Combat Fire, Inc. manufactures steel cylinders

Manufacturing overhead and cost allocation for FireOut, Inc. steel cylinders and nozzles for home and commercial fire extinguishers.

24 Pages6292 Words59 Views

Added on 2022-08-27

Combat Fire, Inc. manufactures steel cylinders

Manufacturing overhead and cost allocation for FireOut, Inc. steel cylinders and nozzles for home and commercial fire extinguishers.

Added on 2022-08-27

ShareRelated Documents

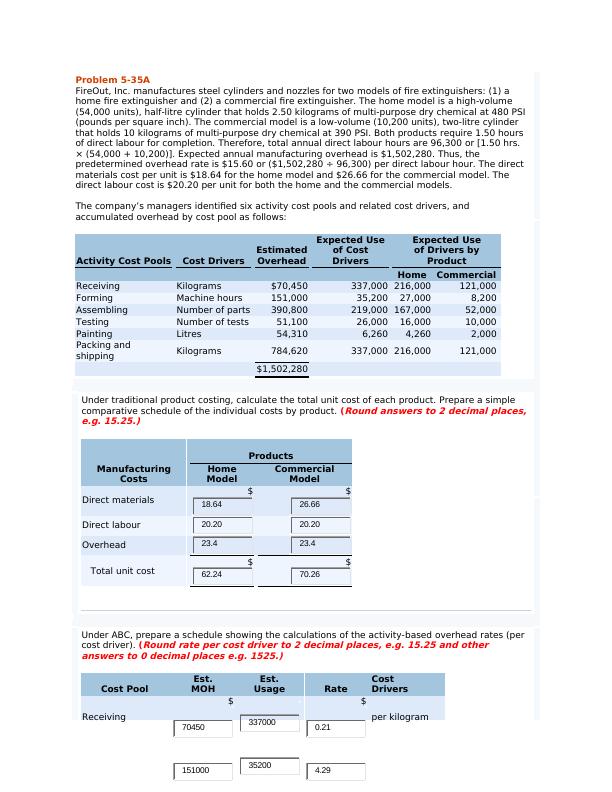

Problem 5-35A

FireOut, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a

home fire extinguisher and (2) a commercial fire extinguisher. The home model is a high-volume

(54,000 units), half-litre cylinder that holds 2.50 kilograms of multi-purpose dry chemical at 480 PSI

(pounds per square inch). The commercial model is a low-volume (10,200 units), two-litre cylinder

that holds 10 kilograms of multi-purpose dry chemical at 390 PSI. Both products require 1.50 hours

of direct labour for completion. Therefore, total annual direct labour hours are 96,300 or [1.50 hrs.

× (54,000 + 10,200)]. Expected annual manufacturing overhead is $1,502,280. Thus, the

predetermined overhead rate is $15.60 or ($1,502,280 ÷ 96,300) per direct labour hour. The direct

materials cost per unit is $18.64 for the home model and $26.66 for the commercial model. The

direct labour cost is $20.20 per unit for both the home and the commercial models.

The company’s managers identified six activity cost pools and related cost drivers, and

accumulated overhead by cost pool as follows:

Activity Cost Pools Cost Drivers

Estimated

Overhead

Expected Use

of Cost

Drivers

Expected Use

of Drivers by

Product

Home Commercial

Receiving Kilograms $70,450 337,000 216,000 121,000

Forming Machine hours 151,000 35,200 27,000 8,200

Assembling Number of parts 390,800 219,000 167,000 52,000

Testing Number of tests 51,100 26,000 16,000 10,000

Painting Litres 54,310 6,260 4,260 2,000

Packing and

shipping Kilograms 784,620 337,000 216,000 121,000

$1,502,280

Under traditional product costing, calculate the total unit cost of each product. Prepare a simple

comparative schedule of the individual costs by product. (

Round answers to 2 decimal places,

e.g. 15.25.)

