Production Management and Supply Chain Homework Assignment Solution

VerifiedAdded on 2022/09/09

|7

|1792

|16

Homework Assignment

AI Summary

This document presents a detailed solution to a production management assignment. The solution addresses key concepts, including the relative nature of productivity, the necessity of safety stock in MRP systems, and the benefits of updating MRP systems more frequently. The assignment further explores a product mix problem, formulating an integer programming model to optimize production based on given constraints and resources. The solution includes an analysis of resource limitations, recommendations for overtime, and an aggregate planning problem for a supply chain, with cost optimization and outsourcing considerations. Finally, it provides a material requirements planning (MRP) analysis, including lot sizing and lead time calculations.

Problem 1

Question(a)

What do we mean when we say productivity is a relative measure? Choose an industry and

measure productivity of the company in two different ways with supportive data.

Answer

In order the word productivity to be meaningful, the same needs to be compared with something

else. The comparison in order to make it meaningful can be done through intracompany or

intercompany just same as done in the case of benchmarking. Due to differences in accounting

practices the intercompany comparisons only with the single factor productivity can be weak .The

accounting policy, assumption ,procedures and practices involved with respect to inter company

comparison is not up to the mark as specially when the comparison is done with the foreign

competitors involved into it (Advameg, Inc., 2019) .Total factor productivity are some were more

strong and good in case of comparison purpose .

There are different ways involved in order to measure the productivity of the company involved,

some are listed here in below:

1. Strategy with involvement of Simple Productivity Output Formula.

2. Strategy relates to 360 Degree feedback

3. Time tracking and project Management Software.

4. Social Media Strategy.

5. If there is an involvement of profit the strategy is productive.

6. “Getting Shit done” Strategy.

7. Strategy which relates to daily check -in.

8. Providing service with a strategy of smiling attitude.

http://www.prism.gatech.edu/~bt71/mgt3501/HW_2_sol

Question(b)

Should safety stock be necessary in an MRP system with dependent demand? If so, why?

If not, why do firms carry it anyway?

Question(a)

What do we mean when we say productivity is a relative measure? Choose an industry and

measure productivity of the company in two different ways with supportive data.

Answer

In order the word productivity to be meaningful, the same needs to be compared with something

else. The comparison in order to make it meaningful can be done through intracompany or

intercompany just same as done in the case of benchmarking. Due to differences in accounting

practices the intercompany comparisons only with the single factor productivity can be weak .The

accounting policy, assumption ,procedures and practices involved with respect to inter company

comparison is not up to the mark as specially when the comparison is done with the foreign

competitors involved into it (Advameg, Inc., 2019) .Total factor productivity are some were more

strong and good in case of comparison purpose .

There are different ways involved in order to measure the productivity of the company involved,

some are listed here in below:

1. Strategy with involvement of Simple Productivity Output Formula.

2. Strategy relates to 360 Degree feedback

3. Time tracking and project Management Software.

4. Social Media Strategy.

5. If there is an involvement of profit the strategy is productive.

6. “Getting Shit done” Strategy.

7. Strategy which relates to daily check -in.

8. Providing service with a strategy of smiling attitude.

http://www.prism.gatech.edu/~bt71/mgt3501/HW_2_sol

Question(b)

Should safety stock be necessary in an MRP system with dependent demand? If so, why?

If not, why do firms carry it anyway?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer

Safety stock sometimes also known as buffer stock. It is the extra stock in hand that the

management of the company needs to keep in hand in order to mitigate the uncertainties involved

(Bendis, 2019). The safety stock is necessary in an MRP system with dependant demand due to

following reason involved which are here in below:

1. In order to protect against the unforeseen differences in supply

2. In order to compensate because of inaccuracy in forecast.

3. Properly keep the customer service at a very high level and mitigate stock out risk.

4. It also prevents disruptions involved during the manufacturing and delivery process.

Question(c)

Many practitioners currently update MRP weekly or biweekly. Would it be more valuable if it

were updated daily?

