University Finance: Profit Before Tax Calculation and Analysis Report

VerifiedAdded on 2023/06/04

|9

|923

|463

Report

AI Summary

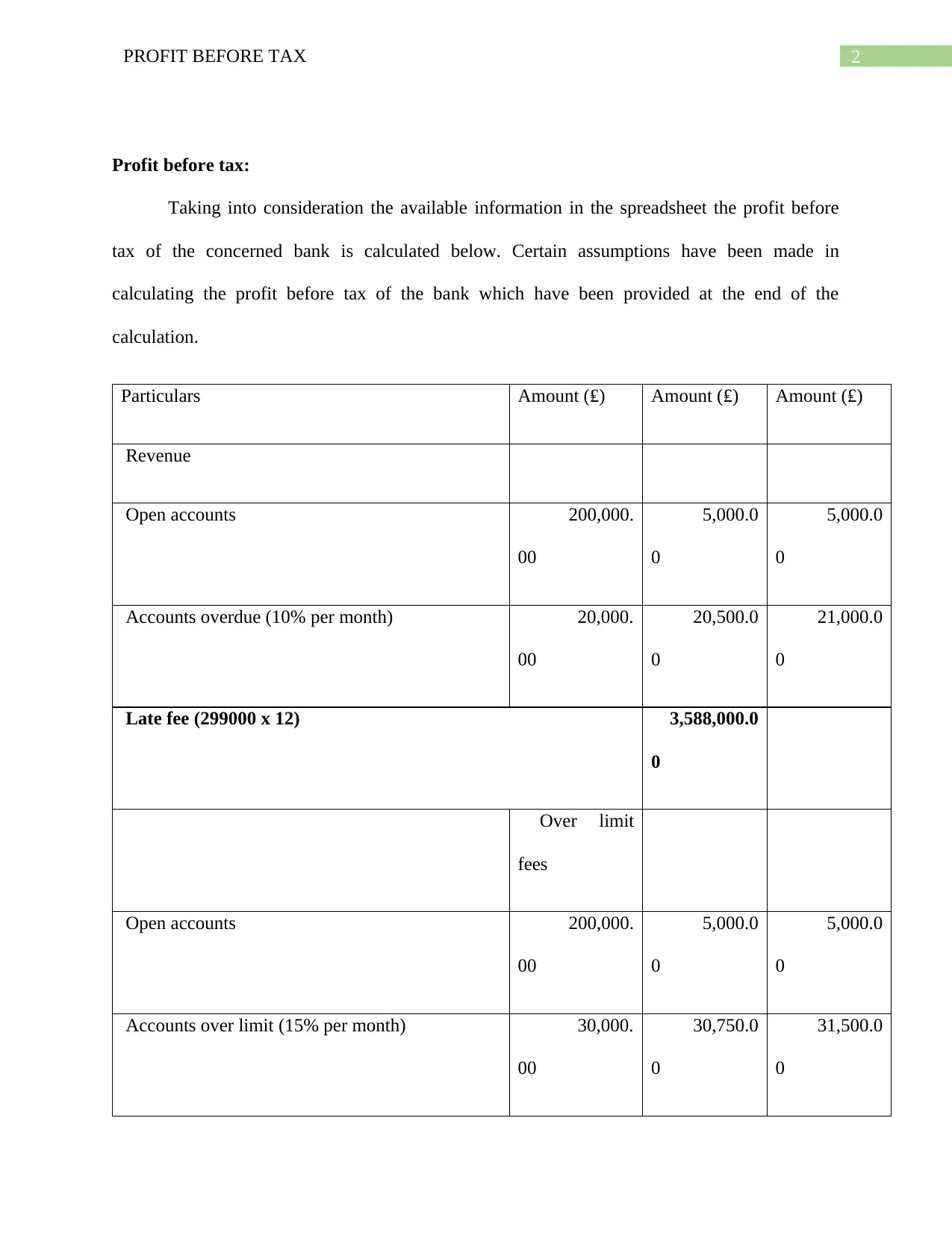

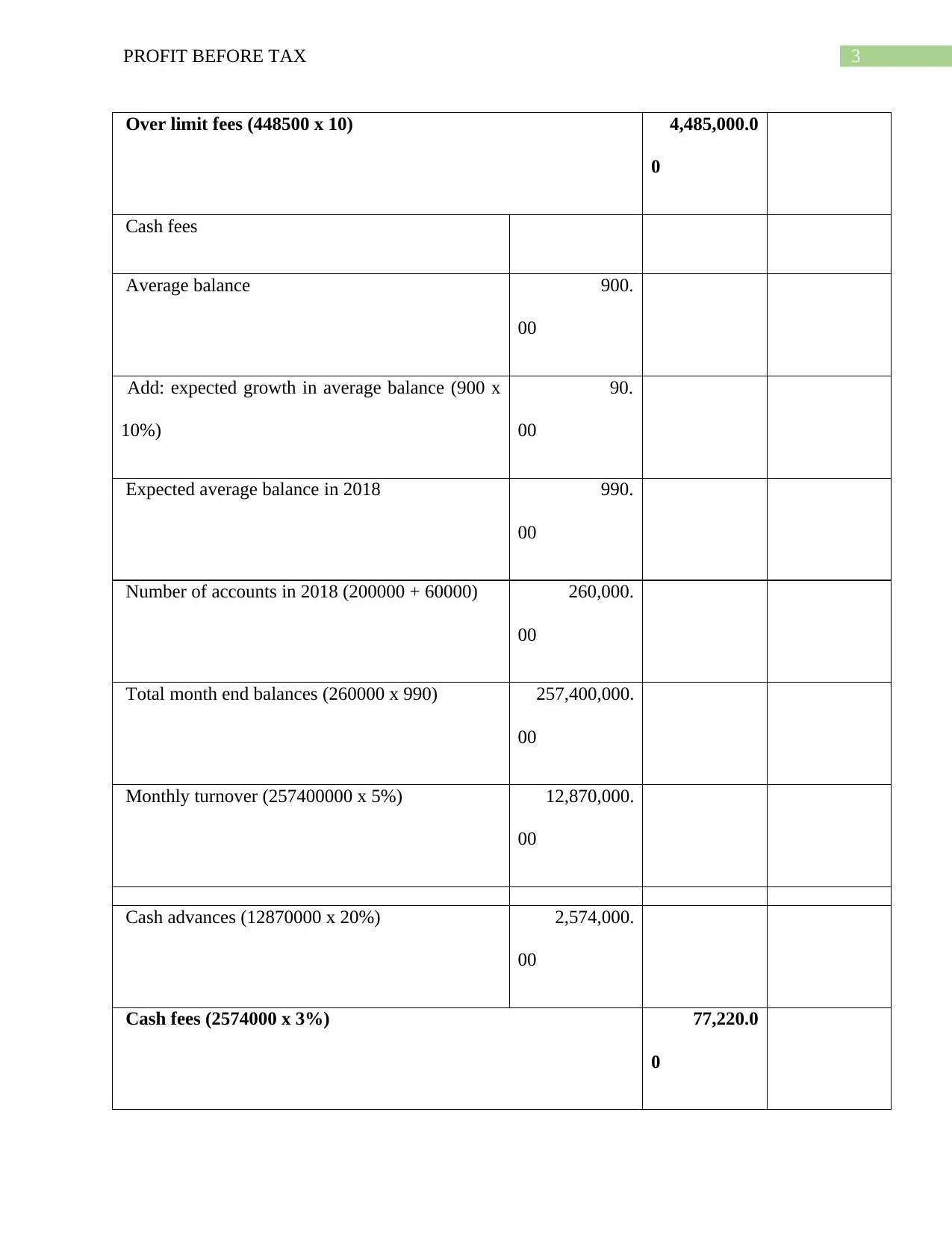

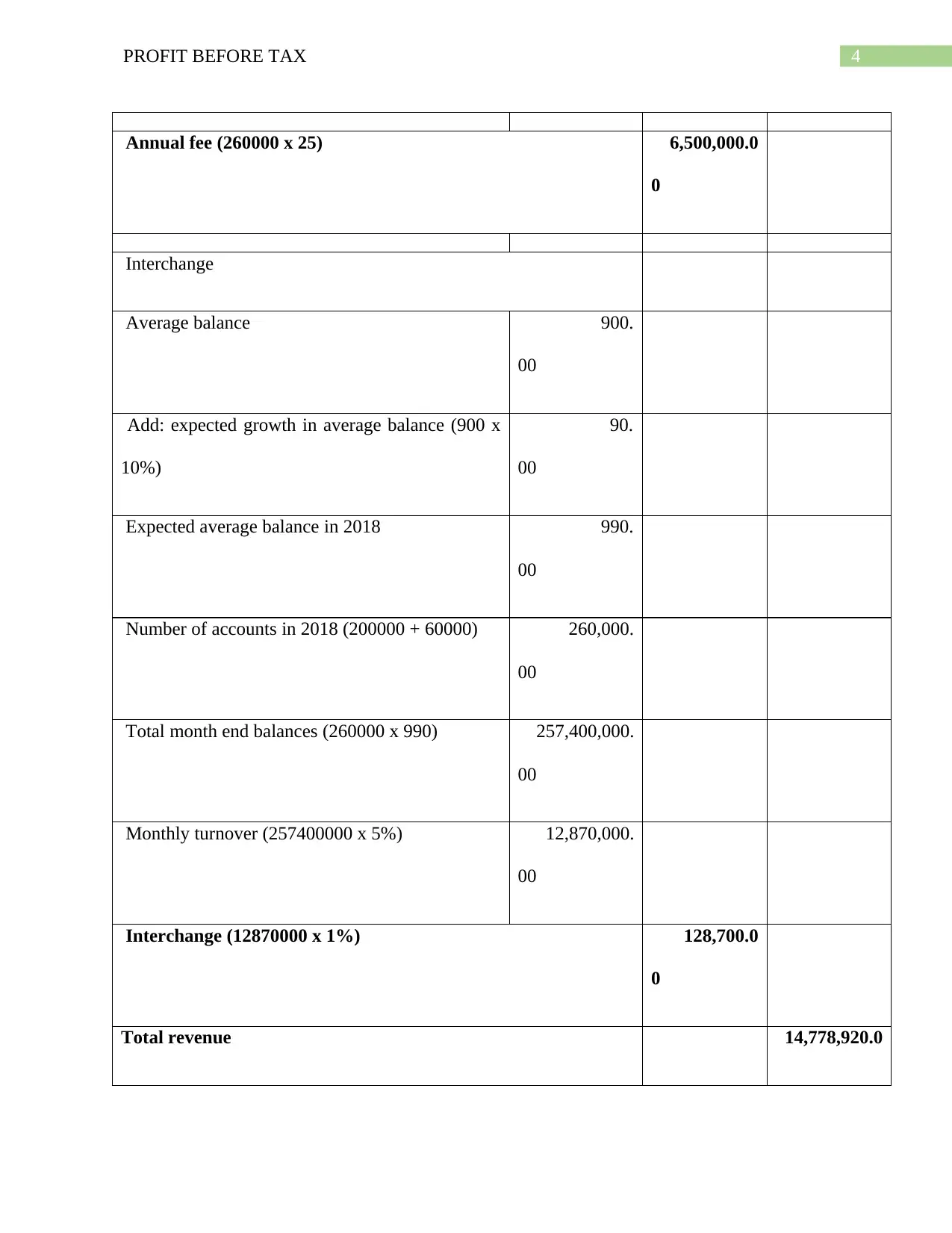

