Financial Accounting Principles: Client Case Study Report Analysis

VerifiedAdded on 2021/02/21

|19

|3901

|33

Report

AI Summary

This report delves into the core principles of financial accounting, providing a comprehensive overview through practical examples and client case studies. It begins with a definition of financial accounting, its purpose, and the various users of financial statements, including internal and external stakeholders. The report then explores key concepts such as journal entries, ledgers, and trial balances, illustrated with detailed examples from client companies. It covers the preparation of financial statements like the Statement of Profit and Loss and the Statement of Financial Position, along with discussions on accounting principles, depreciation methods, bank reconciliation, and control accounts. The report also includes examples of the Imprest system in petty cash books and suspense accounts, offering a practical understanding of accounting procedures. Overall, the report serves as a valuable resource for understanding financial accounting practices and their application in real-world scenarios.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Financial Accounting:......................................................................................................................1

Financial Accounting:..................................................................................................................1

Purpose:........................................................................................................................................1

Users Of Financial Accounting: ..................................................................................................3

CLIENT 1........................................................................................................................................4

Journal Entries and Ledger in the book of Alexandra Study.......................................................4

Ledgers.........................................................................................................................................4

Trial Balance as at 31st January 2019 in the books of Alexandra Study:....................................9

Trial Balance as at 31st January in the books of Alexandra study............................................10

CLIENT 2......................................................................................................................................11

Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018........11

Statement of Financial Position of Munteanu Ltd. As at 31st December 2018.........................11

Accounting Principles:...............................................................................................................12

Purpose and Methods of Depreciation:......................................................................................12

CLIENT 3......................................................................................................................................13

Bank Reconciliation Statement: ................................................................................................13

Imprest system in petty cash book: ...........................................................................................13

Bank Reconciliation Statement as at 30 September 2018.........................................................14

CLIENT 4......................................................................................................................................14

Control Accounts:......................................................................................................................14

Ledger Control Accounts in the books of Hilly:........................................................................15

CLIENT 5......................................................................................................................................15

Suspense Account: ....................................................................................................................15

Journal Entries:..........................................................................................................................16

Trial balance...............................................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

Financial Accounting:......................................................................................................................1

Financial Accounting:..................................................................................................................1

Purpose:........................................................................................................................................1

Users Of Financial Accounting: ..................................................................................................3

CLIENT 1........................................................................................................................................4

Journal Entries and Ledger in the book of Alexandra Study.......................................................4

Ledgers.........................................................................................................................................4

Trial Balance as at 31st January 2019 in the books of Alexandra Study:....................................9

Trial Balance as at 31st January in the books of Alexandra study............................................10

CLIENT 2......................................................................................................................................11

Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018........11

Statement of Financial Position of Munteanu Ltd. As at 31st December 2018.........................11

Accounting Principles:...............................................................................................................12

Purpose and Methods of Depreciation:......................................................................................12

CLIENT 3......................................................................................................................................13

Bank Reconciliation Statement: ................................................................................................13

Imprest system in petty cash book: ...........................................................................................13

Bank Reconciliation Statement as at 30 September 2018.........................................................14

CLIENT 4......................................................................................................................................14

Control Accounts:......................................................................................................................14

Ledger Control Accounts in the books of Hilly:........................................................................15

CLIENT 5......................................................................................................................................15

Suspense Account: ....................................................................................................................15

Journal Entries:..........................................................................................................................16

Trial balance...............................................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

The process of financial accounting is that collects and compiles financial data to

prepare and describe financial statements and reports such as balance sheet and income

statements for the management, lenders, investors, tax authorities, suppliers and other

stakeholders of the establishment(Abela and et.al, 2014). The overall motive to follow the

process of financial accounting is for generating the fund related statements or information that

can be utilised by external users as well as internal users to make their financial decisions.

For the better understanding of financial accounting and its principles, a junior

accountant of an accounting firm has prepared a report which covers the definition and

explanation of financial accounting, users and purpose of financial accounting, basic principles

of it by the help of some practical accounting statements of client companies.

Financial Accounting:

Financial Accounting:

Financial accounting is the field of accounting that mentions for collecting, recording,

summarizing and presentation of the financial data and information deriving from business

operations and transactions (Financial Accounting 2019). In broader terms, financial

accounting is a manner of reporting financial information and business actions to creditors,

investors and other persons outside the business. It find out the operational profit and the worth

of the business to the concerned individuals. It can be said that financial accounting is used for

presenting financial transactions to the stakeholders in a format that is acceptable and adaptable

by all businesses.

Purpose:

The objectives, functions or purpose of financial accounting can be described as under:

Planning: It is essential for the organizations to plan the structure to allocate and assign

their limited and valuable resources such as cash, materials, labour, equipment and machinery

towards competitive requirements in upcoming period. The utilisation of various types of

budgets may be an effective manner to fulfil the purpose. Financial statements enable

enterprises to develop plans by evaluating business resources and necessities.

Decision: Financial accounting assists the management in making developing policies

and business decisions to create more expeditious process of the establishment . Some

1

The process of financial accounting is that collects and compiles financial data to

prepare and describe financial statements and reports such as balance sheet and income

statements for the management, lenders, investors, tax authorities, suppliers and other

stakeholders of the establishment(Abela and et.al, 2014). The overall motive to follow the

process of financial accounting is for generating the fund related statements or information that

can be utilised by external users as well as internal users to make their financial decisions.

For the better understanding of financial accounting and its principles, a junior

accountant of an accounting firm has prepared a report which covers the definition and

explanation of financial accounting, users and purpose of financial accounting, basic principles

of it by the help of some practical accounting statements of client companies.

Financial Accounting:

Financial Accounting:

Financial accounting is the field of accounting that mentions for collecting, recording,

summarizing and presentation of the financial data and information deriving from business

operations and transactions (Financial Accounting 2019). In broader terms, financial

accounting is a manner of reporting financial information and business actions to creditors,

investors and other persons outside the business. It find out the operational profit and the worth

of the business to the concerned individuals. It can be said that financial accounting is used for

presenting financial transactions to the stakeholders in a format that is acceptable and adaptable

by all businesses.

