Managing Human and Financial Resources Assessment 2022

VerifiedAdded on 2022/09/25

|13

|2383

|51

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Student Number (s):

Programme:(e.g. Business

Management)

Module Title: (e.g. Studying

for Business)

Managing Human and Financial

Resources

Seminar

Group

Module Code: HR7003 Word Count

In submitting this assessment, I confirm that no part of this assignment. Except were quoted

and referenced. Has been copied from material belonging to any other person e.g. from a

book. Hand-out, another student. I am aware that it is a breach of UEL regulations to copy

the work of another without clear acknowledgment and that attempting to do so renders me

liable to disciplinary proceedings.

1

Programme:(e.g. Business

Management)

Module Title: (e.g. Studying

for Business)

Managing Human and Financial

Resources

Seminar

Group

Module Code: HR7003 Word Count

In submitting this assessment, I confirm that no part of this assignment. Except were quoted

and referenced. Has been copied from material belonging to any other person e.g. from a

book. Hand-out, another student. I am aware that it is a breach of UEL regulations to copy

the work of another without clear acknowledgment and that attempting to do so renders me

liable to disciplinary proceedings.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive summary

The main focus of this report was on providing a variance analysis report by comparing

actual data and estimated data provided by the management. Based on such analysis, it can be

said that the overall cost of operation has exceeded its estimation which has resulted in a

negative impact on the profit generation capabilities of the company. It can be said that due to

inefficient budgeting activities overall profit generation capabilities of Fleet Highland Cafe

have decreased by 13%.

2

The main focus of this report was on providing a variance analysis report by comparing

actual data and estimated data provided by the management. Based on such analysis, it can be

said that the overall cost of operation has exceeded its estimation which has resulted in a

negative impact on the profit generation capabilities of the company. It can be said that due to

inefficient budgeting activities overall profit generation capabilities of Fleet Highland Cafe

have decreased by 13%.

2

Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

A) The objective of preparing the budget..................................................................................5

B) The report showing the company’s revenue and spending variance.....................................7

C) The variance of concern for the management.......................................................................9

D) Recommendation to survive and maintain profitability......................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

3

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

A) The objective of preparing the budget..................................................................................5

B) The report showing the company’s revenue and spending variance.....................................7

C) The variance of concern for the management.......................................................................9

D) Recommendation to survive and maintain profitability......................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

3

Introduction

The primary objective of this report is to conduct variance analysis following the budget

prepared by the organization. Data concerning the budgeting process and actual data recorded

by the accounting department has been described in the given scenario. The main objective of

the managers will be to identify whether the financial performance of the organization has

been following the developed budgets. This report will help in identifying variances between

the budgeted and actual performance of the company (Jones et.al, 2018). In addition to those

objectives of preparing a budget will also be described in this report along with providing

some recommendations based on variance analysis for the management of Fleet Highlands

Cafe.

4

The primary objective of this report is to conduct variance analysis following the budget

prepared by the organization. Data concerning the budgeting process and actual data recorded

by the accounting department has been described in the given scenario. The main objective of

the managers will be to identify whether the financial performance of the organization has

been following the developed budgets. This report will help in identifying variances between

the budgeted and actual performance of the company (Jones et.al, 2018). In addition to those

objectives of preparing a budget will also be described in this report along with providing

some recommendations based on variance analysis for the management of Fleet Highlands

Cafe.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

A) The objective of preparing the budget

Following are some of the objectives that could have been considered by the management of

Fleet Highlands Cafe before the development of the budgets-

Cost controlling- One of the primary objectives of any business organization behind the

preparation of the budget is controlling the cost of operation. The function that is performed

in the budgeting process is to identify cost elements and develop standards for each of the

elements identified in this process. Example management of the organization will identify

marketing expenses as cost elements and decide a standard based on past marketing expenses

undertaken by the company. The type of standard will help the organization to ensure that all

the activities are under the planning.

Allocation of resources- Another important objective of business that is achieved with the

help of budgeting processes is the allocation of different resources available with the

organization (Marzlin Marzuki & Ismail, 2019). Financial resources and other resources are

generally available in limited nature with any business organization and such organizations

need to make sure that every business activity is getting the appropriate amount of financial

resources to generate revenue for the company. In addition to that other resources such as

human resources can also be allocated based on the priority given to a particular cost element.

