Analyzing Financial Assistance Problems for Canadian SMBs

VerifiedAdded on 2022/10/01

|72

|17068

|351

Report

AI Summary

This report delves into the financial challenges encountered by small businesses in Canada when seeking financial assistance from Canadian banks. It begins by highlighting the difficulties small businesses face in securing capital, particularly in a competitive market. The research explores the various financial assistance options available, including loans and equity financing, while also identifying the problems associated with each. The study utilizes interviews with managers, employees, and owners of small businesses to understand their perspectives on issues such as the time and effort required to find investors, the imposition of ownership or control by investors, and concerns about equity financing. The report investigates the vital issues related to small business operations while gathering financial assistance, approaches to overcome these challenges, and the likely effects of these issues. The findings emphasize the need for the development of a business angel network to connect potential investors with small businesses, along with recommendations to improve financial situations. The report ultimately provides a comprehensive analysis of the problems faced by Canadian small businesses in obtaining financial assistance and suggests potential solutions.

PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL

ASSISTANCE

Small Businesses in Canada Face Problems While Undertaking Financial Assistance from

Canadians Banks

ASSISTANCE

Small Businesses in Canada Face Problems While Undertaking Financial Assistance from

Canadians Banks

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Executive Summary

Canadian Banks are greatly well capitalised in comparison to their peers existing in other nations

and are also better equipped to loan money to a worthy small organisation than they have been

over the past years.

The research question developed intended to explain various issues that are faced by the small

business organisations operating in Canada at the time of undertaking financial assistance from

the Canadian banks.

The individual interview method has been supportive in consideration to the fact that through

following non-probability convenient sampling technique, the managers, employees along with

the small business owners were involved within the interview session.

The research revealed that while the small businesses consider obtaining equity finances from

the Canadian banks they are concerned regarding challenges regarding the time and effort

needed to find the right investor for the business. The investors also tend to impose some

ownerships or controlling interest on the small businesses along with taking part in the business

decisions. This can turn out to be a concern for these Canadian small scale companies.

Based on the study findings recommendations are offered to the small businesses of Canada

regarding development of business angel network that can bring the potential investors along

with the small businesses together with additional benefits. Development of such business angel

networking might have relevant experience along with expertise that can offer advantages in

several small company situations.

Executive Summary

Canadian Banks are greatly well capitalised in comparison to their peers existing in other nations

and are also better equipped to loan money to a worthy small organisation than they have been

over the past years.

The research question developed intended to explain various issues that are faced by the small

business organisations operating in Canada at the time of undertaking financial assistance from

the Canadian banks.

The individual interview method has been supportive in consideration to the fact that through

following non-probability convenient sampling technique, the managers, employees along with

the small business owners were involved within the interview session.

The research revealed that while the small businesses consider obtaining equity finances from

the Canadian banks they are concerned regarding challenges regarding the time and effort

needed to find the right investor for the business. The investors also tend to impose some

ownerships or controlling interest on the small businesses along with taking part in the business

decisions. This can turn out to be a concern for these Canadian small scale companies.

Based on the study findings recommendations are offered to the small businesses of Canada

regarding development of business angel network that can bring the potential investors along

with the small businesses together with additional benefits. Development of such business angel

networking might have relevant experience along with expertise that can offer advantages in

several small company situations.

2PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Acknowledgement

I feel great pleasure in acknowledging the assistance along with contributions of several other

individuals in contribution to the success of the dissertation. Firstly, I would prefer to thank my

supervisor for her support, ideas along with feedbacks at the time of the proceeds in completing

this dissertation. Devoid of her support and guidance, this dissertation cannot be accomplished

within time. Finally, I would also like to express my gratitude to my peers for their total support

along with encouragement.

Acknowledgement

I feel great pleasure in acknowledging the assistance along with contributions of several other

individuals in contribution to the success of the dissertation. Firstly, I would prefer to thank my

supervisor for her support, ideas along with feedbacks at the time of the proceeds in completing

this dissertation. Devoid of her support and guidance, this dissertation cannot be accomplished

within time. Finally, I would also like to express my gratitude to my peers for their total support

along with encouragement.

3PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Table of Contents

Chapter 1: Introduction....................................................................................................................6

1.1 Research Background.......................................................................................................6

1.2. Research Problem and Significance.....................................................................................7

1.3. Research Aim and Objectives...............................................................................................8

1.4. Research Questions...............................................................................................................8

Chapter 2: Literature Review.........................................................................................................10

2.1. Introduction.........................................................................................................................10

2.2. Financial Assistances offered By Canadian Banks............................................................10

2.3. Financial Problems Dealt by Small Businesses..................................................................11

2.4. Challenges and Problems Dealt by Small Companies in Attaining Financial Assistance

from Canadian Banks................................................................................................................14

2.5. Solutions to Businesses faced while Undertaking Financial Assistance............................16

2.6. Research Gap......................................................................................................................18

2.7. Theoretical Framework and Hypotheses............................................................................19

Chapter 3: Research Methodology................................................................................................21

3.1. Introduction.........................................................................................................................21

3.2. Research Design, Philosophy and Approach......................................................................21

3.3. Participants and Data Sources............................................................................................22

3.4. Researchers Role................................................................................................................23

Table of Contents

Chapter 1: Introduction....................................................................................................................6

1.1 Research Background.......................................................................................................6

1.2. Research Problem and Significance.....................................................................................7

1.3. Research Aim and Objectives...............................................................................................8

1.4. Research Questions...............................................................................................................8

Chapter 2: Literature Review.........................................................................................................10

2.1. Introduction.........................................................................................................................10

2.2. Financial Assistances offered By Canadian Banks............................................................10

2.3. Financial Problems Dealt by Small Businesses..................................................................11

2.4. Challenges and Problems Dealt by Small Companies in Attaining Financial Assistance

from Canadian Banks................................................................................................................14

2.5. Solutions to Businesses faced while Undertaking Financial Assistance............................16

2.6. Research Gap......................................................................................................................18

2.7. Theoretical Framework and Hypotheses............................................................................19

Chapter 3: Research Methodology................................................................................................21

3.1. Introduction.........................................................................................................................21

3.2. Research Design, Philosophy and Approach......................................................................21

3.3. Participants and Data Sources............................................................................................22

3.4. Researchers Role................................................................................................................23

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

3.5. Data Gathering Techniques................................................................................................23

3.6. Data Analysis Method........................................................................................................24

3.7. Trustworthiness of the Method...........................................................................................25

3.8. Summary.............................................................................................................................25