Answer

The performance of any manufacturing items varies on a daily basis. If the time period in which the

observation is done is weekly or biweekly, the variations involved on a daily basis can be smoothen

i.e. the performance on a daily basis i.e. high or low can be done average. For better explanation if

there is an average performance in one day the same can be offset through the better performance

in the next day and the cycle continues ( Notesolution Inc., 2019). If the MRP system is updated daily

than it can lead to watching the performance too closely with an abnormal outcome of report.

Answer 2

Part A

Product Mix Problem

The formulation of integer programming for the given set of facts has been presented as under:

Objective Function

Max Z= (30+b)*a+ 32*b+(30+c)*c+32*d-18a-15b-5c-5d-(35/60)*(12+a)*a-(42/60)*(12+a)*b-

(48/60)*(12+a)*c-(52/60)*(12+a)*d

Decision Variable & Decision Variable Domain

Wherein a= Number of Units of Product A,

b= Number of Units of Product B,

c= Number of Units of Product C,

d= Number of Units of Product D,

Safety stock sometimes also known as buffer stock. It is the extra stock in hand that the

management of the company needs to keep in hand in order to mitigate the uncertainties involved

(Bendis, 2019). The safety stock is necessary in an MRP system with dependant demand due to

following reason involved which are here in below:

1. In order to protect against the unforeseen differences in supply

2. In order to compensate because of inaccuracy in forecast.

3. Properly keep the customer service at a very high level and mitigate stock out risk.

4. It also prevents disruptions involved during the manufacturing and delivery process.

Question(c)

Many practitioners currently update MRP weekly or biweekly. Would it be more valuable if it

were updated daily?

Answer

The performance of any manufacturing items varies on a daily basis. If the time period in which the

observation is done is weekly or biweekly, the variations involved on a daily basis can be smoothen

i.e. the performance on a daily basis i.e. high or low can be done average. For better explanation if

there is an average performance in one day the same can be offset through the better performance

in the next day and the cycle continues ( Notesolution Inc., 2019). If the MRP system is updated daily

than it can lead to watching the performance too closely with an abnormal outcome of report.

Answer 2

Part A

Product Mix Problem

The formulation of integer programming for the given set of facts has been presented as under:

Objective Function

Max Z= (30+b)*a+ 32*b+(30+c)*c+32*d-18a-15b-5c-5d-(35/60)*(12+a)*a-(42/60)*(12+a)*b-

