Financial Investment Analysis: Appraisal Methods and Risk Assessment

VerifiedAdded on 2023/01/09

|16

|3840

|25

Homework Assignment

AI Summary

This assignment delves into the principles of financial investments, offering a detailed analysis of project appraisal techniques and risk assessment methodologies. The solution begins with a comprehensive calculation of the payback period, net present value (NPV), and internal rate of return (IRR) for a new project, evaluating its financial viability. It explores the reasons for setting a lower payback period and discusses the strengths and weaknesses of various investment techniques. Furthermore, the assignment examines the components of expected return on risky assets within the Capital Asset Pricing Model (CAPM), including risk-free rate, market risk premium, and beta. It includes calculations of expected return using CAPM, standard deviation, and beta measures. The analysis also covers the factors influencing dividend growth, features of ordinary equity and preference shares, and the determination of stock prices under different scenarios, including the impact of required returns. This assignment, available on Desklib, provides a thorough understanding of financial investment principles and practical application of investment appraisal techniques.

PRINCIPLES OF FINANCIAL

INVESTMENTS

INVESTMENTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

a) Calculation of the payback period for new project..................................................................1

b) NPV for the new project..........................................................................................................1

c) IRR of the new project.............................................................................................................2

d) Financial acceptability of the proposed investment based over the three appraisal method

used..............................................................................................................................................4

e) Reasons for setting lower payback period by the company of three years..............................5

f) Strengths and weaknesses of investment techniques...............................................................5

QUESTION 4..................................................................................................................................6

a) Expected return on risk assets depend over three components...............................................6

b) Standard deviation and beta measures.....................................................................................7

c) Calculation of expected return using CAPM...........................................................................8

d) Calculation of risk and return..................................................................................................9

QUESTION 5................................................................................................................................10

a) Reasons why firm is hesitant in reducing the growth rate of the dividend...........................10

b) i) Ordinary equity and its features. ii) Preference shares and its features.............................11

c) Price willing to pay for stock.................................................................................................12

d) Price of the stock with required return of 9.6%....................................................................12

e) Required rate of return with share price of €79.4 per share,.................................................12

REFERENCES..............................................................................................................................14

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

a) Calculation of the payback period for new project..................................................................1

b) NPV for the new project..........................................................................................................1

c) IRR of the new project.............................................................................................................2

d) Financial acceptability of the proposed investment based over the three appraisal method

used..............................................................................................................................................4

e) Reasons for setting lower payback period by the company of three years..............................5

f) Strengths and weaknesses of investment techniques...............................................................5

QUESTION 4..................................................................................................................................6

a) Expected return on risk assets depend over three components...............................................6

b) Standard deviation and beta measures.....................................................................................7

c) Calculation of expected return using CAPM...........................................................................8

d) Calculation of risk and return..................................................................................................9

QUESTION 5................................................................................................................................10

a) Reasons why firm is hesitant in reducing the growth rate of the dividend...........................10

b) i) Ordinary equity and its features. ii) Preference shares and its features.............................11

c) Price willing to pay for stock.................................................................................................12

d) Price of the stock with required return of 9.6%....................................................................12

e) Required rate of return with share price of €79.4 per share,.................................................12

REFERENCES..............................................................................................................................14

QUESTION 1

a) Calculation of the payback period for new project.

Cost 210000

Terminal value 45000

Calculation of the cash

flows

Year 1 Year 2 Year 3 Year 4 Year 5

Sales 80000 96000 115200 92160 46080

Maintenance cost 20000 22000 24200 26620 29282

Net Cash Flows 60000 74000 91000 65540 16798

Computation of Payback period

Year

Cash

inflows

Cumulative cash

inflows

1 60000 60000

2 74000 134000

3 91000 225000

4 65540 290540

5 61798 352338

Initial

investment 210000

Payback

period 3

-0.2

Payback

period

2 years and 9.5

months

b) NPV for the new project

Computation of NPV

Year

Cash

inflows

PV factor

@ 15%

Discounted

cash inflows

1 60000 0.870 52173.913

2 74000 0.756 55955

3 91000 0.658 59834

4 65540 0.572 37473

1

a) Calculation of the payback period for new project.

