Impacts of Future Technological Innovation on Accounting Skills, Ethics, and Career Opportunities

VerifiedAdded on 2023/03/31

|25

|3342

|203

AI Summary

This study evaluates the impacts of future technological innovation on accounting skills, ethics, and career opportunities. It discusses the current and future technology, accounting skills, and ethics, along with the Australian viewpoint on these aspects. The study also highlights the changes and adaptations required in accounting courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Principles of Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction......................................................................................................................................3

Assessment of technology, accounting skills, Ethics and Career Opportunity for those who

pursue accounting careers................................................................................................................3

Current and Future technology....................................................................................................3

Accounting skills and ethics........................................................................................................5

Information that surprised the group...............................................................................................5

Assessment of Australian viewpoint regarding accounting skills, ethics, and career opportunities

along with changes and adaption required to be accepted...............................................................6

Accounting skills.........................................................................................................................6

Ethics...........................................................................................................................................7

Career opportunities.....................................................................................................................8

Conclusion and Recommendations..................................................................................................9

References......................................................................................................................................11

Appendix........................................................................................................................................14

Accountant Job Advertisements................................................................................................14

Minute of Meetings....................................................................................................................24

Introduction......................................................................................................................................3

Assessment of technology, accounting skills, Ethics and Career Opportunity for those who

pursue accounting careers................................................................................................................3

Current and Future technology....................................................................................................3

Accounting skills and ethics........................................................................................................5

Information that surprised the group...............................................................................................5

Assessment of Australian viewpoint regarding accounting skills, ethics, and career opportunities

along with changes and adaption required to be accepted...............................................................6

Accounting skills.........................................................................................................................6

Ethics...........................................................................................................................................7

Career opportunities.....................................................................................................................8

Conclusion and Recommendations..................................................................................................9

References......................................................................................................................................11

Appendix........................................................................................................................................14

Accountant Job Advertisements................................................................................................14

Minute of Meetings....................................................................................................................24

INTRODUCTION

The present study is based on the critical evaluation and analysis of the impacts of future

technological innovation such as artificial intelligence and accounting software automation on

the accountant skills, ethics, and career opportunities, related with several accounting

designations in future. Along with this, the study considers current as well as future technology,

accountant skills, and ethics and career opportunities for the individuals who are in pursuit of the

accounting career. This piece of work also emphasizes on the ethics and career opportunities for

accountants from the viewpoint of Australia, while describing the aspects, changes or adaptation

that are required to be taken into account for the accounting courses.

ASSESSMENT OF TECHNOLOGY, ACCOUNTING SKILLS, ETHICS

AND CAREER OPPORTUNITY FOR THOSE WHO PURSUE

ACCOUNTING CAREERS

Current and Future technology

Artificial Intelligence

As per the World Congress of Accountants (WCOA) in the process of accounting Artificial

Intelligence will quickly split from the element for observance as well as in the direction of

delivery of advice. On the other hand, it will not put back a human accountant (Gunning, 2017).

Furthermore, according to Carole Barney, head of AI research & development programs at Xero

informed the World Congress of Accountants (WCOA) that Artificial Intelligence is on the way

of affecting the jobs of administration as well as in 2019 quick expansion would come in

consideration. (Wilson, et al., 2016). On the other hand, the accountant should not get tensed

about their replacement. Besides that, it is made clear the AI is majorly formed to enhance the

individual those are in the center, according to the Barany (Franklin, 2017). Thus, it could be

accessed that in order to increase the probability of being successful as an accountant, it is

necessary to learn and accept Artificial Intelligence technology.

The present study is based on the critical evaluation and analysis of the impacts of future

technological innovation such as artificial intelligence and accounting software automation on

the accountant skills, ethics, and career opportunities, related with several accounting

designations in future. Along with this, the study considers current as well as future technology,

accountant skills, and ethics and career opportunities for the individuals who are in pursuit of the

accounting career. This piece of work also emphasizes on the ethics and career opportunities for

accountants from the viewpoint of Australia, while describing the aspects, changes or adaptation

that are required to be taken into account for the accounting courses.

ASSESSMENT OF TECHNOLOGY, ACCOUNTING SKILLS, ETHICS

AND CAREER OPPORTUNITY FOR THOSE WHO PURSUE

ACCOUNTING CAREERS

Current and Future technology

Artificial Intelligence

As per the World Congress of Accountants (WCOA) in the process of accounting Artificial

Intelligence will quickly split from the element for observance as well as in the direction of

delivery of advice. On the other hand, it will not put back a human accountant (Gunning, 2017).

Furthermore, according to Carole Barney, head of AI research & development programs at Xero

informed the World Congress of Accountants (WCOA) that Artificial Intelligence is on the way

of affecting the jobs of administration as well as in 2019 quick expansion would come in

consideration. (Wilson, et al., 2016). On the other hand, the accountant should not get tensed

about their replacement. Besides that, it is made clear the AI is majorly formed to enhance the

individual those are in the center, according to the Barany (Franklin, 2017). Thus, it could be

accessed that in order to increase the probability of being successful as an accountant, it is

necessary to learn and accept Artificial Intelligence technology.

DIY" Cloud Accounting Software

The growing DIY" Cloud Accounting Software that helps in simplifying the traditional

accounting management is not only popular as other technologies but also has a great influence

on the market on a daily basis towards accounting professionals (Ramchand, Chhetri, and

Kowalczyk, 2017). Although such reasonable priced DIY" Cloud Accounting Software can

reduce the book work for small companies, on the other hand in small business, also they need

financial advice which can only be provided by experts (Karamatova, 2017). Such professionals

have knowledge about both technical as well as regulatory services however which is essential

for an accountant in various aspects like it makes solutions easy in the leading bookkeeping that

can be accepted by clients as well as to be their go-to expert for such sets (Nyberg, 2019). Thus,

through accepting this technology accountant can accomplish their obligations in a fast and easy

manner.

