Principles of Auditing : Assignment

VerifiedAdded on 2021/06/14

|13

|2781

|61

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: PRINCIPLES OF AUDITING

Principles of Auditing

Name of the Student

Name of the University

Author’s Note

Principles of Auditing

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1PRINCIPLES OF AUDITING

Table of Contents

Part A...............................................................................................................................................2

Answer to Part A-1......................................................................................................................2

Answer to Part A-2......................................................................................................................2

Answer to Part A-3......................................................................................................................2

Answer to Part A-4......................................................................................................................3

Situation 1................................................................................................................................3

Situation 2................................................................................................................................3

Situation 3................................................................................................................................4

Situation 4................................................................................................................................4

Part B...............................................................................................................................................5

Part C...............................................................................................................................................6

Answer to Part C-1......................................................................................................................6

Answer to Part C-2......................................................................................................................7

Part D...............................................................................................................................................9

References......................................................................................................................................11

Table of Contents

Part A...............................................................................................................................................2

Answer to Part A-1......................................................................................................................2

Answer to Part A-2......................................................................................................................2

Answer to Part A-3......................................................................................................................2

Answer to Part A-4......................................................................................................................3

Situation 1................................................................................................................................3

Situation 2................................................................................................................................3

Situation 3................................................................................................................................4

Situation 4................................................................................................................................4

Part B...............................................................................................................................................5

Part C...............................................................................................................................................6

Answer to Part C-1......................................................................................................................6

Answer to Part C-2......................................................................................................................7

Part D...............................................................................................................................................9

References......................................................................................................................................11

2PRINCIPLES OF AUDITING

Part A

Answer to Part A-1

The auditor of Billings & Associates is required to consider two ethical matters. The first

matter is the continuous spill of toxic chemical into the rove from the manufacturing facility of

Pharmaceuticals. The second ethical matter is the involvement of Pharmaceutical’s management

in covering up this spill in the river. The auditor needs to follow APES 110, Section 210,

Professional Appointment to determine whether the audit engagement would lead to ethical

violation of auditing principles (Doherty 2018).

Answer to Part A-2

The responsibility of the auditor lies in providing recommendations to Pharmaceuticals

for the overall improvement of their internal control. Then the auditor is needed to provide

qualified audit opinion in order to make the major stakeholder inform about the hedging related

issues the company is facing. As a part of qualified audit opinion, the auditor is responsible for

providing the explanation on the reasons for being qualified (William Jr, Glover and Prawitt

2016).

Answer to Part A-3

In the process of auditing, all the terms and conditions along with the nature of audit

engagement are listed in the audit engagement letter (Blay et al. 2014). Thus, both the auditor

and the audit clients are required to go through this letter. The auditor of Billions & Associates

delivered the audit engagement letter to Reaction Pty Ltd that includes all the details of the audit

engagement. Thus, in the presence of this audit engagement letter, the audit client cannot

consider it as a review engagement.

Part A

Answer to Part A-1

The auditor of Billings & Associates is required to consider two ethical matters. The first

matter is the continuous spill of toxic chemical into the rove from the manufacturing facility of

Pharmaceuticals. The second ethical matter is the involvement of Pharmaceutical’s management

in covering up this spill in the river. The auditor needs to follow APES 110, Section 210,

Professional Appointment to determine whether the audit engagement would lead to ethical

violation of auditing principles (Doherty 2018).

Answer to Part A-2

The responsibility of the auditor lies in providing recommendations to Pharmaceuticals

for the overall improvement of their internal control. Then the auditor is needed to provide

qualified audit opinion in order to make the major stakeholder inform about the hedging related

issues the company is facing. As a part of qualified audit opinion, the auditor is responsible for

providing the explanation on the reasons for being qualified (William Jr, Glover and Prawitt

2016).

Answer to Part A-3

In the process of auditing, all the terms and conditions along with the nature of audit

engagement are listed in the audit engagement letter (Blay et al. 2014). Thus, both the auditor

and the audit clients are required to go through this letter. The auditor of Billions & Associates

delivered the audit engagement letter to Reaction Pty Ltd that includes all the details of the audit

engagement. Thus, in the presence of this audit engagement letter, the audit client cannot

consider it as a review engagement.

3PRINCIPLES OF AUDITING

After that, the auditor should issue the Disclaimer of Audit Opinion for modified audit

opinion. The main reason behind the issue of this audit opinion is the lack of required audit

information due to the imposed restriction from the management of the audit client and the

auditors cannot obtain enough information on accounts receivable as a result of lack of

documentation. This reason is enough to issue a disclaimer of audit opinion (William Jr, Glover

and Prawitt 2016).

Answer to Part A-4

Situation 1

a. As per APES 110, Section 290.167, Self-review threat of audit independence arises

when the auditors provide accounting services, bookkeeping and other services to the

audit clients for the preparation of financial statements (apesb.org.au 2018). In the given

situation, the auditor creates self-review threat of audit independence by providing

accounting adjustments for impairment of assets.

b. The most acceptable safeguard in this situation is the removal of this particular from the

audit engagement team of Hail Pty Ltd.

