calculation shown in spreadsheet

Cost of Equity = ( EAT / (no. of current shares

O/s * Price)

7.74%

Cost of Financial Distress = 0.33% (i.e. 7.74 - 7.41)

With reduction in share price, the cost of equity has increased. This has led to financial distress for the

existing shareholders who have to bear the notional cost.

EPS (now) 6.100961538

Now, if the stock continues to trade at a PE multiple of 13.33%,

the share price would be: $81.35

Stock appreciation percentage =8.46%

This is due to increase in EPS after Buy Back.

No. of shares repurchased = 49,17,258

Approach: We have assumed the PE ratio to be constant before and after buyback. Initially, we assumed

the share price of 75 to arrive at new share price and then used the new share price to calculate the

number of shares.

(ii)

Calculation shown in attached spreadsheet.

Cost of Equity = ( EAT / (no. of current shares O/s * Price)

= 7.41%

WACC = (Weight of Debt * Kd) + (Weight of Equity * Ke)

= 6.87%

Directional change: The cost of Capital has reduced with increase in share price. The overall cost of

capital for the company has come down to 6.87% from 7.5%. The cost of equity too has reduced to

7.41%.

(iii)

With reduction in share price, the Cost of equity increases.

Increase in Cost of equity leads to increase in cost of Financial Distress.

Calculation shown in spreadsheet

Cost of Equity = ( EAT / (no. of current shares

O/s * Price)

7.74%

Cost of Financial Distress = 0.33% (i.e. 7.74 - 7.41)

With reduction in share price, the cost of equity has increased. This has led to financial distress for the

existing shareholders who have to bear the notional cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9Principles of Finance