Cryptocurrencies, Blockchain, and Distributed Ledgers

It is obvious that financial technologies are not getting completed without the rising stars of

2017s like bitcoin, cryptocurrencies and the knowledge that strengthens them, i.e. blockchain and

distributed ledgers (Davidson, De Filippi, and Potts, 2016). Whilst cryptocurrencies pretense

their own possessed confronts for accountants that are described in the Digital Currencies of

2015: Where to from here? report particularly with regards to auditing, fraud detection, taxation

along with money-laundering, in spite of their dramatic rise in fiscal values and media

concentration, cryptocurrencies are improbable to go normal in 2018, as per the international

monetary firm UBS (Gong, 2017).

On the other hand, distributed ledger, as well as blockchain technologies, are connected with

much broader insinuation for the upcoming future. According to the discussion of 2017

report The Future of Blockchain, discrete ledgers ( that operates as "cooperative databases" in

which information is detained by numerous computers immediately) endorse sharing,

confirmation, and trust, as lots of computers have to have the same opinion for data edit, and all

computers uphold a documentation of all changes that are made. Moreover, such characteristic

has direct towards some referring to the blockchain as "Triple-Entry Bookkeeping,"10 even

The growing DIY" Cloud Accounting Software that helps in simplifying the traditional

accounting management is not only popular as other technologies but also has a great influence

on the market on a daily basis towards accounting professionals (Ramchand, Chhetri, and

Kowalczyk, 2017). Although such reasonable priced DIY" Cloud Accounting Software can

reduce the book work for small companies, on the other hand in small business, also they need

financial advice which can only be provided by experts (Karamatova, 2017). Such professionals

have knowledge about both technical as well as regulatory services however which is essential

for an accountant in various aspects like it makes solutions easy in the leading bookkeeping that

can be accepted by clients as well as to be their go-to expert for such sets (Nyberg, 2019). Thus,

through accepting this technology accountant can accomplish their obligations in a fast and easy

manner.

Cryptocurrencies, Blockchain, and Distributed Ledgers

It is obvious that financial technologies are not getting completed without the rising stars of

2017s like bitcoin, cryptocurrencies and the knowledge that strengthens them, i.e. blockchain and

distributed ledgers (Davidson, De Filippi, and Potts, 2016). Whilst cryptocurrencies pretense

their own possessed confronts for accountants that are described in the Digital Currencies of

2015: Where to from here? report particularly with regards to auditing, fraud detection, taxation

along with money-laundering, in spite of their dramatic rise in fiscal values and media

concentration, cryptocurrencies are improbable to go normal in 2018, as per the international

monetary firm UBS (Gong, 2017).

On the other hand, distributed ledger, as well as blockchain technologies, are connected with

much broader insinuation for the upcoming future. According to the discussion of 2017

report The Future of Blockchain, discrete ledgers ( that operates as "cooperative databases" in

which information is detained by numerous computers immediately) endorse sharing,

confirmation, and trust, as lots of computers have to have the same opinion for data edit, and all

computers uphold a documentation of all changes that are made. Moreover, such characteristic

has direct towards some referring to the blockchain as "Triple-Entry Bookkeeping,"10 even

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

though the term's suitability has come beneath several discussions (Mainelli, and Smith, 2015). It

could be accessed that above-specified technology has widened the scope of an accountant and

increased its responsibilities as well.

Accounting skills and ethics

It is very obvious that to perform any kind of job; soft skills are very helpful in the place of work

and besides that to perform the specific jobs, there is a greater need of technical skills. In the

same manner in accountancy, soft skills are general skill that is acquired by the experts for

developing the specific program of accounting (West, 2017) According to assessment of U.S.

Bureau of Labor Statistics accountant is supposed to have a following soft skills, i.e. strong oral

and written communication, attention and management of important information, systematic and

decision making aptitude, system and time management, decisive and active learning,

Mathematical and deductive way of thinking, knowledge of accounting as well as expertise in

Microsoft Office Suite (Gerstein, Winter and Hertz, 2016.)

Work related to finance is done by the auditors as well as an accountant. They manage the huge

information and facts correctly and effectively. Therefore, it is important for them to have

knowledge about the budgeting software, financial management as well as their procedures of

accounting and Generally Accepted Accounting Principles (GAAP). People those are going for

their career in accounting must have technical skills relating to evaluation and financial

reporting, tax management software and financial statements, software compliance, settlement of

accounts , project management software, the software’s for spreadsheet, database reporting

software as well as business resource planning software’s (Tang, 2017).

INFORMATION THAT SURPRISED THE GROUP

The manner in which technologies have to widen the scope of the accountant’s responsibilities

surprised the members of the group. As it is no more limited to entering transactions and making

financial reports. Application of technology such as cloud software and their online datasets

makes it simpler than ever to interpret the significant financial facts towards clients as well as

allow the authority to connect with their recommendation and proficiency. On the other hand,

accounting skills and ethics assists in enhancing communication at the place of work and also

could be accessed that above-specified technology has widened the scope of an accountant and

increased its responsibilities as well.

Accounting skills and ethics

It is very obvious that to perform any kind of job; soft skills are very helpful in the place of work

and besides that to perform the specific jobs, there is a greater need of technical skills. In the

same manner in accountancy, soft skills are general skill that is acquired by the experts for

developing the specific program of accounting (West, 2017) According to assessment of U.S.

Bureau of Labor Statistics accountant is supposed to have a following soft skills, i.e. strong oral

and written communication, attention and management of important information, systematic and

decision making aptitude, system and time management, decisive and active learning,

Mathematical and deductive way of thinking, knowledge of accounting as well as expertise in

Microsoft Office Suite (Gerstein, Winter and Hertz, 2016.)

