Accounting Principles and Adjustments

VerifiedAdded on 2020/03/01

|24

|1493

|261

AI Summary

This accounting assignment delves into fundamental concepts like debit and credit balances, trial balance preparation, and accrual adjustments. It includes questions on recognizing revenue, expenses, prepaid items, depreciation, and various types of liabilities. Students are also tasked with calculating liquidity ratios and analyzing financial performance through a 10-column spreadsheet. The assignment provides a practical understanding of accounting principles and their application in real-world scenarios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Page1

Q1 Plagiarism

Plagiarism the use and publication of another author’s language, thoughts, Ideas , or

expression as one's own original work without their consent. These works can be

songs, articles, videos, poems etc. Plagiarism is unfair to honest students who have

put in their time as it underestimates the quality of their work.

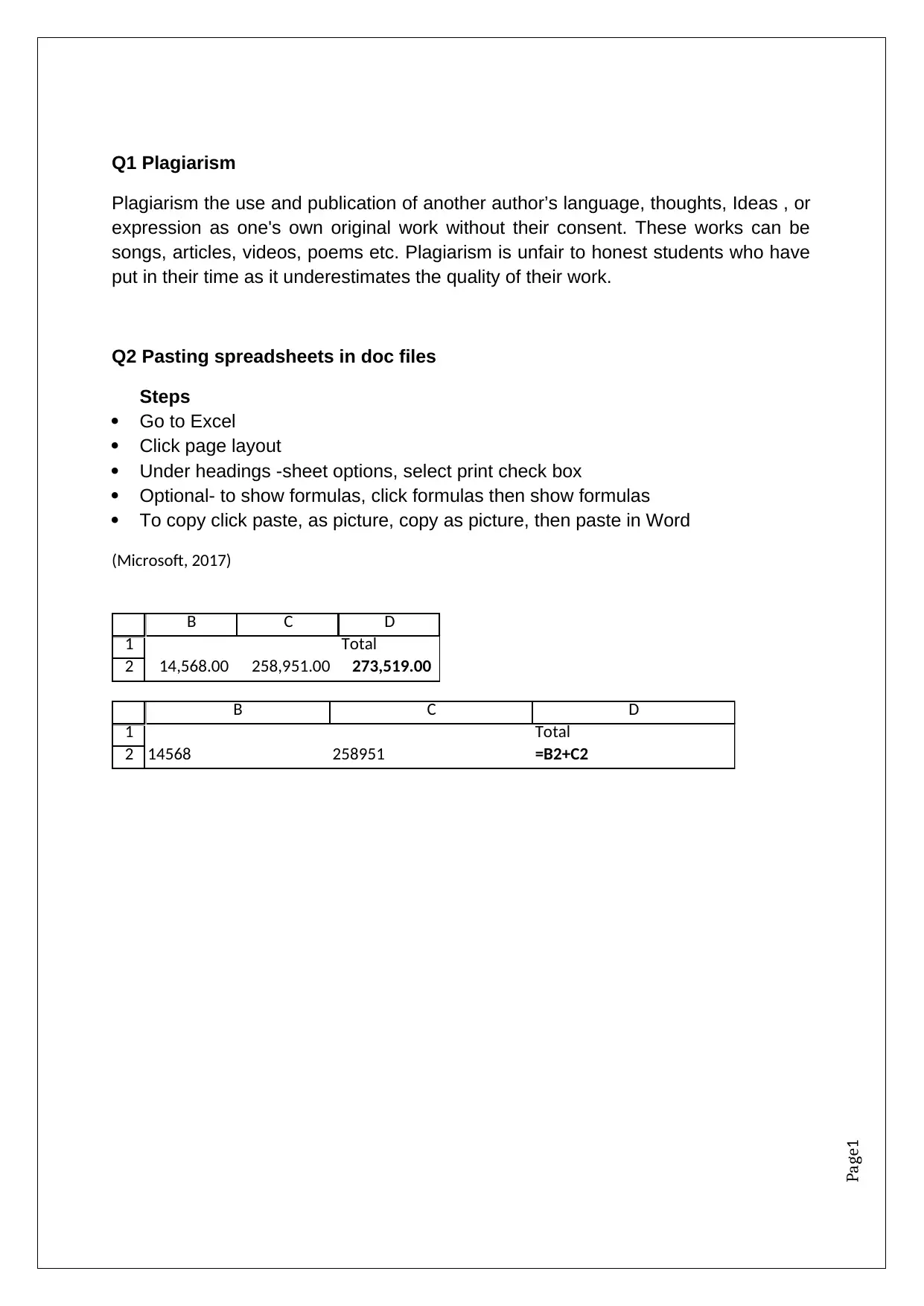

Q2 Pasting spreadsheets in doc files

Steps

Go to Excel

Click page layout

Under headings -sheet options, select print check box

Optional- to show formulas, click formulas then show formulas

To copy click paste, as picture, copy as picture, then paste in Word

(Microsoft, 2017)

1

2

B C D

Total

14,568.00 258,951.00 273,519.00

1

2

B C D

Total

14568 258951 =B2+C2

Q1 Plagiarism

Plagiarism the use and publication of another author’s language, thoughts, Ideas , or

expression as one's own original work without their consent. These works can be

songs, articles, videos, poems etc. Plagiarism is unfair to honest students who have

put in their time as it underestimates the quality of their work.

Q2 Pasting spreadsheets in doc files

Steps

Go to Excel

Click page layout

Under headings -sheet options, select print check box

Optional- to show formulas, click formulas then show formulas

To copy click paste, as picture, copy as picture, then paste in Word

(Microsoft, 2017)

1

2

B C D

Total

14,568.00 258,951.00 273,519.00

1

2

B C D

Total

14568 258951 =B2+C2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page2

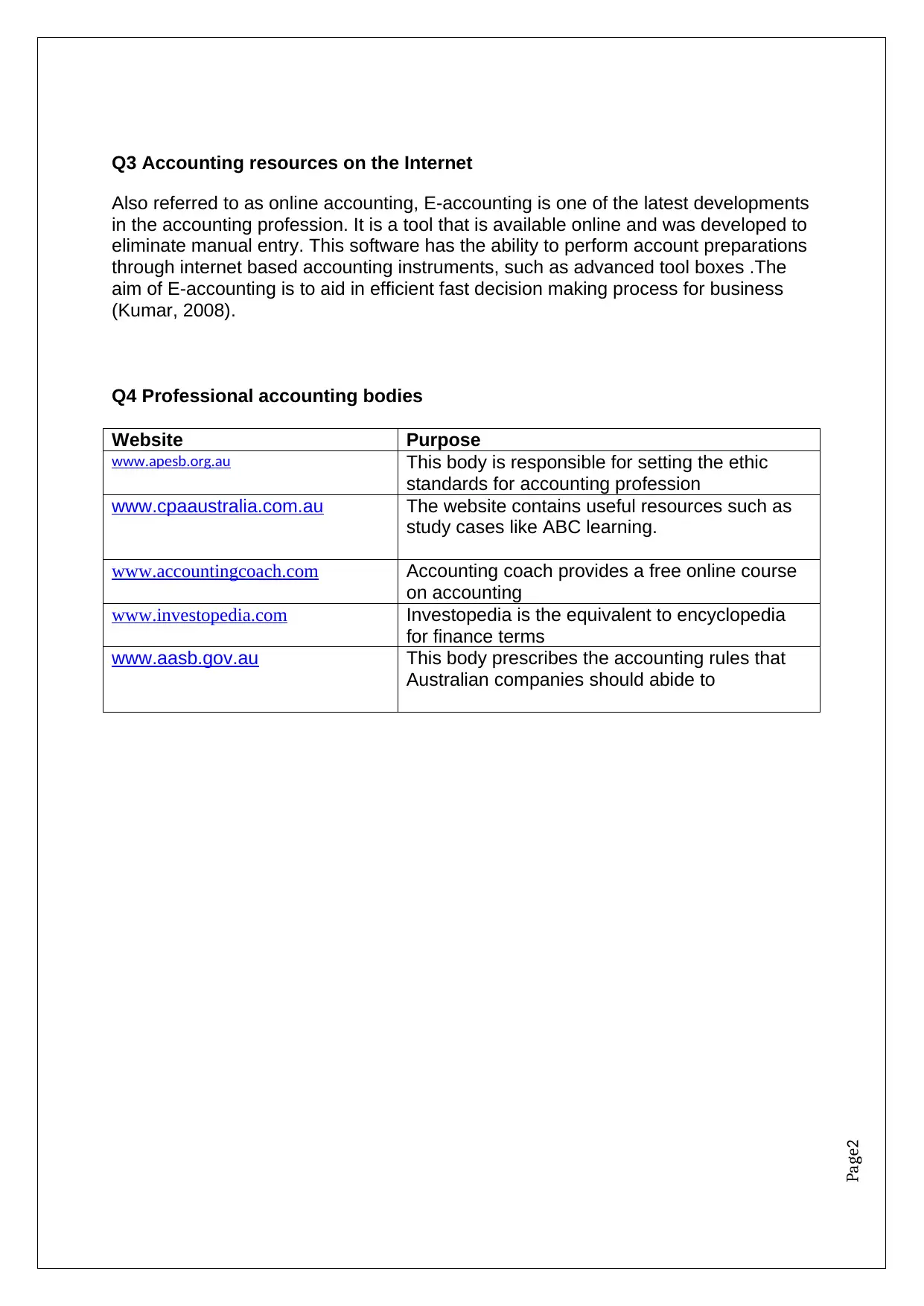

Q3 Accounting resources on the Internet

Also referred to as online accounting, E-accounting is one of the latest developments

in the accounting profession. It is a tool that is available online and was developed to

eliminate manual entry. This software has the ability to perform account preparations

through internet based accounting instruments, such as advanced tool boxes .The

aim of E-accounting is to aid in efficient fast decision making process for business

(Kumar, 2008).

Q4 Professional accounting bodies

Website Purpose

www.apesb.org.au This body is responsible for setting the ethic

standards for accounting profession

www.cpaaustralia.com.au The website contains useful resources such as

study cases like ABC learning.

www.accountingcoach.com Accounting coach provides a free online course

on accounting

www.investopedia.com Investopedia is the equivalent to encyclopedia

for finance terms

www.aasb.gov.au This body prescribes the accounting rules that

Australian companies should abide to

Q3 Accounting resources on the Internet

Also referred to as online accounting, E-accounting is one of the latest developments

in the accounting profession. It is a tool that is available online and was developed to

eliminate manual entry. This software has the ability to perform account preparations

through internet based accounting instruments, such as advanced tool boxes .The

aim of E-accounting is to aid in efficient fast decision making process for business

(Kumar, 2008).