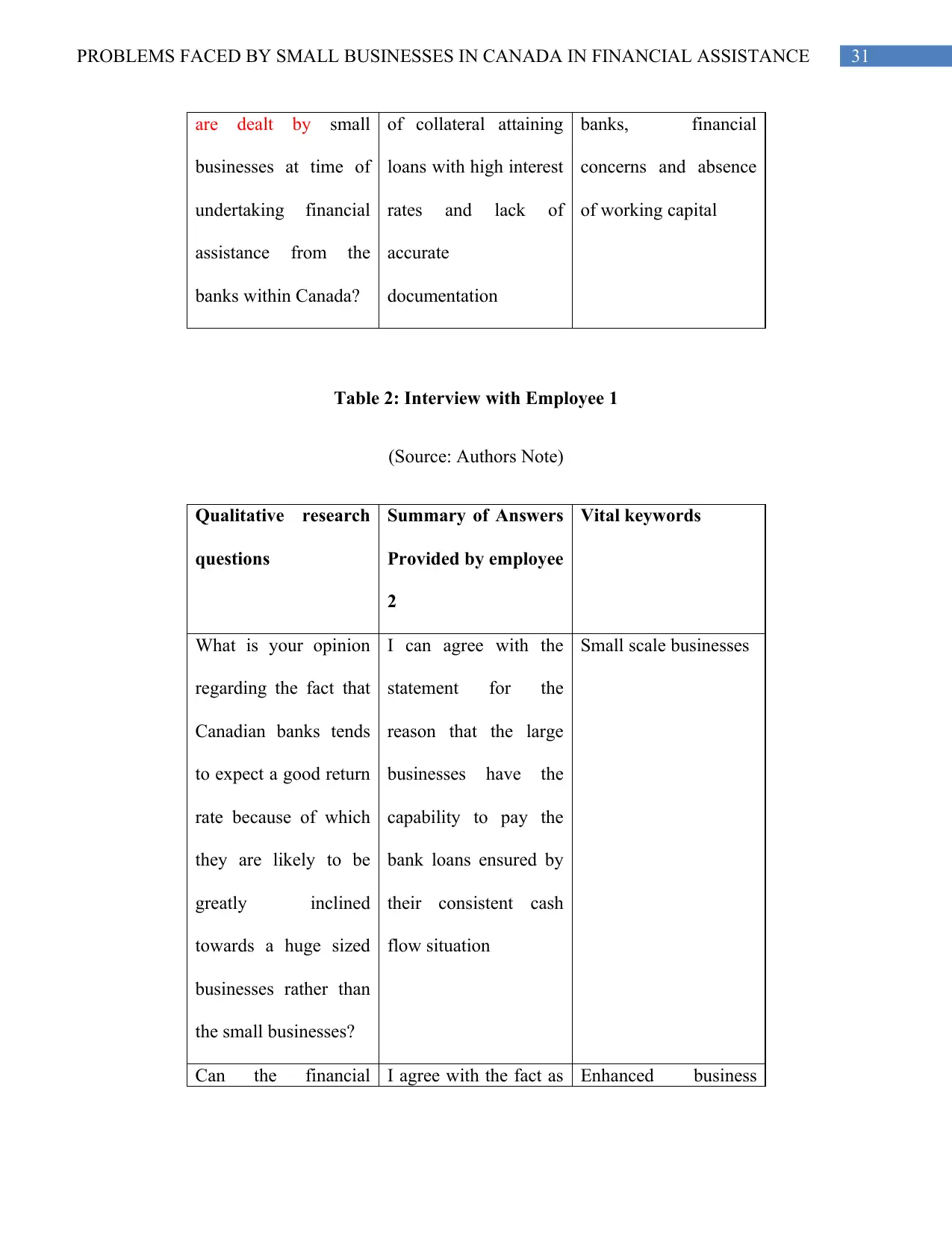

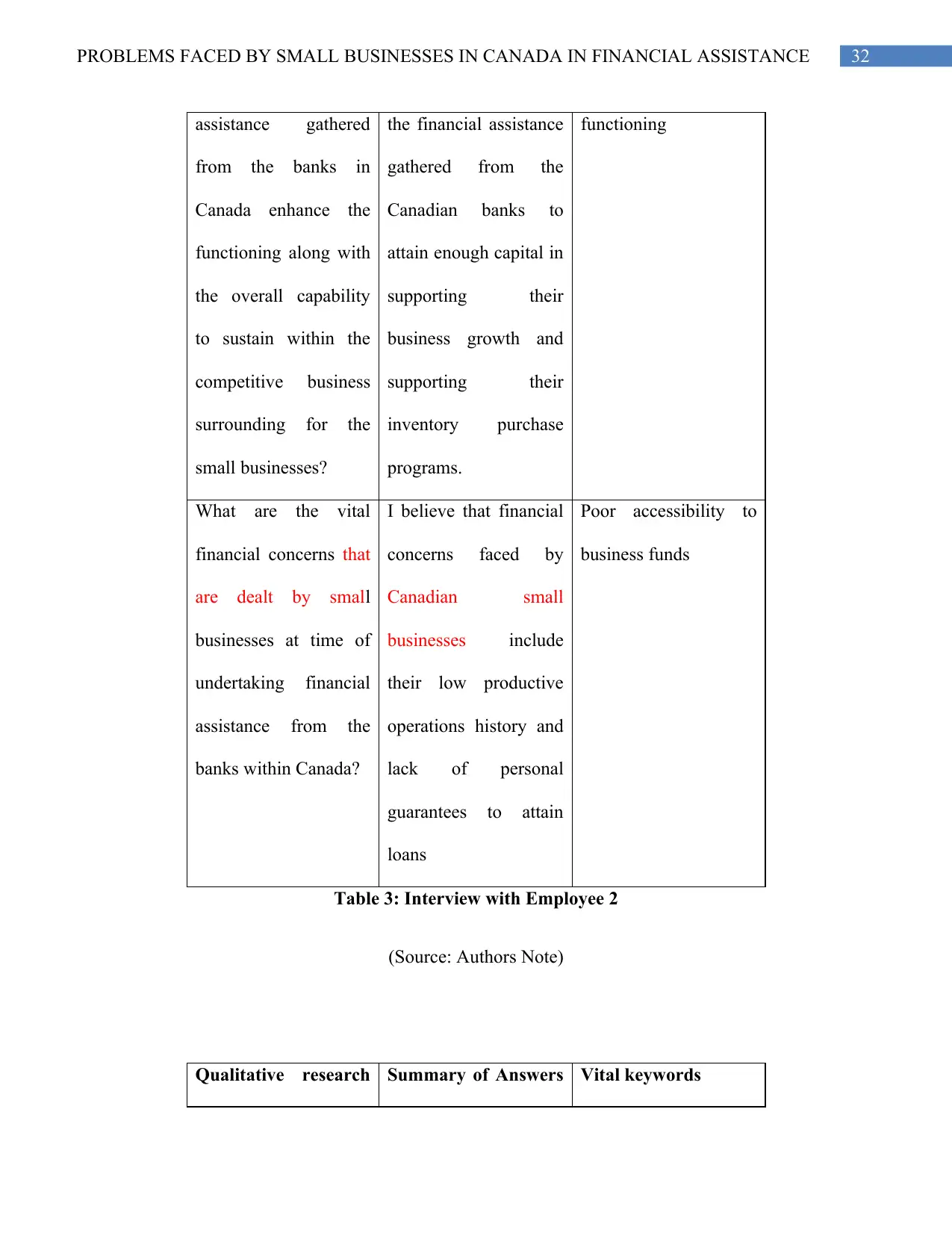

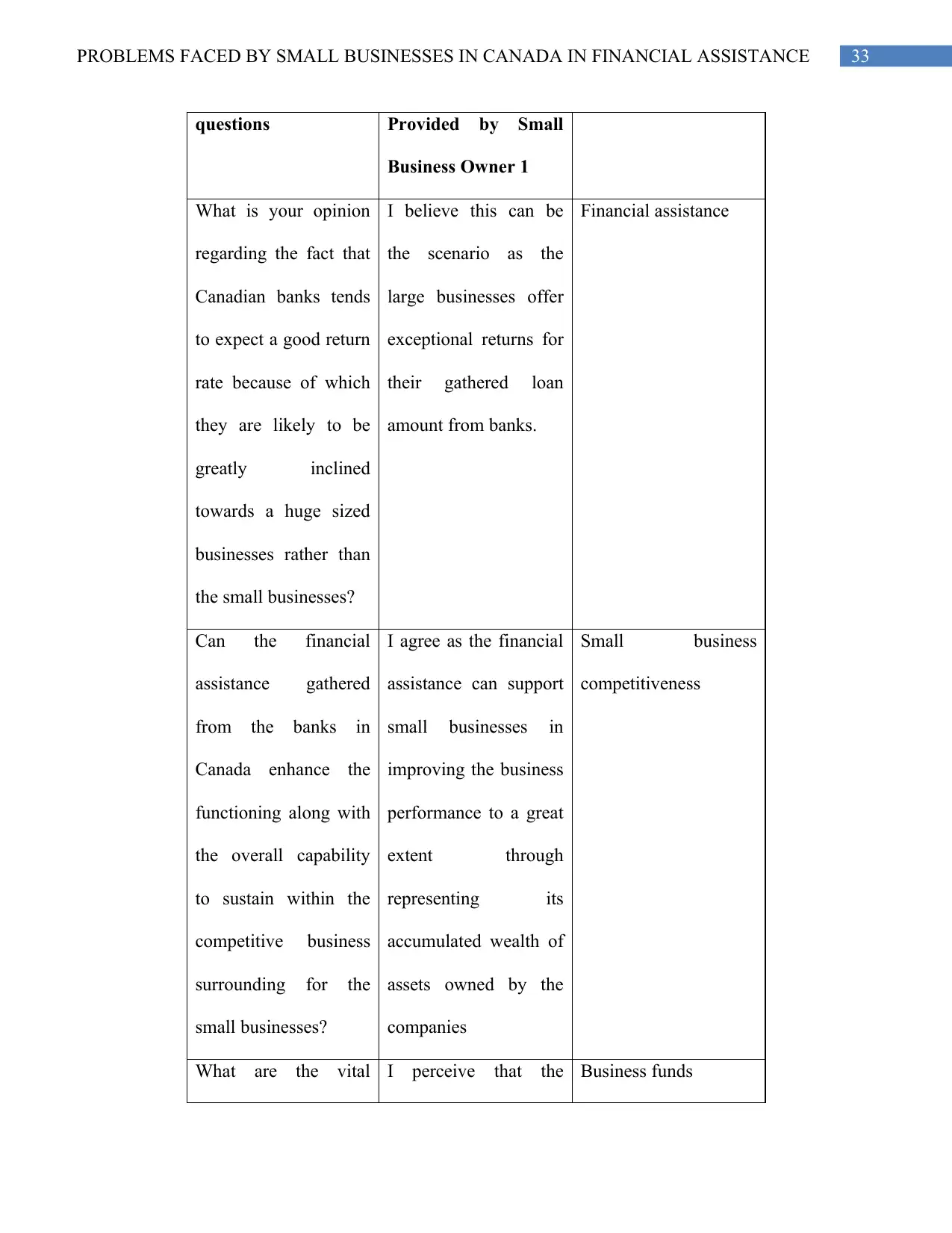

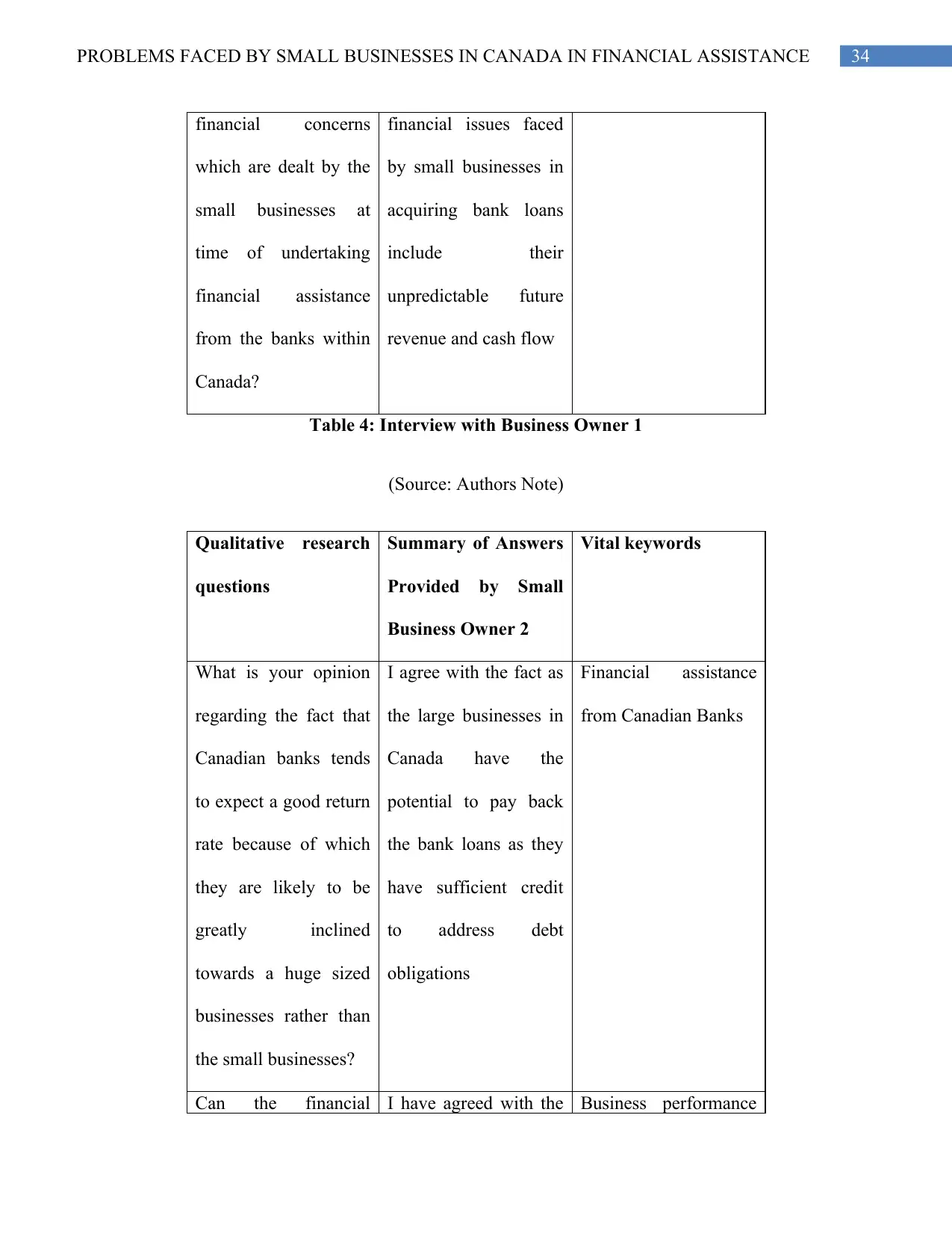

Chapter 4: Presentation of Results.................................................................................................27

4.1. Discussion of Interview with Manager...............................................................................34

4.2. Discussion of Interview with Employee 1..........................................................................34

4.3. Discussion of Interview with Employee 2..........................................................................35

4.4. Discussion of Interview with Owner 1...............................................................................35

4.5. Discussion of Interview with Owner 2...............................................................................35

Chapter 5: Analysis of Data...........................................................................................................36

5.1. Analysis of the Interview Responses Provided by Managers, Employees and Small

Business Owners on Qualitative Questions...............................................................................36

5.1.1. Response for Interview Question 1..............................................................................36

5.1.2. Response for Interview Question 2..............................................................................37

5.1.3. Response for Interview Question 3..............................................................................38

5.2. Findings on Research Question 1: What are the vital issues related with the small

businesses operations while gathering financial assistance from the banks existing within

Canada?......................................................................................................................................39

5.3. Findings on Research Question 2: What are several approaches through which such

challenges can be dealt with in order to obtain a better financial situation?.............................42

3.5. Data Gathering Techniques................................................................................................23

3.6. Data Analysis Method........................................................................................................24

3.7. Trustworthiness of the Method...........................................................................................25

3.8. Summary.............................................................................................................................25

Chapter 4: Presentation of Results.................................................................................................27

4.1. Discussion of Interview with Manager...............................................................................34