Purpose:

The objectives, functions or purpose of financial accounting can be described as under:

Planning: It is essential for the organizations to plan the structure to allocate and assign

their limited and valuable resources such as cash, materials, labour, equipment and machinery

towards competitive requirements in upcoming period. The utilisation of various types of

budgets may be an effective manner to fulfil the purpose. Financial statements enable

enterprises to develop plans by evaluating business resources and necessities.

Decision: Financial accounting assists the management in making developing policies

and business decisions to create more expeditious process of the establishment . Some

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

illustrations related to managerial strategies which are supported by accounting data, involve

pricing policies for products and services, financing policies, investment strategies, product

development policies, credit terms for customers, etc.

Performance: Accounting related to finance provides help in deciding well effective

performance of the business by summarizing and analysing the financial content into standard

measurements and quantifiable (Carnegie and O’Connell, 2014). It is crucial for establishments

to manage a trustworthy informant of evaluating their main objectives so that they may

enhance their effectiveness by examining themselves against competitors and against their own

past performance as well.

Position: Financial statements, generated in this process, indicate the financial

perspective of an organization. Financial condition shows the fiscal status of an organization at

that period of time and also defines the condition of capital investment, utilisation of funds,

cumulative profit and loss, business liabilities and debts, liquidity position of the firm and other

material terms.

Control: One of the major prime objectives of a financial accounting method is to

maintain adequate controls in the organizational environment for the protection of limited and

valuable resources. Financial accounting checks that various hazards are reduced and under-

controlled to an satisfactory level across the business (Deegan, 2017). Organizational assets are

sensitive and may be lost because of theft, error, fraud, obsolescence, mismanagement and

damage. Accounting policies of an organization may require administration to make sure the

reliability and reduce the risk of fraud.

Accountability: Financial accounting renders a base for execution analysis of an

organizational entity over a time slot which encourages reliability across various levels of an

establishment. Directors can be hold by the other stakeholder to make responsible for the

efficiency of the entire organization.

Legal: Financial accounting is a lawful demand for the organizations. It is crucial for

the organizations to follow the required law, regulations and legislations to keep an overall

adequate financial record of their operations and to represent their overall outcomes to the

external as well as internal stakeholders of the establishment (Albu, Albu and Alexander,

2014).

2

pricing policies for products and services, financing policies, investment strategies, product

development policies, credit terms for customers, etc.

Performance: Accounting related to finance provides help in deciding well effective

performance of the business by summarizing and analysing the financial content into standard

measurements and quantifiable (Carnegie and O’Connell, 2014). It is crucial for establishments

to manage a trustworthy informant of evaluating their main objectives so that they may

enhance their effectiveness by examining themselves against competitors and against their own

past performance as well.

Position: Financial statements, generated in this process, indicate the financial

perspective of an organization. Financial condition shows the fiscal status of an organization at

that period of time and also defines the condition of capital investment, utilisation of funds,

cumulative profit and loss, business liabilities and debts, liquidity position of the firm and other

material terms.

Control: One of the major prime objectives of a financial accounting method is to

maintain adequate controls in the organizational environment for the protection of limited and

valuable resources. Financial accounting checks that various hazards are reduced and under-

controlled to an satisfactory level across the business (Deegan, 2017). Organizational assets are

sensitive and may be lost because of theft, error, fraud, obsolescence, mismanagement and

damage. Accounting policies of an organization may require administration to make sure the

reliability and reduce the risk of fraud.

Accountability: Financial accounting renders a base for execution analysis of an

organizational entity over a time slot which encourages reliability across various levels of an

establishment. Directors can be hold by the other stakeholder to make responsible for the

efficiency of the entire organization.

Legal: Financial accounting is a lawful demand for the organizations. It is crucial for

the organizations to follow the required law, regulations and legislations to keep an overall

adequate financial record of their operations and to represent their overall outcomes to the

external as well as internal stakeholders of the establishment (Albu, Albu and Alexander,

