Project 2: Cash Flow, Working Capital, and Budgeting Analysis

VerifiedAdded on 2023/01/12

|10

|3146

|27

Project

AI Summary

This project, divided into two parts, analyzes financial concepts and strategies for Mediterranean Delights Ltd. Part 1 focuses on cash flow, profit, and working capital, explaining key elements like inventory, payables, and receivables, and suggesting steps to improve cash flow through better working capital management. Part 2 delves into budgeting, comparing traditional and alternative methods like incremental and rolling budgets, outlining their strengths and weaknesses, and exploring their application in future cost management. The project emphasizes the importance of accurate financial planning and the impact of working capital changes on cash flow, providing a comprehensive overview of financial analysis and strategic decision-making within the context of the company's operations.

Project 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART 1............................................................................................................................................1

EXECUTIVE SUMMARY.............................................................................................................1

1. Explanation of different elements............................................................................................1

2. Application of all the concepts within the organisation...........................................................3

3. Steps to be taken to improve cash flow by better working capital management.....................4

PART 2............................................................................................................................................4

EXECUTIVE SUMMARY.............................................................................................................4

1. Purpose of preparing budget, traditional and alternative methods of budgeting along with

their strengths and weaknesses....................................................................................................4

2. Application of budgeting methods to plan future cost management.......................................6

3. Analysis of appropriateness of traditional and alternative budgeting approaches...................7

PART 1............................................................................................................................................1

EXECUTIVE SUMMARY.............................................................................................................1

1. Explanation of different elements............................................................................................1

2. Application of all the concepts within the organisation...........................................................3

3. Steps to be taken to improve cash flow by better working capital management.....................4

PART 2............................................................................................................................................4

EXECUTIVE SUMMARY.............................................................................................................4

1. Purpose of preparing budget, traditional and alternative methods of budgeting along with

their strengths and weaknesses....................................................................................................4

2. Application of budgeting methods to plan future cost management.......................................6

3. Analysis of appropriateness of traditional and alternative budgeting approaches...................7

PART 1

EXECUTIVE SUMMARY

First part of this report is based upon basic concepts of profit, cash flow, working capital

etc. It is based upon Mediterranean Delights Ltd which is operating business in South of

England. While managing working capital it is very important for all the organisations to pay

attention towards major elements such as inventory, payables, receivables etc. The company is

recommended to take appropriate steps to improve the cash flow by managing working capital

properly.

1. Explanation of different elements

Explanation of profit: When an organisation perform operations and generate revenues

then the total income which is received by it after deducting all the expenses is known as profit.

There are various direct and indirect expenses which are deducted from total value of sales.

These are rent, salaries, insurance, legal, postage, commission, depreciation etc. All the incomes

which are added in the calculation of it are profit on sale of assets, discount received etc. In order

to determine actual amount of profit which is generated by a company profit and loss statement

is formulated. With the help of it, all the internal and external stakeholders analyse that the entity

is having higher or lower profitability (Aktas, Croci and Petmezas, 2015). In other words, it can

be defined as the amount which is required by an entity to survive in the market and perform

future activities in systematic manner. With the help of it stakeholders such as investors,

employees etc. could be retained as higher profits will build their interest within the entity.

Explanation of cash flow: Cash flow is the total amount of cash which is being

generated by an entity by deducting all the outflows from inflows. In order to maintain liquidity

of the business it is very important for a company to make sure that it is having proper cash flow.

While making decision regarding making investment in a company investors determine liquidity

of business and then finalise that they wish to invest or not. While computing it for the business

cash flow statement is generated. Total value of it is calculated it by adding cash, other

equivalents and bank balance. Slight mistake in it may lead the business towards huge losses

because it is result in inaccurate liquidity (Atrill, 2015).

Differentiation between profit and cash flow: Profit and cash flow both are different

for companies and several bases for it could be understood with the help of following discussion:

1

EXECUTIVE SUMMARY

First part of this report is based upon basic concepts of profit, cash flow, working capital

etc. It is based upon Mediterranean Delights Ltd which is operating business in South of

England. While managing working capital it is very important for all the organisations to pay

attention towards major elements such as inventory, payables, receivables etc. The company is

recommended to take appropriate steps to improve the cash flow by managing working capital

properly.

1. Explanation of different elements

Explanation of profit: When an organisation perform operations and generate revenues

then the total income which is received by it after deducting all the expenses is known as profit.