Work related to finance is done by the auditors as well as an accountant. They manage the huge

information and facts correctly and effectively. Therefore, it is important for them to have

knowledge about the budgeting software, financial management as well as their procedures of

accounting and Generally Accepted Accounting Principles (GAAP). People those are going for

their career in accounting must have technical skills relating to evaluation and financial

reporting, tax management software and financial statements, software compliance, settlement of

accounts , project management software, the software’s for spreadsheet, database reporting

software as well as business resource planning software’s (Tang, 2017).

INFORMATION THAT SURPRISED THE GROUP

The manner in which technologies have to widen the scope of the accountant’s responsibilities

surprised the members of the group. As it is no more limited to entering transactions and making

financial reports. Application of technology such as cloud software and their online datasets

makes it simpler than ever to interpret the significant financial facts towards clients as well as

allow the authority to connect with their recommendation and proficiency. On the other hand,

accounting skills and ethics assists in enhancing communication at the place of work and also

helps in managing a team of different workers (West, 2017.). The fact that accountants also have

to comply with the code of ethics and conducts while taking a decision at work also surprised the

members as they were not aware of the same. The same represents that as professional

accountants also have to comply with ethics so that they can make moral decisions.

ASSESSMENT OF AUSTRALIAN VIEWPOINT REGARDING

ACCOUNTING SKILLS, ETHICS, AND CAREER OPPORTUNITIES

ALONG WITH CHANGES AND ADAPTION REQUIRED TO BE

ACCEPTED

Accounting skills

Accounting faces big challenges as it strives to consider and define reliable skills, abilities, and

knowledge in the ever-evolving world. It can be stated that technological innovation engaged

with AI, big data, automatic and the changing contexts of economy, society, culture, and politics

wherein accountants work, call for a broad variety of qualified transferrable skills as well as

inter-cultural fluency(Pan, & Seow, 2016). It has been evidenced that in audit and assurance,

practices are highly changing, because of the data analytics and the potential that is offered by

big data and innovative technologies. The manners by which resourcing of audit practices are

done are also evolving, with offshoring turning out to be a more general and higher requirement

of new skills from the side of accountants. In terms of financial reporting, organizations are

facing higher pressure from regulatory bodies to seek improvements in the quality of audits and

the revelation of professional skepticism. For staying viable and reliable, auditors are required to

consider new aspects of external reporting that need non-financial information assurance

(O'Connell and et al. 2015). Acting in the best interest of public and ethical conduct are

overarching jobs of accounting professionals, these tasks need particular individual capabilities,

culture, technical skills, and organizational infrastructure. In consideration with the individual

and organizational complex ethical conduct; there is a demand for multidisciplinary insights for

developing a suitable understanding and valuable models of accounting ethics (Watty, McKay, &

Ngo, 2016).

to comply with the code of ethics and conducts while taking a decision at work also surprised the

members as they were not aware of the same. The same represents that as professional

accountants also have to comply with ethics so that they can make moral decisions.

ASSESSMENT OF AUSTRALIAN VIEWPOINT REGARDING

ACCOUNTING SKILLS, ETHICS, AND CAREER OPPORTUNITIES

ALONG WITH CHANGES AND ADAPTION REQUIRED TO BE

ACCEPTED

Accounting skills

Accounting faces big challenges as it strives to consider and define reliable skills, abilities, and

knowledge in the ever-evolving world. It can be stated that technological innovation engaged

with AI, big data, automatic and the changing contexts of economy, society, culture, and politics

wherein accountants work, call for a broad variety of qualified transferrable skills as well as

inter-cultural fluency(Pan, & Seow, 2016). It has been evidenced that in audit and assurance,

practices are highly changing, because of the data analytics and the potential that is offered by

big data and innovative technologies. The manners by which resourcing of audit practices are

done are also evolving, with offshoring turning out to be a more general and higher requirement

of new skills from the side of accountants. In terms of financial reporting, organizations are

facing higher pressure from regulatory bodies to seek improvements in the quality of audits and

the revelation of professional skepticism. For staying viable and reliable, auditors are required to

consider new aspects of external reporting that need non-financial information assurance

(O'Connell and et al. 2015). Acting in the best interest of public and ethical conduct are

overarching jobs of accounting professionals, these tasks need particular individual capabilities,

culture, technical skills, and organizational infrastructure. In consideration with the individual

and organizational complex ethical conduct; there is a demand for multidisciplinary insights for

developing a suitable understanding and valuable models of accounting ethics (Watty, McKay, &

Ngo, 2016).

The technological skills, abilities, and knowledge, ethical competency, as well as the

professional technical and ethical quotient of accountant in Australia, stay as the prime quality

ensuring their overall success. Furthermore, these skills will contain not only the tax and

accounting but also the skills regarding risk as well as governance (Rikhardsson & Yigitbasioglu,

2018) . Additionally, professional accounts will be required

to state the interpersonal skills, conduct, and qualities, in the future to establish more of

networking skills.

Ethics

Ethical conduct is a key trait for professional accountants. The core principles for accountants set

out by the International Ethics Standards Board for Accountants (IESBA) are applicable and

reasonable in the digital age, which is inclusive of Integrity, Objectivity, Professional

Competence and due care, and Confidentiality and Professional behavior (West, 2018).

APES 110 Code of Ethics for Professional Accountants (Code) has been set out by the

Accounting Professional and Ethical Standards Board (APESB). APESB is stated as an

independent body developed in the year 2006, being and Chartered Accountants in Australia and

New Zealand and CPA Australia’s major initiative. The members of APESB are CPA Australia

and Chartered Accountants ANZ and the Institute of Public Accountants (Payne and et al. 2019).

