Finance Report: Analyzing Retail Food Group's Capital Structure

VerifiedAdded on 2021/04/24

|15

|2715

|28

Report

AI Summary

This report provides a comprehensive financial analysis of Retail Food Group (RFG), a prominent food and beverage company in Australia. The report examines RFG's capital structure over a five-year period, utilizing key ratios like debt-to-equity and debt ratios to assess its financial leverage an...

Running head: PRINCIPLES OF FINANCE

Principles of Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Principles of Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PRINCIPLES OF FINANCE

Table of Contents

Introduction:....................................................................................................................................2

Answer to Part i:..............................................................................................................................2

Answer to Part ii:.............................................................................................................................5

Answer to Part iii:............................................................................................................................8

Answer to Part iv:..........................................................................................................................10

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

Table of Contents

Introduction:....................................................................................................................................2

Answer to Part i:..............................................................................................................................2

Answer to Part ii:.............................................................................................................................5

Answer to Part iii:............................................................................................................................8

Answer to Part iv:..........................................................................................................................10

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

2PRINCIPLES OF FINANCE

Introduction:

The current report would focus on analysing the capital structure of Retail Food Group

(RFG), which is a popular food and beverage organisation in Australia. In addition, it supplies

greater quality coffee products and it has become emerging leader in dairy processing, wholesale

bakery and foodservice sectors of the nation (Retail Food Group 2018). The first section of the

report would focus on analysing the capital structure of the organisation for the past five years.

The second segment would evaluate the dividend history over the past five years as well for

enabling the shareholders to provide an overview about the earnings of the shareholders. The

third section would lay stress on evaluating the trend in share price over the past five years.

Finally, the report would shed light on evaluating the attractiveness of the shares of RFG for

investment purpose.

Answer to Part i:

For analysing and commenting on the capital structure of Retail Food Group, the

following capital structure ratios have been taken into consideration, which are illustrated in the

form of a table as follows:

Particulars Details 2013 2014 2015 2016 2017

Total liabilities A 131 88 276 267 464

Total equity B 240 310 404 434 465

Total assets C 371 398 680 702 930

Current liabilities D 20 19 97 50 91

Debt-to-equity A/B 54.58 28.39 68.32 61.52 99.78

Introduction:

The current report would focus on analysing the capital structure of Retail Food Group

(RFG), which is a popular food and beverage organisation in Australia. In addition, it supplies

greater quality coffee products and it has become emerging leader in dairy processing, wholesale

bakery and foodservice sectors of the nation (Retail Food Group 2018). The first section of the

report would focus on analysing the capital structure of the organisation for the past five years.

The second segment would evaluate the dividend history over the past five years as well for

enabling the shareholders to provide an overview about the earnings of the shareholders. The

third section would lay stress on evaluating the trend in share price over the past five years.

Finally, the report would shed light on evaluating the attractiveness of the shares of RFG for

investment purpose.

Answer to Part i:

For analysing and commenting on the capital structure of Retail Food Group, the

following capital structure ratios have been taken into consideration, which are illustrated in the

form of a table as follows:

Particulars Details 2013 2014 2015 2016 2017

Total liabilities A 131 88 276 267 464

Total equity B 240 310 404 434 465

Total assets C 371 398 680 702 930

Current liabilities D 20 19 97 50 91

Debt-to-equity A/B 54.58 28.39 68.32 61.52 99.78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PRINCIPLES OF FINANCE

ratio % % % % %

Debt ratio A/C

35.31

%

22.11

%

40.59

%

38.03

%

49.89

%

Equity ratio B/C

64.69

%

77.89

%

59.41

%

61.82

%

50.00

%

Capital gearing

ratio

(A-D)/(C-

D)

31.62

%

18.21

%

30.70

%

33.28

%

44.46

%

Table 1: Capital structure ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

2013 2014 2015 2016 2017

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

Capital structure ratios of RFG

Debt-to-equity ratio

Debt ratio

Equity ratio

Capital gearing ratio

Figure 1: Capital structure ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

ratio % % % % %

Debt ratio A/C

35.31

%

22.11

%

40.59

%

38.03

%

49.89

%

Equity ratio B/C

64.69

%

77.89

%

59.41

%

61.82

%

50.00

%

Capital gearing

ratio

(A-D)/(C-

D)

31.62

%

18.21

%

30.70

%

33.28

%

44.46

%

Table 1: Capital structure ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

2013 2014 2015 2016 2017

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

Capital structure ratios of RFG

Debt-to-equity ratio

Debt ratio

Equity ratio

Capital gearing ratio

Figure 1: Capital structure ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PRINCIPLES OF FINANCE

