Principles of Taxation Law: Deductions, Credits, and GST Analysis

VerifiedAdded on 2020/02/23

|14

|2540

|139

Homework Assignment

AI Summary

This assignment delves into the intricacies of Australian taxation law, analyzing various scenarios and legal principles. The student explores the deductibility of expenses under section 8-1 of the ITAA 1997, examining issues such as the cost of relocating machinery, revaluation of assets for insurance, legal expenses related to winding up a business, and legal fees for business administration. The assignment also covers the Goods and Services Tax (GST) Act 1999, specifically focusing on input tax credits for advertising expenses, referencing relevant GST rulings and case law like GSTR 2006/3 and Ronpibon Tin NL v. FC of T. The analysis considers the 'extent' and 'to the extent' principles of the GST legislation, determining whether expenses are incurred for a creditable purpose and thus eligible for input tax credits. The student provides detailed legal reasoning and conclusions for each scenario, determining the tax implications of various business expenditures.

Running head: PRINCIPLES OF TAXATION LAW

Principles of Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Principles of Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PRINCIPLES OF TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to scenario 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Legislations:...............................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to Issue 2:......................................................................................................................4

Issue:..........................................................................................................................................4

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................5

Answer to scenario 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Answer to scenario 4:.................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

Application:................................................................................................................................6

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to scenario 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Legislations:...............................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to Issue 2:......................................................................................................................4

Issue:..........................................................................................................................................4

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................5

Answer to scenario 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Answer to scenario 4:.................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

Application:................................................................................................................................6

2PRINCIPLES OF TAXATION LAW

Conclusion:................................................................................................................................7

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

Legislation:.................................................................................................................................7

Application:................................................................................................................................8

Conclusion:................................................................................................................................9

Answer to question 3:...............................................................................................................10

Answer to question 4:...............................................................................................................11

Reference List:.........................................................................................................................13

Conclusion:................................................................................................................................7

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

Legislation:.................................................................................................................................7

Application:................................................................................................................................8

Conclusion:................................................................................................................................9

Answer to question 3:...............................................................................................................10

Answer to question 4:...............................................................................................................11

Reference List:.........................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PRINCIPLES OF TAXATION LAW

Answer to question 1:

Answer to scenario 1:

Issue:

The question brings forward the question that is evidently linked with whether the

cost that is sustained at the time of locating the machine to a new site shall be beheld as the

admissible deductions under section 8-1 of the ITAA 1997.

Legislations:

a. Section 8-1 of the ITAA 1997

b. Taxation Ruling of TD 93/126

c. British Insulated & Helsby Cables

Applications:

Taking into the considerations that is defined under the 8-1 of the ITAA 1997 the

amount of cost involved in moving the assets from one spot to alternative spot would be

considered, as capital in nature and no kind of permissible deductions shall be measured as

acceptable under the above stated section (Coleman and Sadiq 2013). The expenditure might

however result in an increase in the cost of the asset for the purpose of depreciation

(Barkoczy et al. 2016). Any kind of cost that is sustained from the minor changes at the site

would establish the cost as the deductible disbursement “under section 8-1 of the ITAA

1997”. This is because they form the part of the business expenditure resulting from the day

to day activities of carrying on of a business (Harris et al. 2016).

In respect of the decision that is passed under the case of British Insulated & Helsby

Cables the cost that is incurred at the time of transportation will be accounted in the form of

lasting benefit on the commercial properties of the taxpayer’s by locating the depreciable

Answer to question 1:

Answer to scenario 1:

Issue:

The question brings forward the question that is evidently linked with whether the

cost that is sustained at the time of locating the machine to a new site shall be beheld as the

admissible deductions under section 8-1 of the ITAA 1997.

Legislations:

a. Section 8-1 of the ITAA 1997

b. Taxation Ruling of TD 93/126

c. British Insulated & Helsby Cables

Applications:

Taking into the considerations that is defined under the 8-1 of the ITAA 1997 the

amount of cost involved in moving the assets from one spot to alternative spot would be

considered, as capital in nature and no kind of permissible deductions shall be measured as

acceptable under the above stated section (Coleman and Sadiq 2013). The expenditure might

however result in an increase in the cost of the asset for the purpose of depreciation

(Barkoczy et al. 2016). Any kind of cost that is sustained from the minor changes at the site

would establish the cost as the deductible disbursement “under section 8-1 of the ITAA

1997”. This is because they form the part of the business expenditure resulting from the day

to day activities of carrying on of a business (Harris et al. 2016).