There are various direct and indirect expenses which are deducted from total value of sales.

These are rent, salaries, insurance, legal, postage, commission, depreciation etc. All the incomes

which are added in the calculation of it are profit on sale of assets, discount received etc. In order

to determine actual amount of profit which is generated by a company profit and loss statement

is formulated. With the help of it, all the internal and external stakeholders analyse that the entity

is having higher or lower profitability (Aktas, Croci and Petmezas, 2015). In other words, it can

be defined as the amount which is required by an entity to survive in the market and perform

future activities in systematic manner. With the help of it stakeholders such as investors,

employees etc. could be retained as higher profits will build their interest within the entity.

Explanation of cash flow: Cash flow is the total amount of cash which is being

generated by an entity by deducting all the outflows from inflows. In order to maintain liquidity

of the business it is very important for a company to make sure that it is having proper cash flow.

While making decision regarding making investment in a company investors determine liquidity

of business and then finalise that they wish to invest or not. While computing it for the business

cash flow statement is generated. Total value of it is calculated it by adding cash, other

equivalents and bank balance. Slight mistake in it may lead the business towards huge losses

because it is result in inaccurate liquidity (Atrill, 2015).

Differentiation between profit and cash flow: Profit and cash flow both are different

for companies and several bases for it could be understood with the help of following discussion:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