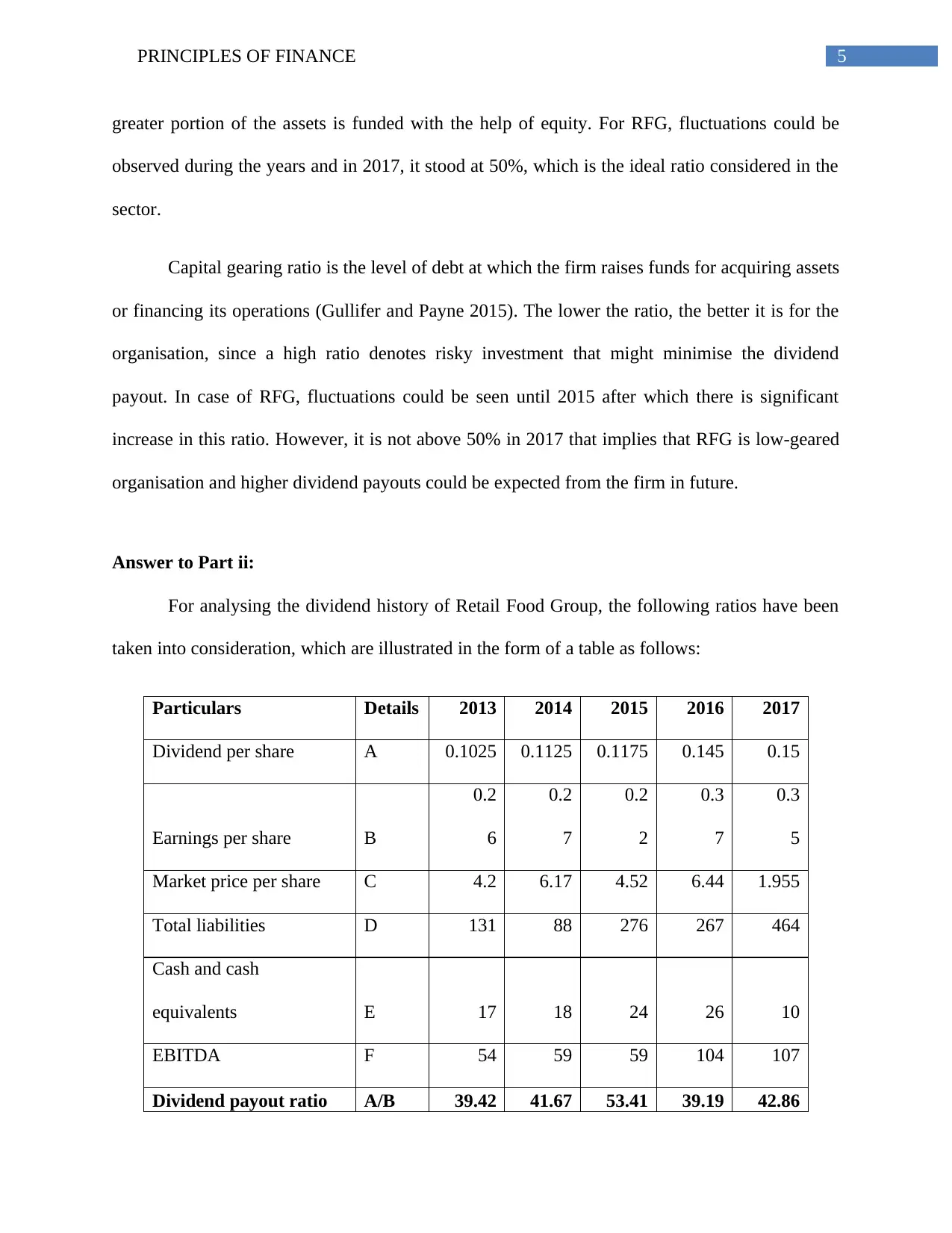

According to the above figure, it could be observed that the debt-to-equity ratio of RFG

has fallen drastically from 54.58% in 2013 to 28.39% in 2014; however, it has increased to

68.32% in 2015 and the trend is declining again to 61.52% in 2016. The increase is significant to

99.78% in 2017, which denotes that the organisation is highly reliant on debt for raising funds

for its capital projects and investments in existing operations. As commented by Brooks (2015),

debt-to-equity ratio is a capital structure ratio that denotes the soundness of long-term financial

policies of the organisation. A ratio of 100% denotes that both the creditors and shareholders’

contribute to the business assets. From the perspective of the creditors, low ratio is favourable, as

greater protection is ensured for their money. However, the shareholders intend to seek benefits

from the funds that the creditors provide and hence, they prefer higher debt-to-equity ratio. A

ratio of 100% is considered ideal for the food and beverage industry of Australia and in case of

RFG, the ratio is closer to the ideal standard in 2017 and thus, it is maintaining optimal balance

of debt and equity.

Debt ratio gauges the financial leverage of an organisation, which enables the creditors

and the investors to evaluate the debt burden on the organisation along with firm’s liabilities to

pay off its debt in future (Ferran and Ho 2014). A ratio of 50% is considered favourable, since it

helps in maintaining optimality in the capital structure of the firm. In case of RFG, the trend is

fluctuating over the five-year period and finally, the ratio stood at 49.89% in 2017. It is closer to

the above-stated ideal ratio, which denotes that the asset base of the organisation is as twice as its

liabilities. Hence, the debt ratio denotes the optimal capital structure of RFG as well.

Equity ratio could be denoted as the capital structure ratio that gauges the asset amount

owned on the part of the owners by contrasting total equity in the organisation to total assets

(Gitman, Juchau and Flanagan 2015). The lower ratio is always favourable, since it denotes that

According to the above figure, it could be observed that the debt-to-equity ratio of RFG

has fallen drastically from 54.58% in 2013 to 28.39% in 2014; however, it has increased to

68.32% in 2015 and the trend is declining again to 61.52% in 2016. The increase is significant to

99.78% in 2017, which denotes that the organisation is highly reliant on debt for raising funds

for its capital projects and investments in existing operations. As commented by Brooks (2015),

debt-to-equity ratio is a capital structure ratio that denotes the soundness of long-term financial

policies of the organisation. A ratio of 100% denotes that both the creditors and shareholders’

contribute to the business assets. From the perspective of the creditors, low ratio is favourable, as

greater protection is ensured for their money. However, the shareholders intend to seek benefits

from the funds that the creditors provide and hence, they prefer higher debt-to-equity ratio. A

ratio of 100% is considered ideal for the food and beverage industry of Australia and in case of

RFG, the ratio is closer to the ideal standard in 2017 and thus, it is maintaining optimal balance

of debt and equity.

Debt ratio gauges the financial leverage of an organisation, which enables the creditors

and the investors to evaluate the debt burden on the organisation along with firm’s liabilities to

pay off its debt in future (Ferran and Ho 2014). A ratio of 50% is considered favourable, since it

helps in maintaining optimality in the capital structure of the firm. In case of RFG, the trend is

fluctuating over the five-year period and finally, the ratio stood at 49.89% in 2017. It is closer to

the above-stated ideal ratio, which denotes that the asset base of the organisation is as twice as its

liabilities. Hence, the debt ratio denotes the optimal capital structure of RFG as well.