4.2. Discussion of Interview with Employee 1..........................................................................34

4.3. Discussion of Interview with Employee 2..........................................................................35

4.4. Discussion of Interview with Owner 1...............................................................................35

4.5. Discussion of Interview with Owner 2...............................................................................35

Chapter 5: Analysis of Data...........................................................................................................36

5.1. Analysis of the Interview Responses Provided by Managers, Employees and Small

Business Owners on Qualitative Questions...............................................................................36

5.1.1. Response for Interview Question 1..............................................................................36

5.1.2. Response for Interview Question 2..............................................................................37

5.1.3. Response for Interview Question 3..............................................................................38

5.2. Findings on Research Question 1: What are the vital issues related with the small

businesses operations while gathering financial assistance from the banks existing within

Canada?......................................................................................................................................39

5.3. Findings on Research Question 2: What are several approaches through which such

challenges can be dealt with in order to obtain a better financial situation?.............................42

5PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

5.4. Findings on Research Question 3: What are the likely effects of such issues that take place

at the time of attaining financial assistance from the banks within Canada?............................44

Chapter 6: Conclusion and Recommendations..............................................................................46

6.1. Conclusion..........................................................................................................................46

6.2. Recommendations and Future Research.............................................................................49

References......................................................................................................................................53

Appendices....................................................................................................................................60

Appendix 1: Ethics Application Form.......................................................................................60

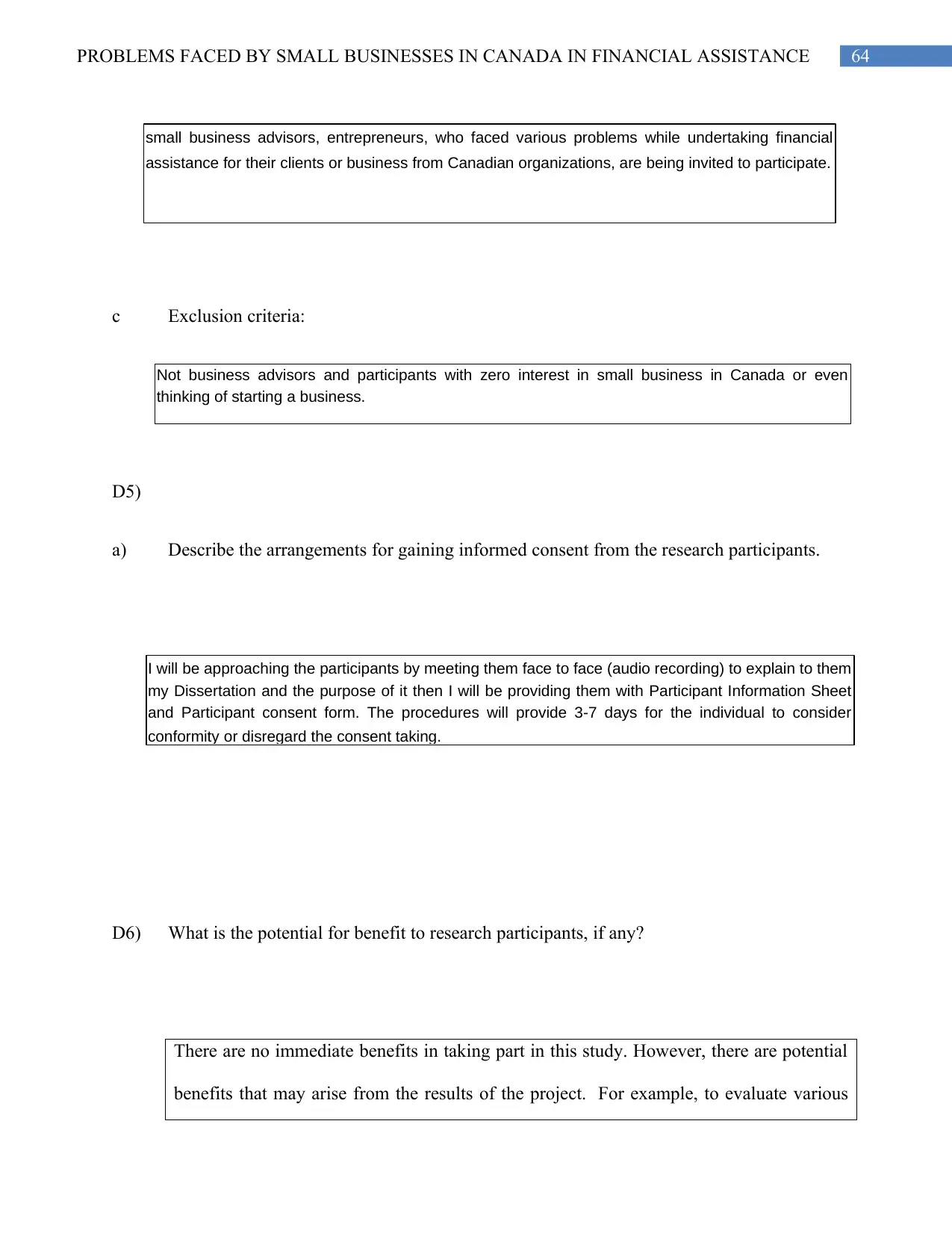

Appendix 2: Banks Offering Financial Assistance to Small and Large Businesses in Canada 63