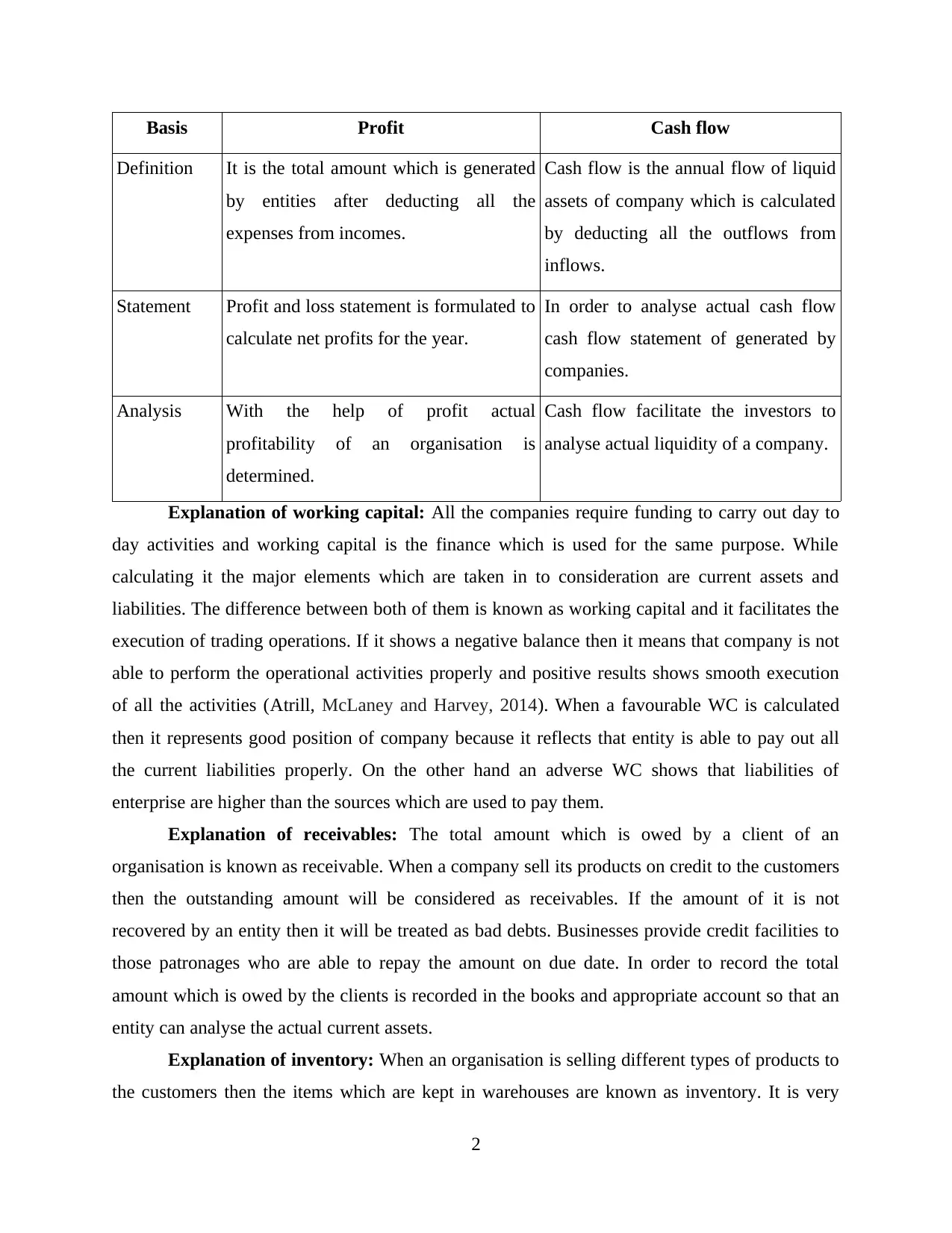

Basis Profit Cash flow

Definition It is the total amount which is generated

by entities after deducting all the

expenses from incomes.

Cash flow is the annual flow of liquid

assets of company which is calculated

by deducting all the outflows from

inflows.

Statement Profit and loss statement is formulated to

calculate net profits for the year.

In order to analyse actual cash flow

cash flow statement of generated by

companies.

Analysis With the help of profit actual

profitability of an organisation is

determined.

Cash flow facilitate the investors to

analyse actual liquidity of a company.

Explanation of working capital: All the companies require funding to carry out day to

day activities and working capital is the finance which is used for the same purpose. While

calculating it the major elements which are taken in to consideration are current assets and

liabilities. The difference between both of them is known as working capital and it facilitates the

execution of trading operations. If it shows a negative balance then it means that company is not

able to perform the operational activities properly and positive results shows smooth execution

of all the activities (Atrill, McLaney and Harvey, 2014). When a favourable WC is calculated

then it represents good position of company because it reflects that entity is able to pay out all

the current liabilities properly. On the other hand an adverse WC shows that liabilities of

enterprise are higher than the sources which are used to pay them.

Explanation of receivables: The total amount which is owed by a client of an

organisation is known as receivable. When a company sell its products on credit to the customers

then the outstanding amount will be considered as receivables. If the amount of it is not

recovered by an entity then it will be treated as bad debts. Businesses provide credit facilities to

those patronages who are able to repay the amount on due date. In order to record the total

amount which is owed by the clients is recorded in the books and appropriate account so that an

entity can analyse the actual current assets.

Explanation of inventory: When an organisation is selling different types of products to

the customers then the items which are kept in warehouses are known as inventory. It is very

2

Definition It is the total amount which is generated

by entities after deducting all the

expenses from incomes.

Cash flow is the annual flow of liquid

assets of company which is calculated

by deducting all the outflows from

inflows.

Statement Profit and loss statement is formulated to

calculate net profits for the year.

In order to analyse actual cash flow

cash flow statement of generated by

companies.

Analysis With the help of profit actual

profitability of an organisation is

determined.

Cash flow facilitate the investors to

analyse actual liquidity of a company.

Explanation of working capital: All the companies require funding to carry out day to

day activities and working capital is the finance which is used for the same purpose. While

calculating it the major elements which are taken in to consideration are current assets and

liabilities. The difference between both of them is known as working capital and it facilitates the

execution of trading operations. If it shows a negative balance then it means that company is not

able to perform the operational activities properly and positive results shows smooth execution

of all the activities (Atrill, McLaney and Harvey, 2014). When a favourable WC is calculated

then it represents good position of company because it reflects that entity is able to pay out all

the current liabilities properly. On the other hand an adverse WC shows that liabilities of

enterprise are higher than the sources which are used to pay them.

Explanation of receivables: The total amount which is owed by a client of an

organisation is known as receivable. When a company sell its products on credit to the customers

then the outstanding amount will be considered as receivables. If the amount of it is not

recovered by an entity then it will be treated as bad debts. Businesses provide credit facilities to

those patronages who are able to repay the amount on due date. In order to record the total

amount which is owed by the clients is recorded in the books and appropriate account so that an

entity can analyse the actual current assets.

