Principles of Financial Accounting: A Comprehensive Guide

VerifiedAdded on 2024/06/05

|28

|4522

|312

AI Summary

This comprehensive guide delves into the fundamental principles of financial accounting, covering key concepts, regulations, and practical applications. Explore the definition of financial accounting, its regulations, accounting rules and principles, conventions like consistency and material disclosure, and real-world examples through client case studies. Gain a thorough understanding of financial accounting practices and their importance in business decision-making.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Principles of Financial Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction.................................................................................................................................................3

LO1.............................................................................................................................................................4

Define financial accounting.....................................................................................................................4

LO2.............................................................................................................................................................5

There are some regulations of the financial accounting explain it...........................................................5

LO3.............................................................................................................................................................7

Describes the accounting rules and the principles....................................................................................7

LO4.............................................................................................................................................................9

Explain the conventions and concepts relating to consistency and material disclosure...........................9

Client 1......................................................................................................................................................10

Client 2......................................................................................................................................................18

Client 3......................................................................................................................................................19

Client 4......................................................................................................................................................21

Client 5......................................................................................................................................................23

Client 6......................................................................................................................................................24

Conclusion.................................................................................................................................................26

Bibliography...............................................................................................................................................27

2

Introduction.................................................................................................................................................3

LO1.............................................................................................................................................................4

Define financial accounting.....................................................................................................................4

LO2.............................................................................................................................................................5

There are some regulations of the financial accounting explain it...........................................................5

LO3.............................................................................................................................................................7

Describes the accounting rules and the principles....................................................................................7

LO4.............................................................................................................................................................9

Explain the conventions and concepts relating to consistency and material disclosure...........................9

Client 1......................................................................................................................................................10

Client 2......................................................................................................................................................18

Client 3......................................................................................................................................................19

Client 4......................................................................................................................................................21

Client 5......................................................................................................................................................23

Client 6......................................................................................................................................................24

Conclusion.................................................................................................................................................26

Bibliography...............................................................................................................................................27

2

Introduction

The main aim of the report is to provide the explanation about the financial accounting with that

the various regulations which are used for the financial accounting are also highlighted. The

journal entries are performed with the reporting of those transactions in their respective accounts.

The profit and loss and the financial statements are prepared so that the financial position of the

organization can be examined. These transactions will provide the overall understanding of the

financial accounts in the report.

3

The main aim of the report is to provide the explanation about the financial accounting with that

the various regulations which are used for the financial accounting are also highlighted. The

journal entries are performed with the reporting of those transactions in their respective accounts.

The profit and loss and the financial statements are prepared so that the financial position of the

organization can be examined. These transactions will provide the overall understanding of the

financial accounts in the report.

3

LO1

Define financial accounting.

Financial accounting is doing everything in the financial prospects of the company; it is a

process of preparing the financial statements of the company which includes the balance sheet,

profit and loss account and other final accounts (Kwok, 2017). This system of accounting is

different from the management accounting which includes the preparation of the financial reports

to help the insider managers.

A process of preparing the financial statements of the company, which help the insiders and

outsiders of the company like the stakeholders, clients, employees, investors and company in

large (Kwok, 2017). It used to prepare the balance sheet, profit and loss account and other

financial reports.

The accounting standards which govern this accounting is the GAAP and IFRS, the purpose of

this accounting is providing the outside people an understanding towards the financial reporting

of the company which is not available to them by management accounting (Narayanaswamy,

2017). The financial reporting consists of cash flow statements, profit and loss statements,

balance sheet other statements of retained earnings.

Thus, financial reporting is successful in providing the outsiders people the study of inner facts

or statements of finance that are useful in knowing the company final position. They also help in

maintain systematic records, ascertaining the true financial position, ascertaining the equity and

solvency ratios (Adkins, 2018).

4

Define financial accounting.

Financial accounting is doing everything in the financial prospects of the company; it is a

process of preparing the financial statements of the company which includes the balance sheet,

profit and loss account and other final accounts (Kwok, 2017). This system of accounting is

different from the management accounting which includes the preparation of the financial reports

to help the insider managers.

A process of preparing the financial statements of the company, which help the insiders and

outsiders of the company like the stakeholders, clients, employees, investors and company in

large (Kwok, 2017). It used to prepare the balance sheet, profit and loss account and other

financial reports.

The accounting standards which govern this accounting is the GAAP and IFRS, the purpose of

this accounting is providing the outside people an understanding towards the financial reporting

of the company which is not available to them by management accounting (Narayanaswamy,

2017). The financial reporting consists of cash flow statements, profit and loss statements,

balance sheet other statements of retained earnings.

Thus, financial reporting is successful in providing the outsiders people the study of inner facts

or statements of finance that are useful in knowing the company final position. They also help in

maintain systematic records, ascertaining the true financial position, ascertaining the equity and

solvency ratios (Adkins, 2018).

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

LO2

There are some regulations of the financial accounting explain it.

The regulations are the bind set of rules that are formed by the govern authority recognized by

the board of finance (Kwok, 2017). The regulations in the context of the financial accounting are

developed rules and principles by the independent body with which all the financial statements

are prepared in the framework of these regulations (Epstein, 2018).

Image: Financial Accounting

Source: Ng Careers, 2018

The financial statements are prepared within the framework of GAAP a regulatory authority that

regulates the rules and regulations governing the financial statements (Kwok, 2017).

The Accounting standards board (ASB): this board is made to provide the principles and rules

to guide the financial standards; it has the power to issue its own accounting standards, it tries to

bring the uniformity and accuracy in the financial accounting (Narayanaswamy, 2017). It

consists of ten members of the board, the members of board are appointed by the nomination

committee which consists of the chairman and some directors of the (FRS) council. It is a

autonomous body in issuing the accounting standards (Kwok, 2017).

5

There are some regulations of the financial accounting explain it.

The regulations are the bind set of rules that are formed by the govern authority recognized by

the board of finance (Kwok, 2017). The regulations in the context of the financial accounting are

developed rules and principles by the independent body with which all the financial statements

are prepared in the framework of these regulations (Epstein, 2018).

Image: Financial Accounting

Source: Ng Careers, 2018

The financial statements are prepared within the framework of GAAP a regulatory authority that

regulates the rules and regulations governing the financial statements (Kwok, 2017).

The Accounting standards board (ASB): this board is made to provide the principles and rules

to guide the financial standards; it has the power to issue its own accounting standards, it tries to

bring the uniformity and accuracy in the financial accounting (Narayanaswamy, 2017). It

consists of ten members of the board, the members of board are appointed by the nomination

committee which consists of the chairman and some directors of the (FRS) council. It is a

autonomous body in issuing the accounting standards (Kwok, 2017).

5

IASB (The international accounting standards board) it is formed in 2001 April an

autonomous body in London. It is sole in providing the UK based standards on the accounting it

consist of the IASC which also gives the international accounting standards.

Statement of principles; they govern the principles used by the ASB it provides the conceptual

framework to the standards. It provides the support to the policies and methods of the ASB it

works for the betterment of the ASB (Narayanaswamy, 2017).

Financial reporting and its examples: it consist of the cash flow statement, intangible assets,

tangible fixed assets, the objectives of the FRS is to provide a authentic framework to all the

transactions conducted by this reporting (Kwok, 2017).

6

autonomous body in London. It is sole in providing the UK based standards on the accounting it

consist of the IASC which also gives the international accounting standards.

Statement of principles; they govern the principles used by the ASB it provides the conceptual

framework to the standards. It provides the support to the policies and methods of the ASB it

works for the betterment of the ASB (Narayanaswamy, 2017).

Financial reporting and its examples: it consist of the cash flow statement, intangible assets,

tangible fixed assets, the objectives of the FRS is to provide a authentic framework to all the

transactions conducted by this reporting (Kwok, 2017).

6

LO3

Describes the accounting rules and the principles

The accounting rules and principles are governed by the GAAP an autonomous body who

controls and directs the affairs of the accounting (Kwok, 2017). The rules and the principles are

the base which teaches any company to layout these sets whenever it’s performing any financial

task. They are the guided rules which everyone needs to be followed in the era of the performing

any financial statements (Kwok, 2017).

Basic accounting principles:

1. Accrual Principle: accordingly all the transactions are recorded when they actually

occurred rather than when they actually entered in the cash flows.

2. Conservatism principle: this principle talks of the conservatism to the financial

statements of recording of expenses and liabilities as early and soon but recording of

revenue and assets when they occur (Epstein, 2018).

3. Consistency principle: this includes the continuous use of the accounting standards

and the principles for a period of time.

4. Cost Principle: all the items of the company assets, liabilities and revenues and other

expenses are recorded at the original cost of purchase.

5. Economic entity principle: the transactions of the company are serrated from its

owners and the business.

6. Full disclosure principle: all the information relating to adoption of accounting

standards is disclosed by the company at the footnote of balance sheet (Adkins, 2018).

7. Going Concern Principle: it tells that the life of a business is ongoing it is not affected

by any rules and regulations it will remain responsible for all the uncertainties in future.

8. Matching principle: it talks about the entering of the expenses along with the

revenues, to match it along (Adkins, 2018).

9. Materiality principle: this concept uses the recording of transactions in the accounting

records.

7

Describes the accounting rules and the principles

The accounting rules and principles are governed by the GAAP an autonomous body who

controls and directs the affairs of the accounting (Kwok, 2017). The rules and the principles are

the base which teaches any company to layout these sets whenever it’s performing any financial

task. They are the guided rules which everyone needs to be followed in the era of the performing

any financial statements (Kwok, 2017).

Basic accounting principles:

1. Accrual Principle: accordingly all the transactions are recorded when they actually

occurred rather than when they actually entered in the cash flows.

2. Conservatism principle: this principle talks of the conservatism to the financial

statements of recording of expenses and liabilities as early and soon but recording of

revenue and assets when they occur (Epstein, 2018).

3. Consistency principle: this includes the continuous use of the accounting standards

and the principles for a period of time.

4. Cost Principle: all the items of the company assets, liabilities and revenues and other

expenses are recorded at the original cost of purchase.

5. Economic entity principle: the transactions of the company are serrated from its

owners and the business.

6. Full disclosure principle: all the information relating to adoption of accounting

standards is disclosed by the company at the footnote of balance sheet (Adkins, 2018).

7. Going Concern Principle: it tells that the life of a business is ongoing it is not affected

by any rules and regulations it will remain responsible for all the uncertainties in future.

8. Matching principle: it talks about the entering of the expenses along with the

revenues, to match it along (Adkins, 2018).

9. Materiality principle: this concept uses the recording of transactions in the accounting

records.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10. Monetary principle: all the transactions are recorded at some units and are measurable

in monetary terms (Epstein, 2018).

11. Time period principle: all the transactions are reported and monitored within a period

of time.

12. Revenue recognition principle: recognizing the revenue when the company has

completed its earnings process.

Basic rules of accounting: there are 3 rules of the accounting.

1. Personal accounts: it includes the debit the receiver and credit the giver it includes all

personal accounts like person names, firms name and other personal accounts (carrers,

2018).

2. Real account: debit what comes in credit what goes out it consist of real assets like

furniture, purchase and all.

3. Nominal account: debit all the expenses and losses and credit all incomes and gains.

Like commission received, wages, salaries etc.