2014).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

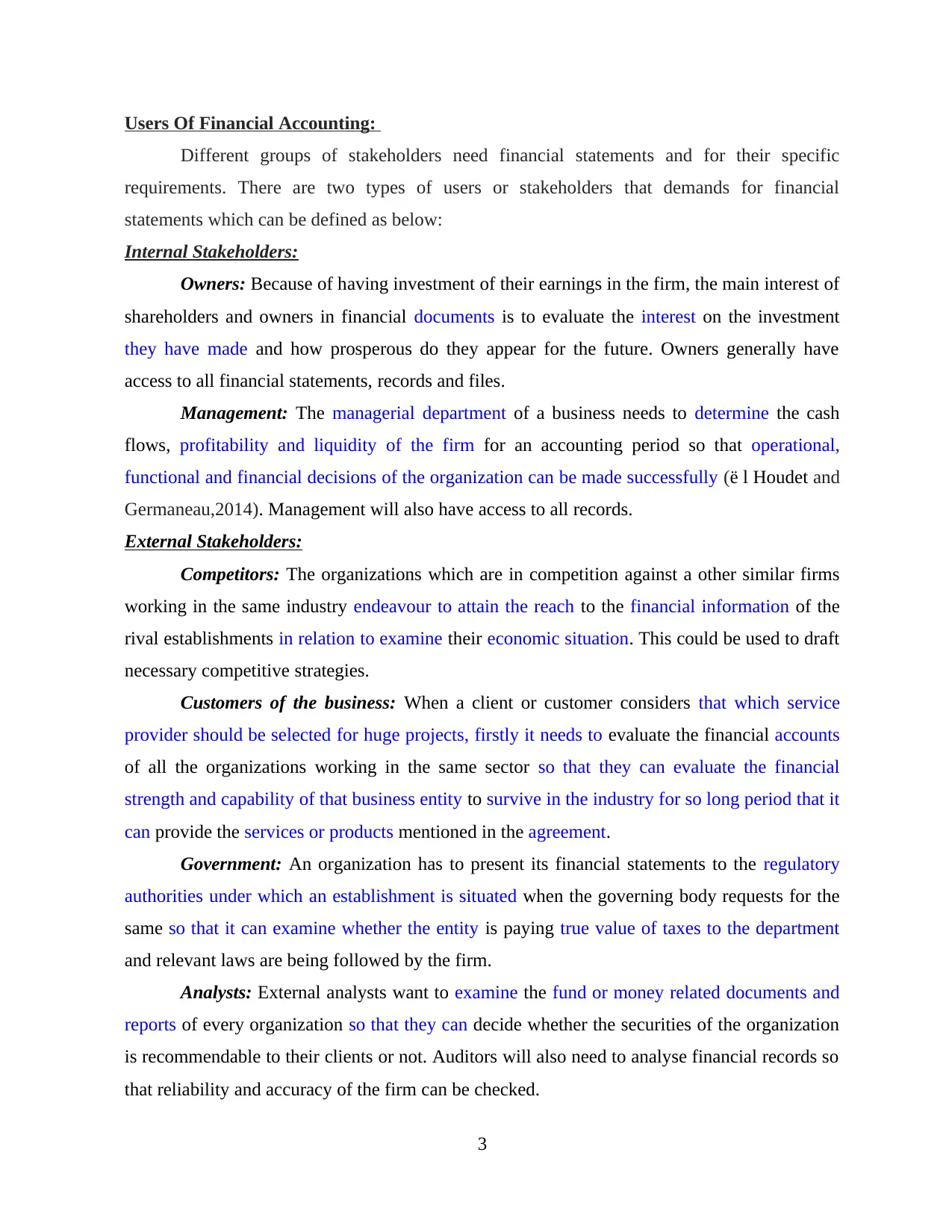

Users Of Financial Accounting:

Different groups of stakeholders need financial statements and for their specific

requirements. There are two types of users or stakeholders that demands for financial

statements which can be defined as below:

Internal Stakeholders:

Owners: Because of having investment of their earnings in the firm, the main interest of

shareholders and owners in financial documents is to evaluate the interest on the investment

they have made and how prosperous do they appear for the future. Owners generally have

access to all financial statements, records and files.

Management: The managerial department of a business needs to determine the cash

flows, profitability and liquidity of the firm for an accounting period so that operational,

functional and financial decisions of the organization can be made successfully (ë l Houdet and

Germaneau,2014). Management will also have access to all records.

External Stakeholders:

Competitors: The organizations which are in competition against a other similar firms

working in the same industry endeavour to attain the reach to the financial information of the

rival establishments in relation to examine their economic situation. This could be used to draft

necessary competitive strategies.

Customers of the business: When a client or customer considers that which service

provider should be selected for huge projects, firstly it needs to evaluate the financial accounts

of all the organizations working in the same sector so that they can evaluate the financial

strength and capability of that business entity to survive in the industry for so long period that it

can provide the services or products mentioned in the agreement.

Government: An organization has to present its financial statements to the regulatory

authorities under which an establishment is situated when the governing body requests for the

same so that it can examine whether the entity is paying true value of taxes to the department

and relevant laws are being followed by the firm.

Analysts: External analysts want to examine the fund or money related documents and

reports of every organization so that they can decide whether the securities of the organization

is recommendable to their clients or not. Auditors will also need to analyse financial records so

that reliability and accuracy of the firm can be checked.

3

Different groups of stakeholders need financial statements and for their specific

requirements. There are two types of users or stakeholders that demands for financial

statements which can be defined as below:

Internal Stakeholders:

Owners: Because of having investment of their earnings in the firm, the main interest of

shareholders and owners in financial documents is to evaluate the interest on the investment

they have made and how prosperous do they appear for the future. Owners generally have

access to all financial statements, records and files.

Management: The managerial department of a business needs to determine the cash

flows, profitability and liquidity of the firm for an accounting period so that operational,

functional and financial decisions of the organization can be made successfully (ë l Houdet and

Germaneau,2014). Management will also have access to all records.

External Stakeholders:

Competitors: The organizations which are in competition against a other similar firms

working in the same industry endeavour to attain the reach to the financial information of the

rival establishments in relation to examine their economic situation. This could be used to draft

necessary competitive strategies.

Customers of the business: When a client or customer considers that which service

provider should be selected for huge projects, firstly it needs to evaluate the financial accounts

of all the organizations working in the same sector so that they can evaluate the financial

strength and capability of that business entity to survive in the industry for so long period that it

can provide the services or products mentioned in the agreement.

Government: An organization has to present its financial statements to the regulatory

authorities under which an establishment is situated when the governing body requests for the

same so that it can examine whether the entity is paying true value of taxes to the department

and relevant laws are being followed by the firm.

Analysts: External analysts want to examine the fund or money related documents and

reports of every organization so that they can decide whether the securities of the organization

is recommendable to their clients or not. Auditors will also need to analyse financial records so

that reliability and accuracy of the firm can be checked.