Q4 Professional accounting bodies

Website Purpose

www.apesb.org.au This body is responsible for setting the ethic

standards for accounting profession

www.cpaaustralia.com.au The website contains useful resources such as

study cases like ABC learning.

www.accountingcoach.com Accounting coach provides a free online course

on accounting

www.investopedia.com Investopedia is the equivalent to encyclopedia

for finance terms

www.aasb.gov.au This body prescribes the accounting rules that

Australian companies should abide to

Page3

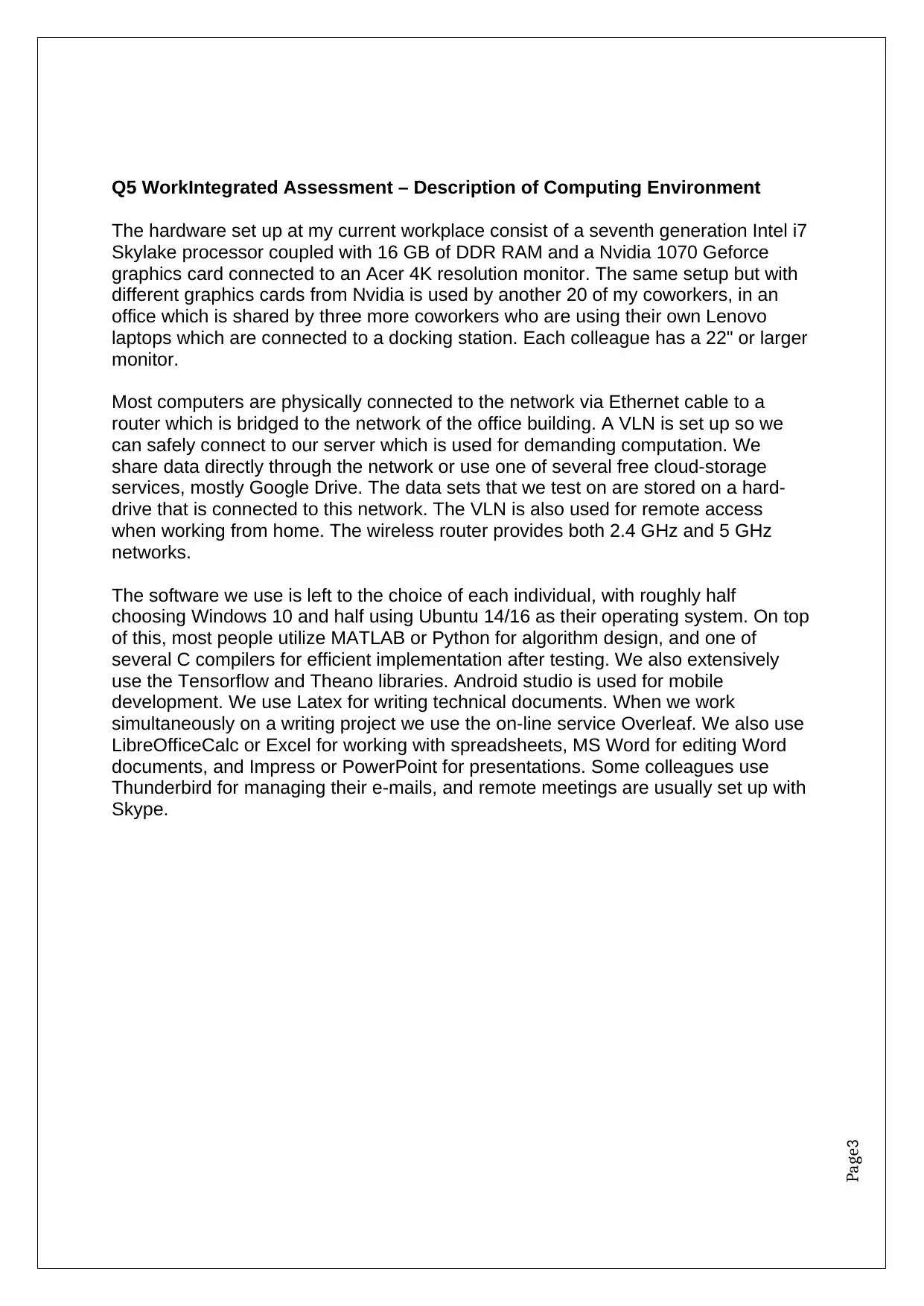

Q5 WorkIntegrated Assessment – Description of Computing Environment

The hardware set up at my current workplace consist of a seventh generation Intel i7

Skylake processor coupled with 16 GB of DDR RAM and a Nvidia 1070 Geforce

graphics card connected to an Acer 4K resolution monitor. The same setup but with

different graphics cards from Nvidia is used by another 20 of my coworkers, in an

office which is shared by three more coworkers who are using their own Lenovo

laptops which are connected to a docking station. Each colleague has a 22" or larger

monitor.

Most computers are physically connected to the network via Ethernet cable to a

router which is bridged to the network of the office building. A VLN is set up so we

can safely connect to our server which is used for demanding computation. We

share data directly through the network or use one of several free cloud-storage

services, mostly Google Drive. The data sets that we test on are stored on a hard-

drive that is connected to this network. The VLN is also used for remote access

when working from home. The wireless router provides both 2.4 GHz and 5 GHz

networks.

The software we use is left to the choice of each individual, with roughly half

choosing Windows 10 and half using Ubuntu 14/16 as their operating system. On top

of this, most people utilize MATLAB or Python for algorithm design, and one of

several C compilers for efficient implementation after testing. We also extensively

use the Tensorflow and Theano libraries. Android studio is used for mobile

development. We use Latex for writing technical documents. When we work

simultaneously on a writing project we use the on-line service Overleaf. We also use

LibreOfficeCalc or Excel for working with spreadsheets, MS Word for editing Word

documents, and Impress or PowerPoint for presentations. Some colleagues use

Thunderbird for managing their e-mails, and remote meetings are usually set up with

Skype.

Q5 WorkIntegrated Assessment – Description of Computing Environment

The hardware set up at my current workplace consist of a seventh generation Intel i7

Skylake processor coupled with 16 GB of DDR RAM and a Nvidia 1070 Geforce

graphics card connected to an Acer 4K resolution monitor. The same setup but with

different graphics cards from Nvidia is used by another 20 of my coworkers, in an

office which is shared by three more coworkers who are using their own Lenovo

laptops which are connected to a docking station. Each colleague has a 22" or larger

monitor.

Most computers are physically connected to the network via Ethernet cable to a

router which is bridged to the network of the office building. A VLN is set up so we

can safely connect to our server which is used for demanding computation. We

share data directly through the network or use one of several free cloud-storage

services, mostly Google Drive. The data sets that we test on are stored on a hard-

drive that is connected to this network. The VLN is also used for remote access

when working from home. The wireless router provides both 2.4 GHz and 5 GHz

networks.

The software we use is left to the choice of each individual, with roughly half

choosing Windows 10 and half using Ubuntu 14/16 as their operating system. On top

of this, most people utilize MATLAB or Python for algorithm design, and one of

several C compilers for efficient implementation after testing. We also extensively

use the Tensorflow and Theano libraries. Android studio is used for mobile

development. We use Latex for writing technical documents. When we work

simultaneously on a writing project we use the on-line service Overleaf. We also use

LibreOfficeCalc or Excel for working with spreadsheets, MS Word for editing Word

documents, and Impress or PowerPoint for presentations. Some colleagues use

Thunderbird for managing their e-mails, and remote meetings are usually set up with

Skype.

Page4

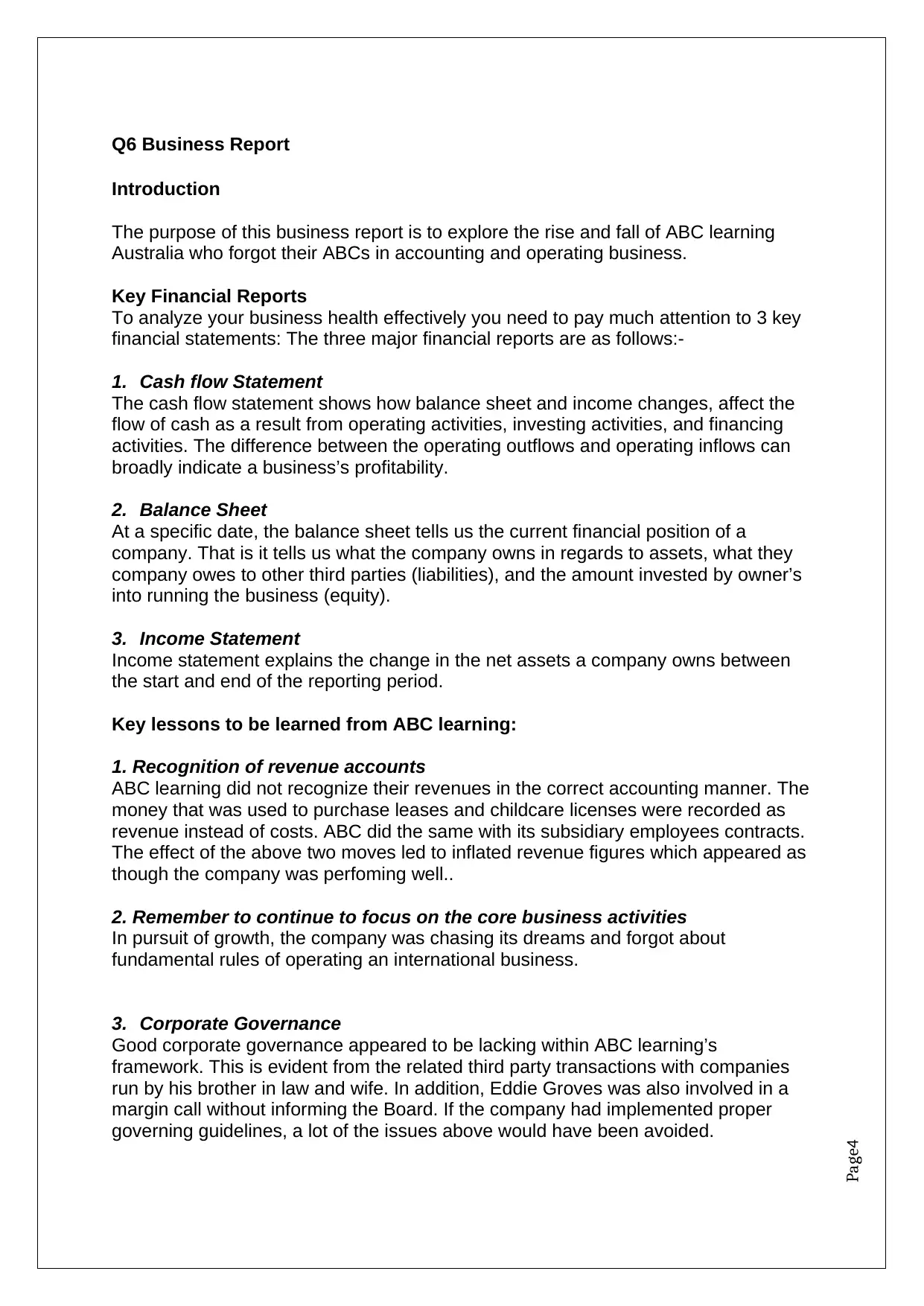

Q6 Business Report

Introduction

The purpose of this business report is to explore the rise and fall of ABC learning

Australia who forgot their ABCs in accounting and operating business.

Key Financial Reports

To analyze your business health effectively you need to pay much attention to 3 key

financial statements: The three major financial reports are as follows:-

1. Cash flow Statement

The cash flow statement shows how balance sheet and income changes, affect the

flow of cash as a result from operating activities, investing activities, and financing

activities. The difference between the operating outflows and operating inflows can

broadly indicate a business’s profitability.

2. Balance Sheet

At a specific date, the balance sheet tells us the current financial position of a

company. That is it tells us what the company owns in regards to assets, what they

company owes to other third parties (liabilities), and the amount invested by owner’s

into running the business (equity).

3. Income Statement

Income statement explains the change in the net assets a company owns between

the start and end of the reporting period.

Key lessons to be learned from ABC learning:

1. Recognition of revenue accounts

ABC learning did not recognize their revenues in the correct accounting manner. The

money that was used to purchase leases and childcare licenses were recorded as

revenue instead of costs. ABC did the same with its subsidiary employees contracts.

The effect of the above two moves led to inflated revenue figures which appeared as

though the company was perfoming well..

2. Remember to continue to focus on the core business activities

In pursuit of growth, the company was chasing its dreams and forgot about

fundamental rules of operating an international business.