Thus, the rules and principles of the accounting standards facilitate the uniformity,

accuracy and flexibility in the transactions (carrers, 2018).

8

in monetary terms (Epstein, 2018).

11. Time period principle: all the transactions are reported and monitored within a period

of time.

12. Revenue recognition principle: recognizing the revenue when the company has

completed its earnings process.

Basic rules of accounting: there are 3 rules of the accounting.

1. Personal accounts: it includes the debit the receiver and credit the giver it includes all

personal accounts like person names, firms name and other personal accounts (carrers,

2018).

2. Real account: debit what comes in credit what goes out it consist of real assets like

furniture, purchase and all.

3. Nominal account: debit all the expenses and losses and credit all incomes and gains.

Like commission received, wages, salaries etc.

Thus, the rules and principles of the accounting standards facilitate the uniformity,

accuracy and flexibility in the transactions (carrers, 2018).

8

LO4

Explain the conventions and concepts relating to consistency and material disclosure.

The principles of the consistency and the material disclosure govern that all the accounting

standards and the policies while ones adapted to the financial statements must be consistent to be

for a period of time (Berger, 2018). The materiality principle explains the disclosure of all the

related methods in the financial report.

The concept of consistency teaches us that when ones the company adopted a method of doing

accounting it must continue that in future years to attain the consistency or accuracy because

change in methods and techniques can lead to multiplication or discomfort in the whole

accounting process (Stockenstrand, 2017). Example straight line method, FIFO or LIFO methods

The concept of materiality explains that all the financial information are material to the financial

statements so they should be disclosed or attached in the financial reporting to be known by the

outsiders and insiders of the company (Narayanaswamy, 2017). For example contingent

liabilities which are shown on the footnote of the balance sheet.

Thus, all the information or the principles which are adopted in the company at a particular time

must be disclosed with final reports and must be use the constant methods to draw a accurate

result (Berger, 2018).

9

Explain the conventions and concepts relating to consistency and material disclosure.

The principles of the consistency and the material disclosure govern that all the accounting

standards and the policies while ones adapted to the financial statements must be consistent to be

for a period of time (Berger, 2018). The materiality principle explains the disclosure of all the

related methods in the financial report.

The concept of consistency teaches us that when ones the company adopted a method of doing

accounting it must continue that in future years to attain the consistency or accuracy because

change in methods and techniques can lead to multiplication or discomfort in the whole

accounting process (Stockenstrand, 2017). Example straight line method, FIFO or LIFO methods

The concept of materiality explains that all the financial information are material to the financial

statements so they should be disclosed or attached in the financial reporting to be known by the

outsiders and insiders of the company (Narayanaswamy, 2017). For example contingent

liabilities which are shown on the footnote of the balance sheet.

Thus, all the information or the principles which are adopted in the company at a particular time

must be disclosed with final reports and must be use the constant methods to draw a accurate

result (Berger, 2018).

9

Client 1

I. The book of Prime entry

Calculation of Owner's Capital

Particulars Amount

Assets:

Van 51250

Premises 340000

Fixture 8100

Receivables 4500

Inventory 63900

Cash at Bank 62400

Cash in Hand 5600

Total Assets 484500

Liabilities:

Payables 6750

Total Liabilities 6750

Owner's Equity 477750

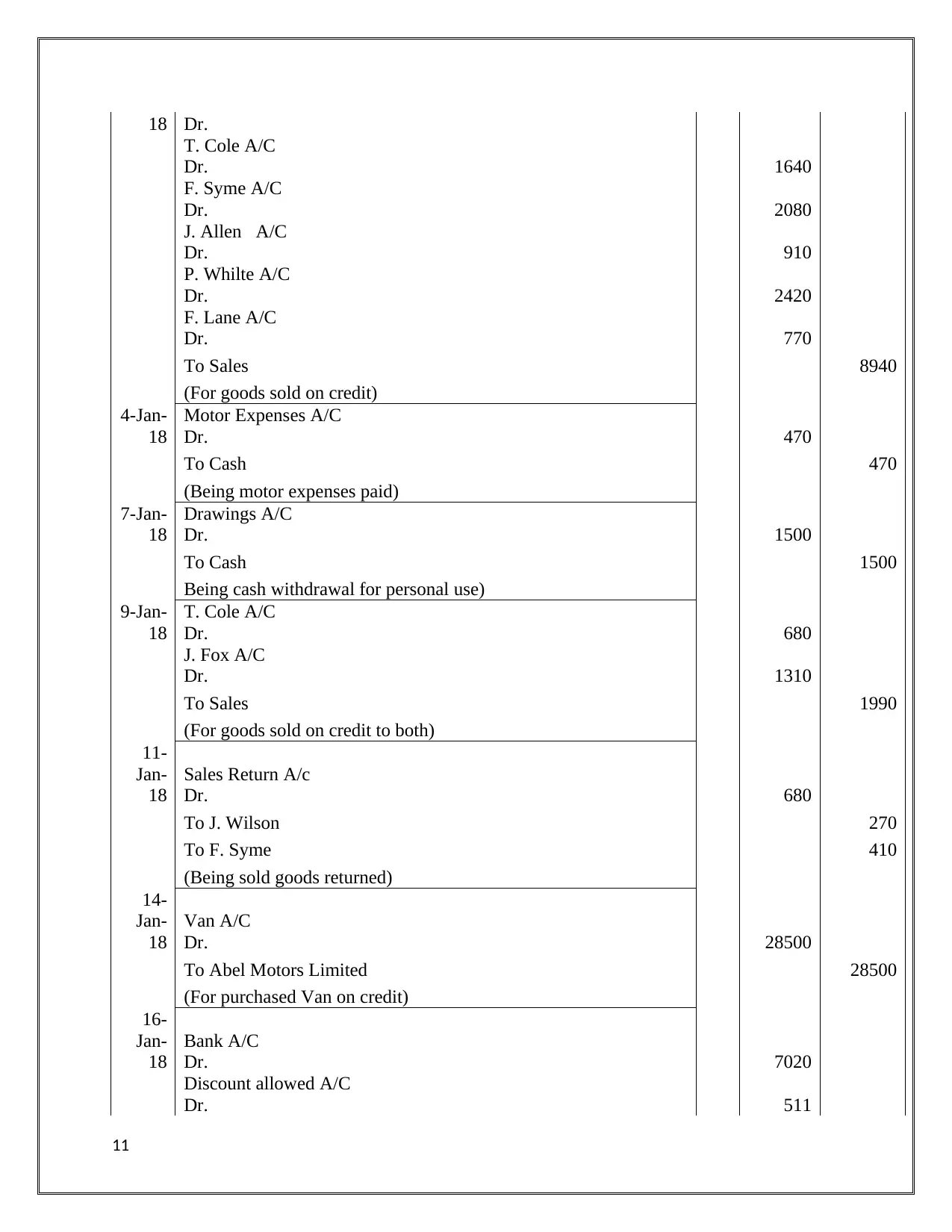

Journal Entries

In the books of Alexandra

For the Year ended January 2018

Date Particular LF Debit Credit

1-Jan-

18

Storage Expenses A/C

Dr. 400

To Bank A/C 400

(For Storage Cost paid by Cheque)

2-Jan-

18

Purchases A/C

Dr. 6080

To S. Hood 1450

To D. Main 2060

To W. Tone 960

To R. Foot 1610

(Being goods purchased on credit)

3-Jan- J. Wilson A/C 1120

10

I. The book of Prime entry

Calculation of Owner's Capital

Particulars Amount

Assets:

Van 51250

Premises 340000

Fixture 8100

Receivables 4500

Inventory 63900

Cash at Bank 62400

Cash in Hand 5600

Total Assets 484500

Liabilities:

Payables 6750

Total Liabilities 6750

Owner's Equity 477750

Journal Entries

In the books of Alexandra

For the Year ended January 2018

Date Particular LF Debit Credit

1-Jan-

18

Storage Expenses A/C

Dr. 400

To Bank A/C 400

(For Storage Cost paid by Cheque)

2-Jan-

18

Purchases A/C

Dr. 6080

To S. Hood 1450

To D. Main 2060

To W. Tone 960

To R. Foot 1610

(Being goods purchased on credit)

3-Jan- J. Wilson A/C 1120

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

18 Dr.

T. Cole A/C

Dr. 1640

F. Syme A/C

Dr. 2080

J. Allen A/C

Dr. 910

P. Whilte A/C

Dr. 2420

F. Lane A/C

Dr. 770

To Sales 8940

(For goods sold on credit)

4-Jan-

18

Motor Expenses A/C

Dr. 470

To Cash 470

(Being motor expenses paid)

7-Jan-

18

Drawings A/C

Dr. 1500

To Cash 1500

Being cash withdrawal for personal use)

9-Jan-

18

T. Cole A/C

Dr. 680

J. Fox A/C

Dr. 1310

To Sales 1990

(For goods sold on credit to both)

11-

Jan-

18

Sales Return A/c

Dr. 680

To J. Wilson 270

To F. Syme 410

(Being sold goods returned)

14-

Jan-

18

Van A/C

Dr. 28500

To Abel Motors Limited 28500

(For purchased Van on credit)

16-

Jan-

18

Bank A/C

Dr. 7020

Discount allowed A/C

Dr. 511

11

T. Cole A/C

Dr. 1640

F. Syme A/C

Dr. 2080

J. Allen A/C

Dr. 910

P. Whilte A/C

Dr. 2420

F. Lane A/C

Dr. 770

To Sales 8940

(For goods sold on credit)

4-Jan-

18

Motor Expenses A/C

Dr. 470

To Cash 470

(Being motor expenses paid)

7-Jan-

18

Drawings A/C

Dr. 1500

To Cash 1500

Being cash withdrawal for personal use)

9-Jan-

18

T. Cole A/C

Dr. 680

J. Fox A/C

Dr. 1310

To Sales 1990

(For goods sold on credit to both)

11-

Jan-

18

Sales Return A/c

Dr. 680

To J. Wilson 270

To F. Syme 410

(Being sold goods returned)

14-

Jan-

18

Van A/C

Dr. 28500

To Abel Motors Limited 28500

(For purchased Van on credit)