Financial performance analysis- Financial analysis of a business organization can also be

conducted with the help of variance analysis which is an integral part of the budgeting

process. This type of analysis helps a business organization to identify the areas of concerned

or problematic areas in a particular organization. For example, if a particular cost element is

exceeding significantly as compared to its standard so that there is a probability that

management is not to operating efficiently concerning such elements. It can be said that the

overall efficiency of business operations can be increased significantly with the help of the

budgeting process (Matsuoka, 2018).

Assignment of priority and resource utilization - The budgeting process will also help in

identifying the significance of a particular cost element on the overall financial and

operational aspects of the business. This type of analysis can help the business organization

to allocate financial resources and other resources such as human resources in a more

effective manner (Kolias and Arnis, 2019). It can be said that the overall resource utilization

of business operations can be increased significantly with the help of priority alignment.

5

Following are some of the objectives that could have been considered by the management of

Fleet Highlands Cafe before the development of the budgets-

Cost controlling- One of the primary objectives of any business organization behind the

preparation of the budget is controlling the cost of operation. The function that is performed

in the budgeting process is to identify cost elements and develop standards for each of the

elements identified in this process. Example management of the organization will identify

marketing expenses as cost elements and decide a standard based on past marketing expenses

undertaken by the company. The type of standard will help the organization to ensure that all

the activities are under the planning.

Allocation of resources- Another important objective of business that is achieved with the

help of budgeting processes is the allocation of different resources available with the

organization (Marzlin Marzuki & Ismail, 2019). Financial resources and other resources are

generally available in limited nature with any business organization and such organizations

need to make sure that every business activity is getting the appropriate amount of financial

resources to generate revenue for the company. In addition to that other resources such as

human resources can also be allocated based on the priority given to a particular cost element.

Financial performance analysis- Financial analysis of a business organization can also be

conducted with the help of variance analysis which is an integral part of the budgeting

process. This type of analysis helps a business organization to identify the areas of concerned

or problematic areas in a particular organization. For example, if a particular cost element is

exceeding significantly as compared to its standard so that there is a probability that

management is not to operating efficiently concerning such elements. It can be said that the

overall efficiency of business operations can be increased significantly with the help of the

budgeting process (Matsuoka, 2018).

Assignment of priority and resource utilization - The budgeting process will also help in

identifying the significance of a particular cost element on the overall financial and

operational aspects of the business. This type of analysis can help the business organization

to allocate financial resources and other resources such as human resources in a more

effective manner (Kolias and Arnis, 2019). It can be said that the overall resource utilization

of business operations can be increased significantly with the help of priority alignment.

5

Governance on operational departments- Governance of operational department by general

managers can also be executed effectively as standard will be set concerning departmental

cost to be spent by an organization. In addition to that direction can also be provided by

managers to employees by the allocated cost (Banerjee, 2019).

6

managers can also be executed effectively as standard will be set concerning departmental

cost to be spent by an organization. In addition to that direction can also be provided by

managers to employees by the allocated cost (Banerjee, 2019).