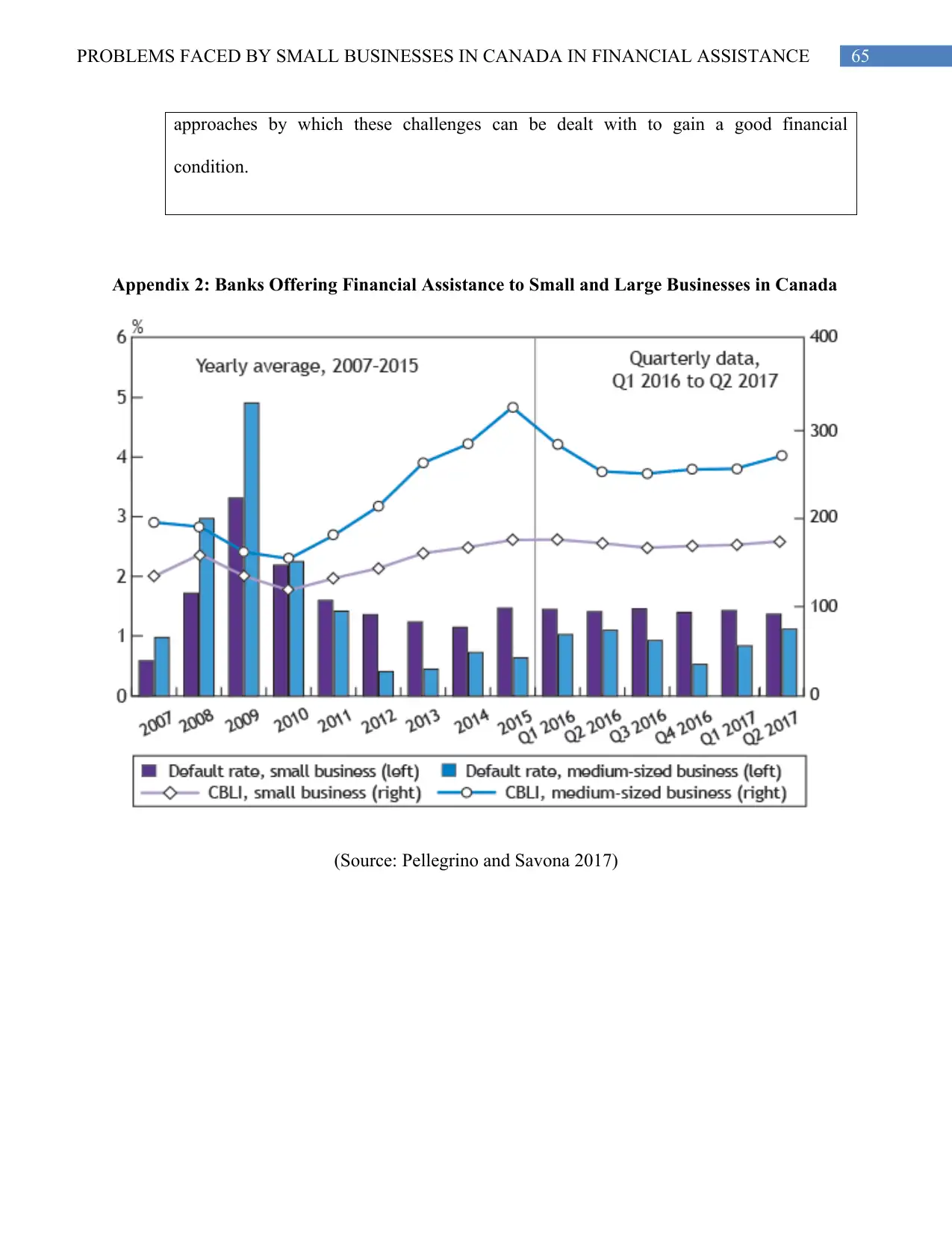

Appendix 3: Small Business Lending by Canadian Banks over Years.....................................64

Appendix 4: Interview Transcript for Manager.........................................................................64

Appendix 5: Interview Transcript for Employee 1....................................................................65

Appendix 6: Interview Transcript for Employee 2....................................................................66

Appendix 7: Interview Transcript for Owner 1.........................................................................67

Appendix 8: Interview Transcript for Owner 2.........................................................................68

5.4. Findings on Research Question 3: What are the likely effects of such issues that take place

at the time of attaining financial assistance from the banks within Canada?............................44

Chapter 6: Conclusion and Recommendations..............................................................................46

6.1. Conclusion..........................................................................................................................46

6.2. Recommendations and Future Research.............................................................................49

References......................................................................................................................................53

Appendices....................................................................................................................................60

Appendix 1: Ethics Application Form.......................................................................................60

Appendix 2: Banks Offering Financial Assistance to Small and Large Businesses in Canada 63

Appendix 3: Small Business Lending by Canadian Banks over Years.....................................64

Appendix 4: Interview Transcript for Manager.........................................................................64

Appendix 5: Interview Transcript for Employee 1....................................................................65

Appendix 6: Interview Transcript for Employee 2....................................................................66

Appendix 7: Interview Transcript for Owner 1.........................................................................67

Appendix 8: Interview Transcript for Owner 2.........................................................................68

6PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Chapter 1: Introduction

1.1 Research Background

In the era of highly competitive business environment, it has been revealed that when the

small businesses aim to address needs of a market niche, the necessary amount of capital is quite

complex to attain that can further impact the ability to undertake a project in an effective manner

(Alvesson and Sköldberg 2017). Despite the fact that the banks in Canada have offered sufficient

financial assistance through offering loans to the organisations, still there might be certain

uncertainties related with poor sourcing of credit by the smaller organizations. This can also

impact their capability to sustain within the competitive business surrounding (Bebchuk, Cohen

and Hirst 2017).Canadian Banks are greatly well capitalised in comparison to their peers existing

in other nations and are also better equipped to loan money to a worthy small organisation than

they have been over the past years (Alvesson and Sköldberg 2017). It has also been observed that

the financial position for all the Canadian small businesses is also observed to be improving.

Considering same, it has also been evident that the business insolvencies are decreased by 17%

in the year end in comparison to the previous year (Bebchuk, Cohen and Hirst 2017).More than

70% of the small business owners are evidenced to fail in their 10th year of business and around

20% of small business fail in the first year of their business surrounding (Bebchuk, Cohen and

Hirst 2017). Certain small businesses in Canada are likely to face difficulties whole seeking

funds from the banks existing within Canada. This is evident for the reason that while the

established businesses find it to be considerably simple to raise finance, the small companies

operating within Canada find it greatly difficult in raising finance for all their operational

activities. For instance, consumer service applications such as Zebdesk faced the issue of initial

Chapter 1: Introduction

1.1 Research Background

In the era of highly competitive business environment, it has been revealed that when the

small businesses aim to address needs of a market niche, the necessary amount of capital is quite

complex to attain that can further impact the ability to undertake a project in an effective manner

(Alvesson and Sköldberg 2017). Despite the fact that the banks in Canada have offered sufficient

financial assistance through offering loans to the organisations, still there might be certain

uncertainties related with poor sourcing of credit by the smaller organizations. This can also

impact their capability to sustain within the competitive business surrounding (Bebchuk, Cohen

and Hirst 2017).Canadian Banks are greatly well capitalised in comparison to their peers existing

in other nations and are also better equipped to loan money to a worthy small organisation than

they have been over the past years (Alvesson and Sköldberg 2017). It has also been observed that

the financial position for all the Canadian small businesses is also observed to be improving.

Considering same, it has also been evident that the business insolvencies are decreased by 17%

in the year end in comparison to the previous year (Bebchuk, Cohen and Hirst 2017).More than

70% of the small business owners are evidenced to fail in their 10th year of business and around

20% of small business fail in the first year of their business surrounding (Bebchuk, Cohen and

Hirst 2017). Certain small businesses in Canada are likely to face difficulties whole seeking

funds from the banks existing within Canada. This is evident for the reason that while the

established businesses find it to be considerably simple to raise finance, the small companies

operating within Canada find it greatly difficult in raising finance for all their operational

activities. For instance, consumer service applications such as Zebdesk faced the issue of initial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

undercapitalisation. There are several factors that are responsible for the financial problems

faced by the small businesses in their attempt to raise finance that includes risk, lack of credit

sourcing, absence of enough press coverage, intertwined position, maturity along with interest

rated bias (Becherer and Helms 2016). Certain issues related with equity finance such as absence

of market trust, equity space and absence of exit route causes problems for the small businesses

to attain adequate finds for their business operations for the Canadian banks (Bresler. and Stake

2017). The study is intended to analysevarious issues that are faced by the small business

organisations operating in Canada at the time of undertaking financial support from Canadian

banks.

1.2. Research Problem and Significance

The research subject was analysed because of the associated advantages that can be

obtained from the small businesses along with the overall industry. This research has

significance in identifying several issues which can take place at the time of attaining financial

assistance in the form of loans and financial advices from the banks existing within

Canada(Brigham, Nason and Gessaroli 2016). However, these banks in Canada offer financial

support to large as well as small businesses with the objective of attaining a huge amount of

interest and profit from them. Focused on such research problem, the research has increased

significance in analysing several concerns related with the management of financial support from

the Canadian banks (Brigham, Ehrhardt, Nason and Gessaroli 2016). This can also therefore

enable all the precautionary measures in dealing with the issues faced at the time of gathering

financial support from the banks operating within Canada.