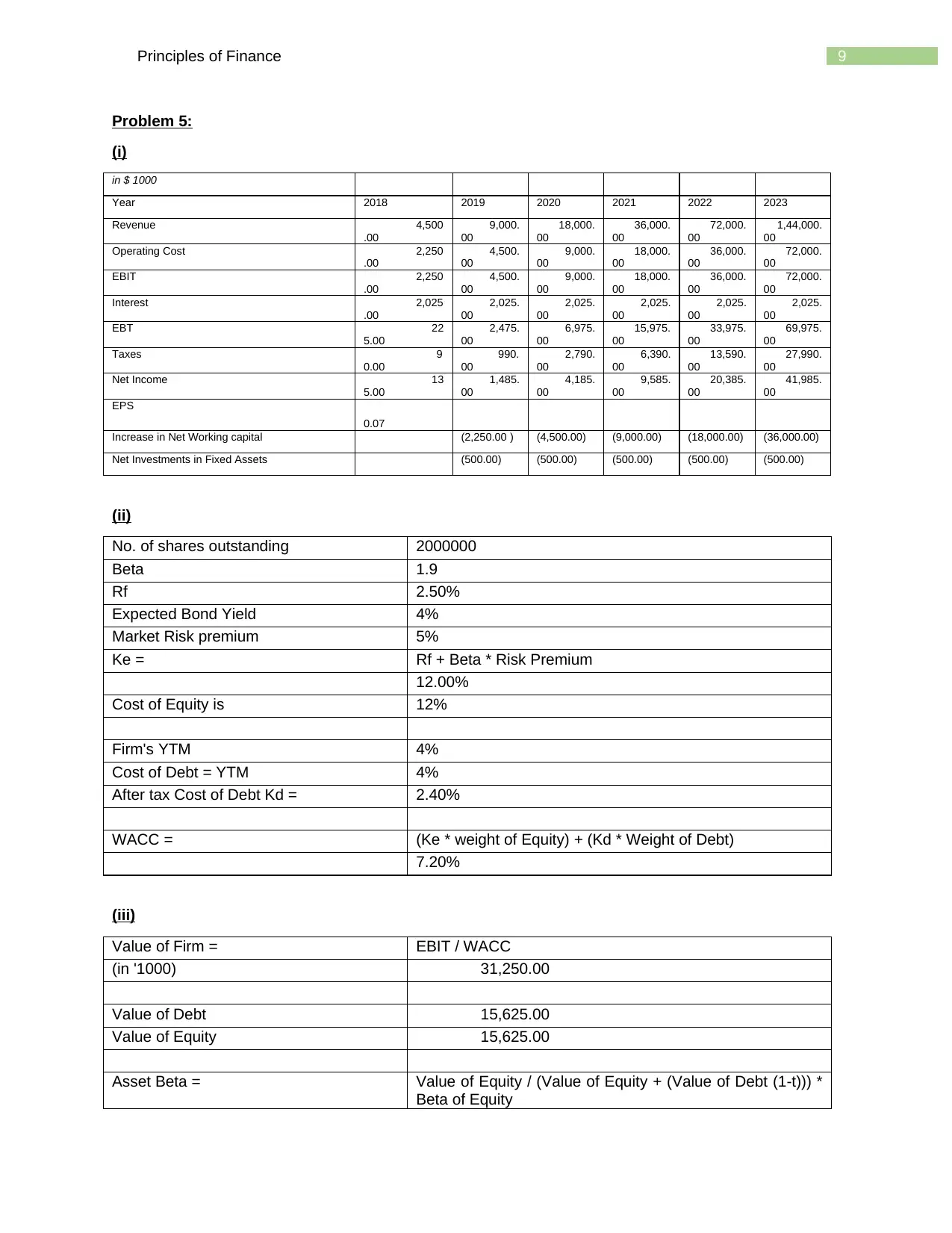

Problem 5:

(i)

in $ 1000

Year 2018 2019 2020 2021 2022 2023

Revenue 4,500

.00

9,000.

00

18,000.

00

36,000.

00

72,000.

00

1,44,000.

00

Operating Cost 2,250

.00

4,500.

00

9,000.

00

18,000.

00

36,000.

00

72,000.

00

EBIT 2,250

.00

4,500.

00

9,000.

00

18,000.

00

36,000.

00

72,000.

00

Interest 2,025

.00

2,025.

00

2,025.

00

2,025.

00

2,025.

00

2,025.

00

EBT 22

5.00

2,475.

00

6,975.

00

15,975.

00

33,975.

00

69,975.

00

Taxes 9

0.00

990.

00

2,790.

00

6,390.

00

13,590.

00

27,990.

00

Net Income 13

5.00

1,485.

00

4,185.

00

9,585.

00

20,385.

00

41,985.

00

EPS

0.07

Increase in Net Working capital (2,250.00 ) (4,500.00) (9,000.00) (18,000.00) (36,000.00)

Net Investments in Fixed Assets (500.00) (500.00) (500.00) (500.00) (500.00)

(ii)

No. of shares outstanding 2000000

Beta 1.9

Rf 2.50%

Expected Bond Yield 4%

Market Risk premium 5%

Ke = Rf + Beta * Risk Premium

12.00%

Cost of Equity is 12%

Firm's YTM 4%

Cost of Debt = YTM 4%

After tax Cost of Debt Kd = 2.40%

WACC = (Ke * weight of Equity) + (Kd * Weight of Debt)

7.20%

(iii)

Value of Firm = EBIT / WACC

(in '1000) 31,250.00

Value of Debt 15,625.00

Value of Equity 15,625.00

Asset Beta = Value of Equity / (Value of Equity + (Value of Debt (1-t))) *

Beta of Equity

Problem 5:

(i)

in $ 1000

Year 2018 2019 2020 2021 2022 2023

Revenue 4,500

.00

9,000.

00

18,000.

00

36,000.

00

72,000.

00

1,44,000.

00

Operating Cost 2,250

.00

4,500.

00

9,000.

00

18,000.

00

36,000.

00

72,000.

00

EBIT 2,250

.00

4,500.

00

9,000.

00

18,000.

00

36,000.

00

72,000.

00

Interest 2,025

.00

2,025.

00

2,025.

00

2,025.

00

2,025.

00

2,025.

00

EBT 22

5.00

2,475.

00

6,975.

00

15,975.

00

33,975.

00

69,975.

00

Taxes 9

0.00

990.

00

2,790.

00

6,390.

00

13,590.

00

27,990.

00

Net Income 13

5.00

1,485.

00

4,185.

00

9,585.

00

20,385.

00

41,985.