6

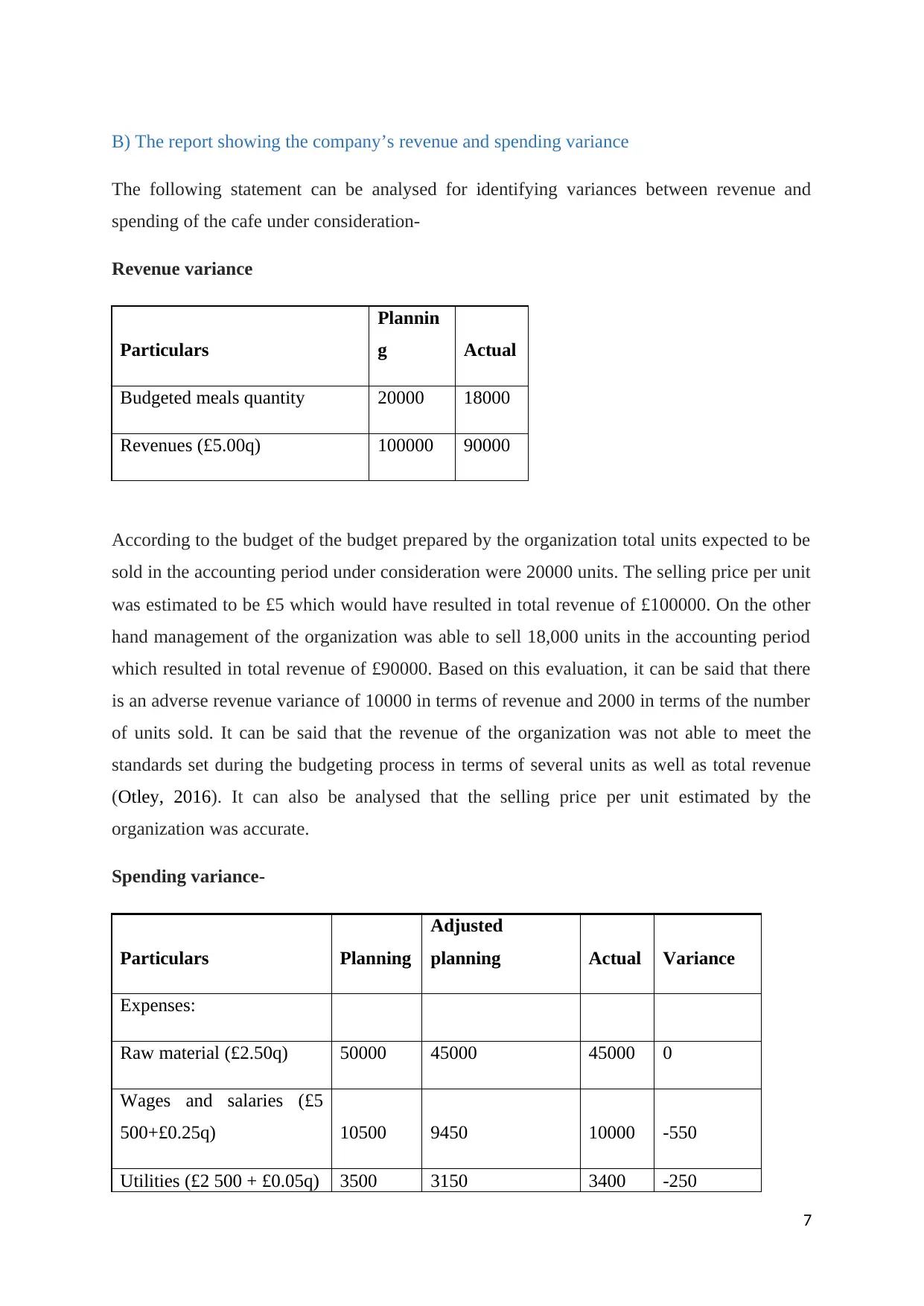

B) The report showing the company’s revenue and spending variance

The following statement can be analysed for identifying variances between revenue and

spending of the cafe under consideration-

Revenue variance

Particulars

Plannin

g Actual

Budgeted meals quantity 20000 18000

Revenues (£5.00q) 100000 90000

According to the budget of the budget prepared by the organization total units expected to be

sold in the accounting period under consideration were 20000 units. The selling price per unit

was estimated to be £5 which would have resulted in total revenue of £100000. On the other

hand management of the organization was able to sell 18,000 units in the accounting period

which resulted in total revenue of £90000. Based on this evaluation, it can be said that there

is an adverse revenue variance of 10000 in terms of revenue and 2000 in terms of the number

of units sold. It can be said that the revenue of the organization was not able to meet the

standards set during the budgeting process in terms of several units as well as total revenue

(Otley, 2016). It can also be analysed that the selling price per unit estimated by the

organization was accurate.