Equity ratio could be denoted as the capital structure ratio that gauges the asset amount

owned on the part of the owners by contrasting total equity in the organisation to total assets

(Gitman, Juchau and Flanagan 2015). The lower ratio is always favourable, since it denotes that

5PRINCIPLES OF FINANCE

greater portion of the assets is funded with the help of equity. For RFG, fluctuations could be

observed during the years and in 2017, it stood at 50%, which is the ideal ratio considered in the

sector.

Capital gearing ratio is the level of debt at which the firm raises funds for acquiring assets

or financing its operations (Gullifer and Payne 2015). The lower the ratio, the better it is for the

organisation, since a high ratio denotes risky investment that might minimise the dividend

payout. In case of RFG, fluctuations could be seen until 2015 after which there is significant

increase in this ratio. However, it is not above 50% in 2017 that implies that RFG is low-geared

organisation and higher dividend payouts could be expected from the firm in future.

Answer to Part ii:

For analysing the dividend history of Retail Food Group, the following ratios have been

taken into consideration, which are illustrated in the form of a table as follows:

Particulars Details 2013 2014 2015 2016 2017

Dividend per share A 0.1025 0.1125 0.1175 0.145 0.15

Earnings per share B

0.2

6

0.2

7

0.2

2

0.3

7

0.3

5

Market price per share C 4.2 6.17 4.52 6.44 1.955

Total liabilities D 131 88 276 267 464

Cash and cash

equivalents E 17 18 24 26 10

EBITDA F 54 59 59 104 107

Dividend payout ratio A/B 39.42 41.67 53.41 39.19 42.86

greater portion of the assets is funded with the help of equity. For RFG, fluctuations could be

observed during the years and in 2017, it stood at 50%, which is the ideal ratio considered in the

sector.

Capital gearing ratio is the level of debt at which the firm raises funds for acquiring assets

or financing its operations (Gullifer and Payne 2015). The lower the ratio, the better it is for the

organisation, since a high ratio denotes risky investment that might minimise the dividend

payout. In case of RFG, fluctuations could be seen until 2015 after which there is significant

increase in this ratio. However, it is not above 50% in 2017 that implies that RFG is low-geared

organisation and higher dividend payouts could be expected from the firm in future.

Answer to Part ii:

For analysing the dividend history of Retail Food Group, the following ratios have been

taken into consideration, which are illustrated in the form of a table as follows:

Particulars Details 2013 2014 2015 2016 2017

Dividend per share A 0.1025 0.1125 0.1175 0.145 0.15

Earnings per share B

0.2

6

0.2

7

0.2

2

0.3

7

0.3

5

Market price per share C 4.2 6.17 4.52 6.44 1.955

Total liabilities D 131 88 276 267 464

Cash and cash

equivalents E 17 18 24 26 10

EBITDA F 54 59 59 104 107

Dividend payout ratio A/B 39.42 41.67 53.41 39.19 42.86

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PRINCIPLES OF FINANCE

% % % % %

Dividend coverage ratio B/A

2.5

4

2.4

0

1.8

7

2.5

5

2.3

3

Dividend yield ratio A/C 2.44% 1.82% 2.60% 2.25% 7.67%

Net debt to EBITDA

ratio

(D-

E)/F 2.11 1.19 4.27 2.32 4.24

Table 2: Dividend ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

2013 2014 2015 2016 2017

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Dividend history of RFG

Dividend payout ratio

Dividend coverage ratio

Dividend yield ratio

Net debt to EBITDA ratio

Figure 2: Dividend ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

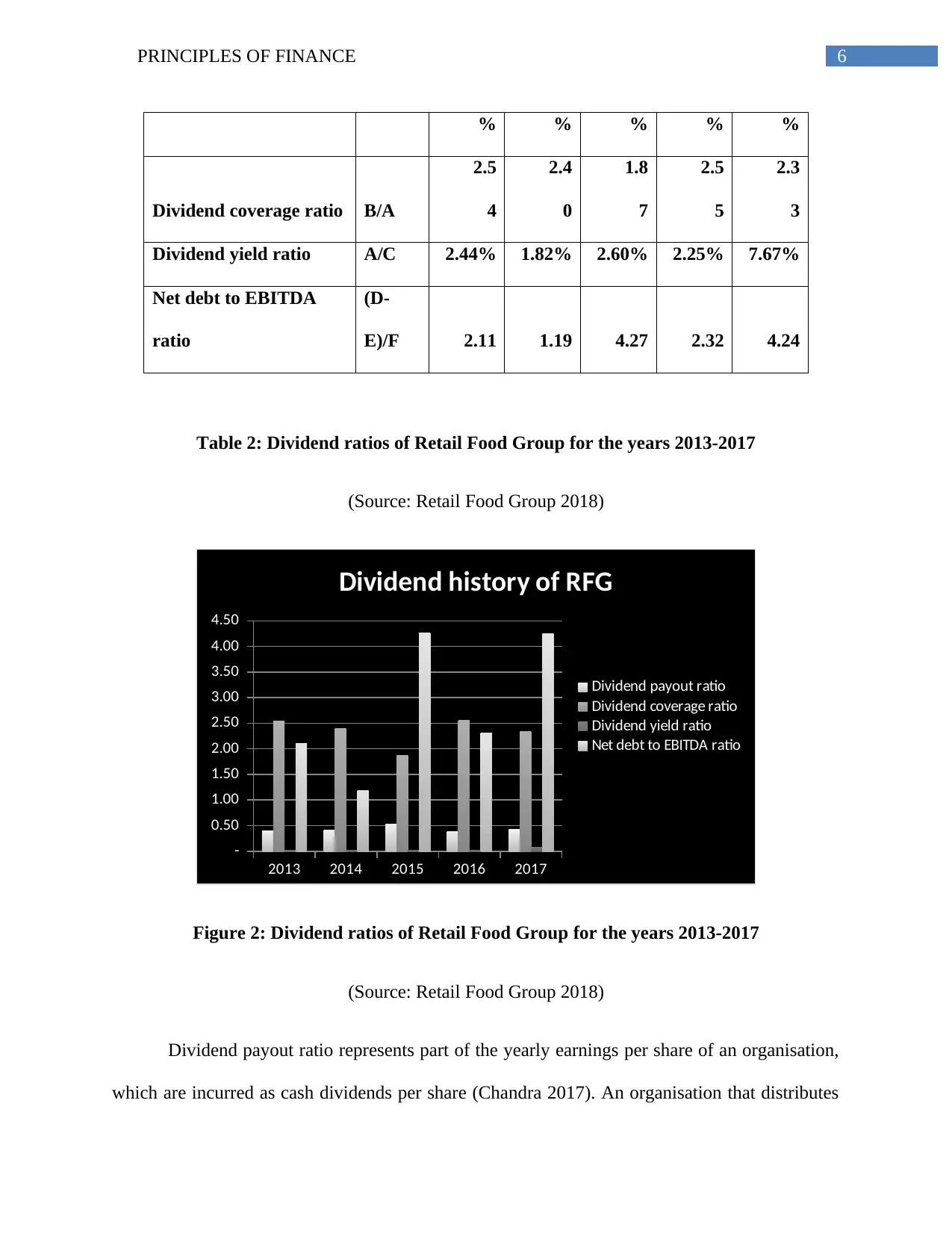

Dividend payout ratio represents part of the yearly earnings per share of an organisation,

which are incurred as cash dividends per share (Chandra 2017). An organisation that distributes

% % % % %

Dividend coverage ratio B/A

2.5

4

2.4

0

1.8

7

2.5

5

2.3

3

Dividend yield ratio A/C 2.44% 1.82% 2.60% 2.25% 7.67%

Net debt to EBITDA

ratio

(D-

E)/F 2.11 1.19 4.27 2.32 4.24

Table 2: Dividend ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

2013 2014 2015 2016 2017

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Dividend history of RFG

Dividend payout ratio

Dividend coverage ratio

Dividend yield ratio

Net debt to EBITDA ratio

Figure 2: Dividend ratios of Retail Food Group for the years 2013-2017

(Source: Retail Food Group 2018)

Dividend payout ratio represents part of the yearly earnings per share of an organisation,

which are incurred as cash dividends per share (Chandra 2017). An organisation that distributes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRINCIPLES OF FINANCE

nearly 50% of its earnings is stable, since earnings could be generated in long-term. On the other

hand, the companies paying higher dividend payout ratio above 50% might struggle to maintain

their dividends over long-term. In case of RFG, the dividend payout ratio has remained stable

over the years below 50%; the only exception could be observed in 2015 where the organisation

has made greater net income.

Dividend cover ratio denotes the number of times an organisation could pay dividends to

the common shareholders by using its net income over a particular year. A higher ratio is more

preferable, since greater dividend stock payments are estimated in future. If the ratio is above 1,

it is expected that the organisation is financially stable to ensure higher returns to the

shareholders (Damodaran 2016). In case of RFG, the dividend cover ratio is above 1 all the

years, which denotes that the organisation has adequate stability in the market.

The above figure clearly denotes that the dividend yield ratio of RFG has increased

significantly in 2017, which implies greater amount of dividends has been earned on each dollar

of investment. The higher ratio denotes that maximum amount of the dollar earned is not utilised

for reinvestment in business operations to make capital gains (Frank and Keith 2016). Thus, in

case of RFG, decline might be observed in dividend payments to the shareholders in future;

however, the other pertinent factors need to be taken into consideration.

As commented by Ihori (2016), net debt to EBITDA ratio gauges the leverage of an

organisation and its capability of clearing the overall debt obligations (Kane 2018). A lower ratio

is always preferable for the investors, since a higher ratio indicates that the organisation might

minimise its dividend in future. In this case, a significant increase in the ratio could be observed

for RFG in 2017, which denotes that the dividend payments could be minimised in future.

nearly 50% of its earnings is stable, since earnings could be generated in long-term. On the other

hand, the companies paying higher dividend payout ratio above 50% might struggle to maintain

their dividends over long-term. In case of RFG, the dividend payout ratio has remained stable

over the years below 50%; the only exception could be observed in 2015 where the organisation

has made greater net income.

Dividend cover ratio denotes the number of times an organisation could pay dividends to

the common shareholders by using its net income over a particular year. A higher ratio is more

preferable, since greater dividend stock payments are estimated in future. If the ratio is above 1,

it is expected that the organisation is financially stable to ensure higher returns to the

shareholders (Damodaran 2016). In case of RFG, the dividend cover ratio is above 1 all the

years, which denotes that the organisation has adequate stability in the market.

The above figure clearly denotes that the dividend yield ratio of RFG has increased

significantly in 2017, which implies greater amount of dividends has been earned on each dollar

of investment. The higher ratio denotes that maximum amount of the dollar earned is not utilised

for reinvestment in business operations to make capital gains (Frank and Keith 2016). Thus, in

case of RFG, decline might be observed in dividend payments to the shareholders in future;

however, the other pertinent factors need to be taken into consideration.

As commented by Ihori (2016), net debt to EBITDA ratio gauges the leverage of an

organisation and its capability of clearing the overall debt obligations (Kane 2018). A lower ratio

is always preferable for the investors, since a higher ratio indicates that the organisation might

minimise its dividend in future. In this case, a significant increase in the ratio could be observed

for RFG in 2017, which denotes that the dividend payments could be minimised in future.