The significance of the research subject is to attain the study objectives of knowledge

acquisition and with the objective of developing solutions required to deal with the financial

undercapitalisation. There are several factors that are responsible for the financial problems

faced by the small businesses in their attempt to raise finance that includes risk, lack of credit

sourcing, absence of enough press coverage, intertwined position, maturity along with interest

rated bias (Becherer and Helms 2016). Certain issues related with equity finance such as absence

of market trust, equity space and absence of exit route causes problems for the small businesses

to attain adequate finds for their business operations for the Canadian banks (Bresler. and Stake

2017). The study is intended to analysevarious issues that are faced by the small business

organisations operating in Canada at the time of undertaking financial support from Canadian

banks.

1.2. Research Problem and Significance

The research subject was analysed because of the associated advantages that can be

obtained from the small businesses along with the overall industry. This research has

significance in identifying several issues which can take place at the time of attaining financial

assistance in the form of loans and financial advices from the banks existing within

Canada(Brigham, Nason and Gessaroli 2016). However, these banks in Canada offer financial

support to large as well as small businesses with the objective of attaining a huge amount of

interest and profit from them. Focused on such research problem, the research has increased

significance in analysing several concerns related with the management of financial support from

the Canadian banks (Brigham, Ehrhardt, Nason and Gessaroli 2016). This can also therefore

enable all the precautionary measures in dealing with the issues faced at the time of gathering

financial support from the banks operating within Canada.

The significance of the research subject is to attain the study objectives of knowledge

acquisition and with the objective of developing solutions required to deal with the financial

8PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

concerns which might be faced by the small businesses at the time of attaining help from the

banks within Canada. In consideration to the financial concerns dealt by the small businesses, it

is vital to take into consideration that there are several important aspects necessary in facilitating

better contributions to the research related factors. Furthermore, the current research is also

focused on recommending solutions for addressing the financial needs of the small businesses.

1.3. Research Aim and Objectives

The aim of the current study is to evaluate major challenges dealt by small business

organisations while taking financial support from Canadian banks. The research objectives that

will be attained after completion of the study are indicated under:

To recognise range of vital issues elated with the small businesses operations while

gathering financial support from the banks existing within Canada

To analyse several approaches through which such challenges can be dealt with in order

ensure better financial situation

To evaluate effects of issues that taking place at the time of attaining financial assistance

from the banks within Canada

To recommend important measures in dealing with issues taking place at the time of

taking financial assistance from the banks in Canada.

1.4. Research Questions

The research questions to be answered by successful accomplishment of the research are

formulated below:

What are the vital issues related with the small businesses operations while gathering

financial assistance from the banks existing within Canada?

concerns which might be faced by the small businesses at the time of attaining help from the

banks within Canada. In consideration to the financial concerns dealt by the small businesses, it

is vital to take into consideration that there are several important aspects necessary in facilitating

better contributions to the research related factors. Furthermore, the current research is also

focused on recommending solutions for addressing the financial needs of the small businesses.

1.3. Research Aim and Objectives

The aim of the current study is to evaluate major challenges dealt by small business

organisations while taking financial support from Canadian banks. The research objectives that

will be attained after completion of the study are indicated under:

To recognise range of vital issues elated with the small businesses operations while

gathering financial support from the banks existing within Canada

To analyse several approaches through which such challenges can be dealt with in order

ensure better financial situation

To evaluate effects of issues that taking place at the time of attaining financial assistance

from the banks within Canada

To recommend important measures in dealing with issues taking place at the time of

taking financial assistance from the banks in Canada.

1.4. Research Questions

The research questions to be answered by successful accomplishment of the research are

formulated below:

What are the vital issues related with the small businesses operations while gathering

financial assistance from the banks existing within Canada?

9PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

What are several approaches through which such challenges can be dealt with in attaining

better financial position?

What are likely effects of such issues that take place at the time of attaining financial

assistance from the banks within Canada?

What are recommended measures in dealing with issues taking place at the time of taking

financial support from the Canadian banks?

What are several approaches through which such challenges can be dealt with in attaining

better financial position?

What are likely effects of such issues that take place at the time of attaining financial

assistance from the banks within Canada?

What are recommended measures in dealing with issues taking place at the time of taking

financial support from the Canadian banks?

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Chapter 2: Literature Review

2.1. Introduction

The literature review chapter considered analysis and existing arguments in the past

researches on research subject that analysed the challenges faced by small businesses in Canada

in obtaining financial assistance from the banks existing within Canada (Calomiris and Haber

2015). This chapter also focussed on analysing the findings from various past researches

regarding financial assistance offered by the Canadian banks, financial funds attainment

problems faced by them from domestic banks and solutions offered to businesses by several

researchers on best ways to attain funds for their small businesses.

2.2. Financial Assistances offered By Canadian Banks

Campbell and Cartwright (2017) revealed in their research that business owners in

Canada generally report that attaining enough financing for their businesses turns out to be

highly challenging factor of operating business. There are several government as well as private

sector financing sources existing within Canada that can facilitate large and small businesses to

develop their businesses. This can include business loans, capital, indigenous entrepreneur loan,

new Canadian entrepreneur loan, small businesses loan for existing companies, start-up

financing, farm credit Canada for various loans and lending options and the agricultural loans act

program (Campbell 2017). Campbell and Cartwright (2017) stated that the large and small

businesses of Canada also have access to private setup financing for their business operations.

For instance, Canada’s major financial institutions like the banks, cooperatives and the credit

unions. Based on the type of businesses these companies intend to start, they have the access to

secure venture capital or financing from the Canadian angel investors. Campbell (2017) added

Chapter 2: Literature Review

2.1. Introduction

The literature review chapter considered analysis and existing arguments in the past

researches on research subject that analysed the challenges faced by small businesses in Canada

in obtaining financial assistance from the banks existing within Canada (Calomiris and Haber

2015). This chapter also focussed on analysing the findings from various past researches

regarding financial assistance offered by the Canadian banks, financial funds attainment

problems faced by them from domestic banks and solutions offered to businesses by several

researchers on best ways to attain funds for their small businesses.

2.2. Financial Assistances offered By Canadian Banks

Campbell and Cartwright (2017) revealed in their research that business owners in

Canada generally report that attaining enough financing for their businesses turns out to be

highly challenging factor of operating business. There are several government as well as private

sector financing sources existing within Canada that can facilitate large and small businesses to

develop their businesses. This can include business loans, capital, indigenous entrepreneur loan,

new Canadian entrepreneur loan, small businesses loan for existing companies, start-up

financing, farm credit Canada for various loans and lending options and the agricultural loans act

program (Campbell 2017). Campbell and Cartwright (2017) stated that the large and small

businesses of Canada also have access to private setup financing for their business operations.

For instance, Canada’s major financial institutions like the banks, cooperatives and the credit

unions. Based on the type of businesses these companies intend to start, they have the access to

secure venture capital or financing from the Canadian angel investors. Campbell (2017) added

11PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

that certain other sources of the private sector financing can be in debt and equity financing form

available from the financing institutions for addressing business needs of the small and large

businesses in Canada. The researcher also revealed that before attaining any financial assistance

or loan from the Canadian banks, the banker evaluate whether the small or large scale

organization represents an acceptable risk for the and whether will be capable to pay off their

obligations against the loan. Such risk assessment carried out by the Canadian banks also

impacts the rate of interest the companies pay on loan (Crane et al. 2019).

Cunningham, Gök and Larédo (2016) explained that it also determines whether the

business will get their desired financial assistances or loan along with the lending terms and

conditions. A banker of the Canadian financial institutions will be quite hesitant in lending

financial assistance in case the organisations assets along with performance signifies as

inacceptable risk level. Once the loans get approved by the Canadian financial institutions they

consider carrying out yearly reviews in order to attract the loan's performance in a situation

where the loan performance on a Canadian business risk turns out to be unacceptable, the

bankers are likely to demand for any additional collateral security or demand complete

repayment.

2.3. Financial Problems Dealt by Small Businesses

As indicated within the research of Dumay and Cai (2015) it was gathered that small

business companies operate with a promise and in a situation the leader or manager of the

company has a sound mission and vision then the activities turn out to be simpler. This further

promotes innovation along with suitable project management techniques. These researchers also

confirmed that in order to ensure management of an exceptional fraction of working capital

along with enough financial resources, the small businesses requires to secure the initial funding

that certain other sources of the private sector financing can be in debt and equity financing form

available from the financing institutions for addressing business needs of the small and large

businesses in Canada. The researcher also revealed that before attaining any financial assistance

or loan from the Canadian banks, the banker evaluate whether the small or large scale

organization represents an acceptable risk for the and whether will be capable to pay off their

obligations against the loan. Such risk assessment carried out by the Canadian banks also

impacts the rate of interest the companies pay on loan (Crane et al. 2019).

Cunningham, Gök and Larédo (2016) explained that it also determines whether the

business will get their desired financial assistances or loan along with the lending terms and

conditions. A banker of the Canadian financial institutions will be quite hesitant in lending

financial assistance in case the organisations assets along with performance signifies as

inacceptable risk level. Once the loans get approved by the Canadian financial institutions they

consider carrying out yearly reviews in order to attract the loan's performance in a situation

where the loan performance on a Canadian business risk turns out to be unacceptable, the

bankers are likely to demand for any additional collateral security or demand complete

repayment.