Spending variance-

Particulars Planning

Adjusted

planning Actual Variance

Expenses:

Raw material (£2.50q) 50000 45000 45000 0

Wages and salaries (£5

500+£0.25q) 10500 9450 10000 -550

Utilities (£2 500 + £0.05q) 3500 3150 3400 -250

7

The following statement can be analysed for identifying variances between revenue and

spending of the cafe under consideration-

Revenue variance

Particulars

Plannin

g Actual

Budgeted meals quantity 20000 18000

Revenues (£5.00q) 100000 90000

According to the budget of the budget prepared by the organization total units expected to be

sold in the accounting period under consideration were 20000 units. The selling price per unit

was estimated to be £5 which would have resulted in total revenue of £100000. On the other

hand management of the organization was able to sell 18,000 units in the accounting period

which resulted in total revenue of £90000. Based on this evaluation, it can be said that there

is an adverse revenue variance of 10000 in terms of revenue and 2000 in terms of the number

of units sold. It can be said that the revenue of the organization was not able to meet the

standards set during the budgeting process in terms of several units as well as total revenue

(Otley, 2016). It can also be analysed that the selling price per unit estimated by the

organization was accurate.

Spending variance-

Particulars Planning

Adjusted

planning Actual Variance

Expenses:

Raw material (£2.50q) 50000 45000 45000 0

Wages and salaries (£5

500+£0.25q) 10500 9450 10000 -550

Utilities (£2 500 + £0.05q) 3500 3150 3400 -250

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

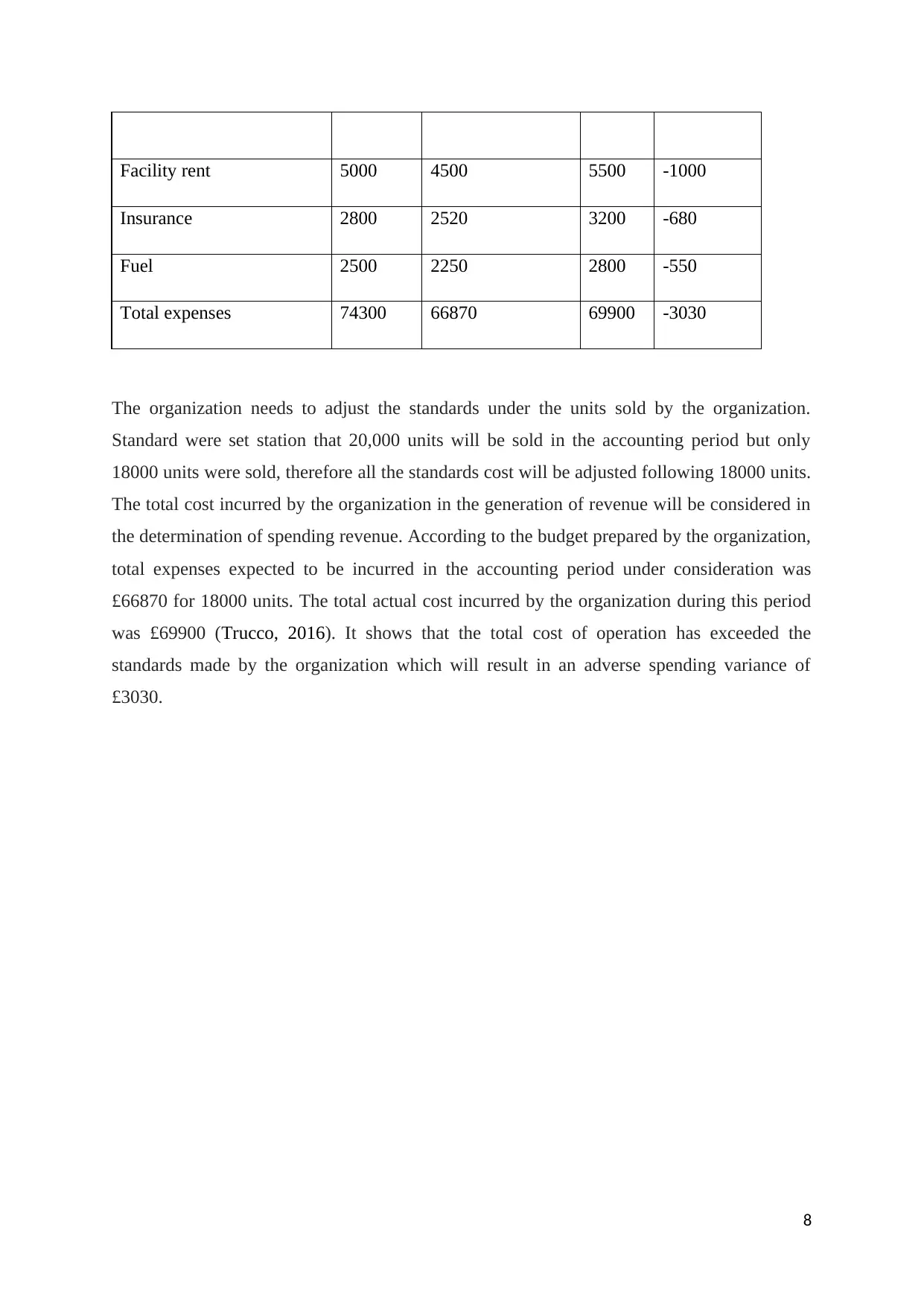

Facility rent 5000 4500 5500 -1000

Insurance 2800 2520 3200 -680

Fuel 2500 2250 2800 -550

