University Economics: Production and Cost Minimizing Output Analysis

VerifiedAdded on 2022/08/21

|6

|935

|16

Homework Assignment

AI Summary

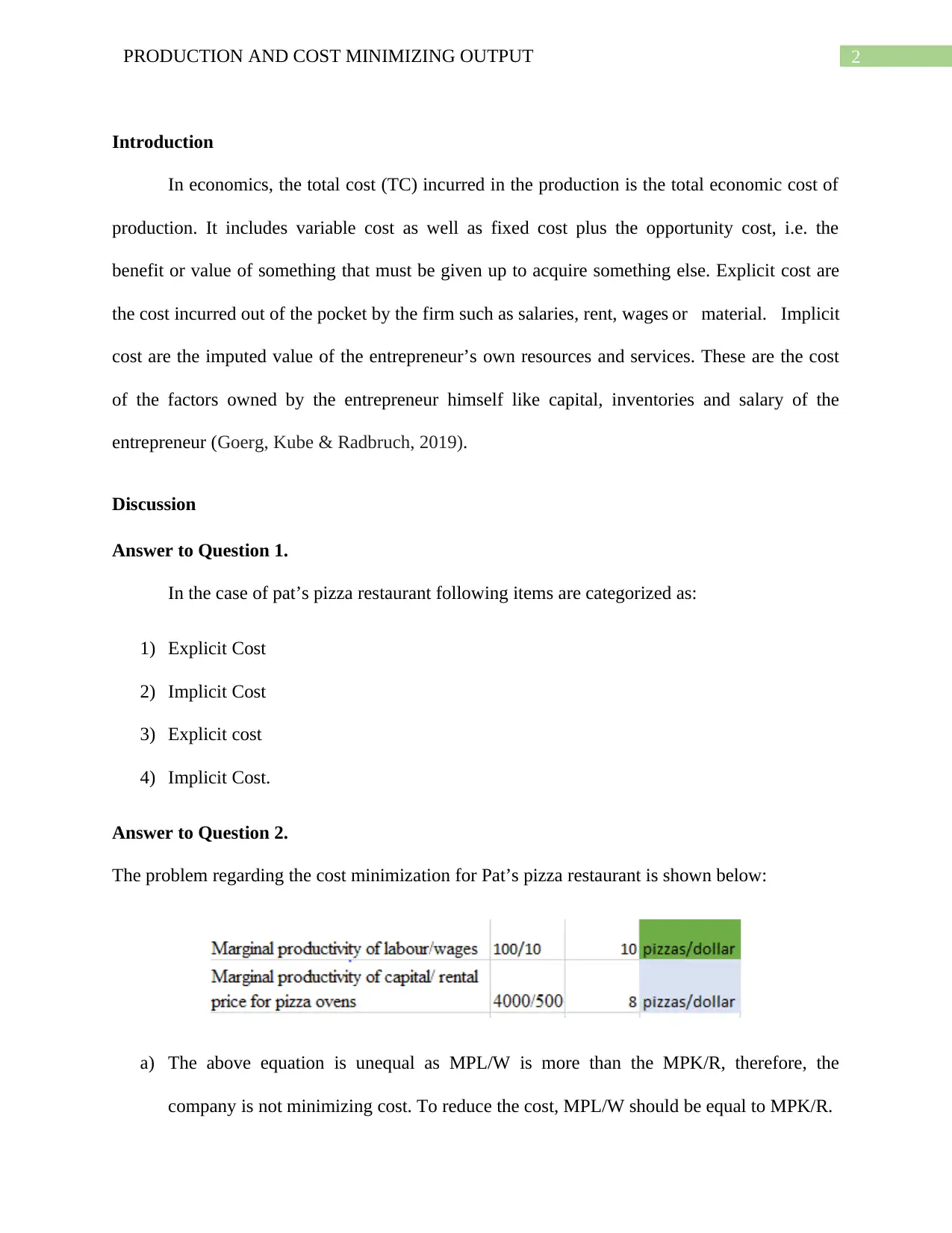

This assignment analyzes the principles of cost minimization in the context of a small business, specifically Pat's Pizza Restaurant. It explores the concepts of explicit and implicit costs, and how they impact profit maximization. The analysis includes a breakdown of costs, a discussion of how to minimize costs by adjusting input factors (labor and capital), and strategies for improving productivity in both the short and long run. The assignment also provides recommendations for Pat to increase productivity and maximize profits, including decisions regarding plant capacity and technology changes, while emphasizing the importance of managing short-run costs to achieve long-term goals. The report suggests the importance of cost in deciding the pricing policy of the company.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.