00

EPS

0.07

Increase in Net Working capital (2,250.00 ) (4,500.00) (9,000.00) (18,000.00) (36,000.00)

Net Investments in Fixed Assets (500.00) (500.00) (500.00) (500.00) (500.00)

(ii)

No. of shares outstanding 2000000

Beta 1.9

Rf 2.50%

Expected Bond Yield 4%

Market Risk premium 5%

Ke = Rf + Beta * Risk Premium

12.00%

Cost of Equity is 12%

Firm's YTM 4%

Cost of Debt = YTM 4%

After tax Cost of Debt Kd = 2.40%

WACC = (Ke * weight of Equity) + (Kd * Weight of Debt)

7.20%

(iii)

Value of Firm = EBIT / WACC

(in '1000) 31,250.00

Value of Debt 15,625.00

Value of Equity 15,625.00

Asset Beta = Value of Equity / (Value of Equity + (Value of Debt (1-t))) *

Beta of Equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10Principles of Finance

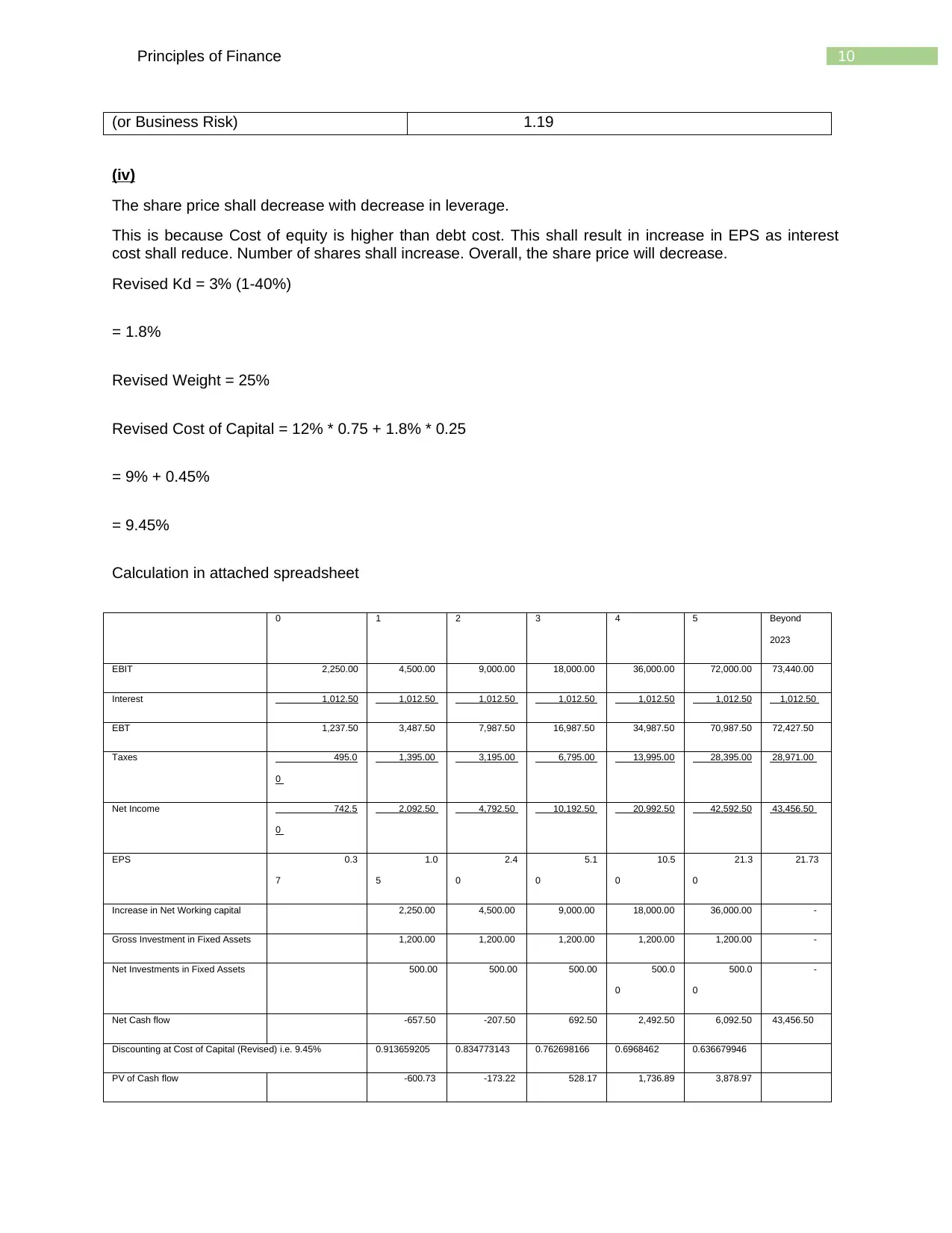

(or Business Risk) 1.19

(iv)

The share price shall decrease with decrease in leverage.