8PRINCIPLES OF FINANCE

Answer to Part iii:

Date RFG share price ASX share price

1/31/2012 2.75 29.08

2/29/2012 2.65 29.80

3/31/2012 2.72 30.76

4/30/2012 2.7 28.64

5/31/2012 2.65 28.38

6/30/2012 2.6 29.45

7/31/2012 2.91 27.10

8/31/2012 2.96 28.96

9/30/2012 3.18 28.93

10/31/2012 2.98 28.26

11/30/2012 3.17 28.98

12/31/2012 3.39 30.73

1/31/2013 3.61 34.42

2/28/2013 3.59 34.34

3/31/2013 3.98 35.30

4/30/2013 3.84 36.62

5/31/2013 3.95 32.06

6/30/2013 4.2 32.94

7/31/2013 4.23 34.33

8/31/2013 4.3 34.20

9/30/2013 4.36 34.01

10/31/2013 4.44 36.00

11/30/2013 4.6 35.00

12/31/2013 4.2 35.26

1/31/2014 4.51 34.21

2/28/2014 4.37 35.62

3/31/2014 4.18 34.66

4/30/2014 4.23 35.04

5/31/2014 4.54 35.10

6/30/2014 4.68 35.21

7/31/2014 4.74 35.22

8/31/2014 4.94 35.49

9/30/2014 5.57 34.07

10/31/2014 5.65 35.14

11/30/2014 5.76 34.99

12/31/2014 6.17 36.05

1/31/2015 7.56 38.00

2/28/2015 7.06 41.16

3/31/2015 6.95 41.10

4/30/2015 6.65 40.85

5/31/2015 5.43 39.19

6/30/2015 5.34 39.94

7/31/2015 5.28 37.83

8/31/2015 4.14 36.66

9/30/2015 4.63 38.12

10/31/2015 4.48 39.25

11/30/2015 4.63 39.28

12/31/2015 4.52 37.40

1/31/2016 4.31 38.40

2/29/2016 5.16 40.65

3/31/2016 5.5 40.65

4/30/2016 5.52 43.01

5/31/2016 5.53 43.43

6/30/2016 5.77 45.65

7/31/2016 6.87 48.58

8/31/2016 6.97 47.16

9/30/2016 6.77 46.71

10/31/2016 6.19 44.57

11/30/2016 7.02 47.19

12/31/2016 6.44 48.54

1/31/2017 5.55 49.38

2/28/2017 5.33 48.87

3/31/2017 5.46 48.56

4/30/2017 5.14 50.64

5/31/2017 4.7 49.40

6/30/2017 4.85 51.41

7/31/2017 5 52.00

8/31/2017 4.28 51.81

9/30/2017 4.4 52.15

10/31/2017 4.51 53.75

11/30/2017 2.47 53.99

12/31/2017 1.955 54.09

Correlation

Average return 4.66 38.94

Risk 1.29 7.53

0.45

Answer to Part iii:

Date RFG share price ASX share price

1/31/2012 2.75 29.08

2/29/2012 2.65 29.80

3/31/2012 2.72 30.76

4/30/2012 2.7 28.64

5/31/2012 2.65 28.38

6/30/2012 2.6 29.45

7/31/2012 2.91 27.10

8/31/2012 2.96 28.96

9/30/2012 3.18 28.93

10/31/2012 2.98 28.26

11/30/2012 3.17 28.98

12/31/2012 3.39 30.73

1/31/2013 3.61 34.42

2/28/2013 3.59 34.34

3/31/2013 3.98 35.30

4/30/2013 3.84 36.62

5/31/2013 3.95 32.06

6/30/2013 4.2 32.94

7/31/2013 4.23 34.33

8/31/2013 4.3 34.20

9/30/2013 4.36 34.01

10/31/2013 4.44 36.00

11/30/2013 4.6 35.00

12/31/2013 4.2 35.26

1/31/2014 4.51 34.21

2/28/2014 4.37 35.62

3/31/2014 4.18 34.66

4/30/2014 4.23 35.04

5/31/2014 4.54 35.10

6/30/2014 4.68 35.21

7/31/2014 4.74 35.22

8/31/2014 4.94 35.49

9/30/2014 5.57 34.07

10/31/2014 5.65 35.14

11/30/2014 5.76 34.99

12/31/2014 6.17 36.05

1/31/2015 7.56 38.00

2/28/2015 7.06 41.16

3/31/2015 6.95 41.10

4/30/2015 6.65 40.85

5/31/2015 5.43 39.19

6/30/2015 5.34 39.94

7/31/2015 5.28 37.83

8/31/2015 4.14 36.66

9/30/2015 4.63 38.12

10/31/2015 4.48 39.25

11/30/2015 4.63 39.28

12/31/2015 4.52 37.40

1/31/2016 4.31 38.40

2/29/2016 5.16 40.65

3/31/2016 5.5 40.65

4/30/2016 5.52 43.01

5/31/2016 5.53 43.43

6/30/2016 5.77 45.65

7/31/2016 6.87 48.58

8/31/2016 6.97 47.16

9/30/2016 6.77 46.71

10/31/2016 6.19 44.57

11/30/2016 7.02 47.19

12/31/2016 6.44 48.54

1/31/2017 5.55 49.38

2/28/2017 5.33 48.87

3/31/2017 5.46 48.56

4/30/2017 5.14 50.64

5/31/2017 4.7 49.40

6/30/2017 4.85 51.41

7/31/2017 5 52.00

8/31/2017 4.28 51.81

9/30/2017 4.4 52.15

10/31/2017 4.51 53.75

11/30/2017 2.47 53.99

12/31/2017 1.955 54.09

Correlation

Average return 4.66 38.94

Risk 1.29 7.53

0.45

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PRINCIPLES OF FINANCE

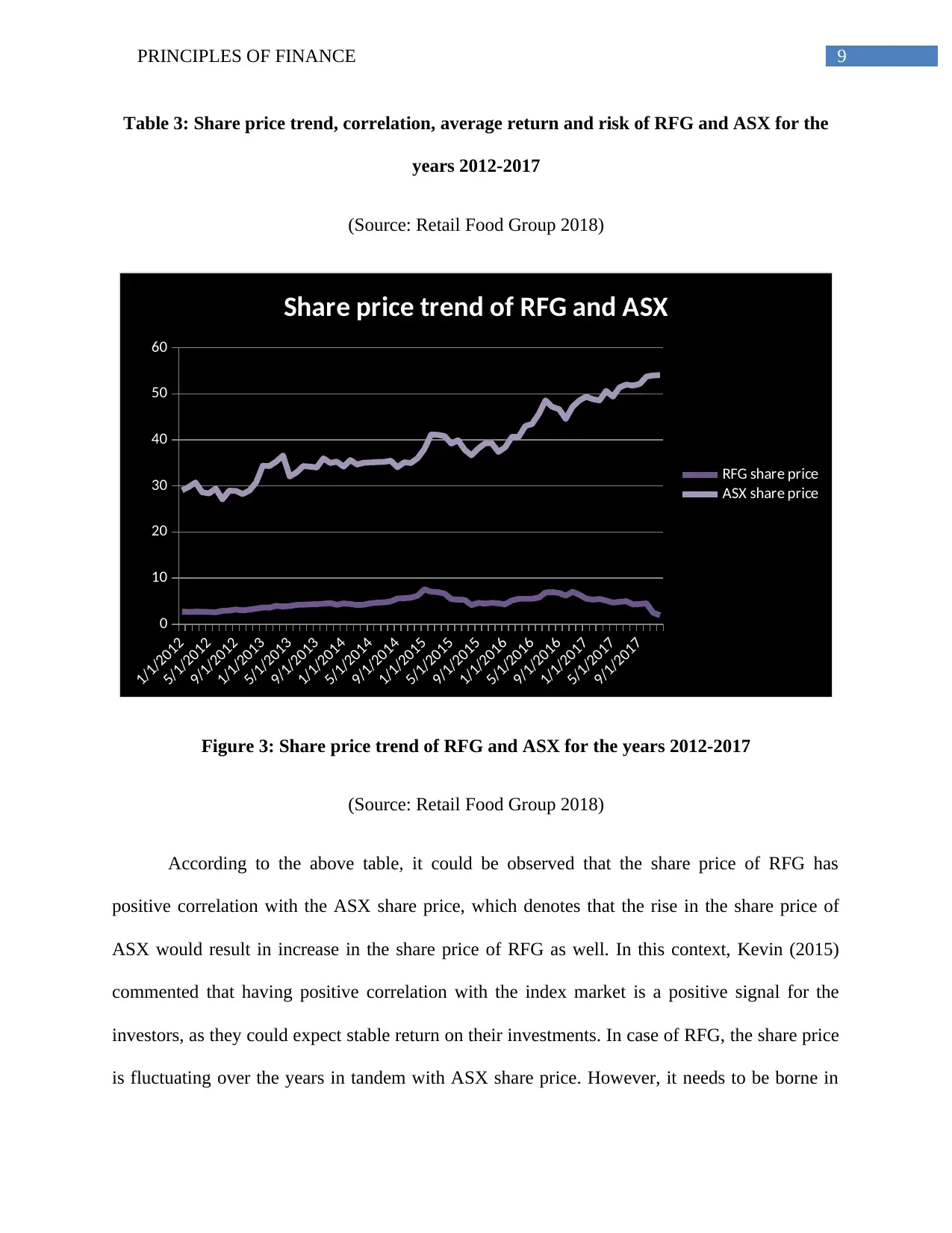

Table 3: Share price trend, correlation, average return and risk of RFG and ASX for the

years 2012-2017

(Source: Retail Food Group 2018)

1/1/2012

5/1/2012

9/1/2012

1/1/2013

5/1/2013

9/1/2013

1/1/2014

5/1/2014

9/1/2014

1/1/2015

5/1/2015

9/1/2015

1/1/2016

5/1/2016

9/1/2016

1/1/2017

5/1/2017

9/1/2017

0

10

20

30

40

50

60

Share price trend of RFG and ASX

RFG share price

ASX share price

Figure 3: Share price trend of RFG and ASX for the years 2012-2017

(Source: Retail Food Group 2018)