Situation 2

a. As per APES 110, Section 100.12, Advocacy Threat of audit independence arises while

the auditor is involved in the promotion of the business of audit client (apesb.org.au

2018). As per the provided situation, the auditor ensures Travel Time Ltd about

recommending their services to others due to satisfied by the services and this aspect

raises advocacy threat of audit independence.

After that, the auditor should issue the Disclaimer of Audit Opinion for modified audit

opinion. The main reason behind the issue of this audit opinion is the lack of required audit

information due to the imposed restriction from the management of the audit client and the

auditors cannot obtain enough information on accounts receivable as a result of lack of

documentation. This reason is enough to issue a disclaimer of audit opinion (William Jr, Glover

and Prawitt 2016).

Answer to Part A-4

Situation 1

a. As per APES 110, Section 290.167, Self-review threat of audit independence arises

when the auditors provide accounting services, bookkeeping and other services to the

audit clients for the preparation of financial statements (apesb.org.au 2018). In the given

situation, the auditor creates self-review threat of audit independence by providing

accounting adjustments for impairment of assets.

b. The most acceptable safeguard in this situation is the removal of this particular from the

audit engagement team of Hail Pty Ltd.

Situation 2

a. As per APES 110, Section 100.12, Advocacy Threat of audit independence arises while

the auditor is involved in the promotion of the business of audit client (apesb.org.au

2018). As per the provided situation, the auditor ensures Travel Time Ltd about

recommending their services to others due to satisfied by the services and this aspect

raises advocacy threat of audit independence.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4PRINCIPLES OF AUDITING

b. Ensuring the introduction of corporate governance policies in auditing is the main

safeguard of this scenario.

Situation 3

a. According to APES 110, Section 100.12, Familiarity Threat of audit independence

arises in the presence of any relationship between the auditors and the audit client

(apesb.org.au 2018). In the given situation, there is familiarity threat due to the relation

between the wife of one of the auditors and the client as a result of the acquisition of

major shareholding in Civil Constructions Ltd.

b. It is required to remove the particular auditor from the audit engagement for safeguard.

Situation 4

a. According to APES 110, Section 100.12, Intimidation Threat is there in the presence of

any actual or perceived pressure on the auditor from the audit so that the auditors cannot

act objectively (apesb.org.au 2018). In the given case, the request of extra time on the

auditors from Pleasure Cruises Ltd is creating pressure on the auditors that lead to the

creation of intimidation threat of audit independence.

b. Implementation of correct corporate governance policies is the major safeguard of this

threat.

b. Ensuring the introduction of corporate governance policies in auditing is the main

safeguard of this scenario.

Situation 3

a. According to APES 110, Section 100.12, Familiarity Threat of audit independence

arises in the presence of any relationship between the auditors and the audit client

(apesb.org.au 2018). In the given situation, there is familiarity threat due to the relation

between the wife of one of the auditors and the client as a result of the acquisition of

major shareholding in Civil Constructions Ltd.

b. It is required to remove the particular auditor from the audit engagement for safeguard.

Situation 4

a. According to APES 110, Section 100.12, Intimidation Threat is there in the presence of

any actual or perceived pressure on the auditor from the audit so that the auditors cannot

act objectively (apesb.org.au 2018). In the given case, the request of extra time on the

auditors from Pleasure Cruises Ltd is creating pressure on the auditors that lead to the

creation of intimidation threat of audit independence.

b. Implementation of correct corporate governance policies is the major safeguard of this

threat.