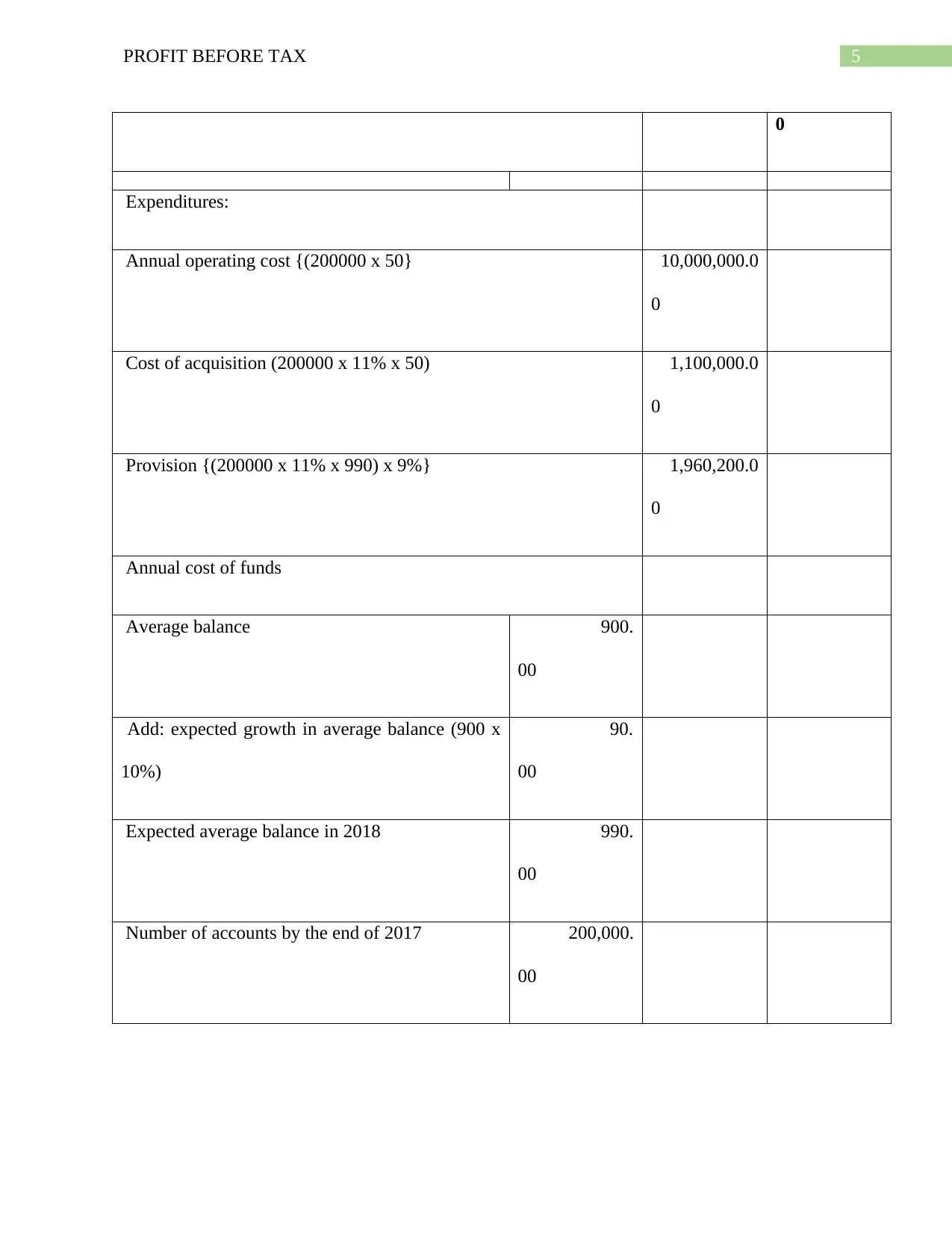

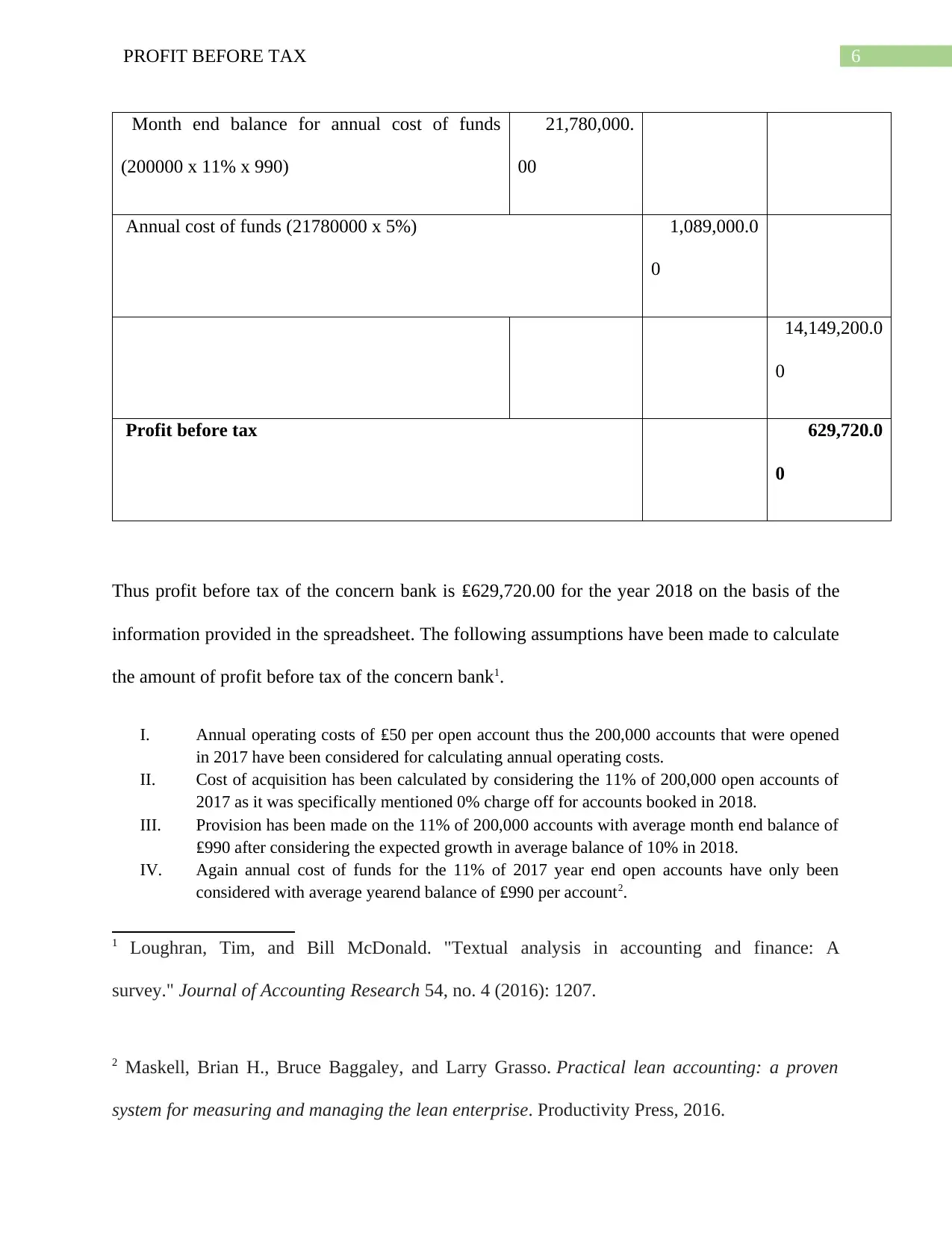

This report provides a detailed calculation of a bank's profit before tax for the year 2018, based on provided financial information. The analysis includes a breakdown of revenue streams, such as open accounts, late fees, over-limit fees, cash fees, annual fees, and interchange. It also considers expenditures, including annual operating costs, cost of acquisition, and provision for potential losses, and annual cost of funds. The report highlights key assumptions made during the calculation process, such as the annual operating cost per account, and the percentage used for calculating cost of acquisition and provision. The final profit before tax is determined to be £629,720.00. The report includes definitions of key terms like monthly turnover, annual fees, total revenue, annual operating costs, and provision. It also provides references to relevant accounting and finance literature.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.