In respect of the decision that is passed under the case of British Insulated & Helsby

Cables the cost that is incurred at the time of transportation will be accounted in the form of

lasting benefit on the commercial properties of the taxpayer’s by locating the depreciable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PRINCIPLES OF TAXATION LAW

asset (Kenny 2013). Once the plant is installed and it is in an operational state, the cost

involved in brining the machinery in the full operation, however not the cost of additions or

modifications would constitute revenue in nature under Taxation Ruling of TD 93/126.

From the above defined analysis in the present circumstances it is discerned that the

cost involved in shifting the machine to new site characterises a cost that holds the anture

capital and it will measured as non- permissible deductions.

Conclusion:

As it has been defined from the above conduced analysis it can be concluded that

moving of fixed asset from one location to another location would be held possessing the

characteristics of capital expenditure and no deductions shall be allowed in section 8-1 of the

ITAA 1997. The expenditure might however result in a rise in the cost of the item for the

purpose of depreciation.

Answer to Issue 2:

Issue:

The existent question introduces the issues that is related with the revaluation of

assets to the effect of insurance cover, which would be measured as acceptable deductions

under section 8-1 of the ITAA 1997.

Legislation:

a. Section 8-1 of the ITAA 1997

Application:

As evident from the scenario, though the expenditure is associated with the fixed

assets, in determining the deductibility it is important whether the expenditure incurred on

revaluing the assets represents the expense that is incurred in enlarging the income producing

asset (Kenny 2013). Once the plant is installed and it is in an operational state, the cost

involved in brining the machinery in the full operation, however not the cost of additions or

modifications would constitute revenue in nature under Taxation Ruling of TD 93/126.

From the above defined analysis in the present circumstances it is discerned that the

cost involved in shifting the machine to new site characterises a cost that holds the anture

capital and it will measured as non- permissible deductions.

Conclusion:

As it has been defined from the above conduced analysis it can be concluded that

moving of fixed asset from one location to another location would be held possessing the

characteristics of capital expenditure and no deductions shall be allowed in section 8-1 of the

ITAA 1997. The expenditure might however result in a rise in the cost of the item for the

purpose of depreciation.

Answer to Issue 2:

Issue:

The existent question introduces the issues that is related with the revaluation of

assets to the effect of insurance cover, which would be measured as acceptable deductions

under section 8-1 of the ITAA 1997.

Legislation:

a. Section 8-1 of the ITAA 1997

Application:

As evident from the scenario, though the expenditure is associated with the fixed

assets, in determining the deductibility it is important whether the expenditure incurred on

revaluing the assets represents the expense that is incurred in enlarging the income producing

5PRINCIPLES OF TAXATION LAW

capacity or they are incurred simply to safeguard or preserve the asset. If the latter results in

the form of benefit that is very much expected to possess the characteristics of provisional,

exclusively if the spending are in most of the scenario is periodic then it is going to be

measured as the deductible spending under section 8-1 of the ITAA 1997 (Keyzer, Goff and

Fisher 2015). From the analysis it is discerned that the cost sustained on revaluing the asset to

the effect of insurance cover in most likely scenario will be treated as the acceptable

deductions from the time when the expenditure is perhaps is possessing the characteristics of

frequent and periodic under section 8-1.

Conclusion:

On arriving at the conclusion, it can be ascertained that the cost incurred represents as

an allowable deductions since the expenditure are recurring in nature and satisfies the criteria

of deductibility under section 8-1 of the ITAA 1997.

Answer to scenario 3:

Issue:

The existent question is evidently related to the ascertainment of whether or not the

lawful spending incurred by the firm for the purpose of differing an appeal for winding up

would be measured as the acceptable deductions under section 8-1 of the ITAA 1997 (Krever

2013).

Legislation:

a. FC of T v Snowden and Wilson Pty Ltd (1958)

b. Taxation ruling of ID 2004/367

c. Section 8-1 of the ITAA 1997

capacity or they are incurred simply to safeguard or preserve the asset. If the latter results in

the form of benefit that is very much expected to possess the characteristics of provisional,

exclusively if the spending are in most of the scenario is periodic then it is going to be

measured as the deductible spending under section 8-1 of the ITAA 1997 (Keyzer, Goff and

Fisher 2015). From the analysis it is discerned that the cost sustained on revaluing the asset to

the effect of insurance cover in most likely scenario will be treated as the acceptable

deductions from the time when the expenditure is perhaps is possessing the characteristics of

frequent and periodic under section 8-1.

