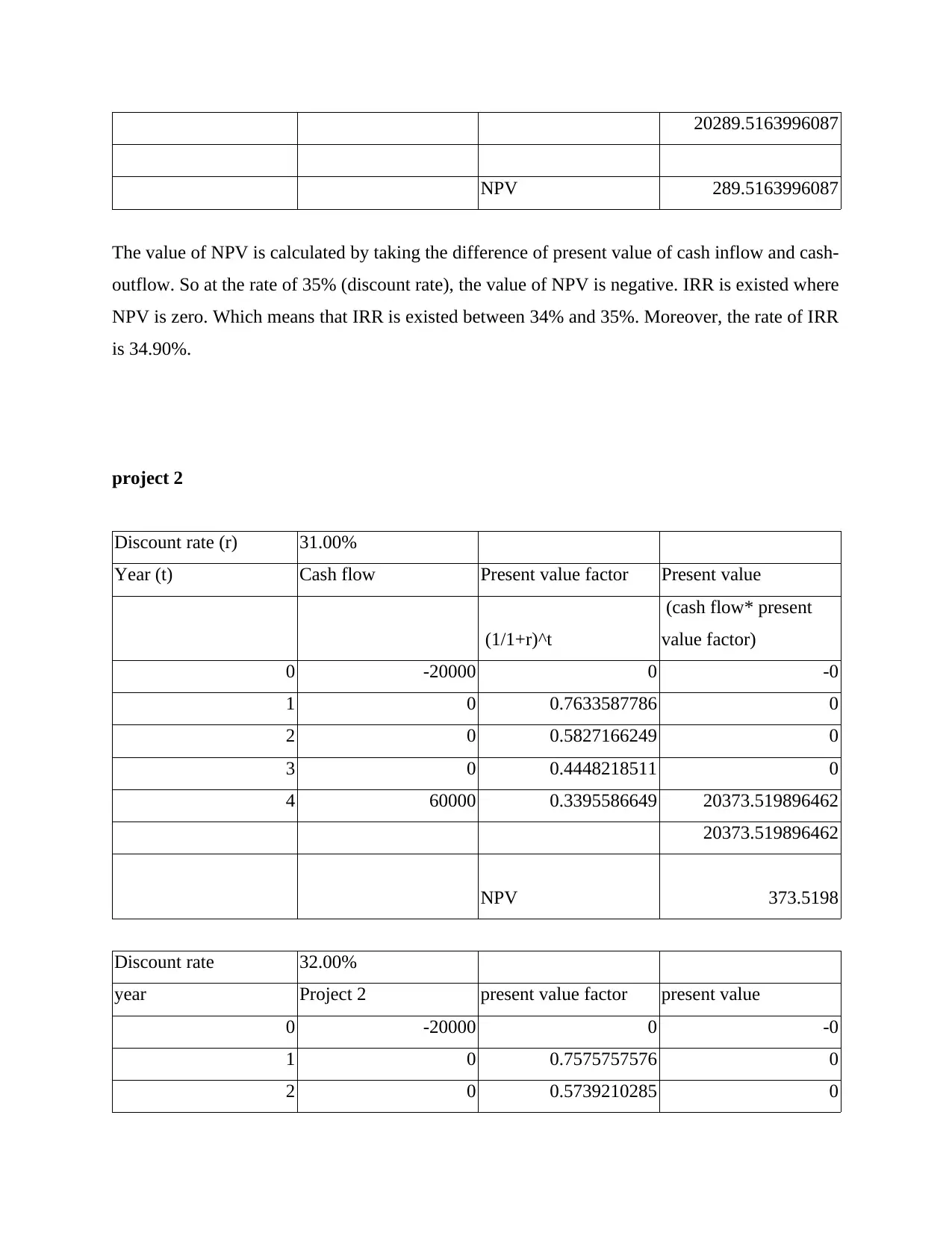

Principles of Finance: IRR, NPV, Bond Pricing, Cash Flow, Savage Value, and NPV Calculation

VerifiedAdded on 2023/06/17

|17

|3055

|388

AI Summary

This article covers topics related to Principles of Finance such as IRR, NPV, Bond Pricing, Cash Flow, Savage Value, and NPV Calculation. It includes solved examples and calculations for better understanding.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

PRINCIPLES OF FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

(a) calculation of IRR..................................................................................................................3

(b) calculation of NPV.................................................................................................................5

Question 2....................................................................................................................................6

Question 3....................................................................................................................................7

Question 4....................................................................................................................................7

a....................................................................................................................................................7

Question 4.b.................................................................................................................................7

Question 4.c.................................................................................................................................7

Question 5....................................................................................................................................8

Question 6....................................................................................................................................8

a)..................................................................................................................................................8

b)..................................................................................................................................................9

c)..................................................................................................................................................9

d)..................................................................................................................................................9

Question 7..................................................................................................................................10

Question 8..................................................................................................................................10

SECTION B...................................................................................................................................12

Question 1..................................................................................................................................12

Question 3..................................................................................................................................12

REFERENCES................................................................................................................................1

SECTION A.....................................................................................................................................3

Question 1....................................................................................................................................3

(a) calculation of IRR..................................................................................................................3

(b) calculation of NPV.................................................................................................................5

Question 2....................................................................................................................................6

Question 3....................................................................................................................................7

Question 4....................................................................................................................................7

a....................................................................................................................................................7

Question 4.b.................................................................................................................................7

Question 4.c.................................................................................................................................7

Question 5....................................................................................................................................8

Question 6....................................................................................................................................8

a)..................................................................................................................................................8

b)..................................................................................................................................................9

c)..................................................................................................................................................9

d)..................................................................................................................................................9

Question 7..................................................................................................................................10

Question 8..................................................................................................................................10

SECTION B...................................................................................................................................12

Question 1..................................................................................................................................12

Question 3..................................................................................................................................12

REFERENCES................................................................................................................................1

SECTION A

Question 1

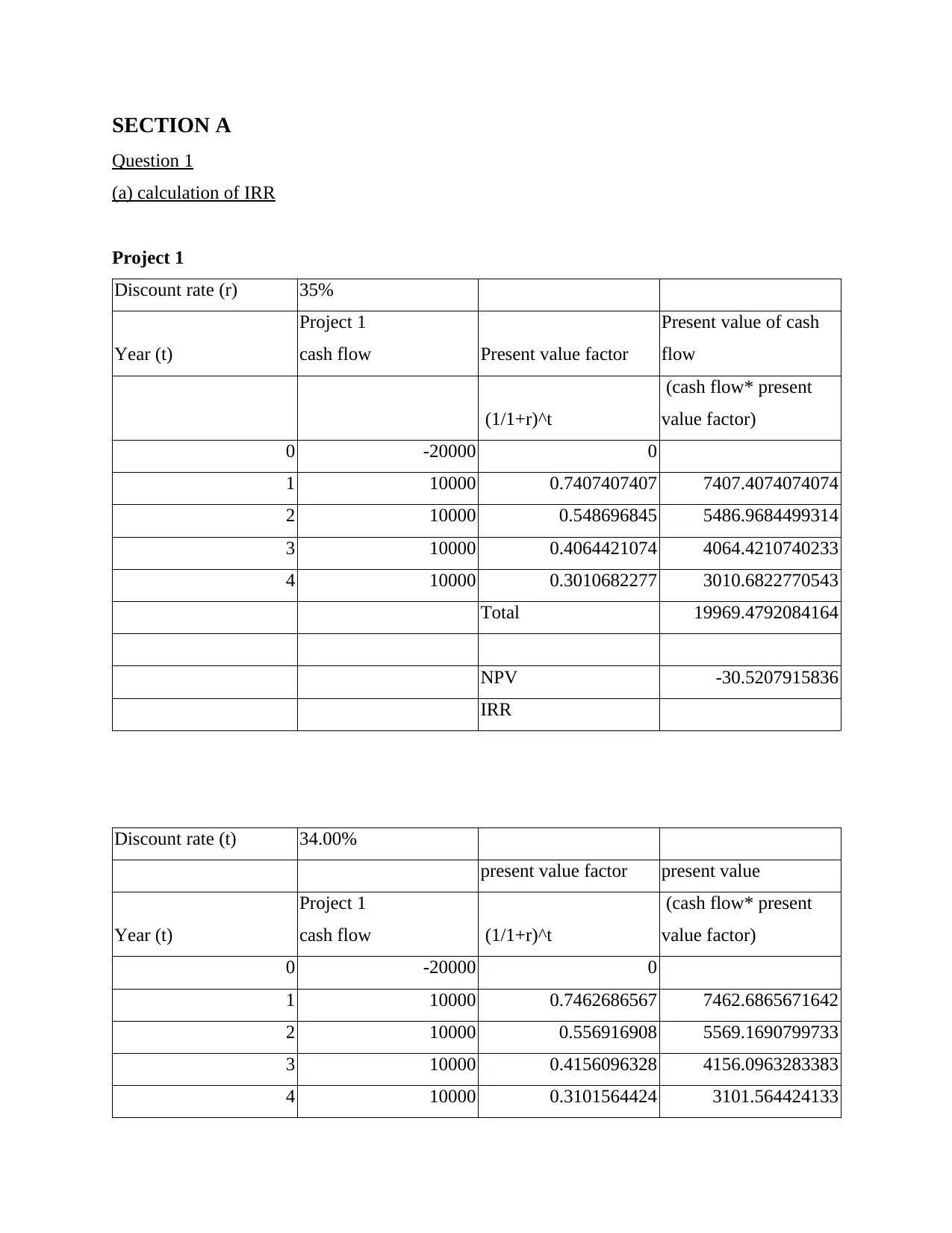

(a) calculation of IRR

Project 1

Discount rate (r) 35%

Year (t)