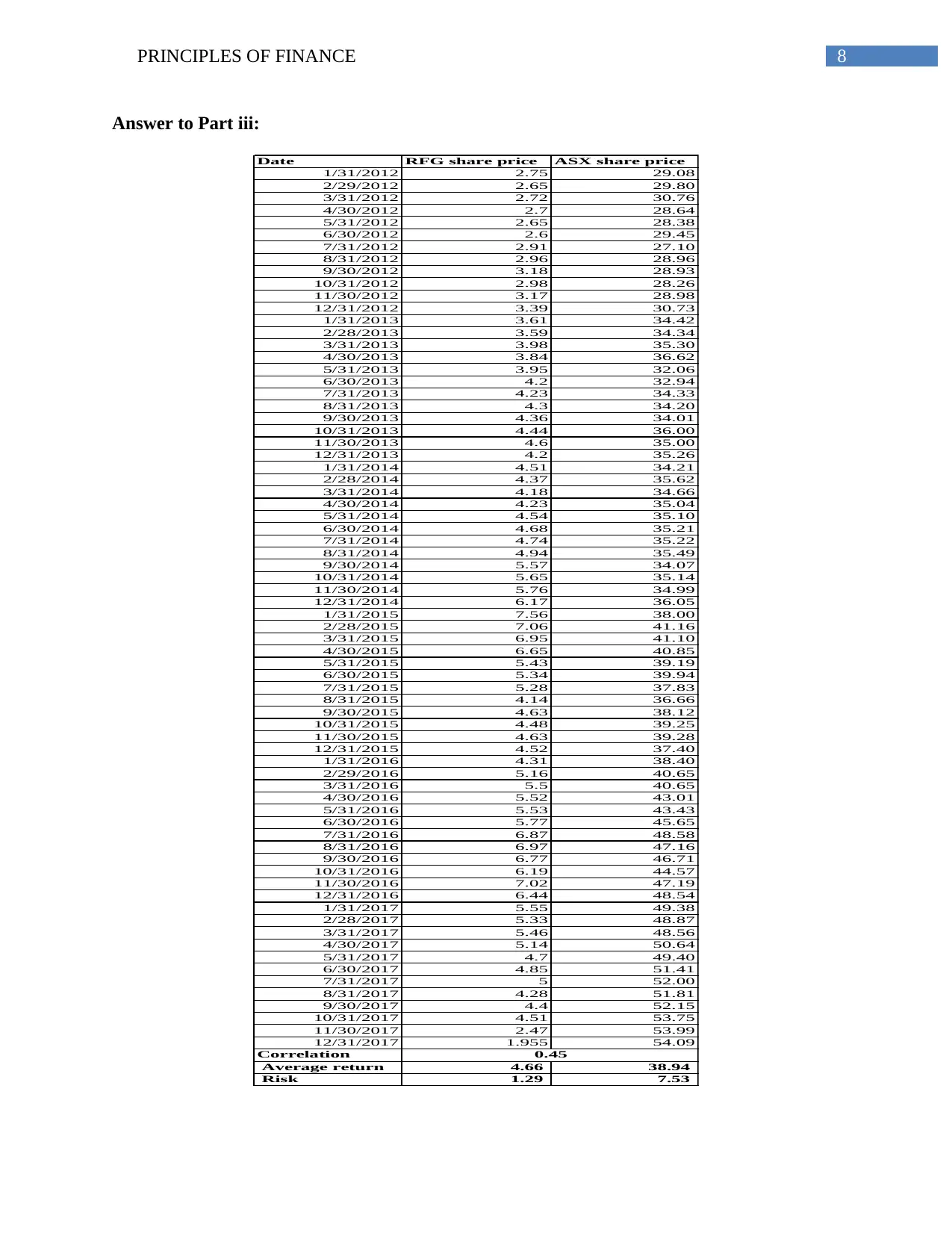

According to the above table, it could be observed that the share price of RFG has

positive correlation with the ASX share price, which denotes that the rise in the share price of

ASX would result in increase in the share price of RFG as well. In this context, Kevin (2015)

commented that having positive correlation with the index market is a positive signal for the

investors, as they could expect stable return on their investments. In case of RFG, the share price

is fluctuating over the years in tandem with ASX share price. However, it needs to be borne in

Table 3: Share price trend, correlation, average return and risk of RFG and ASX for the

years 2012-2017

(Source: Retail Food Group 2018)

1/1/2012

5/1/2012

9/1/2012

1/1/2013

5/1/2013

9/1/2013

1/1/2014

5/1/2014

9/1/2014

1/1/2015

5/1/2015

9/1/2015

1/1/2016

5/1/2016

9/1/2016

1/1/2017

5/1/2017

9/1/2017

0

10

20

30

40

50

60

Share price trend of RFG and ASX

RFG share price

ASX share price

Figure 3: Share price trend of RFG and ASX for the years 2012-2017

(Source: Retail Food Group 2018)

According to the above table, it could be observed that the share price of RFG has

positive correlation with the ASX share price, which denotes that the rise in the share price of

ASX would result in increase in the share price of RFG as well. In this context, Kevin (2015)

commented that having positive correlation with the index market is a positive signal for the

investors, as they could expect stable return on their investments. In case of RFG, the share price

is fluctuating over the years in tandem with ASX share price. However, it needs to be borne in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PRINCIPLES OF FINANCE

mind that even though both the stocks have provided positive returns to the investors over the

year; however, significant risk is inherent in both the stocks. This is because a stock having

standard deviation of above 1 is considered risky for the investors, as the return could be

minimised significantly due to inflationary effects (Mahakud and Mishra 2014). Therefore, as

per the share price analysis trend, it could be stated that RFG is maintaining a stable financial

position in the food and beverage industry of Australia. However, it needs to focus on

maximising its retained earnings due to higher level of risk in the stocks for combating with any

unforeseen events like inflation or fall in sudden market price in order to ensure regular returns

to its shareholders (Titman, Keown and Martin 2017).

Answer to Part iv:

For evaluating the financial attractiveness of Retail Food Group, the following ratios

have been taken into consideration:

Particulars Details 2013 2014 2015 2016 2017

Market value per

share A 4.20 6.17 4.52 6.44 1.955

Earnings per share B 0.26 0.27 0.22 0.37 0.35

Market value of

equity C 240 310 404 434 465

Market value of debt D 131 88 276 267 464

Cash and

investments E 17 18 24 26 10

Price/earnings ratio A/B 16.15 22.85 20.55 17.41 5.59

mind that even though both the stocks have provided positive returns to the investors over the

year; however, significant risk is inherent in both the stocks. This is because a stock having

standard deviation of above 1 is considered risky for the investors, as the return could be

minimised significantly due to inflationary effects (Mahakud and Mishra 2014). Therefore, as

per the share price analysis trend, it could be stated that RFG is maintaining a stable financial

position in the food and beverage industry of Australia. However, it needs to focus on

maximising its retained earnings due to higher level of risk in the stocks for combating with any

unforeseen events like inflation or fall in sudden market price in order to ensure regular returns

to its shareholders (Titman, Keown and Martin 2017).