(48/60)*(12+a)*c-(52/60)*(12+a)*d

Decision Variable & Decision Variable Domain

Wherein a= Number of Units of Product A,

b= Number of Units of Product B,

c= Number of Units of Product C,

d= Number of Units of Product D,

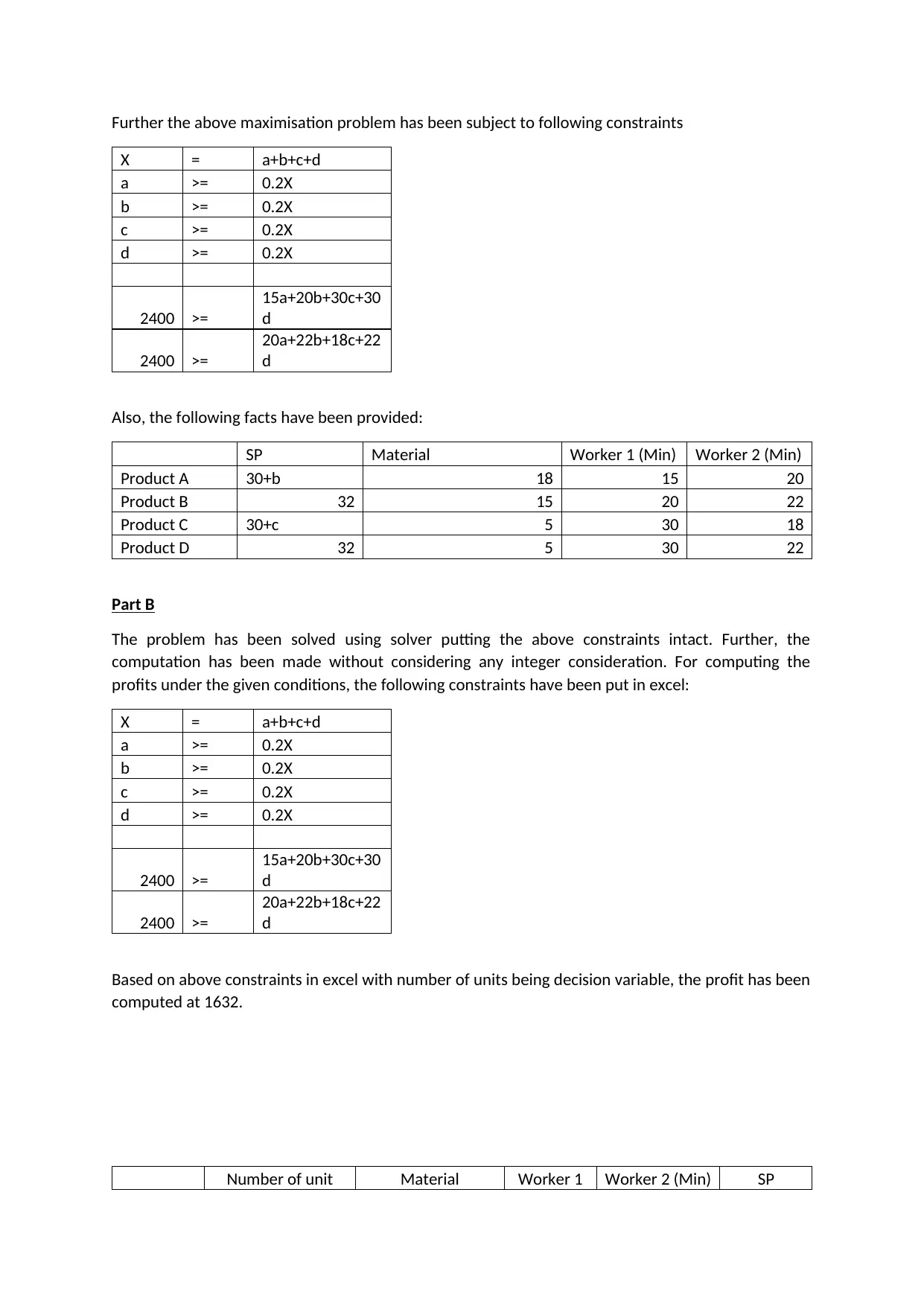

Further the above maximisation problem has been subject to following constraints

X = a+b+c+d

a >= 0.2X

b >= 0.2X

c >= 0.2X

d >= 0.2X

2400 >=

15a+20b+30c+30

d

2400 >=

20a+22b+18c+22

d

Also, the following facts have been provided:

SP Material Worker 1 (Min) Worker 2 (Min)

Product A 30+b 18 15 20

Product B 32 15 20 22

Product C 30+c 5 30 18

Product D 32 5 30 22

Part B

The problem has been solved using solver putting the above constraints intact. Further, the

computation has been made without considering any integer consideration. For computing the

profits under the given conditions, the following constraints have been put in excel:

X = a+b+c+d

a >= 0.2X

b >= 0.2X

c >= 0.2X

d >= 0.2X

2400 >=

15a+20b+30c+30

d

2400 >=

20a+22b+18c+22

d

Based on above constraints in excel with number of units being decision variable, the profit has been

computed at 1632.