3. Corporate Governance

Good corporate governance appeared to be lacking within ABC learning’s

framework. This is evident from the related third party transactions with companies

run by his brother in law and wife. In addition, Eddie Groves was also involved in a

margin call without informing the Board. If the company had implemented proper

governing guidelines, a lot of the issues above would have been avoided.

Q6 Business Report

Introduction

The purpose of this business report is to explore the rise and fall of ABC learning

Australia who forgot their ABCs in accounting and operating business.

Key Financial Reports

To analyze your business health effectively you need to pay much attention to 3 key

financial statements: The three major financial reports are as follows:-

1. Cash flow Statement

The cash flow statement shows how balance sheet and income changes, affect the

flow of cash as a result from operating activities, investing activities, and financing

activities. The difference between the operating outflows and operating inflows can

broadly indicate a business’s profitability.

2. Balance Sheet

At a specific date, the balance sheet tells us the current financial position of a

company. That is it tells us what the company owns in regards to assets, what they

company owes to other third parties (liabilities), and the amount invested by owner’s

into running the business (equity).

3. Income Statement

Income statement explains the change in the net assets a company owns between

the start and end of the reporting period.

Key lessons to be learned from ABC learning:

1. Recognition of revenue accounts

ABC learning did not recognize their revenues in the correct accounting manner. The

money that was used to purchase leases and childcare licenses were recorded as

revenue instead of costs. ABC did the same with its subsidiary employees contracts.

The effect of the above two moves led to inflated revenue figures which appeared as

though the company was perfoming well..

2. Remember to continue to focus on the core business activities

In pursuit of growth, the company was chasing its dreams and forgot about

fundamental rules of operating an international business.

3. Corporate Governance

Good corporate governance appeared to be lacking within ABC learning’s

framework. This is evident from the related third party transactions with companies

run by his brother in law and wife. In addition, Eddie Groves was also involved in a

margin call without informing the Board. If the company had implemented proper

governing guidelines, a lot of the issues above would have been avoided.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page5

Three Ethical issues faced by ABC learning

1. Related party transactions.

ABC learning directors used to make transactions with their relatives which were not

recorded properly in financial statements. Ethical disclosure of related party

transaction is crucial in analyzing business’ transparency and health.

2. Decision-making issues.

Directors of ABC learning were aimed to expand into more and more markets. They

bought assets in the US and UK. Due to the rapid growth of the business, they

overlooked some fundamentals about operating on local markets.

3. Accounting practices

ABC learning forgot its ABCs in accounting. They did not properly record revenues

and costs. Mostly, they recorded their costs as revenue that was misread by

investors who bought shares that did not show real value.

Conclusion

In conclusion, the fall of ABC learning can be traced to the poor decision-making

process by Eddy Groves, complex transactions such as valuation of intangible

assets and inflated revenues, poor corporate governance systems and an overly

ambitious growth strategy (Koch, 2009).

References

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia. Retrieved from

https://www.youtube.com/watch?v=YYF6JW9vJKo&list=PL12C0ADD577F6B741Jjj

Three Ethical issues faced by ABC learning

1. Related party transactions.

ABC learning directors used to make transactions with their relatives which were not

recorded properly in financial statements. Ethical disclosure of related party

transaction is crucial in analyzing business’ transparency and health.

2. Decision-making issues.

Directors of ABC learning were aimed to expand into more and more markets. They

bought assets in the US and UK. Due to the rapid growth of the business, they

overlooked some fundamentals about operating on local markets.

3. Accounting practices

ABC learning forgot its ABCs in accounting. They did not properly record revenues

and costs. Mostly, they recorded their costs as revenue that was misread by

investors who bought shares that did not show real value.

Conclusion

In conclusion, the fall of ABC learning can be traced to the poor decision-making

process by Eddy Groves, complex transactions such as valuation of intangible

assets and inflated revenues, poor corporate governance systems and an overly

ambitious growth strategy (Koch, 2009).