16-

Jan-

18

Bank A/C

Dr. 7020

Discount allowed A/C

Dr. 511

11

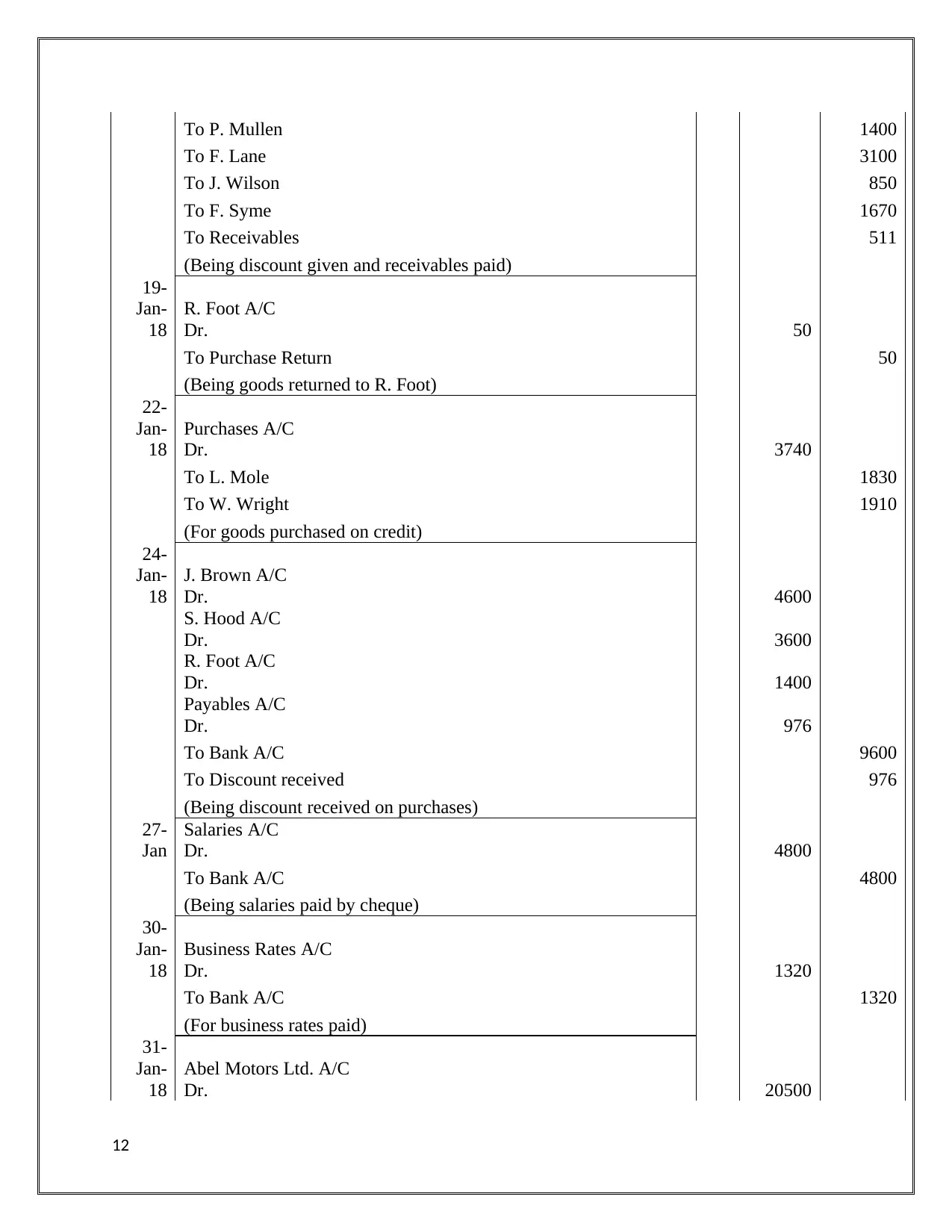

To P. Mullen 1400

To F. Lane 3100

To J. Wilson 850

To F. Syme 1670

To Receivables 511

(Being discount given and receivables paid)

19-

Jan-

18

R. Foot A/C

Dr. 50

To Purchase Return 50

(Being goods returned to R. Foot)

22-

Jan-

18

Purchases A/C

Dr. 3740

To L. Mole 1830

To W. Wright 1910

(For goods purchased on credit)

24-

Jan-

18

J. Brown A/C

Dr. 4600

S. Hood A/C

Dr. 3600

R. Foot A/C

Dr. 1400

Payables A/C

Dr. 976

To Bank A/C 9600

To Discount received 976

(Being discount received on purchases)

27-

Jan

Salaries A/C

Dr. 4800

To Bank A/C 4800

(Being salaries paid by cheque)

30-

Jan-

18

Business Rates A/C

Dr. 1320

To Bank A/C 1320

(For business rates paid)

31-

Jan-

18

Abel Motors Ltd. A/C

Dr. 20500

12

To F. Lane 3100

To J. Wilson 850

To F. Syme 1670

To Receivables 511

(Being discount given and receivables paid)

19-

Jan-

18

R. Foot A/C

Dr. 50

To Purchase Return 50

(Being goods returned to R. Foot)

22-

Jan-

18

Purchases A/C

Dr. 3740

To L. Mole 1830

To W. Wright 1910

(For goods purchased on credit)

24-

Jan-

18

J. Brown A/C

Dr. 4600

S. Hood A/C

Dr. 3600

R. Foot A/C

Dr. 1400

Payables A/C

Dr. 976

To Bank A/C 9600

To Discount received 976

(Being discount received on purchases)

27-

Jan

Salaries A/C

Dr. 4800

To Bank A/C 4800

(Being salaries paid by cheque)

30-

Jan-

18

Business Rates A/C

Dr. 1320

To Bank A/C 1320

(For business rates paid)

31-

Jan-

18

Abel Motors Ltd. A/C

Dr. 20500

12

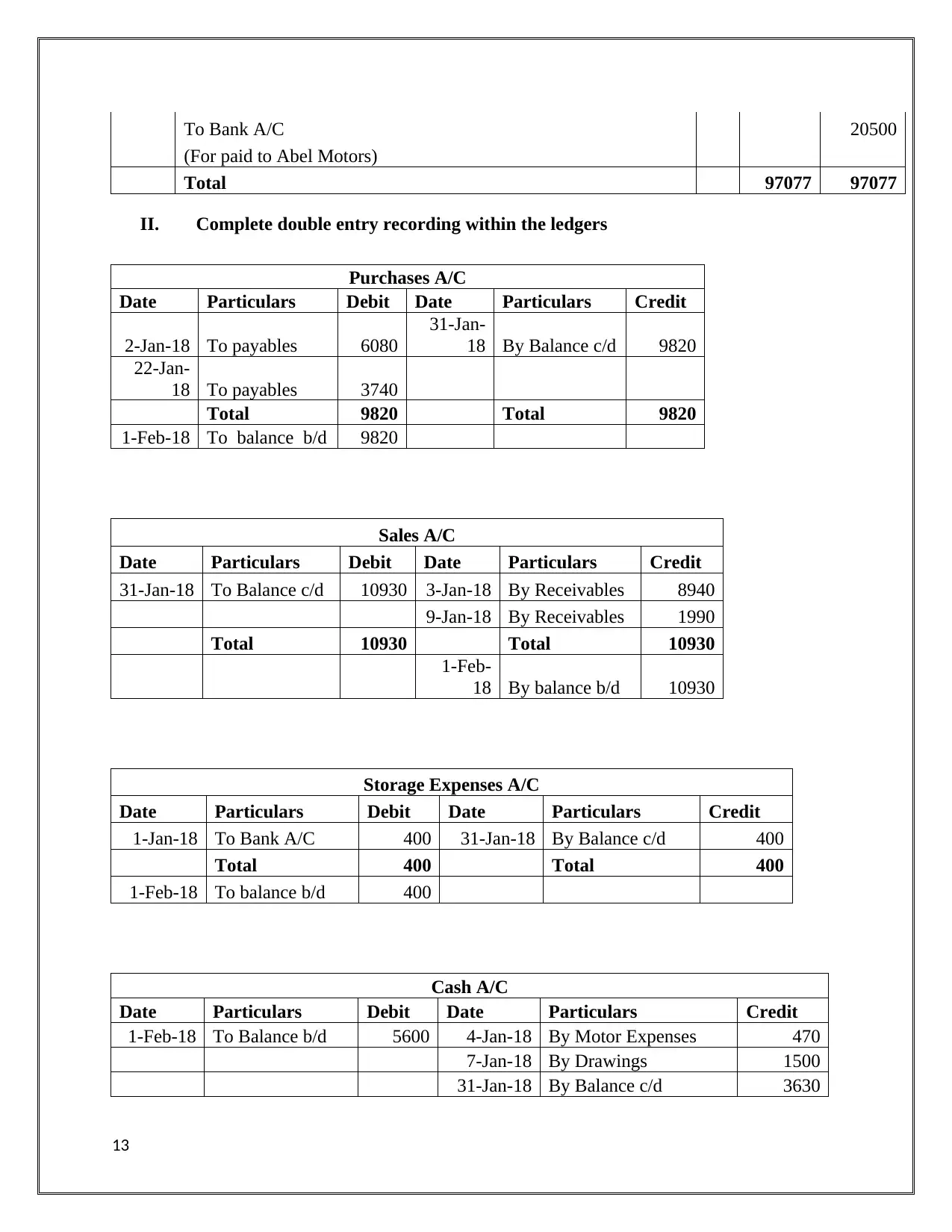

To Bank A/C 20500

(For paid to Abel Motors)