Further, the APESB aims to establish and develop professionally as well as ethical standards in

the best interest of the public that is applicable to the CPA Australian members and other two

accounting bodies of Australia. The basic principles of the professional accountants are

described as below:

Integrity: In this principle, all accountants are required to act in a straightforward, fair, and

honest way in terms of their business as well as professional relationships.

Objectivity: Accountant shall never allow biases, undue influence of others for overruling

professional judgments while avoiding conflict of interest (CPA, 2019).

Professional competence and due care: Accountants are required to maintain business skills and

professional skills at the level for the objective to ensure that a client derives competent

professional services which are in accordance with relevant technical and professional standards.

professional technical and ethical quotient of accountant in Australia, stay as the prime quality

ensuring their overall success. Furthermore, these skills will contain not only the tax and

accounting but also the skills regarding risk as well as governance (Rikhardsson & Yigitbasioglu,

2018) . Additionally, professional accounts will be required

to state the interpersonal skills, conduct, and qualities, in the future to establish more of

networking skills.

Ethics

Ethical conduct is a key trait for professional accountants. The core principles for accountants set

out by the International Ethics Standards Board for Accountants (IESBA) are applicable and

reasonable in the digital age, which is inclusive of Integrity, Objectivity, Professional

Competence and due care, and Confidentiality and Professional behavior (West, 2018).

APES 110 Code of Ethics for Professional Accountants (Code) has been set out by the

Accounting Professional and Ethical Standards Board (APESB). APESB is stated as an

independent body developed in the year 2006, being and Chartered Accountants in Australia and

New Zealand and CPA Australia’s major initiative. The members of APESB are CPA Australia

and Chartered Accountants ANZ and the Institute of Public Accountants (Payne and et al. 2019).

Further, the APESB aims to establish and develop professionally as well as ethical standards in

the best interest of the public that is applicable to the CPA Australian members and other two

accounting bodies of Australia. The basic principles of the professional accountants are

described as below:

Integrity: In this principle, all accountants are required to act in a straightforward, fair, and

honest way in terms of their business as well as professional relationships.

Objectivity: Accountant shall never allow biases, undue influence of others for overruling

professional judgments while avoiding conflict of interest (CPA, 2019).

Professional competence and due care: Accountants are required to maintain business skills and

professional skills at the level for the objective to ensure that a client derives competent

professional services which are in accordance with relevant technical and professional standards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Confidentiality: It is significant to give priority to confidential information acquired as a

conclusion of business relationships, it is the responsibility of account to not to disclose any

information to the third party in the absence of consent. Under this principle, accountants are

obliged to prevent; revealing the confidential information to external parties, using

confidentiality of information attained on a business account and professional relationships for

the individual benefit (APESB, 2018).

Professional behavior: This principle is engaged with the duties that are implied on all members

to meet the considerable regulations and rules while avoiding any action that can potentially

disrepute the profession. It is essential that accountant make full compliance towards the

reasonable laws, rules, and regulation, with acting professionally and good interest for the public.

In terms of ethical conflict resolution, a member might be capable of addressing ethical

situations and are needed to resolve a conflict in compliance with the fundamental principles

mentioned above. For resolving the ethical conflict, the factors which are relevant for the

accountants are relevant facts, involved ethical issues, basic principles regarding the matter in

questions, set internal procedure, and alternative action courses. It is integral that accountants

consider all such relevant factors while identifying the suitable action course, putting weight on

outcomes of each potential course of action and if or if not other individuals and those entitled

with governance must be consulted (Sheehan & Schmidt, 2015). It has been stated under

Paragraph 100.22, that members must act in the best interest of the public, for the matter of the

issues, the discussion detailers and the decisions which are considered in regards with the issue

are required to be determined. In a situation where an important conflict is not able to be

resolved, then under paragraph 100.21, it has been stated that the members might take into the

account the acquiring professional consultancy from the reliable, professional accounting bodies

or the legal advisors, while making sure that there is no breach of the fundamental principle of

confidentiality. Furthermore, this can be attained by the discussion of issues based anonymously

with the professional bodies or as per the protection of legal rights with the legal advisor. In a

situation where all such reliable possibilities are exhausted, and still the ethical conflict stays as

unresolved, then, in this case, the member is required to refuse to stay as associated with the

issue that is forming the conflict. Additionally, the described principles which are applicable to

conclusion of business relationships, it is the responsibility of account to not to disclose any

information to the third party in the absence of consent. Under this principle, accountants are

obliged to prevent; revealing the confidential information to external parties, using

confidentiality of information attained on a business account and professional relationships for

the individual benefit (APESB, 2018).

Professional behavior: This principle is engaged with the duties that are implied on all members

to meet the considerable regulations and rules while avoiding any action that can potentially

disrepute the profession. It is essential that accountant make full compliance towards the

reasonable laws, rules, and regulation, with acting professionally and good interest for the public.

In terms of ethical conflict resolution, a member might be capable of addressing ethical

situations and are needed to resolve a conflict in compliance with the fundamental principles

mentioned above. For resolving the ethical conflict, the factors which are relevant for the

accountants are relevant facts, involved ethical issues, basic principles regarding the matter in

questions, set internal procedure, and alternative action courses. It is integral that accountants

consider all such relevant factors while identifying the suitable action course, putting weight on

outcomes of each potential course of action and if or if not other individuals and those entitled

with governance must be consulted (Sheehan & Schmidt, 2015). It has been stated under

Paragraph 100.22, that members must act in the best interest of the public, for the matter of the

issues, the discussion detailers and the decisions which are considered in regards with the issue

are required to be determined. In a situation where an important conflict is not able to be

resolved, then under paragraph 100.21, it has been stated that the members might take into the

account the acquiring professional consultancy from the reliable, professional accounting bodies

or the legal advisors, while making sure that there is no breach of the fundamental principle of

confidentiality. Furthermore, this can be attained by the discussion of issues based anonymously

with the professional bodies or as per the protection of legal rights with the legal advisor. In a

situation where all such reliable possibilities are exhausted, and still the ethical conflict stays as

unresolved, then, in this case, the member is required to refuse to stay as associated with the

issue that is forming the conflict. Additionally, the described principles which are applicable to

all of the members, and the specified requirement provided by the Code for the members in the

interest and practice of the public should be followed.