Project 1

cash flow Present value factor

Present value of cash

flow

(1/1+r)^t

(cash flow* present

value factor)

0 -20000 0

1 10000 0.7407407407 7407.4074074074

2 10000 0.548696845 5486.9684499314

3 10000 0.4064421074 4064.4210740233

4 10000 0.3010682277 3010.6822770543

Total 19969.4792084164

NPV -30.5207915836

IRR

Discount rate (t) 34.00%

present value factor present value

Year (t)

Project 1

cash flow (1/1+r)^t

(cash flow* present

value factor)

0 -20000 0

1 10000 0.7462686567 7462.6865671642

2 10000 0.556916908 5569.1690799733

3 10000 0.4156096328 4156.0963283383

4 10000 0.3101564424 3101.564424133

Question 1

(a) calculation of IRR

Project 1

Discount rate (r) 35%

Year (t)

Project 1

cash flow Present value factor

Present value of cash

flow

(1/1+r)^t

(cash flow* present

value factor)

0 -20000 0

1 10000 0.7407407407 7407.4074074074

2 10000 0.548696845 5486.9684499314

3 10000 0.4064421074 4064.4210740233

4 10000 0.3010682277 3010.6822770543

Total 19969.4792084164

NPV -30.5207915836

IRR

Discount rate (t) 34.00%

present value factor present value

Year (t)

Project 1

cash flow (1/1+r)^t

(cash flow* present

value factor)

0 -20000 0

1 10000 0.7462686567 7462.6865671642

2 10000 0.556916908 5569.1690799733

3 10000 0.4156096328 4156.0963283383

4 10000 0.3101564424 3101.564424133

20289.5163996087

NPV 289.5163996087

The value of NPV is calculated by taking the difference of present value of cash inflow and cash-

outflow. So at the rate of 35% (discount rate), the value of NPV is negative. IRR is existed where

NPV is zero. Which means that IRR is existed between 34% and 35%. Moreover, the rate of IRR

is 34.90%.

project 2

Discount rate (r) 31.00%

Year (t) Cash flow Present value factor Present value

(1/1+r)^t

(cash flow* present

value factor)

0 -20000 0 -0

1 0 0.7633587786 0

2 0 0.5827166249 0

3 0 0.4448218511 0

4 60000 0.3395586649 20373.519896462

20373.519896462

NPV 373.5198

Discount rate 32.00%

year Project 2 present value factor present value

0 -20000 0 -0

1 0 0.7575757576 0

2 0 0.5739210285 0

NPV 289.5163996087

The value of NPV is calculated by taking the difference of present value of cash inflow and cash-

outflow. So at the rate of 35% (discount rate), the value of NPV is negative. IRR is existed where

NPV is zero. Which means that IRR is existed between 34% and 35%. Moreover, the rate of IRR

is 34.90%.

project 2

Discount rate (r) 31.00%

Year (t) Cash flow Present value factor Present value

(1/1+r)^t

(cash flow* present

value factor)

0 -20000 0 -0

1 0 0.7633587786 0

2 0 0.5827166249 0

3 0 0.4448218511 0

4 60000 0.3395586649 20373.519896462

20373.519896462

NPV 373.5198

Discount rate 32.00%

year Project 2 present value factor present value

0 -20000 0 -0

1 0 0.7575757576 0

2 0 0.5739210285 0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

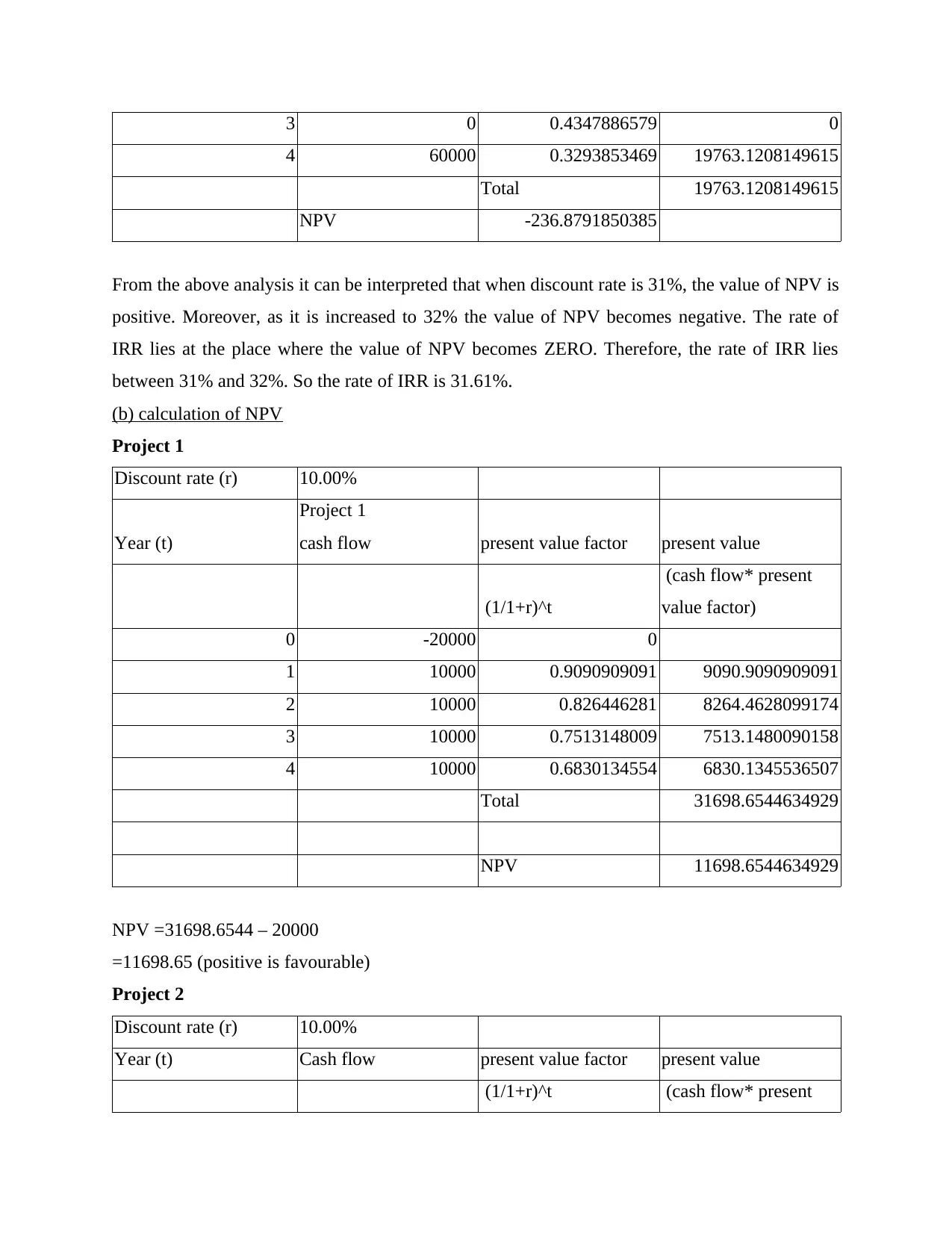

3 0 0.4347886579 0

4 60000 0.3293853469 19763.1208149615

Total 19763.1208149615

NPV -236.8791850385

From the above analysis it can be interpreted that when discount rate is 31%, the value of NPV is

positive. Moreover, as it is increased to 32% the value of NPV becomes negative. The rate of

IRR lies at the place where the value of NPV becomes ZERO. Therefore, the rate of IRR lies

between 31% and 32%. So the rate of IRR is 31.61%.

(b) calculation of NPV

Project 1

Discount rate (r) 10.00%

Year (t)

Project 1

cash flow present value factor present value

(1/1+r)^t

(cash flow* present

value factor)

0 -20000 0

1 10000 0.9090909091 9090.9090909091

2 10000 0.826446281 8264.4628099174

3 10000 0.7513148009 7513.1480090158

4 10000 0.6830134554 6830.1345536507

Total 31698.6544634929

NPV 11698.6544634929

NPV =31698.6544 – 20000

=11698.65 (positive is favourable)

Project 2

Discount rate (r) 10.00%

Year (t) Cash flow present value factor present value

(1/1+r)^t (cash flow* present

4 60000 0.3293853469 19763.1208149615

Total 19763.1208149615

NPV -236.8791850385

From the above analysis it can be interpreted that when discount rate is 31%, the value of NPV is

positive. Moreover, as it is increased to 32% the value of NPV becomes negative. The rate of

IRR lies at the place where the value of NPV becomes ZERO. Therefore, the rate of IRR lies

between 31% and 32%. So the rate of IRR is 31.61%.