Number of unit Material Worker 1 Worker 2 (Min) SP

X = a+b+c+d

a >= 0.2X

b >= 0.2X

c >= 0.2X

d >= 0.2X

2400 >=

15a+20b+30c+30

d

2400 >=

20a+22b+18c+22

d

Also, the following facts have been provided:

SP Material Worker 1 (Min) Worker 2 (Min)

Product A 30+b 18 15 20

Product B 32 15 20 22

Product C 30+c 5 30 18

Product D 32 5 30 22

Part B

The problem has been solved using solver putting the above constraints intact. Further, the

computation has been made without considering any integer consideration. For computing the

profits under the given conditions, the following constraints have been put in excel:

X = a+b+c+d

a >= 0.2X

b >= 0.2X

c >= 0.2X

d >= 0.2X

2400 >=

15a+20b+30c+30

d

2400 >=

20a+22b+18c+22

d

Based on above constraints in excel with number of units being decision variable, the profit has been

computed at 1632.

Number of unit Material Worker 1 Worker 2 (Min) SP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

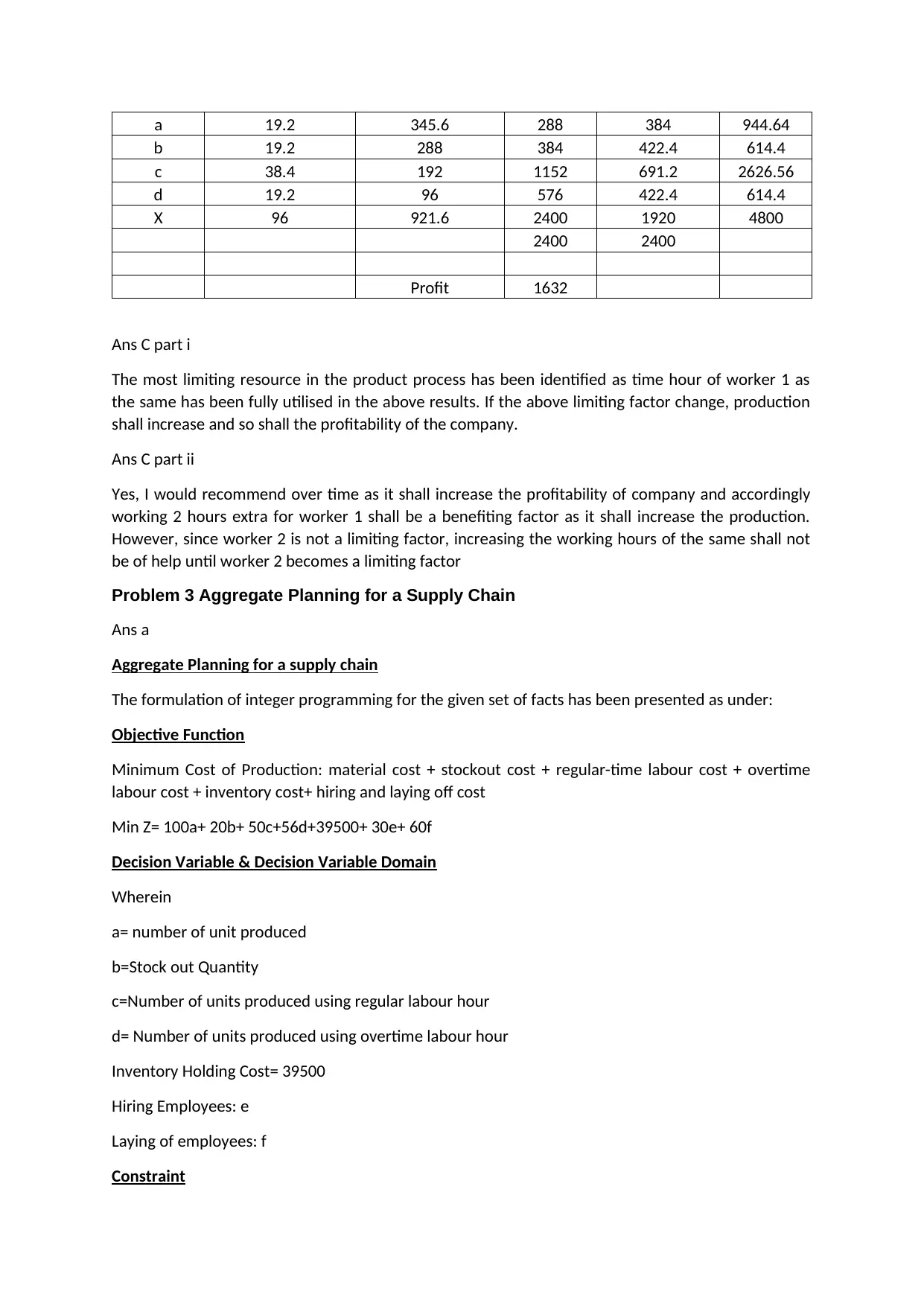

a 19.2 345.6 288 384 944.64

b 19.2 288 384 422.4 614.4

c 38.4 192 1152 691.2 2626.56

d 19.2 96 576 422.4 614.4

X 96 921.6 2400 1920 4800

2400 2400

Profit 1632

Ans C part i

The most limiting resource in the product process has been identified as time hour of worker 1 as

the same has been fully utilised in the above results. If the above limiting factor change, production

shall increase and so shall the profitability of the company.

Ans C part ii

Yes, I would recommend over time as it shall increase the profitability of company and accordingly

working 2 hours extra for worker 1 shall be a benefiting factor as it shall increase the production.

However, since worker 2 is not a limiting factor, increasing the working hours of the same shall not

be of help until worker 2 becomes a limiting factor

Problem 3 Aggregate Planning for a Supply Chain

Ans a

Aggregate Planning for a supply chain

The formulation of integer programming for the given set of facts has been presented as under:

Objective Function