5PRINCIPLES OF AUDITING

Part B

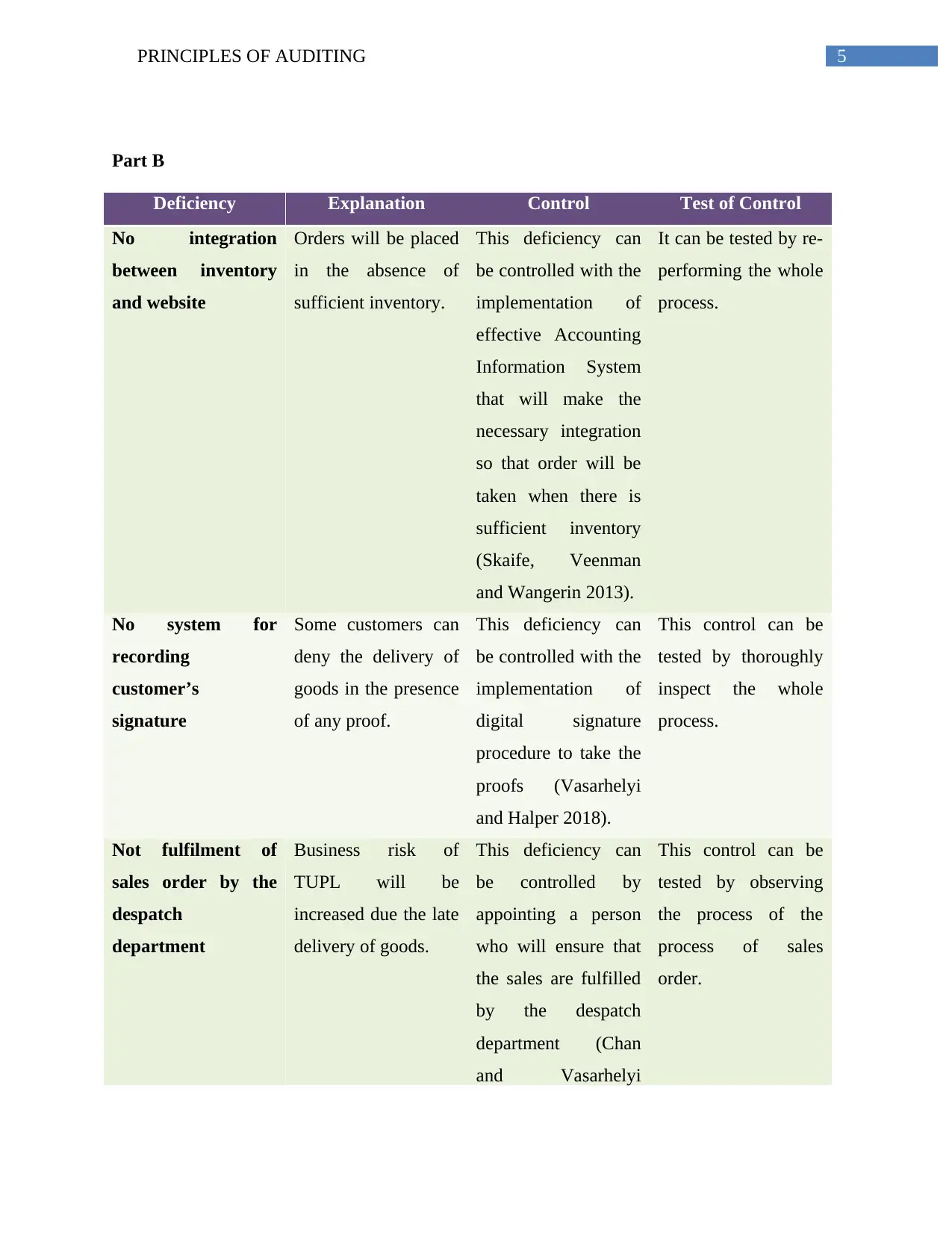

Deficiency Explanation Control Test of Control

No integration

between inventory

and website

Orders will be placed

in the absence of

sufficient inventory.

This deficiency can

be controlled with the

implementation of

effective Accounting

Information System

that will make the

necessary integration

so that order will be

taken when there is

sufficient inventory

(Skaife, Veenman

and Wangerin 2013).

It can be tested by re-

performing the whole

process.

No system for

recording

customer’s

signature

Some customers can

deny the delivery of

goods in the presence

of any proof.

This deficiency can

be controlled with the

implementation of

digital signature

procedure to take the

proofs (Vasarhelyi

and Halper 2018).

This control can be

tested by thoroughly

inspect the whole

process.

Not fulfilment of

sales order by the

despatch

department

Business risk of

TUPL will be

increased due the late

delivery of goods.

This deficiency can

be controlled by

appointing a person

who will ensure that

the sales are fulfilled

by the despatch

department (Chan

and Vasarhelyi

This control can be

tested by observing

the process of the

process of sales

order.

Part B

Deficiency Explanation Control Test of Control

No integration

between inventory

and website

Orders will be placed

in the absence of

sufficient inventory.

This deficiency can

be controlled with the

implementation of

effective Accounting

Information System

that will make the

necessary integration

so that order will be

taken when there is

sufficient inventory

(Skaife, Veenman

and Wangerin 2013).

It can be tested by re-

performing the whole

process.

No system for

recording

customer’s

signature

Some customers can

deny the delivery of

goods in the presence

of any proof.

This deficiency can

be controlled with the

implementation of

digital signature

procedure to take the

proofs (Vasarhelyi

and Halper 2018).

This control can be

tested by thoroughly

inspect the whole

process.

Not fulfilment of

sales order by the

despatch

department

Business risk of

TUPL will be

increased due the late

delivery of goods.

This deficiency can

be controlled by

appointing a person

who will ensure that

the sales are fulfilled

by the despatch

department (Chan

and Vasarhelyi

This control can be

tested by observing

the process of the

process of sales

order.