Explanation of inventory: When an organisation is selling different types of products to

the customers then the items which are kept in warehouses are known as inventory. It is very

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

important for entities to manage it properly so that desired goals could be accomplished. There

are various types of inventory management systems which could be used by companies for

maintain the level of stock. These are LIFO, FIFO and AVCO. Business enterprises can use any

of them for making sure that goods are managed by them in warehouses properly. Main purpose

of it is to assure that all the production related activities are performed appropriately so that long

term business goals could be accomplished (de Almeida and Eid Jr, 2014).

Explanation of payables: When an entity is buying goods or services on credit from the

suppliers then the total owed amount by the organisation will be recorded as payables. It is a type

of current liability which is required to be paid by company within one year. In order to maintain

good relations with external parties such as suppliers it is very important for companies to make

sure that the total owed amount is paid on time. Any default in payment may result in bad image

of company in the market which is not beneficial for the business.

While calculating working capital all the above described three elements are required to

be calculated and analysed properly. These are receivables, payables and inventory. Inaccurate

computation of them may result in negative or adverse results for working capital which may

affect execution of day to day trading operations.

Changes in working capital affect cash flow: For all the business entities it is very

important to analyse all the potential modifications in the working capital so that changes in cash

flow could be determined. For example, if an organisation is not able to recover its debtors then

it will create difficulties in managing cash flow because it will result in decreased current assets.

2. Application of all the concepts within the organisation

Mediterranean Delights Ltd is one of the entities which are operating business in South of

England. The organisation is managing its working capital by paying attention towards

receivables, payables, cash, profits and inventory (Drury, 2016). Total operating profits of the

entity for last year before interest and tax was 5 million pounds and total debts of the entity were

increased by 2 million pounds in current year. Due to this liabilities are increased which may

affect working capital. Total outstanding amount which is required to be paid by the entity is 1.5

million pounds which is considered as payables for the year. The total receivables of the entity

against San Pedro is around 2 million pounds. All these concepts are applied by the entity

properly which helps it to manage working capital.

3

are various types of inventory management systems which could be used by companies for

maintain the level of stock. These are LIFO, FIFO and AVCO. Business enterprises can use any

of them for making sure that goods are managed by them in warehouses properly. Main purpose

of it is to assure that all the production related activities are performed appropriately so that long

term business goals could be accomplished (de Almeida and Eid Jr, 2014).

Explanation of payables: When an entity is buying goods or services on credit from the

suppliers then the total owed amount by the organisation will be recorded as payables. It is a type

of current liability which is required to be paid by company within one year. In order to maintain

good relations with external parties such as suppliers it is very important for companies to make

sure that the total owed amount is paid on time. Any default in payment may result in bad image

of company in the market which is not beneficial for the business.

While calculating working capital all the above described three elements are required to

be calculated and analysed properly. These are receivables, payables and inventory. Inaccurate

computation of them may result in negative or adverse results for working capital which may

affect execution of day to day trading operations.

Changes in working capital affect cash flow: For all the business entities it is very

important to analyse all the potential modifications in the working capital so that changes in cash

flow could be determined. For example, if an organisation is not able to recover its debtors then

it will create difficulties in managing cash flow because it will result in decreased current assets.

2. Application of all the concepts within the organisation

Mediterranean Delights Ltd is one of the entities which are operating business in South of

England. The organisation is managing its working capital by paying attention towards

receivables, payables, cash, profits and inventory (Drury, 2016). Total operating profits of the

entity for last year before interest and tax was 5 million pounds and total debts of the entity were

increased by 2 million pounds in current year. Due to this liabilities are increased which may

affect working capital. Total outstanding amount which is required to be paid by the entity is 1.5

million pounds which is considered as payables for the year. The total receivables of the entity

against San Pedro is around 2 million pounds. All these concepts are applied by the entity

properly which helps it to manage working capital.

3

3. Steps to be taken to improve cash flow by better working capital management

Every entity ways to make improvement in cash flow which is possible with the help of

better working capital management. Several steps which could be taken by Mediterranean

Delights Ltd are as follows:

The organisation should pay all the debts on time so that current liabilities could be

managed which will be beneficial to manage working capital and improve cash flow

(Kaplan and Atkinson, 2015).

Inventory management is also important for all the organisations as it is a part of current

assets and by managing it working capital could be managed. It will be beneficial to

improve cash flow because when stock will be controlled properly then it could be

ordered when it is required which helps to maintain cash.