Cost 210000

Terminal value 45000

Calculation of the cash

flows

Year 1 Year 2 Year 3 Year 4 Year 5

Sales 80000 96000 115200 92160 46080

Maintenance cost 20000 22000 24200 26620 29282

Net Cash Flows 60000 74000 91000 65540 16798

Computation of Payback period

Year

Cash

inflows

Cumulative cash

inflows

1 60000 60000

2 74000 134000

3 91000 225000

4 65540 290540

5 61798 352338

Initial

investment 210000

Payback

period 3

-0.2

Payback

period

2 years and 9.5

months

b) NPV for the new project

Computation of NPV

Year

Cash

inflows

PV factor

@ 15%

Discounted

cash inflows

1 60000 0.870 52173.913

2 74000 0.756 55955

3 91000 0.658 59834

4 65540 0.572 37473

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

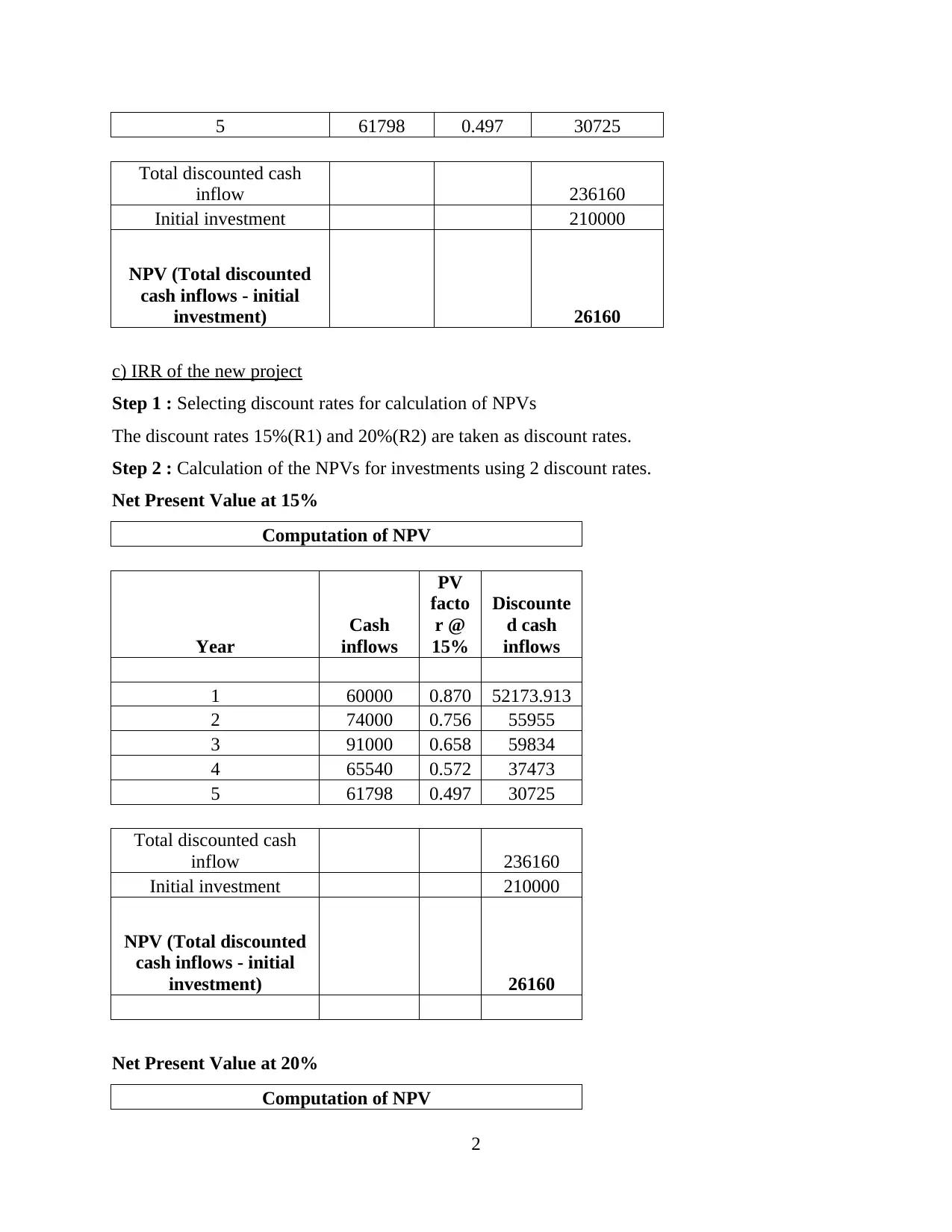

5 61798 0.497 30725

Total discounted cash

inflow 236160

Initial investment 210000

NPV (Total discounted

cash inflows - initial

investment) 26160

c) IRR of the new project

Step 1 : Selecting discount rates for calculation of NPVs

The discount rates 15%(R1) and 20%(R2) are taken as discount rates.

Step 2 : Calculation of the NPVs for investments using 2 discount rates.