References

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia. Retrieved from

https://www.youtube.com/watch?v=YYF6JW9vJKo&list=PL12C0ADD577F6B741Jjj

Page6

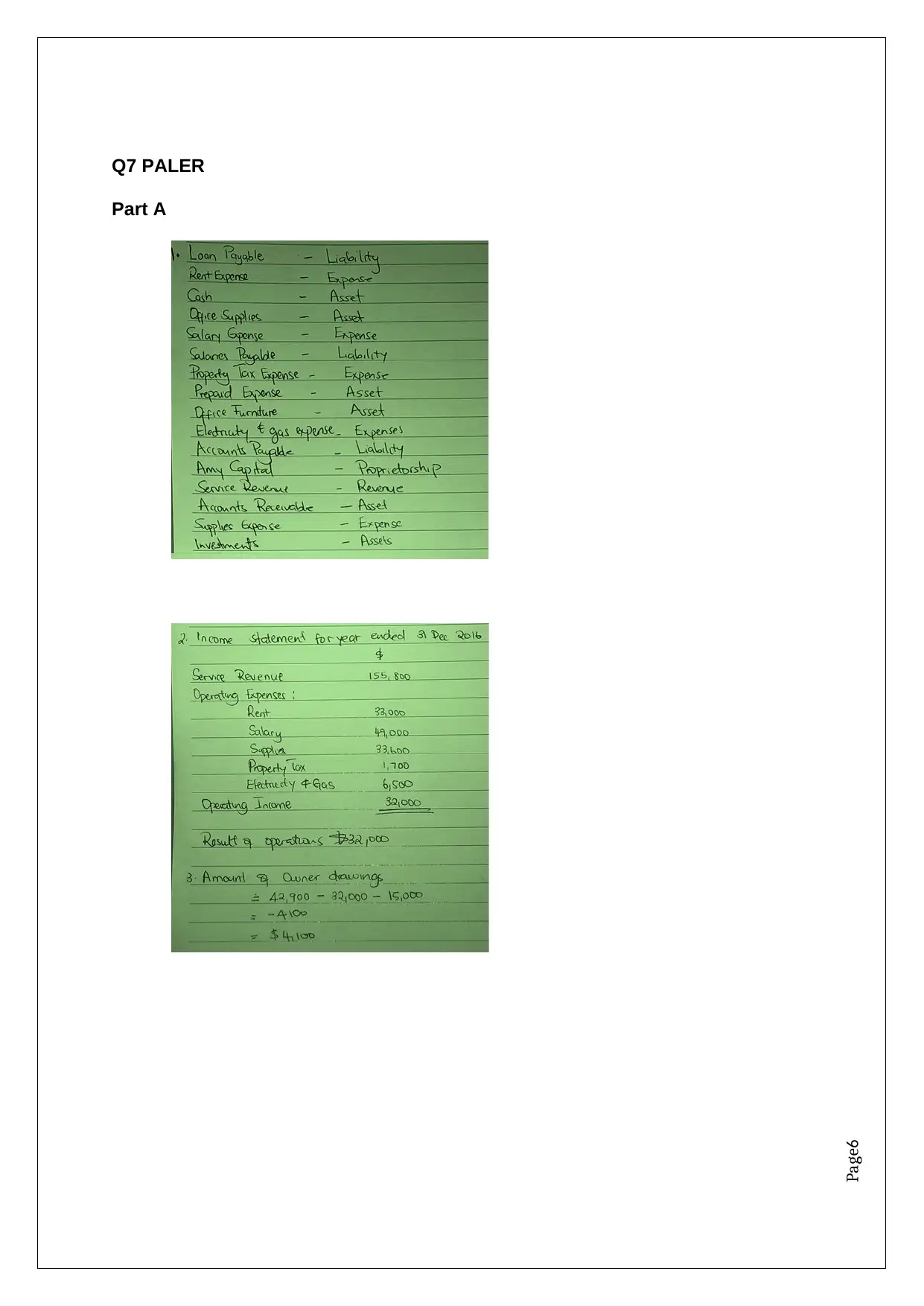

Q7 PALER

Part A

Q7 PALER

Part A

Page7

Part B

Part B

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page8

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

B C D

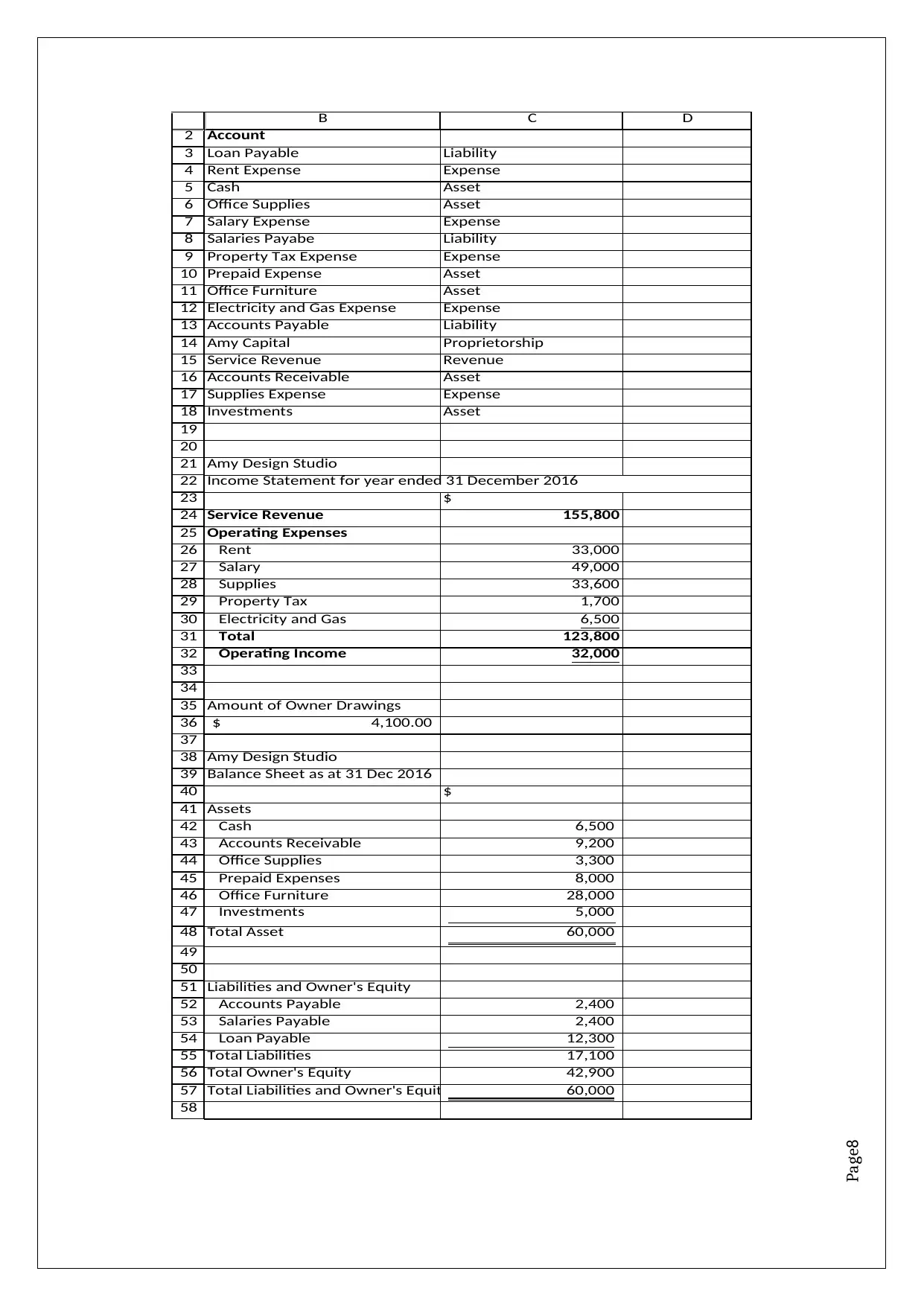

Account

Loan Payable Liability

Rent Expense Expense

Cash Asset

Office Supplies Asset

Salary Expense Expense

Salaries Payabe Liability

Property Tax Expense Expense

Prepaid Expense Asset

Office Furniture Asset

Electricity and Gas Expense Expense

Accounts Payable Liability

Amy Capital Proprietorship

Service Revenue Revenue

Accounts Receivable Asset

Supplies Expense Expense

Investments Asset

Amy Design Studio

$

Service Revenue 155,800

Operating Expenses

Rent 33,000

Salary 49,000

Supplies 33,600

Property Tax 1,700

Electricity and Gas 6,500

Total 123,800

Operating Income 32,000

Amount of Owner Drawings

4,100.00$

Amy Design Studio

Balance Sheet as at 31 Dec 2016

$

Assets

Cash 6,500

Accounts Receivable 9,200

Office Supplies 3,300

Prepaid Expenses 8,000

Office Furniture 28,000

Investments 5,000

Total Asset 60,000

Liabilities and Owner's Equity

Accounts Payable 2,400

Salaries Payable 2,400

Loan Payable 12,300

Total Liabilities 17,100

Total Owner's Equity 42,900

Total Liabilities and Owner's Equity 60,000

Income Statement for year ended 31 December 2016

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

B C D

Account

Loan Payable Liability

Rent Expense Expense

Cash Asset

Office Supplies Asset

Salary Expense Expense

Salaries Payabe Liability

Property Tax Expense Expense

Prepaid Expense Asset

Office Furniture Asset

Electricity and Gas Expense Expense

Accounts Payable Liability

Amy Capital Proprietorship

Service Revenue Revenue

Accounts Receivable Asset

Supplies Expense Expense

Investments Asset

Amy Design Studio

$

Service Revenue 155,800

Operating Expenses

Rent 33,000

Salary 49,000

Supplies 33,600

Property Tax 1,700

Electricity and Gas 6,500

Total 123,800

Operating Income 32,000

Amount of Owner Drawings

4,100.00$

Amy Design Studio

Balance Sheet as at 31 Dec 2016

$

Assets

Cash 6,500

Accounts Receivable 9,200

Office Supplies 3,300

Prepaid Expenses 8,000

Office Furniture 28,000

Investments 5,000

Total Asset 60,000

Liabilities and Owner's Equity

Accounts Payable 2,400

Salaries Payable 2,400

Loan Payable 12,300

Total Liabilities 17,100

Total Owner's Equity 42,900

Total Liabilities and Owner's Equity 60,000

Income Statement for year ended 31 December 2016

Page9

Q8 BALANCE SHEET

Part A

Q8 BALANCE SHEET

Part A

Page10

Part B

Part B

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page11

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

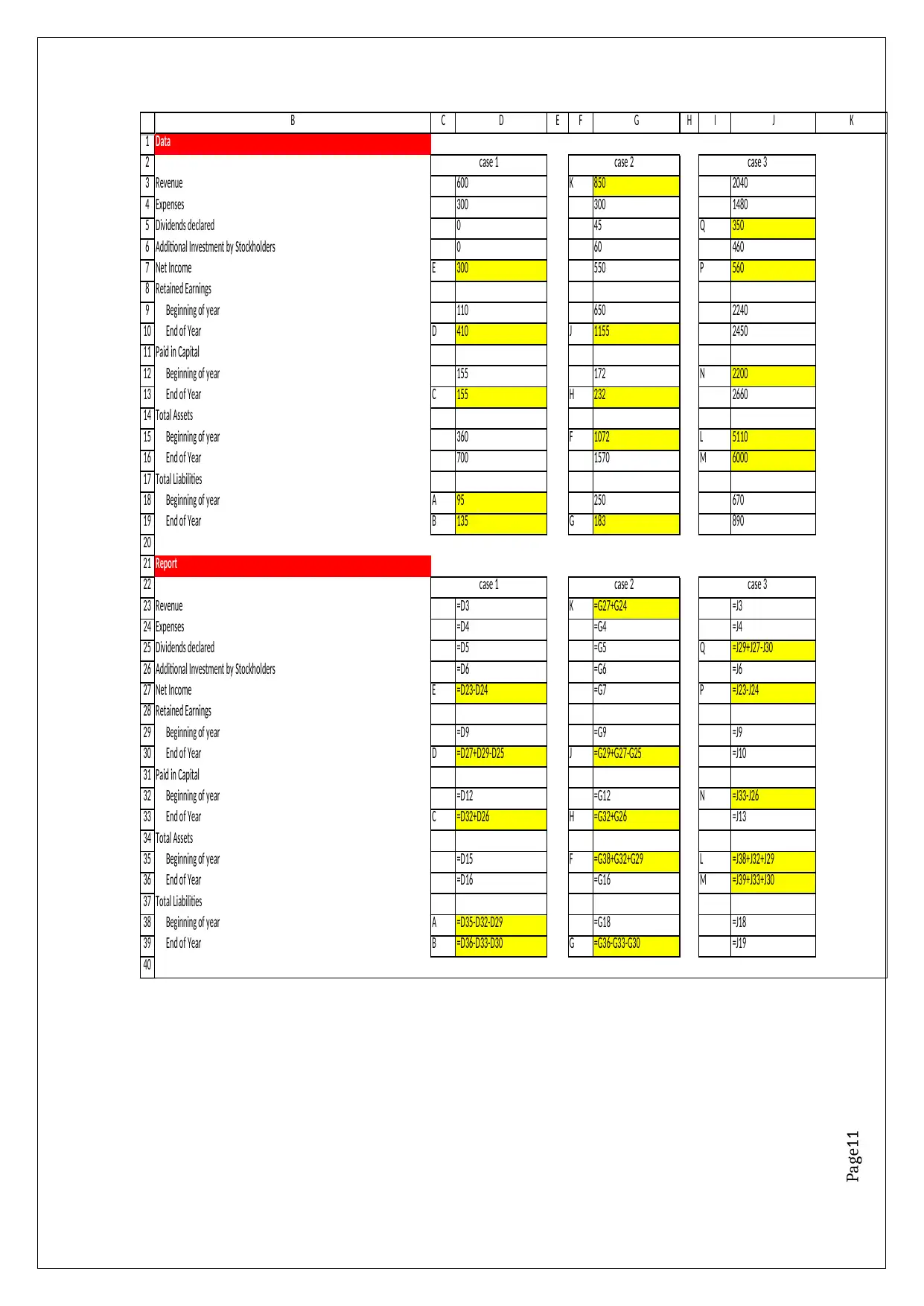

B C D E F G H I J K

Data

Revenue 600 K 850 2040

Expenses 300 300 1480

Dividends declared 0 45 Q 350

Additional Investment by Stockholders 0 60 460

Net Income E 300 550 P 560

Retained Earnings

Beginning of year 110 650 2240

End of Year D 410 J 1155 2450

Paid in Capital

Beginning of year 155 172 N 2200

End of Year C 155 H 232 2660

Total Assets

Beginning of year 360 F 1072 L 5110

End of Year 700 1570 M 6000

Total Liabilities

Beginning of year A 95 250 670

End of Year B 135 G 183 890

Report

Revenue =D3 K =G27+G24 =J3

Expenses =D4 =G4 =J4

Dividends declared =D5 =G5 Q =J29+J27-J30

Additional Investment by Stockholders =D6 =G6 =J6

Net Income E =D23-D24 =G7 P =J23-J24

Retained Earnings

Beginning of year =D9 =G9 =J9

End of Year D =D27+D29-D25 J =G29+G27-G25 =J10

Paid in Capital

Beginning of year =D12 =G12 N =J33-J26