(b) calculation of NPV

Project 1

Discount rate (r) 10.00%

Year (t)

Project 1

cash flow present value factor present value

(1/1+r)^t

(cash flow* present

value factor)

0 -20000 0

1 10000 0.9090909091 9090.9090909091

2 10000 0.826446281 8264.4628099174

3 10000 0.7513148009 7513.1480090158

4 10000 0.6830134554 6830.1345536507

Total 31698.6544634929

NPV 11698.6544634929

NPV =31698.6544 – 20000

=11698.65 (positive is favourable)

Project 2

Discount rate (r) 10.00%

Year (t) Cash flow present value factor present value

(1/1+r)^t (cash flow* present

value factor)

0 -20000 0 -0

1 0 0.9090909091 0

2 0 0.826446281 0

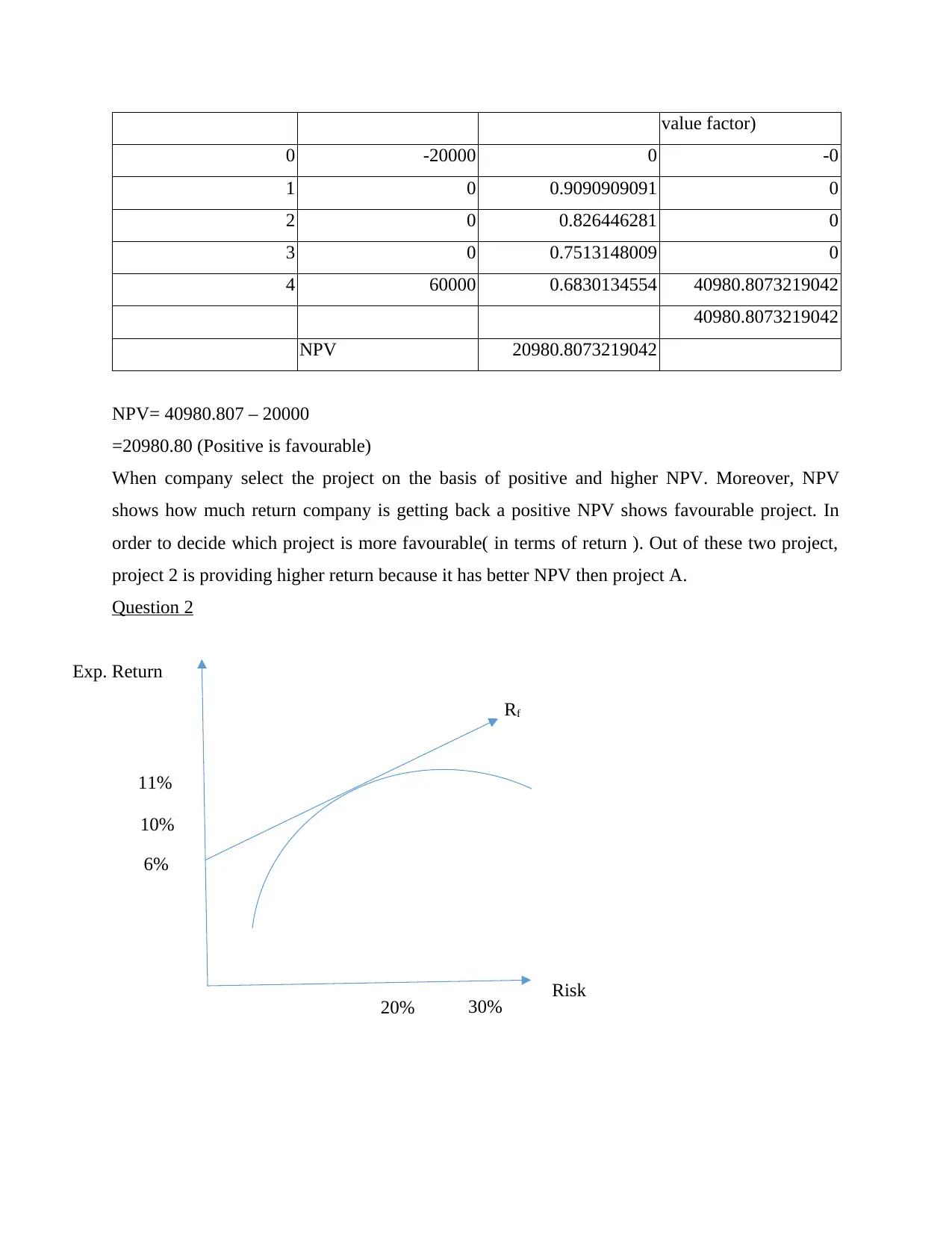

3 0 0.7513148009 0

4 60000 0.6830134554 40980.8073219042

40980.8073219042

NPV 20980.8073219042

NPV= 40980.807 – 20000

=20980.80 (Positive is favourable)

When company select the project on the basis of positive and higher NPV. Moreover, NPV

shows how much return company is getting back a positive NPV shows favourable project. In

order to decide which project is more favourable( in terms of return ). Out of these two project,

project 2 is providing higher return because it has better NPV then project A.

Question 2

6%

Risk

Rf

10%

20%

Exp. Return

30%

11%

0 -20000 0 -0

1 0 0.9090909091 0

2 0 0.826446281 0

3 0 0.7513148009 0

4 60000 0.6830134554 40980.8073219042

40980.8073219042

NPV 20980.8073219042

NPV= 40980.807 – 20000

=20980.80 (Positive is favourable)

When company select the project on the basis of positive and higher NPV. Moreover, NPV

shows how much return company is getting back a positive NPV shows favourable project. In

order to decide which project is more favourable( in terms of return ). Out of these two project,

project 2 is providing higher return because it has better NPV then project A.

Question 2

6%

Risk

Rf

10%

20%

Exp. Return

30%

11%

Question 3

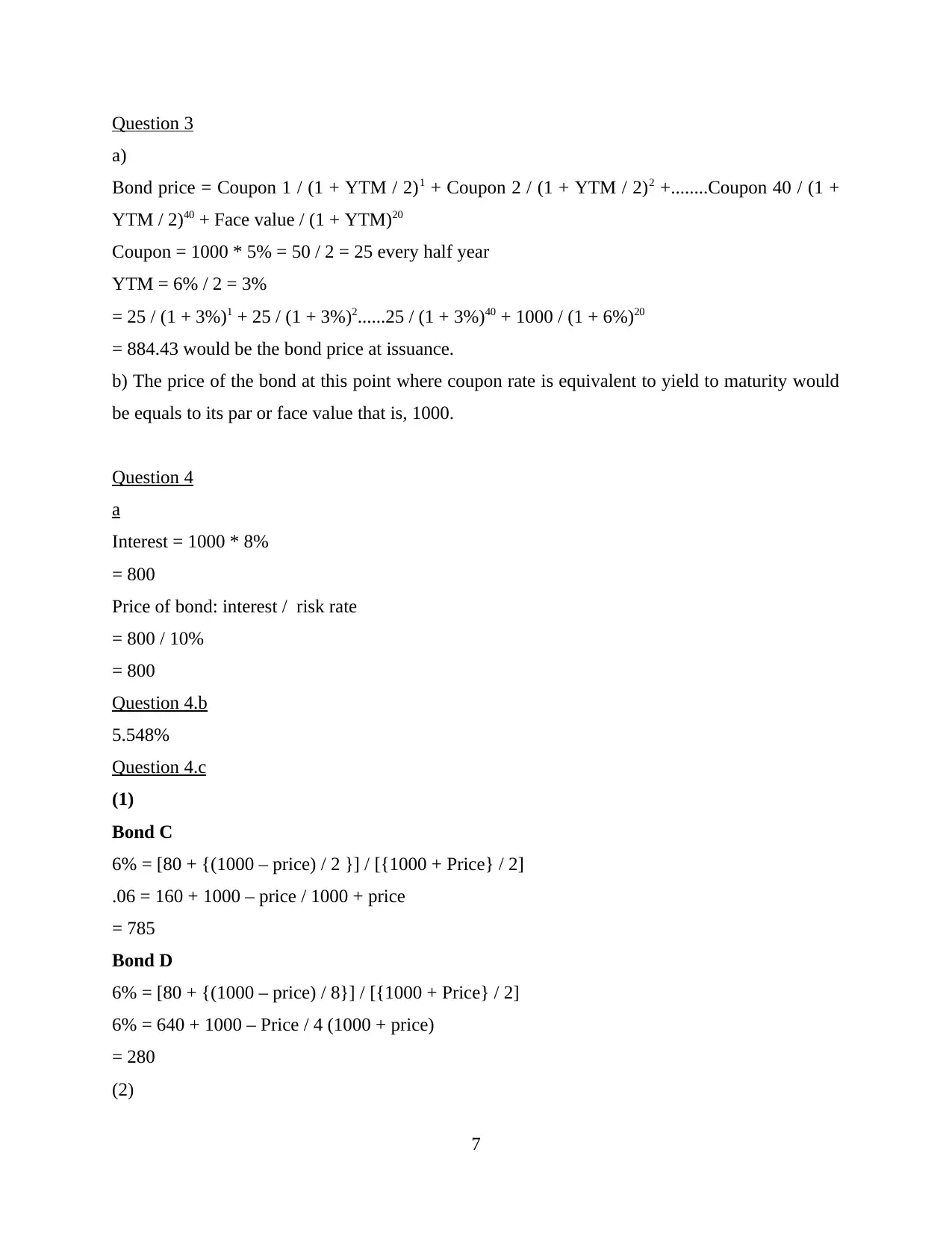

a)

Bond price = Coupon 1 / (1 + YTM / 2)1 + Coupon 2 / (1 + YTM / 2)2 +........Coupon 40 / (1 +

YTM / 2)40 + Face value / (1 + YTM)20

Coupon = 1000 * 5% = 50 / 2 = 25 every half year

YTM = 6% / 2 = 3%

= 25 / (1 + 3%)1 + 25 / (1 + 3%)2......25 / (1 + 3%)40 + 1000 / (1 + 6%)20

= 884.43 would be the bond price at issuance.

b) The price of the bond at this point where coupon rate is equivalent to yield to maturity would

be equals to its par or face value that is, 1000.