Net Present Value at 15%

Computation of NPV

Year

Cash

inflows

PV

facto

r @

15%

Discounte

d cash

inflows

1 60000 0.870 52173.913

2 74000 0.756 55955

3 91000 0.658 59834

4 65540 0.572 37473

5 61798 0.497 30725

Total discounted cash

inflow 236160

Initial investment 210000

NPV (Total discounted

cash inflows - initial

investment) 26160

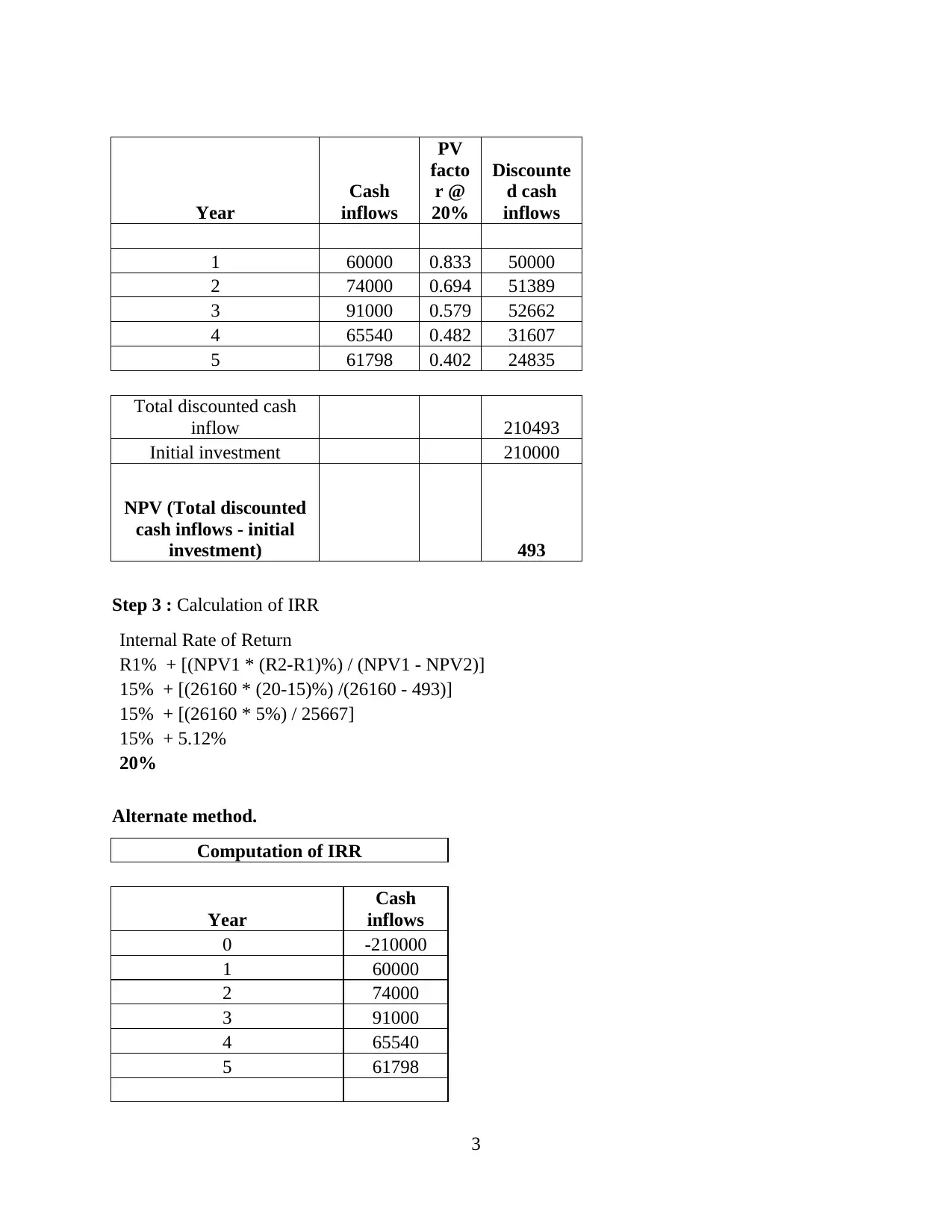

Net Present Value at 20%

Computation of NPV

2

Total discounted cash

inflow 236160

Initial investment 210000

NPV (Total discounted

cash inflows - initial

investment) 26160

c) IRR of the new project

Step 1 : Selecting discount rates for calculation of NPVs

The discount rates 15%(R1) and 20%(R2) are taken as discount rates.

Step 2 : Calculation of the NPVs for investments using 2 discount rates.

Net Present Value at 15%

Computation of NPV

Year

Cash

inflows

PV

facto

r @

15%

Discounte

d cash

inflows

1 60000 0.870 52173.913

2 74000 0.756 55955

3 91000 0.658 59834

4 65540 0.572 37473

5 61798 0.497 30725

Total discounted cash

inflow 236160

Initial investment 210000

NPV (Total discounted

cash inflows - initial

investment) 26160

Net Present Value at 20%

Computation of NPV

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year

Cash

inflows

PV

facto

r @

20%

Discounte

d cash

inflows

1 60000 0.833 50000

2 74000 0.694 51389

3 91000 0.579 52662

4 65540 0.482 31607

5 61798 0.402 24835

Total discounted cash

inflow 210493

Initial investment 210000

NPV (Total discounted

cash inflows - initial

investment) 493

Step 3 : Calculation of IRR

Internal Rate of Return

R1% + [(NPV1 * (R2-R1)%) / (NPV1 - NPV2)]

15% + [(26160 * (20-15)%) /(26160 - 493)]

15% + [(26160 * 5%) / 25667]

15% + 5.12%

20%

Alternate method.

Computation of IRR

Year

Cash

inflows

0 -210000

1 60000

2 74000

3 91000

4 65540

5 61798

3

Cash

inflows

PV

facto

r @

20%

Discounte

d cash

inflows

1 60000 0.833 50000

2 74000 0.694 51389

3 91000 0.579 52662

4 65540 0.482 31607

5 61798 0.402 24835

Total discounted cash

inflow 210493

Initial investment 210000

NPV (Total discounted

cash inflows - initial

investment) 493

Step 3 : Calculation of IRR

Internal Rate of Return

R1% + [(NPV1 * (R2-R1)%) / (NPV1 - NPV2)]

15% + [(26160 * (20-15)%) /(26160 - 493)]

15% + [(26160 * 5%) / 25667]

15% + 5.12%

20%

Alternate method.

Computation of IRR

Year

Cash

inflows

0 -210000

1 60000

2 74000

3 91000

4 65540

5 61798

3

Internal rate of return

(IRR) 20%

d) Financial acceptability of the proposed investment based over the three appraisal method used.

Company is proposing to make investment in the new business having initial outlay of

£210,000. Machine will be having annual cost of 20000 which will be growing 10% every year.

This is the only cost associated with the project. The project is estimated to have useful life of 5

years. The viability of the project is assessed using investment appraisal techniques. It enables

the management to make more effective decisions regarding the projects or investment and to

make the choice from different options.

Payback Period

It is also used by the management and investors to identify the profitability of the project

or investment that company is planning to adopt. The technique requires the project to have

adequate payback period so that company can earn profits over investments. The technique is

used for assessing the time period within which the proposed investment will be covering the

cost of initial investment. It could be evaluated that company will be covering the cost of

investments in 2 years and 9.5 months where the total estimated life of the investment is 5 years.

The payback period is adequate but not shorter. It will be earning profits after covering the cost.

As per the outcomes it could be evaluated that project is viable and should be adopted.

Net Present Value

The method is used for measuring the profitability of the project. Applying this technique

over the investment appraisal it could be evaluated that the net present value of the project is

26160. As per this technique project is considered profitable if the NPV is positive and also it is

of adequate amount. The method considers discounting rate to identify whether the future cash

flows will be enough or not for covering the cost of investment or project. The technique shows

that NPV is adequate and positive from which it could be evaluated that the project is profitable

and company should adopt the proposed investment. Company can also compare it with other

investment options and choose the one which is having higher NPV at similar costing. As per the

approach investment is viable and should be adopted.

IRR

4

(IRR) 20%

d) Financial acceptability of the proposed investment based over the three appraisal method used.

Company is proposing to make investment in the new business having initial outlay of

£210,000. Machine will be having annual cost of 20000 which will be growing 10% every year.

This is the only cost associated with the project. The project is estimated to have useful life of 5

years. The viability of the project is assessed using investment appraisal techniques. It enables

the management to make more effective decisions regarding the projects or investment and to

make the choice from different options.