Products

Manufacturing

Costs

Home

Model

Commercial

Model

Direct materials

$ $

Direct labour

Overhead

Total unit cost

$ $

Under ABC, prepare a schedule showing the calculations of the activity-based overhead rates (per

cost driver). (

Round rate per cost driver to 2 decimal places, e.g. 15.25 and other

answers to 0 decimal places e.g. 1525.)

Cost Pool

Est.

MOH

Est.

Usage Rate

Cost

Drivers

Receiving

$ $

per kilogram

18.64 26.66

20.20 20.20

23.4 23.4

62.24 70.26

70450 337000 0.21

151000 35200 4.29

FireOut, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a

home fire extinguisher and (2) a commercial fire extinguisher. The home model is a high-volume

(54,000 units), half-litre cylinder that holds 2.50 kilograms of multi-purpose dry chemical at 480 PSI

(pounds per square inch). The commercial model is a low-volume (10,200 units), two-litre cylinder

that holds 10 kilograms of multi-purpose dry chemical at 390 PSI. Both products require 1.50 hours

of direct labour for completion. Therefore, total annual direct labour hours are 96,300 or [1.50 hrs.

× (54,000 + 10,200)]. Expected annual manufacturing overhead is $1,502,280. Thus, the

predetermined overhead rate is $15.60 or ($1,502,280 ÷ 96,300) per direct labour hour. The direct

materials cost per unit is $18.64 for the home model and $26.66 for the commercial model. The

direct labour cost is $20.20 per unit for both the home and the commercial models.

The company’s managers identified six activity cost pools and related cost drivers, and

accumulated overhead by cost pool as follows:

Activity Cost Pools Cost Drivers

Estimated

Overhead

Expected Use

of Cost

Drivers

Expected Use

of Drivers by

Product

Home Commercial

Receiving Kilograms $70,450 337,000 216,000 121,000

Forming Machine hours 151,000 35,200 27,000 8,200

Assembling Number of parts 390,800 219,000 167,000 52,000

Testing Number of tests 51,100 26,000 16,000 10,000

Painting Litres 54,310 6,260 4,260 2,000

Packing and

shipping Kilograms 784,620 337,000 216,000 121,000

$1,502,280

Under traditional product costing, calculate the total unit cost of each product. Prepare a simple

comparative schedule of the individual costs by product. (

Round answers to 2 decimal places,

e.g. 15.25.)

Products

Manufacturing

Costs

Home

Model

Commercial

Model

Direct materials

$ $

Direct labour

Overhead

Total unit cost

$ $

Under ABC, prepare a schedule showing the calculations of the activity-based overhead rates (per

cost driver). (

Round rate per cost driver to 2 decimal places, e.g. 15.25 and other

answers to 0 decimal places e.g. 1525.)

Cost Pool

Est.

MOH

Est.