Career opportunities

Career opportunities that are accessible to the highly qualified accountants are inclusive of

management, tax, auditing, financial control, business services, insolvency, financial, corporate,

funds, costs, forensic. Australia has two major professional accounting bodies, and an

accountant for gaining a competitive edge must aim to turn out to be a member of the bodies

after the graduation (Ahmad, Ismail, and Anantharaman, 2015). There are several accounting

careers which can be pursued including, accounts clerk, auditor, bookkeeper, business service

accounting, Chief Financial Officer (CFO), corporate accounting, cost accounting, financial

accounting, financial controllers, forensic accounting, fund accounting, group accounting,

graduate accountant, insolvency accounting, management accounting, mine accounting project,

accounting, revenue accounting and tax accounting. The opportunities available to the

accountant are:

Chartered Accountant: For becoming a Chartered Accountant (CA), the individual pursuing the

same is required to obtained an accounting degree by the Chartered Accountants Australia New

Zealand (Chartered Accountants ANZ, and also required to fulfill the overall CA program, while

passing the needed examinations and tests, along with doing approved employment of 3 years.

CPA: For qualifying as a Certified Practising Accountant (CPA), the person pursuing the same

is required to obtain an accounting degree that is completely recognized by the CPA Australia,

while finishing the Practical Experience Requirement and other requirements for study with

passing all the eligible examinations. In addition, there are key three study options made

available by the CPA programs, including a combined postgraduate degree, distance learning,

and full-time study.

Other roles: The roles in demand for accountants are including of the mid-level management of

technological positions. In terms of accounting, there is more demand for financial business

analytics and those with higher experience in governance.

interest and practice of the public should be followed.

Career opportunities

Career opportunities that are accessible to the highly qualified accountants are inclusive of

management, tax, auditing, financial control, business services, insolvency, financial, corporate,

funds, costs, forensic. Australia has two major professional accounting bodies, and an

accountant for gaining a competitive edge must aim to turn out to be a member of the bodies

after the graduation (Ahmad, Ismail, and Anantharaman, 2015). There are several accounting

careers which can be pursued including, accounts clerk, auditor, bookkeeper, business service

accounting, Chief Financial Officer (CFO), corporate accounting, cost accounting, financial

accounting, financial controllers, forensic accounting, fund accounting, group accounting,

graduate accountant, insolvency accounting, management accounting, mine accounting project,

accounting, revenue accounting and tax accounting. The opportunities available to the

accountant are:

Chartered Accountant: For becoming a Chartered Accountant (CA), the individual pursuing the

same is required to obtained an accounting degree by the Chartered Accountants Australia New

Zealand (Chartered Accountants ANZ, and also required to fulfill the overall CA program, while

passing the needed examinations and tests, along with doing approved employment of 3 years.

CPA: For qualifying as a Certified Practising Accountant (CPA), the person pursuing the same

is required to obtain an accounting degree that is completely recognized by the CPA Australia,

while finishing the Practical Experience Requirement and other requirements for study with

passing all the eligible examinations. In addition, there are key three study options made

available by the CPA programs, including a combined postgraduate degree, distance learning,

and full-time study.

Other roles: The roles in demand for accountants are including of the mid-level management of

technological positions. In terms of accounting, there is more demand for financial business

analytics and those with higher experience in governance.

CONCLUSION AND RECOMMENDATIONS

On the basis of the above analysis, it can be concluded that future technological innovation, such

as AI and automation can help an accountant in delivering benefits in practice. However, they

can also come up with various impacts, implication, challenges, as well as opportunities. It can

be recommended that professional accountants are required to consider the aspects such as

building understanding and skills of emerging technologies and digital issues, integrating process

control in aligned with strategic views, monitoring measures for the reporting of non-ethical

behavior. Since accountants will make increased use of innovative and sophisticated

technologies to improvise their practicing, and ways of working, for this aspect, have to enhance

their skills and replace their traditional approach with the new and digital aspects. It is also

recommended that future accountants must increase their education in digital technology and

changing regulations, new types of company accounting, etc. Thus, these following aspects are

required to be considered as they navigate ethical issues in the future technological age.

On the basis of the above analysis, it can be concluded that future technological innovation, such

as AI and automation can help an accountant in delivering benefits in practice. However, they

can also come up with various impacts, implication, challenges, as well as opportunities. It can

be recommended that professional accountants are required to consider the aspects such as

building understanding and skills of emerging technologies and digital issues, integrating process

control in aligned with strategic views, monitoring measures for the reporting of non-ethical

behavior. Since accountants will make increased use of innovative and sophisticated

technologies to improvise their practicing, and ways of working, for this aspect, have to enhance

their skills and replace their traditional approach with the new and digital aspects. It is also

recommended that future accountants must increase their education in digital technology and

changing regulations, new types of company accounting, etc. Thus, these following aspects are

required to be considered as they navigate ethical issues in the future technological age.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Ahmad, Z., Ismail, H. and Anantharaman, R.N., 2015. To be or not to be: an investigation of

accounting students’ career intentions. Education+ Training, 57(3), pp.360-376.

Davidson, S., De Filippi, P. and Potts, J., 2016. Disrupting governance: The new institutional

economics of distributed ledger technology. Available at SSRN 2811995.