Total expenses 74300 66870 69900 -3030

The organization needs to adjust the standards under the units sold by the organization.

Standard were set station that 20,000 units will be sold in the accounting period but only

18000 units were sold, therefore all the standards cost will be adjusted following 18000 units.

The total cost incurred by the organization in the generation of revenue will be considered in

the determination of spending revenue. According to the budget prepared by the organization,

total expenses expected to be incurred in the accounting period under consideration was

£66870 for 18000 units. The total actual cost incurred by the organization during this period

was £69900 (Trucco, 2016). It shows that the total cost of operation has exceeded the

standards made by the organization which will result in an adverse spending variance of

£3030.

8

Insurance 2800 2520 3200 -680

Fuel 2500 2250 2800 -550

Total expenses 74300 66870 69900 -3030

The organization needs to adjust the standards under the units sold by the organization.

Standard were set station that 20,000 units will be sold in the accounting period but only

18000 units were sold, therefore all the standards cost will be adjusted following 18000 units.

The total cost incurred by the organization in the generation of revenue will be considered in

the determination of spending revenue. According to the budget prepared by the organization,

total expenses expected to be incurred in the accounting period under consideration was

£66870 for 18000 units. The total actual cost incurred by the organization during this period

was £69900 (Trucco, 2016). It shows that the total cost of operation has exceeded the

standards made by the organization which will result in an adverse spending variance of

£3030.