Usage Rate

Cost

Drivers

Receiving

$ $

per kilogram

18.64 26.66

20.20 20.20

23.4 23.4

62.24 70.26

70450 337000 0.21

151000 35200 4.29

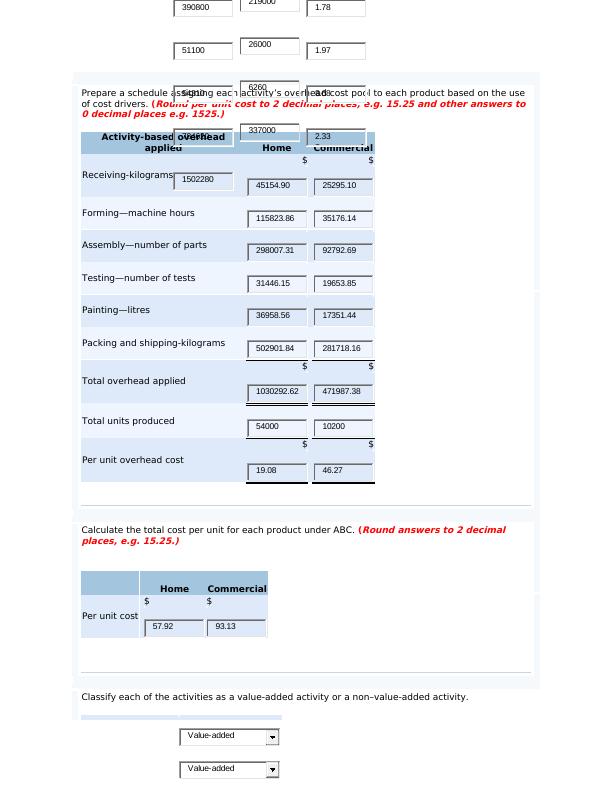

Prepare a schedule assigning each activity’s overhead cost pool to each product based on the use

of cost drivers. (

Round per unit cost to 2 decimal places, e.g. 15.25 and other answers to

0 decimal places e.g. 1525.)

Activity-based overhead

applied Home Commercial

Receiving-kilograms

$ $

Forming—machine hours

Assembly—number of parts

Testing—number of tests

Painting—litres

Packing and shipping-kilograms

Total overhead applied

$ $

Total units produced

Per unit overhead cost

$ $

Calculate the total cost per unit for each product under ABC. (

Round answers to 2 decimal

places, e.g. 15.25.)

Home Commercial

Per unit cost

$ $

Classify each of the activities as a value-added activity or a non–value-added activity.

390800 219000 1.78

51100 26000 1.97

54310 6260 8.68

784620 337000 2.33

1502280 45154.90 25295.10

115823.86 35176.14

298007.31 92792.69

31446.15 19653.85

36958.56 17351.44

502901.84 281718.16

1030292.62 471987.38

54000 10200

19.08 46.27

57.92 93.13

Value-added

Value-added

of cost drivers. (

Round per unit cost to 2 decimal places, e.g. 15.25 and other answers to

0 decimal places e.g. 1525.)

Activity-based overhead

applied Home Commercial

Receiving-kilograms

$ $

Forming—machine hours

Assembly—number of parts

Testing—number of tests

Painting—litres

Packing and shipping-kilograms

Total overhead applied

$ $

Total units produced

Per unit overhead cost

$ $

Calculate the total cost per unit for each product under ABC. (

Round answers to 2 decimal

places, e.g. 15.25.)

Home Commercial

Per unit cost

$ $

Classify each of the activities as a value-added activity or a non–value-added activity.

390800 219000 1.78

51100 26000 1.97

54310 6260 8.68

784620 337000 2.33

1502280 45154.90 25295.10

115823.86 35176.14

298007.31 92792.69

31446.15 19653.85

36958.56 17351.44

502901.84 281718.16

1030292.62 471987.38

54000 10200

19.08 46.27

57.92 93.13

Value-added

Value-added

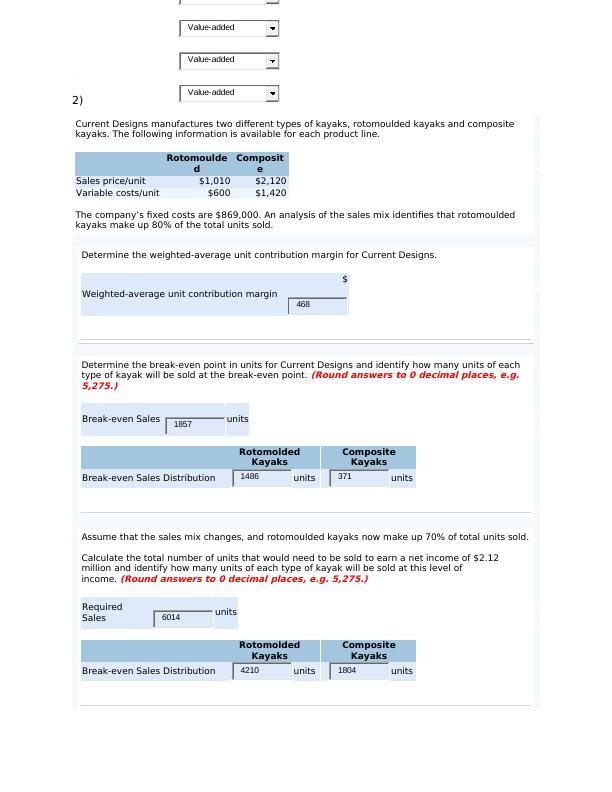

2)