Question 4

a

Interest = 1000 * 8%

= 800

Price of bond: interest / risk rate

= 800 / 10%

= 800

Question 4.b

5.548%

Question 4.c

(1)

Bond C

6% = [80 + {(1000 – price) / 2 }] / [{1000 + Price} / 2]

.06 = 160 + 1000 – price / 1000 + price

= 785

Bond D

6% = [80 + {(1000 – price) / 8}] / [{1000 + Price} / 2]

6% = 640 + 1000 – Price / 4 (1000 + price)

= 280

(2)

7

a)

Bond price = Coupon 1 / (1 + YTM / 2)1 + Coupon 2 / (1 + YTM / 2)2 +........Coupon 40 / (1 +

YTM / 2)40 + Face value / (1 + YTM)20

Coupon = 1000 * 5% = 50 / 2 = 25 every half year

YTM = 6% / 2 = 3%

= 25 / (1 + 3%)1 + 25 / (1 + 3%)2......25 / (1 + 3%)40 + 1000 / (1 + 6%)20

= 884.43 would be the bond price at issuance.

b) The price of the bond at this point where coupon rate is equivalent to yield to maturity would

be equals to its par or face value that is, 1000.

Question 4

a

Interest = 1000 * 8%

= 800

Price of bond: interest / risk rate

= 800 / 10%

= 800

Question 4.b

5.548%

Question 4.c

(1)

Bond C

6% = [80 + {(1000 – price) / 2 }] / [{1000 + Price} / 2]

.06 = 160 + 1000 – price / 1000 + price

= 785

Bond D

6% = [80 + {(1000 – price) / 8}] / [{1000 + Price} / 2]

6% = 640 + 1000 – Price / 4 (1000 + price)

= 280

(2)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

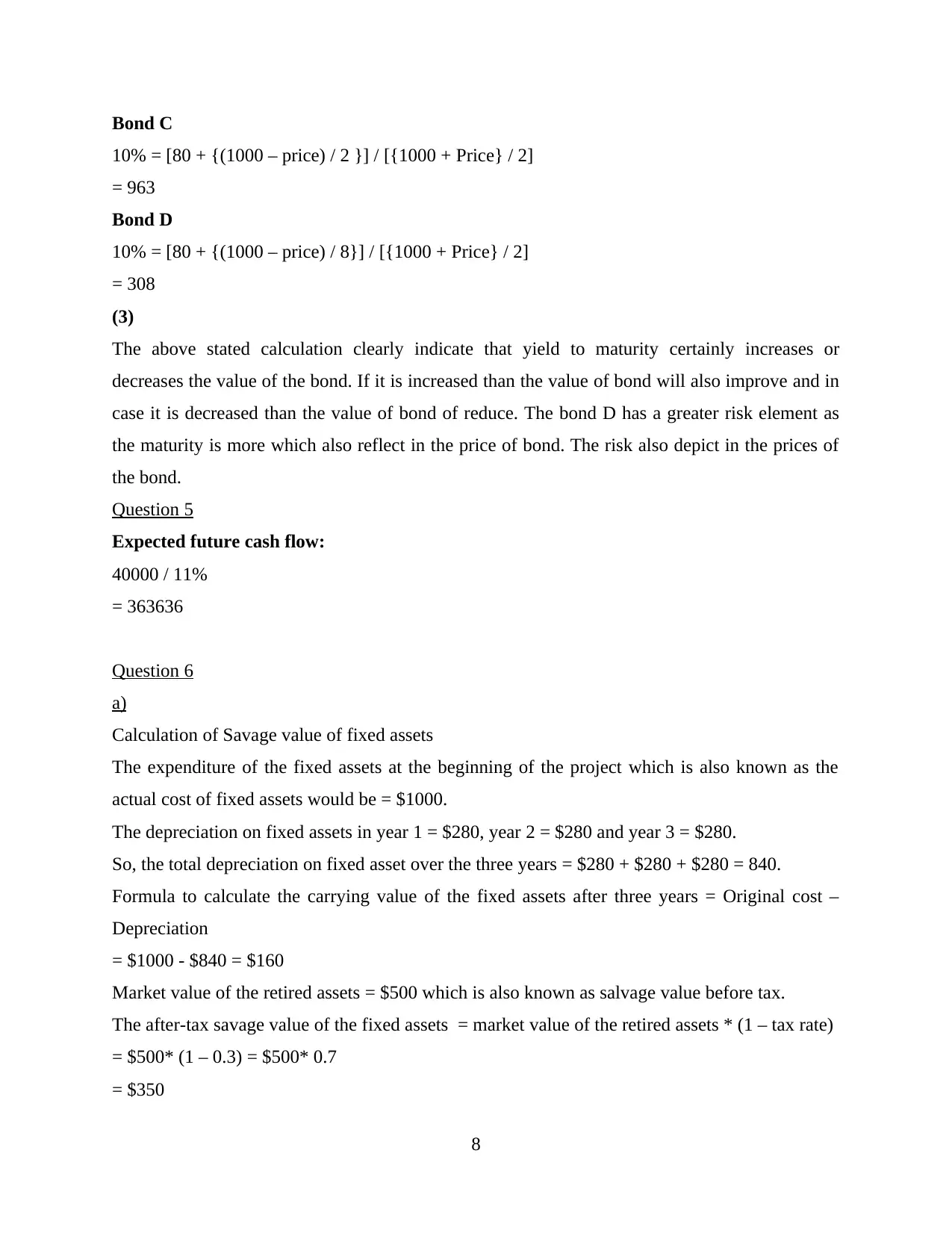

Bond C

10% = [80 + {(1000 – price) / 2 }] / [{1000 + Price} / 2]

= 963

Bond D

10% = [80 + {(1000 – price) / 8}] / [{1000 + Price} / 2]

= 308

(3)

The above stated calculation clearly indicate that yield to maturity certainly increases or

decreases the value of the bond. If it is increased than the value of bond will also improve and in

case it is decreased than the value of bond of reduce. The bond D has a greater risk element as

the maturity is more which also reflect in the price of bond. The risk also depict in the prices of

the bond.

Question 5

Expected future cash flow:

40000 / 11%

= 363636

Question 6

a)

Calculation of Savage value of fixed assets

The expenditure of the fixed assets at the beginning of the project which is also known as the

actual cost of fixed assets would be = $1000.

The depreciation on fixed assets in year 1 = $280, year 2 = $280 and year 3 = $280.

So, the total depreciation on fixed asset over the three years = $280 + $280 + $280 = 840.

Formula to calculate the carrying value of the fixed assets after three years = Original cost –

Depreciation

= $1000 - $840 = $160

Market value of the retired assets = $500 which is also known as salvage value before tax.

The after-tax savage value of the fixed assets = market value of the retired assets * (1 – tax rate)

= $500* (1 – 0.3) = $500* 0.7

= $350

8

10% = [80 + {(1000 – price) / 2 }] / [{1000 + Price} / 2]

= 963

Bond D

10% = [80 + {(1000 – price) / 8}] / [{1000 + Price} / 2]

= 308

(3)

The above stated calculation clearly indicate that yield to maturity certainly increases or

decreases the value of the bond. If it is increased than the value of bond will also improve and in

case it is decreased than the value of bond of reduce. The bond D has a greater risk element as

the maturity is more which also reflect in the price of bond. The risk also depict in the prices of

the bond.

Question 5

Expected future cash flow:

40000 / 11%

= 363636

Question 6

a)

Calculation of Savage value of fixed assets

The expenditure of the fixed assets at the beginning of the project which is also known as the

actual cost of fixed assets would be = $1000.

The depreciation on fixed assets in year 1 = $280, year 2 = $280 and year 3 = $280.

So, the total depreciation on fixed asset over the three years = $280 + $280 + $280 = 840.

Formula to calculate the carrying value of the fixed assets after three years = Original cost –

Depreciation

= $1000 - $840 = $160

Market value of the retired assets = $500 which is also known as salvage value before tax.

The after-tax savage value of the fixed assets = market value of the retired assets * (1 – tax rate)