Payback Period

It is also used by the management and investors to identify the profitability of the project

or investment that company is planning to adopt. The technique requires the project to have

adequate payback period so that company can earn profits over investments. The technique is

used for assessing the time period within which the proposed investment will be covering the

cost of initial investment. It could be evaluated that company will be covering the cost of

investments in 2 years and 9.5 months where the total estimated life of the investment is 5 years.

The payback period is adequate but not shorter. It will be earning profits after covering the cost.

As per the outcomes it could be evaluated that project is viable and should be adopted.

Net Present Value

The method is used for measuring the profitability of the project. Applying this technique

over the investment appraisal it could be evaluated that the net present value of the project is

26160. As per this technique project is considered profitable if the NPV is positive and also it is

of adequate amount. The method considers discounting rate to identify whether the future cash

flows will be enough or not for covering the cost of investment or project. The technique shows

that NPV is adequate and positive from which it could be evaluated that the project is profitable

and company should adopt the proposed investment. Company can also compare it with other

investment options and choose the one which is having higher NPV at similar costing. As per the

approach investment is viable and should be adopted.

IRR

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is known as internal rate of return of the project that states the return that will be

generated. It could be analysed that IRR of the above investment project is 20%. Project having

IRR above 7% are considered adequate. The project is having high IRR and it should be adopted.

e) Reasons for setting lower payback period by the company of three years

Payback period is an investment appraisal technique used by the management for knowing

the time within which it will be covering the costs of investment. The technique requires the

project to have adequate payback period so that company can earn profits over investments.

Company has set benchmark of 3 years as the life of project is 5 years. Payback period is kept

shorter as it is the point after which it starts earning profits. If project is having payback higher

than 3 years it will not earn adequate profits for company. it is also known as the break even

point which is beneficial if lower. If project only covers the cost of project it is not profitable for

company to make investments over such projects. The lower payback period will allow company

to earn sufficient profits after covering cost of project. In the present case payback period is 2

years and 9 months which is lower than the benchmark of 3 years which states the project is

profitable and should be adopted by company.

f) Strengths and weaknesses of investment techniques

i) Payback Period

It is an investment appraisal technique enables the management to identify the

profitability of the project. The method states project is considered profitable if the NPV is

positive and high.

Strengths

It is simple and easy method used for calculating viability of project.

It identifies the time taken by investment to cover the cost.

The technique is highly beneficial for identifying the profitability of the proposed

investments.

It allows investors to identify whether future cash flows are adequate for covering the

cost of investment.

Weaknesses

The method does not consider other factors influencing cash flows.

The investment technique does not consider time value of money which makes it less

reliable and accurate as compared with other technique.

5

generated. It could be analysed that IRR of the above investment project is 20%. Project having

IRR above 7% are considered adequate. The project is having high IRR and it should be adopted.

e) Reasons for setting lower payback period by the company of three years

Payback period is an investment appraisal technique used by the management for knowing

the time within which it will be covering the costs of investment. The technique requires the

project to have adequate payback period so that company can earn profits over investments.

Company has set benchmark of 3 years as the life of project is 5 years. Payback period is kept

shorter as it is the point after which it starts earning profits. If project is having payback higher

than 3 years it will not earn adequate profits for company. it is also known as the break even

point which is beneficial if lower. If project only covers the cost of project it is not profitable for

company to make investments over such projects. The lower payback period will allow company

to earn sufficient profits after covering cost of project. In the present case payback period is 2

years and 9 months which is lower than the benchmark of 3 years which states the project is

profitable and should be adopted by company.

f) Strengths and weaknesses of investment techniques

i) Payback Period

It is an investment appraisal technique enables the management to identify the

profitability of the project. The method states project is considered profitable if the NPV is

positive and high.

Strengths

It is simple and easy method used for calculating viability of project.

It identifies the time taken by investment to cover the cost.

The technique is highly beneficial for identifying the profitability of the proposed

investments.

It allows investors to identify whether future cash flows are adequate for covering the

cost of investment.

Weaknesses

The method does not consider other factors influencing cash flows.

The investment technique does not consider time value of money which makes it less

reliable and accurate as compared with other technique.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ii) Accounting Rate of Return

It the expected rate of return over projects or investments in comparison with initial cost

of investment which is determined in percentage terms.

Strengths

The method is based over the accounting profits that do not require other special reports

to determine ARR.

The method does not involve complex calculations which make it simple and easy to

understand.

Management could identify whether the return generated by the investment is adequate or

not.

Weaknesses

This investment technique does not account for time value of money in calculation.

It does not consider cash flows generated after the investment period.

iii) Internal Rate of Return

It is an annual growth rate of the investment which is expected to be generated over investments.

Strengths

The method calculates return rate using time value of money.

The method is highly beneficial in comparing the return rates of different projects.

It allows company to make informed decisions about the projects.

Weaknesses

Size of the investment is not considered while comparing investments.

It is not beneficial for long term projects with changing discount rates.

QUESTION 4

a) Expected return on risk assets depend over three components

In capital asset pricing model return over the risky assets is dependent over three

components. The components are essential for determining the expected return of the security.

These components are risk free rate of return, market risk premium and beta of the stock.

Risk free rate: It is described as risk free rate or the interest rate that investor could get over the

investment that carries zero amount of risk. Risk free rate are generally considered equivalent to

the government bonds or treasury bonds. If the investor does not wants to take risks it will invest

6

It the expected rate of return over projects or investments in comparison with initial cost

of investment which is determined in percentage terms.

Strengths

The method is based over the accounting profits that do not require other special reports

to determine ARR.

The method does not involve complex calculations which make it simple and easy to

understand.

Management could identify whether the return generated by the investment is adequate or

not.

Weaknesses

This investment technique does not account for time value of money in calculation.

It does not consider cash flows generated after the investment period.

iii) Internal Rate of Return

It is an annual growth rate of the investment which is expected to be generated over investments.

Strengths

The method calculates return rate using time value of money.

The method is highly beneficial in comparing the return rates of different projects.

It allows company to make informed decisions about the projects.

Weaknesses

Size of the investment is not considered while comparing investments.