8

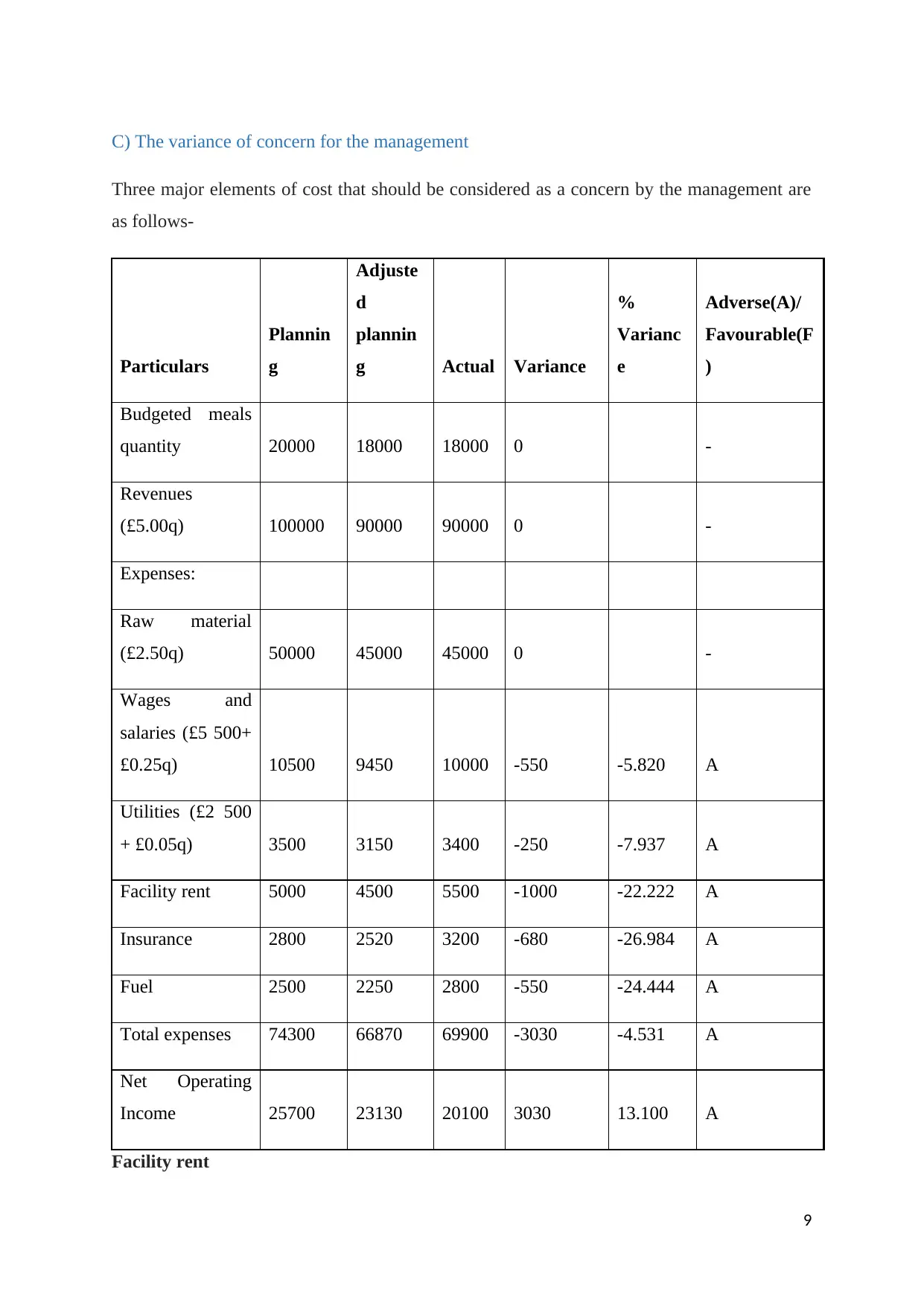

C) The variance of concern for the management

Three major elements of cost that should be considered as a concern by the management are

as follows-

Particulars

Plannin

g

Adjuste

d

plannin

g Actual Variance

%

Varianc

e

Adverse(A)/

Favourable(F

)

Budgeted meals

quantity 20000 18000 18000 0 -

Revenues

(£5.00q) 100000 90000 90000 0 -

Expenses:

Raw material

(£2.50q) 50000 45000 45000 0 -

Wages and

salaries (£5 500+

£0.25q) 10500 9450 10000 -550 -5.820 A

Utilities (£2 500

+ £0.05q) 3500 3150 3400 -250 -7.937 A

Facility rent 5000 4500 5500 -1000 -22.222 A

Insurance 2800 2520 3200 -680 -26.984 A

Fuel 2500 2250 2800 -550 -24.444 A

Total expenses 74300 66870 69900 -3030 -4.531 A

Net Operating

Income 25700 23130 20100 3030 13.100 A

Facility rent

9

Three major elements of cost that should be considered as a concern by the management are

as follows-

Particulars

Plannin

g

Adjuste

d

plannin

g Actual Variance

%

Varianc

e

Adverse(A)/

Favourable(F

)

Budgeted meals

quantity 20000 18000 18000 0 -

Revenues

(£5.00q) 100000 90000 90000 0 -

Expenses:

Raw material

(£2.50q) 50000 45000 45000 0 -

Wages and

salaries (£5 500+

£0.25q) 10500 9450 10000 -550 -5.820 A

Utilities (£2 500

+ £0.05q) 3500 3150 3400 -250 -7.937 A

Facility rent 5000 4500 5500 -1000 -22.222 A

Insurance 2800 2520 3200 -680 -26.984 A

Fuel 2500 2250 2800 -550 -24.444 A

Total expenses 74300 66870 69900 -3030 -4.531 A

Net Operating

Income 25700 23130 20100 3030 13.100 A

Facility rent

9

This type of expense generally pre-determined by the organization and it is important to

ensure that accuracy is maintained in the process of making assumptions. Total expected rent

during the initiation of the accounting period was estimated to be 4500 where is expensive

was 22% higher as compared to the standard (Weetman, 2019).