Answer to Part iv:

For evaluating the financial attractiveness of Retail Food Group, the following ratios

have been taken into consideration:

Particulars Details 2013 2014 2015 2016 2017

Market value per

share A 4.20 6.17 4.52 6.44 1.955

Earnings per share B 0.26 0.27 0.22 0.37 0.35

Market value of

equity C 240 310 404 434 465

Market value of debt D 131 88 276 267 464

Cash and

investments E 17 18 24 26 10

Price/earnings ratio A/B 16.15 22.85 20.55 17.41 5.59

11PRINCIPLES OF FINANCE

Enterprise value C+D-E 354 380 656 675 919

Table 4: Price/earnings ratio and enterprise value of RFG Limited for the years 2013-2017

(Source: Retail Food Group 2018)

As laid out by Peirson et al. (2014), price/earnings ratio signifies the amount that an

investor could expect to invest in an organisation for earnings a single dollar of its earnings. A

ratio above 1 is considered feasible for the organisations running their business operations in the

food and beverage industry of Australia. In this case, even though there is significant decline in

the ratio from 17.41 in 2016 to 5.59 in 2017, it is still above the ideal standard. In addition,

increase in enterprise value could be observed for RFG over the years as well. Hence, it denotes

the organisation is highly attractive in the market for making investments. This could be

elaborated in a better way by relating with the efficient market hypothesis.

According to Titman and Martin (2014), efficient market hypothesis states that the stock

market could not be beaten, since stock market efficiency causes the current share prices to

incorporate and include all pertinent information. This theory assumes that stocks are traded at

fair values in the market. As a result, the investors find it difficult to buy undervalued shares or

sell securities at overvalued prices. In case of RFG, it could be observed that the market value of

the shares of the organisation is rightly valued, since its risk is high as well. In addition, the

return provided has increased in tandem with ASX as well. Hence, it could be stated that the

investors might find high prospects by investing in the shares of RFG, since their returns are

expected to be maximised over the years.

Enterprise value C+D-E 354 380 656 675 919

Table 4: Price/earnings ratio and enterprise value of RFG Limited for the years 2013-2017

(Source: Retail Food Group 2018)

As laid out by Peirson et al. (2014), price/earnings ratio signifies the amount that an

investor could expect to invest in an organisation for earnings a single dollar of its earnings. A

ratio above 1 is considered feasible for the organisations running their business operations in the

food and beverage industry of Australia. In this case, even though there is significant decline in

the ratio from 17.41 in 2016 to 5.59 in 2017, it is still above the ideal standard. In addition,

increase in enterprise value could be observed for RFG over the years as well. Hence, it denotes

the organisation is highly attractive in the market for making investments. This could be

elaborated in a better way by relating with the efficient market hypothesis.

According to Titman and Martin (2014), efficient market hypothesis states that the stock

market could not be beaten, since stock market efficiency causes the current share prices to

incorporate and include all pertinent information. This theory assumes that stocks are traded at

fair values in the market. As a result, the investors find it difficult to buy undervalued shares or

sell securities at overvalued prices. In case of RFG, it could be observed that the market value of

the shares of the organisation is rightly valued, since its risk is high as well. In addition, the

return provided has increased in tandem with ASX as well. Hence, it could be stated that the

investors might find high prospects by investing in the shares of RFG, since their returns are

expected to be maximised over the years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12PRINCIPLES OF FINANCE

Conclusion:

Based on the above evaluation, it could be stated that RFG has maintained optimal capital

structure by proper balance of debt and equity. The dividend payments for the organisation are

consistent as well over the years; however, it is expected to be minimised in future. It could be

observed that the market value of the shares of the organisation is rightly valued, since its risk is

high as well. In addition, the return provided has increased in tandem with ASX as well. Hence,

it could be stated that the investors might find high prospects by investing in the shares of RFG,

since their returns are expected to be maximised over the years.

Conclusion:

Based on the above evaluation, it could be stated that RFG has maintained optimal capital

structure by proper balance of debt and equity. The dividend payments for the organisation are

consistent as well over the years; however, it is expected to be minimised in future. It could be

observed that the market value of the shares of the organisation is rightly valued, since its risk is

high as well. In addition, the return provided has increased in tandem with ASX as well. Hence,

it could be stated that the investors might find high prospects by investing in the shares of RFG,

since their returns are expected to be maximised over the years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13PRINCIPLES OF FINANCE

References:

Brooks, R., 2015. Financial management: core concepts. Pearson.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University Press.

Frank, K.R. and Keith, C.B., 2016. Investment analysis and portfolio management.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy. Bloomsbury

Publishing.

Ihori, T., 2016. Principles of Public Finance. Springer.

Kane, D.R., 2018. Principles of international finance. Routledge.

Kevin, S., 2015. Security analysis and portfolio management. PHI Learning Pvt. Ltd.

Mahakud, J. and Mishra, C.S., 2014. Security Analysis and Portfolio Management.

Peirson, G., Brown, R., Easton, S. and Howard, P., 2014. Business finance. McGraw-Hill

Education Australia.

References:

Brooks, R., 2015. Financial management: core concepts. Pearson.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University Press.

Frank, K.R. and Keith, C.B., 2016. Investment analysis and portfolio management.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy. Bloomsbury

Publishing.

Ihori, T., 2016. Principles of Public Finance. Springer.

Kane, D.R., 2018. Principles of international finance. Routledge.

Kevin, S., 2015. Security analysis and portfolio management. PHI Learning Pvt. Ltd.

Mahakud, J. and Mishra, C.S., 2014. Security Analysis and Portfolio Management.

Peirson, G., Brown, R., Easton, S. and Howard, P., 2014. Business finance. McGraw-Hill

Education Australia.

14PRINCIPLES OF FINANCE

Retail Food Group., 2018. Annual Reports - Retail Food Group. [online] Available at:

http://rfg.com.au/shareholder-center/annual-reports/ [Accessed 11 May 2018].

Retail Food Group., 2018. Home - Retail Food Group. [online] Available at: http://rfg.com.au/

[Accessed 11 May 2018].

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Retail Food Group., 2018. Annual Reports - Retail Food Group. [online] Available at:

http://rfg.com.au/shareholder-center/annual-reports/ [Accessed 11 May 2018].

Retail Food Group., 2018. Home - Retail Food Group. [online] Available at: http://rfg.com.au/

[Accessed 11 May 2018].

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.