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

Rotomoulde

d

Composit

e

Sales price/unit $1,010 $2,120

Variable costs/unit $600 $1,420

The company’s fixed costs are $869,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point.

(Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Assume that the sales mix changes, and rotomoulded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2.12

million and identify how many units of each type of kayak will be sold at this level of

income.

(Round answers to 0 decimal places, e.g. 5,275.)

Required

Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Value-added

Value-added

Value-added

468

1857

1486 371

6014

4210 1804

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

Rotomoulde

d

Composit

e

Sales price/unit $1,010 $2,120

Variable costs/unit $600 $1,420

The company’s fixed costs are $869,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point.

(Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Assume that the sales mix changes, and rotomoulded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2.12

million and identify how many units of each type of kayak will be sold at this level of

income.

(Round answers to 0 decimal places, e.g. 5,275.)

Required

Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

Value-added

Value-added

Value-added

468

1857

1486 371

6014

4210 1804

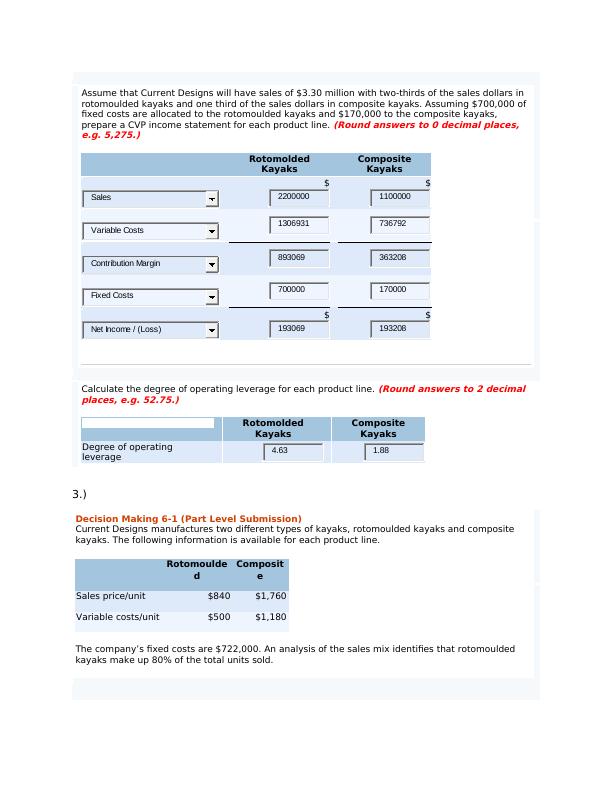

Assume that Current Designs will have sales of $3.30 million with two-thirds of the sales dollars in

rotomoulded kayaks and one third of the sales dollars in composite kayaks. Assuming $700,000 of

fixed costs are allocated to the rotomoulded kayaks and $170,000 to the composite kayaks,

prepare a CVP income statement for each product line.

(Round answers to 0 decimal places,

e.g. 5,275.)

Rotomolded

Kayaks

Composite

Kayaks

$ $

$ $

Calculate the degree of operating leverage for each product line.

(Round answers to 2 decimal

places, e.g. 52.75.)

Rotomolded

Kayaks

Composite

Kayaks

Degree of operating

leverage

3.)