Conclusion:

On arriving at the conclusion, it can be ascertained that the cost incurred represents as

an allowable deductions since the expenditure are recurring in nature and satisfies the criteria

of deductibility under section 8-1 of the ITAA 1997.

Answer to scenario 3:

Issue:

The existent question is evidently related to the ascertainment of whether or not the

lawful spending incurred by the firm for the purpose of differing an appeal for winding up

would be measured as the acceptable deductions under section 8-1 of the ITAA 1997 (Krever

2013).

Legislation:

a. FC of T v Snowden and Wilson Pty Ltd (1958)

b. Taxation ruling of ID 2004/367

c. Section 8-1 of the ITAA 1997

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PRINCIPLES OF TAXATION LAW

Application:

As defined under the taxation ruling of ID 2004/367 legal cost are generally

considered as deductible given the fact that they are incurred or the claim is made because of

very act of executing the work through which the taxpayers derives the taxable income. In

agreement with the section 8-1 of the ITAA 1997 cost that a taxpayer sustains in the process

of winding up of a commercial business are commonly not arisen for the determination of

carrying of an occupation and therefore they are not viewed as allowable deduction (Morgan,

Mortimer and Pinto 2013). Considering the decision that has been passed in the instance of

FC of T v Snowden and Wilson Pty Ltd (1958) the element that the outflow are sustained are

infrequent and the taxpayer has in kind of earlier instances was required to commence such

legalised activities that in no circumstances avert the disbursement from being regarded as

the admissible deductions.

From the above stated discussion, it can be discerned that the legal charge sustained in

the process of differing a winding up plea would in no circumstances will be acceptable as

deductible outflow for the reason that they possess the character of are capital and such

outlays falls inside the process of the trade.

Conclusion:

On arriving at the conclusion, in compliance with section 8-1 of the ITAA 1997 it can

be concluded that the cost of opposing a petition for winding up would be considered as non-

allowable deductions.

Answer to scenario 4:

Issue:

The existent question is related with the ascertainment of whether or not the legal

disbursement sustained for the amenities of a solicitor for the administration business

Application:

As defined under the taxation ruling of ID 2004/367 legal cost are generally

considered as deductible given the fact that they are incurred or the claim is made because of

very act of executing the work through which the taxpayers derives the taxable income. In

agreement with the section 8-1 of the ITAA 1997 cost that a taxpayer sustains in the process

of winding up of a commercial business are commonly not arisen for the determination of

carrying of an occupation and therefore they are not viewed as allowable deduction (Morgan,

Mortimer and Pinto 2013). Considering the decision that has been passed in the instance of

FC of T v Snowden and Wilson Pty Ltd (1958) the element that the outflow are sustained are

infrequent and the taxpayer has in kind of earlier instances was required to commence such

legalised activities that in no circumstances avert the disbursement from being regarded as

the admissible deductions.

From the above stated discussion, it can be discerned that the legal charge sustained in

the process of differing a winding up plea would in no circumstances will be acceptable as

deductible outflow for the reason that they possess the character of are capital and such

outlays falls inside the process of the trade.

Conclusion:

On arriving at the conclusion, in compliance with section 8-1 of the ITAA 1997 it can

be concluded that the cost of opposing a petition for winding up would be considered as non-

allowable deductions.

Answer to scenario 4:

Issue:

The existent question is related with the ascertainment of whether or not the legal

disbursement sustained for the amenities of a solicitor for the administration business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRINCIPLES OF TAXATION LAW

procedures shall be measured as the acceptable deductions under section 8-1 of the ITAA

1997 (Lang 2014).

Legislation:

a. section 8-1 of the ITAA 1997

Application:

In respect of the principles that is defined under the section 8-1 of the ITAA 1997,

whenever an individual taxpayer concerning the operation of the business to generate the

assessable income incurs a legal spending, it will mostly be measured as the acceptable

deductions. Nonetheless, there is definite exception whenever the legal spending is sustained

signifies the characterises of capital, domestic or private or if it is explicitly sustained in

acquiring the exempted and non-taxable non-exempt returns (Nethercott et al. 2016). In this

regard, for individual occurring legal fees, the expenditure would not be considered as

allowable deductions unless it is clearly incurred in deriving the assessable income.