It is not beneficial for long term projects with changing discount rates.

QUESTION 4

a) Expected return on risk assets depend over three components

In capital asset pricing model return over the risky assets is dependent over three

components. The components are essential for determining the expected return of the security.

These components are risk free rate of return, market risk premium and beta of the stock.

Risk free rate: It is described as risk free rate or the interest rate that investor could get over the

investment that carries zero amount of risk. Risk free rate are generally considered equivalent to

the government bonds or treasury bonds. If the investor does not wants to take risks it will invest

6

at risk free rate where return will be received whatsoever may be the circumstances of the

project. It is used in CAPM for determining relationship between expected return and risk.

Market Risk Premium: Market risk premium in CAPM is difference between expected return

over market portfolio and risk free return. Market risk premium in capm is equal to slope of

security market line. It is used for measuring excess return that is demanded by the investors for

bearing greater risks of overall market as compared with risk free rate of return. It is mainly

concerned with determining relationship between the risks and rewards. In CAPM market risk

premium is multiplied with the beta of asset. it is not possible to determine expected return

without market risk premium as it will not be able to calculate the premium it should get for

taking the risk.

Beta: It is the most important component in CAPM for determining the expected return of asset.

It is measure of systematic risk or volatility of the portfolio or security as compared with market

as whole. Beta 1 implies that volatility of the asset is equal to market, beta higher than 1 is

considered more volatile where less than 1 implies less volatility. If beta of asset is higher than 1

investor is bearing increased risk as compared to market, for risk premium associated with asset

tends to be greater than overall market risk premium.

All the three components of the CAPM works in conjunction with one another for

measuring risk & return of assets to give formula in CAPM which is Er =Rf + (Rm-Rf)*Beta

b) Standard deviation and beta measures

i) What does a stock’s standard deviation measures?

The standard deviation is statistical measure of the market volatility which measures how

wide the prices of stock are dispersed from average prices. If the prices of stocks are trading in

narrower trading range, standard deviation will show lower value which implies lower volatility.

If the prices of stock swing up & down wildly then the standard deviation return high value

which indicates higher volatility. Standard deviation of stocks rise as the prices becomes more

volatile. If the prices are moving with increased S.D. it shows strengths & weakness above

average.

ii) What does a stock’s beta measures?

Beta is the numeric value which measures fluctuations of the stocks to changes in

occurring overall stock markets. The beta measures responsiveness of changes in stock prices in

7

project. It is used in CAPM for determining relationship between expected return and risk.

Market Risk Premium: Market risk premium in CAPM is difference between expected return

over market portfolio and risk free return. Market risk premium in capm is equal to slope of

security market line. It is used for measuring excess return that is demanded by the investors for

bearing greater risks of overall market as compared with risk free rate of return. It is mainly

concerned with determining relationship between the risks and rewards. In CAPM market risk

premium is multiplied with the beta of asset. it is not possible to determine expected return

without market risk premium as it will not be able to calculate the premium it should get for

taking the risk.

Beta: It is the most important component in CAPM for determining the expected return of asset.

It is measure of systematic risk or volatility of the portfolio or security as compared with market

as whole. Beta 1 implies that volatility of the asset is equal to market, beta higher than 1 is

considered more volatile where less than 1 implies less volatility. If beta of asset is higher than 1

investor is bearing increased risk as compared to market, for risk premium associated with asset

tends to be greater than overall market risk premium.

All the three components of the CAPM works in conjunction with one another for

measuring risk & return of assets to give formula in CAPM which is Er =Rf + (Rm-Rf)*Beta

b) Standard deviation and beta measures

i) What does a stock’s standard deviation measures?

The standard deviation is statistical measure of the market volatility which measures how

wide the prices of stock are dispersed from average prices. If the prices of stocks are trading in

narrower trading range, standard deviation will show lower value which implies lower volatility.

If the prices of stock swing up & down wildly then the standard deviation return high value

which indicates higher volatility. Standard deviation of stocks rise as the prices becomes more

volatile. If the prices are moving with increased S.D. it shows strengths & weakness above

average.

ii) What does a stock’s beta measures?

Beta is the numeric value which measures fluctuations of the stocks to changes in

occurring overall stock markets. The beta measures responsiveness of changes in stock prices in