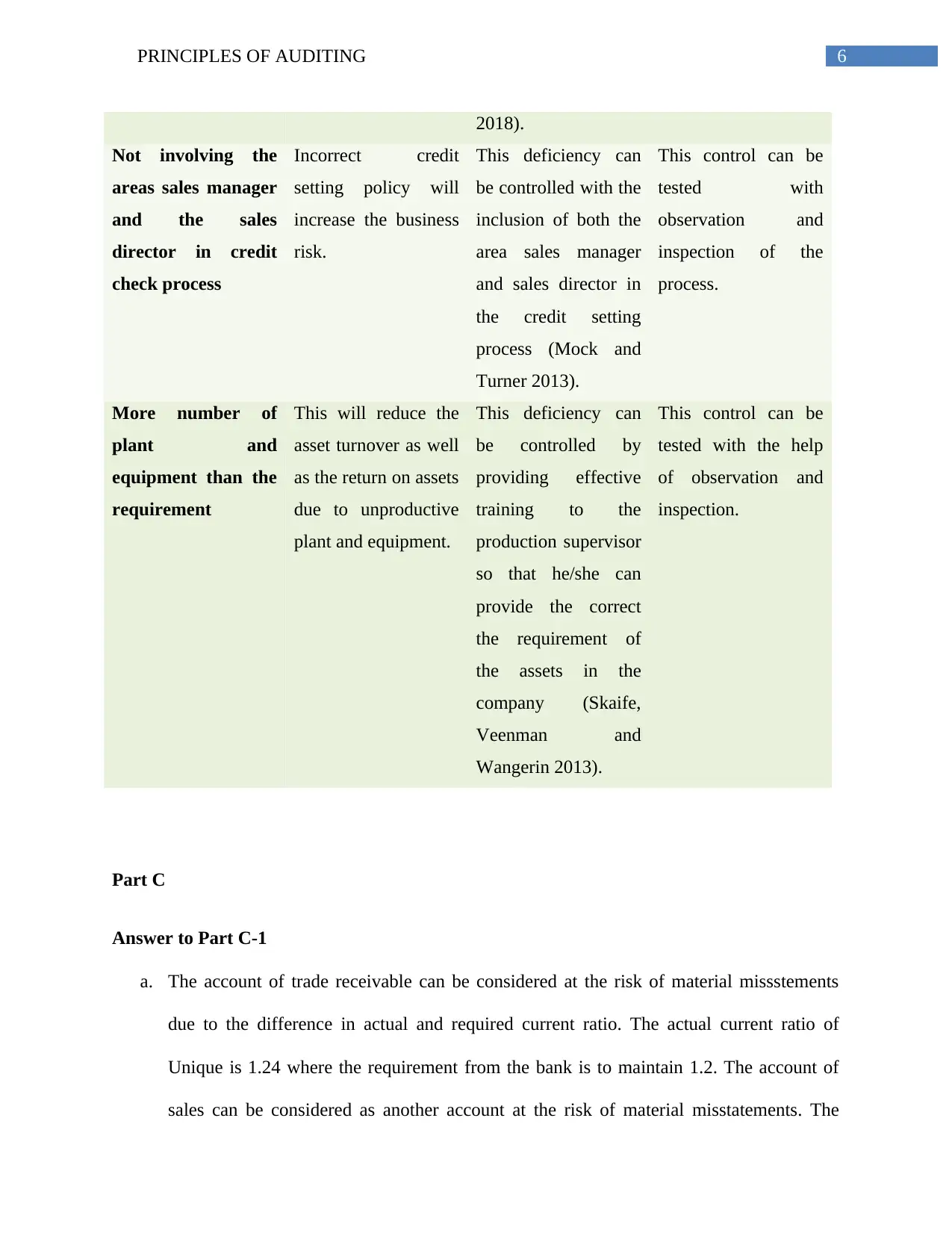

6PRINCIPLES OF AUDITING

2018).

Not involving the

areas sales manager

and the sales

director in credit

check process

Incorrect credit

setting policy will

increase the business

risk.

This deficiency can

be controlled with the

inclusion of both the

area sales manager

and sales director in

the credit setting

process (Mock and

Turner 2013).

This control can be

tested with

observation and

inspection of the

process.

More number of

plant and

equipment than the

requirement

This will reduce the

asset turnover as well

as the return on assets

due to unproductive

plant and equipment.

This deficiency can

be controlled by

providing effective

training to the

production supervisor

so that he/she can

provide the correct

the requirement of

the assets in the

company (Skaife,

Veenman and

Wangerin 2013).

This control can be

tested with the help

of observation and

inspection.

Part C

Answer to Part C-1

a. The account of trade receivable can be considered at the risk of material missstements

due to the difference in actual and required current ratio. The actual current ratio of

Unique is 1.24 where the requirement from the bank is to maintain 1.2. The account of

sales can be considered as another account at the risk of material misstatements. The

2018).

Not involving the

areas sales manager

and the sales

director in credit

check process

Incorrect credit

setting policy will

increase the business

risk.

This deficiency can

be controlled with the

inclusion of both the

area sales manager

and sales director in

the credit setting

process (Mock and

Turner 2013).

This control can be

tested with

observation and

inspection of the

process.

More number of

plant and

equipment than the

requirement

This will reduce the

asset turnover as well

as the return on assets

due to unproductive

plant and equipment.

This deficiency can

be controlled by

providing effective

training to the

production supervisor

so that he/she can

provide the correct

the requirement of

the assets in the

company (Skaife,

Veenman and

Wangerin 2013).

This control can be

tested with the help

of observation and

inspection.

Part C

Answer to Part C-1

a. The account of trade receivable can be considered at the risk of material missstements

due to the difference in actual and required current ratio. The actual current ratio of

Unique is 1.24 where the requirement from the bank is to maintain 1.2. The account of

sales can be considered as another account at the risk of material misstatements. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRINCIPLES OF AUDITING

actual sales of Unique is $350,000 for the entire year where the requirement from the

bank is to maintain $100,000 of net sales per quarter. These aspects indicate towards any

kind of errors, fraud or manipulation in these accounts (Knechel and Salterio 2016).

b. The profit margin of Unique has issue related to the prior year due to the reason that there

is a major decrease in both the gross profit and net profit margin of Unique.

c. Large decline in both the gross profit and net profit can question the going concern

assumption of the company due to the reason that Unique will have to wind up their

business due to massive loss in future. The increase in the timber price for the last two

years as a result of the increase and decrease in US dollar and Australian dollar

respectively can also question the going concern status of Unique as the company may

face difficulty in future to cope up with the increasing cost of timber. The increase in the

labour cost of the business of Unique that can contribute to high wages. Due to this,

Unique may face large amount of indirect expenses in future (Ratzinger-Sakel 2013).

d. While planning the audit operation, the obligation on the auditors is to consider the

accents at the risk of material misstatements and obtain sufficient information to get the

assurance about the presence of material misstatements. The application of required

analytical procedures is another major responsibility for the auditor to get the information

about the going concern status of Unique (Feldmann and Read 2013).