End of Year C =D32+D26 H =G32+G26 =J13

Total Assets

Beginning of year =D15 F =G38+G32+G29 L =J38+J32+J29

End of Year =D16 =G16 M =J39+J33+J30

Total Liabilities

Beginning of year A =D35-D32-D29 =G18 =J18

End of Year B =D36-D33-D30 G =G36-G33-G30 =J19

case 1 case 2 case 3

case 1 case 2 case 3

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

B C D E F G H I J K

Data

Revenue 600 K 850 2040

Expenses 300 300 1480

Dividends declared 0 45 Q 350

Additional Investment by Stockholders 0 60 460

Net Income E 300 550 P 560

Retained Earnings

Beginning of year 110 650 2240

End of Year D 410 J 1155 2450

Paid in Capital

Beginning of year 155 172 N 2200

End of Year C 155 H 232 2660

Total Assets

Beginning of year 360 F 1072 L 5110

End of Year 700 1570 M 6000

Total Liabilities

Beginning of year A 95 250 670

End of Year B 135 G 183 890

Report

Revenue =D3 K =G27+G24 =J3

Expenses =D4 =G4 =J4

Dividends declared =D5 =G5 Q =J29+J27-J30

Additional Investment by Stockholders =D6 =G6 =J6

Net Income E =D23-D24 =G7 P =J23-J24

Retained Earnings

Beginning of year =D9 =G9 =J9

End of Year D =D27+D29-D25 J =G29+G27-G25 =J10

Paid in Capital

Beginning of year =D12 =G12 N =J33-J26

End of Year C =D32+D26 H =G32+G26 =J13

Total Assets

Beginning of year =D15 F =G38+G32+G29 L =J38+J32+J29

End of Year =D16 =G16 M =J39+J33+J30

Total Liabilities

Beginning of year A =D35-D32-D29 =G18 =J18

End of Year B =D36-D33-D30 G =G36-G33-G30 =J19

case 1 case 2 case 3

case 1 case 2 case 3

Page12

Q9 Debit and credit balances

Debit- Assets, Contra Liability, Drawings, Expenses

Credit- Liability, Contra Asset, Owner’s Equity, Revenue

Q9 Debit and credit balances

Debit- Assets, Contra Liability, Drawings, Expenses

Credit- Liability, Contra Asset, Owner’s Equity, Revenue

Page13

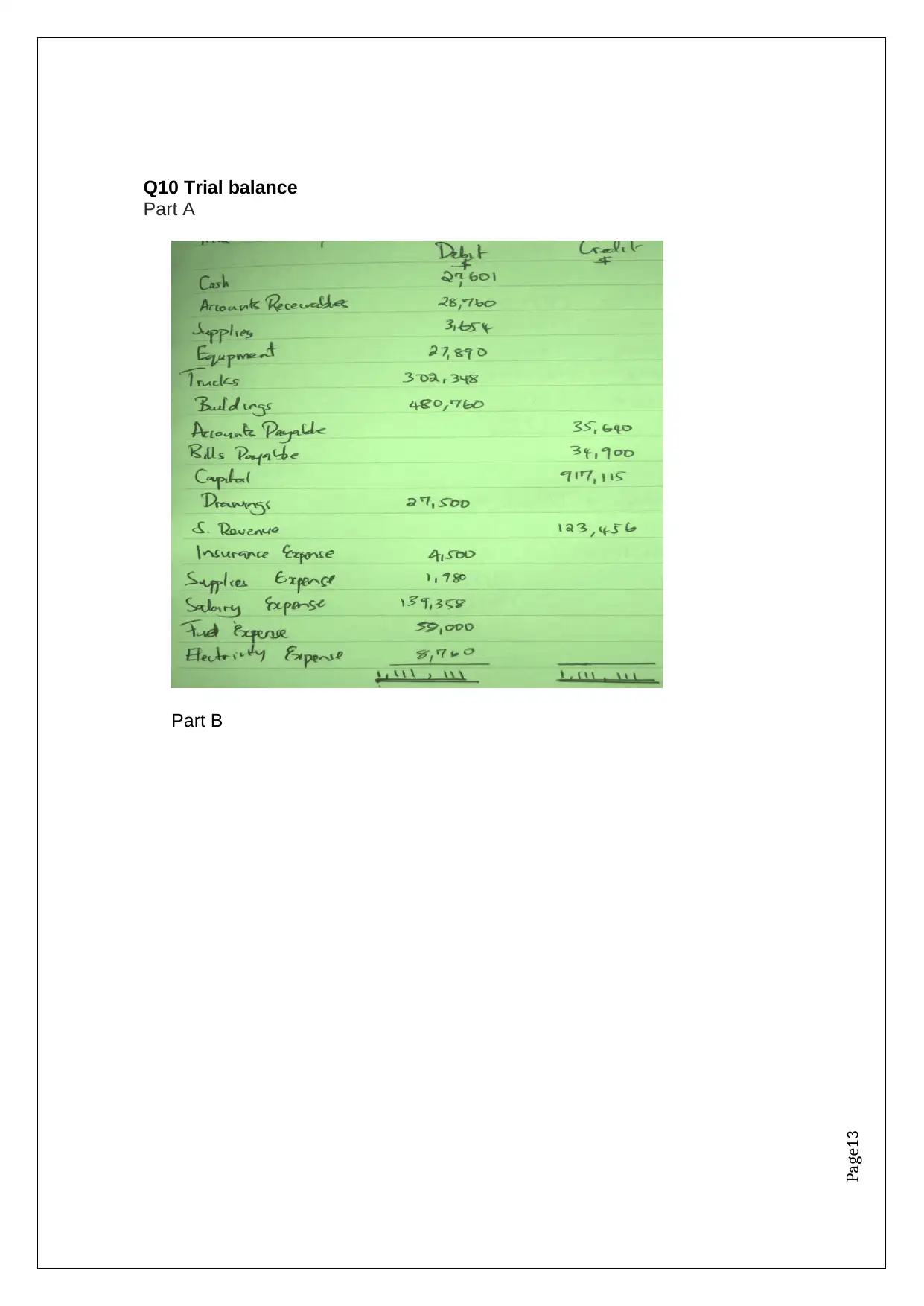

Q10 Trial balance

Part A

Part B

Q10 Trial balance

Part A

Part B

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

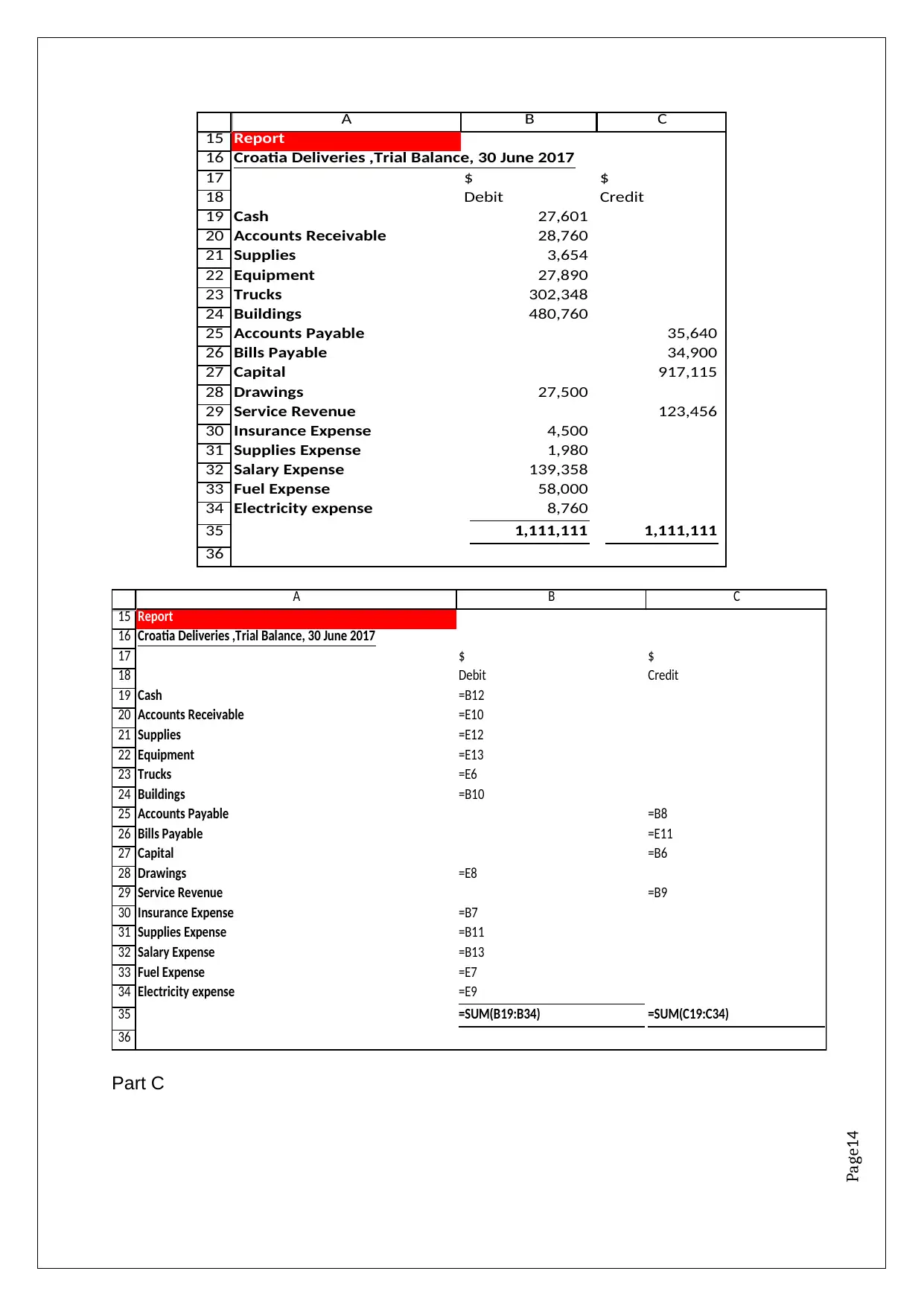

A B C

Report

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash 27,601

Accounts Receivable 28,760

Supplies 3,654

Equipment 27,890

Trucks 302,348

Buildings 480,760

Accounts Payable 35,640

Bills Payable 34,900

Capital 917,115

Drawings 27,500

Service Revenue 123,456

Insurance Expense 4,500

Supplies Expense 1,980

Salary Expense 139,358

Fuel Expense 58,000

Electricity expense 8,760

1,111,111 1,111,111

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

A B C

Report

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash =B12

Accounts Receivable =E10

Supplies =E12

Equipment =E13

Trucks =E6

Buildings =B10

Accounts Payable =B8

Bills Payable =E11

Capital =B6

Drawings =E8

Service Revenue =B9

Insurance Expense =B7

Supplies Expense =B11

Salary Expense =B13

Fuel Expense =E7

Electricity expense =E9

=SUM(B19:B34) =SUM(C19:C34)

Part C

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

A B C

Report

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash 27,601

Accounts Receivable 28,760

Supplies 3,654

Equipment 27,890

Trucks 302,348

Buildings 480,760

Accounts Payable 35,640

Bills Payable 34,900

Capital 917,115

Drawings 27,500

Service Revenue 123,456

Insurance Expense 4,500

Supplies Expense 1,980

Salary Expense 139,358

Fuel Expense 58,000

Electricity expense 8,760

1,111,111 1,111,111

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

A B C

Report

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash =B12

Accounts Receivable =E10

Supplies =E12

Equipment =E13

Trucks =E6

Buildings =B10

Accounts Payable =B8

Bills Payable =E11

Capital =B6

Drawings =E8

Service Revenue =B9

Insurance Expense =B7

Supplies Expense =B11

Salary Expense =B13

Fuel Expense =E7

Electricity expense =E9

=SUM(B19:B34) =SUM(C19:C34)