Franklin, M.A., 2017. Integration of Ethics into the Introductory Accounting Course Through Active

Learning. ASBBS Proceedings, 24(1), p.199.

Gerstein, M., Winter, E. and Hertz, S., 2016. Teaching accounting ethics: a problem-based learning

approach. Journal of Accounting, Ethics and Public Policy, 17(1).

Gong, J.J., 2017. Ethics in Accounting: A Decision-Making Approach.

Gunning, D., 2017. Explainable artificial intelligence (xai). Defense Advanced Research Projects

Agency (DARPA), nd Web.

Karamatova, L., 2017. Management Accounting and ERP Systems: Factors behind the Choice of

Information Systems when Exercising Management Accounting.

Mainelli, M. and Smith, M., 2015. Sharing ledgers for sharing economies: an exploration of mutual

distributed ledgers (aka blockchain technology). Journal of Financial Perspectives, 3(3).

Nyberg, C., 2019. Intuit, Inc.’s Small Business and Self Employed Unit: A Strategic Analysis

O'Connell, B., Carnegie, G., Carter, A., de Lange, P., Hancock, P., Helliar, C., and Watty, K. 2015.

Shaping the future of accounting in business education in Australia.

Pan, G., and Seow, P. S. 2015. Preparing accounting graduates for digital revolution: A critical review

of information technology competencies and skills development. Journal of Education for

Business, 91(3), 166-175.

Books and Journals

Ahmad, Z., Ismail, H. and Anantharaman, R.N., 2015. To be or not to be: an investigation of

accounting students’ career intentions. Education+ Training, 57(3), pp.360-376.

Davidson, S., De Filippi, P. and Potts, J., 2016. Disrupting governance: The new institutional

economics of distributed ledger technology. Available at SSRN 2811995.

Franklin, M.A., 2017. Integration of Ethics into the Introductory Accounting Course Through Active

Learning. ASBBS Proceedings, 24(1), p.199.

Gerstein, M., Winter, E. and Hertz, S., 2016. Teaching accounting ethics: a problem-based learning

approach. Journal of Accounting, Ethics and Public Policy, 17(1).

Gong, J.J., 2017. Ethics in Accounting: A Decision-Making Approach.

Gunning, D., 2017. Explainable artificial intelligence (xai). Defense Advanced Research Projects

Agency (DARPA), nd Web.

Karamatova, L., 2017. Management Accounting and ERP Systems: Factors behind the Choice of

Information Systems when Exercising Management Accounting.

Mainelli, M. and Smith, M., 2015. Sharing ledgers for sharing economies: an exploration of mutual

distributed ledgers (aka blockchain technology). Journal of Financial Perspectives, 3(3).

Nyberg, C., 2019. Intuit, Inc.’s Small Business and Self Employed Unit: A Strategic Analysis

O'Connell, B., Carnegie, G., Carter, A., de Lange, P., Hancock, P., Helliar, C., and Watty, K. 2015.

Shaping the future of accounting in business education in Australia.

Pan, G., and Seow, P. S. 2015. Preparing accounting graduates for digital revolution: A critical review

of information technology competencies and skills development. Journal of Education for

Business, 91(3), 166-175.

Payne, D. M., Corey, C., Raiborn, C., and Zingoni, M. 2019. An applied code of ethics model for

decision-making in the accounting profession. Management Research Review.

Ramchand, K., Chhetri, M.B. and Kowalczyk, R., 2017, December. Towards a Flexible Cloud

Architectural Decision Framework for Diverse Application Architectures. In The 28th Australasian

Conference on Information Systems,(ACIS2017), WestPoint Tasmania, Hobart, Tasmania, 4-6

December 2017.

Rikhardsson, P., and Yigitbasioglu, O. 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting Information

Systems, 29, 37-58.

Sheehan, N. T., and Schmidt, J. A. 2015. Preparing accounting students for ethical decision making:

Developing individual codes of conduct based on personal values. Journal of Accounting

Education, 33(3), 183-197.

Tang, Y., 2017, June. Combination of Innovative Thinking with Accounting Teaching. In 2nd

International Conference on Contemporary Education, Social Sciences and Humanities (ICCESSH

2017). Atlantis Press.

Watty, K., McKay, J., and Ngo, L. 2016. Innovators or inhibitors? Accounting faculty resistance to new

educational technologies in higher education. Journal of Accounting Education, 36, 1-15.

West, A. 2018. After virtue and accounting ethics. Journal of Business Ethics, 148(1), 21-36.

West, A., 2017. The ethics of professional accountants: An Aristotelian perspective. Accounting,

Auditing & Accountability Journal, 30(2), pp.328-351..

Wilson, S.K. and Benson, R.E., Florida Agricultural and Mechanical University, 2016. Artificial

intelligence valet systems and methods. U.S. Patent 9,429,943.

Online

APESB, 2018. Proposed Standard: APES 110 Code of Ethics for Professional Accountants (including

Independence Standards) (pdf) Available through <

decision-making in the accounting profession. Management Research Review.

Ramchand, K., Chhetri, M.B. and Kowalczyk, R., 2017, December. Towards a Flexible Cloud

Architectural Decision Framework for Diverse Application Architectures. In The 28th Australasian

Conference on Information Systems,(ACIS2017), WestPoint Tasmania, Hobart, Tasmania, 4-6

December 2017.

Rikhardsson, P., and Yigitbasioglu, O. 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting Information

Systems, 29, 37-58.

Sheehan, N. T., and Schmidt, J. A. 2015. Preparing accounting students for ethical decision making:

Developing individual codes of conduct based on personal values. Journal of Accounting

Education, 33(3), 183-197.

Tang, Y., 2017, June. Combination of Innovative Thinking with Accounting Teaching. In 2nd

International Conference on Contemporary Education, Social Sciences and Humanities (ICCESSH

2017). Atlantis Press.