Consequently as it has been noticed from the present scenario it can is discerned that the legal

outflow of expenditure sustained by the tax payer signifies a relationship with the trade in

acquiring the chargeable proceeds and it would be beheld as admissible deductions in

conformity with the section 8-1 of the ITAA 1997.

Conclusion:

In conformity with above stated analysis and section 8-1 of the ITAA 1997 it can be

evidently discerned that legal fee that is sustained in the process of the trade to yield the

taxable proceeds will measured as the admissible deductions.

procedures shall be measured as the acceptable deductions under section 8-1 of the ITAA

1997 (Lang 2014).

Legislation:

a. section 8-1 of the ITAA 1997

Application:

In respect of the principles that is defined under the section 8-1 of the ITAA 1997,

whenever an individual taxpayer concerning the operation of the business to generate the

assessable income incurs a legal spending, it will mostly be measured as the acceptable

deductions. Nonetheless, there is definite exception whenever the legal spending is sustained

signifies the characterises of capital, domestic or private or if it is explicitly sustained in

acquiring the exempted and non-taxable non-exempt returns (Nethercott et al. 2016). In this

regard, for individual occurring legal fees, the expenditure would not be considered as

allowable deductions unless it is clearly incurred in deriving the assessable income.

Consequently as it has been noticed from the present scenario it can is discerned that the legal

outflow of expenditure sustained by the tax payer signifies a relationship with the trade in

acquiring the chargeable proceeds and it would be beheld as admissible deductions in

conformity with the section 8-1 of the ITAA 1997.

Conclusion:

In conformity with above stated analysis and section 8-1 of the ITAA 1997 it can be

evidently discerned that legal fee that is sustained in the process of the trade to yield the

taxable proceeds will measured as the admissible deductions.

8PRINCIPLES OF TAXATION LAW

Answer to question 2:

Issue:

With regard to the GSTR Act 1999 the existing matter deals with the issue of input

tax credit that can be claimed for the expense that is incurred in advertisement.

Legislation:

a. GSTR Act 1999

b. GSTR 2006/3

c. Ronpibon Tin NL v. FC of T

Application:

As it has be clearly made evident in the GST ruling of GSTR 2006/3, the ruling

introduces introduces the way on the methods that implemented to figure out the input tax

credits. It also defines the method of adjustment to be used by the suppliers of the saleable

provisions that is made under the new system of assessment defined under the GST Act 1999.

The ruling considers the extent to which the creditable purpose and definite use of the ruling

under the division 11, 15 and 129 of the GST Act 1999 (Woellner 2013).

The current case study of Big Bank Ltd evidently lay down that fact the company

acquired a spending of $1,650,000, which additionally included the amount of GST that is

incurred by the company on the advertising campaign in the past year. Taking into the

account the evidence of Big Bank Ltd the “GST ruling of GSTR 2006/3” is relevant to the

units that are registered or compulsory required to attain for registration. It is discerned from

the present issue of Big Bank Ltd that it makes the business supplies, which outdoes the fiscal

attainment verge; it will be measured at the unit that is authorised for claiming the input tax

credits or lowered input tax credits. If an organization is registered or it is required to be

Answer to question 2:

Issue:

With regard to the GSTR Act 1999 the existing matter deals with the issue of input

tax credit that can be claimed for the expense that is incurred in advertisement.

Legislation:

a. GSTR Act 1999

b. GSTR 2006/3

c. Ronpibon Tin NL v. FC of T

Application:

As it has be clearly made evident in the GST ruling of GSTR 2006/3, the ruling

introduces introduces the way on the methods that implemented to figure out the input tax

credits. It also defines the method of adjustment to be used by the suppliers of the saleable

provisions that is made under the new system of assessment defined under the GST Act 1999.

The ruling considers the extent to which the creditable purpose and definite use of the ruling

under the division 11, 15 and 129 of the GST Act 1999 (Woellner 2013).