Answer to Part C-2

a. The payment of sales bonus involves internal control issue in Unique. The provide

information shows that there is payment of sales bonuses while the required criteria are

not met. It indicates towards internal control weaknesses (Badara and Saidin 2013).

actual sales of Unique is $350,000 for the entire year where the requirement from the

bank is to maintain $100,000 of net sales per quarter. These aspects indicate towards any

kind of errors, fraud or manipulation in these accounts (Knechel and Salterio 2016).

b. The profit margin of Unique has issue related to the prior year due to the reason that there

is a major decrease in both the gross profit and net profit margin of Unique.

c. Large decline in both the gross profit and net profit can question the going concern

assumption of the company due to the reason that Unique will have to wind up their

business due to massive loss in future. The increase in the timber price for the last two

years as a result of the increase and decrease in US dollar and Australian dollar

respectively can also question the going concern status of Unique as the company may

face difficulty in future to cope up with the increasing cost of timber. The increase in the

labour cost of the business of Unique that can contribute to high wages. Due to this,

Unique may face large amount of indirect expenses in future (Ratzinger-Sakel 2013).

d. While planning the audit operation, the obligation on the auditors is to consider the

accents at the risk of material misstatements and obtain sufficient information to get the

assurance about the presence of material misstatements. The application of required

analytical procedures is another major responsibility for the auditor to get the information

about the going concern status of Unique (Feldmann and Read 2013).

Answer to Part C-2

a. The payment of sales bonus involves internal control issue in Unique. The provide

information shows that there is payment of sales bonuses while the required criteria are

not met. It indicates towards internal control weaknesses (Badara and Saidin 2013).

8PRINCIPLES OF AUDITING

b. No change in the gross margin can be considered as the first factor. It is definite that the

gross profit margin will face decline in the presence of decline in the gross profit. For this

reason, no change in the gross profit margin can be a result of fraudulent activities.

Debtors can be considered as the second factor. Large change in the debtor level is there

between the last day of the year and during the six months after that. This unusual change

indicates towards the presence of any kind of fraud activity (Abdullatif 2013).

c. As a result of the above discussion, it can be said that the debtor balances can be at risk

due to the happening of different types of fraudulent activity around this account. The

main reason for the fraudulent activities or manipulations in the debtor balances is the

gaining of sales bonuses. This aspect creates risk for two management assertions. The

initiation and approval of customer invoice while sales take place is one assertion. The

approval and issue of credit notes within 60 days of return is another assertion. The main

reason for making these assertions is to manipulate the balances of debtors (Abdullatif

2013).

d. The introduction of test of control is one audit procedure to address the issue of material

misstatements. The duty of the auditors is to conduct the test of control for measuring the

effectiveness of the internal control of Unique. The introduction and implementation of

substantive audit procedures can be considered as another audit procedure to address

material misstatements. In this aspect, the duty of the auditors is to design and perform

the substantive audit procedure for testing all the assertions developed by the

management of Unique (DeFond and Zhang 2014). These are the two audit procedures

for addressing material misstatements.

b. No change in the gross margin can be considered as the first factor. It is definite that the

gross profit margin will face decline in the presence of decline in the gross profit. For this

reason, no change in the gross profit margin can be a result of fraudulent activities.

Debtors can be considered as the second factor. Large change in the debtor level is there

between the last day of the year and during the six months after that. This unusual change

indicates towards the presence of any kind of fraud activity (Abdullatif 2013).

c. As a result of the above discussion, it can be said that the debtor balances can be at risk

due to the happening of different types of fraudulent activity around this account. The

main reason for the fraudulent activities or manipulations in the debtor balances is the

gaining of sales bonuses. This aspect creates risk for two management assertions. The

initiation and approval of customer invoice while sales take place is one assertion. The

approval and issue of credit notes within 60 days of return is another assertion. The main

reason for making these assertions is to manipulate the balances of debtors (Abdullatif

2013).

d. The introduction of test of control is one audit procedure to address the issue of material

misstatements. The duty of the auditors is to conduct the test of control for measuring the

effectiveness of the internal control of Unique. The introduction and implementation of

substantive audit procedures can be considered as another audit procedure to address

material misstatements. In this aspect, the duty of the auditors is to design and perform

the substantive audit procedure for testing all the assertions developed by the

management of Unique (DeFond and Zhang 2014). These are the two audit procedures

for addressing material misstatements.