PART 2

EXECUTIVE SUMMARY

1. Purpose of preparing budget, traditional and alternative methods of budgeting along with their

strengths and weaknesses

Budget is a type of advance plan which is generated by an organisation for the purpose of

carrying out future activities in systematic manner. With the help of it, business entities allocate

funds to all the departments according to their requirements so that they can perform all their

functions. Main purpose of a budget is to make sure that all the planned activities are performed

in appropriately so that the desired goals of higher profitability and revenues could be achieved

successfully. Another purpose of preparing a budget is to fulfil monetary requirements of all the

divisions of company so that all the tasks which are allocated to them could be accomplished

(Oseifuah, 2016).

It is very important for all the entities to pay attention towards different approaches of

budgeting so that best suitable from all of them could be selected for allocation of funds to

different activities. There are two types of approaches which are traditional and alternative.

Description of different methods of them is as follows:

Traditional approach: It is a type of budgeting method in which data from previous

years is used for generating reports from present period. It is mainly based upon estimation of

4

Every entity ways to make improvement in cash flow which is possible with the help of

better working capital management. Several steps which could be taken by Mediterranean

Delights Ltd are as follows:

The organisation should pay all the debts on time so that current liabilities could be

managed which will be beneficial to manage working capital and improve cash flow

(Kaplan and Atkinson, 2015).

Inventory management is also important for all the organisations as it is a part of current

assets and by managing it working capital could be managed. It will be beneficial to

improve cash flow because when stock will be controlled properly then it could be

ordered when it is required which helps to maintain cash.

PART 2

EXECUTIVE SUMMARY

1. Purpose of preparing budget, traditional and alternative methods of budgeting along with their

strengths and weaknesses

Budget is a type of advance plan which is generated by an organisation for the purpose of

carrying out future activities in systematic manner. With the help of it, business entities allocate

funds to all the departments according to their requirements so that they can perform all their

functions. Main purpose of a budget is to make sure that all the planned activities are performed

in appropriately so that the desired goals of higher profitability and revenues could be achieved

successfully. Another purpose of preparing a budget is to fulfil monetary requirements of all the

divisions of company so that all the tasks which are allocated to them could be accomplished

(Oseifuah, 2016).

It is very important for all the entities to pay attention towards different approaches of

budgeting so that best suitable from all of them could be selected for allocation of funds to

different activities. There are two types of approaches which are traditional and alternative.

Description of different methods of them is as follows:

Traditional approach: It is a type of budgeting method in which data from previous

years is used for generating reports from present period. It is mainly based upon estimation of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

different expenses which may take place in future while carrying out operations. One of the main

type of it is incremental budgeting which is as follows:

Incremental budgeting: When organisations prepare budget for current year on the basis

of previous performance or old budgets then it is known as incremental budgeting. All the details

which are used for generating new records are based estimation. It is mainly focused with

making changes in existing budget to perform future activities. Some of the strengths and

weaknesses of this approach of traditional budgeting are described below:

Strengths: It is a simple method which could be used by organisations generate budgets

for future. The records which are generated by following this approach is easy to

understand which helps to analyse business performance effortlessly (Otley, 2016).

Weaknesses: The level of flexibility in this budget is very low as it does not allow to

make modifications in the reports according to changes in business expenses. The

information recorded in it is not accurate because it is based upon estimation.

Alternative approach: When organisations have different options which could be used

for preparation of budgets for future period then it is known as alternative method of budgeting.

There are various approaches of it which are described below:

Rolling budget: It can be defined as a budget which is updated on the basis of business

activities. It is highly flexible which helps the managers to analyse the actual expenses and

incomes for the accounting year. All the strengths and weaknesses of using this budget are

discussed below:

Strengths: Changes in the records could be made on the basis of different expenses

which are taking place within the accounting year. With the help of it accurate funds

could be assigned to different activities as provides information about actual expenditures

which are related to operations.

Weaknesses: The process of generating it is time consuming which may affect

engagement of management in operations. Specific knowledge is required to create

rolling budget for which the organisation will be required to hire experienced staff.

Zero based budget: When an organisation is generating its budget with nil balance then

it is known as zero based budget. It is very important for the managers to justify all the

transactions which are recoded in it for assuring accuracy. Strengths and weaknesses of this

budgeting approach for the organisations which are used it are as follows:

5

type of it is incremental budgeting which is as follows:

Incremental budgeting: When organisations prepare budget for current year on the basis

of previous performance or old budgets then it is known as incremental budgeting. All the details

which are used for generating new records are based estimation. It is mainly focused with

making changes in existing budget to perform future activities. Some of the strengths and

weaknesses of this approach of traditional budgeting are described below:

Strengths: It is a simple method which could be used by organisations generate budgets

for future. The records which are generated by following this approach is easy to

understand which helps to analyse business performance effortlessly (Otley, 2016).