Total 97077 97077

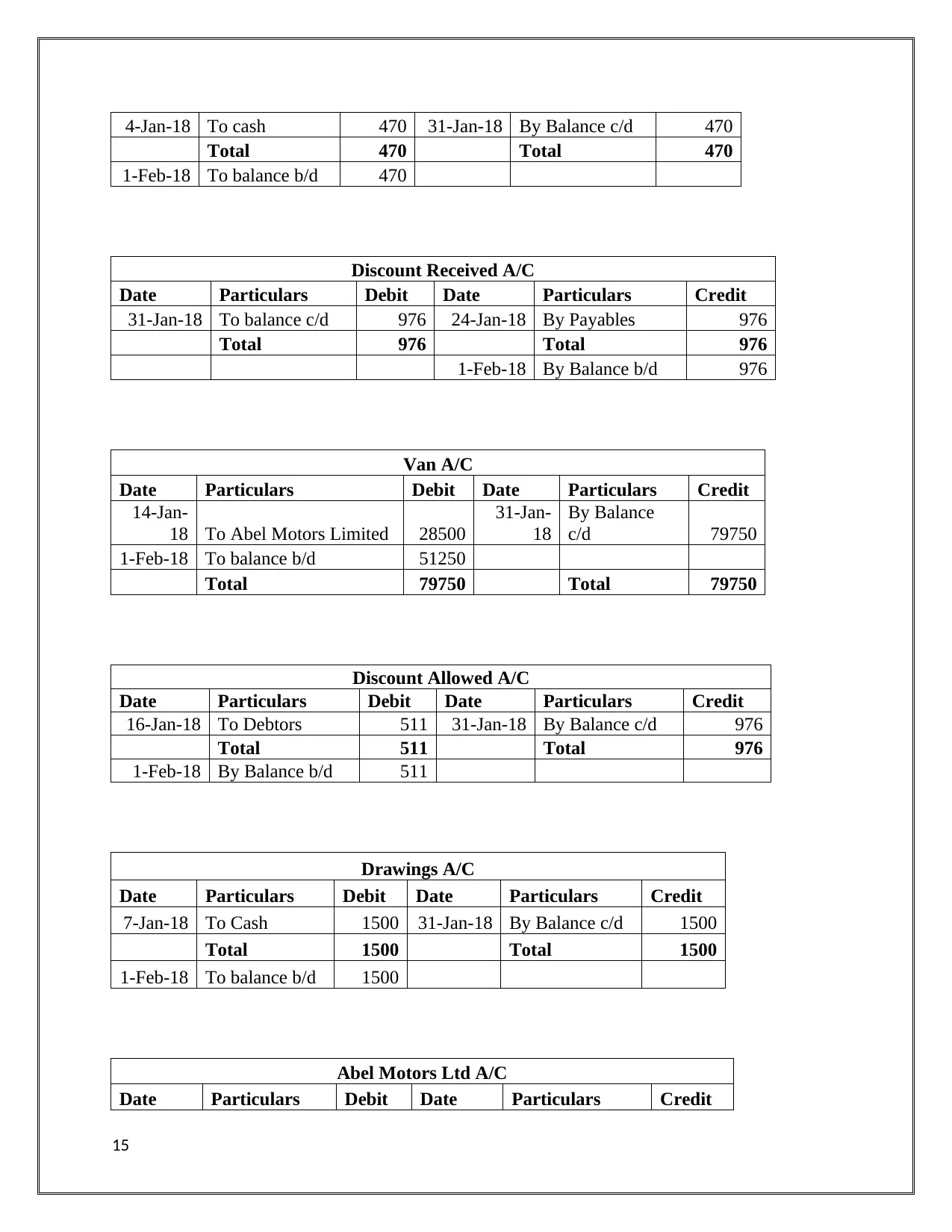

II. Complete double entry recording within the ledgers

Purchases A/C

Date Particulars Debit Date Particulars Credit

2-Jan-18 To payables 6080

31-Jan-

18 By Balance c/d 9820

22-Jan-

18 To payables 3740

Total 9820 Total 9820

1-Feb-18 To balance b/d 9820

Sales A/C

Date Particulars Debit Date Particulars Credit

31-Jan-18 To Balance c/d 10930 3-Jan-18 By Receivables 8940

9-Jan-18 By Receivables 1990

Total 10930 Total 10930

1-Feb-

18 By balance b/d 10930

Storage Expenses A/C

Date Particulars Debit Date Particulars Credit

1-Jan-18 To Bank A/C 400 31-Jan-18 By Balance c/d 400

Total 400 Total 400

1-Feb-18 To balance b/d 400

Cash A/C

Date Particulars Debit Date Particulars Credit

1-Feb-18 To Balance b/d 5600 4-Jan-18 By Motor Expenses 470

7-Jan-18 By Drawings 1500

31-Jan-18 By Balance c/d 3630

13

(For paid to Abel Motors)