3

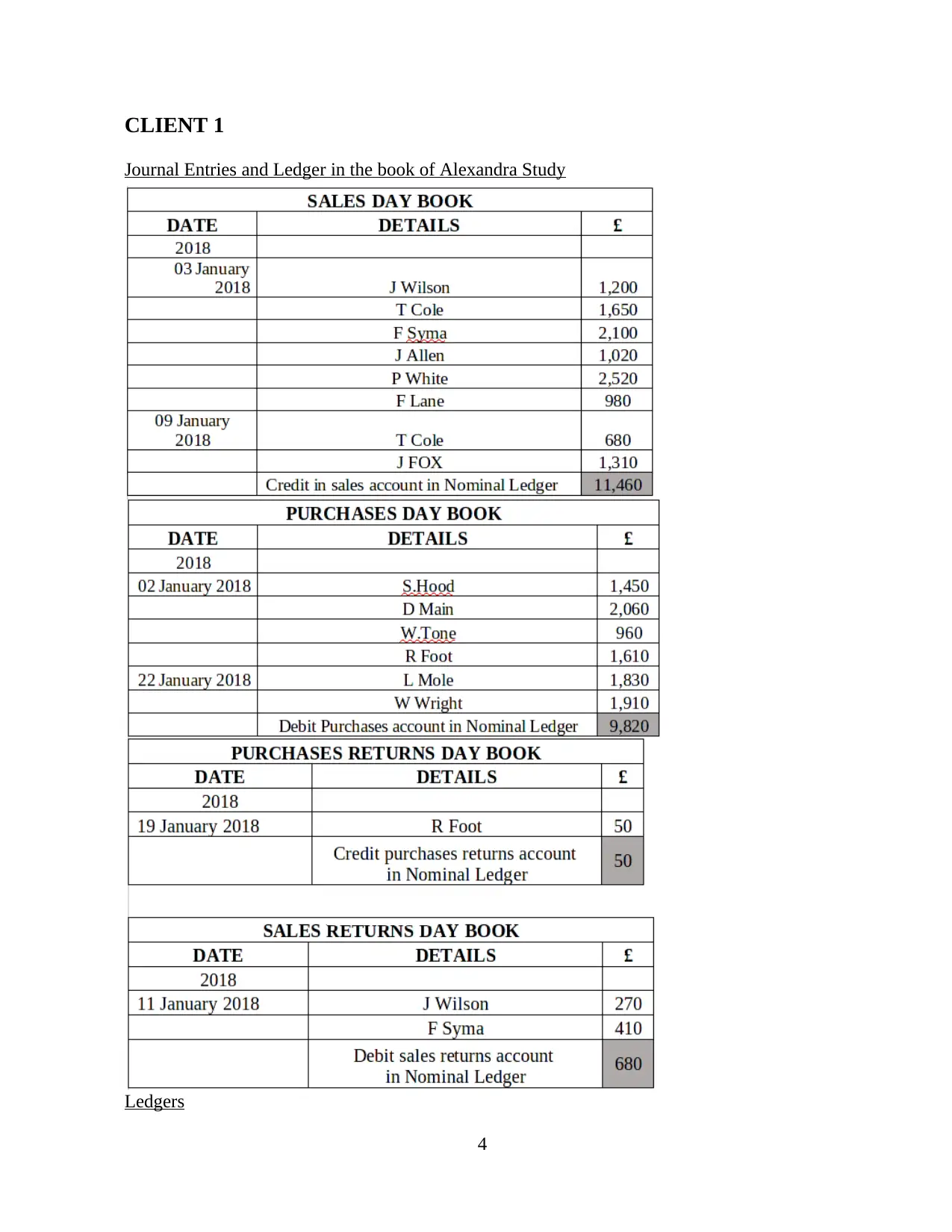

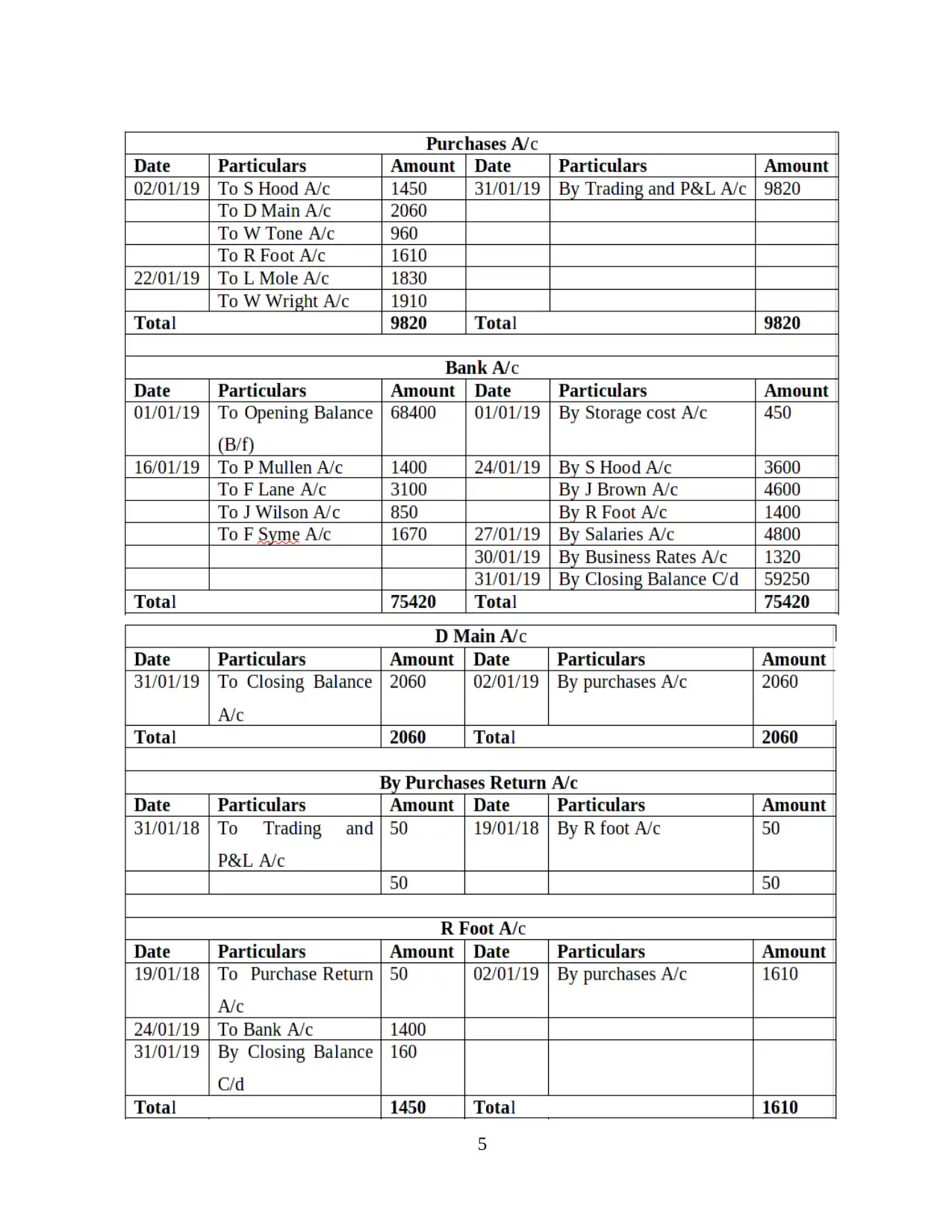

CLIENT 1

Journal Entries and Ledger in the book of Alexandra Study

Ledgers

4

Journal Entries and Ledger in the book of Alexandra Study

Ledgers

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

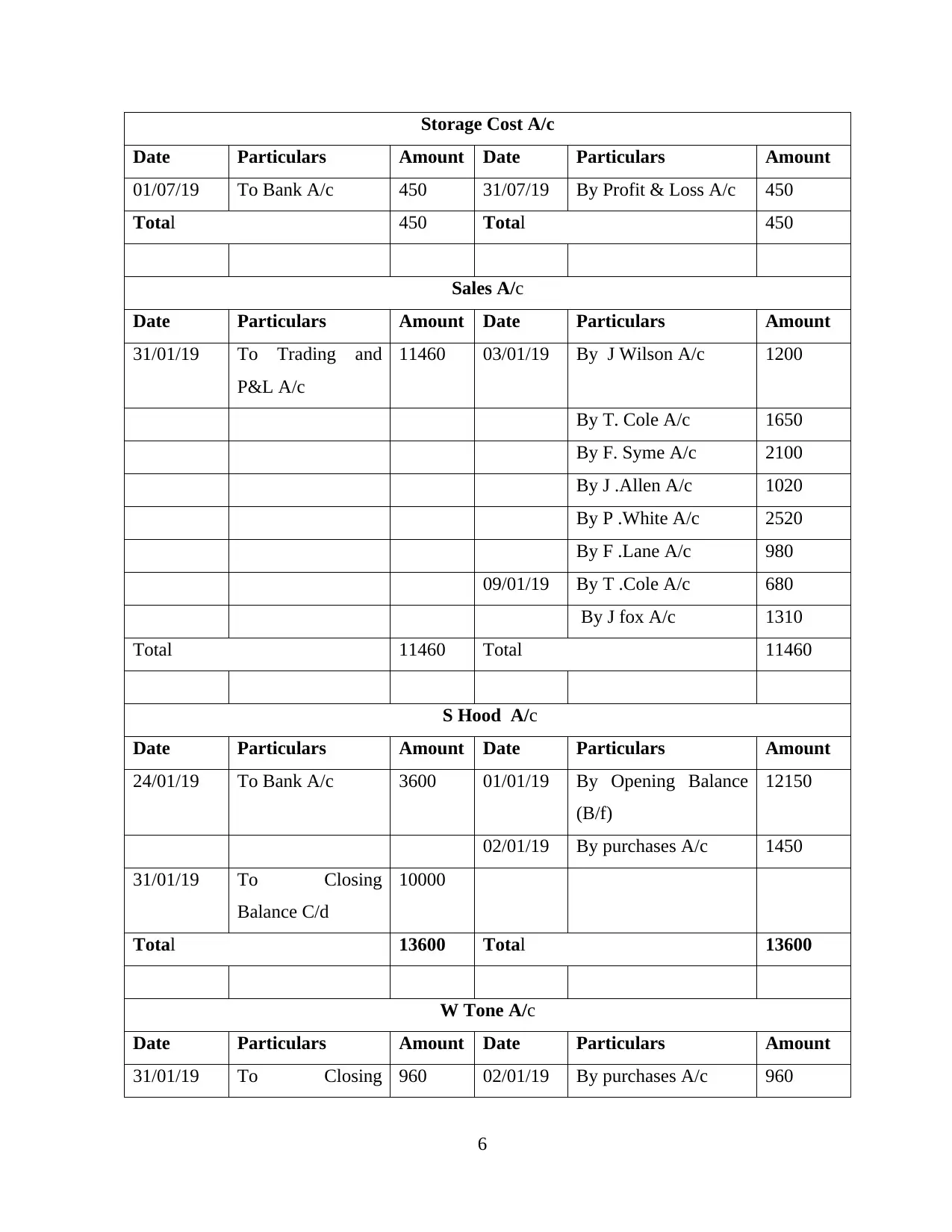

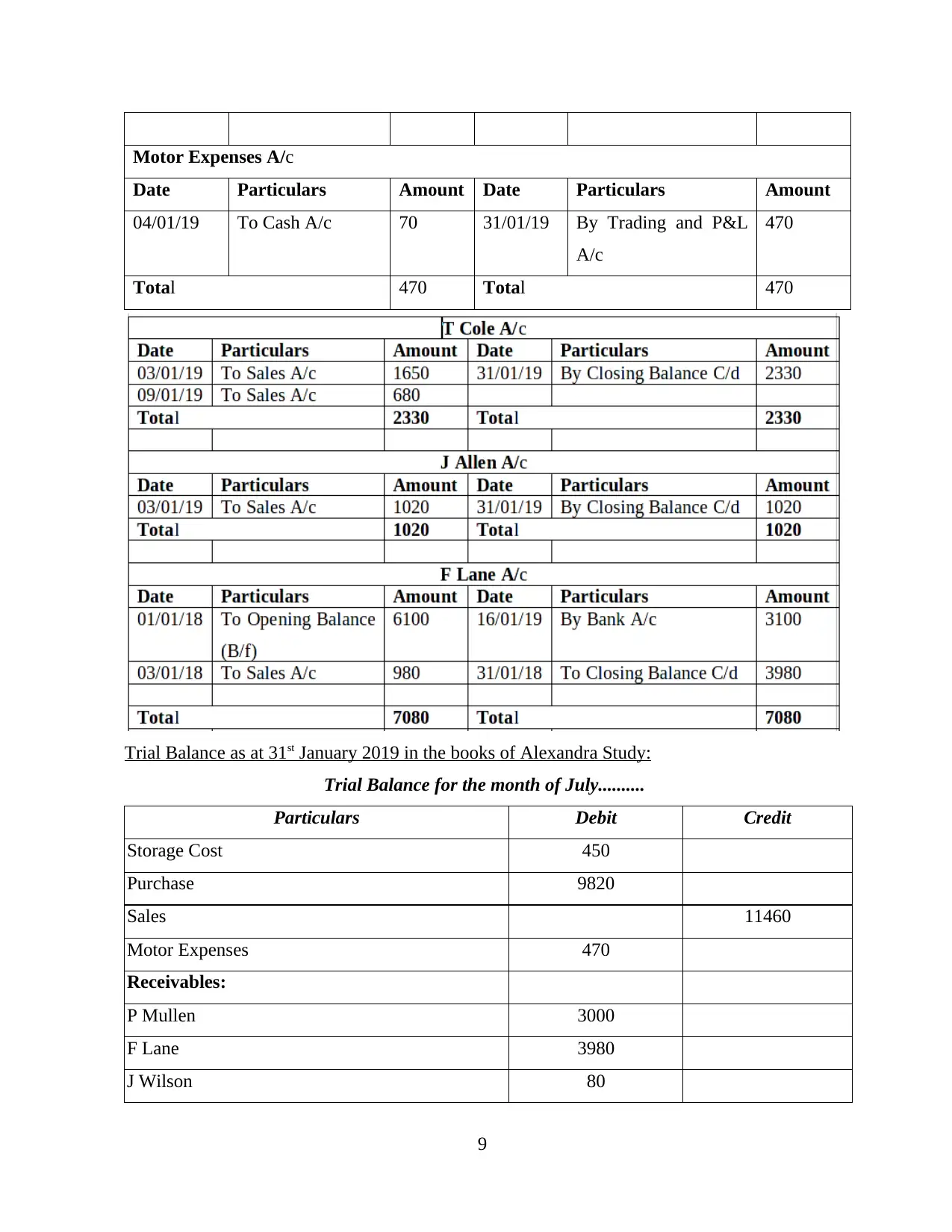

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/19 To Bank A/c 450 31/07/19 By Profit & Loss A/c 450

Total 450 Total 450

Sales A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Trading and

