Principles of Economics: Market Structures and Efficiency Analysis

VerifiedAdded on 2023/04/21

|14

|2225

|92

Homework Assignment

AI Summary

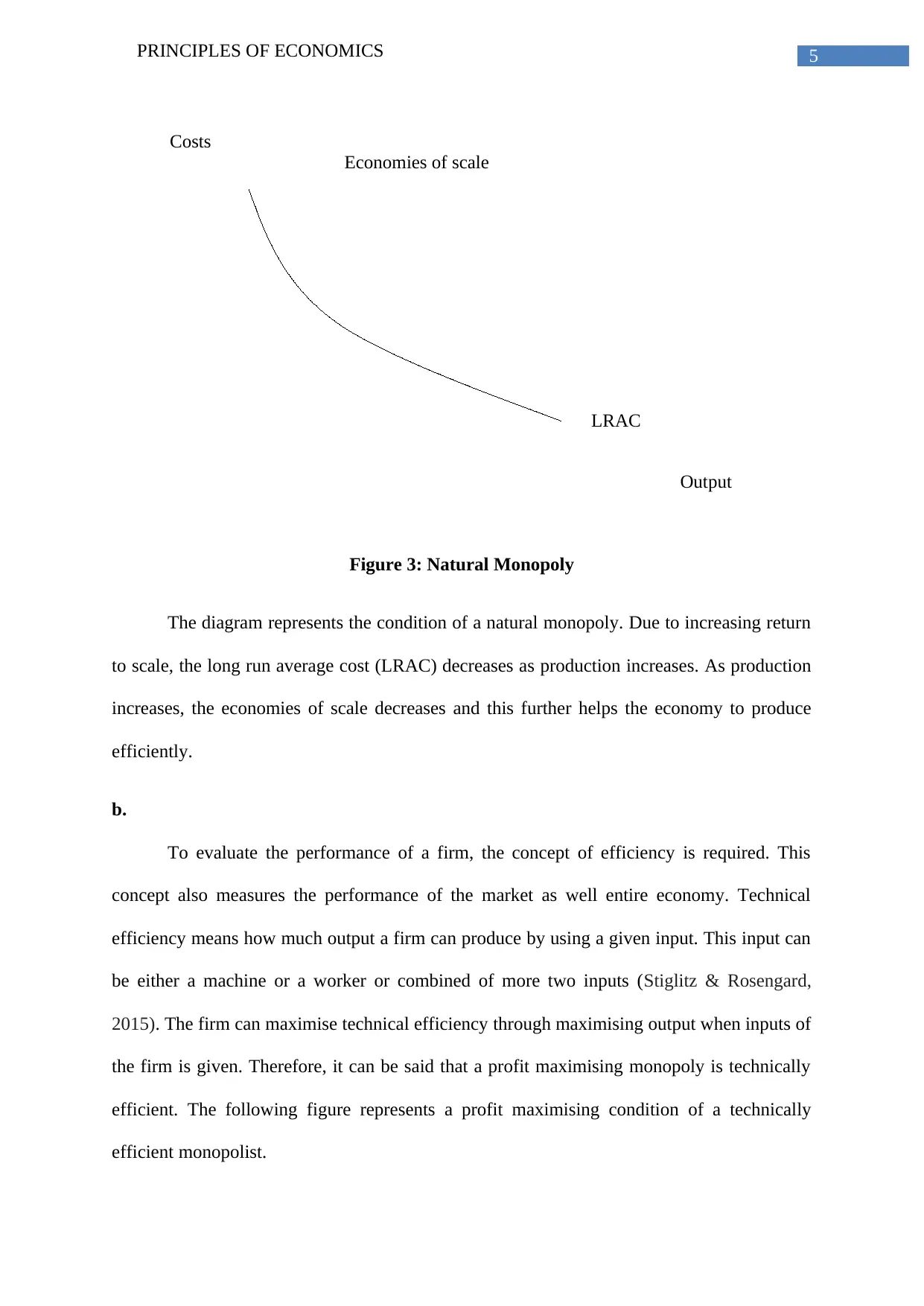

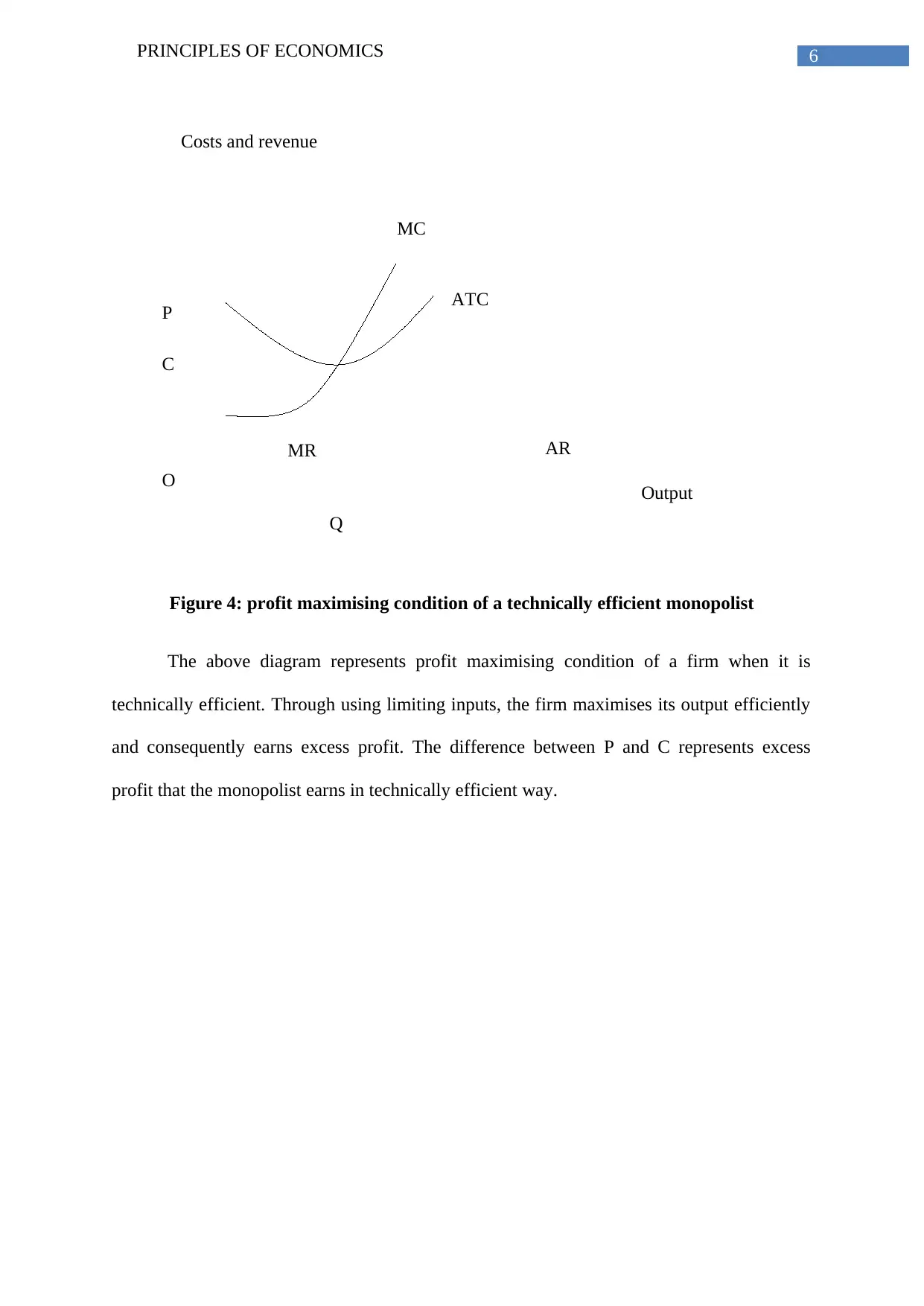

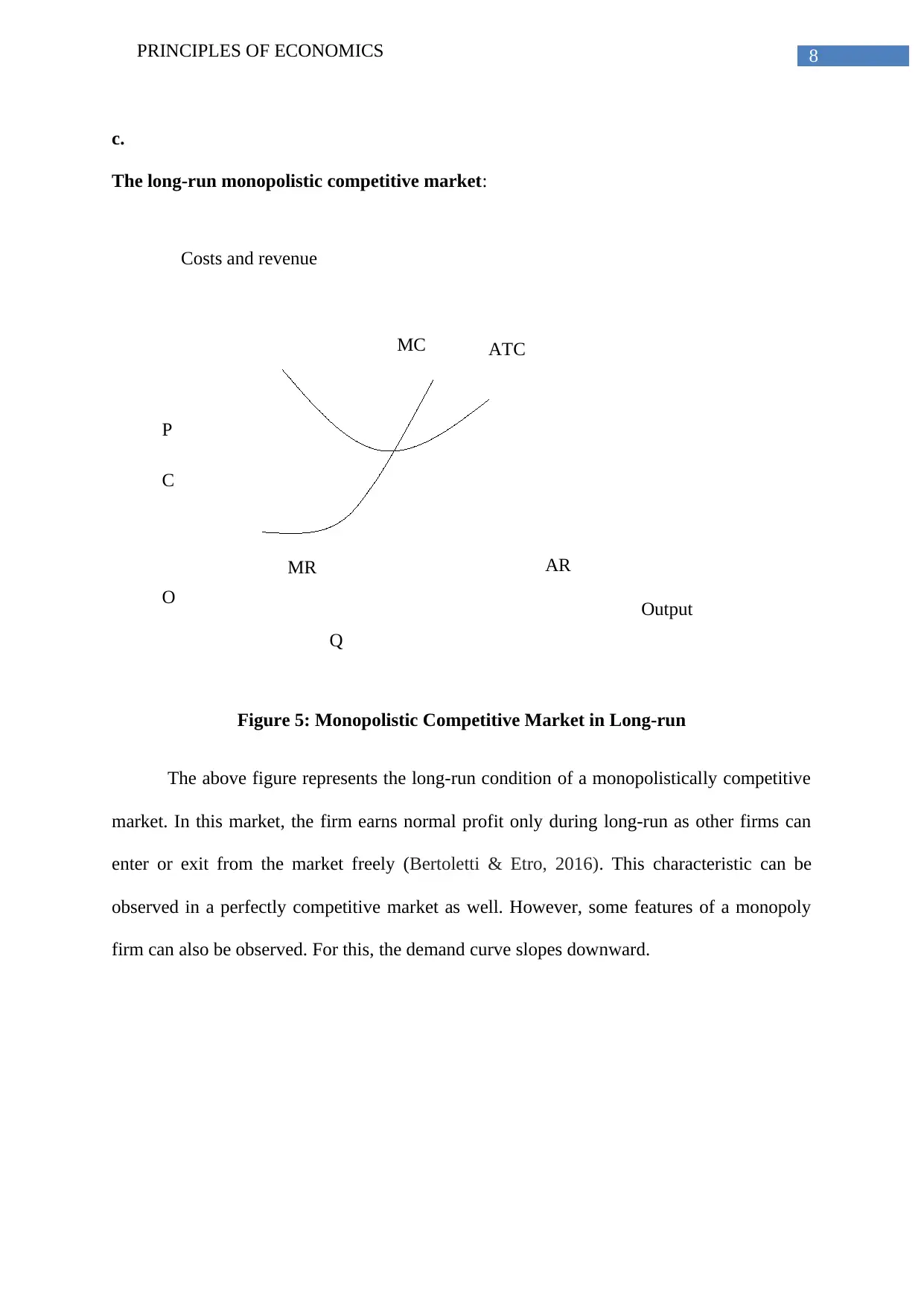

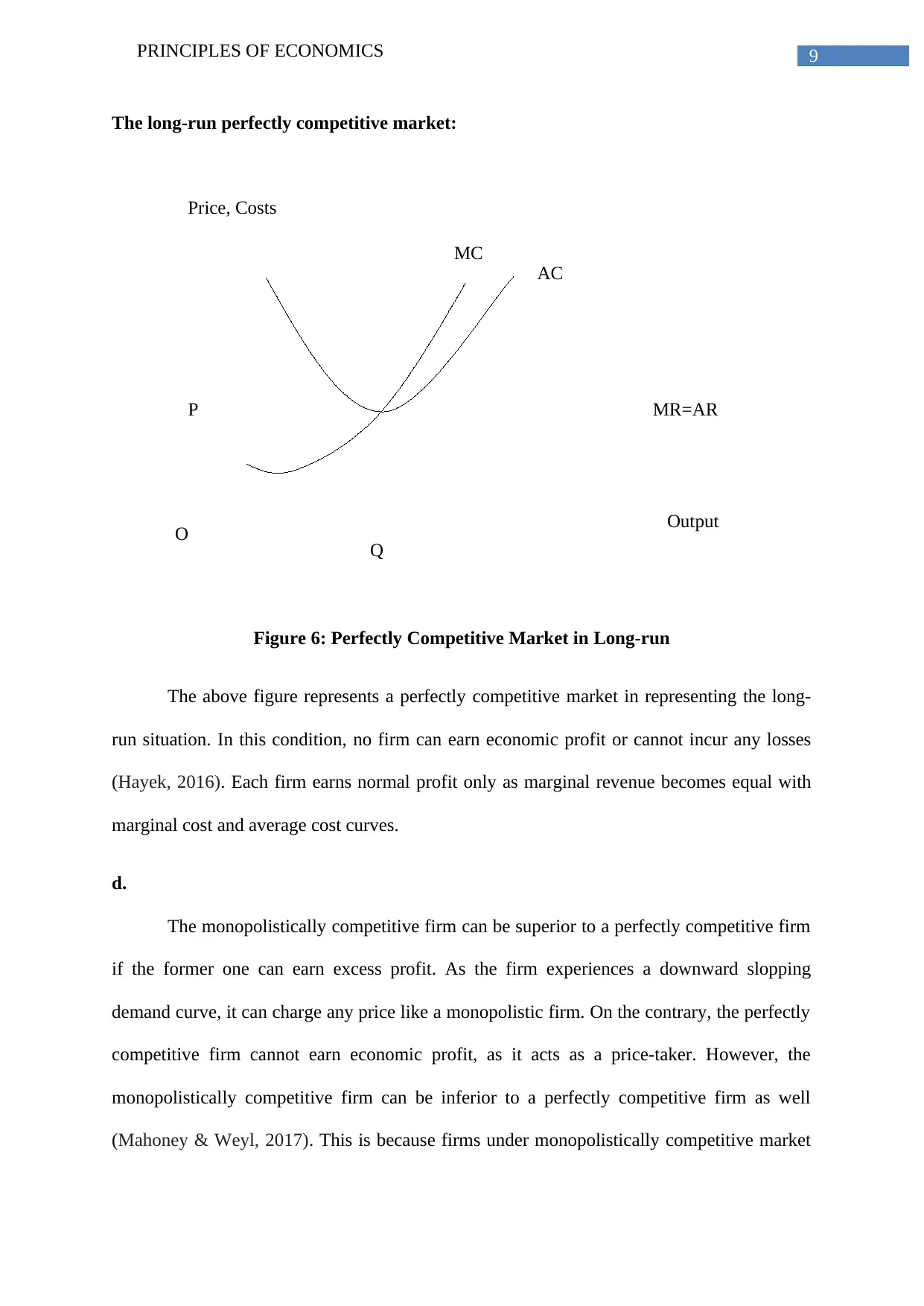

This economics assignment delves into the core principles of market structures, efficiency, and the classification of goods. It begins by examining perfect competition, detailing how firms operate as price takers and achieve equilibrium in both the short and long run, including the conditions for profit and loss. The assignment then explores natural monopolies, explaining their unique characteristics and the concept of economies of scale. It continues with an analysis of oligopolies, discussing the interdependence among firms and the concept of kinked demand curves. The assignment also contrasts monopolistically competitive markets with perfectly competitive markets. Finally, the assignment concludes with a discussion of different types of goods (private, public, and club goods) and the concept of economic efficiency, including private and social costs, externalities, and how firms maximize profits in competitive markets.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.