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

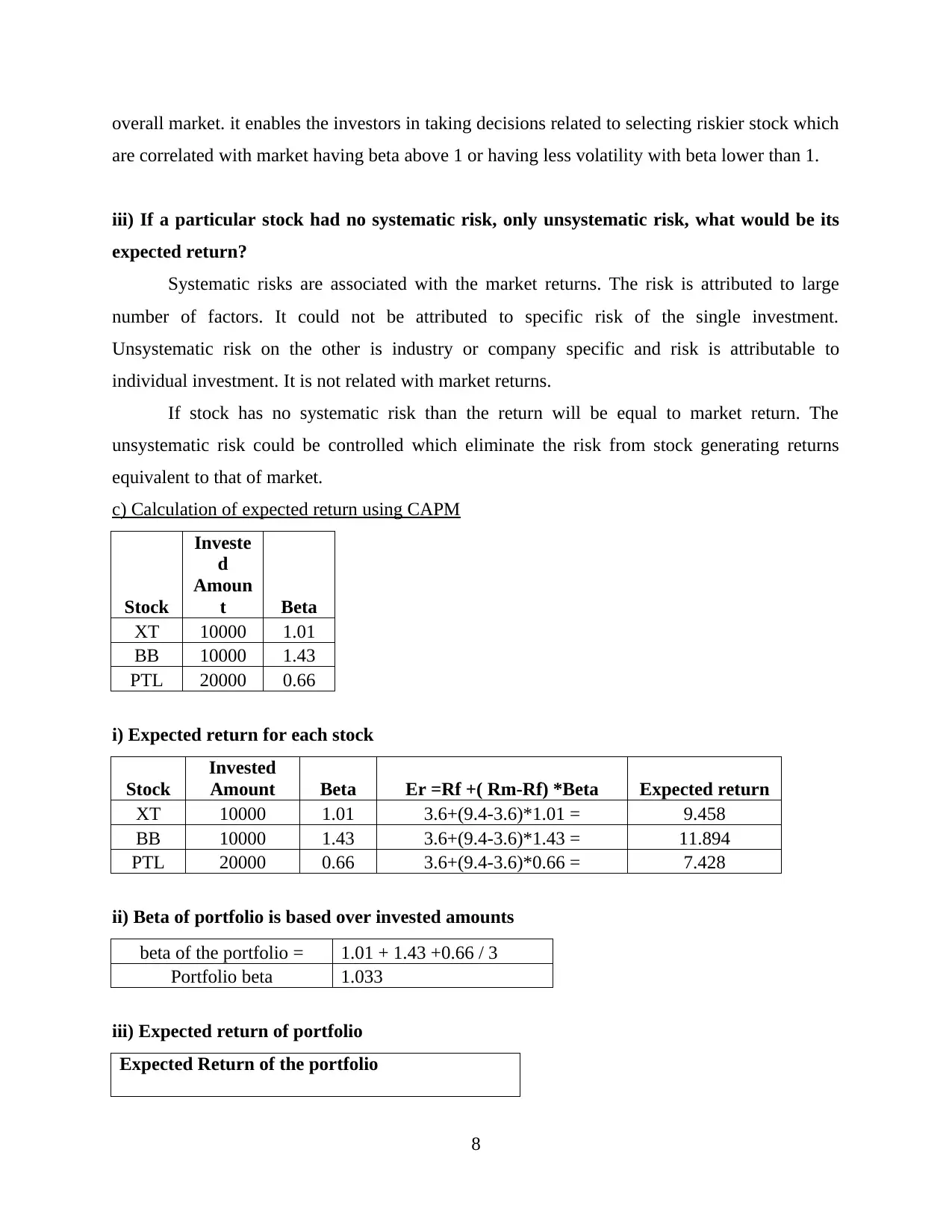

overall market. it enables the investors in taking decisions related to selecting riskier stock which

are correlated with market having beta above 1 or having less volatility with beta lower than 1.

iii) If a particular stock had no systematic risk, only unsystematic risk, what would be its

expected return?

Systematic risks are associated with the market returns. The risk is attributed to large

number of factors. It could not be attributed to specific risk of the single investment.

Unsystematic risk on the other is industry or company specific and risk is attributable to

individual investment. It is not related with market returns.

If stock has no systematic risk than the return will be equal to market return. The

unsystematic risk could be controlled which eliminate the risk from stock generating returns

equivalent to that of market.

c) Calculation of expected return using CAPM

Stock

Investe

d

Amoun

t Beta

XT 10000 1.01

BB 10000 1.43

PTL 20000 0.66

i) Expected return for each stock

Stock

Invested

Amount Beta Er =Rf +( Rm-Rf) *Beta Expected return

XT 10000 1.01 3.6+(9.4-3.6)*1.01 = 9.458

BB 10000 1.43 3.6+(9.4-3.6)*1.43 = 11.894

PTL 20000 0.66 3.6+(9.4-3.6)*0.66 = 7.428

ii) Beta of portfolio is based over invested amounts

beta of the portfolio = 1.01 + 1.43 +0.66 / 3

Portfolio beta 1.033

iii) Expected return of portfolio

Expected Return of the portfolio

8

are correlated with market having beta above 1 or having less volatility with beta lower than 1.

iii) If a particular stock had no systematic risk, only unsystematic risk, what would be its

expected return?

Systematic risks are associated with the market returns. The risk is attributed to large

number of factors. It could not be attributed to specific risk of the single investment.

Unsystematic risk on the other is industry or company specific and risk is attributable to

individual investment. It is not related with market returns.

If stock has no systematic risk than the return will be equal to market return. The

unsystematic risk could be controlled which eliminate the risk from stock generating returns

equivalent to that of market.