2.3. Financial Problems Dealt by Small Businesses

As indicated within the research of Dumay and Cai (2015) it was gathered that small

business companies operate with a promise and in a situation the leader or manager of the

company has a sound mission and vision then the activities turn out to be simpler. This further

promotes innovation along with suitable project management techniques. These researchers also

confirmed that in order to ensure management of an exceptional fraction of working capital

along with enough financial resources, the small businesses requires to secure the initial funding

12PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

and along with that must also consider carrying out proper planning in preventing the unexpected

expenses and ensuring prevention of any delay which might be faced in management of the

business.

Researchers namely, Engert and Fung (2017) has also explained that there are certain

major concerns dealt by the small businesses with an intention of attaining growth or expansion

which has further increased difficulty in securing the business funding. These researchers also

indicated that just implementing such idea might not be highly efficient in ensuring success. Past

researches also revealed that absence of suitable planning might result in certain difficulties for

all the small businesses in attaining support for obtaining start-up costs operations cost, tax along

with expenditures related with the emergency conditions.Eniola and Entebang (2015) also

provided an argument that there are several concerns that take place in the form of unexpected

expenditures which are not taken into consideration which might also have resulted in numerous

complexities at the time of bill payments and development of payroll. These researchers also

confirmed that the small businesses face the difficulties related with offering a huge amount of

wages and other benefits to all their employees which that can further result in increased

financial stress which can negatively affect the performance of the employees.

Moreover, research conducted by Erbenova et al. (2016) revealed that small businesses in

Canada are at an increased disadvantageous situation in comparison to the larger and established

organisations in the nation. It has also been revealed that 29% of the small businesses in Canada

fail because they eventually run out of capital and such findings confirm that access to the right

funding solution is vital in ensuring successful business growth (Fraser, Bhaumik, and Wright

2015). Glover and Kusterer (2016) added that attaining financial assistance from alternative

lenders in Canada mean having to pay an increased rate of interest that can cause financial

and along with that must also consider carrying out proper planning in preventing the unexpected

expenses and ensuring prevention of any delay which might be faced in management of the

business.

Researchers namely, Engert and Fung (2017) has also explained that there are certain

major concerns dealt by the small businesses with an intention of attaining growth or expansion

which has further increased difficulty in securing the business funding. These researchers also

indicated that just implementing such idea might not be highly efficient in ensuring success. Past

researches also revealed that absence of suitable planning might result in certain difficulties for

all the small businesses in attaining support for obtaining start-up costs operations cost, tax along

with expenditures related with the emergency conditions.Eniola and Entebang (2015) also

provided an argument that there are several concerns that take place in the form of unexpected

expenditures which are not taken into consideration which might also have resulted in numerous

complexities at the time of bill payments and development of payroll. These researchers also

confirmed that the small businesses face the difficulties related with offering a huge amount of

wages and other benefits to all their employees which that can further result in increased

financial stress which can negatively affect the performance of the employees.

Moreover, research conducted by Erbenova et al. (2016) revealed that small businesses in

Canada are at an increased disadvantageous situation in comparison to the larger and established

organisations in the nation. It has also been revealed that 29% of the small businesses in Canada

fail because they eventually run out of capital and such findings confirm that access to the right

funding solution is vital in ensuring successful business growth (Fraser, Bhaumik, and Wright

2015). Glover and Kusterer (2016) added that attaining financial assistance from alternative

lenders in Canada mean having to pay an increased rate of interest that can cause financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

concerns for the companies in supporting business operations smoothly. Another financial

problem that is observed to be faced by small businesses in operating profitable business in

Canada is debt repayment as many small business owners lack enough capital to establish their

businesses. These researchers also explained that in order to address such financial problems, the

small businesses look for traditional loan options or alternative financing solutions. Kusterer

(2016) conformed that as the small business is new to the market it is difficult for them to

determine the performance of their products and services within the market. Even if the company

has high potential, sales are quite slow in the initial months of their operations. For this reason

the small business owners in Canada might find themselves to be struggling in ensuring debt

repayment as these companies strive to maintain their market stability (Tucker 2016).

Research carried out by Goldberg et al. (2017) confirmed that the small businesses in

Canada face issues related with day-to-day money management as just 40% of these companies

perceive that they are knowledgeable on finance. Lack of knowledge regarding the effective

ways to ensure money management increases difficulty for the business owners in attaining

financial assistance or funds from the Canadian banks. These researchers also revealed that the

Canadian small businesses lack experience related with managing invoices, receipts along with

maintaining track of expenses which results in delayed payments, inaccurate calculation and

incorrect recordings. Moreover, in the study of Goss (2015) it was evidenced that over the years,

small business owners in Canada licensed access to business funds as one of their greatest

concerns indicating doubts regarding the future success of the business. While it is not deemed to

be government’s responsibility to ensure small business success, it is deemed to be their

accountability to ensure that innovative and the growing small scale companies attain necessary

capital access along with suitable infrastructure which can accelerate their company’s growth.

concerns for the companies in supporting business operations smoothly. Another financial

problem that is observed to be faced by small businesses in operating profitable business in

Canada is debt repayment as many small business owners lack enough capital to establish their

businesses. These researchers also explained that in order to address such financial problems, the

small businesses look for traditional loan options or alternative financing solutions. Kusterer

(2016) conformed that as the small business is new to the market it is difficult for them to

determine the performance of their products and services within the market. Even if the company

has high potential, sales are quite slow in the initial months of their operations. For this reason

the small business owners in Canada might find themselves to be struggling in ensuring debt

repayment as these companies strive to maintain their market stability (Tucker 2016).

Research carried out by Goldberg et al. (2017) confirmed that the small businesses in

Canada face issues related with day-to-day money management as just 40% of these companies

perceive that they are knowledgeable on finance. Lack of knowledge regarding the effective

ways to ensure money management increases difficulty for the business owners in attaining

financial assistance or funds from the Canadian banks. These researchers also revealed that the

Canadian small businesses lack experience related with managing invoices, receipts along with

maintaining track of expenses which results in delayed payments, inaccurate calculation and

incorrect recordings. Moreover, in the study of Goss (2015) it was evidenced that over the years,

small business owners in Canada licensed access to business funds as one of their greatest

concerns indicating doubts regarding the future success of the business. While it is not deemed to

be government’s responsibility to ensure small business success, it is deemed to be their

accountability to ensure that innovative and the growing small scale companies attain necessary

capital access along with suitable infrastructure which can accelerate their company’s growth.

14PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Gozzi and Schmukler (2016) added that several small businesses of Canada particularly

belonging to the advanced sectors such as agriculture, manufacturing and food processing tends

to overlook several beneficial funding opportunities that are assessable by means of prudential as

well as federal government levels. It has also been confirmed that a small scale business which is

determined to address obstacles in future business growth focuses on leveraging the government

loans and grants as an attempt of obtaining successful financial assistance (He et al. 2017). To

deal with the financial problems faced by these small businesses, several small business loans

and grants programs are present which supports these small scale companies to expand and take

part in activities that are gathered to enhance global competitiveness.

2.4. Challenges and Problems Dealt by Small Companies in Attaining Financial Assistance

from Canadian Banks

As explained by the Hillary (2017), in order to deal with the financial concerns,

managing suitable budgeting activities along with ensuing maintenance of better financial

situation, the small businesses often wanted financial support along with assistance from the

banks existing within Canada. The financial aspects are deemed to be the lifeline of the small

businesses and for this reason the dent along with the equity finance are deemed to be vital

sources of finance employed by the organisation. IbnBoamah and Alam (2016) stated that at the

time of seeking the financial assistance the vital concerns faced by the small business companies

within Canada also encompass uncertainties taking place from the poor accessibility to the

necessary funds for managing the expansion of business. These researchers also highlighted that

absence of suitable credit scoring is one of vital concerns which is generally neglected by the

small businesses. In addition, this also leads to the uncertainties which makes the banks within

Gozzi and Schmukler (2016) added that several small businesses of Canada particularly

belonging to the advanced sectors such as agriculture, manufacturing and food processing tends

to overlook several beneficial funding opportunities that are assessable by means of prudential as

well as federal government levels. It has also been confirmed that a small scale business which is

determined to address obstacles in future business growth focuses on leveraging the government

loans and grants as an attempt of obtaining successful financial assistance (He et al. 2017). To

deal with the financial problems faced by these small businesses, several small business loans

and grants programs are present which supports these small scale companies to expand and take

part in activities that are gathered to enhance global competitiveness.

2.4. Challenges and Problems Dealt by Small Companies in Attaining Financial Assistance

from Canadian Banks

As explained by the Hillary (2017), in order to deal with the financial concerns,

managing suitable budgeting activities along with ensuing maintenance of better financial

situation, the small businesses often wanted financial support along with assistance from the

banks existing within Canada. The financial aspects are deemed to be the lifeline of the small

businesses and for this reason the dent along with the equity finance are deemed to be vital

sources of finance employed by the organisation. IbnBoamah and Alam (2016) stated that at the

time of seeking the financial assistance the vital concerns faced by the small business companies

within Canada also encompass uncertainties taking place from the poor accessibility to the

necessary funds for managing the expansion of business. These researchers also highlighted that

absence of suitable credit scoring is one of vital concerns which is generally neglected by the

small businesses. In addition, this also leads to the uncertainties which makes the banks within

15PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Canada requires all its important consumers to deliver a suitable credit scoring relied on the

decisions made for managing the exposures.