9PRINCIPLES OF AUDITING

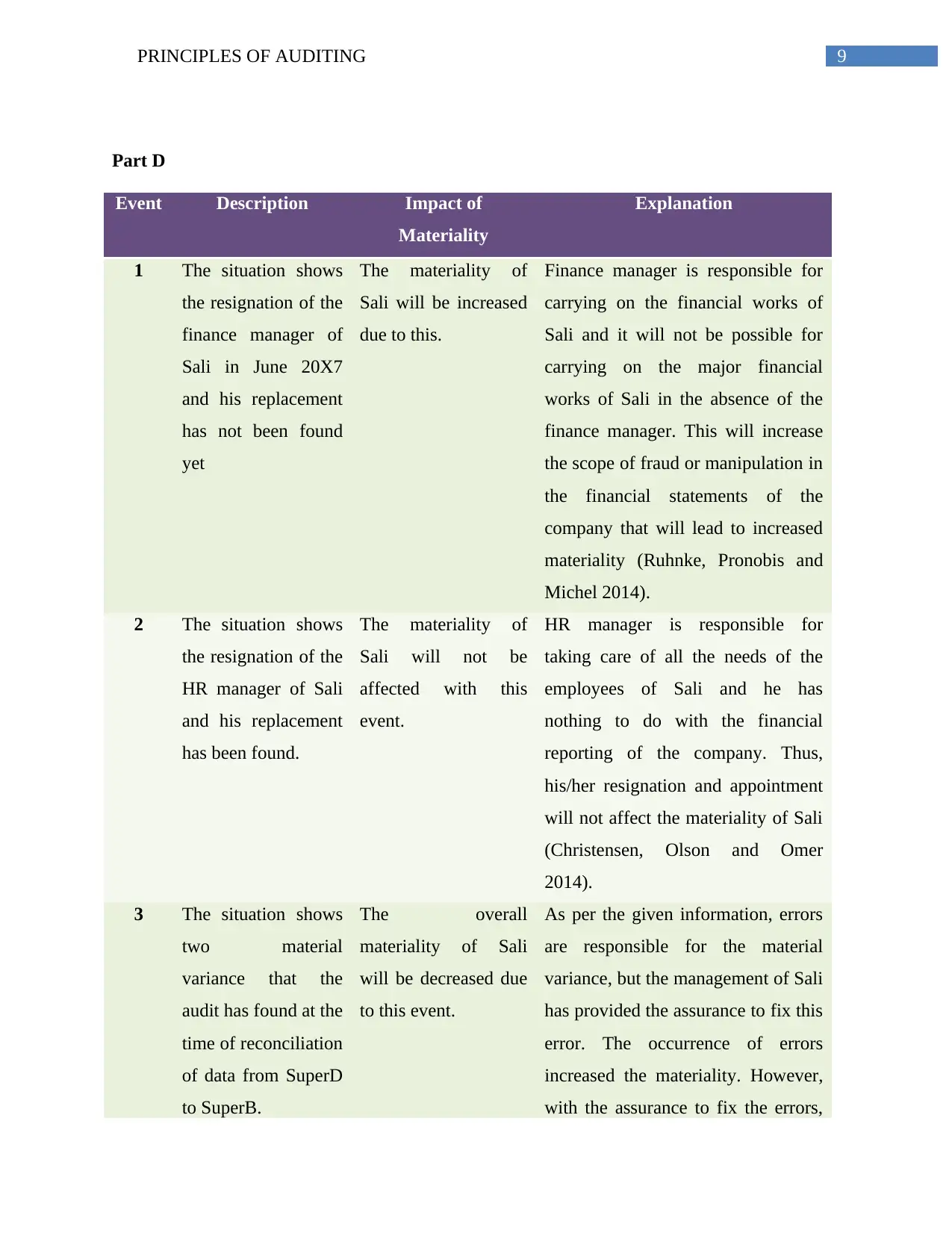

Part D

Event Description Impact of

Materiality

Explanation

1 The situation shows

the resignation of the

finance manager of

Sali in June 20X7

and his replacement

has not been found

yet

The materiality of

Sali will be increased

due to this.

Finance manager is responsible for

carrying on the financial works of

Sali and it will not be possible for

carrying on the major financial

works of Sali in the absence of the

finance manager. This will increase

the scope of fraud or manipulation in

the financial statements of the

company that will lead to increased

materiality (Ruhnke, Pronobis and

Michel 2014).

2 The situation shows

the resignation of the

HR manager of Sali

and his replacement

has been found.

The materiality of

Sali will not be

affected with this

event.

HR manager is responsible for

taking care of all the needs of the

employees of Sali and he has

nothing to do with the financial

reporting of the company. Thus,

his/her resignation and appointment

will not affect the materiality of Sali

(Christensen, Olson and Omer

2014).

3 The situation shows

two material

variance that the

audit has found at the

time of reconciliation

of data from SuperD

to SuperB.

The overall

materiality of Sali

will be decreased due

to this event.

As per the given information, errors

are responsible for the material

variance, but the management of Sali

has provided the assurance to fix this

error. The occurrence of errors

increased the materiality. However,

with the assurance to fix the errors,

Part D

Event Description Impact of

Materiality

Explanation

1 The situation shows

the resignation of the

finance manager of

Sali in June 20X7

and his replacement

has not been found

yet

The materiality of

Sali will be increased

due to this.