Minimum Cost of Production: material cost + stockout cost + regular-time labour cost + overtime

labour cost + inventory cost+ hiring and laying off cost

Min Z= 100a+ 20b+ 50c+56d+39500+ 30e+ 60f

Decision Variable & Decision Variable Domain

Wherein

a= number of unit produced

b=Stock out Quantity

c=Number of units produced using regular labour hour

d= Number of units produced using overtime labour hour

Inventory Holding Cost= 39500

Hiring Employees: e

Laying of employees: f

Constraint

b 19.2 288 384 422.4 614.4

c 38.4 192 1152 691.2 2626.56

d 19.2 96 576 422.4 614.4

X 96 921.6 2400 1920 4800

2400 2400

Profit 1632

Ans C part i

The most limiting resource in the product process has been identified as time hour of worker 1 as

the same has been fully utilised in the above results. If the above limiting factor change, production

shall increase and so shall the profitability of the company.

Ans C part ii

Yes, I would recommend over time as it shall increase the profitability of company and accordingly

working 2 hours extra for worker 1 shall be a benefiting factor as it shall increase the production.

However, since worker 2 is not a limiting factor, increasing the working hours of the same shall not

be of help until worker 2 becomes a limiting factor

Problem 3 Aggregate Planning for a Supply Chain

Ans a

Aggregate Planning for a supply chain

The formulation of integer programming for the given set of facts has been presented as under:

Objective Function

Minimum Cost of Production: material cost + stockout cost + regular-time labour cost + overtime

labour cost + inventory cost+ hiring and laying off cost

Min Z= 100a+ 20b+ 50c+56d+39500+ 30e+ 60f

Decision Variable & Decision Variable Domain

Wherein

a= number of unit produced

b=Stock out Quantity

c=Number of units produced using regular labour hour

d= Number of units produced using overtime labour hour

Inventory Holding Cost= 39500

Hiring Employees: e

Laying of employees: f

Constraint

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units produced each month shall be atleast 90% of units demanded + carry over