Research carried out by Johnson (2018) clarified that the banks in Canada are not that

much interested to improve the credit facility devoid of making any suitable estimation of certain

collateral increment from the small business perspective that might not be ready to make any

increment thereafter. There are certain concerns like the maturity gap that have taken place

because of the difference among the small businesses and the Canadian banks in consideration to

the maturity if assets and liabilities. Kariv and Coleman (2015) added to this fact and stated that

the small businesses in Canada dealt with issues and challenges related with attaining short and

medium term loans that further resulted in attaining the loans which were not secured by means

of mortgages against their property. These researchers also revealed that as the banks in Canada

attains a better return rate for the loans granted by them, the banks are likely to set an increased

rate to obtain personal guarantee from these small business owners while such rate of interest is

quite low fir the larger organisations operating in Canada. Kochenkova, Grimaldi and Munari

(2016) revealed that the stock market in Canada might also not have an exceptional confidence

on the operations of the small businesses that can also lead to decreased value creation along

with increasing several issues and complexities for them while acquiring equity finance.

Based on the finding of Lee, Wall and Kovacs (2015) it has been observed in a survey

press that maximum number of people perceived the fact that certain absence of the financing

options tuned out to be among the major challenge that is greatly faced by all the small

businesses operating in Canada. Multiple issues related with attaining financial assistance from

Canadian banks are diverse and also encompass the factors that combine for take form of a

financial management long with condition of the small business. These researchers also revealed

Canada requires all its important consumers to deliver a suitable credit scoring relied on the

decisions made for managing the exposures.

Research carried out by Johnson (2018) clarified that the banks in Canada are not that

much interested to improve the credit facility devoid of making any suitable estimation of certain

collateral increment from the small business perspective that might not be ready to make any

increment thereafter. There are certain concerns like the maturity gap that have taken place

because of the difference among the small businesses and the Canadian banks in consideration to

the maturity if assets and liabilities. Kariv and Coleman (2015) added to this fact and stated that

the small businesses in Canada dealt with issues and challenges related with attaining short and

medium term loans that further resulted in attaining the loans which were not secured by means

of mortgages against their property. These researchers also revealed that as the banks in Canada

attains a better return rate for the loans granted by them, the banks are likely to set an increased

rate to obtain personal guarantee from these small business owners while such rate of interest is

quite low fir the larger organisations operating in Canada. Kochenkova, Grimaldi and Munari

(2016) revealed that the stock market in Canada might also not have an exceptional confidence

on the operations of the small businesses that can also lead to decreased value creation along

with increasing several issues and complexities for them while acquiring equity finance.

Based on the finding of Lee, Wall and Kovacs (2015) it has been observed in a survey

press that maximum number of people perceived the fact that certain absence of the financing

options tuned out to be among the major challenge that is greatly faced by all the small

businesses operating in Canada. Multiple issues related with attaining financial assistance from

Canadian banks are diverse and also encompass the factors that combine for take form of a

financial management long with condition of the small business. These researchers also revealed

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

that such financial assistance issues were majorly dealt with for the reason that the small

businesses attempted to acquire bank financing at the time of the recession. Mason, Botelho and

Harrison (2016) revealed that in order to derive better solutions and ensuring addressing such

issues in a better manner, the Government of Canada has also introduced certain effective new

loan guarantee schemes that have the capability to deal with such financing situations. Moreover,

it can also ensure creation of broad opportunities for small businesses operating within Canada to

attain financial assistance devoid of any hurdles.

It has also been argued by Massaro et al. (2016) that there are certain major concerns that

has affected the small businesses of Canada to obtain financial assistance from the banks within

Canada included existence of poor amount of collateral, absence of maintaining better track

records long with maintainable of poor return rate offered to the banks by small businesses in

comparison to large business companies. Researchers namely McCann and Ortega-Argilés

(2016) indicated that the small businesses operating within Canada generally deal with certain

other issues that include facing a higher interest rate, slow payment, extra charges from banks as

well as poor financing. According to the research carried out by Owen and Mason (2017) it has

been revealed that the Canadian banks are likely to treat the businesses distinctly relied on the

sizes due to a good return rate which can be attained by the large businesses that is even more in

comparison to the smaller businesses. Such concerns related with gathering financial assistance

from Canadian banks takes place from poor services, strict terms of payment and conditions

from the suppliers along with extremely high pressure on the prices and slower payment given

by the consumers within Canada.

that such financial assistance issues were majorly dealt with for the reason that the small

businesses attempted to acquire bank financing at the time of the recession. Mason, Botelho and

Harrison (2016) revealed that in order to derive better solutions and ensuring addressing such

issues in a better manner, the Government of Canada has also introduced certain effective new

loan guarantee schemes that have the capability to deal with such financing situations. Moreover,

it can also ensure creation of broad opportunities for small businesses operating within Canada to

attain financial assistance devoid of any hurdles.

It has also been argued by Massaro et al. (2016) that there are certain major concerns that

has affected the small businesses of Canada to obtain financial assistance from the banks within

Canada included existence of poor amount of collateral, absence of maintaining better track

records long with maintainable of poor return rate offered to the banks by small businesses in

comparison to large business companies. Researchers namely McCann and Ortega-Argilés

(2016) indicated that the small businesses operating within Canada generally deal with certain

other issues that include facing a higher interest rate, slow payment, extra charges from banks as

well as poor financing. According to the research carried out by Owen and Mason (2017) it has

been revealed that the Canadian banks are likely to treat the businesses distinctly relied on the

sizes due to a good return rate which can be attained by the large businesses that is even more in

comparison to the smaller businesses. Such concerns related with gathering financial assistance

from Canadian banks takes place from poor services, strict terms of payment and conditions

from the suppliers along with extremely high pressure on the prices and slower payment given

by the consumers within Canada.

17PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

2.5. Solutions to Businesses faced while Undertaking Financial Assistance

Based on the research carried out by Paschen (2017) it has been elucidated that in order

to improve the business performance of small companies solutions are needed against several

obligations along with concerns related with the financial issues and problems dealt with at the

time of undertaking financial assistance from the Canadian banks. The major causes encompass

insufficient capital or absence of capitalisation or even other issues related with the business

financing. For instance, SBA or Small Business Association makes an effort in analysing and

revealing certain factors related with the causes of financial issues with great focus on poor

capital structure, sense of reserve funding and the issue of overspending. Pellegrino and Savona

(2017) explained in their research that the SBA is capable of offering better assistance as well as

help in the financial advice form to the owners as well as the small businesses and then

considering making certain strategic plans in better management of the small businesses easily.

At the same time it is also beneficial to attain advantages from the resources the financial as well

as the human resources for addressing the small and the medium sized business’s needs. This

might also turn out to be efficient for making the funding attained from Canadian banks to get

extended that can also ensure small business within the nation is acquiring adequate working

capital in order to sustain within a competitive business surrounding.

In contrast, researchers namely Peters and Panayi (2016) indicated that dealing with the

financial issues can turn out to be advantageous for reviewing, analyses, revamping as well as for

the purpose of carrying out research prior to the development of the business plan for the

businesses that are generally small sized while gathering financial assistance from the banks that

particularly operate within Canada. In certain situations where the expenses experienced by the

organisation and the business plan of the company are not that efficient than the small businesses

2.5. Solutions to Businesses faced while Undertaking Financial Assistance

Based on the research carried out by Paschen (2017) it has been elucidated that in order

to improve the business performance of small companies solutions are needed against several

obligations along with concerns related with the financial issues and problems dealt with at the

time of undertaking financial assistance from the Canadian banks. The major causes encompass

insufficient capital or absence of capitalisation or even other issues related with the business

financing. For instance, SBA or Small Business Association makes an effort in analysing and

revealing certain factors related with the causes of financial issues with great focus on poor

capital structure, sense of reserve funding and the issue of overspending. Pellegrino and Savona

(2017) explained in their research that the SBA is capable of offering better assistance as well as

help in the financial advice form to the owners as well as the small businesses and then

considering making certain strategic plans in better management of the small businesses easily.

At the same time it is also beneficial to attain advantages from the resources the financial as well

as the human resources for addressing the small and the medium sized business’s needs. This

might also turn out to be efficient for making the funding attained from Canadian banks to get

extended that can also ensure small business within the nation is acquiring adequate working

capital in order to sustain within a competitive business surrounding.

In contrast, researchers namely Peters and Panayi (2016) indicated that dealing with the

financial issues can turn out to be advantageous for reviewing, analyses, revamping as well as for

the purpose of carrying out research prior to the development of the business plan for the

businesses that are generally small sized while gathering financial assistance from the banks that

particularly operate within Canada. In certain situations where the expenses experienced by the

organisation and the business plan of the company are not that efficient than the small businesses

18PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

feel the need to implement certain changes that further allows the business owners to attain high

loans with great ease along with attaining certain grant which have been developed for offering

these businesses with great opportunities of growth. Pilbeam (2018) elucidated that the small

business owners within Canada can play a great role in the training seminars as well as within

the developmental sessions in order to offer better financial assistance. Whereas, the angel

invests and the venture capitalists are offered with exceptional roles and responsibilities of

accepting risks and offering funding support to all owners of small business in sustaining the

consistency in the regular operations of the businesses processes and operations.

