Business Analysis: Evaluating FIFO and Weighted Average Cost Methods

VerifiedAdded on 2023/06/10

|8

|1004

|255

Report

AI Summary

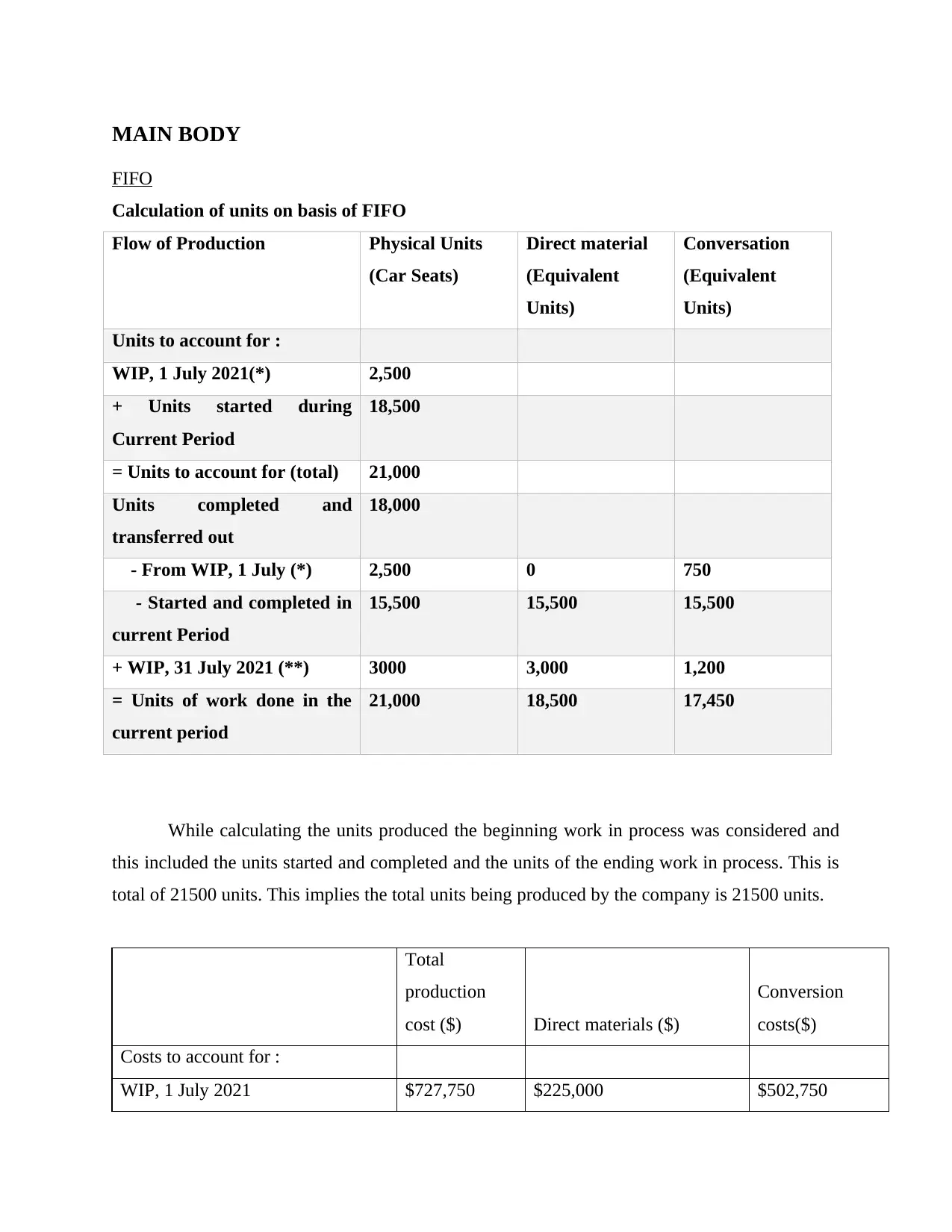

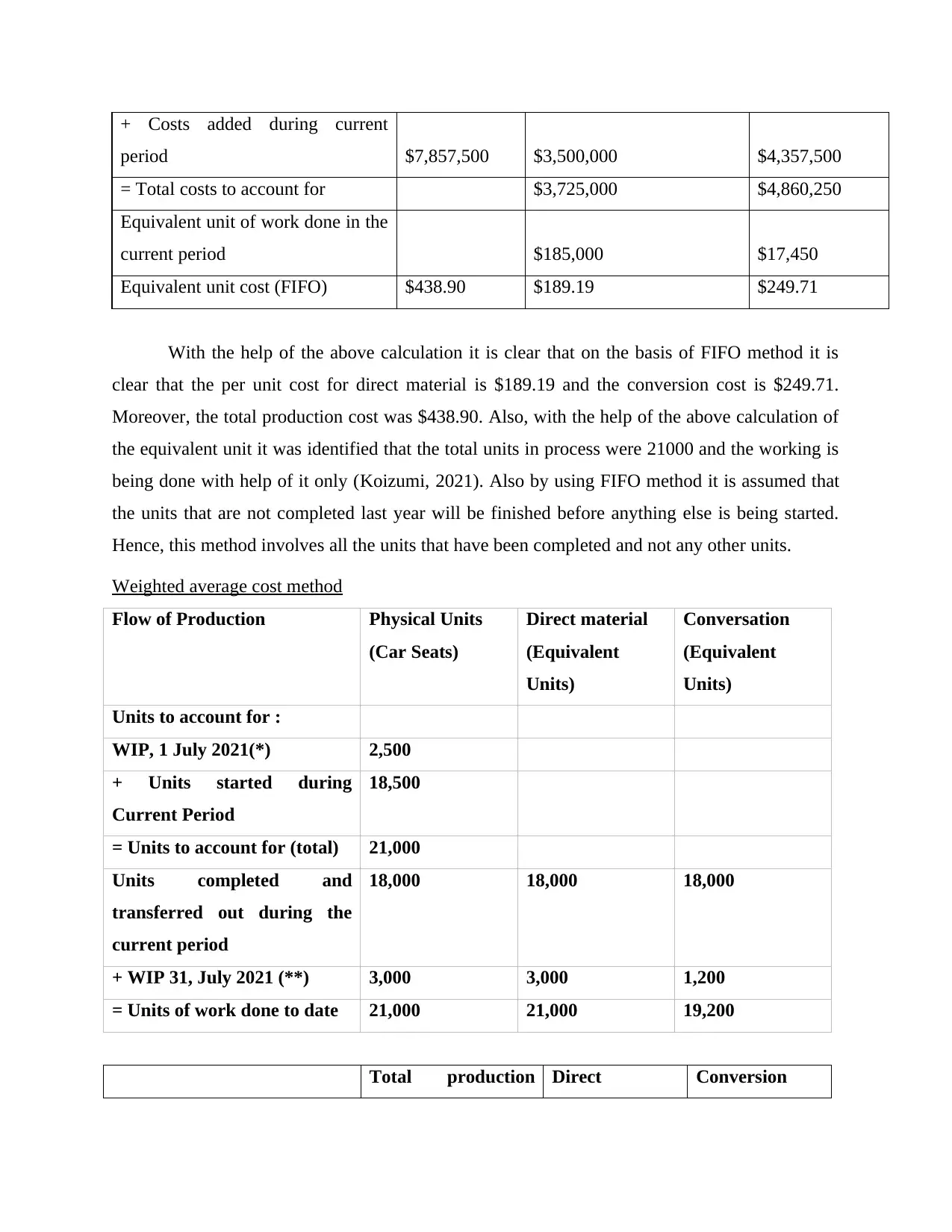

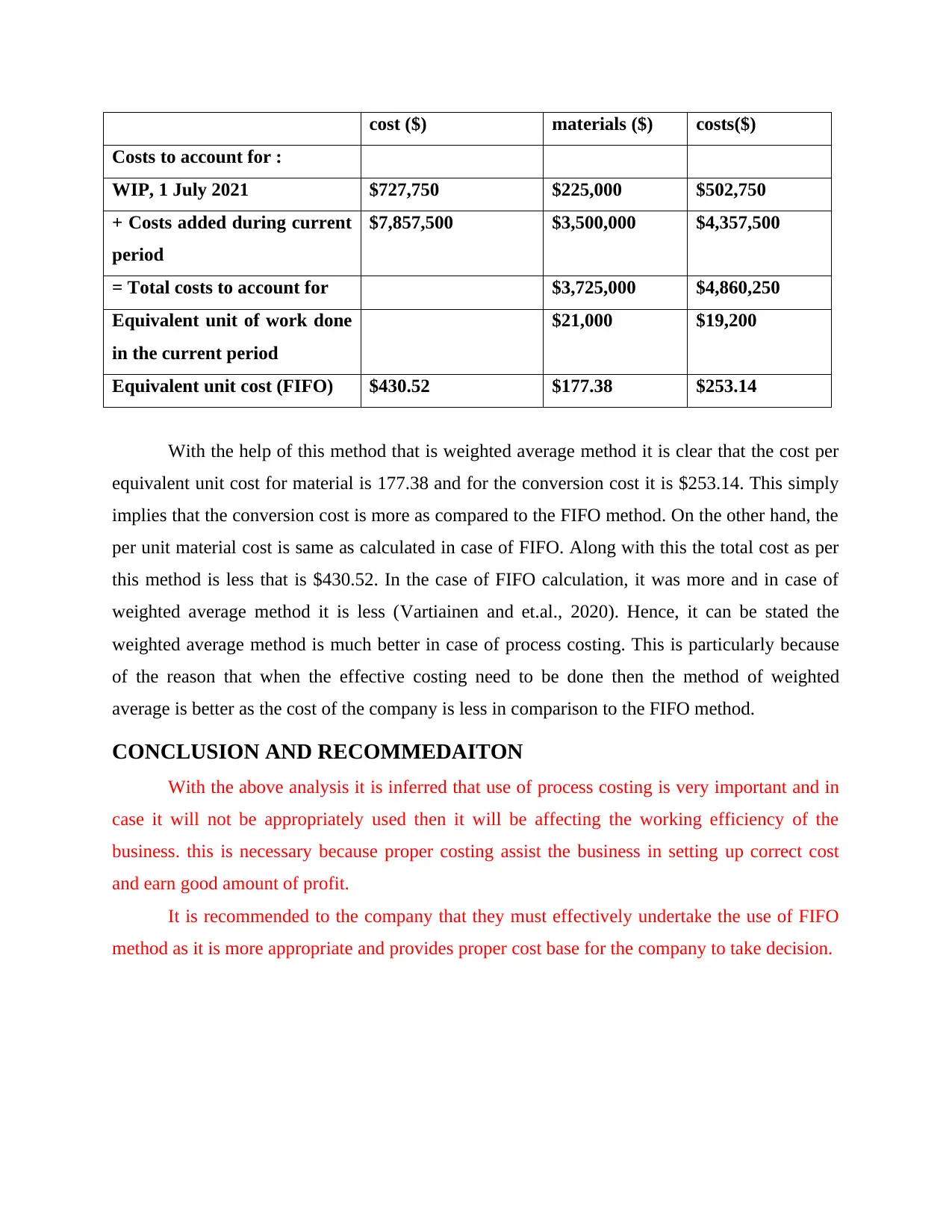

This report provides a detailed analysis of process costing, comparing the FIFO (First-In, First-Out) and weighted average methods. It includes calculations for units produced, direct material costs, and conversion costs under both methods. The FIFO method calculates per-unit costs for direct materials at $189.19 and conversion costs at $249.71, resulting in a total production cost of $438.90. The weighted average method shows a per-unit material cost of $177.38 and a conversion cost of $253.14, with a total cost of $430.52. The report concludes that while the weighted average method results in a slightly lower total cost, the FIFO method is recommended for providing a more accurate cost basis for decision-making. Desklib provides access to this and many other solved assignments to assist students in their learning.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.