Financial Analysis: Wilcox Industries LBO for Private Equity Fund

VerifiedAdded on 2020/10/22

|9

|2195

|173

Report

AI Summary

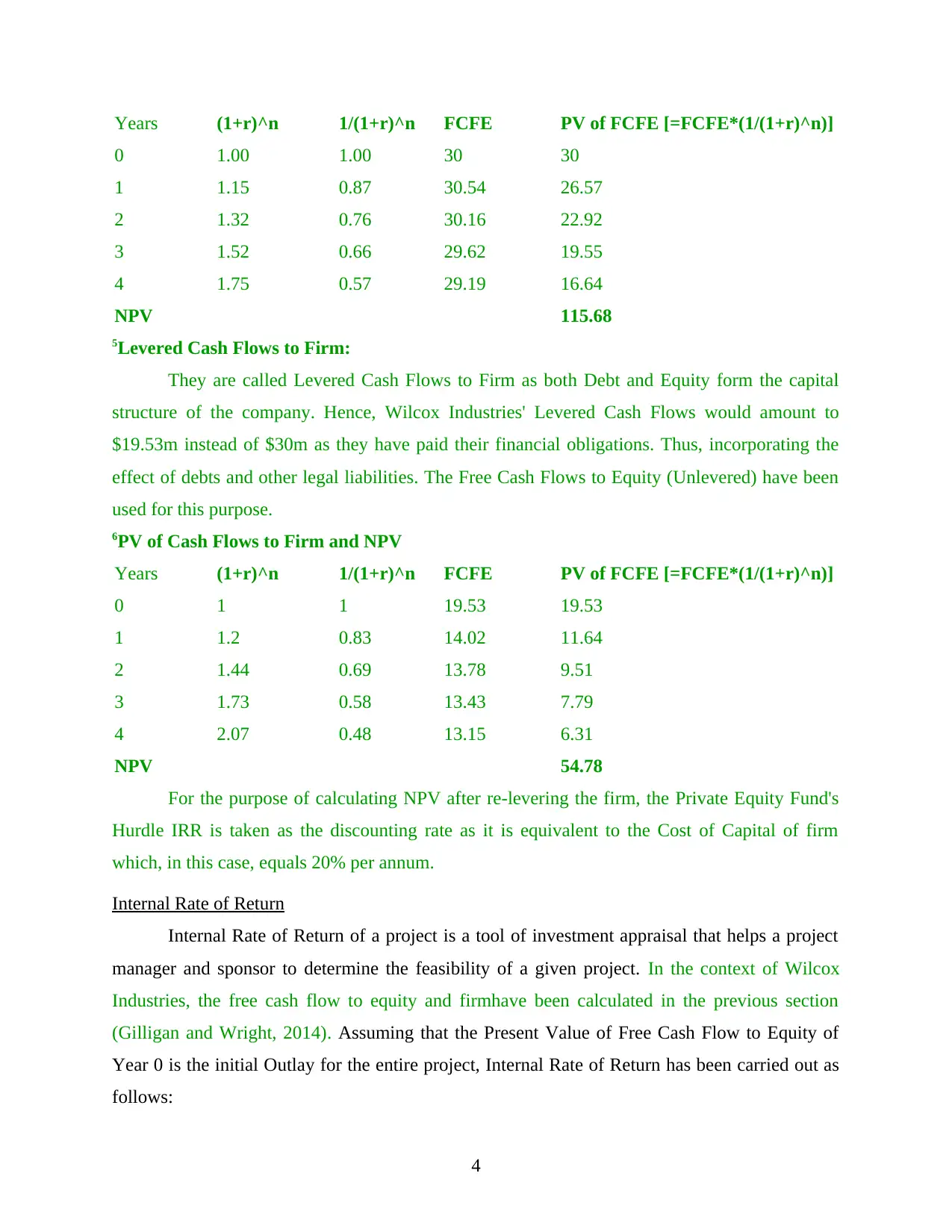

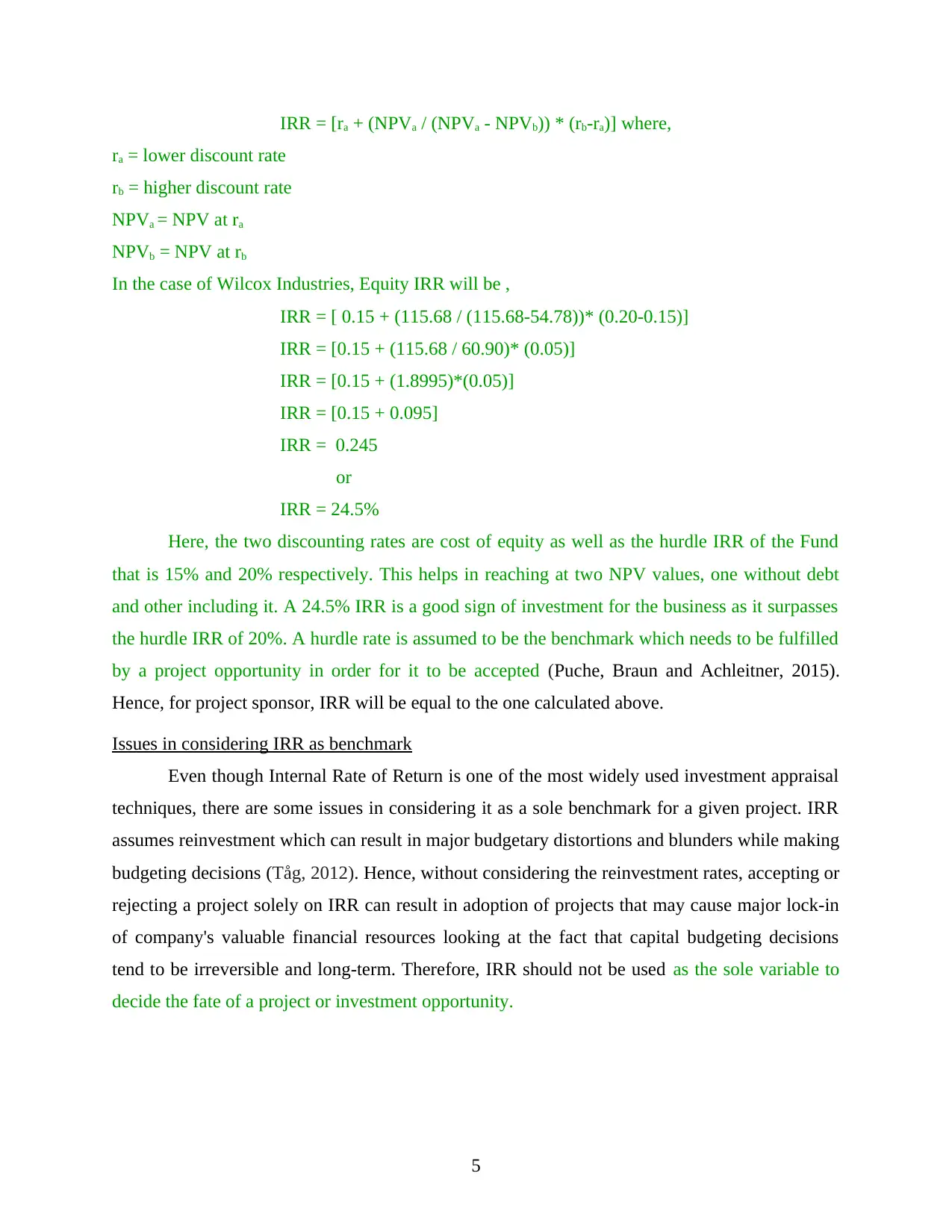

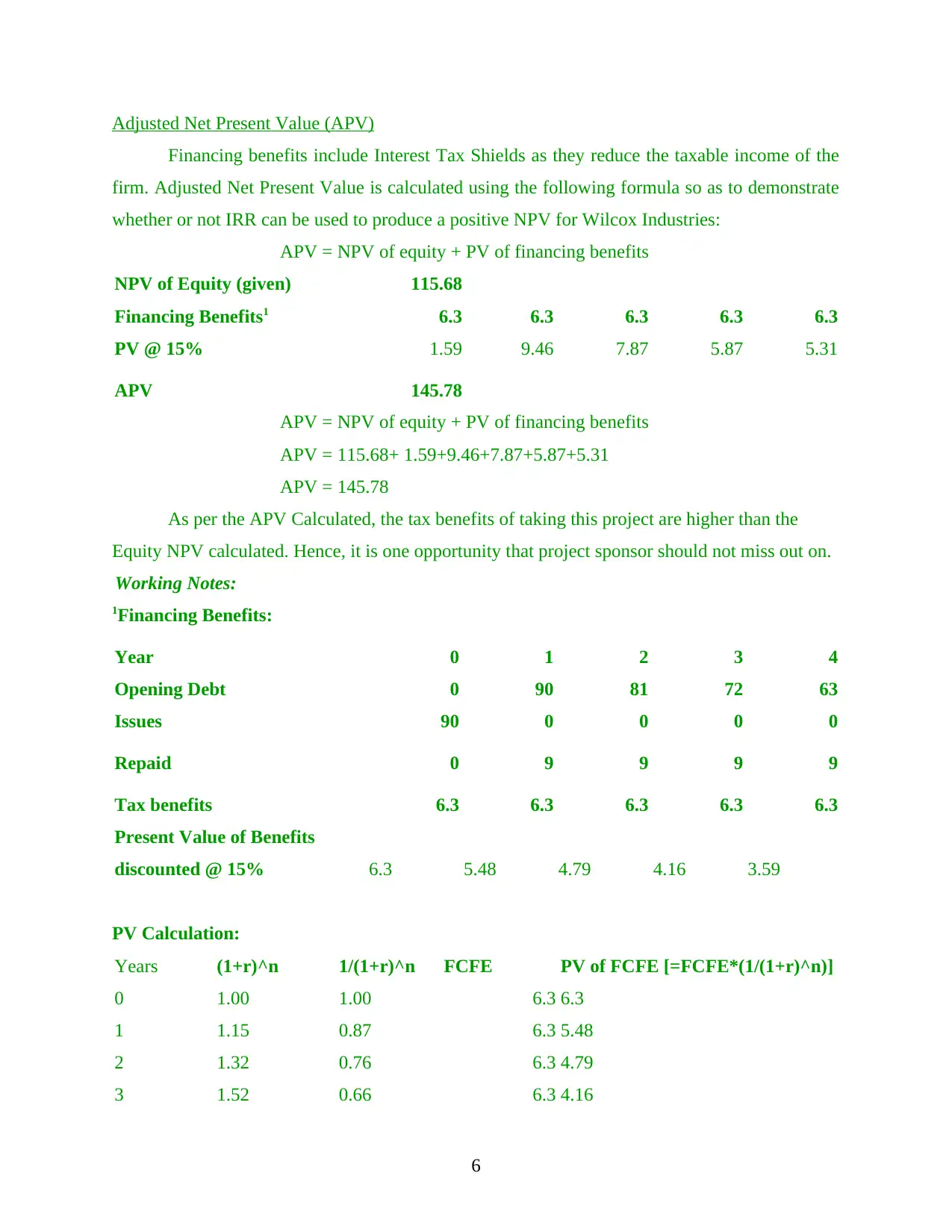

This report analyzes the proposed Leverage Buyout (LBO) of Wilcox Industries, assessing its potential for a private equity fund. The analysis begins with forecasted cash flows, including revenue, EBIT, and capital expenditures, to determine the Equity Free Cash Flows. These cash flows are then used to calculate the Internal Rate of Return (IRR), which is compared to the fund's hurdle rate to evaluate the investment's profitability. The report also addresses issues with relying solely on IRR and calculates the Adjusted Net Present Value (APV) to incorporate the benefits of financing, specifically interest tax shields. The conclusion emphasizes the importance of capital budgeting and highlights that while LBOs can be beneficial, IRR should not be the sole determinant for investment decisions. The report provides detailed calculations for cash flows, IRR, and APV, along with working notes for key assumptions and calculations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.