Quarter, Mook and Armstrong (2017) stated that this is deemed to be important in

improving the validity and reliability the business plan prepared by these Canadian small

businesses in sustaining consistency within the regularity of businesses process and operations

that is important for dealing with financial concerns experienced at the time of undertaking

required financial funds from the Canadian banks. These researchers have also observed in their

study that the Canadian banks are likely to be inclined towards the large business operating

within Canada for the reason that they attain an increased amount of profit which can further be

derived along with an increased interest rate. Rostamkalaei and Freel (2017) added that there

exist several non-profit companies in Canada as well as business service companies that provides

free funding to be a planning tool for cash flow. Through attaining government grants along with

business related loans they attain increased access to enhanced cash, improving strategic plans

implementation along with imposing the capabilities of business growth (Rugman and Verbeke

2017). Collateral is asset of exceptional value and in case the small companies fail with financial

troubles in gathering financial assistance these companies can attain funds from banks through

feel the need to implement certain changes that further allows the business owners to attain high

loans with great ease along with attaining certain grant which have been developed for offering

these businesses with great opportunities of growth. Pilbeam (2018) elucidated that the small

business owners within Canada can play a great role in the training seminars as well as within

the developmental sessions in order to offer better financial assistance. Whereas, the angel

invests and the venture capitalists are offered with exceptional roles and responsibilities of

accepting risks and offering funding support to all owners of small business in sustaining the

consistency in the regular operations of the businesses processes and operations.

Quarter, Mook and Armstrong (2017) stated that this is deemed to be important in

improving the validity and reliability the business plan prepared by these Canadian small

businesses in sustaining consistency within the regularity of businesses process and operations

that is important for dealing with financial concerns experienced at the time of undertaking

required financial funds from the Canadian banks. These researchers have also observed in their

study that the Canadian banks are likely to be inclined towards the large business operating

within Canada for the reason that they attain an increased amount of profit which can further be

derived along with an increased interest rate. Rostamkalaei and Freel (2017) added that there

exist several non-profit companies in Canada as well as business service companies that provides

free funding to be a planning tool for cash flow. Through attaining government grants along with

business related loans they attain increased access to enhanced cash, improving strategic plans

implementation along with imposing the capabilities of business growth (Rugman and Verbeke

2017). Collateral is asset of exceptional value and in case the small companies fail with financial

troubles in gathering financial assistance these companies can attain funds from banks through

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

keeping collateral with the bank in the form of land, machinery, personal assets or commercial

vehicles.

2.6. Research Gap

From analysing past researches on the issues dealt by Canadian small businesses in

attaining financial assistance from the banks within the nation, it has been gathered that there

exist a research gap in the existing literature because of lack of peer reviewed articles that at

times included improper information and data which might further impact the successful

management of research (Shaw and Barry 2015). The past researches majorly focussed on

analysing three major challenges that were issues dealt by Canadian small businesses at the time

of undertaking financial assistance from banks within the nation. For this reason, this can be

considered as the research gap gathered from the literature review section of the study (Snyder,

Mathers and Crooks 2016).

In consideration to the identified research gap within the literature review part of this

research, the current study has focussed on gathering relevant data from several secondary

sources that supported in collecting vast knowledge and information regarding the research

subject. This has not only contributed to the significance of the current study but has also

facilitated the researcher in understanding the management of small businesses (Ughetto,

Skeleton and Cowling 2017).

2.7. Theoretical Framework and Hypotheses

The theoretical framework that has been developed for attaining guidance on successful

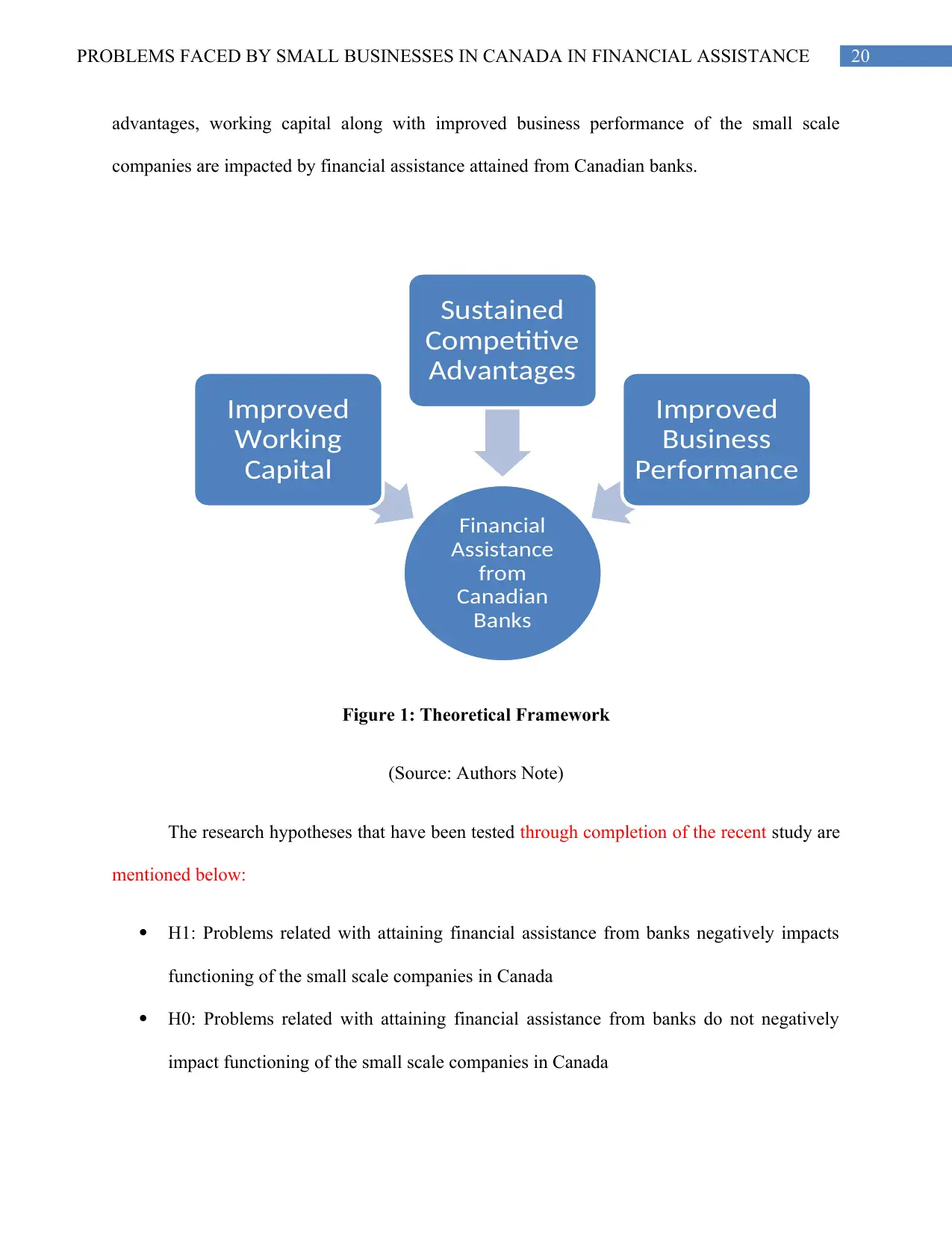

completion of the report is indicated below. This framework indicates that sustained competitive

keeping collateral with the bank in the form of land, machinery, personal assets or commercial

vehicles.

2.6. Research Gap

From analysing past researches on the issues dealt by Canadian small businesses in

attaining financial assistance from the banks within the nation, it has been gathered that there

exist a research gap in the existing literature because of lack of peer reviewed articles that at

times included improper information and data which might further impact the successful

management of research (Shaw and Barry 2015). The past researches majorly focussed on

analysing three major challenges that were issues dealt by Canadian small businesses at the time

of undertaking financial assistance from banks within the nation. For this reason, this can be

considered as the research gap gathered from the literature review section of the study (Snyder,

Mathers and Crooks 2016).

In consideration to the identified research gap within the literature review part of this

research, the current study has focussed on gathering relevant data from several secondary

sources that supported in collecting vast knowledge and information regarding the research

subject. This has not only contributed to the significance of the current study but has also

facilitated the researcher in understanding the management of small businesses (Ughetto,

Skeleton and Cowling 2017).

2.7. Theoretical Framework and Hypotheses

The theoretical framework that has been developed for attaining guidance on successful

completion of the report is indicated below. This framework indicates that sustained competitive

20PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

advantages, working capital along with improved business performance of the small scale

companies are impacted by financial assistance attained from Canadian banks.

Figure 1: Theoretical Framework

(Source: Authors Note)

The research hypotheses that have been tested through completion of the recent study are

mentioned below:

H1: Problems related with attaining financial assistance from banks negatively impacts

functioning of the small scale companies in Canada

H0: Problems related with attaining financial assistance from banks do not negatively

impact functioning of the small scale companies in Canada

Financial

Assistance

from

Canadian

Banks

Improved

Working

Capital

Sustained

Competitive

Advantages

Improved

Business

Performance

advantages, working capital along with improved business performance of the small scale

companies are impacted by financial assistance attained from Canadian banks.

Figure 1: Theoretical Framework

(Source: Authors Note)

The research hypotheses that have been tested through completion of the recent study are

mentioned below:

H1: Problems related with attaining financial assistance from banks negatively impacts

functioning of the small scale companies in Canada

H0: Problems related with attaining financial assistance from banks do not negatively

impact functioning of the small scale companies in Canada

Financial

Assistance

from

Canadian

Banks

Improved

Working

Capital

Sustained

Competitive

Advantages

Improved

Business

Performance

21PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22PROBLEMS FACED BY SMALL BUSINESSES IN CANADA IN FINANCIAL ASSISTANCE

Chapter 3: Research Methodology

3.1. Introduction

The third chapter elaborates the suitable research methodology which has been employed

by the researcher in selecting suitable study approaches, philosophy, design, sampling and

strategies in attaining suitable study findings. Suitability of gathered responses from the