c) Calculation of expected return using CAPM

Stock

Investe

d

Amoun

t Beta

XT 10000 1.01

BB 10000 1.43

PTL 20000 0.66

i) Expected return for each stock

Stock

Invested

Amount Beta Er =Rf +( Rm-Rf) *Beta Expected return

XT 10000 1.01 3.6+(9.4-3.6)*1.01 = 9.458

BB 10000 1.43 3.6+(9.4-3.6)*1.43 = 11.894

PTL 20000 0.66 3.6+(9.4-3.6)*0.66 = 7.428

ii) Beta of portfolio is based over invested amounts

beta of the portfolio = 1.01 + 1.43 +0.66 / 3

Portfolio beta 1.033

iii) Expected return of portfolio

Expected Return of the portfolio

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

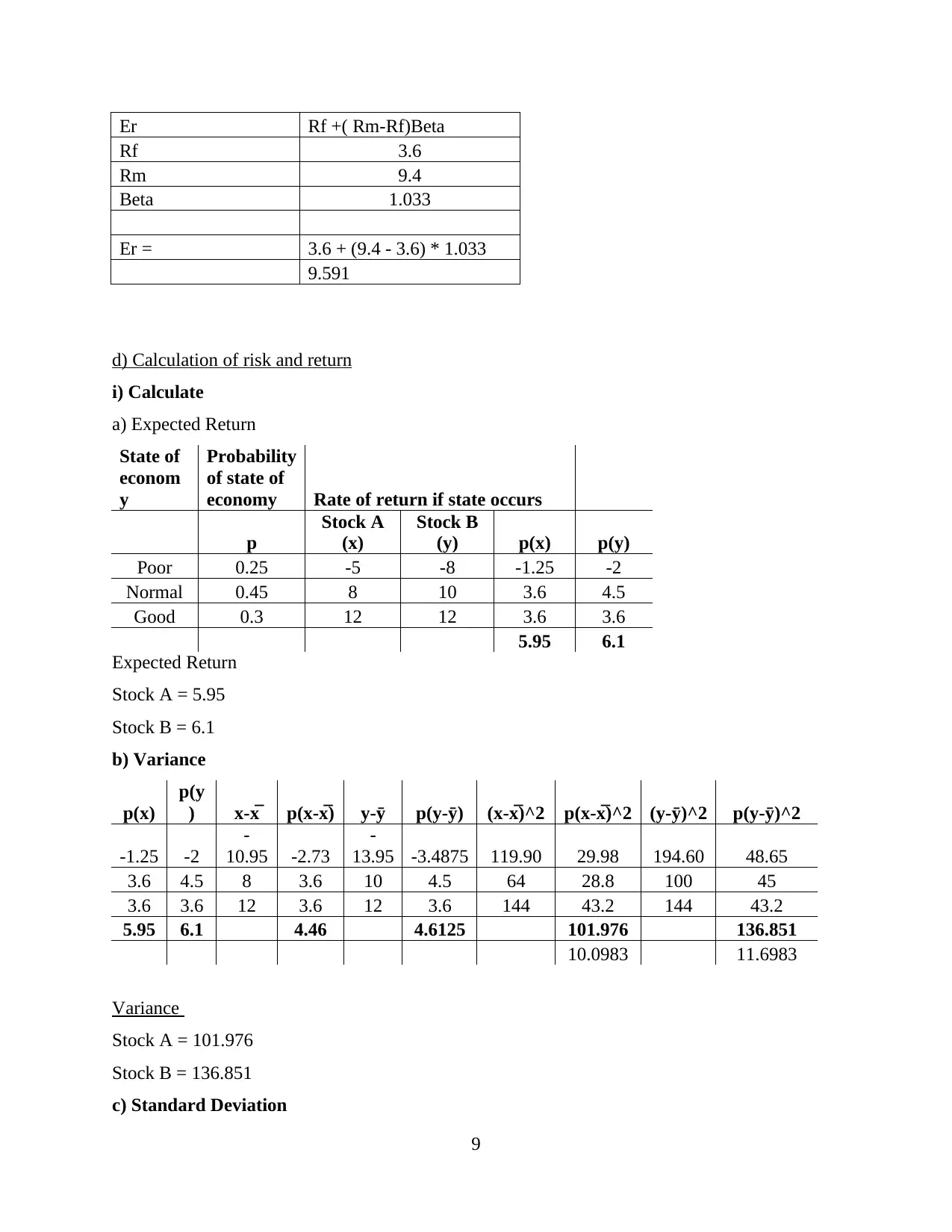

Er Rf +( Rm-Rf)Beta

Rf 3.6

Rm 9.4

Beta 1.033

Er = 3.6 + (9.4 - 3.6) * 1.033

9.591

d) Calculation of risk and return

i) Calculate

a) Expected Return

State of

econom

y

Probability

of state of

economy Rate of return if state occurs

p

Stock A

(x)

Stock B

(y) p(x) p(y)

Poor 0.25 -5 -8 -1.25 -2

Normal 0.45 8 10 3.6 4.5

Good 0.3 12 12 3.6 3.6

5.95 6.1

Expected Return

Stock A = 5.95

Stock B = 6.1

b) Variance

p(x)

p(y

) x-x̅ p(x-x̅) y-ȳ p(y-ȳ) (x-x̅)^2 p(x-x̅)^2 (y-ȳ)^2 p(y-ȳ)^2

-1.25 -2

-

10.95 -2.73

-

13.95 -3.4875 119.90 29.98 194.60 48.65

3.6 4.5 8 3.6 10 4.5 64 28.8 100 45

3.6 3.6 12 3.6 12 3.6 144 43.2 144 43.2

5.95 6.1 4.46 4.6125 101.976 136.851

10.0983 11.6983

Variance

Stock A = 101.976

Stock B = 136.851

c) Standard Deviation

9

Rf 3.6

Rm 9.4

Beta 1.033

Er = 3.6 + (9.4 - 3.6) * 1.033

9.591

d) Calculation of risk and return

i) Calculate

a) Expected Return

State of

econom

y

Probability

of state of

economy Rate of return if state occurs

p

Stock A

(x)

Stock B

(y) p(x) p(y)

Poor 0.25 -5 -8 -1.25 -2

Normal 0.45 8 10 3.6 4.5

Good 0.3 12 12 3.6 3.6

5.95 6.1

Expected Return

Stock A = 5.95

Stock B = 6.1

b) Variance

p(x)