Part C

Page15

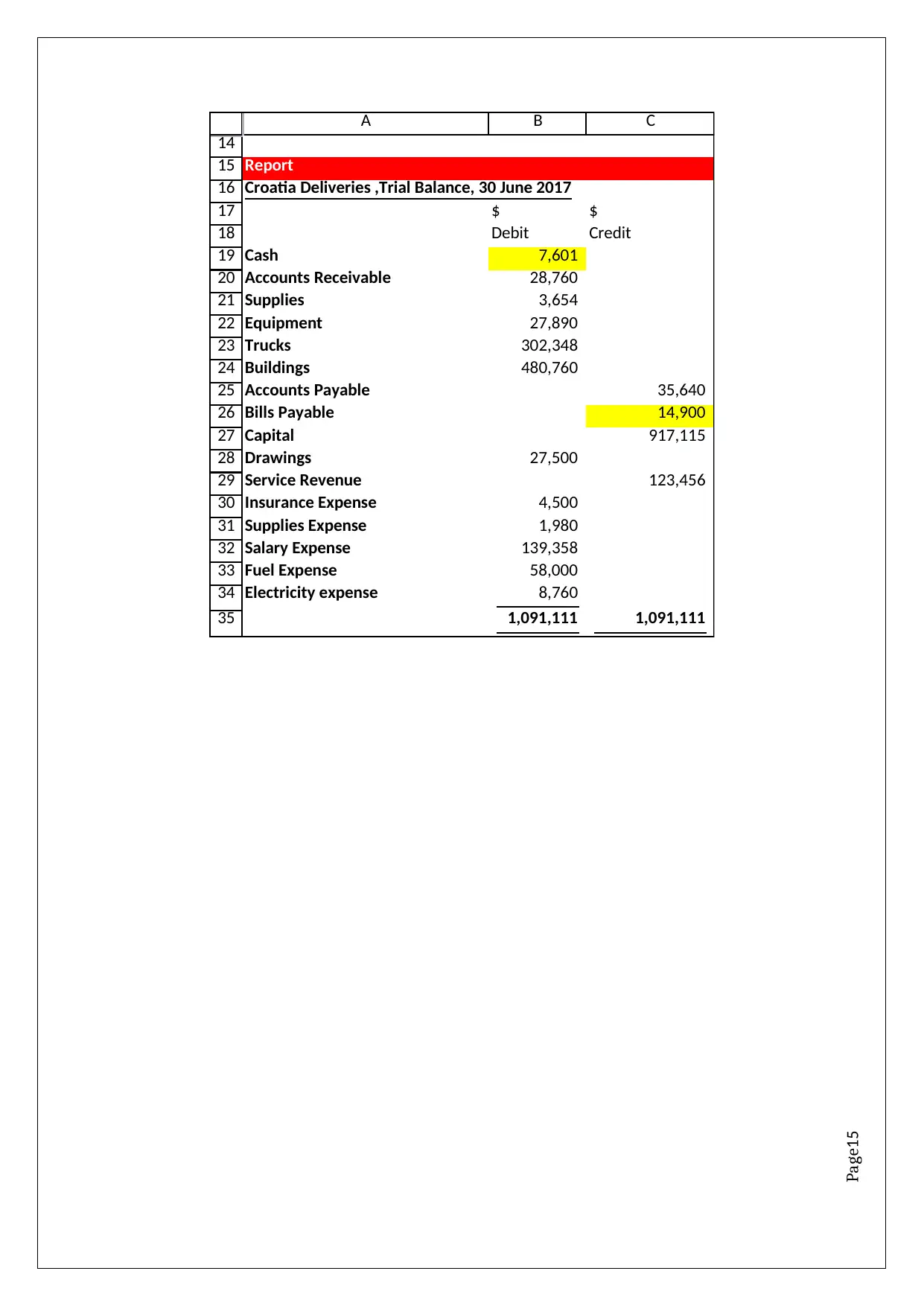

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

A B C

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash 7,601

Accounts Receivable 28,760

Supplies 3,654

Equipment 27,890

Trucks 302,348

Buildings 480,760

Accounts Payable 35,640

Bills Payable 14,900

Capital 917,115

Drawings 27,500

Service Revenue 123,456

Insurance Expense 4,500

Supplies Expense 1,980

Salary Expense 139,358

Fuel Expense 58,000

Electricity expense 8,760

1,091,111 1,091,111

Report

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

A B C

Croatia Deliveries ,Trial Balance, 30 June 2017

$ $

Debit Credit

Cash 7,601

Accounts Receivable 28,760

Supplies 3,654

Equipment 27,890

Trucks 302,348

Buildings 480,760

Accounts Payable 35,640

Bills Payable 14,900

Capital 917,115

Drawings 27,500

Service Revenue 123,456

Insurance Expense 4,500

Supplies Expense 1,980

Salary Expense 139,358

Fuel Expense 58,000

Electricity expense 8,760

1,091,111 1,091,111

Report

Page16

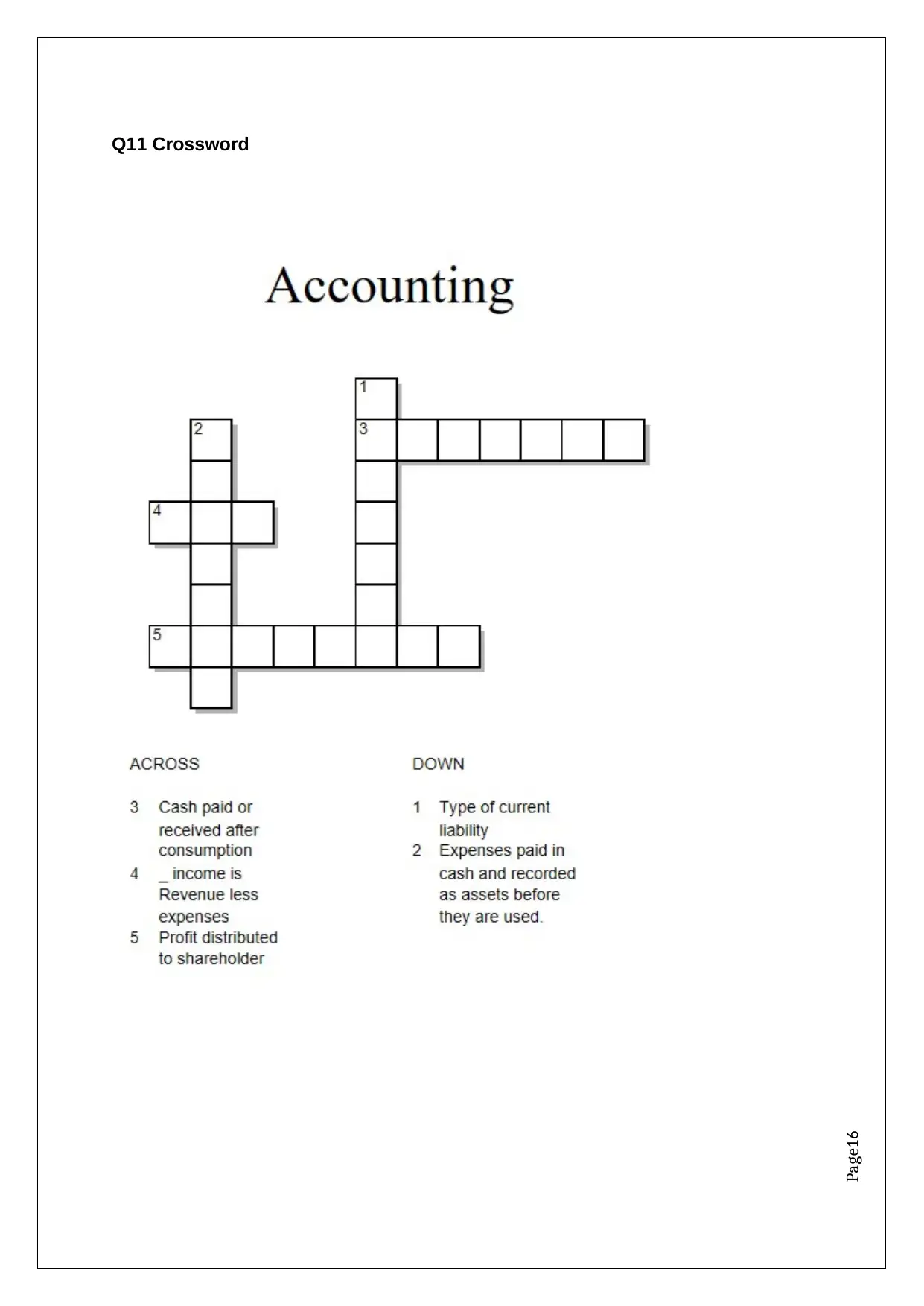

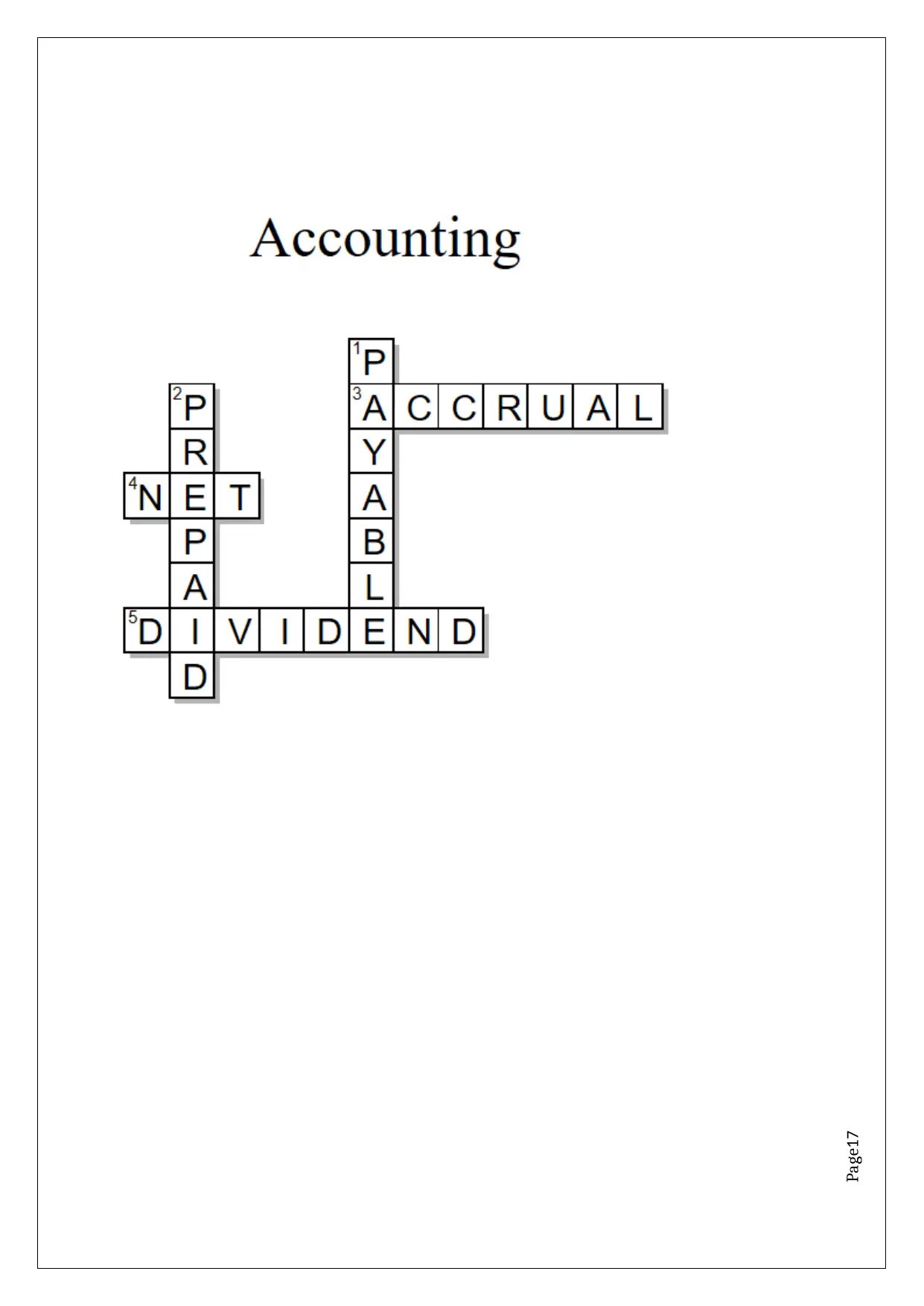

Q11 Crossword

Q11 Crossword

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page17

Page18

Q12 Solution

Unearned Service Revenue

Prepaid expenses

Depreciation Expense

Accrued Revenue

Example 1

Annual subscription fees of $1200 paid in advance would be adjusted after one

month as below:

Debit Credit

Unearned Service Revenue 100

Revenue 100

Example 2

A company that pays insurance in advance of $1200 would be adjusted after one

month as below:

Debit Credit

Insurance expense 100

Prepaid Insurance 100

Q13 TypesLiabilities

Current liabilities are financial obligations due by company within the current year.

Non-current liabilities are long term financial obligations i.e outside the current year

e.g. bonds payable and long term lease(Investopidia, 2017).

Q14 Ratios

Current ratio = current assets/current liabilities

Current ratio is a type of liquidity ratio in financial analysis. It is used to measures the

company’s ability to meet its short term obligations.

Q12 Solution

Unearned Service Revenue

Prepaid expenses

Depreciation Expense

Accrued Revenue

Example 1

Annual subscription fees of $1200 paid in advance would be adjusted after one

month as below:

Debit Credit

Unearned Service Revenue 100

Revenue 100

Example 2

A company that pays insurance in advance of $1200 would be adjusted after one

month as below:

Debit Credit

Insurance expense 100

Prepaid Insurance 100

Q13 TypesLiabilities

Current liabilities are financial obligations due by company within the current year.

Non-current liabilities are long term financial obligations i.e outside the current year

e.g. bonds payable and long term lease(Investopidia, 2017).

Q14 Ratios

Current ratio = current assets/current liabilities

Current ratio is a type of liquidity ratio in financial analysis. It is used to measures the

company’s ability to meet its short term obligations.