Fuel expenses

Total fuel expenses have also been very high as compared to the estimations mean by the

organization during the initial phase. The budgeted cost was estimated in terms of 18000

units was estimated to be £2250 whereas actual expenses went up to £2800 (Shields, 2018). It

clearly shows that management was not able to control the cost of operation as it has

exceeded by 24% as compared to the expectation.

Insurance cost

The budgeted cost was estimated in terms of 18000 units was estimated to be £2520 whereas

actual expenses went up to £3200. It clearly shows that management was not able to control

the cost of operation as it has exceeded by 24% as compared to the expectation.

On an overall analysis, it can be said that the management of the organization is required to

focus on controlling the cost of operation. This is one of the reasons that the overall

profitability of the organization has decreased in the accounting period under consideration

(Jiambalvo, 2019). The total profit recorded by the organization concerning 1800 units was

estimated to be £23130 where is the actual profit generated in this accounting period was

only £20100. Net income generated by the organization has been 13% lower as compared to

expectations. The primary reasons behind this decreased profitability margin of three cost

elements as described above.

10

ensure that accuracy is maintained in the process of making assumptions. Total expected rent

during the initiation of the accounting period was estimated to be 4500 where is expensive

was 22% higher as compared to the standard (Weetman, 2019).

Fuel expenses

Total fuel expenses have also been very high as compared to the estimations mean by the

organization during the initial phase. The budgeted cost was estimated in terms of 18000

units was estimated to be £2250 whereas actual expenses went up to £2800 (Shields, 2018). It

clearly shows that management was not able to control the cost of operation as it has

exceeded by 24% as compared to the expectation.

Insurance cost

The budgeted cost was estimated in terms of 18000 units was estimated to be £2520 whereas

actual expenses went up to £3200. It clearly shows that management was not able to control

the cost of operation as it has exceeded by 24% as compared to the expectation.

On an overall analysis, it can be said that the management of the organization is required to

focus on controlling the cost of operation. This is one of the reasons that the overall

profitability of the organization has decreased in the accounting period under consideration

(Jiambalvo, 2019). The total profit recorded by the organization concerning 1800 units was

estimated to be £23130 where is the actual profit generated in this accounting period was

only £20100. Net income generated by the organization has been 13% lower as compared to

expectations. The primary reasons behind this decreased profitability margin of three cost

elements as described above.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

D) Recommendation to survive and maintain profitability

Following are the steps that are required to be taken by the management of Fleet Highlands

Cafe are as follows-

The efficiency of the budgeting process- First of all, experts in the field of budgeting should

be hired by the organization to conduct the process of budgeting. This is because the

management of the organization was not able to make correct estimations concerning the

demand for the product in the market (Weygandt et.al, 2018). Experts will help in conducting

primary research in the industry which will help in making correct estimations under the

business environment.

Resource utilization- Management of the organization should consider the three cost elements

i.e. facility rent, insurance and fuel as the problem area under consideration as variance

associated with these three cost elements are more than 20% in the negative direction. A

better resource utilization processor should be used to make sure that the cost of operation

does not exceed the expectation (Weygandt, Kimmel and Kieso, 2018).

Cost controlling strategies- Apart from budgeting other cost controlling strategies should also

be executed in the company. For example, bonus and commission should be dependent on the

cost variance identified for each department working in the company. If a particular

department is exceeding its cost of estimated without any justifiable reason, then the amount

of variance should be deducted from the commissions and bonus is to be distributed to

employees in such departments (Yadav and Avhad, 2019).

11

Following are the steps that are required to be taken by the management of Fleet Highlands

Cafe are as follows-

The efficiency of the budgeting process- First of all, experts in the field of budgeting should

be hired by the organization to conduct the process of budgeting. This is because the

management of the organization was not able to make correct estimations concerning the

demand for the product in the market (Weygandt et.al, 2018). Experts will help in conducting

primary research in the industry which will help in making correct estimations under the

business environment.

Resource utilization- Management of the organization should consider the three cost elements

i.e. facility rent, insurance and fuel as the problem area under consideration as variance

associated with these three cost elements are more than 20% in the negative direction. A

better resource utilization processor should be used to make sure that the cost of operation

does not exceed the expectation (Weygandt, Kimmel and Kieso, 2018).