= $500* (1 – 0.3) = $500* 0.7

= $350

8

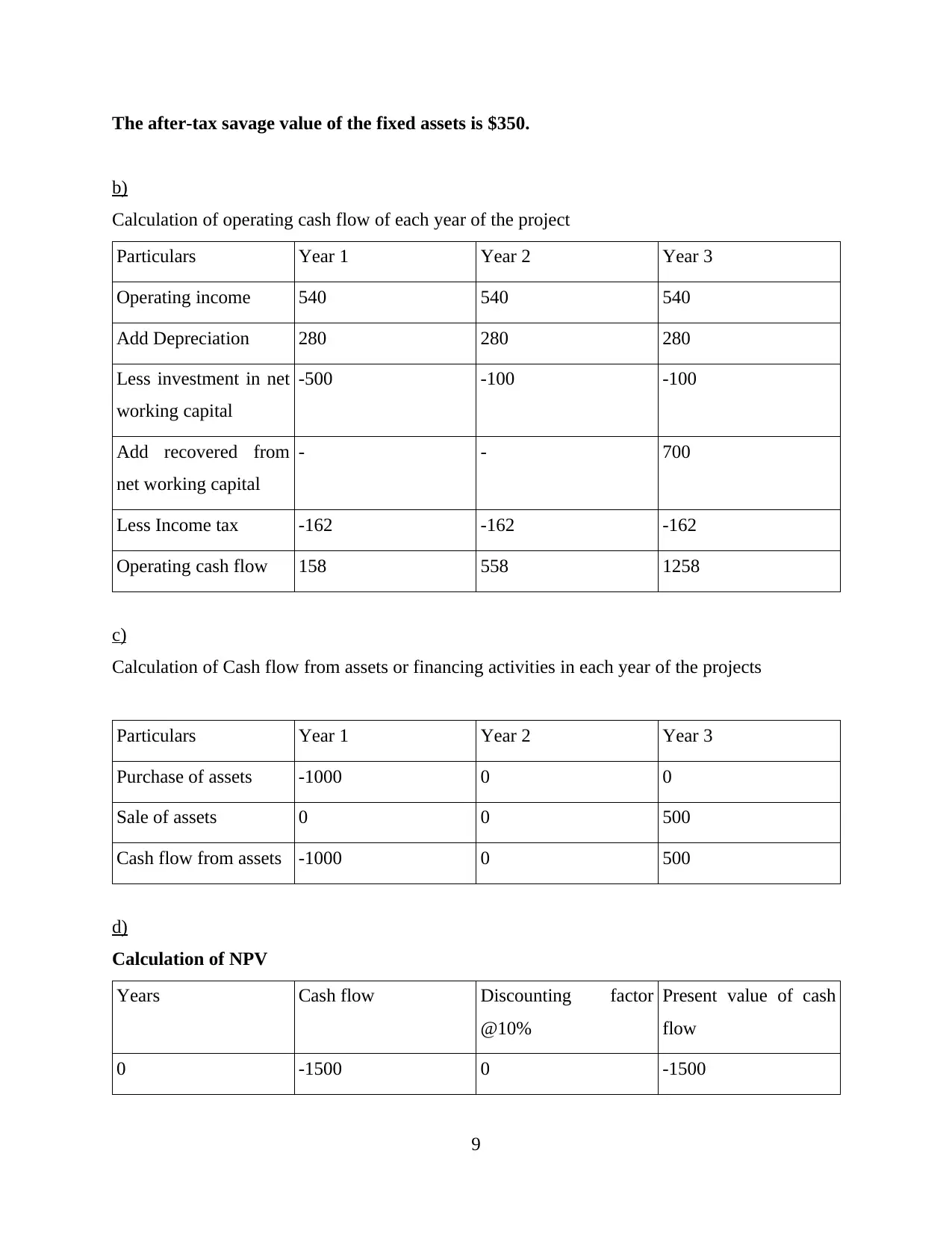

The after-tax savage value of the fixed assets is $350.

b)

Calculation of operating cash flow of each year of the project

Particulars Year 1 Year 2 Year 3

Operating income 540 540 540

Add Depreciation 280 280 280

Less investment in net

working capital

-500 -100 -100

Add recovered from

net working capital

- - 700

Less Income tax -162 -162 -162

Operating cash flow 158 558 1258

c)

Calculation of Cash flow from assets or financing activities in each year of the projects

Particulars Year 1 Year 2 Year 3

Purchase of assets -1000 0 0

Sale of assets 0 0 500

Cash flow from assets -1000 0 500

d)

Calculation of NPV

Years Cash flow Discounting factor

@10%

Present value of cash

flow

0 -1500 0 -1500

9

b)

Calculation of operating cash flow of each year of the project

Particulars Year 1 Year 2 Year 3

Operating income 540 540 540

Add Depreciation 280 280 280

Less investment in net

working capital

-500 -100 -100

Add recovered from

net working capital

- - 700

Less Income tax -162 -162 -162

Operating cash flow 158 558 1258

c)

Calculation of Cash flow from assets or financing activities in each year of the projects

Particulars Year 1 Year 2 Year 3

Purchase of assets -1000 0 0

Sale of assets 0 0 500

Cash flow from assets -1000 0 500

d)

Calculation of NPV

Years Cash flow Discounting factor

@10%

Present value of cash

flow

0 -1500 0 -1500

9

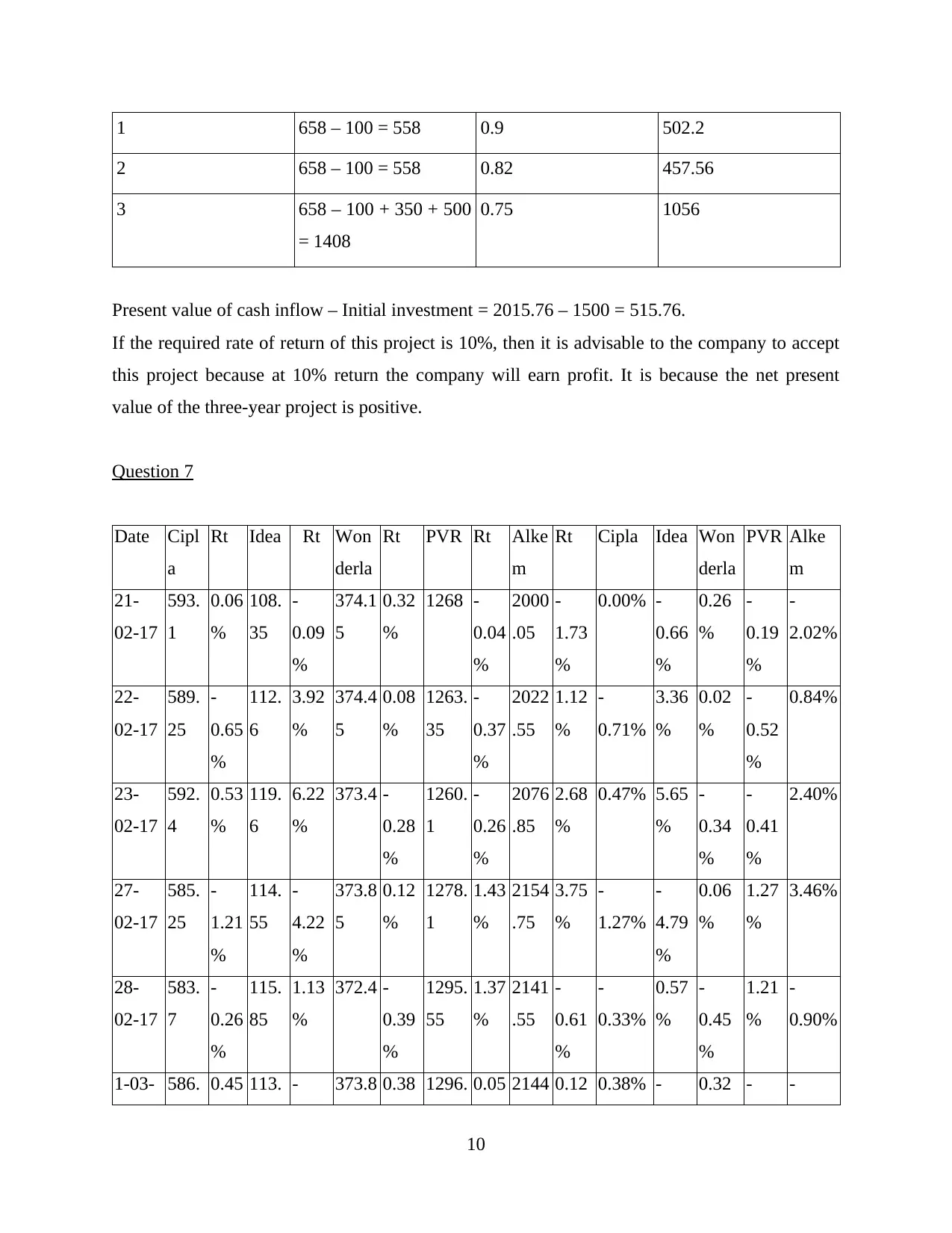

1 658 – 100 = 558 0.9 502.2

2 658 – 100 = 558 0.82 457.56

3 658 – 100 + 350 + 500

= 1408

0.75 1056

Present value of cash inflow – Initial investment = 2015.76 – 1500 = 515.76.

If the required rate of return of this project is 10%, then it is advisable to the company to accept

this project because at 10% return the company will earn profit. It is because the net present

value of the three-year project is positive.