Page19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page20

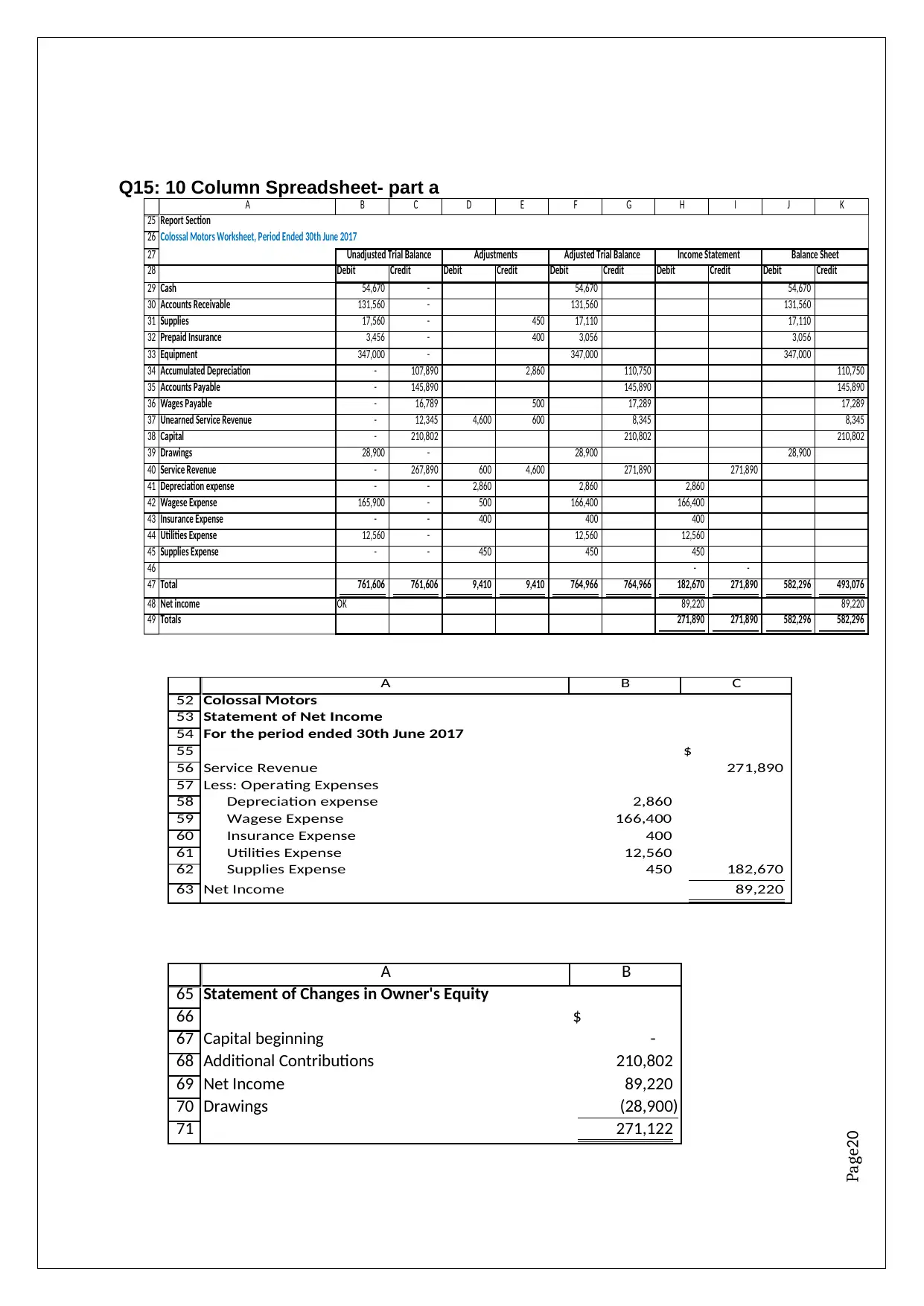

Q15: 10 Column Spreadsheet- part a

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

A B C D E F G H I J K

Report Section

Colossal Motors Worksheet, Period Ended 30th June 2017

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 54,670 - 54,670 54,670

Accounts Receivable 131,560 - 131,560 131,560

Supplies 17,560 - 450 17,110 17,110

Prepaid Insurance 3,456 - 400 3,056 3,056

Equipment 347,000 - 347,000 347,000

Accumulated Depreciation - 107,890 2,860 110,750 110,750

Accounts Payable - 145,890 145,890 145,890

Wages Payable - 16,789 500 17,289 17,289

Unearned Service Revenue - 12,345 4,600 600 8,345 8,345

Capital - 210,802 210,802 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 271,890

Depreciation expense - - 2,860 2,860 2,860

Wagese Expense 165,900 - 500 166,400 166,400

Insurance Expense - - 400 400 400

Utilities Expense 12,560 - 12,560 12,560

Supplies Expense - - 450 450 450

- -

Total 761,606 761,606 9,410 9,410 764,966 764,966 182,670 271,890 582,296 493,076

Net income OK 89,220 89,220

Totals 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

52

53

54

55

56

57

58

59

60

61

62

63

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June 2017

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 166,400

Insurance Expense 400

Utilities Expense 12,560

Supplies Expense 450 182,670

Net Income 89,220

65

66

67

68

69

70

71

A B

Statement of Changes in Owner's Equity

$

Capital beginning -

Additional Contributions 210,802

Net Income 89,220

Drawings (28,900)

271,122

Q15: 10 Column Spreadsheet- part a

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

A B C D E F G H I J K

Report Section

Colossal Motors Worksheet, Period Ended 30th June 2017

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 54,670 - 54,670 54,670

Accounts Receivable 131,560 - 131,560 131,560

Supplies 17,560 - 450 17,110 17,110

Prepaid Insurance 3,456 - 400 3,056 3,056

Equipment 347,000 - 347,000 347,000

Accumulated Depreciation - 107,890 2,860 110,750 110,750

Accounts Payable - 145,890 145,890 145,890

Wages Payable - 16,789 500 17,289 17,289

Unearned Service Revenue - 12,345 4,600 600 8,345 8,345

Capital - 210,802 210,802 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 271,890

Depreciation expense - - 2,860 2,860 2,860

Wagese Expense 165,900 - 500 166,400 166,400

Insurance Expense - - 400 400 400

Utilities Expense 12,560 - 12,560 12,560

Supplies Expense - - 450 450 450

- -

Total 761,606 761,606 9,410 9,410 764,966 764,966 182,670 271,890 582,296 493,076

Net income OK 89,220 89,220

Totals 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

52

53

54

55

56

57

58

59

60

61

62

63

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June 2017

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 166,400

Insurance Expense 400

Utilities Expense 12,560

Supplies Expense 450 182,670

Net Income 89,220

65

66

67

68

69

70

71

A B

Statement of Changes in Owner's Equity

$

Capital beginning -

Additional Contributions 210,802

Net Income 89,220

Drawings (28,900)

271,122

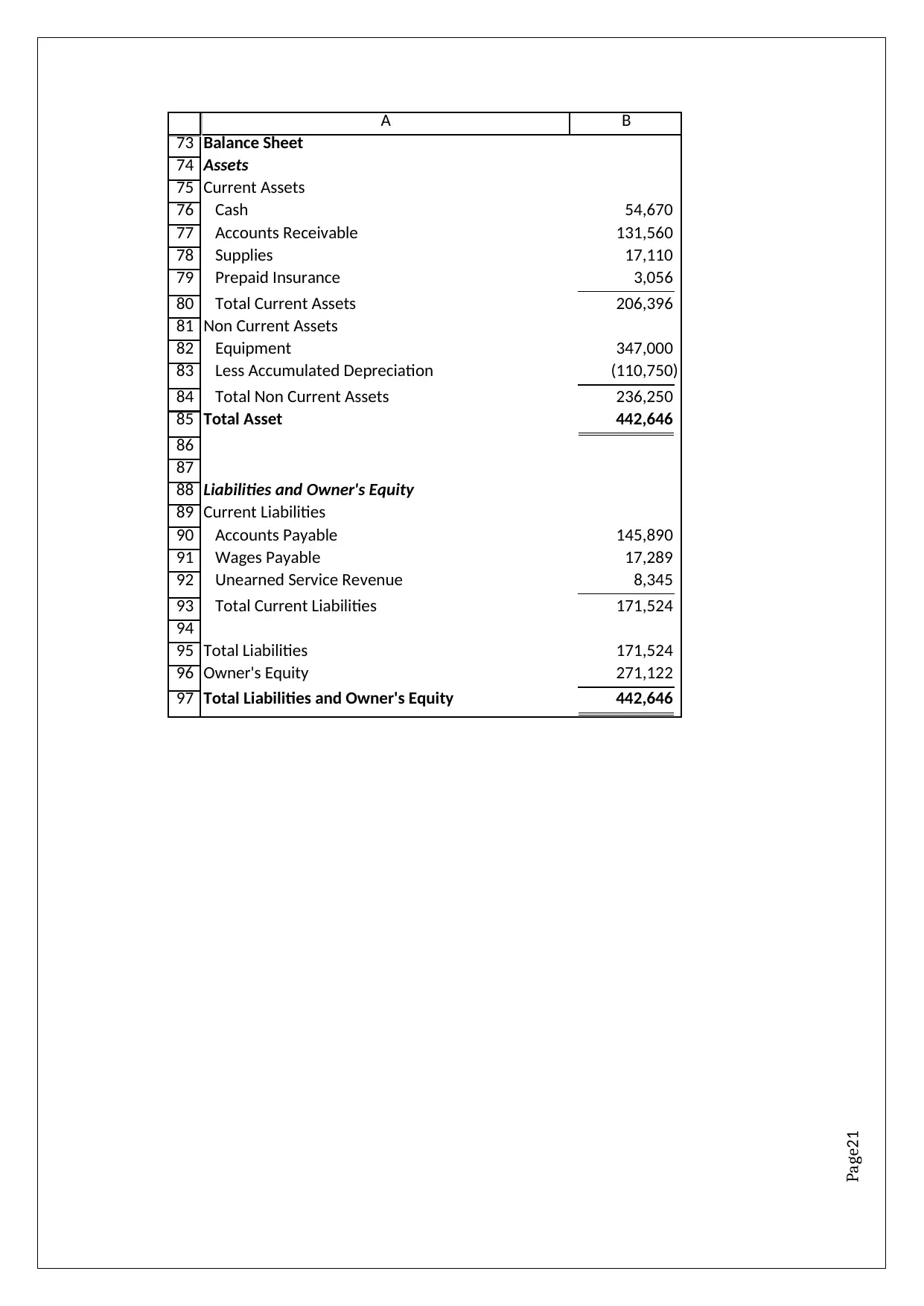

Page21

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

A B

Balance Sheet

Assets

Current Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Total Current Assets 206,396

Non Current Assets

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Non Current Assets 236,250

Total Asset 442,646

Liabilities and Owner's Equity

Current Liabilities

Accounts Payable 145,890

Wages Payable 17,289

Unearned Service Revenue 8,345

Total Current Liabilities 171,524

Total Liabilities 171,524

Owner's Equity 271,122

Total Liabilities and Owner's Equity 442,646

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

A B

Balance Sheet

Assets

Current Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Total Current Assets 206,396