This is because Cost of equity is higher than debt cost. This shall result in increase in EPS as interest

cost shall reduce. Number of shares shall increase. Overall, the share price will decrease.

Revised Kd = 3% (1-40%)

= 1.8%

Revised Weight = 25%

Revised Cost of Capital = 12% * 0.75 + 1.8% * 0.25

= 9% + 0.45%

= 9.45%

Calculation in attached spreadsheet

0 1 2 3 4 5 Beyond

2023

EBIT 2,250.00 4,500.00 9,000.00 18,000.00 36,000.00 72,000.00 73,440.00

Interest 1,012.50 1,012.50 1,012.50 1,012.50 1,012.50 1,012.50 1,012.50

EBT 1,237.50 3,487.50 7,987.50 16,987.50 34,987.50 70,987.50 72,427.50

Taxes 495.0

0

1,395.00 3,195.00 6,795.00 13,995.00 28,395.00 28,971.00

Net Income 742.5

0

2,092.50 4,792.50 10,192.50 20,992.50 42,592.50 43,456.50

EPS 0.3

7

1.0

5

2.4

0

5.1

0

10.5

0

21.3

0

21.73

Increase in Net Working capital 2,250.00 4,500.00 9,000.00 18,000.00 36,000.00 -

Gross Investment in Fixed Assets 1,200.00 1,200.00 1,200.00 1,200.00 1,200.00 -

Net Investments in Fixed Assets 500.00 500.00 500.00 500.0

0

500.0

0

-

Net Cash flow -657.50 -207.50 692.50 2,492.50 6,092.50 43,456.50

Discounting at Cost of Capital (Revised) i.e. 9.45% 0.913659205 0.834773143 0.762698166 0.6968462 0.636679946

PV of Cash flow -600.73 -173.22 528.17 1,736.89 3,878.97

(or Business Risk) 1.19

(iv)

The share price shall decrease with decrease in leverage.

This is because Cost of equity is higher than debt cost. This shall result in increase in EPS as interest

cost shall reduce. Number of shares shall increase. Overall, the share price will decrease.

Revised Kd = 3% (1-40%)

= 1.8%

Revised Weight = 25%

Revised Cost of Capital = 12% * 0.75 + 1.8% * 0.25

= 9% + 0.45%

= 9.45%

Calculation in attached spreadsheet

0 1 2 3 4 5 Beyond

2023

EBIT 2,250.00 4,500.00 9,000.00 18,000.00 36,000.00 72,000.00 73,440.00

Interest 1,012.50 1,012.50 1,012.50 1,012.50 1,012.50 1,012.50 1,012.50

EBT 1,237.50 3,487.50 7,987.50 16,987.50 34,987.50 70,987.50 72,427.50

Taxes 495.0

0

1,395.00 3,195.00 6,795.00 13,995.00 28,395.00 28,971.00

Net Income 742.5

0

2,092.50 4,792.50 10,192.50 20,992.50 42,592.50 43,456.50

EPS 0.3

7

1.0

5

2.4

0

5.1

0

10.5

0

21.3

0

21.73

Increase in Net Working capital 2,250.00 4,500.00 9,000.00 18,000.00 36,000.00 -

Gross Investment in Fixed Assets 1,200.00 1,200.00 1,200.00 1,200.00 1,200.00 -

Net Investments in Fixed Assets 500.00 500.00 500.00 500.0

0

500.0

0

-

Net Cash flow -657.50 -207.50 692.50 2,492.50 6,092.50 43,456.50

Discounting at Cost of Capital (Revised) i.e. 9.45% 0.913659205 0.834773143 0.762698166 0.6968462 0.636679946