Decision Making 6-1 (Part Level Submission)

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

Rotomoulde

d

Composit

e

Sales price/unit $840 $1,760

Variable costs/unit $500 $1,180

The company’s fixed costs are $722,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

Sales 2200000 1100000

Variable Costs 1306931 736792

Contribution Margin 893069 363208

Fixed Costs 700000 170000

Net Income / (Loss) 193069 193208

4.63 1.88

rotomoulded kayaks and one third of the sales dollars in composite kayaks. Assuming $700,000 of

fixed costs are allocated to the rotomoulded kayaks and $170,000 to the composite kayaks,

prepare a CVP income statement for each product line.

(Round answers to 0 decimal places,

e.g. 5,275.)

Rotomolded

Kayaks

Composite

Kayaks

$ $

$ $

Calculate the degree of operating leverage for each product line.

(Round answers to 2 decimal

places, e.g. 52.75.)

Rotomolded

Kayaks

Composite

Kayaks

Degree of operating

leverage

3.)

Decision Making 6-1 (Part Level Submission)

Current Designs manufactures two different types of kayaks, rotomoulded kayaks and composite

kayaks. The following information is available for each product line.

Rotomoulde

d

Composit

e

Sales price/unit $840 $1,760

Variable costs/unit $500 $1,180

The company’s fixed costs are $722,000. An analysis of the sales mix identifies that rotomoulded

kayaks make up 80% of the total units sold.

Sales 2200000 1100000

Variable Costs 1306931 736792

Contribution Margin 893069 363208

Fixed Costs 700000 170000

Net Income / (Loss) 193069 193208

4.63 1.88

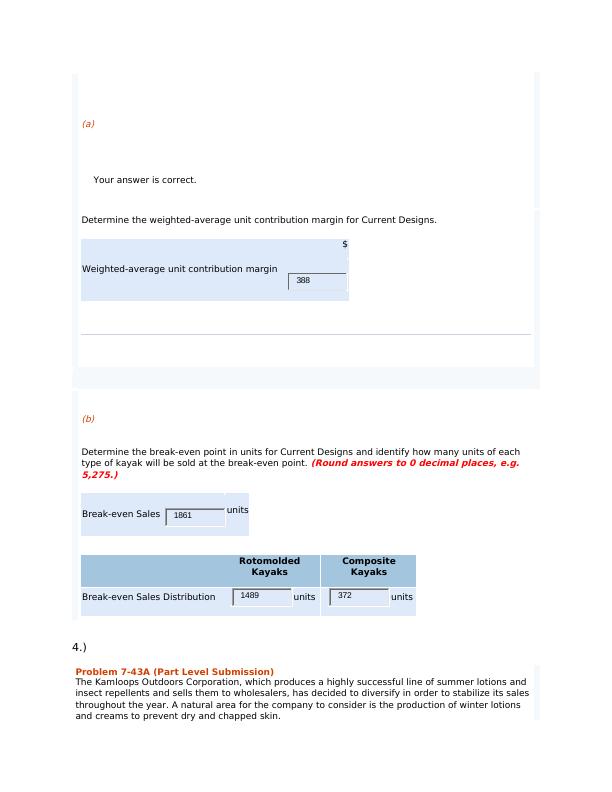

(a)

Your answer is correct.

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

(b)

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point.

(Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

4.)

Problem 7-43A (Part Level Submission)

The Kamloops Outdoors Corporation, which produces a highly successful line of summer lotions and

insect repellents and sells them to wholesalers, has decided to diversify in order to stabilize its sales

throughout the year. A natural area for the company to consider is the production of winter lotions

and creams to prevent dry and chapped skin.

388

1861

1489 372

Your answer is correct.

Determine the weighted-average unit contribution margin for Current Designs.

Weighted-average unit contribution margin

$

(b)

Determine the break-even point in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point.

(Round answers to 0 decimal places, e.g.

5,275.)

Break-even Sales units

Rotomolded

Kayaks

Composite

Kayaks

Break-even Sales Distribution units units

4.)

Problem 7-43A (Part Level Submission)

The Kamloops Outdoors Corporation, which produces a highly successful line of summer lotions and

insect repellents and sells them to wholesalers, has decided to diversify in order to stabilize its sales

throughout the year. A natural area for the company to consider is the production of winter lotions

and creams to prevent dry and chapped skin.