P&L A/c

11460 03/01/19 By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/19 By T .Cole A/c 680

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/19 To Bank A/c 3600 01/01/19 By Opening Balance

(B/f)

12150

02/01/19 By purchases A/c 1450

31/01/19 To Closing

Balance C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing 960 02/01/19 By purchases A/c 960

6

Date Particulars Amount Date Particulars Amount

01/07/19 To Bank A/c 450 31/07/19 By Profit & Loss A/c 450

Total 450 Total 450

Sales A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Trading and

P&L A/c

11460 03/01/19 By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/19 By T .Cole A/c 680

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/19 To Bank A/c 3600 01/01/19 By Opening Balance

(B/f)

12150

02/01/19 By purchases A/c 1450

31/01/19 To Closing

Balance C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing 960 02/01/19 By purchases A/c 960

6

Balance C/d

Total 960 Total 960

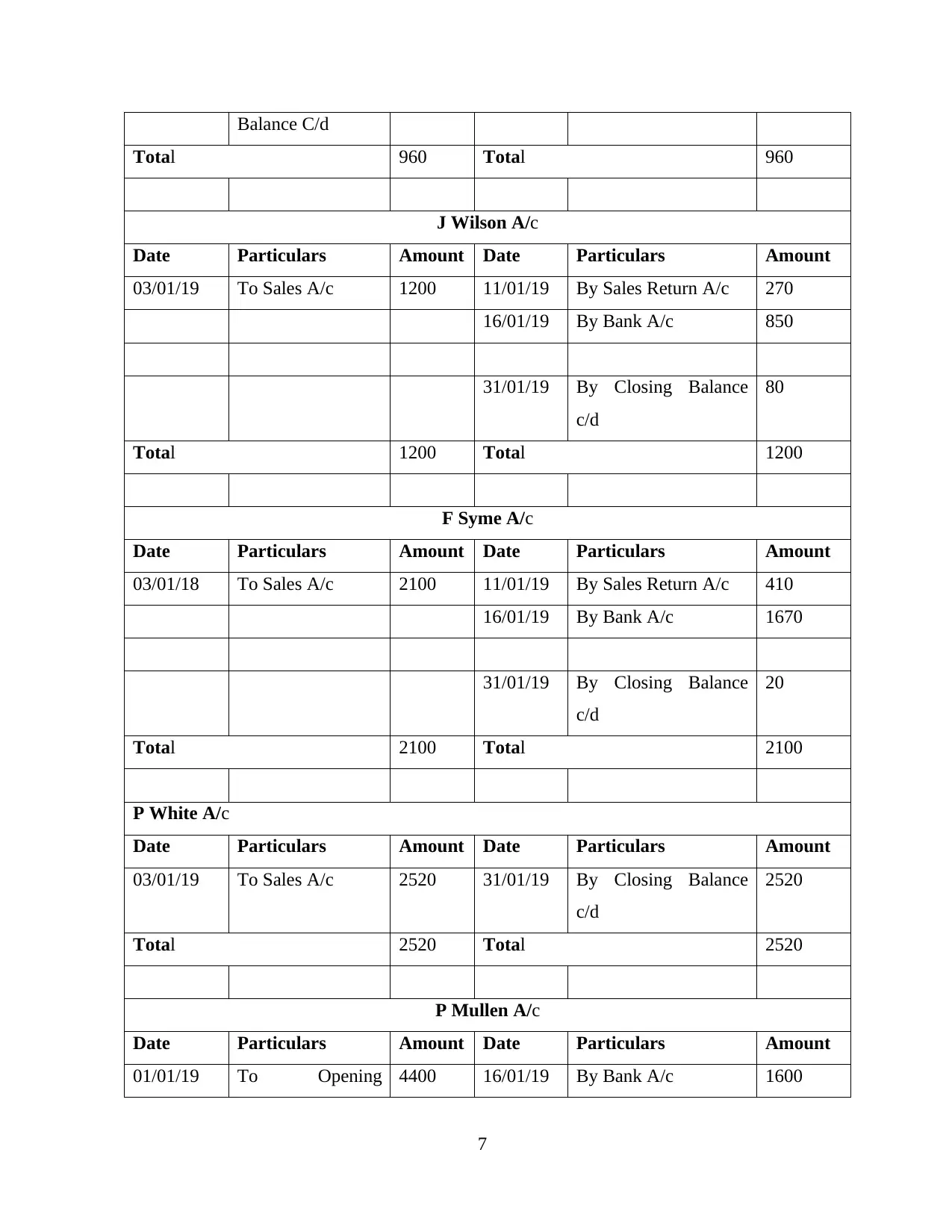

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1200 11/01/19 By Sales Return A/c 270