Total 97077 97077

II. Complete double entry recording within the ledgers

Purchases A/C

Date Particulars Debit Date Particulars Credit

2-Jan-18 To payables 6080

31-Jan-

18 By Balance c/d 9820

22-Jan-

18 To payables 3740

Total 9820 Total 9820

1-Feb-18 To balance b/d 9820

Sales A/C

Date Particulars Debit Date Particulars Credit

31-Jan-18 To Balance c/d 10930 3-Jan-18 By Receivables 8940

9-Jan-18 By Receivables 1990

Total 10930 Total 10930

1-Feb-

18 By balance b/d 10930

Storage Expenses A/C

Date Particulars Debit Date Particulars Credit

1-Jan-18 To Bank A/C 400 31-Jan-18 By Balance c/d 400

Total 400 Total 400

1-Feb-18 To balance b/d 400

Cash A/C

Date Particulars Debit Date Particulars Credit

1-Feb-18 To Balance b/d 5600 4-Jan-18 By Motor Expenses 470

7-Jan-18 By Drawings 1500

31-Jan-18 By Balance c/d 3630

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

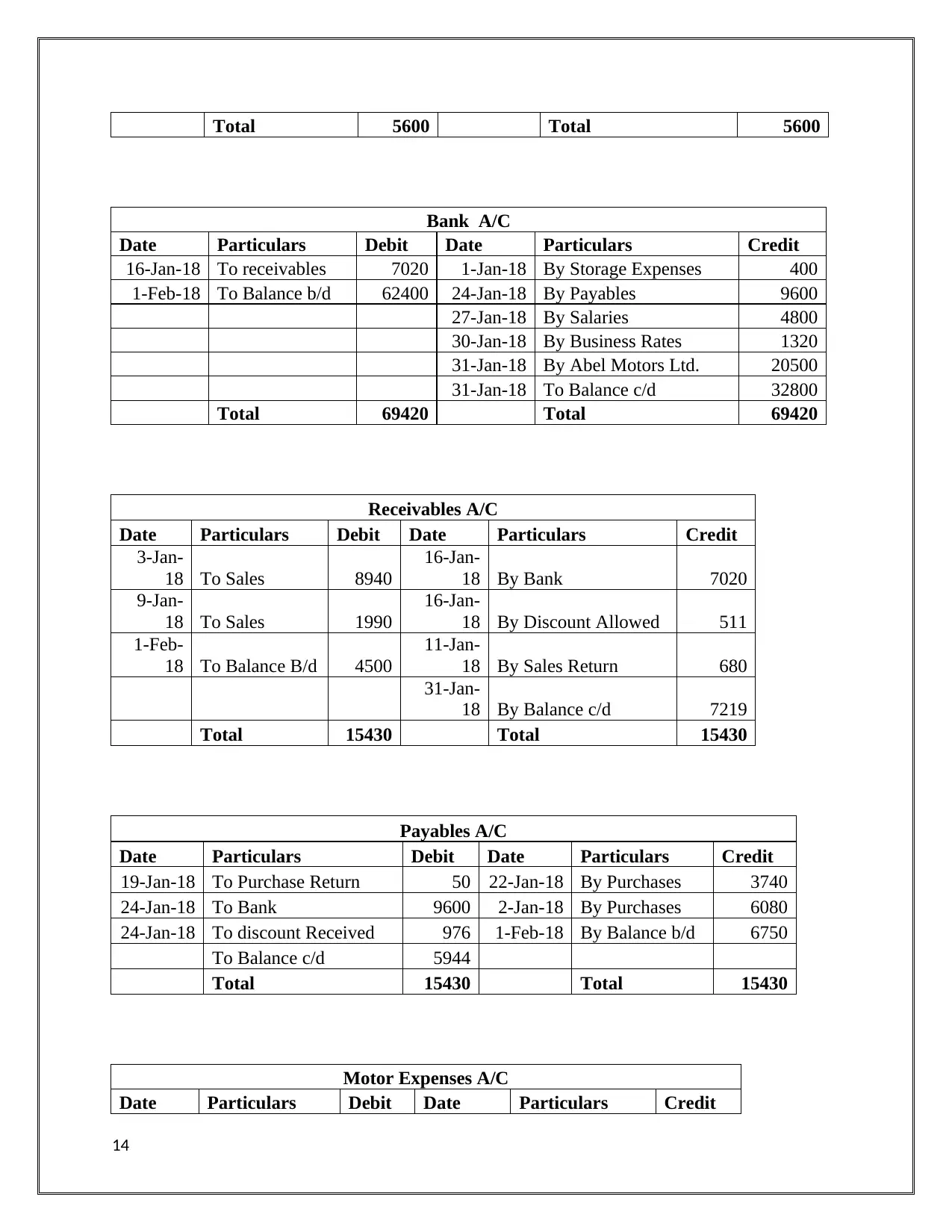

Total 5600 Total 5600

Bank A/C

Date Particulars Debit Date Particulars Credit

16-Jan-18 To receivables 7020 1-Jan-18 By Storage Expenses 400

1-Feb-18 To Balance b/d 62400 24-Jan-18 By Payables 9600

27-Jan-18 By Salaries 4800

30-Jan-18 By Business Rates 1320

31-Jan-18 By Abel Motors Ltd. 20500

31-Jan-18 To Balance c/d 32800

Total 69420 Total 69420

Receivables A/C

Date Particulars Debit Date Particulars Credit

3-Jan-

18 To Sales 8940

16-Jan-

18 By Bank 7020

9-Jan-

18 To Sales 1990

16-Jan-

18 By Discount Allowed 511

1-Feb-

18 To Balance B/d 4500

11-Jan-

18 By Sales Return 680

31-Jan-

18 By Balance c/d 7219

Total 15430 Total 15430

Payables A/C

Date Particulars Debit Date Particulars Credit

19-Jan-18 To Purchase Return 50 22-Jan-18 By Purchases 3740

24-Jan-18 To Bank 9600 2-Jan-18 By Purchases 6080

24-Jan-18 To discount Received 976 1-Feb-18 By Balance b/d 6750

To Balance c/d 5944

Total 15430 Total 15430

Motor Expenses A/C

Date Particulars Debit Date Particulars Credit

14

Bank A/C

Date Particulars Debit Date Particulars Credit

16-Jan-18 To receivables 7020 1-Jan-18 By Storage Expenses 400

1-Feb-18 To Balance b/d 62400 24-Jan-18 By Payables 9600

27-Jan-18 By Salaries 4800

30-Jan-18 By Business Rates 1320

31-Jan-18 By Abel Motors Ltd. 20500

31-Jan-18 To Balance c/d 32800

Total 69420 Total 69420

Receivables A/C

Date Particulars Debit Date Particulars Credit

3-Jan-

18 To Sales 8940

16-Jan-

18 By Bank 7020

9-Jan-

18 To Sales 1990

16-Jan-

18 By Discount Allowed 511

1-Feb-

18 To Balance B/d 4500

11-Jan-

18 By Sales Return 680

31-Jan-

18 By Balance c/d 7219

Total 15430 Total 15430

Payables A/C

Date Particulars Debit Date Particulars Credit

19-Jan-18 To Purchase Return 50 22-Jan-18 By Purchases 3740

24-Jan-18 To Bank 9600 2-Jan-18 By Purchases 6080

24-Jan-18 To discount Received 976 1-Feb-18 By Balance b/d 6750

To Balance c/d 5944

Total 15430 Total 15430

Motor Expenses A/C

Date Particulars Debit Date Particulars Credit

14

4-Jan-18 To cash 470 31-Jan-18 By Balance c/d 470

Total 470 Total 470

1-Feb-18 To balance b/d 470

Discount Received A/C

Date Particulars Debit Date Particulars Credit

31-Jan-18 To balance c/d 976 24-Jan-18 By Payables 976

Total 976 Total 976

1-Feb-18 By Balance b/d 976

Van A/C

Date Particulars Debit Date Particulars Credit

14-Jan-

18 To Abel Motors Limited 28500

31-Jan-

18

By Balance

c/d 79750

1-Feb-18 To balance b/d 51250

Total 79750 Total 79750

Discount Allowed A/C

Date Particulars Debit Date Particulars Credit

16-Jan-18 To Debtors 511 31-Jan-18 By Balance c/d 976

Total 511 Total 976

1-Feb-18 By Balance b/d 511

Drawings A/C

Date Particulars Debit Date Particulars Credit

7-Jan-18 To Cash 1500 31-Jan-18 By Balance c/d 1500

Total 1500 Total 1500

1-Feb-18 To balance b/d 1500

Abel Motors Ltd A/C

Date Particulars Debit Date Particulars Credit

15

Total 470 Total 470

1-Feb-18 To balance b/d 470

Discount Received A/C

Date Particulars Debit Date Particulars Credit

31-Jan-18 To balance c/d 976 24-Jan-18 By Payables 976

Total 976 Total 976

1-Feb-18 By Balance b/d 976

Van A/C

Date Particulars Debit Date Particulars Credit

14-Jan-

18 To Abel Motors Limited 28500

31-Jan-

18

By Balance

c/d 79750

1-Feb-18 To balance b/d 51250

Total 79750 Total 79750

Discount Allowed A/C

Date Particulars Debit Date Particulars Credit

16-Jan-18 To Debtors 511 31-Jan-18 By Balance c/d 976

Total 511 Total 976

1-Feb-18 By Balance b/d 511

Drawings A/C

Date Particulars Debit Date Particulars Credit

7-Jan-18 To Cash 1500 31-Jan-18 By Balance c/d 1500

Total 1500 Total 1500

1-Feb-18 To balance b/d 1500

Abel Motors Ltd A/C

Date Particulars Debit Date Particulars Credit

15

31-Jan-18 To Bank 2050 14-Jan-18 By Van 28500

31-Jan-18 To balance c/d 8000

Total 28500 Total 28500

1-Feb-18 By Balance B/d 8000

Business Rates A/C

Date Particulars Debit Date Particulars Credit

30-Jan-18 To Bank 1320 31-Jan-18 By Balance c/d 1320

Total 1320 Total 1320

1-Feb-18 To Balance b/d 1320

Salary A/C

Date Particulars Debit Date Particulars Credit

27-Jan-18 To Bank 4800 31-Jan-18 By Balance c/d 4800

Total 4800 Total 4800

1-Feb-18 To Balance b/d 4800

Sales Return A/C

Date Particulars Debit Date Particulars Credit

11-Jan-18 To receivables 680 31-Jan-18 By Balance c/d 680

Total 680 Total 680

1-Feb-18 To Balance b/d 680

Purchase Return A/C

Date Particulars Debit Date Particulars Credit

31-Jan-18 To Balance c/d 50 19-Jan-18 By Payables 50

Total 50 Total 50

1-Feb-18 By Balance b/d 50

III. Trial Balance to check the accuracy of double entry systems

Trial Balance of Alexandra

16

31-Jan-18 To balance c/d 8000

Total 28500 Total 28500

1-Feb-18 By Balance B/d 8000

Business Rates A/C

Date Particulars Debit Date Particulars Credit

30-Jan-18 To Bank 1320 31-Jan-18 By Balance c/d 1320

Total 1320 Total 1320

1-Feb-18 To Balance b/d 1320

Salary A/C

Date Particulars Debit Date Particulars Credit

27-Jan-18 To Bank 4800 31-Jan-18 By Balance c/d 4800

Total 4800 Total 4800

1-Feb-18 To Balance b/d 4800

Sales Return A/C

Date Particulars Debit Date Particulars Credit

11-Jan-18 To receivables 680 31-Jan-18 By Balance c/d 680

Total 680 Total 680

1-Feb-18 To Balance b/d 680

Purchase Return A/C

Date Particulars Debit Date Particulars Credit

31-Jan-18 To Balance c/d 50 19-Jan-18 By Payables 50

Total 50 Total 50

1-Feb-18 By Balance b/d 50

III. Trial Balance to check the accuracy of double entry systems

Trial Balance of Alexandra

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

for January 2018

Particulars Debit Credit

Purchases 9770

Business Rates 1320

Van 79750

Discount allowed 511

Receivables 7219

Salary 4800

Premises 340000

Inventory 63900

Fixtures 8100

Motor Expenses 470

Drawings 1500

Storage Expenses 400

Cash 3630

Bank 32800

Sales 10250

Payables 5944

Capital 529000

Discount received 976

Abel Motors Ltd. 8000

Trial Balance 554170 554170

17

Particulars Debit Credit

Purchases 9770

Business Rates 1320

Van 79750

Discount allowed 511

Receivables 7219

Salary 4800

Premises 340000

Inventory 63900

Fixtures 8100

Motor Expenses 470

Drawings 1500

Storage Expenses 400

Cash 3630

Bank 32800

Sales 10250

Payables 5944

Capital 529000

Discount received 976

Abel Motors Ltd. 8000

Trial Balance 554170 554170

17

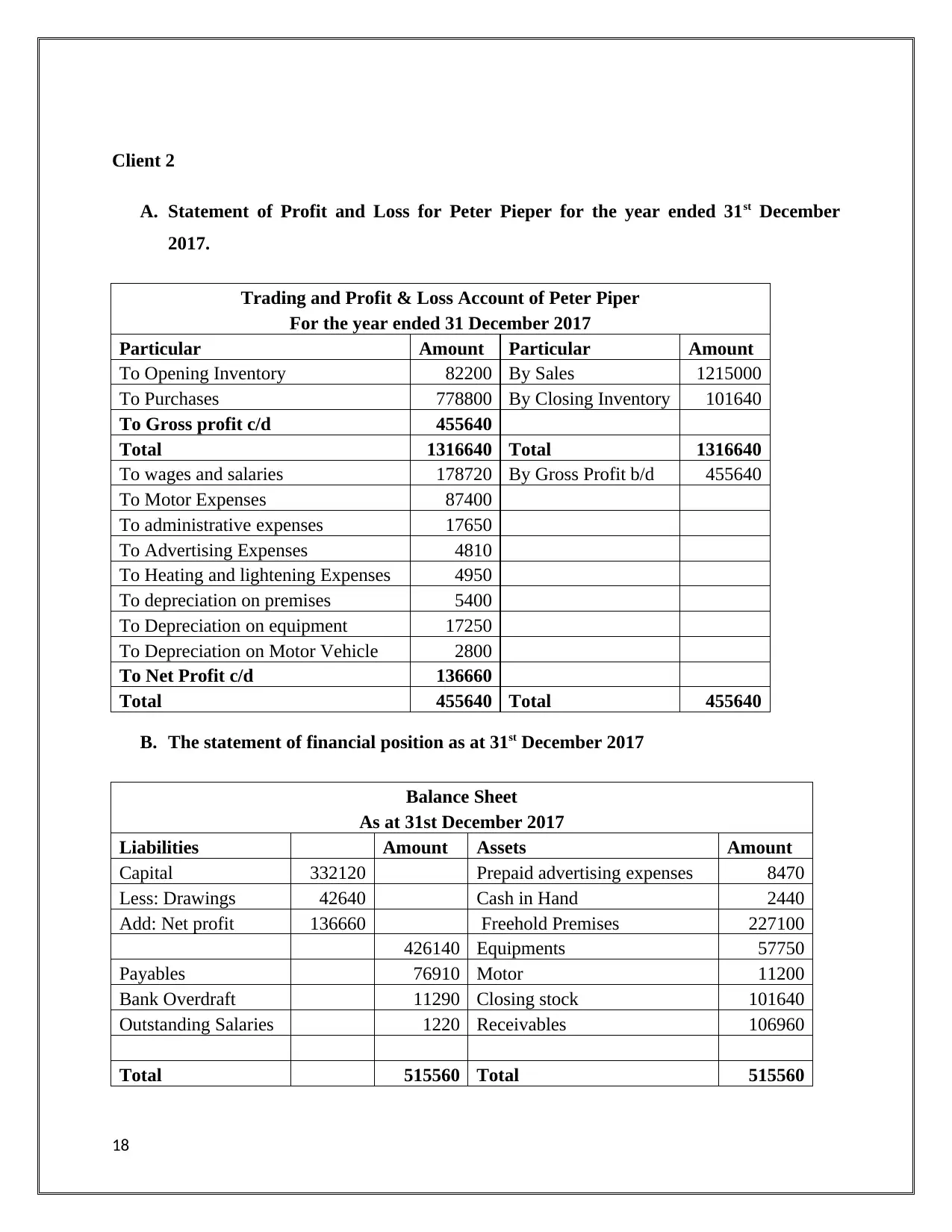

Client 2

A. Statement of Profit and Loss for Peter Pieper for the year ended 31st December

2017.

Trading and Profit & Loss Account of Peter Piper

For the year ended 31 December 2017

Particular Amount Particular Amount

To Opening Inventory 82200 By Sales 1215000

To Purchases 778800 By Closing Inventory 101640

To Gross profit c/d 455640

Total 1316640 Total 1316640

To wages and salaries 178720 By Gross Profit b/d 455640

To Motor Expenses 87400

To administrative expenses 17650

To Advertising Expenses 4810

To Heating and lightening Expenses 4950

To depreciation on premises 5400

To Depreciation on equipment 17250

To Depreciation on Motor Vehicle 2800

To Net Profit c/d 136660

Total 455640 Total 455640

B. The statement of financial position as at 31st December 2017

Balance Sheet

As at 31st December 2017

Liabilities Amount Assets Amount

Capital 332120 Prepaid advertising expenses 8470

Less: Drawings 42640 Cash in Hand 2440

Add: Net profit 136660 Freehold Premises 227100

426140 Equipments 57750

Payables 76910 Motor 11200

Bank Overdraft 11290 Closing stock 101640

Outstanding Salaries 1220 Receivables 106960

Total 515560 Total 515560

18

A. Statement of Profit and Loss for Peter Pieper for the year ended 31st December

2017.