388

1861

1489 372

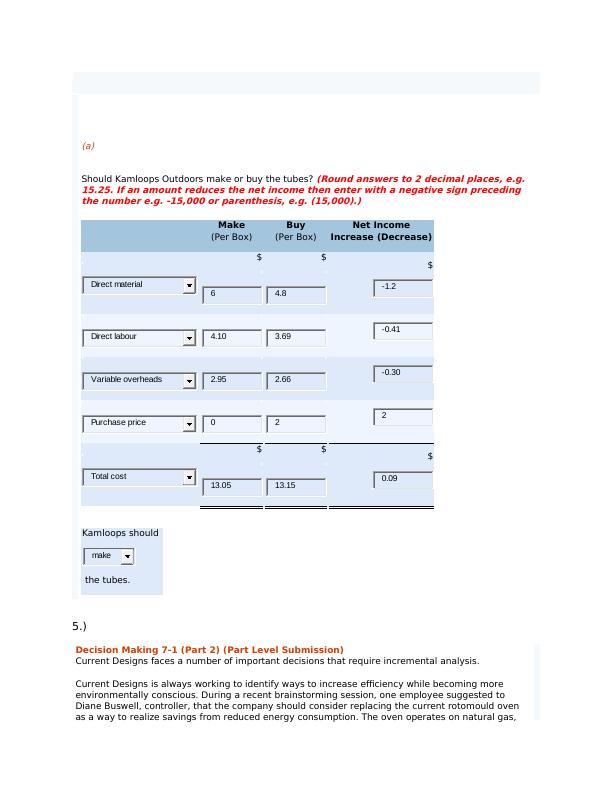

(a)

Should Kamloops Outdoors make or buy the tubes?

(Round answers to 2 decimal places, e.g.

15.25. If an amount reduces the net income then enter with a negative sign preceding

the number e.g. -15,000 or parenthesis, e.g. (15,000).)

Make

(Per Box)

Buy

(Per Box)

Net Income

Increase (Decrease)

$ $ $

$ $ $

Kamloops should

the tubes.

5.)

Decision Making 7-1 (Part 2) (Part Level Submission)

Current Designs faces a number of important decisions that require incremental analysis.

Current Designs is always working to identify ways to increase efficiency while becoming more

environmentally conscious. During a recent brainstorming session, one employee suggested to

Diane Buswell, controller, that the company should consider replacing the current rotomould oven

as a way to realize savings from reduced energy consumption. The oven operates on natural gas,

Direct material

6 4.8 -1.2

Direct labour 4.10 3.69 -0.41

Variable overheads 2.95 2.66 -0.30

Purchase price 0 2 2

Total cost

13.05 13.15 0.09

make

Should Kamloops Outdoors make or buy the tubes?

(Round answers to 2 decimal places, e.g.

15.25. If an amount reduces the net income then enter with a negative sign preceding

the number e.g. -15,000 or parenthesis, e.g. (15,000).)

Make

(Per Box)

Buy

(Per Box)

Net Income

Increase (Decrease)

$ $ $

$ $ $

Kamloops should

the tubes.

5.)

Decision Making 7-1 (Part 2) (Part Level Submission)

Current Designs faces a number of important decisions that require incremental analysis.

Current Designs is always working to identify ways to increase efficiency while becoming more

environmentally conscious. During a recent brainstorming session, one employee suggested to

Diane Buswell, controller, that the company should consider replacing the current rotomould oven

as a way to realize savings from reduced energy consumption. The oven operates on natural gas,

Direct material

6 4.8 -1.2

Direct labour 4.10 3.69 -0.41

Variable overheads 2.95 2.66 -0.30

Purchase price 0 2 2

Total cost

13.05 13.15 0.09

make

End of preview

Want to access all the pages? Upload your documents or become a member.