The current case study of Big Bank Ltd evidently lay down that fact the company

acquired a spending of $1,650,000, which additionally included the amount of GST that is

incurred by the company on the advertising campaign in the past year. Taking into the

account the evidence of Big Bank Ltd the “GST ruling of GSTR 2006/3” is relevant to the

units that are registered or compulsory required to attain for registration. It is discerned from

the present issue of Big Bank Ltd that it makes the business supplies, which outdoes the fiscal

attainment verge; it will be measured at the unit that is authorised for claiming the input tax

credits or lowered input tax credits. If an organization is registered or it is required to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PRINCIPLES OF TAXATION LAW

registered under the GST Act 1999, GST shall be payable by the individual or the company

on the taxable supplies that it makes (Woellner et al. 2016).

As stated under the scheme of the GST legislation an individual shall be permitted to

input tax credits for the sum of GST that is included in the value of the things an individual

acquires or importation for their enterprise (Nethercott et al. 2016). However, if an individual

making supplies exceed the threshold limits of the financial acquisition, they will be not be

allowed to recover the entire amount of GST charged to them, hence a fragment of the GST

shall be able to be recuperated.

In respect of the reference to the case of Ronpibon Tin NL v. FC of T the principles

of “extent” and “to the extent” applies in the understanding of the GST regulation. This

comprises of the obligation where the allotment method is accepted in order to be rational

and judicious under the situations of the respective enterprise (Morgan, Mortimer and Pinto

2013). Bearing in mind the provisions that has been specified under paragraphs 11-5 and 15-

5 for an acquisition to be treated as the creditable realisation or creditable import it ought to

be in such a manner that the acquirement is exclusively or somewhat partially for the

creditable purpose.

Considering the guidelines defined under the subsection 15-25 an import will be

somewhat partly be treated as the creditable acquisition if the same is solitarily for a partially

creditable purpose. Taking account of the guidelines defined under the section 11-15 or 15-

10 an import is partly measured as creditable if an entity makes financial supplies for the

purpose of the input tax credit or partly for the domestic purpose (Coleman and Sadiq 2013).

As evident in the present Scenario of Big Bank Ltd, the advertising expenditure was incurred

for the creditable acquisition purpose. Big Bank Ltd in agreement with the GSTR ruling of

2006/3 it has discerned that the company made the procurement of the fiscal purchases that

registered under the GST Act 1999, GST shall be payable by the individual or the company

on the taxable supplies that it makes (Woellner et al. 2016).

As stated under the scheme of the GST legislation an individual shall be permitted to

input tax credits for the sum of GST that is included in the value of the things an individual

acquires or importation for their enterprise (Nethercott et al. 2016). However, if an individual

making supplies exceed the threshold limits of the financial acquisition, they will be not be

allowed to recover the entire amount of GST charged to them, hence a fragment of the GST

shall be able to be recuperated.

In respect of the reference to the case of Ronpibon Tin NL v. FC of T the principles

of “extent” and “to the extent” applies in the understanding of the GST regulation. This

comprises of the obligation where the allotment method is accepted in order to be rational

and judicious under the situations of the respective enterprise (Morgan, Mortimer and Pinto

2013). Bearing in mind the provisions that has been specified under paragraphs 11-5 and 15-

5 for an acquisition to be treated as the creditable realisation or creditable import it ought to

be in such a manner that the acquirement is exclusively or somewhat partially for the

creditable purpose.

Considering the guidelines defined under the subsection 15-25 an import will be

somewhat partly be treated as the creditable acquisition if the same is solitarily for a partially

creditable purpose. Taking account of the guidelines defined under the section 11-15 or 15-

10 an import is partly measured as creditable if an entity makes financial supplies for the

purpose of the input tax credit or partly for the domestic purpose (Coleman and Sadiq 2013).

As evident in the present Scenario of Big Bank Ltd, the advertising expenditure was incurred

for the creditable acquisition purpose. Big Bank Ltd in agreement with the GSTR ruling of

2006/3 it has discerned that the company made the procurement of the fiscal purchases that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PRINCIPLES OF TAXATION LAW

surpasses the monetary procurement verge and the bill that is issued to the company by their

tax consultant will considered eligible for input tax credit or reduced tax credit (Schenk

2016). In compliance with the GST legislation, Big Bank is entitled to input tax credit for the

purpose of GST in the price of advertising expenses acquired or imported by the company.