Finance manager is responsible for

carrying on the financial works of

Sali and it will not be possible for

carrying on the major financial

works of Sali in the absence of the

finance manager. This will increase

the scope of fraud or manipulation in

the financial statements of the

company that will lead to increased

materiality (Ruhnke, Pronobis and

Michel 2014).

2 The situation shows

the resignation of the

HR manager of Sali

and his replacement

has been found.

The materiality of

Sali will not be

affected with this

event.

HR manager is responsible for

taking care of all the needs of the

employees of Sali and he has

nothing to do with the financial

reporting of the company. Thus,

his/her resignation and appointment

will not affect the materiality of Sali

(Christensen, Olson and Omer

2014).

3 The situation shows

two material

variance that the

audit has found at the

time of reconciliation

of data from SuperD

to SuperB.

The overall

materiality of Sali

will be decreased due

to this event.

As per the given information, errors

are responsible for the material

variance, but the management of Sali

has provided the assurance to fix this

error. The occurrence of errors

increased the materiality. However,

with the assurance to fix the errors,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

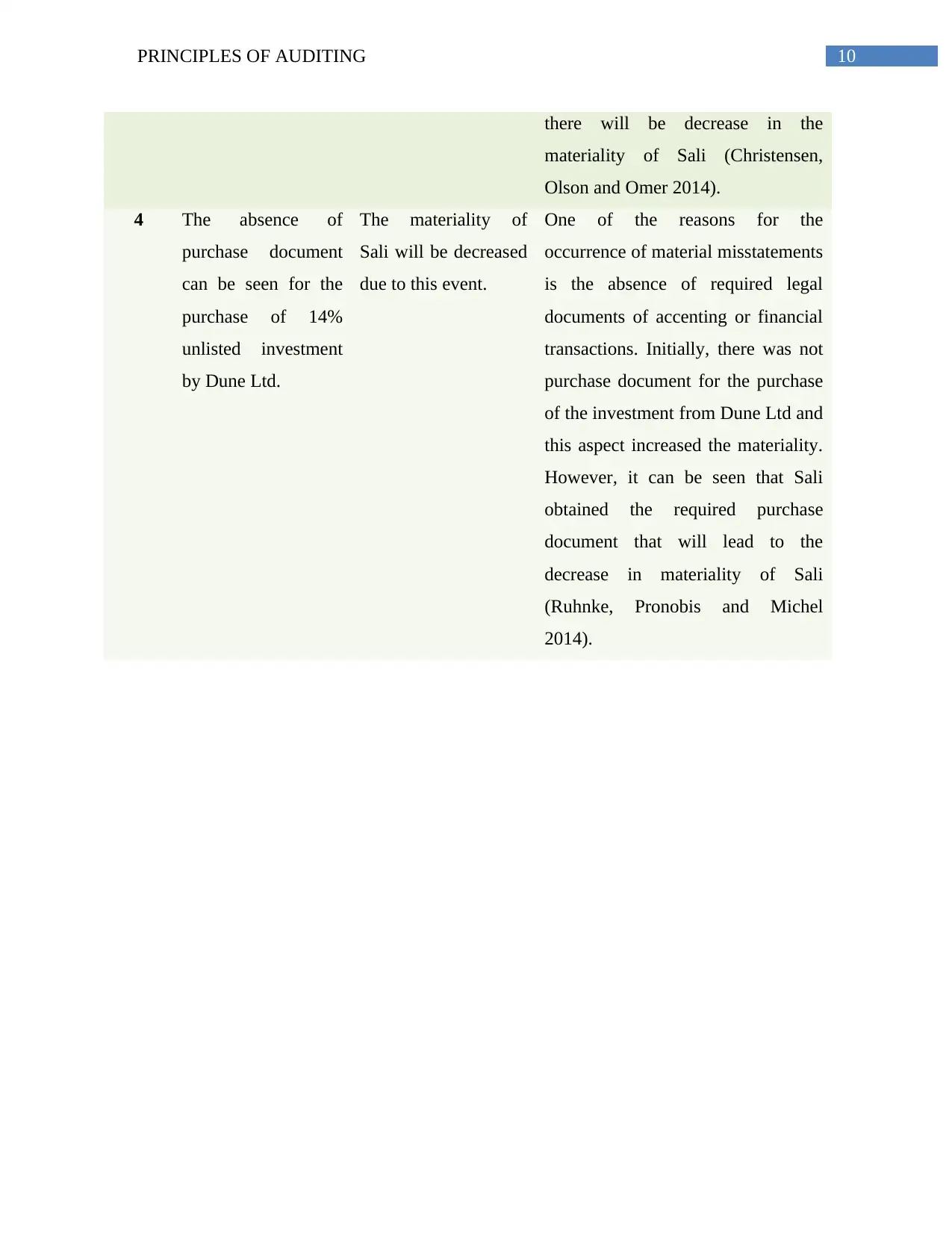

10PRINCIPLES OF AUDITING

there will be decrease in the

materiality of Sali (Christensen,

Olson and Omer 2014).

4 The absence of

purchase document

can be seen for the

purchase of 14%

unlisted investment

by Dune Ltd.

The materiality of

Sali will be decreased

due to this event.

One of the reasons for the

occurrence of material misstatements

is the absence of required legal

documents of accenting or financial

transactions. Initially, there was not

purchase document for the purchase

of the investment from Dune Ltd and

this aspect increased the materiality.