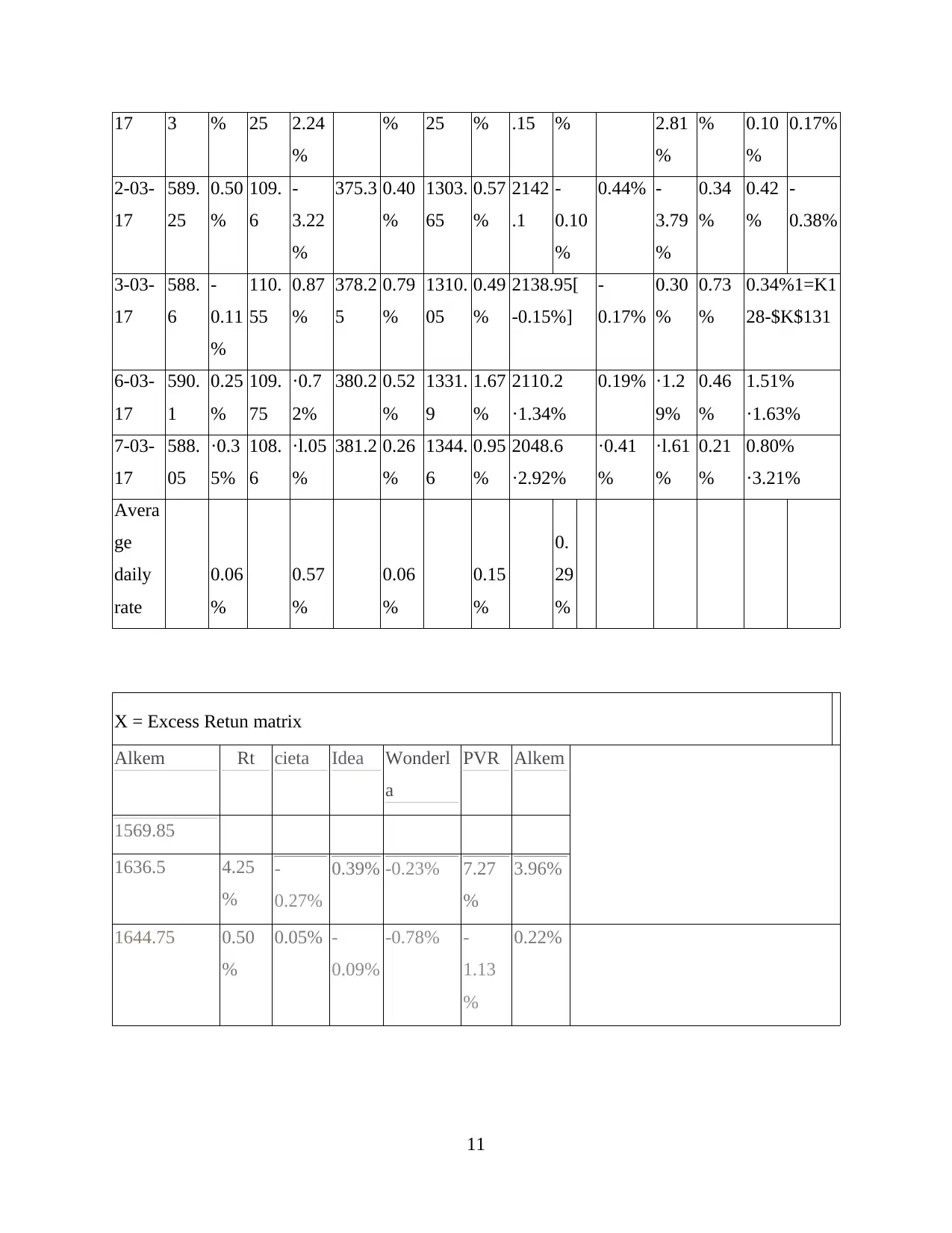

Question 7

Date Cipl

a

Rt Idea Rt Won

derla

Rt PVR Rt Alke

m

Rt Cipla Idea Won

derla

PVR Alke

m

21-

02-17

593.

1

0.06

%

108.

35

-

0.09

%

374.1

5

0.32

%

1268 -

0.04

%

2000

.05

-

1.73

%

0.00% -

0.66

%

0.26

%

-

0.19

%

-

2.02%

22-

02-17

589.

25

-

0.65

%

112.

6

3.92

%

374.4

5

0.08

%

1263.

35

-

0.37

%

2022

.55

1.12

%

-

0.71%

3.36

%

0.02

%

-

0.52

%

0.84%

23-

02-17

592.

4

0.53

%

119.

6

6.22

%

373.4 -

0.28

%

1260.

1

-

0.26

%

2076

.85

2.68

%

0.47% 5.65

%

-

0.34

%

-

0.41

%

2.40%

27-

02-17

585.

25

-

1.21

%

114.

55

-

4.22

%

373.8

5

0.12

%

1278.

1

1.43

%

2154

.75

3.75

%

-

1.27%

-

4.79

%

0.06

%

1.27

%

3.46%

28-

02-17

583.

7

-

0.26

%

115.

85

1.13

%

372.4 -

0.39

%

1295.

55

1.37

%

2141

.55

-

0.61

%

-

0.33%

0.57

%

-

0.45

%

1.21

%

-

0.90%

1-03- 586. 0.45 113. - 373.8 0.38 1296. 0.05 2144 0.12 0.38% - 0.32 - -

10

2 658 – 100 = 558 0.82 457.56

3 658 – 100 + 350 + 500

= 1408

0.75 1056

Present value of cash inflow – Initial investment = 2015.76 – 1500 = 515.76.

If the required rate of return of this project is 10%, then it is advisable to the company to accept

this project because at 10% return the company will earn profit. It is because the net present

value of the three-year project is positive.

Question 7

Date Cipl

a

Rt Idea Rt Won

derla

Rt PVR Rt Alke

m

Rt Cipla Idea Won

derla

PVR Alke

m

21-

02-17

593.

1

0.06

%

108.

35

-

0.09

%

374.1

5

0.32

%

1268 -

0.04

%

2000

.05

-

1.73

%

0.00% -

0.66

%

0.26

%

-

0.19

%

-

2.02%

22-

02-17

589.

25

-

0.65

%

112.

6

3.92

%

374.4

5

0.08

%

1263.

35

-

0.37

%

2022

.55

1.12

%

-

0.71%

3.36

%

0.02

%

-

0.52

%

0.84%

23-

02-17

592.

4

0.53

%

119.

6

6.22

%

373.4 -

0.28

%

1260.

1

-

0.26

%

2076

.85

2.68

%

0.47% 5.65

%

-

0.34

%

-

0.41

%

2.40%

27-

02-17

585.

25

-

1.21

%

114.

55

-

4.22

%

373.8

5

0.12

%

1278.

1

1.43

%

2154

.75

3.75

%

-

1.27%

-

4.79

%

0.06

%

1.27

%

3.46%

28-

02-17

583.

7

-

0.26

%

115.

85

1.13

%

372.4 -

0.39

%

1295.

55

1.37

%

2141

.55

-

0.61

%

-

0.33%

0.57

%

-

0.45

%

1.21

%

-

0.90%

1-03- 586. 0.45 113. - 373.8 0.38 1296. 0.05 2144 0.12 0.38% - 0.32 - -

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17 3 % 25 2.24

%

% 25 % .15 % 2.81

%

% 0.10

%

0.17%

2-03-

17

589.

25

0.50

%

109.

6

-

3.22

%

375.3 0.40

%

1303.

65

0.57

%

2142

.1

-

0.10

%

0.44% -

3.79

%

0.34

%

0.42

%

-

0.38%

3-03-

17

588.

6

-

0.11

%

110.

55

0.87

%

378.2

5

0.79

%

1310.

05

0.49

%

2138.95[

-0.15%]

-

0.17%

0.30

%

0.73

%

0.34%1=K1

28-$K$131

6-03-

17

590.

1

0.25

%

109.

75

·0.7

2%

380.2 0.52

%

1331.

9

1.67

%

2110.2

·1.34%

0.19% ·1.2

9%

0.46

%

1.51%

·1.63%

7-03-

17

588.

05

·0.3

5%

108.

6

·l.05

%

381.2 0.26

%

1344.

6

0.95

%

2048.6

·2.92%

·0.41

%

·l.61

%

0.21

%

0.80%

·3.21%

Avera

ge

daily

rate

0.06

%

0.57

%

0.06

%

0.15

%

0.

29

%

X = Excess Retun matrix

Alkem Rt cieta Idea Wonderl

a

PVR Alkem

1569.85

1636.5 4.25

%

-

0.27%

0.39% -0.23% 7.27

%

3.96%

1644.75 0.50

%

0.05% -

0.09%

-0.78% -

1.13

%

0.22%

11

%

% 25 % .15 % 2.81

%

% 0.10

%

0.17%

2-03-

17

589.

25

0.50

%

109.

6

-

3.22

%

375.3 0.40

%

1303.

65

0.57

%

2142

.1

-

0.10

%

0.44% -

3.79

%

0.34

%

0.42

%

-

0.38%

3-03-

17

588.

6

-

0.11

%

110.

55

0.87

%

378.2

5

0.79

%

1310.

05

0.49

%

2138.95[

-0.15%]

-

0.17%

0.30

%

0.73

%

0.34%1=K1

28-$K$131

6-03-

17

590.

1

0.25

%

109.

75

·0.7

2%

380.2 0.52

%

1331.

9

1.67

%

2110.2

·1.34%

0.19% ·1.2

9%

0.46

%

1.51%

·1.63%

7-03-

17

588.

05

·0.3

5%

108.

6

·l.05

%

381.2 0.26

%

1344.

6

0.95

%

2048.6

·2.92%

·0.41

%

·l.61

%

0.21

%

0.80%

·3.21%

Avera

ge

daily

rate

0.06

%

0.57

%

0.06

%

0.15

%

0.

29

%

X = Excess Retun matrix

Alkem Rt cieta Idea Wonderl

a

PVR Alkem

1569.85

1636.5 4.25

%

-

0.27%

0.39% -0.23% 7.27

%

3.96%

1644.75 0.50

%

0.05% -

0.09%

-0.78% -

1.13

%

0.22%

11

1616.9 -

1.69

%

0.31% -

1.92%

-0.30% -

1.69

%

-

1.98%

I Ciola Idea Wonderla PVR Alkem

TRANSPOSE{LS:P130),LS:P130)

Idea Wonderla PVR

Alkem

1635.9 1.18% 2.42% 0.39% -0.06% -0.46% =MMULT{TR

1602.. 85 ·2.02% ·2.52% ·1.63% ·0.32% ·1.62% ·2.31%

1616.35 0.84% ·1.85% ·1.52% ·1.06% ·3.47" 0.55%

1624.3 0.49% 1.24% 0.58% ·0.12% ·0.63% 0.20%

1622.35 ·0.12% 1.31% 0.33% ·0.21% ·1.43% ·0.41%

X transpose multipied by X

Cipla Cipla

0.02788

Idea

0.00679

Wonderla

0.00425

PVR

0.00515

Alkem

0.00804

Idea 0.00679 0.14084 0.00497 0.00289 0.00475

Wonderla 0.00425 0.00497 0.03055 0.00500 0.00351

PVR 0.00515 0.00289 0.00500 0.05109 0.00338

Alkem 0.00804 0.00475 0.00351 0.00338 0.04310

transpose multipied by X

Cipla Cipla

0.02788

Idea

0.00679

Wonderla

0.00425

PVR

0.00515

Alkem

0.00804

Idea 0.00679 0.14084 0.00497 0.00289 0.00475

12

1.69

%

0.31% -

1.92%

-0.30% -

1.69

%

-

1.98%

I Ciola Idea Wonderla PVR Alkem

TRANSPOSE{LS:P130),LS:P130)