Labour hours normal limited to per month days* 8* 15

Overtime labour hours limited to per month days*1*15

Ans B

Based on above constraints and domain, the computation of minimum cost has been presented as

under:

Jan Feb Mar Apr May Jun

Number of Unit Demanded 500 600 710 871 987.1 500

Number of Unit Produced 500 540 639 783.9 987.1 500

Shortfall 0 60 71 87.1 0.00 0.00

Minimum Production 450 540 639 783.9 888.39 450.00

Stock Out Cost 0 1200 1420 1742 0.00 0.00

Holding Cost 5000 5400 6390 7839 9871 5000

Labour Hours 2000 2160 2556 3135.6 3948.4 2000

Labour Normal Hours 2640 2280 2520 2520 2640 2400

Used Normal Hour 2000 2160 2640 2640 2640 2000

Max overtime hours 330 285 315 315 330 300

Labour Overtime Hours 0 0 36 315 330 0

Excess Hours 0 0 0 300.6 978.4 0

Number of worker required 0 0 0 2 3 0

Training Cost 0 0 0 60 90 0

Laying off cost 0 0 0 0 180 0

Labour Cost Normal 25000 27000 33000 33000 33000 25000

Labour Cost Overtime 0 0 504 4410 4620 0

Normal Hours 0 0 0 336 880 0

Excess Hours Available 0 0 0 42 66 0

Excess hour required 0 0 0 0 98.4 0

Temporary Labour cost

Normal 0 0 0 4200 6600 0

Temporary Labour cost

Overtime 0 0 0 0 1377.6 0

Component cost 50000 54000 63900 78390 98710 50000

Total cost 80000 87600 105214 129641

154448.

6 80000

Overall Cost

636903.

6

Cost per unit

161.241

4

Ans C

Any price offer made by third party lower than $ 156 shall be accepted immediately as the cost of

company is higher per unit. Further, if the price is in the range of $ 156 to $ 162 company should

accept the offer. Also, any price above $ 162 shall be pondered upon.

Labour hours normal limited to per month days* 8* 15

Overtime labour hours limited to per month days*1*15

Ans B

Based on above constraints and domain, the computation of minimum cost has been presented as

under:

Jan Feb Mar Apr May Jun

Number of Unit Demanded 500 600 710 871 987.1 500

Number of Unit Produced 500 540 639 783.9 987.1 500

Shortfall 0 60 71 87.1 0.00 0.00

Minimum Production 450 540 639 783.9 888.39 450.00

Stock Out Cost 0 1200 1420 1742 0.00 0.00

Holding Cost 5000 5400 6390 7839 9871 5000

Labour Hours 2000 2160 2556 3135.6 3948.4 2000

Labour Normal Hours 2640 2280 2520 2520 2640 2400

Used Normal Hour 2000 2160 2640 2640 2640 2000

Max overtime hours 330 285 315 315 330 300

Labour Overtime Hours 0 0 36 315 330 0

Excess Hours 0 0 0 300.6 978.4 0

Number of worker required 0 0 0 2 3 0

Training Cost 0 0 0 60 90 0

Laying off cost 0 0 0 0 180 0

Labour Cost Normal 25000 27000 33000 33000 33000 25000

Labour Cost Overtime 0 0 504 4410 4620 0

Normal Hours 0 0 0 336 880 0

Excess Hours Available 0 0 0 42 66 0

Excess hour required 0 0 0 0 98.4 0

Temporary Labour cost

Normal 0 0 0 4200 6600 0

Temporary Labour cost

Overtime 0 0 0 0 1377.6 0

Component cost 50000 54000 63900 78390 98710 50000

Total cost 80000 87600 105214 129641

154448.

6 80000

Overall Cost

636903.

6

Cost per unit

161.241

4

Ans C

Any price offer made by third party lower than $ 156 shall be accepted immediately as the cost of

company is higher per unit. Further, if the price is in the range of $ 156 to $ 162 company should

accept the offer. Also, any price above $ 162 shall be pondered upon.