However, it can be seen that Sali

obtained the required purchase

document that will lead to the

decrease in materiality of Sali

(Ruhnke, Pronobis and Michel

2014).

there will be decrease in the

materiality of Sali (Christensen,

Olson and Omer 2014).

4 The absence of

purchase document

can be seen for the

purchase of 14%

unlisted investment

by Dune Ltd.

The materiality of

Sali will be decreased

due to this event.

One of the reasons for the

occurrence of material misstatements

is the absence of required legal

documents of accenting or financial

transactions. Initially, there was not

purchase document for the purchase

of the investment from Dune Ltd and

this aspect increased the materiality.

However, it can be seen that Sali

obtained the required purchase

document that will lead to the

decrease in materiality of Sali

(Ruhnke, Pronobis and Michel

2014).

11PRINCIPLES OF AUDITING

References

Abdullatif, M., 2013. Fraud risk factors and audit programme modifications: Evidence from

Jordan. Australasian Accounting Business & Finance Journal, 7(1), p.59.

Apesb.org.au. (2018). APES 110 Code of Ethics for Professional Accountants. [online] Available

at: https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf [Accessed 10

May 2018].

Badara, M.A.S. and Saidin, S.Z., 2013. Impact of the effective internal control system on the

internal audit effectiveness at local government level. Journal of Social and Development

Sciences, 4(1), pp.16-23.

Blay, A.D., Notbohm, M., Schelleman, C. and Valencia, A., 2014. Audit quality effects of an

individual audit engagement partner signature mandate. International Journal of Auditing, 18(3),

pp.172-192.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Christensen, B.E., Olson, A.J. and Omer, T.C., 2014. The role of audit firm expertise and

knowledge spillover in mitigating earnings management through the tax accounts. The Journal of

the American Taxation Association, 37(1), pp.3-36.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2-3), pp.275-326.

Doherty, M., 2018. Ethics of Auditing.

References

Abdullatif, M., 2013. Fraud risk factors and audit programme modifications: Evidence from

Jordan. Australasian Accounting Business & Finance Journal, 7(1), p.59.

Apesb.org.au. (2018). APES 110 Code of Ethics for Professional Accountants. [online] Available

at: https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf [Accessed 10

May 2018].

Badara, M.A.S. and Saidin, S.Z., 2013. Impact of the effective internal control system on the

internal audit effectiveness at local government level. Journal of Social and Development

Sciences, 4(1), pp.16-23.

Blay, A.D., Notbohm, M., Schelleman, C. and Valencia, A., 2014. Audit quality effects of an

individual audit engagement partner signature mandate. International Journal of Auditing, 18(3),

pp.172-192.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Christensen, B.E., Olson, A.J. and Omer, T.C., 2014. The role of audit firm expertise and

knowledge spillover in mitigating earnings management through the tax accounts. The Journal of

the American Taxation Association, 37(1), pp.3-36.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2-3), pp.275-326.

Doherty, M., 2018. Ethics of Auditing.

12PRINCIPLES OF AUDITING

Feldmann, D. and Read, W.J., 2013. Going-concern audit opinions for bankrupt companies–

impact of credit rating. Managerial Auditing Journal, 28(4), pp.345-363.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Mock, T.J. and Turner, J.L., 2013. Internal Accounting Control Evaluation and Auditor

Judgement: An Anthology. Routledge.

Ratzinger-Sakel, N.V., 2013. Auditor fees and auditor independence—Evidence from going

concern reporting decisions in Germany. Auditing: A Journal of Practice & Theory, 32(4),

pp.129-168.

Ruhnke, K., Pronobis, P. and Michel, M., 2014. Audit materiality disclosures and credit lending

decisions.

Skaife, H.A., Veenman, D. and Wangerin, D., 2013. Internal control over financial reporting and

managerial rent extraction: Evidence from the profitability of insider trading. Journal of

Accounting and Economics, 55(1), pp.91-110.

Vasarhelyi, M.A. and Halper, F.B., 2018. The continuous audit of online systems. In Continuous

Auditing: Theory and Application (pp. 87-104). Emerald Publishing Limited.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Feldmann, D. and Read, W.J., 2013. Going-concern audit opinions for bankrupt companies–

impact of credit rating. Managerial Auditing Journal, 28(4), pp.345-363.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Mock, T.J. and Turner, J.L., 2013. Internal Accounting Control Evaluation and Auditor

Judgement: An Anthology. Routledge.

Ratzinger-Sakel, N.V., 2013. Auditor fees and auditor independence—Evidence from going

concern reporting decisions in Germany. Auditing: A Journal of Practice & Theory, 32(4),

pp.129-168.

Ruhnke, K., Pronobis, P. and Michel, M., 2014. Audit materiality disclosures and credit lending

decisions.

Skaife, H.A., Veenman, D. and Wangerin, D., 2013. Internal control over financial reporting and

managerial rent extraction: Evidence from the profitability of insider trading. Journal of

Accounting and Economics, 55(1), pp.91-110.

Vasarhelyi, M.A. and Halper, F.B., 2018. The continuous audit of online systems. In Continuous

Auditing: Theory and Application (pp. 87-104). Emerald Publishing Limited.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.