Trading and Profit & Loss Account of Peter Piper

For the year ended 31 December 2017

Particular Amount Particular Amount

To Opening Inventory 82200 By Sales 1215000

To Purchases 778800 By Closing Inventory 101640

To Gross profit c/d 455640

Total 1316640 Total 1316640

To wages and salaries 178720 By Gross Profit b/d 455640

To Motor Expenses 87400

To administrative expenses 17650

To Advertising Expenses 4810

To Heating and lightening Expenses 4950

To depreciation on premises 5400

To Depreciation on equipment 17250

To Depreciation on Motor Vehicle 2800

To Net Profit c/d 136660

Total 455640 Total 455640

B. The statement of financial position as at 31st December 2017

Balance Sheet

As at 31st December 2017

Liabilities Amount Assets Amount

Capital 332120 Prepaid advertising expenses 8470

Less: Drawings 42640 Cash in Hand 2440

Add: Net profit 136660 Freehold Premises 227100

426140 Equipments 57750

Payables 76910 Motor 11200

Bank Overdraft 11290 Closing stock 101640

Outstanding Salaries 1220 Receivables 106960

Total 515560 Total 515560

18

Client 3

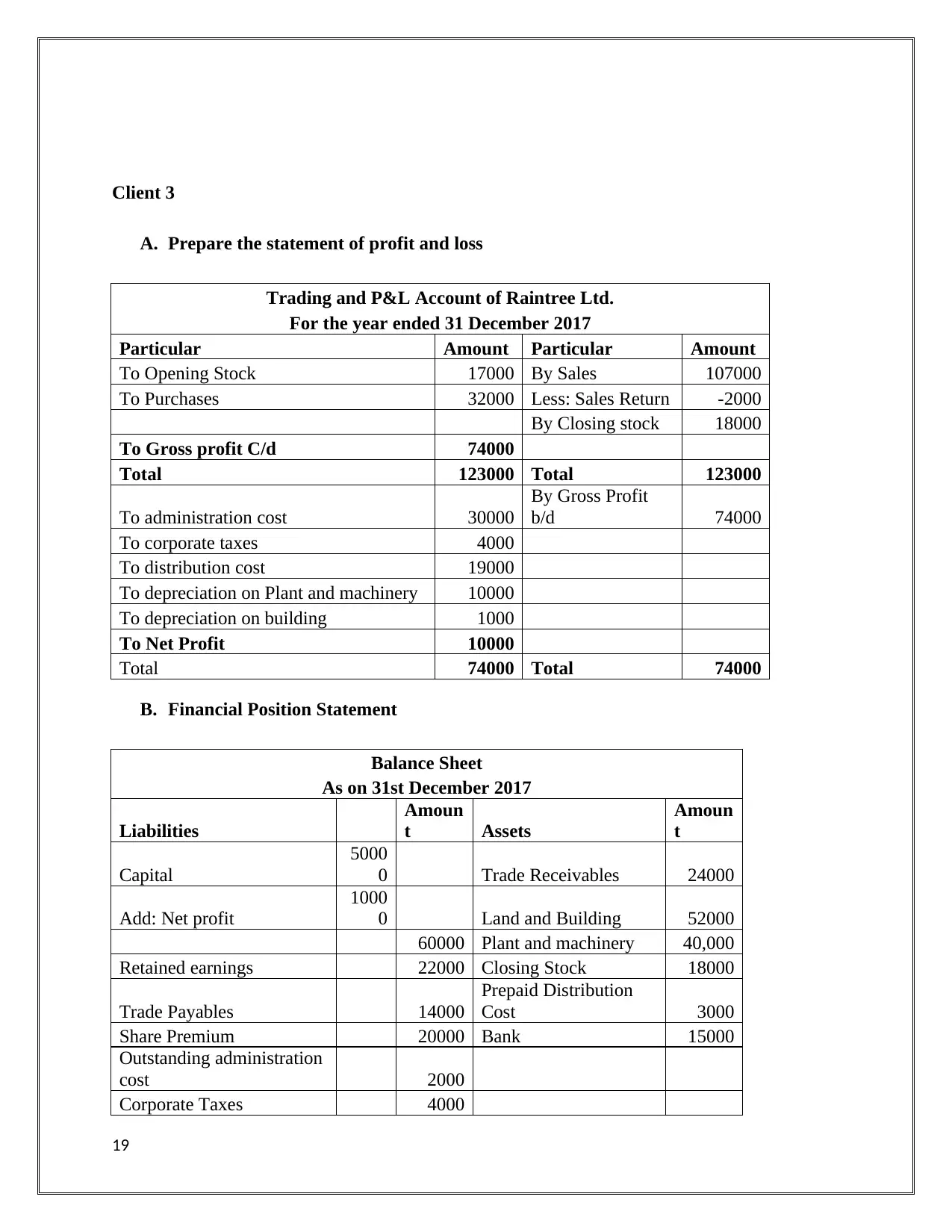

A. Prepare the statement of profit and loss

Trading and P&L Account of Raintree Ltd.

For the year ended 31 December 2017

Particular Amount Particular Amount

To Opening Stock 17000 By Sales 107000

To Purchases 32000 Less: Sales Return -2000

By Closing stock 18000

To Gross profit C/d 74000

Total 123000 Total 123000

To administration cost 30000

By Gross Profit

b/d 74000

To corporate taxes 4000

To distribution cost 19000

To depreciation on Plant and machinery 10000

To depreciation on building 1000

To Net Profit 10000

Total 74000 Total 74000

B. Financial Position Statement

Balance Sheet

As on 31st December 2017

Liabilities

Amoun

t Assets

Amoun

t

Capital

5000

0 Trade Receivables 24000

Add: Net profit

1000

0 Land and Building 52000

60000 Plant and machinery 40,000

Retained earnings 22000 Closing Stock 18000

Trade Payables 14000

Prepaid Distribution

Cost 3000

Share Premium 20000 Bank 15000

Outstanding administration

cost 2000

Corporate Taxes 4000

19

A. Prepare the statement of profit and loss

Trading and P&L Account of Raintree Ltd.

For the year ended 31 December 2017

Particular Amount Particular Amount

To Opening Stock 17000 By Sales 107000

To Purchases 32000 Less: Sales Return -2000

By Closing stock 18000

To Gross profit C/d 74000

Total 123000 Total 123000

To administration cost 30000

By Gross Profit

b/d 74000

To corporate taxes 4000

To distribution cost 19000

To depreciation on Plant and machinery 10000

To depreciation on building 1000

To Net Profit 10000

Total 74000 Total 74000

B. Financial Position Statement

Balance Sheet

As on 31st December 2017

Liabilities

Amoun

t Assets

Amoun

t

Capital

5000

0 Trade Receivables 24000

Add: Net profit

1000

0 Land and Building 52000

60000 Plant and machinery 40,000

Retained earnings 22000 Closing Stock 18000

Trade Payables 14000

Prepaid Distribution

Cost 3000

Share Premium 20000 Bank 15000

Outstanding administration

cost 2000

Corporate Taxes 4000

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Suspense account 30000

Total 152000 Total 152000

C. The concept of consistency means that the method which is adopted should be

consistently is used in future so as to avoid the issues which are related to the evaluation

of the financial position (Narayanaswamy, 2017). This concept is important as it enables

the investors to take the investment related decisions.

The prudence concept states that the organization should be conservative in recording the

transactions related to the assets and should not underestimate the liabilities of organization. This

concept reveals that there should be conservatism in financial statements (Kwok, 2017).

D. The main purpose of depreciation is that it helps in evaluating the actual value of assets

which are used for the long term operations (Narayanaswamy, 2017). Without

depreciation the managers would not be able to evaluate the actual financial state of the

organization. With this it also determines the decrease in the assets value. The methods of

depreciation are as follows:

Written down Value Method: the written down value method is also called the diminishing

value method. Under this method the depreciation is calculated at the fixed rate every year at

book value (Berger, 2018). This is done so that the actual value of the asset can be determined in

the current accounting period.

Straight Line Method: This method uses the same amount of depreciation every year so as to

evaluate the value of assets. This method is one of the easy methods to calculate the amount of

assets as it is charged at the same amount (Narayanaswamy, 2017).

20

Total 152000 Total 152000

C. The concept of consistency means that the method which is adopted should be

consistently is used in future so as to avoid the issues which are related to the evaluation

of the financial position (Narayanaswamy, 2017). This concept is important as it enables

the investors to take the investment related decisions.

The prudence concept states that the organization should be conservative in recording the

transactions related to the assets and should not underestimate the liabilities of organization. This

concept reveals that there should be conservatism in financial statements (Kwok, 2017).

D. The main purpose of depreciation is that it helps in evaluating the actual value of assets

which are used for the long term operations (Narayanaswamy, 2017). Without

depreciation the managers would not be able to evaluate the actual financial state of the

organization. With this it also determines the decrease in the assets value. The methods of

depreciation are as follows:

Written down Value Method: the written down value method is also called the diminishing

value method. Under this method the depreciation is calculated at the fixed rate every year at

book value (Berger, 2018). This is done so that the actual value of the asset can be determined in

the current accounting period.

Straight Line Method: This method uses the same amount of depreciation every year so as to

evaluate the value of assets. This method is one of the easy methods to calculate the amount of

assets as it is charged at the same amount (Narayanaswamy, 2017).

20

Client 4

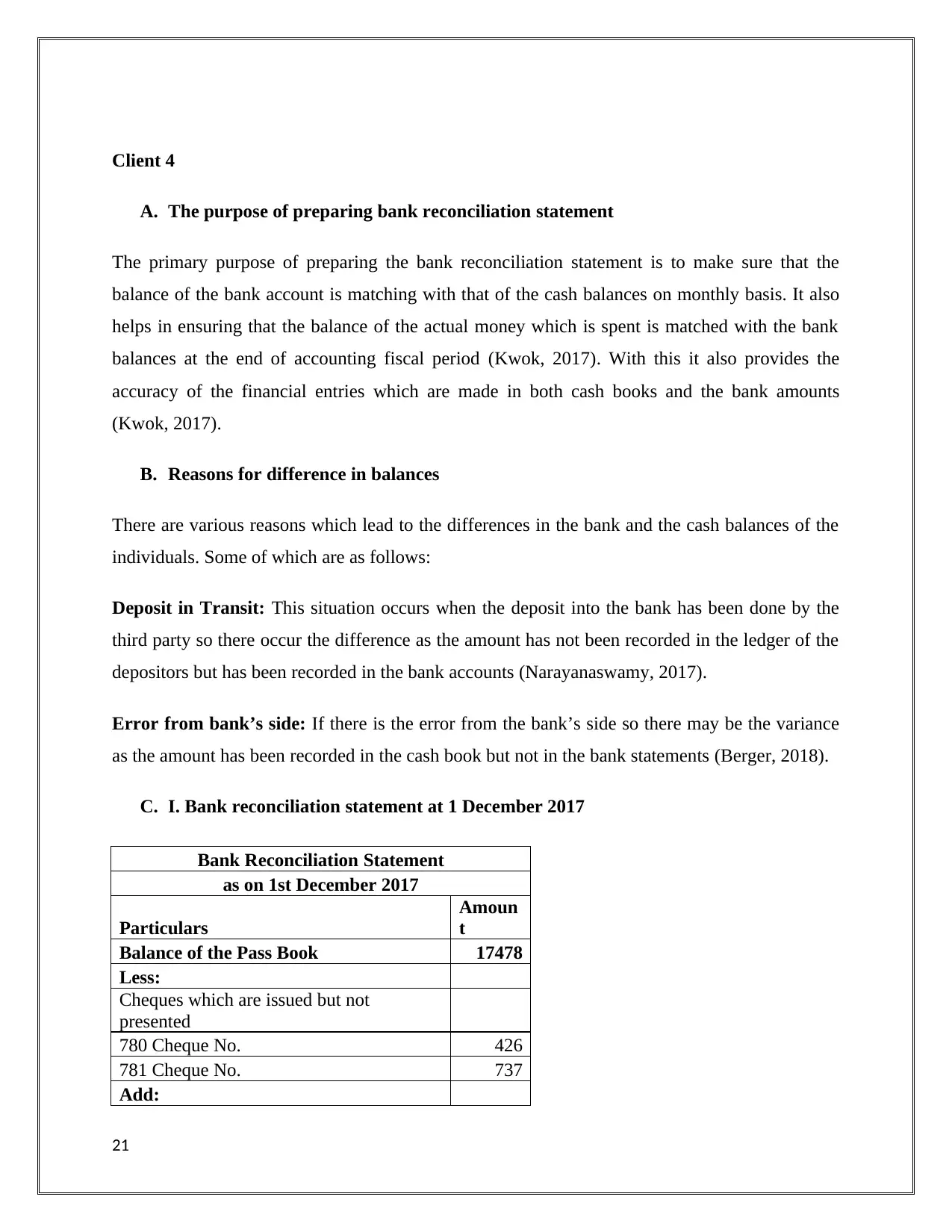

A. The purpose of preparing bank reconciliation statement

The primary purpose of preparing the bank reconciliation statement is to make sure that the

balance of the bank account is matching with that of the cash balances on monthly basis. It also

helps in ensuring that the balance of the actual money which is spent is matched with the bank

balances at the end of accounting fiscal period (Kwok, 2017). With this it also provides the

accuracy of the financial entries which are made in both cash books and the bank amounts

(Kwok, 2017).

B. Reasons for difference in balances

There are various reasons which lead to the differences in the bank and the cash balances of the

individuals. Some of which are as follows:

Deposit in Transit: This situation occurs when the deposit into the bank has been done by the

third party so there occur the difference as the amount has not been recorded in the ledger of the

depositors but has been recorded in the bank accounts (Narayanaswamy, 2017).

Error from bank’s side: If there is the error from the bank’s side so there may be the variance

as the amount has been recorded in the cash book but not in the bank statements (Berger, 2018).