Non Current Assets

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Non Current Assets 236,250

Total Asset 442,646

Liabilities and Owner's Equity

Current Liabilities

Accounts Payable 145,890

Wages Payable 17,289

Unearned Service Revenue 8,345

Total Current Liabilities 171,524

Total Liabilities 171,524

Owner's Equity 271,122

Total Liabilities and Owner's Equity 442,646

Page22

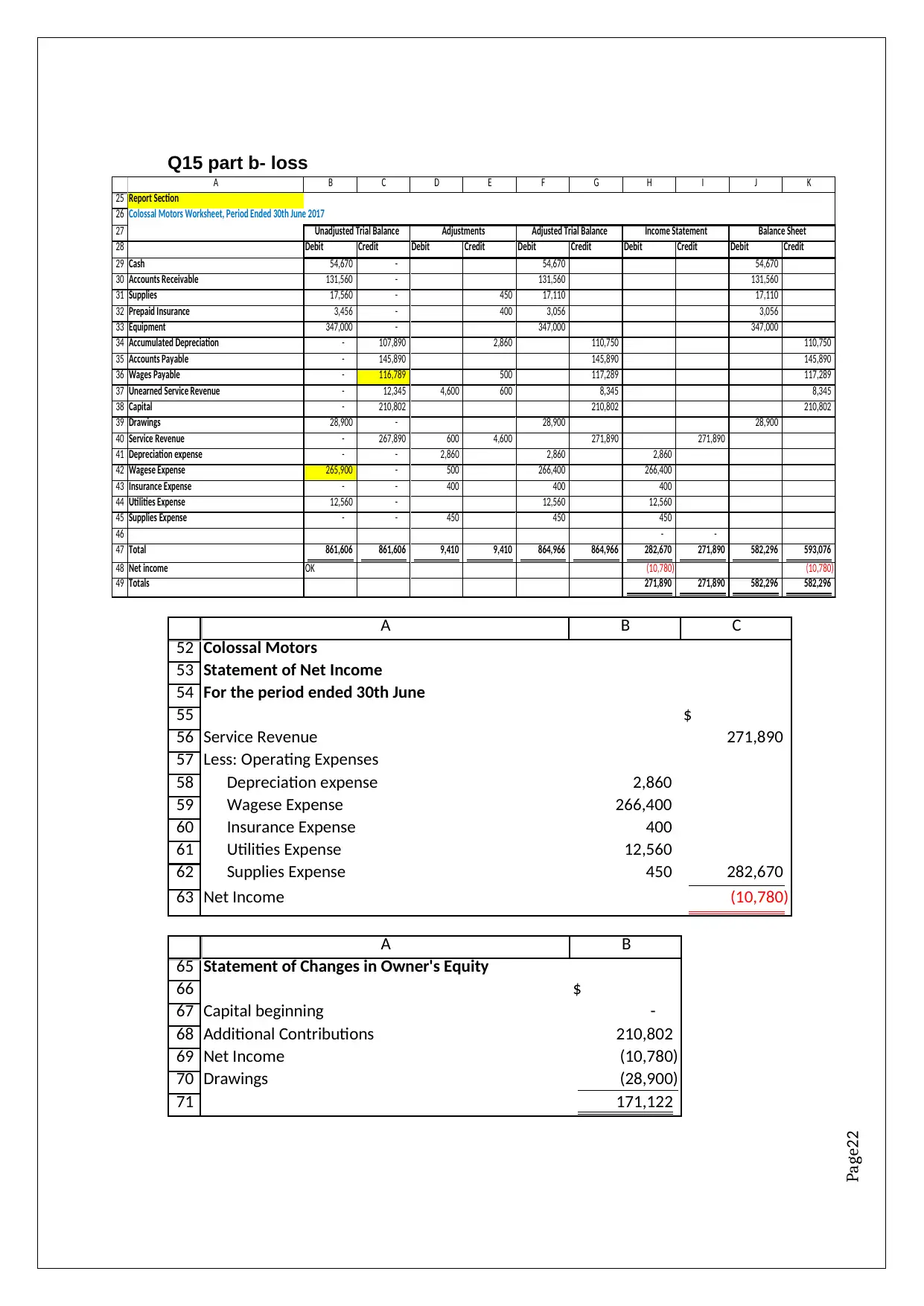

Q15 part b- loss

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

A B C D E F G H I J K

Report Section

Colossal Motors Worksheet, Period Ended 30th June 2017

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 54,670 - 54,670 54,670

Accounts Receivable 131,560 - 131,560 131,560

Supplies 17,560 - 450 17,110 17,110

Prepaid Insurance 3,456 - 400 3,056 3,056

Equipment 347,000 - 347,000 347,000

Accumulated Depreciation - 107,890 2,860 110,750 110,750

Accounts Payable - 145,890 145,890 145,890

Wages Payable - 116,789 500 117,289 117,289

Unearned Service Revenue - 12,345 4,600 600 8,345 8,345

Capital - 210,802 210,802 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 271,890

Depreciation expense - - 2,860 2,860 2,860

Wagese Expense 265,900 - 500 266,400 266,400

Insurance Expense - - 400 400 400

Utilities Expense 12,560 - 12,560 12,560

Supplies Expense - - 450 450 450

- -

Total 861,606 861,606 9,410 9,410 864,966 864,966 282,670 271,890 582,296 593,076

Net income OK (10,780) (10,780)

Totals 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

52

53

54

55

56

57

58

59

60

61

62

63

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 266,400

Insurance Expense 400

Utilities Expense 12,560

Supplies Expense 450 282,670

Net Income (10,780)

65

66

67

68

69

70

71

A B

Statement of Changes in Owner's Equity

$

Capital beginning -

Additional Contributions 210,802

Net Income (10,780)

Drawings (28,900)

171,122

Q15 part b- loss

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

A B C D E F G H I J K

Report Section

Colossal Motors Worksheet, Period Ended 30th June 2017

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 54,670 - 54,670 54,670

Accounts Receivable 131,560 - 131,560 131,560

Supplies 17,560 - 450 17,110 17,110

Prepaid Insurance 3,456 - 400 3,056 3,056

Equipment 347,000 - 347,000 347,000

Accumulated Depreciation - 107,890 2,860 110,750 110,750

Accounts Payable - 145,890 145,890 145,890

Wages Payable - 116,789 500 117,289 117,289

Unearned Service Revenue - 12,345 4,600 600 8,345 8,345

Capital - 210,802 210,802 210,802

Drawings 28,900 - 28,900 28,900

Service Revenue - 267,890 600 4,600 271,890 271,890

Depreciation expense - - 2,860 2,860 2,860

Wagese Expense 265,900 - 500 266,400 266,400

Insurance Expense - - 400 400 400

Utilities Expense 12,560 - 12,560 12,560

Supplies Expense - - 450 450 450

- -

Total 861,606 861,606 9,410 9,410 864,966 864,966 282,670 271,890 582,296 593,076

Net income OK (10,780) (10,780)

Totals 271,890 271,890 582,296 582,296

Unadjusted Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet

52

53

54

55

56

57

58

59

60

61

62

63

A B C

Colossal Motors

Statement of Net Income

For the period ended 30th June

$

Service Revenue 271,890

Less: Operating Expenses

Depreciation expense 2,860

Wagese Expense 266,400

Insurance Expense 400

Utilities Expense 12,560

Supplies Expense 450 282,670

Net Income (10,780)

65

66

67

68

69

70

71

A B

Statement of Changes in Owner's Equity

$

Capital beginning -

Additional Contributions 210,802

Net Income (10,780)

Drawings (28,900)

171,122

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

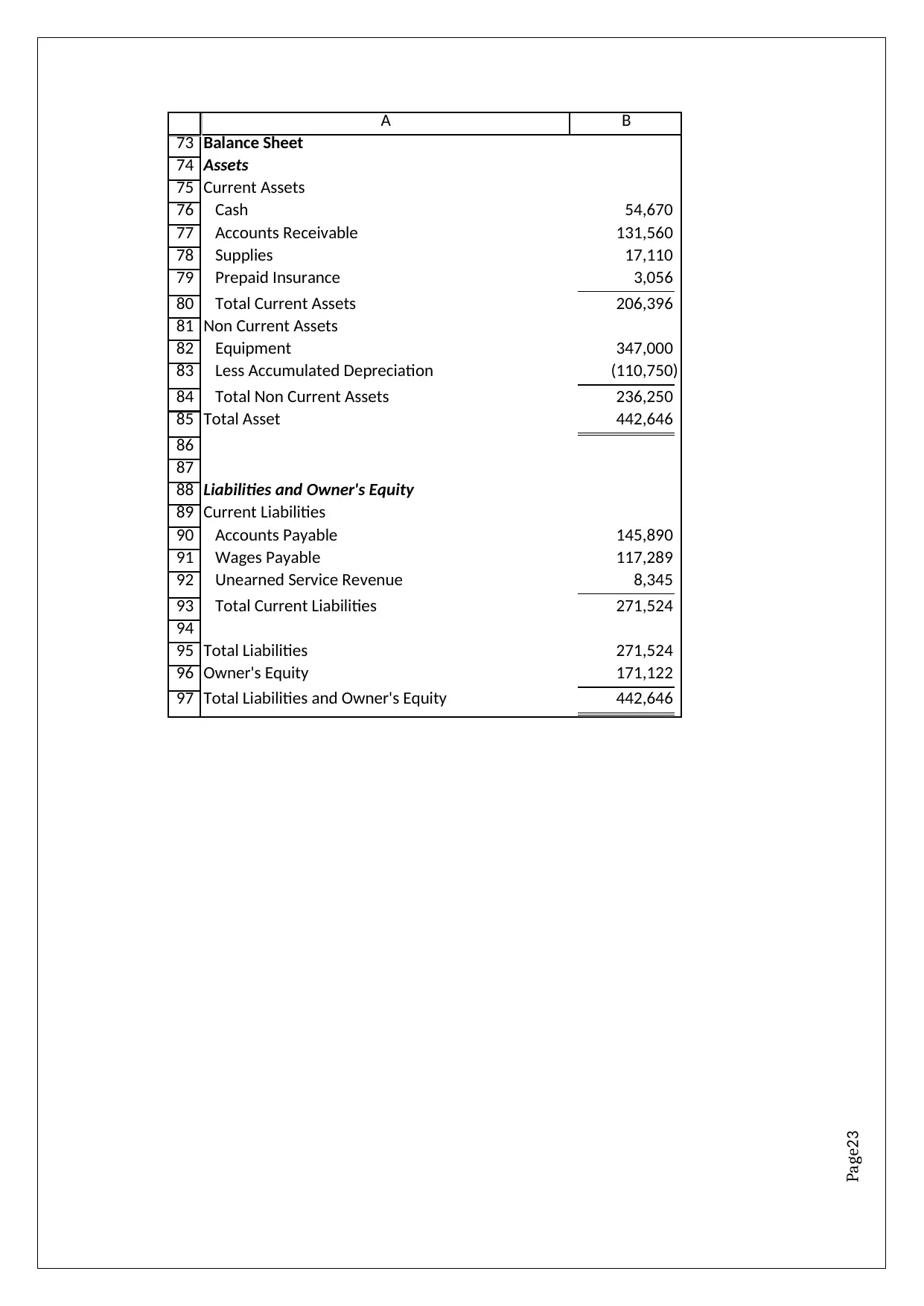

Page23

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

A B

Balance Sheet

Assets

Current Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Total Current Assets 206,396

Non Current Assets

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Non Current Assets 236,250

Total Asset 442,646

Liabilities and Owner's Equity

Current Liabilities

Accounts Payable 145,890

Wages Payable 117,289

Unearned Service Revenue 8,345

Total Current Liabilities 271,524

Total Liabilities 271,524

Owner's Equity 171,122

Total Liabilities and Owner's Equity 442,646

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

A B

Balance Sheet

Assets

Current Assets

Cash 54,670

Accounts Receivable 131,560

Supplies 17,110

Prepaid Insurance 3,056

Total Current Assets 206,396

Non Current Assets

Equipment 347,000

Less Accumulated Depreciation (110,750)

Total Non Current Assets 236,250

Total Asset 442,646

Liabilities and Owner's Equity

Current Liabilities

Accounts Payable 145,890

Wages Payable 117,289

Unearned Service Revenue 8,345

Total Current Liabilities 271,524

Total Liabilities 271,524

Owner's Equity 171,122

Total Liabilities and Owner's Equity 442,646

Page24

References

Investopidia. (2017). Terms. Retrieved from Investopidia:

www.investopidia.com/terms/n/noncurrent-liabilities.asp

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia.

Kumar, V. (2008, December 1). E-Accounting. Retrieved from Accounting Education:

http://www.svtuition.org/2008/12/e-accounting.html

Microsoft. (2017). Print row and column headings. Retrieved from Support Office:

https://support.office.com/en-gb/article/Print-row-and-column-headings-de41db7e-b716-

4d8b-a5fd-5fb50645101f

References

Investopidia. (2017). Terms. Retrieved from Investopidia:

www.investopidia.com/terms/n/noncurrent-liabilities.asp

Koch, D. (2009, November). The ABC of a Corporate Collapse. CPA Australia.

Kumar, V. (2008, December 1). E-Accounting. Retrieved from Accounting Education:

http://www.svtuition.org/2008/12/e-accounting.html

Microsoft. (2017). Print row and column headings. Retrieved from Support Office:

https://support.office.com/en-gb/article/Print-row-and-column-headings-de41db7e-b716-

4d8b-a5fd-5fb50645101f

1 out of 24

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.