Watty, K., McKay, J., and Ngo, L. 2016. Innovators or inhibitors? Accounting faculty resistance to new

educational technologies in higher education. Journal of Accounting Education, 36, 1-15.

West, A. 2018. After virtue and accounting ethics. Journal of Business Ethics, 148(1), 21-36.

West, A., 2017. The ethics of professional accountants: An Aristotelian perspective. Accounting,

Auditing & Accountability Journal, 30(2), pp.328-351..

Wilson, S.K. and Benson, R.E., Florida Agricultural and Mechanical University, 2016. Artificial

intelligence valet systems and methods. U.S. Patent 9,429,943.

Online

APESB, 2018. Proposed Standard: APES 110 Code of Ethics for Professional Accountants (including

Independence Standards) (pdf) Available through <

https://www.apesb.org.au/uploads/home/11052018154637_ED_02_18_APES_110_Restructured_Code

_May_2018.pdf> [Accessed on 20 January 2019].

CPA, 2019. APES 110 CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS (Online)

Available through <https://www.cpaaustralia.com.au/professional-resources/accounting-professional-

and-ethical-standards/apes-110-code-of-ethics-for-professional-accountants> [Accessed on 20 January

2019].

_May_2018.pdf> [Accessed on 20 January 2019].

CPA, 2019. APES 110 CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS (Online)

Available through <https://www.cpaaustralia.com.au/professional-resources/accounting-professional-

and-ethical-standards/apes-110-code-of-ethics-for-professional-accountants> [Accessed on 20 January