Management of Acron shall opt for third party offer as it shall be advantageous on the part of the

company as the company current cost of production is higher than the third party offer. Further, it

shall relieve the management of production issues, labour management problems and other issues

identified with the production process. Also, it shall relieve the management of production

scheduling and other issues. Further, it is also cost efficient on the part of the company

The major drawback associated with the manufacturing outsource is dependent on third party for

product which results in quality issues. Also, dependent on third party shall create problem in order

scheduling and other customisations. Further, lack of control over production shall bring down the

sales in the long run.

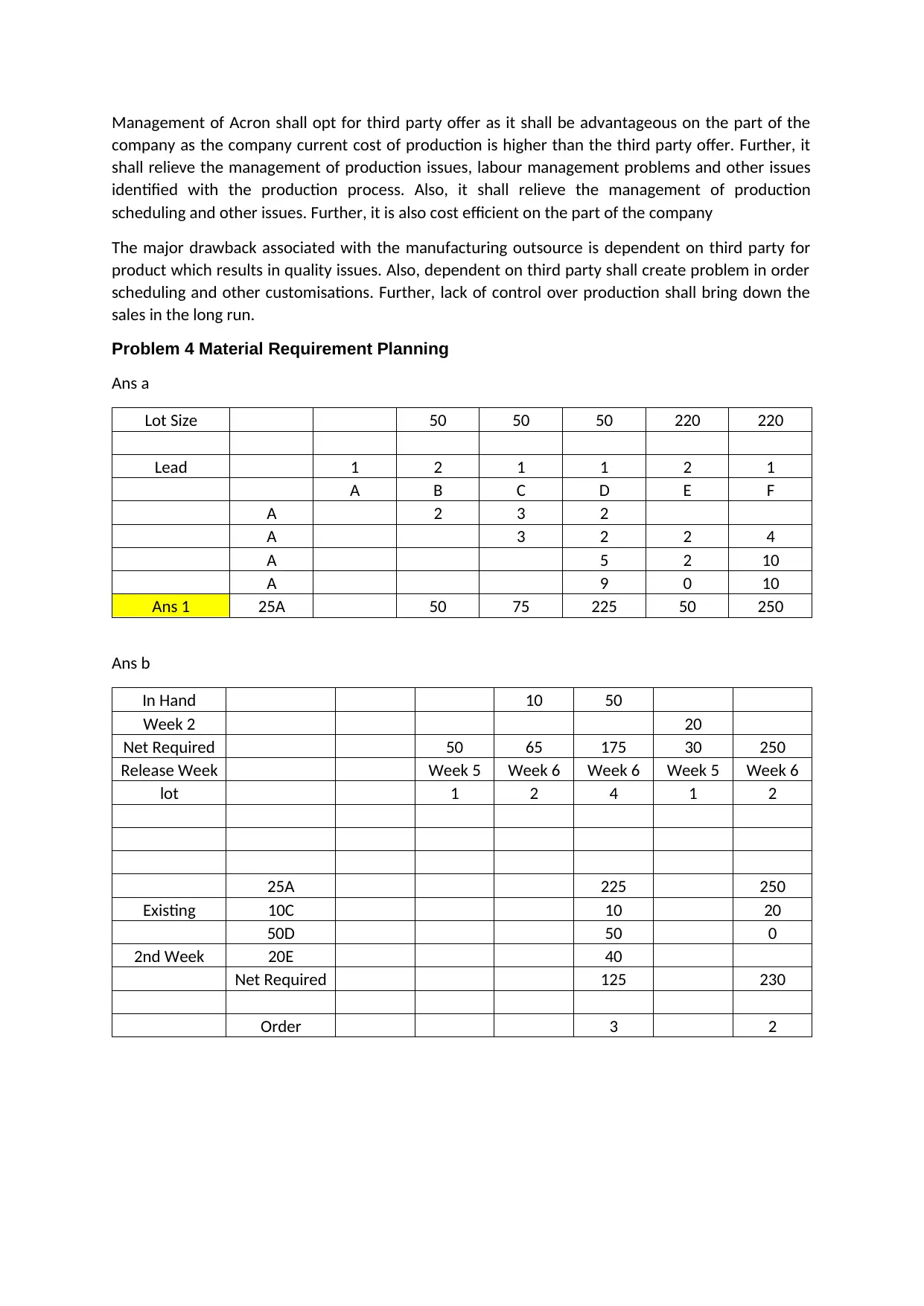

Problem 4 Material Requirement Planning

Ans a

Lot Size 50 50 50 220 220

Lead 1 2 1 1 2 1

A B C D E F

A 2 3 2

A 3 2 2 4

A 5 2 10

A 9 0 10

Ans 1 25A 50 75 225 50 250

Ans b

In Hand 10 50

Week 2 20

Net Required 50 65 175 30 250

Release Week Week 5 Week 6 Week 6 Week 5 Week 6

lot 1 2 4 1 2

25A 225 250

Existing 10C 10 20

50D 50 0

2nd Week 20E 40

Net Required 125 230

Order 3 2

company as the company current cost of production is higher than the third party offer. Further, it

shall relieve the management of production issues, labour management problems and other issues

identified with the production process. Also, it shall relieve the management of production

scheduling and other issues. Further, it is also cost efficient on the part of the company

The major drawback associated with the manufacturing outsource is dependent on third party for

product which results in quality issues. Also, dependent on third party shall create problem in order

scheduling and other customisations. Further, lack of control over production shall bring down the