C. I. Bank reconciliation statement at 1 December 2017

Bank Reconciliation Statement

as on 1st December 2017

Particulars

Amoun

t

Balance of the Pass Book 17478

Less:

Cheques which are issued but not

presented

780 Cheque No. 426

781 Cheque No. 737

Add:

21

A. The purpose of preparing bank reconciliation statement

The primary purpose of preparing the bank reconciliation statement is to make sure that the

balance of the bank account is matching with that of the cash balances on monthly basis. It also

helps in ensuring that the balance of the actual money which is spent is matched with the bank

balances at the end of accounting fiscal period (Kwok, 2017). With this it also provides the

accuracy of the financial entries which are made in both cash books and the bank amounts

(Kwok, 2017).

B. Reasons for difference in balances

There are various reasons which lead to the differences in the bank and the cash balances of the

individuals. Some of which are as follows:

Deposit in Transit: This situation occurs when the deposit into the bank has been done by the

third party so there occur the difference as the amount has not been recorded in the ledger of the

depositors but has been recorded in the bank accounts (Narayanaswamy, 2017).

Error from bank’s side: If there is the error from the bank’s side so there may be the variance

as the amount has been recorded in the cash book but not in the bank statements (Berger, 2018).

C. I. Bank reconciliation statement at 1 December 2017

Bank Reconciliation Statement

as on 1st December 2017

Particulars

Amoun

t

Balance of the Pass Book 17478

Less:

Cheques which are issued but not

presented

780 Cheque No. 426

781 Cheque No. 737

Add:

21

Deposits as on 2 December 176

Balance as per Cash Book 16491

II.

The updated cash book cannot be prepared in this scenario as all the adjustments has been done

in the reconciliation statement.

III.

Bank Reconciliation Statement

as at 1st December 2017

Particulars Amount

Balance of the pass Book 19738

Less:

Cheque issued but not presented

783 Cheque No. 9

785 Cheque No. 97

787 Cheque No. 260

366

Add:

Standing Order 137

310923 297

Bank Charges 47

Deposits 1

Fred 119

601

Balance as per Cash Book 19973

22

Balance as per Cash Book 16491

II.

The updated cash book cannot be prepared in this scenario as all the adjustments has been done

in the reconciliation statement.

III.

Bank Reconciliation Statement

as at 1st December 2017

Particulars Amount

Balance of the pass Book 19738

Less:

Cheque issued but not presented

783 Cheque No. 9

785 Cheque No. 97

787 Cheque No. 260

366

Add:

Standing Order 137

310923 297

Bank Charges 47

Deposits 1

Fred 119

601

Balance as per Cash Book 19973

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

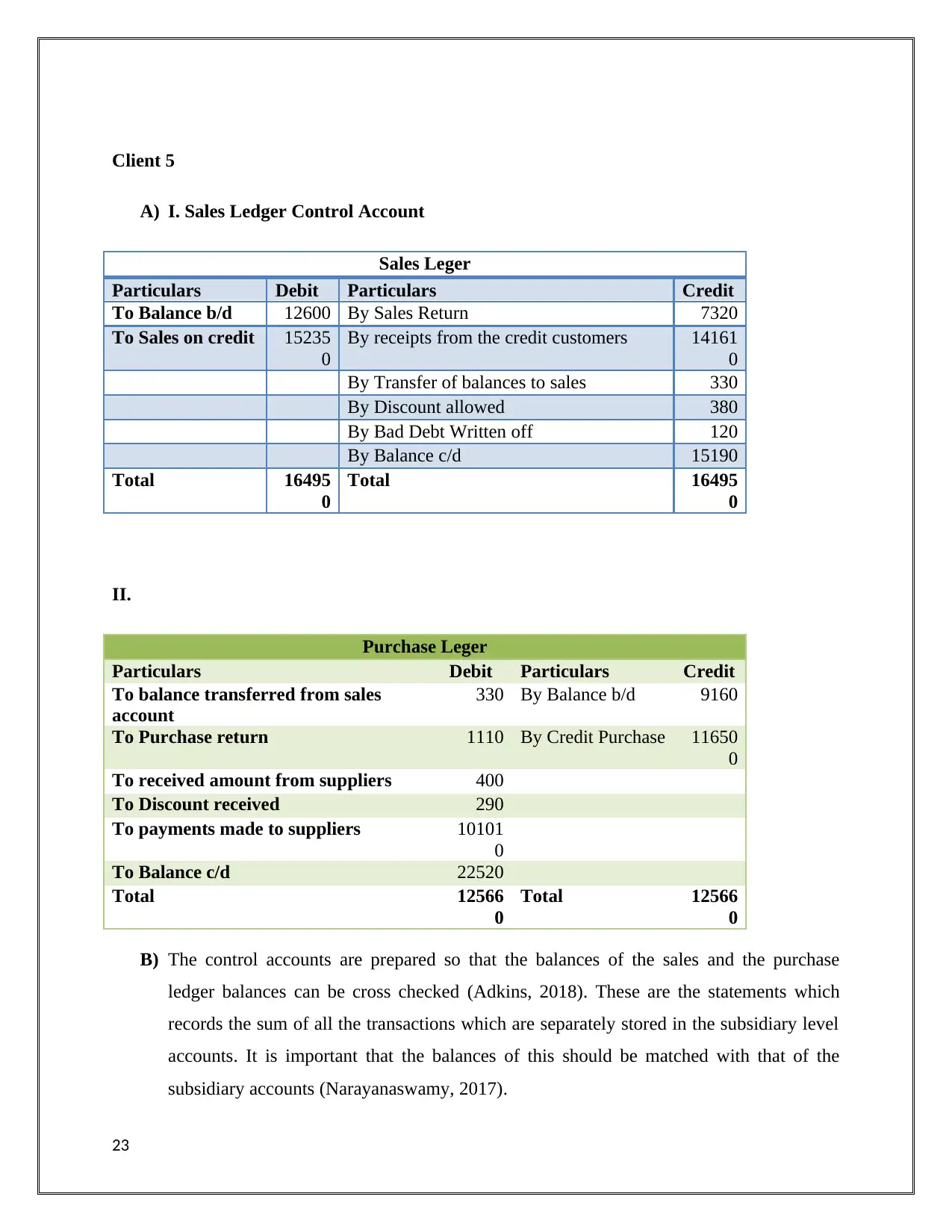

Client 5

A) I. Sales Ledger Control Account

Sales Leger

Particulars Debit Particulars Credit

To Balance b/d 12600 By Sales Return 7320

To Sales on credit 15235

0

By receipts from the credit customers 14161

0

By Transfer of balances to sales 330

By Discount allowed 380

By Bad Debt Written off 120

By Balance c/d 15190

Total 16495

0

Total 16495

0

II.

Purchase Leger

Particulars Debit Particulars Credit

To balance transferred from sales

account

330 By Balance b/d 9160

To Purchase return 1110 By Credit Purchase 11650

0

To received amount from suppliers 400

To Discount received 290

To payments made to suppliers 10101

0

To Balance c/d 22520

Total 12566

0

Total 12566

0

B) The control accounts are prepared so that the balances of the sales and the purchase

ledger balances can be cross checked (Adkins, 2018). These are the statements which

records the sum of all the transactions which are separately stored in the subsidiary level

accounts. It is important that the balances of this should be matched with that of the

subsidiary accounts (Narayanaswamy, 2017).

23

A) I. Sales Ledger Control Account

Sales Leger

Particulars Debit Particulars Credit

To Balance b/d 12600 By Sales Return 7320

To Sales on credit 15235

0

By receipts from the credit customers 14161

0

By Transfer of balances to sales 330

By Discount allowed 380

By Bad Debt Written off 120

By Balance c/d 15190

Total 16495

0

Total 16495

0

II.

Purchase Leger

Particulars Debit Particulars Credit

To balance transferred from sales

account

330 By Balance b/d 9160

To Purchase return 1110 By Credit Purchase 11650

0

To received amount from suppliers 400

To Discount received 290

To payments made to suppliers 10101

0

To Balance c/d 22520

Total 12566

0

Total 12566

0

B) The control accounts are prepared so that the balances of the sales and the purchase

ledger balances can be cross checked (Adkins, 2018). These are the statements which

records the sum of all the transactions which are separately stored in the subsidiary level

accounts. It is important that the balances of this should be matched with that of the

subsidiary accounts (Narayanaswamy, 2017).

23

24

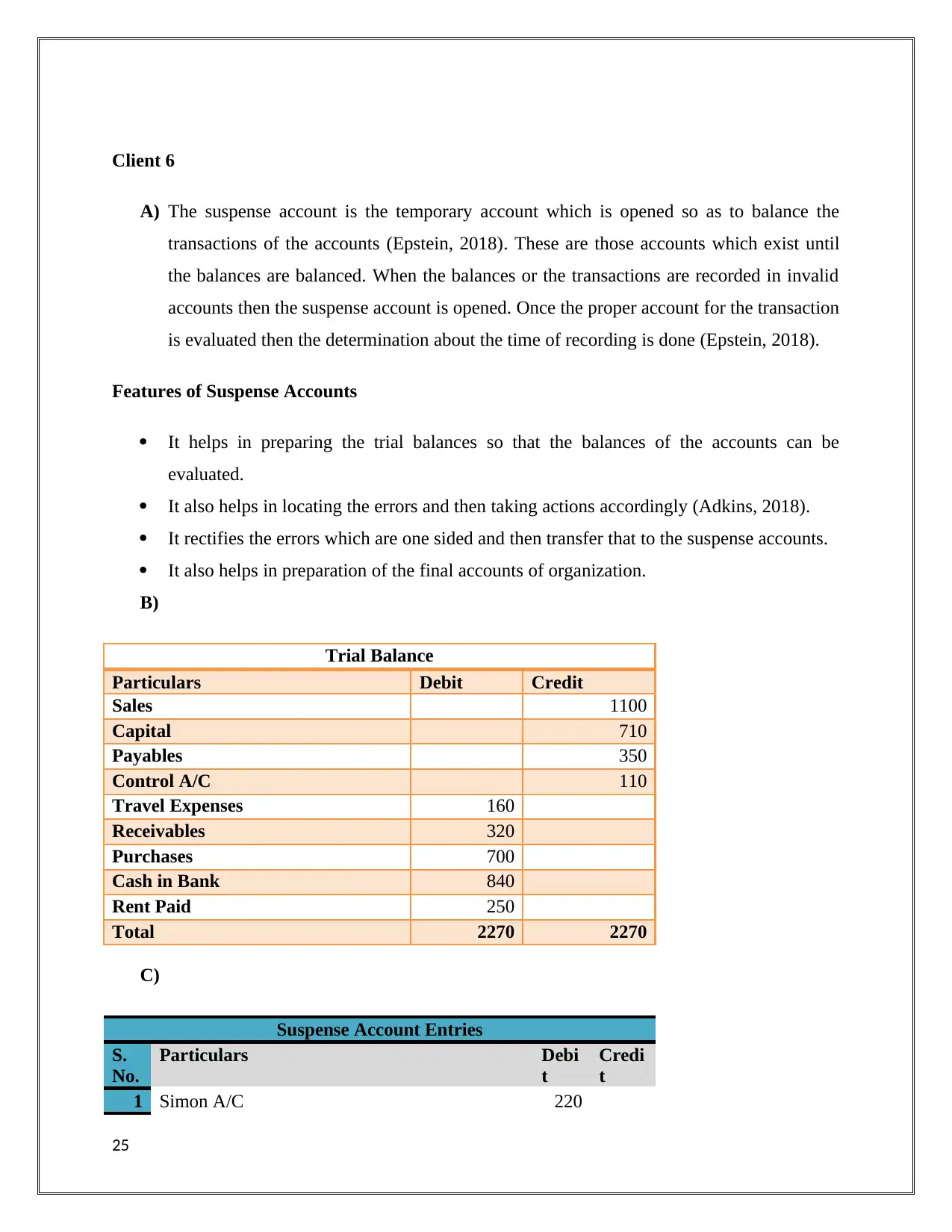

Client 6

A) The suspense account is the temporary account which is opened so as to balance the

transactions of the accounts (Epstein, 2018). These are those accounts which exist until

the balances are balanced. When the balances or the transactions are recorded in invalid

accounts then the suspense account is opened. Once the proper account for the transaction

is evaluated then the determination about the time of recording is done (Epstein, 2018).