2019].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

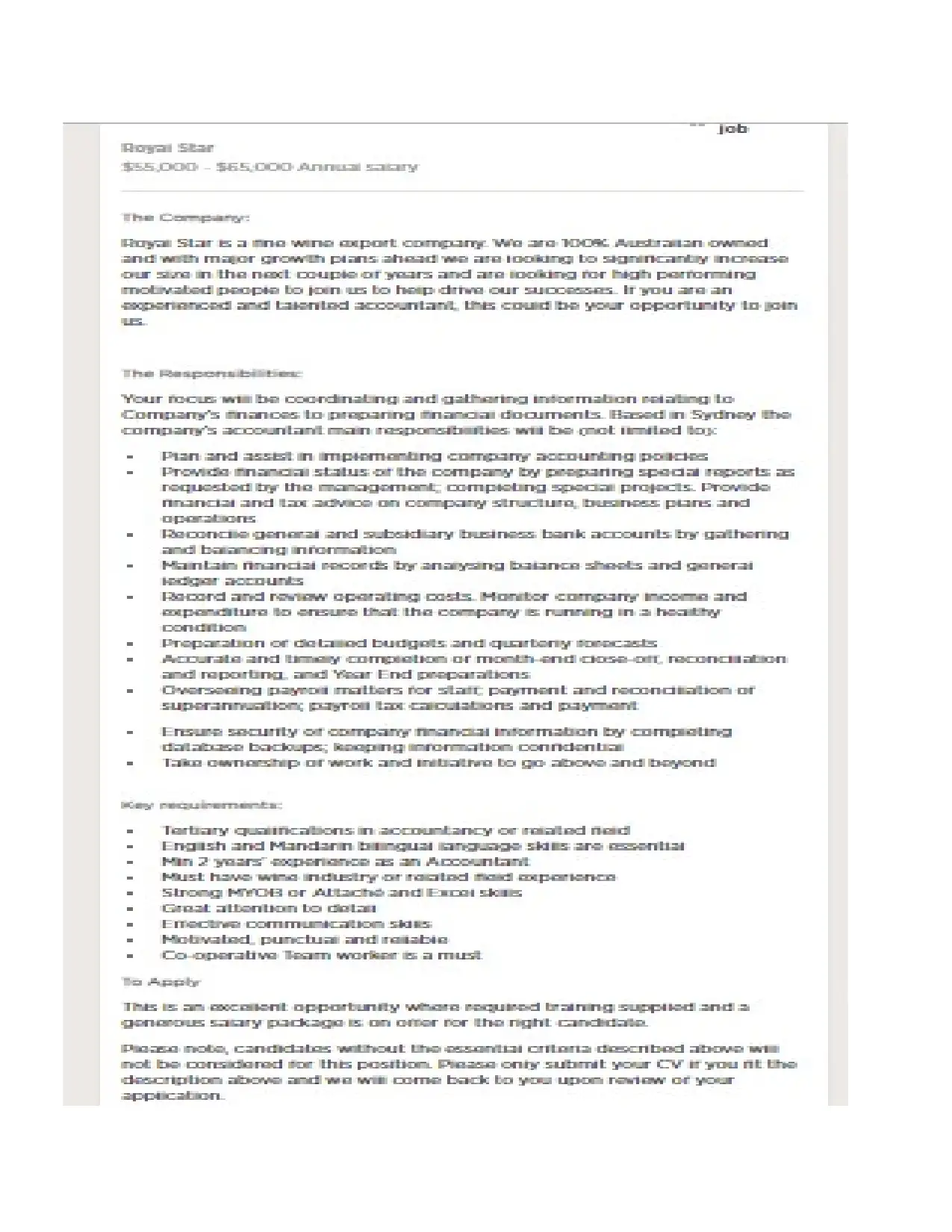

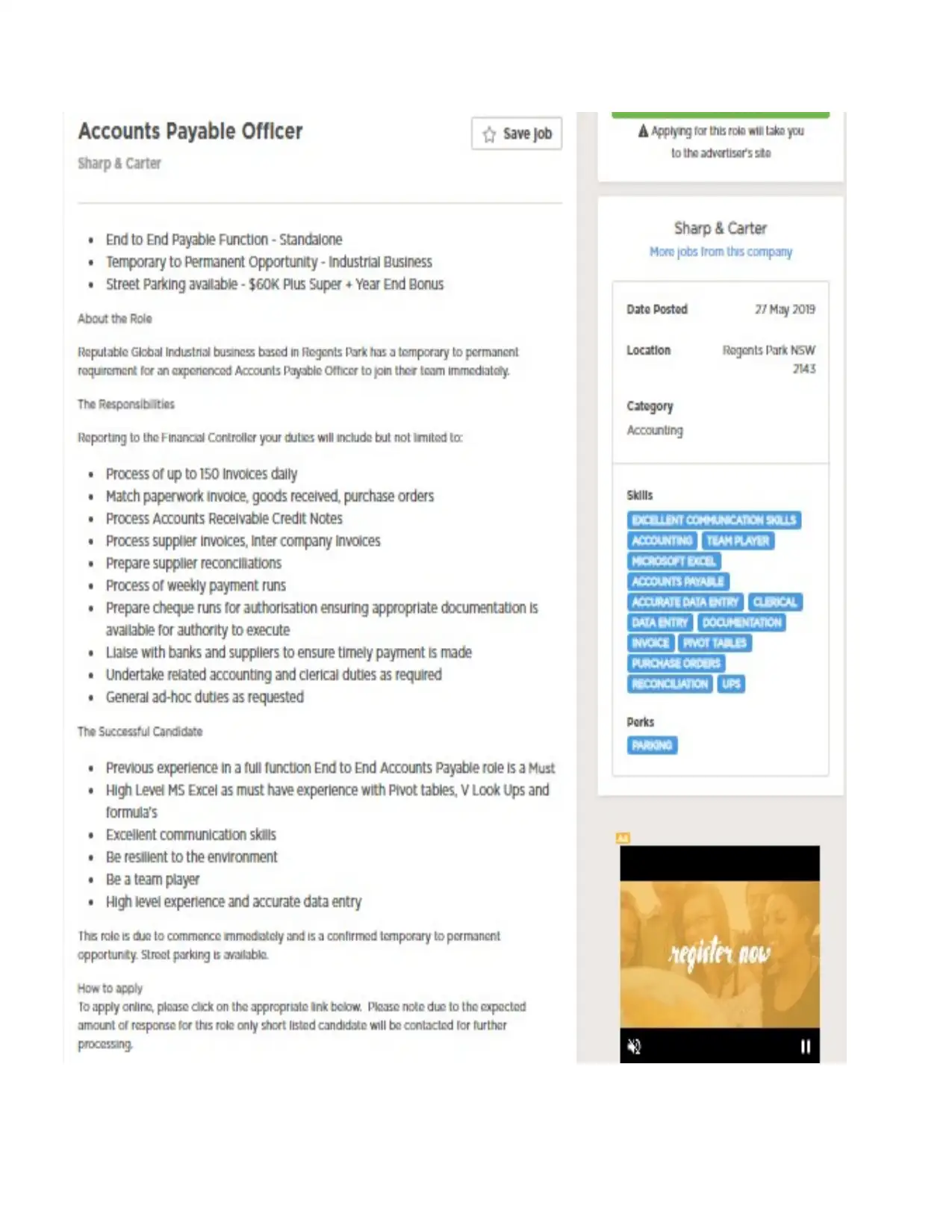

Accountant Job Advertisements

Accountant Job Advertisements

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Minute of Meetings

(I)

Minutes

Date: 5th February

Sub: Discussion regarding opportunities available with accountant in Australia

A variety of options are available to accountants which comprises cost accounts, trade and cost

accountant, commercial financial manager, cost controller, financial controller etc. Above specified

career opportunities are available to the accountants along with many other options. Thus, in case an

accountant is qualified than a variety of options are available for attaining growth in career.

Thanks

(II)

Minutes

Date: 5th March

Sub: Changes in technology relating to accounts.

The technology has changed with time and it is necessary for accountant to learn and accept same in

order to sustain their position as accountant.Artificial Intelligenceand Cloud accounting are two

technologies which have been transformed the role of accountants. As accounting has widen its scope

due to specified technologies. Thus, it can be concluded that it is necessary to accept as well as learn

changes in technologies with time.

Thanks

(I)

Minutes

Date: 5th February

Sub: Discussion regarding opportunities available with accountant in Australia

A variety of options are available to accountants which comprises cost accounts, trade and cost

accountant, commercial financial manager, cost controller, financial controller etc. Above specified

career opportunities are available to the accountants along with many other options. Thus, in case an

accountant is qualified than a variety of options are available for attaining growth in career.

Thanks

(II)

Minutes

Date: 5th March

Sub: Changes in technology relating to accounts.

The technology has changed with time and it is necessary for accountant to learn and accept same in

order to sustain their position as accountant.Artificial Intelligenceand Cloud accounting are two

technologies which have been transformed the role of accountants. As accounting has widen its scope

due to specified technologies. Thus, it can be concluded that it is necessary to accept as well as learn

changes in technologies with time.

Thanks

(III)

Minutes

Date: 5th April

Sub: Ethics to be complied by an accountant

Accountants are require to comply with APES 110 Code of Ethics for professional accounts. The code

specifies five accounting principles which are to be followed by accountant i.e. integrity, objectivity,

professional competence and due care. These principles assists an accountant in taking appropriate

decision while providing services to customers.

Thanks

Minutes

Date: 5th April

Sub: Ethics to be complied by an accountant

Accountants are require to comply with APES 110 Code of Ethics for professional accounts. The code

specifies five accounting principles which are to be followed by accountant i.e. integrity, objectivity,

professional competence and due care. These principles assists an accountant in taking appropriate

decision while providing services to customers.

Thanks

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.