sales in the long run.

Problem 4 Material Requirement Planning

Ans a

Lot Size 50 50 50 220 220

Lead 1 2 1 1 2 1

A B C D E F

A 2 3 2

A 3 2 2 4

A 5 2 10

A 9 0 10

Ans 1 25A 50 75 225 50 250

Ans b

In Hand 10 50

Week 2 20

Net Required 50 65 175 30 250

Release Week Week 5 Week 6 Week 6 Week 5 Week 6

lot 1 2 4 1 2

25A 225 250

Existing 10C 10 20

50D 50 0

2nd Week 20E 40

Net Required 125 230

Order 3 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Notesolution Inc., 2019. CON 1010 Lecture Notes - Material Requirements Planning, Master

Production Schedule, Lead Time. [Online]

Available at: https://oneclass.com/class-notes/ca/york/econ/econ-1010/271699-

chap011doc.en.html

[Accessed 21 December 2019].

Advameg, Inc., 2019. PRODUCTIVITY CONCEPTS AND MEASURES. [Online]

Available at: https://www.referenceforbusiness.com/management/Pr-Sa/Productivity-Concepts-

and-Measures.html

[Accessed 21 December 2019].

Bendis, M., 2019. 4 Reasons for Carrying Safety Stock Inventory. [Online]

Available at: https://www.eazystock.com/blog/4-reasons-for-carrying-safety-stock-inventory/

[Accessed 21 December 2019].

Notesolution Inc., 2019. CON 1010 Lecture Notes - Material Requirements Planning, Master

Production Schedule, Lead Time. [Online]

Available at: https://oneclass.com/class-notes/ca/york/econ/econ-1010/271699-

chap011doc.en.html

[Accessed 21 December 2019].

Advameg, Inc., 2019. PRODUCTIVITY CONCEPTS AND MEASURES. [Online]

Available at: https://www.referenceforbusiness.com/management/Pr-Sa/Productivity-Concepts-

and-Measures.html

[Accessed 21 December 2019].

Bendis, M., 2019. 4 Reasons for Carrying Safety Stock Inventory. [Online]

Available at: https://www.eazystock.com/blog/4-reasons-for-carrying-safety-stock-inventory/

[Accessed 21 December 2019].

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.