Weaknesses: The level of flexibility in this budget is very low as it does not allow to

make modifications in the reports according to changes in business expenses. The

information recorded in it is not accurate because it is based upon estimation.

Alternative approach: When organisations have different options which could be used

for preparation of budgets for future period then it is known as alternative method of budgeting.

There are various approaches of it which are described below:

Rolling budget: It can be defined as a budget which is updated on the basis of business

activities. It is highly flexible which helps the managers to analyse the actual expenses and

incomes for the accounting year. All the strengths and weaknesses of using this budget are

discussed below:

Strengths: Changes in the records could be made on the basis of different expenses

which are taking place within the accounting year. With the help of it accurate funds

could be assigned to different activities as provides information about actual expenditures

which are related to operations.

Weaknesses: The process of generating it is time consuming which may affect

engagement of management in operations. Specific knowledge is required to create

rolling budget for which the organisation will be required to hire experienced staff.

Zero based budget: When an organisation is generating its budget with nil balance then

it is known as zero based budget. It is very important for the managers to justify all the

transactions which are recoded in it for assuring accuracy. Strengths and weaknesses of this

budgeting approach for the organisations which are used it are as follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strengths: All the figures that are mentioned in it is accurate ans related to the current

accounting year which helps to allocate funds to different activities according to their

requirements.

Weaknesses: The records could be biased by the managers as information of previous

years is not considered as the base for present year's budget. Process of preparing zero

based budget is very complex which may result in errors in future.

Activity based budget: This budgeting technique is mainly focused with identification,

analysis and assessment of different activities. With the help of it, management will be able to

assign budgets to all the operations according to their requirements. Different strengths and

weaknesses of this budget are as follows:

Strengths: It is beneficial for the organisations to assign funds to different operations

according to their requirements. With the help of it managers can differentiate between

direct and indirect costs as it facilitate to assign funds to activities according to their

needs (Watson and et.al., 2016).

Weaknesses: In order to generate it, it is essential for the managers to make sure that

they have proper understanding of it because lack of knowledge may result in failure of

operations.

2. Application of budgeting methods to plan future cost management

Second Sight Plc is an internation company which is planning to expand its business in

Netherlands by signing a joint venture with an Indian company. In order to plan the future cost

management traditional and alternative budgeting techniques could be used. Discussion of them

is as follows:

Incremental budgeting could be used to prepare records in the basis of previous year

which will help to estimate the cost of expansion and allocate funds to different activities

according to their requirements. All the products and process for the business will be budgeted

on the basis of prior year's records.

Zero based budgeting can also be used for future cost management of Second Sight Plc in

the expansion plan. By using it managers can formulate records with a zero balance. If it will be

used then products and process will be analysed accurately because information regarding the

operations in Netherlands will be recorded in the budget.

6

accounting year which helps to allocate funds to different activities according to their

requirements.

Weaknesses: The records could be biased by the managers as information of previous

years is not considered as the base for present year's budget. Process of preparing zero

based budget is very complex which may result in errors in future.

Activity based budget: This budgeting technique is mainly focused with identification,

analysis and assessment of different activities. With the help of it, management will be able to

assign budgets to all the operations according to their requirements. Different strengths and

weaknesses of this budget are as follows:

Strengths: It is beneficial for the organisations to assign funds to different operations

according to their requirements. With the help of it managers can differentiate between

direct and indirect costs as it facilitate to assign funds to activities according to their

needs (Watson and et.al., 2016).

Weaknesses: In order to generate it, it is essential for the managers to make sure that

they have proper understanding of it because lack of knowledge may result in failure of

operations.

2. Application of budgeting methods to plan future cost management

Second Sight Plc is an internation company which is planning to expand its business in

Netherlands by signing a joint venture with an Indian company. In order to plan the future cost

management traditional and alternative budgeting techniques could be used. Discussion of them

is as follows:

Incremental budgeting could be used to prepare records in the basis of previous year

which will help to estimate the cost of expansion and allocate funds to different activities

according to their requirements. All the products and process for the business will be budgeted

on the basis of prior year's records.