Idea Wonderla PVR

Alkem

1635.9 1.18% 2.42% 0.39% -0.06% -0.46% =MMULT{TR

1602.. 85 ·2.02% ·2.52% ·1.63% ·0.32% ·1.62% ·2.31%

1616.35 0.84% ·1.85% ·1.52% ·1.06% ·3.47" 0.55%

1624.3 0.49% 1.24% 0.58% ·0.12% ·0.63% 0.20%

1622.35 ·0.12% 1.31% 0.33% ·0.21% ·1.43% ·0.41%

X transpose multipied by X

Cipla Cipla

0.02788

Idea

0.00679

Wonderla

0.00425

PVR

0.00515

Alkem

0.00804

Idea 0.00679 0.14084 0.00497 0.00289 0.00475

Wonderla 0.00425 0.00497 0.03055 0.00500 0.00351

PVR 0.00515 0.00289 0.00500 0.05109 0.00338

Alkem 0.00804 0.00475 0.00351 0.00338 0.04310

transpose multipied by X

Cipla Cipla

0.02788

Idea

0.00679

Wonderla

0.00425

PVR

0.00515

Alkem

0.00804

Idea 0.00679 0.14084 0.00497 0.00289 0.00475

12

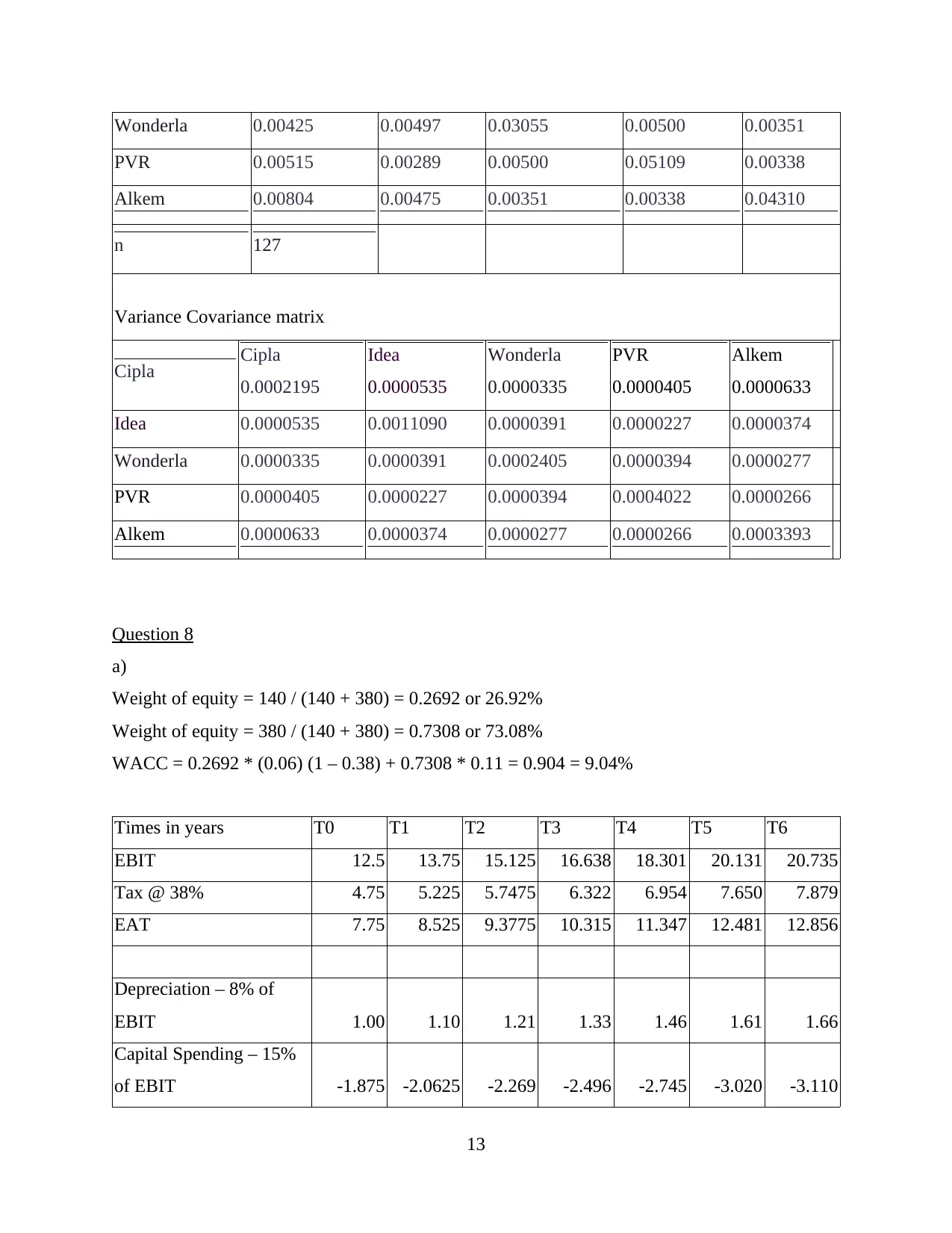

Wonderla 0.00425 0.00497 0.03055 0.00500 0.00351

PVR 0.00515 0.00289 0.00500 0.05109 0.00338

Alkem 0.00804 0.00475 0.00351 0.00338 0.04310

n 127

Variance Covariance matrix

Cipla Cipla

0.0002195

Idea

0.0000535

Wonderla

0.0000335

PVR

0.0000405

Alkem

0.0000633

Idea 0.0000535 0.0011090 0.0000391 0.0000227 0.0000374

Wonderla 0.0000335 0.0000391 0.0002405 0.0000394 0.0000277

PVR 0.0000405 0.0000227 0.0000394 0.0004022 0.0000266

Alkem 0.0000633 0.0000374 0.0000277 0.0000266 0.0003393

Question 8

a)

Weight of equity = 140 / (140 + 380) = 0.2692 or 26.92%

Weight of equity = 380 / (140 + 380) = 0.7308 or 73.08%

WACC = 0.2692 * (0.06) (1 – 0.38) + 0.7308 * 0.11 = 0.904 = 9.04%

Times in years T0 T1 T2 T3 T4 T5 T6

EBIT 12.5 13.75 15.125 16.638 18.301 20.131 20.735

Tax @ 38% 4.75 5.225 5.7475 6.322 6.954 7.650 7.879

EAT 7.75 8.525 9.3775 10.315 11.347 12.481 12.856

Depreciation – 8% of

EBIT 1.00 1.10 1.21 1.33 1.46 1.61 1.66

Capital Spending – 15%

of EBIT -1.875 -2.0625 -2.269 -2.496 -2.745 -3.020 -3.110

13

PVR 0.00515 0.00289 0.00500 0.05109 0.00338

Alkem 0.00804 0.00475 0.00351 0.00338 0.04310

n 127

Variance Covariance matrix

Cipla Cipla

0.0002195

Idea

0.0000535

Wonderla

0.0000335

PVR

0.0000405

Alkem

0.0000633

Idea 0.0000535 0.0011090 0.0000391 0.0000227 0.0000374

Wonderla 0.0000335 0.0000391 0.0002405 0.0000394 0.0000277

PVR 0.0000405 0.0000227 0.0000394 0.0004022 0.0000266

Alkem 0.0000633 0.0000374 0.0000277 0.0000266 0.0003393

Question 8

a)