PV of Cash flow -600.73 -173.22 528.17 1,736.89 3,878.97

11Principles of Finance

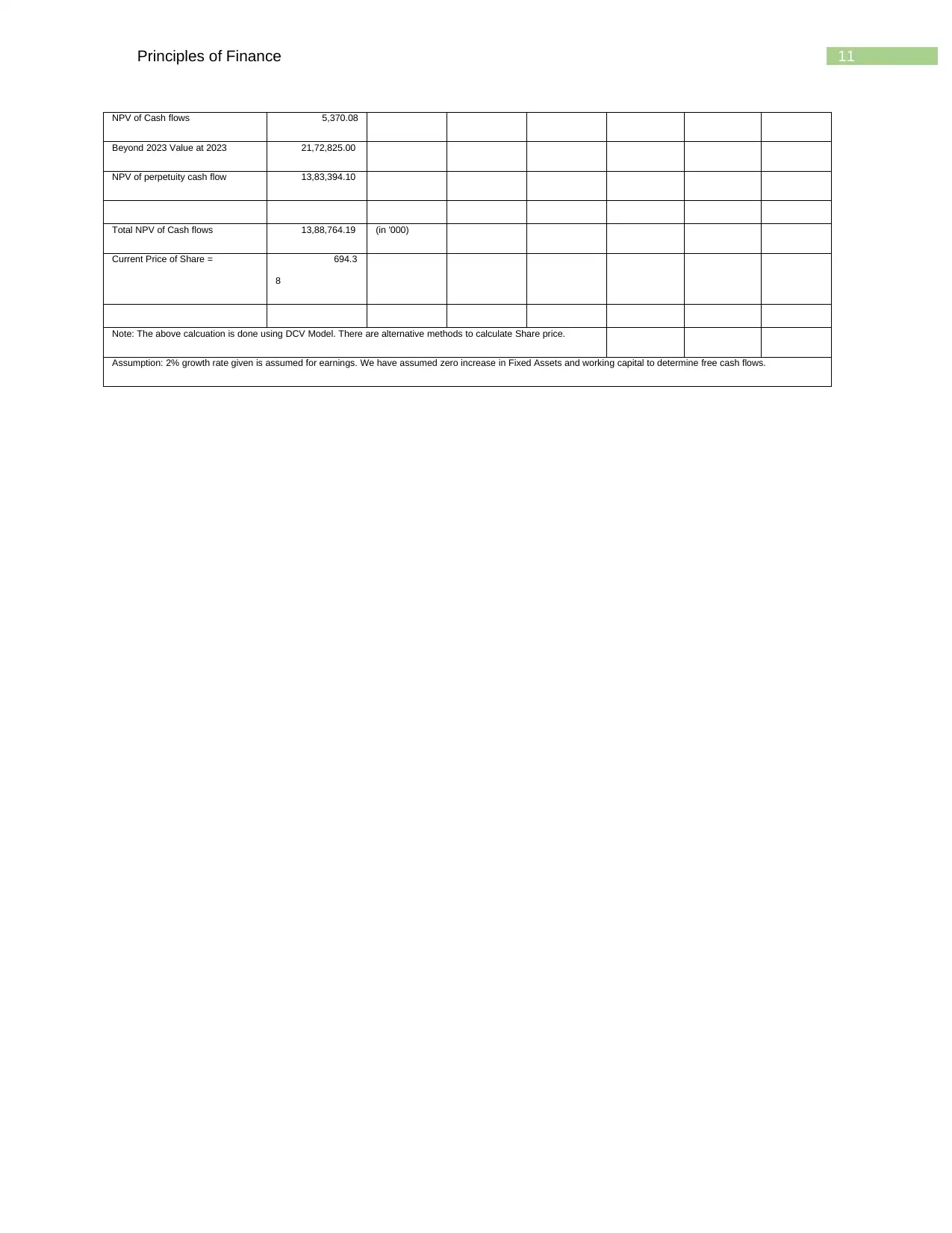

NPV of Cash flows 5,370.08

Beyond 2023 Value at 2023 21,72,825.00

NPV of perpetuity cash flow 13,83,394.10

Total NPV of Cash flows 13,88,764.19 (in '000)

Current Price of Share = 694.3

8

Note: The above calcuation is done using DCV Model. There are alternative methods to calculate Share price.

Assumption: 2% growth rate given is assumed for earnings. We have assumed zero increase in Fixed Assets and working capital to determine free cash flows.

NPV of Cash flows 5,370.08

Beyond 2023 Value at 2023 21,72,825.00

NPV of perpetuity cash flow 13,83,394.10

Total NPV of Cash flows 13,88,764.19 (in '000)

Current Price of Share = 694.3

8

Note: The above calcuation is done using DCV Model. There are alternative methods to calculate Share price.

Assumption: 2% growth rate given is assumed for earnings. We have assumed zero increase in Fixed Assets and working capital to determine free cash flows.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.