Features of Suspense Accounts

It helps in preparing the trial balances so that the balances of the accounts can be

evaluated.

It also helps in locating the errors and then taking actions accordingly (Adkins, 2018).

It rectifies the errors which are one sided and then transfer that to the suspense accounts.

It also helps in preparation of the final accounts of organization.

B)

Trial Balance

Particulars Debit Credit

Sales 1100

Capital 710

Payables 350

Control A/C 110

Travel Expenses 160

Receivables 320

Purchases 700

Cash in Bank 840

Rent Paid 250

Total 2270 2270

C)

Suspense Account Entries

S.

No.

Particulars Debi

t

Credi

t

1 Simon A/C 220

25

A) The suspense account is the temporary account which is opened so as to balance the

transactions of the accounts (Epstein, 2018). These are those accounts which exist until

the balances are balanced. When the balances or the transactions are recorded in invalid

accounts then the suspense account is opened. Once the proper account for the transaction

is evaluated then the determination about the time of recording is done (Epstein, 2018).

Features of Suspense Accounts

It helps in preparing the trial balances so that the balances of the accounts can be

evaluated.

It also helps in locating the errors and then taking actions accordingly (Adkins, 2018).

It rectifies the errors which are one sided and then transfer that to the suspense accounts.

It also helps in preparation of the final accounts of organization.

B)

Trial Balance

Particulars Debit Credit

Sales 1100

Capital 710

Payables 350

Control A/C 110

Travel Expenses 160

Receivables 320

Purchases 700

Cash in Bank 840

Rent Paid 250

Total 2270 2270

C)

Suspense Account Entries

S.

No.

Particulars Debi

t

Credi

t

1 Simon A/C 220

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

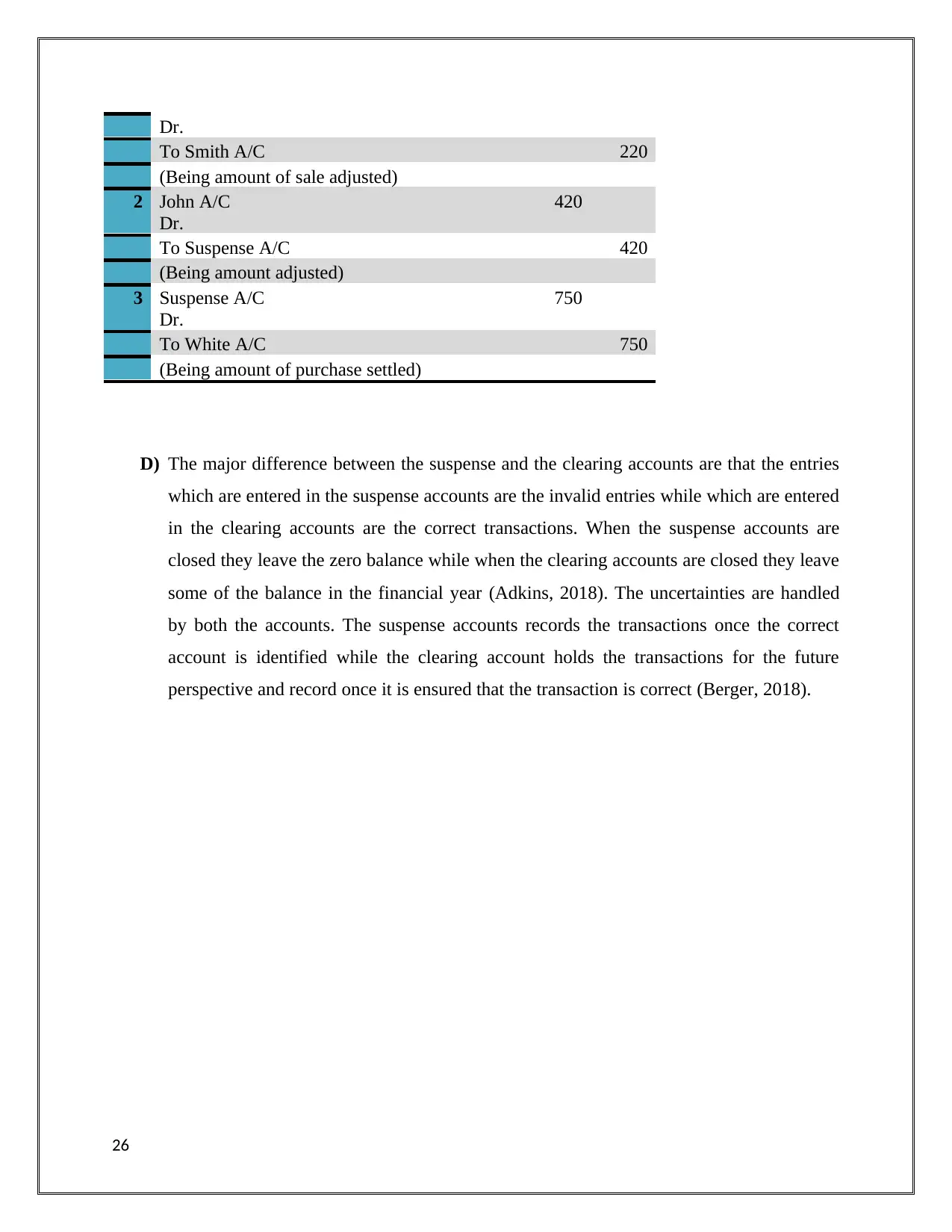

Dr.

To Smith A/C 220

(Being amount of sale adjusted)

2 John A/C

Dr.

420

To Suspense A/C 420

(Being amount adjusted)

3 Suspense A/C

Dr.

750

To White A/C 750

(Being amount of purchase settled)

D) The major difference between the suspense and the clearing accounts are that the entries

which are entered in the suspense accounts are the invalid entries while which are entered

in the clearing accounts are the correct transactions. When the suspense accounts are

closed they leave the zero balance while when the clearing accounts are closed they leave

some of the balance in the financial year (Adkins, 2018). The uncertainties are handled

by both the accounts. The suspense accounts records the transactions once the correct

account is identified while the clearing account holds the transactions for the future

perspective and record once it is ensured that the transaction is correct (Berger, 2018).

26

To Smith A/C 220

(Being amount of sale adjusted)

2 John A/C

Dr.

420

To Suspense A/C 420

(Being amount adjusted)

3 Suspense A/C

Dr.

750

To White A/C 750

(Being amount of purchase settled)

D) The major difference between the suspense and the clearing accounts are that the entries

which are entered in the suspense accounts are the invalid entries while which are entered

in the clearing accounts are the correct transactions. When the suspense accounts are

closed they leave the zero balance while when the clearing accounts are closed they leave

some of the balance in the financial year (Adkins, 2018). The uncertainties are handled

by both the accounts. The suspense accounts records the transactions once the correct

account is identified while the clearing account holds the transactions for the future

perspective and record once it is ensured that the transaction is correct (Berger, 2018).

26

Conclusion

It can be stated from the discussion that the reporting of the transactions is necessary so as to

ensure that the decisions for the long term can be taken accordingly. The journal entries are done

so that the transactions can be journalized and then those transactions are posted in their

respective accounts. The profit & Loss and balance sheet is prepared so that the financial

performance and the position of the organization can be determined. The reasons for the

preparation of the bank reconciliation statement are highlighted with that the factors which lead

to difference are also determined. The suspense account is also prepared to make the corrections

in the entries which are wrongly posted in their accounts so that the correct financial status of the

organization can be evaluated. Besides, this the report also explains the difference between the

clearing and suspense accounts so that the confusion regarding that can be cleared.

27

It can be stated from the discussion that the reporting of the transactions is necessary so as to

ensure that the decisions for the long term can be taken accordingly. The journal entries are done

so that the transactions can be journalized and then those transactions are posted in their

respective accounts. The profit & Loss and balance sheet is prepared so that the financial

performance and the position of the organization can be determined. The reasons for the

preparation of the bank reconciliation statement are highlighted with that the factors which lead

to difference are also determined. The suspense account is also prepared to make the corrections

in the entries which are wrongly posted in their accounts so that the correct financial status of the

organization can be evaluated. Besides, this the report also explains the difference between the

clearing and suspense accounts so that the confusion regarding that can be cleared.

27

Bibliography

Adkins, W. (2018). Retrieved June 12, 2018, from Chron:

http://smallbusiness.chron.com/difference-between-suspense-account-clearing-account-

81560.html

Berger, T. (2018). Ipsas Explained: A Summary of Standards and Principles of

International Public Sector Accounting Standards. John Wiley & Sons .

carrers, N. (2018). Retrieved June 12, 2018, from Ng carrers:

https://ngcareers.com/course/258/financial-accounting

Epstein, L. a. (2018). Optimal Learning under Robustness and Time $ Consistency.

Kwok, B. (2017). Accounting irregularities in financial statements: A definitive guide for

litigators, auditors and fraud investigators. Routledge .

Narayanaswamy, R. (2017). Financial accounting: a managerial perspective. PHI

Learning Pvt. Ltd.

Stockenstrand, A. a. (2017). Bank Regulation: Effects on Strategy, Financial Accounting

and Management Control. Taylor & Francis , 19.

28

Adkins, W. (2018). Retrieved June 12, 2018, from Chron:

http://smallbusiness.chron.com/difference-between-suspense-account-clearing-account-

81560.html

Berger, T. (2018). Ipsas Explained: A Summary of Standards and Principles of

International Public Sector Accounting Standards. John Wiley & Sons .

carrers, N. (2018). Retrieved June 12, 2018, from Ng carrers:

https://ngcareers.com/course/258/financial-accounting

Epstein, L. a. (2018). Optimal Learning under Robustness and Time $ Consistency.

Kwok, B. (2017). Accounting irregularities in financial statements: A definitive guide for

litigators, auditors and fraud investigators. Routledge .

Narayanaswamy, R. (2017). Financial accounting: a managerial perspective. PHI

Learning Pvt. Ltd.

Stockenstrand, A. a. (2017). Bank Regulation: Effects on Strategy, Financial Accounting

and Management Control. Taylor & Francis , 19.

28

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.