Weight of equity = 140 / (140 + 380) = 0.2692 or 26.92%

Weight of equity = 380 / (140 + 380) = 0.7308 or 73.08%

WACC = 0.2692 * (0.06) (1 – 0.38) + 0.7308 * 0.11 = 0.904 = 9.04%

Times in years T0 T1 T2 T3 T4 T5 T6

EBIT 12.5 13.75 15.125 16.638 18.301 20.131 20.735

Tax @ 38% 4.75 5.225 5.7475 6.322 6.954 7.650 7.879

EAT 7.75 8.525 9.3775 10.315 11.347 12.481 12.856

Depreciation – 8% of

EBIT 1.00 1.10 1.21 1.33 1.46 1.61 1.66

Capital Spending – 15%

of EBIT -1.875 -2.0625 -2.269 -2.496 -2.745 -3.020 -3.110

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

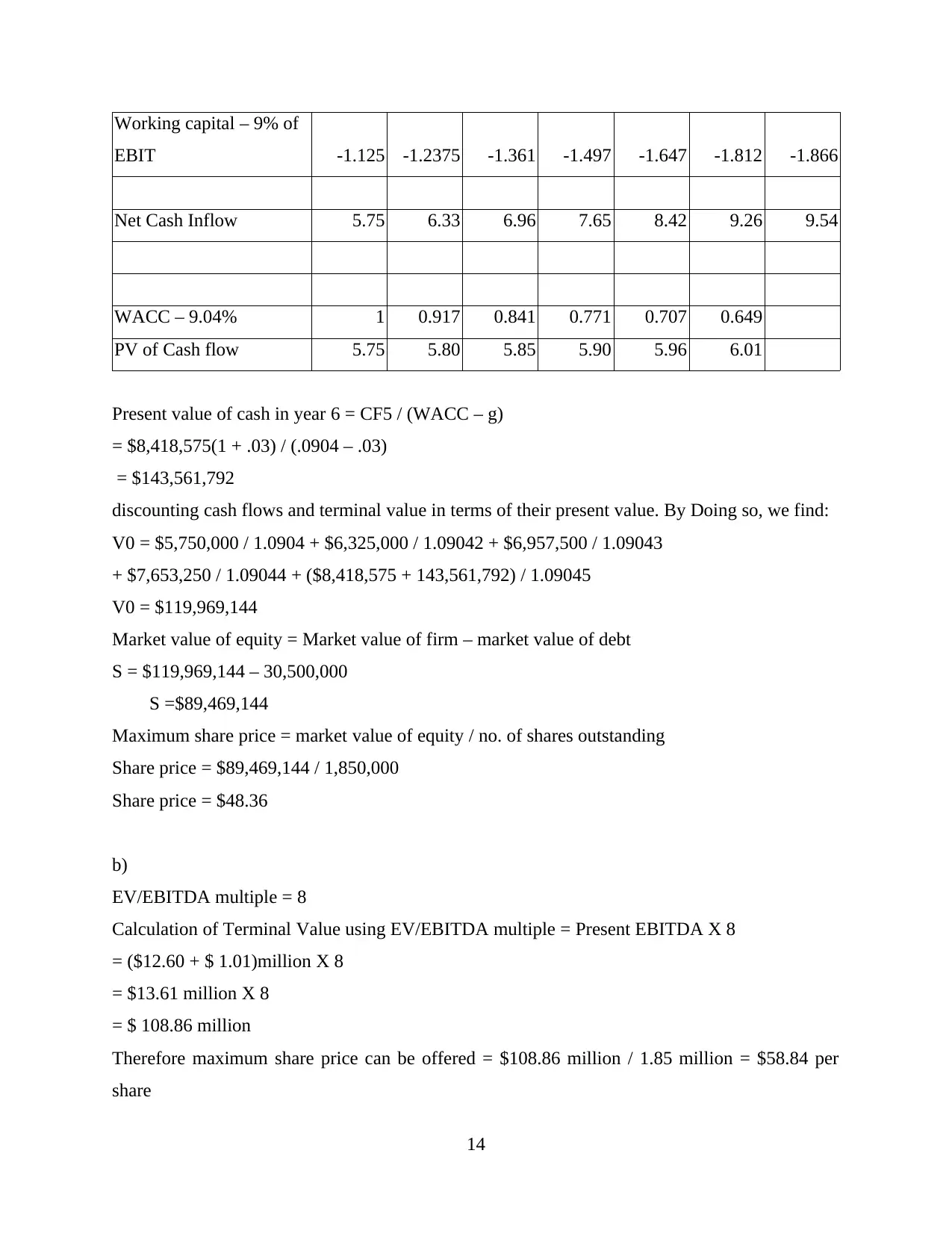

Working capital – 9% of

EBIT -1.125 -1.2375 -1.361 -1.497 -1.647 -1.812 -1.866

Net Cash Inflow 5.75 6.33 6.96 7.65 8.42 9.26 9.54

WACC – 9.04% 1 0.917 0.841 0.771 0.707 0.649

PV of Cash flow 5.75 5.80 5.85 5.90 5.96 6.01

Present value of cash in year 6 = CF5 / (WACC – g)

= $8,418,575(1 + .03) / (.0904 – .03)

= $143,561,792

discounting cash flows and terminal value in terms of their present value. By Doing so, we find:

V0 = $5,750,000 / 1.0904 + $6,325,000 / 1.09042 + $6,957,500 / 1.09043

+ $7,653,250 / 1.09044 + ($8,418,575 + 143,561,792) / 1.09045

V0 = $119,969,144

Market value of equity = Market value of firm – market value of debt

S = $119,969,144 – 30,500,000

S =$89,469,144

Maximum share price = market value of equity / no. of shares outstanding

Share price = $89,469,144 / 1,850,000

Share price = $48.36

b)

EV/EBITDA multiple = 8

Calculation of Terminal Value using EV/EBITDA multiple = Present EBITDA X 8

= ($12.60 + $ 1.01)million X 8

= $13.61 million X 8

= $ 108.86 million

Therefore maximum share price can be offered = $108.86 million / 1.85 million = $58.84 per

share

14

EBIT -1.125 -1.2375 -1.361 -1.497 -1.647 -1.812 -1.866

Net Cash Inflow 5.75 6.33 6.96 7.65 8.42 9.26 9.54

WACC – 9.04% 1 0.917 0.841 0.771 0.707 0.649

PV of Cash flow 5.75 5.80 5.85 5.90 5.96 6.01

Present value of cash in year 6 = CF5 / (WACC – g)

= $8,418,575(1 + .03) / (.0904 – .03)

= $143,561,792

discounting cash flows and terminal value in terms of their present value. By Doing so, we find:

V0 = $5,750,000 / 1.0904 + $6,325,000 / 1.09042 + $6,957,500 / 1.09043

+ $7,653,250 / 1.09044 + ($8,418,575 + 143,561,792) / 1.09045

V0 = $119,969,144

Market value of equity = Market value of firm – market value of debt

S = $119,969,144 – 30,500,000

S =$89,469,144

Maximum share price = market value of equity / no. of shares outstanding

Share price = $89,469,144 / 1,850,000

Share price = $48.36

b)

EV/EBITDA multiple = 8

Calculation of Terminal Value using EV/EBITDA multiple = Present EBITDA X 8

= ($12.60 + $ 1.01)million X 8

= $13.61 million X 8

= $ 108.86 million

Therefore maximum share price can be offered = $108.86 million / 1.85 million = $58.84 per

share

14

SECTION B

Question 1

The internal rate of return technique do not provide the clearly picture of future. It ignore

the overall size of project. It ignores future cost with calculation . Mutually exclusive projects

got ignored while calculating the internal rate of return. Different term of project is not

considered while evaluating the internal rate of return technique. In case the later cash inflow are

not sufficient than the IRR is not possible to calculate in the project. Also the wealth of the

project is not possible to measure with the support of internal rate of return method or technique.

It does not account for investment. It suggests to keep match up with multiple cash (Kim, Kim

and Yook, 2021). The disadvantage of the Internal rate of return technique can be solved with the

use of other method or techniques like net present value and the payback period and other

relevant techniques. To overcome the challenges of IRR time horizon can cut down to deal with

the time related issues. Also the management can use this technique only for the projects contain

only a shirt time duration.

Question 3

Beta is a measure of a stock volatility in relation to the overall market. The Beta is one of the

most popular indicator with the help of which investors can measure the risk of the securities.

Beta is a concept that measures the expected move in a stock relative to movements in the

overall market. A beta greater than 1.0 suggest that the particular stock and security is more

volatile than the broader market. While in the case, when Beta is less than 1.0 indicate a stock

with lower volatile. Beta is basically and probably a better indicator of the short-term risk not for

the long term risk (Xiang and et.al., 2019). In order to calculate and estimate the beta of the

securities, the two factors is need to be used. The two factors likely to determine its value is the

risk free return rate and the other one is stocks rate of return.

Beta = Covariance/ variance.

Covariance = measure of a stocks return relative to that of the market

Variance = measure of how the market moves relative to its mean

15

Question 1

The internal rate of return technique do not provide the clearly picture of future. It ignore

the overall size of project. It ignores future cost with calculation . Mutually exclusive projects

got ignored while calculating the internal rate of return. Different term of project is not

considered while evaluating the internal rate of return technique. In case the later cash inflow are

not sufficient than the IRR is not possible to calculate in the project. Also the wealth of the

project is not possible to measure with the support of internal rate of return method or technique.

It does not account for investment. It suggests to keep match up with multiple cash (Kim, Kim

and Yook, 2021). The disadvantage of the Internal rate of return technique can be solved with the

use of other method or techniques like net present value and the payback period and other

relevant techniques. To overcome the challenges of IRR time horizon can cut down to deal with

the time related issues. Also the management can use this technique only for the projects contain

only a shirt time duration.

Question 3

Beta is a measure of a stock volatility in relation to the overall market. The Beta is one of the

most popular indicator with the help of which investors can measure the risk of the securities.

Beta is a concept that measures the expected move in a stock relative to movements in the

overall market. A beta greater than 1.0 suggest that the particular stock and security is more

volatile than the broader market. While in the case, when Beta is less than 1.0 indicate a stock

with lower volatile. Beta is basically and probably a better indicator of the short-term risk not for

the long term risk (Xiang and et.al., 2019). In order to calculate and estimate the beta of the

securities, the two factors is need to be used. The two factors likely to determine its value is the

risk free return rate and the other one is stocks rate of return.

Beta = Covariance/ variance.

Covariance = measure of a stocks return relative to that of the market

Variance = measure of how the market moves relative to its mean

15

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and journals

Kim, K., Kim, J. and Yook, D., 2021. Analysis of Features Affecting Contracted Rate of Return

of Korean PPP Projects. Sustainability. 13(6). p.3311.

Xiang, J. and et.al., 2019. Hydroxycinnamic acid amide (HCAA) derivatives, flavonoid C-

glycosides, phenolic acids and antioxidant properties of foxtail millet. Food

chemistry. 295. pp.214-223.

1

Books and journals

Kim, K., Kim, J. and Yook, D., 2021. Analysis of Features Affecting Contracted Rate of Return

of Korean PPP Projects. Sustainability. 13(6). p.3311.

Xiang, J. and et.al., 2019. Hydroxycinnamic acid amide (HCAA) derivatives, flavonoid C-

glycosides, phenolic acids and antioxidant properties of foxtail millet. Food

chemistry. 295. pp.214-223.

1

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.