p(y

) x-x̅ p(x-x̅) y-ȳ p(y-ȳ) (x-x̅)^2 p(x-x̅)^2 (y-ȳ)^2 p(y-ȳ)^2

-1.25 -2

-

10.95 -2.73

-

13.95 -3.4875 119.90 29.98 194.60 48.65

3.6 4.5 8 3.6 10 4.5 64 28.8 100 45

3.6 3.6 12 3.6 12 3.6 144 43.2 144 43.2

5.95 6.1 4.46 4.6125 101.976 136.851

10.0983 11.6983

Variance

Stock A = 101.976

Stock B = 136.851

c) Standard Deviation

9

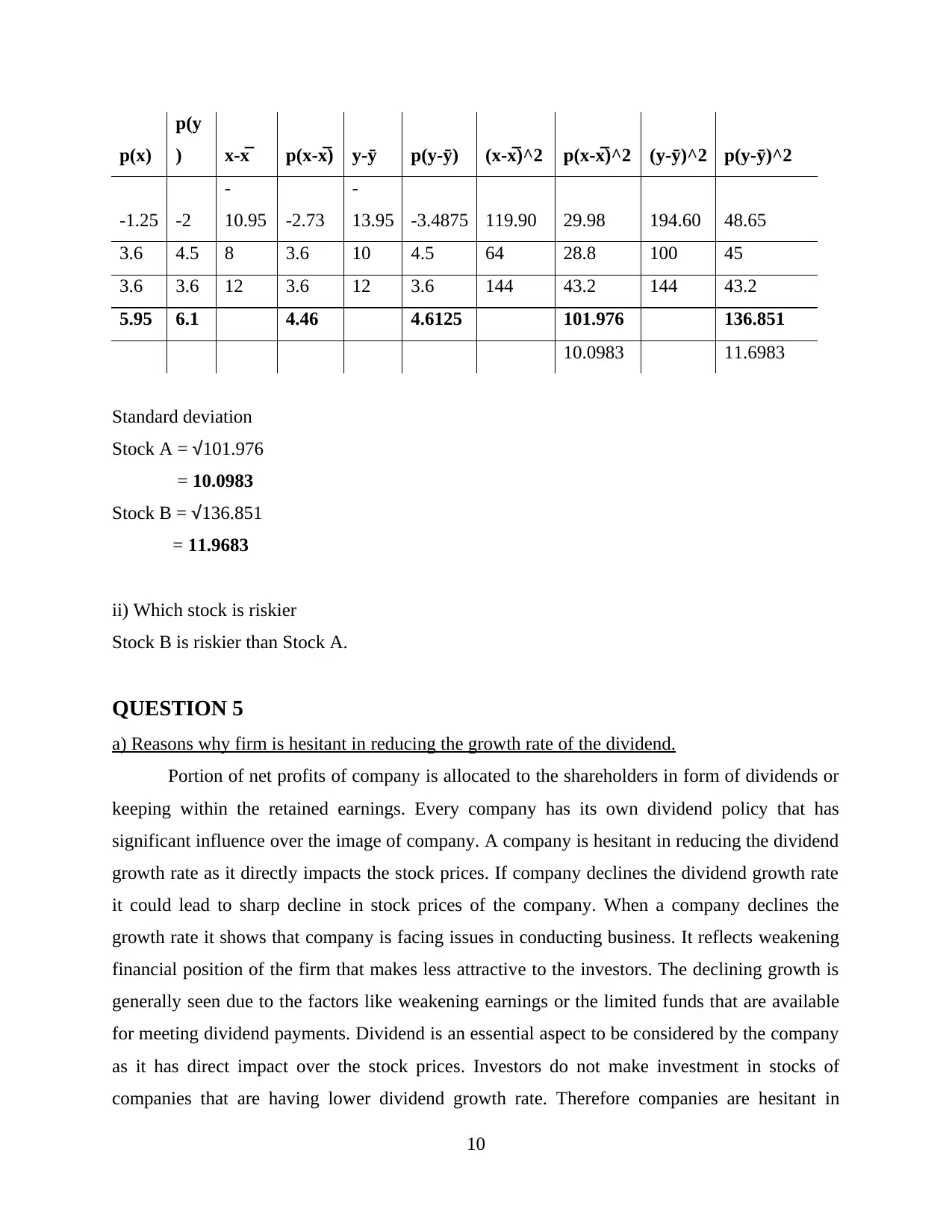

p(x)

p(y

) x-x̅ p(x-x̅) y-ȳ p(y-ȳ) (x-x̅)^2 p(x-x̅)^2 (y-ȳ)^2 p(y-ȳ)^2

-1.25 -2

-

10.95 -2.73

-

13.95 -3.4875 119.90 29.98 194.60 48.65

3.6 4.5 8 3.6 10 4.5 64 28.8 100 45

3.6 3.6 12 3.6 12 3.6 144 43.2 144 43.2

5.95 6.1 4.46 4.6125 101.976 136.851

10.0983 11.6983

Standard deviation

Stock A = √101.976

= 10.0983

Stock B = √136.851

= 11.9683

ii) Which stock is riskier

Stock B is riskier than Stock A.

QUESTION 5

a) Reasons why firm is hesitant in reducing the growth rate of the dividend.

Portion of net profits of company is allocated to the shareholders in form of dividends or

keeping within the retained earnings. Every company has its own dividend policy that has

significant influence over the image of company. A company is hesitant in reducing the dividend

growth rate as it directly impacts the stock prices. If company declines the dividend growth rate

it could lead to sharp decline in stock prices of the company. When a company declines the

growth rate it shows that company is facing issues in conducting business. It reflects weakening

financial position of the firm that makes less attractive to the investors. The declining growth is

generally seen due to the factors like weakening earnings or the limited funds that are available

for meeting dividend payments. Dividend is an essential aspect to be considered by the company

as it has direct impact over the stock prices. Investors do not make investment in stocks of

companies that are having lower dividend growth rate. Therefore companies are hesitant in

10

p(y

) x-x̅ p(x-x̅) y-ȳ p(y-ȳ) (x-x̅)^2 p(x-x̅)^2 (y-ȳ)^2 p(y-ȳ)^2

-1.25 -2

-

10.95 -2.73

-

13.95 -3.4875 119.90 29.98 194.60 48.65

3.6 4.5 8 3.6 10 4.5 64 28.8 100 45

3.6 3.6 12 3.6 12 3.6 144 43.2 144 43.2

5.95 6.1 4.46 4.6125 101.976 136.851

10.0983 11.6983

Standard deviation

Stock A = √101.976

= 10.0983

Stock B = √136.851

= 11.9683

ii) Which stock is riskier

Stock B is riskier than Stock A.

QUESTION 5

a) Reasons why firm is hesitant in reducing the growth rate of the dividend.

Portion of net profits of company is allocated to the shareholders in form of dividends or

keeping within the retained earnings. Every company has its own dividend policy that has

significant influence over the image of company. A company is hesitant in reducing the dividend

growth rate as it directly impacts the stock prices. If company declines the dividend growth rate

it could lead to sharp decline in stock prices of the company. When a company declines the

growth rate it shows that company is facing issues in conducting business. It reflects weakening

financial position of the firm that makes less attractive to the investors. The declining growth is

generally seen due to the factors like weakening earnings or the limited funds that are available

for meeting dividend payments. Dividend is an essential aspect to be considered by the company

as it has direct impact over the stock prices. Investors do not make investment in stocks of

companies that are having lower dividend growth rate. Therefore companies are hesitant in

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.