Cost controlling strategies- Apart from budgeting other cost controlling strategies should also

be executed in the company. For example, bonus and commission should be dependent on the

cost variance identified for each department working in the company. If a particular

department is exceeding its cost of estimated without any justifiable reason, then the amount

of variance should be deducted from the commissions and bonus is to be distributed to

employees in such departments (Yadav and Avhad, 2019).

11

Conclusion

An overall conclusion of this report it can be said that the budgeting process is an effective

cost controlling strategy that can help organizations to maintain desired profitability margin.

The overall process of budgeting undertaken by fleet Highland Cafe is not very efficient as

the majority of the expenses are exceeding the expectation. Management of the organization

is required to conduct an overall analysis of the process and implement other cost controlling

strategies to maintain profitability.

12

An overall conclusion of this report it can be said that the budgeting process is an effective

cost controlling strategy that can help organizations to maintain desired profitability margin.

The overall process of budgeting undertaken by fleet Highland Cafe is not very efficient as

the majority of the expenses are exceeding the expectation. Management of the organization

is required to conduct an overall analysis of the process and implement other cost controlling

strategies to maintain profitability.

12

References

Banerjee, B., 2019. Labour Cost Variance Analysis Through Diagrams-Integration to MIS.

The Management Accountant Journal, 54(6), pp.61-66.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Jones, C., Finkler, S.A., Kovner, C.T. and Mose, J., 2018. Financial Management for Nurse

Managers and Executives-E-Book. Elsevier Health Sciences.

Kolias, G. and Arnis, N., 2019. The optimal allocation of current assets using mean-variance

analysis. Accounting and Management Information Systems, 18(1), pp.50-72.

Marzlin Marzuki, N. A. R., & Ismail, J. (2019). Benefits and limitations of variance analysis

in management accounting. ACCOUNTING BULLETIN, 15.

Matsuoka, K. (2018). Variance Analysis in Fixed Revenue Accounting. Fixed Revenue

Accounting: A New Management Accounting Framework, 15, 69.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research, 31, pp.45-62.

Shields, M.D., 2018. A Perspective on Management Accounting Research. Journal of

Management Accounting Research, 30(3), pp.1-11.

Trucco, S., 2016. Financial accounting. Springer international PU.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2018. Financial and Managerial Accounting.

John Wiley & Sons.

Weygandt, J.J., Kimmel, P.D., Kieso, D.E. and Aly, I.M., 2018. Managerial Accounting:

Tools for Business Decision-making. John Wiley & Sons.

Yadav, R.R. and Avhad, S.M., 2020. Introduction to Cost and Managerial Accounting.

13

Banerjee, B., 2019. Labour Cost Variance Analysis Through Diagrams-Integration to MIS.

The Management Accountant Journal, 54(6), pp.61-66.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Jones, C., Finkler, S.A., Kovner, C.T. and Mose, J., 2018. Financial Management for Nurse

Managers and Executives-E-Book. Elsevier Health Sciences.

Kolias, G. and Arnis, N., 2019. The optimal allocation of current assets using mean-variance

analysis. Accounting and Management Information Systems, 18(1), pp.50-72.

Marzlin Marzuki, N. A. R., & Ismail, J. (2019). Benefits and limitations of variance analysis

in management accounting. ACCOUNTING BULLETIN, 15.

Matsuoka, K. (2018). Variance Analysis in Fixed Revenue Accounting. Fixed Revenue

Accounting: A New Management Accounting Framework, 15, 69.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research, 31, pp.45-62.

Shields, M.D., 2018. A Perspective on Management Accounting Research. Journal of

Management Accounting Research, 30(3), pp.1-11.

Trucco, S., 2016. Financial accounting. Springer international PU.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2018. Financial and Managerial Accounting.

John Wiley & Sons.

Weygandt, J.J., Kimmel, P.D., Kieso, D.E. and Aly, I.M., 2018. Managerial Accounting:

Tools for Business Decision-making. John Wiley & Sons.

Yadav, R.R. and Avhad, S.M., 2020. Introduction to Cost and Managerial Accounting.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.