16/01/19 By Bank A/c 850

31/01/19 By Closing Balance

c/d

80

Total 1200 Total 1200

F Syme A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2100 11/01/19 By Sales Return A/c 410

16/01/19 By Bank A/c 1670

31/01/19 By Closing Balance

c/d

20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 2520 31/01/19 By Closing Balance

c/d

2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening 4400 16/01/19 By Bank A/c 1600

7

Total 960 Total 960

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1200 11/01/19 By Sales Return A/c 270

16/01/19 By Bank A/c 850

31/01/19 By Closing Balance

c/d

80

Total 1200 Total 1200

F Syme A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2100 11/01/19 By Sales Return A/c 410

16/01/19 By Bank A/c 1670

31/01/19 By Closing Balance

c/d

20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 2520 31/01/19 By Closing Balance

c/d

2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening 4400 16/01/19 By Bank A/c 1600

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

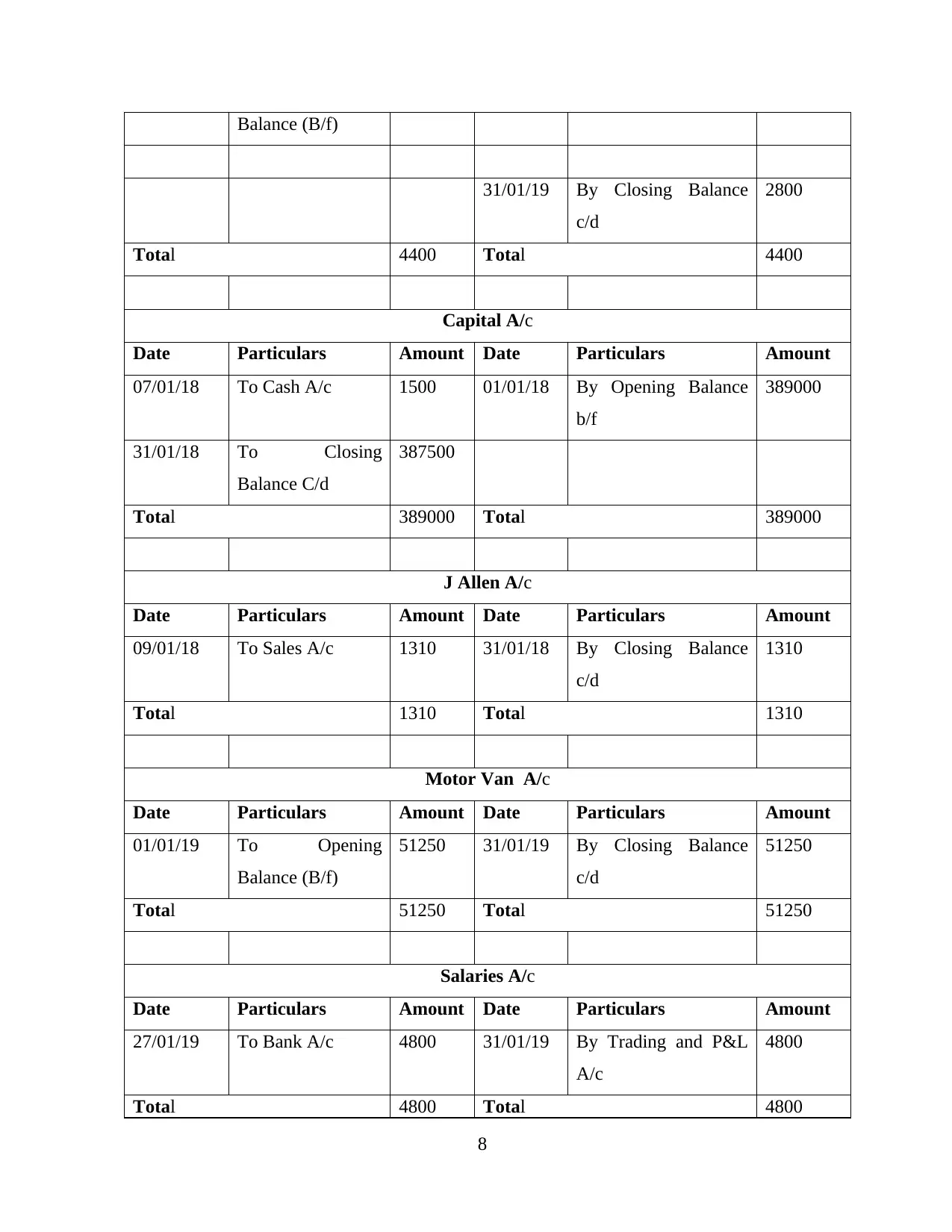

Balance (B/f)

31/01/19 By Closing Balance

c/d

2800

Total 4400 Total 4400

Capital A/c

Date Particulars Amount Date Particulars Amount

07/01/18 To Cash A/c 1500 01/01/18 By Opening Balance

b/f

389000

31/01/18 To Closing

Balance C/d

387500

Total 389000 Total 389000

J Allen A/c

Date Particulars Amount Date Particulars Amount

09/01/18 To Sales A/c 1310 31/01/18 By Closing Balance

c/d

1310

Total 1310 Total 1310

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

51250 31/01/19 By Closing Balance

c/d

51250

Total 51250 Total 51250

Salaries A/c

Date Particulars Amount Date Particulars Amount

27/01/19 To Bank A/c 4800 31/01/19 By Trading and P&L

A/c

4800

Total 4800 Total 4800

8

31/01/19 By Closing Balance

c/d

2800

Total 4400 Total 4400

Capital A/c

Date Particulars Amount Date Particulars Amount

07/01/18 To Cash A/c 1500 01/01/18 By Opening Balance

b/f

389000

31/01/18 To Closing

Balance C/d

387500

Total 389000 Total 389000

J Allen A/c

Date Particulars Amount Date Particulars Amount

09/01/18 To Sales A/c 1310 31/01/18 By Closing Balance

c/d

1310

Total 1310 Total 1310

Motor Van A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

51250 31/01/19 By Closing Balance

c/d

51250

Total 51250 Total 51250

Salaries A/c

Date Particulars Amount Date Particulars Amount

27/01/19 To Bank A/c 4800 31/01/19 By Trading and P&L

A/c

4800

Total 4800 Total 4800

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Motor Expenses A/c

Date Particulars Amount Date Particulars Amount

04/01/19 To Cash A/c 70 31/01/19 By Trading and P&L

A/c

470

Total 470 Total 470

Trial Balance as at 31st January 2019 in the books of Alexandra Study:

Trial Balance for the month of July..........