Conclusion:

From the analysis that is conducted above, it can be detected that Big Bank Ltd will

be qualifies for claiming input tax credit in conformity with GSTR 2006/13 for the

expenditure that is incurred on the advertising for the creditable acquisition.

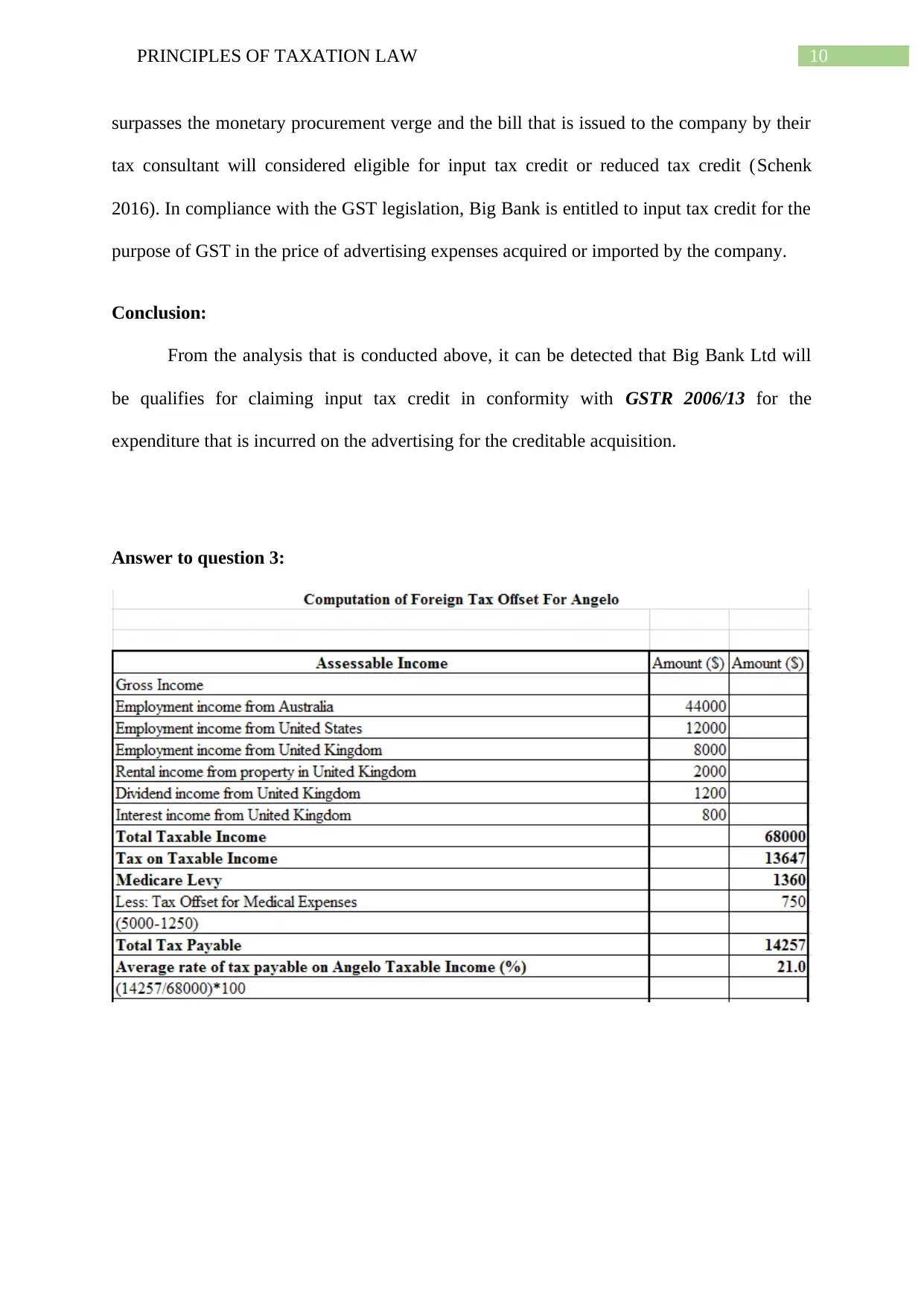

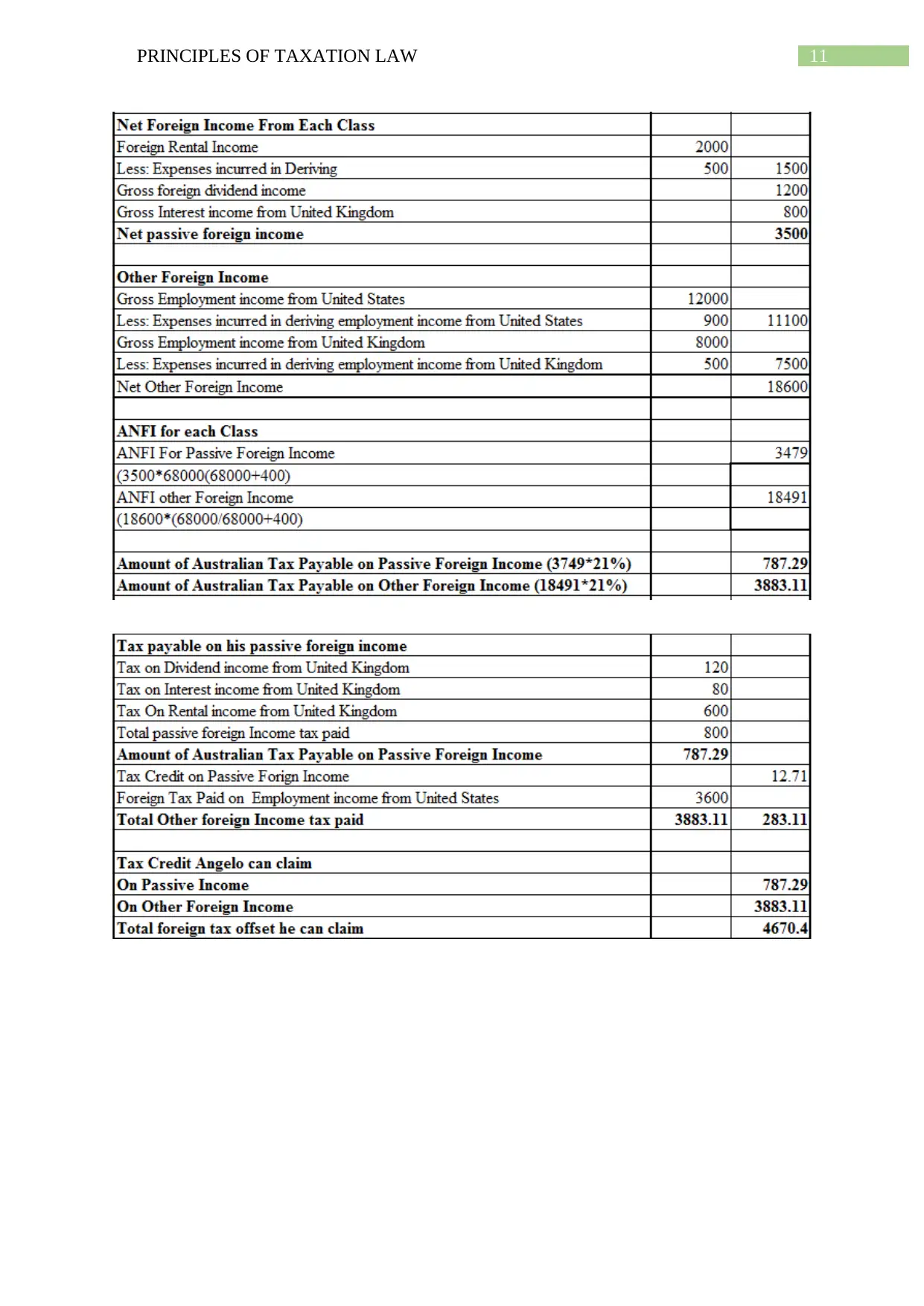

Answer to question 3:

surpasses the monetary procurement verge and the bill that is issued to the company by their

tax consultant will considered eligible for input tax credit or reduced tax credit (Schenk

2016). In compliance with the GST legislation, Big Bank is entitled to input tax credit for the

purpose of GST in the price of advertising expenses acquired or imported by the company.

Conclusion:

From the analysis that is conducted above, it can be detected that Big Bank Ltd will

be qualifies for claiming input tax credit in conformity with GSTR 2006/13 for the

expenditure that is incurred on the advertising for the creditable acquisition.

Answer to question 3:

11PRINCIPLES OF TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.