Zero based budgeting can also be used for future cost management of Second Sight Plc in

the expansion plan. By using it managers can formulate records with a zero balance. If it will be

used then products and process will be analysed accurately because information regarding the

operations in Netherlands will be recorded in the budget.

6

Rolling budget helps to make appropriate modifications in the records which could be

used to plan future cost management by Second Sight Plc while expanding business in

Netherlands. With the help of it, managers will be able to make changes in the budget or

transactions according to the expanses which are taking place continuously. It will facilitate the

budgeting of products and process as use of it will result in accurate costs of all the operations.

Activity based budget can also be used by Second Sight Plc while planning for business

expansion for future cost management because with the help of it actual expenses which may

take place while performing specific activities could be determined. It will be beneficial to

budget all the processes and products as it will help the mangers to allocate funds to the activities

according to their requirements (Weetman, 2010).

3. Analysis of appropriateness of traditional and alternative budgeting approaches

Second Sight Plc is planning to expand business in Netherlands therefore it is very

important for it to make sure that appropriate budgeting techniques used by it. It has been

recommended to the enterprise that alternative approaches such as rolling, zero based and

activity based budgets. With the help of them, accurate budgets could be generated and then

funds funds could be allocated to activities according to their requirements.

7

used to plan future cost management by Second Sight Plc while expanding business in

Netherlands. With the help of it, managers will be able to make changes in the budget or

transactions according to the expanses which are taking place continuously. It will facilitate the

budgeting of products and process as use of it will result in accurate costs of all the operations.

Activity based budget can also be used by Second Sight Plc while planning for business

expansion for future cost management because with the help of it actual expenses which may

take place while performing specific activities could be determined. It will be beneficial to

budget all the processes and products as it will help the mangers to allocate funds to the activities

according to their requirements (Weetman, 2010).

3. Analysis of appropriateness of traditional and alternative budgeting approaches

Second Sight Plc is planning to expand business in Netherlands therefore it is very

important for it to make sure that appropriate budgeting techniques used by it. It has been

recommended to the enterprise that alternative approaches such as rolling, zero based and

activity based budgets. With the help of them, accurate budgets could be generated and then

funds funds could be allocated to activities according to their requirements.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-enhancing?

Evidence from firm performance and investments. Journal of Corporate Finance. 30.

pp.98-113.

Atrill, P., 2015. Financial management for decision makers. Pearson Education

Atrill, P., McLaney, E. and Harvey, D., 2014. Accounting: An Introduction, 6/E (Vol. 6).

Pearson Higher Education AU.

de Almeida, J. R. and Eid Jr, W., 2014. Access to finance, working capital management and

company value: Evidences from Brazilian companies listed on

BM&FBOVESPA. Journal of Business Research. 67(5). pp.924-934.

Drury, C., 2016. Management accounting for business. Cengage Learning EMEA.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Oseifuah, E. K., 2016. Cash Conversion Cycle theory and corporate profitability.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Watson, A. and et.al., 2016. When do franchisors select entrepreneurial franchisees? An

organizational identity perspective. Journal of Business Research. 69(12). pp.5934-

5945.

Weetman, P., 2010. Management accounting. Pearson Education.

Online

8

Books and Journals:

Aktas, N., Croci, E. and Petmezas, D., 2015. Is working capital management value-enhancing?

Evidence from firm performance and investments. Journal of Corporate Finance. 30.

pp.98-113.

Atrill, P., 2015. Financial management for decision makers. Pearson Education

Atrill, P., McLaney, E. and Harvey, D., 2014. Accounting: An Introduction, 6/E (Vol. 6).

Pearson Higher Education AU.

de Almeida, J. R. and Eid Jr, W., 2014. Access to finance, working capital management and

company value: Evidences from Brazilian companies listed on

BM&FBOVESPA. Journal of Business Research. 67(5). pp.924-934.

Drury, C., 2016. Management accounting for business. Cengage Learning EMEA.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Oseifuah, E. K., 2016. Cash Conversion Cycle theory and corporate profitability.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Watson, A. and et.al., 2016. When do franchisors select entrepreneurial franchisees? An

organizational identity perspective. Journal of Business Research. 69(12). pp.5934-

5945.

Weetman, P., 2010. Management accounting. Pearson Education.

Online

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.