Particulars Debit Credit

Storage Cost 450

Purchase 9820

Sales 11460

Motor Expenses 470

Receivables:

P Mullen 3000

F Lane 3980

J Wilson 80

9

Date Particulars Amount Date Particulars Amount

04/01/19 To Cash A/c 70 31/01/19 By Trading and P&L

A/c

470

Total 470 Total 470

Trial Balance as at 31st January 2019 in the books of Alexandra Study:

Trial Balance for the month of July..........

Particulars Debit Credit

Storage Cost 450

Purchase 9820

Sales 11460

Motor Expenses 470

Receivables:

P Mullen 3000

F Lane 3980

J Wilson 80

9

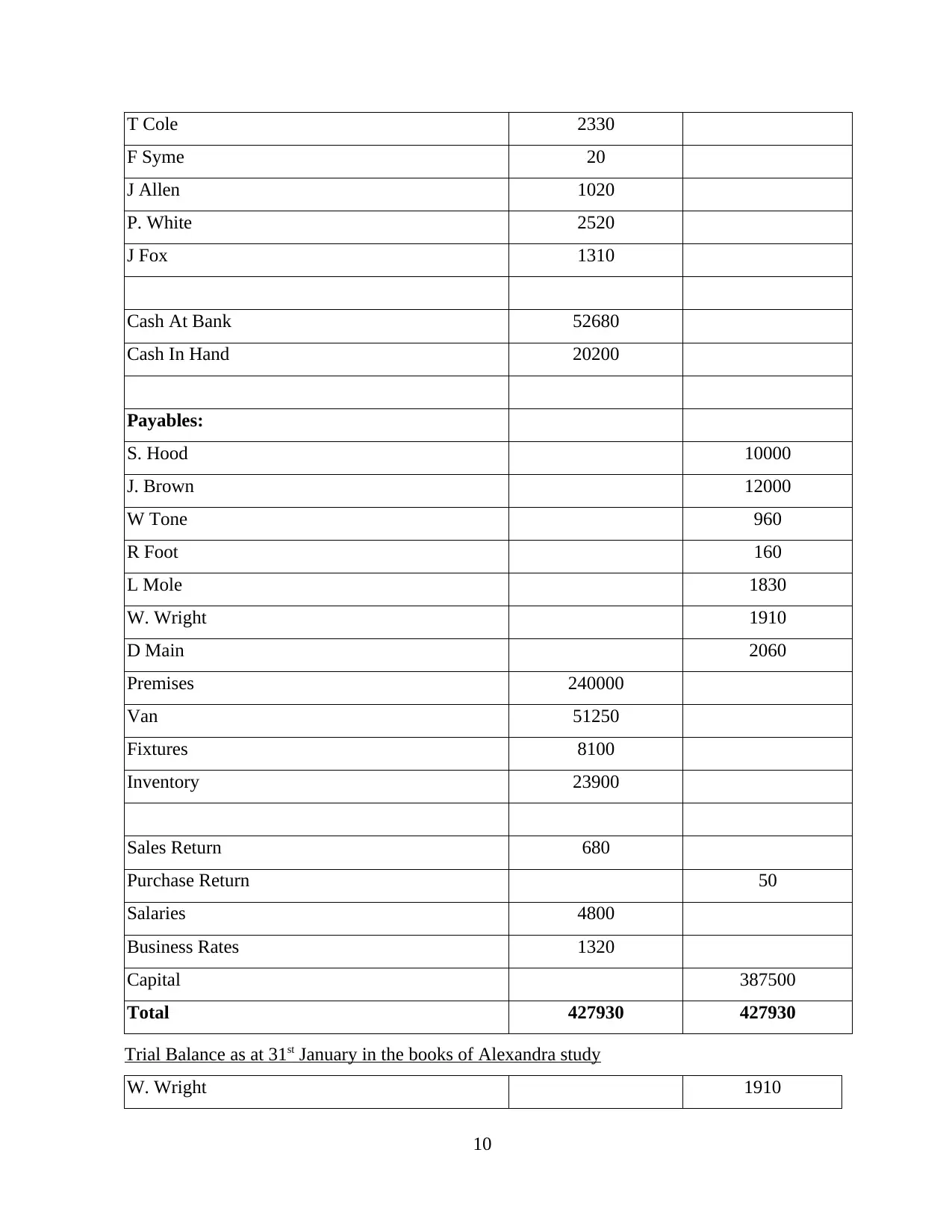

T Cole 2330

F Syme 20

J Allen 1020

P. White 2520

J Fox 1310

Cash At Bank 52680

Cash In Hand 20200

Payables:

S. Hood 10000

J. Brown 12000

W Tone 960

R Foot 160

L Mole 1830

W. Wright 1910

D Main 2060

Premises 240000

Van 51250

Fixtures 8100

Inventory 23900

Sales Return 680

Purchase Return 50

Salaries 4800

Business Rates 1320

Capital 387500

Total 427930 427930

Trial Balance as at 31st January in the books of Alexandra study

W. Wright 1910

10

F Syme 20

J Allen 1020

P. White 2520

J Fox 1310

Cash At Bank 52680

Cash In Hand 20200

Payables:

S. Hood 10000

J. Brown 12000

W Tone 960

R Foot 160

L Mole 1830

W. Wright 1910

D Main 2060

Premises 240000

Van 51250

Fixtures 8100

Inventory 23900

Sales Return 680

Purchase Return 50

Salaries 4800

Business Rates 1320

Capital 387500

Total 427930 427930

Trial Balance as at 31st January in the books of Alexandra study

W. Wright 1910

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.