Types of Business Organisation and Main Users of Accounting Information

VerifiedAdded on 2023/01/19

|11

|1971

|68

AI Summary

This report discusses the different types of business organisations and their advantages, as well as the main users of accounting information and how they use it. It also includes journal entries and ledgers for recording transactions, and an income statement and statement of financial position for S Keyes.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

REPORT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

a. Types of business organisation and advantages of using profit business structures................1

b. Main users of accounting informations and use of information by the users..........................2

PART 2............................................................................................................................................3

PART 3............................................................................................................................................4

PART 4............................................................................................................................................7

a) Income Statement of S Keyes for year ending 30th September 2019.....................................7

b) Statement of Financial Position as at 30th September 2019. .................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

a. Types of business organisation and advantages of using profit business structures................1

b. Main users of accounting informations and use of information by the users..........................2

PART 2............................................................................................................................................3

PART 3............................................................................................................................................4

PART 4............................................................................................................................................7

a) Income Statement of S Keyes for year ending 30th September 2019.....................................7

b) Statement of Financial Position as at 30th September 2019. .................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

In present times there are different organisations existing that are using profit based

business structures. Report will reveal bout different types of organisation with their advantages.

It will provide who are the main users of accounting information and and the use of accounting

information by these users. It will give an understanding about recording of transactions in books

from journals to ledgers and preparation of trial balance by numeric solution of the questions.

PART 1

a. Types of business organisation and advantages of using profit business structures.

Types of business organisations

Sole Proprietorship

Business is owned by single individual and is most common and simple form in

businesses. This business is run for making benefit to the self. Existence of business is

completely dependent on decision of the owner. Business comes to end when there are no

nominees to continue the business. In Sole proprietorship owner have the unlimited liabilities

and is personally responsible for all liabilities.

Advantages

Owner is not under obligation to decide for place and here activities related to business.

Proprietor is sole person who receives all profits that are generated in the business and

does not have share to with others as there is no legal obligation (Petty and Mandel,

2015).

Business do not have to follow various regulatory requirements and there are not much

requirements for establishing business.

Partnership

In this type of business ownership is shared by two or more partners who make

contribution of resources in enterprise. Partnership is divided into 2 parts i.e. limited and general.

In general ones owners collectively invest their funds in business. All partners investing their

funds are having unlimited liabilities for debts of business. Even a small contribution will make

the partner liable to all the debts of business. Formal agreements are not required in general

partnership and could be implied between business owners. Where in limited liability formal

agreements are must between partners. Certificate of partnership is required to be filed with

1

In present times there are different organisations existing that are using profit based

business structures. Report will reveal bout different types of organisation with their advantages.

It will provide who are the main users of accounting information and and the use of accounting

information by these users. It will give an understanding about recording of transactions in books

from journals to ledgers and preparation of trial balance by numeric solution of the questions.

PART 1

a. Types of business organisation and advantages of using profit business structures.

Types of business organisations

Sole Proprietorship

Business is owned by single individual and is most common and simple form in

businesses. This business is run for making benefit to the self. Existence of business is

completely dependent on decision of the owner. Business comes to end when there are no

nominees to continue the business. In Sole proprietorship owner have the unlimited liabilities

and is personally responsible for all liabilities.

Advantages

Owner is not under obligation to decide for place and here activities related to business.

Proprietor is sole person who receives all profits that are generated in the business and

does not have share to with others as there is no legal obligation (Petty and Mandel,

2015).

Business do not have to follow various regulatory requirements and there are not much

requirements for establishing business.

Partnership

In this type of business ownership is shared by two or more partners who make

contribution of resources in enterprise. Partnership is divided into 2 parts i.e. limited and general.

In general ones owners collectively invest their funds in business. All partners investing their

funds are having unlimited liabilities for debts of business. Even a small contribution will make

the partner liable to all the debts of business. Formal agreements are not required in general

partnership and could be implied between business owners. Where in limited liability formal

agreements are must between partners. Certificate of partnership is required to be filed with

1

respective states. This partnership allows partners for limiting own liability for debts of business

on basis of their investment and ownership (Spence and Hyams-Ssekasi, 2015).

Advantages

Business gets more capital as resources are shared by partners. Resource availability is

increased due to partnership.

Profits are shared by all the partners of enterprise and also the liability is shared between

partners of the enterprise. Liability can be limited up to the amount of their contributions

in business.

Partnership is easy to establish and is flexible form of business.

Corporation

Corporation refers to business organisation that is having distinct legal personality from

its owners. Corporation is having a separate standing from its owners and held personally liable

for all its owners. All the transactions are incurred in the name of company and not in name of

owners. It can open bank account, receive loans and can sue or be sued in its own name separate

from its owners. Profits which are generated by corporations are assessed and taxed under

personal income of company (Steingard and Gilbert, 2016). But establishing a corporation is

costly and complex process with many legal requirements.

Advantages

Owners of the company limit their liability is limited to debts and losses. Personal assets

of owners are not seized for business debts.

All the profits & losses incurred belong to corporation only.

Ownership can be transferred from one person to another easily.

b. Main users of accounting informations and use of information by the users.

Objective behind accounting information are correlated to requirements of decision-

making by the users of financial informations. Needs of users define the factors that are to be

taken into considerations while designing accounting information system. Users require

accounting information for facilitating process of decision-making, this is serving as platform for

framing guidelines for ensuring uniformity, accuracy and relevance of accounting informations

& procedures over different organisations (Schroeder, Clark and Cathey, 2019).

Owners

2

on basis of their investment and ownership (Spence and Hyams-Ssekasi, 2015).

Advantages

Business gets more capital as resources are shared by partners. Resource availability is

increased due to partnership.

Profits are shared by all the partners of enterprise and also the liability is shared between

partners of the enterprise. Liability can be limited up to the amount of their contributions

in business.

Partnership is easy to establish and is flexible form of business.

Corporation

Corporation refers to business organisation that is having distinct legal personality from

its owners. Corporation is having a separate standing from its owners and held personally liable

for all its owners. All the transactions are incurred in the name of company and not in name of

owners. It can open bank account, receive loans and can sue or be sued in its own name separate

from its owners. Profits which are generated by corporations are assessed and taxed under

personal income of company (Steingard and Gilbert, 2016). But establishing a corporation is

costly and complex process with many legal requirements.

Advantages

Owners of the company limit their liability is limited to debts and losses. Personal assets

of owners are not seized for business debts.

All the profits & losses incurred belong to corporation only.

Ownership can be transferred from one person to another easily.

b. Main users of accounting informations and use of information by the users.

Objective behind accounting information are correlated to requirements of decision-

making by the users of financial informations. Needs of users define the factors that are to be

taken into considerations while designing accounting information system. Users require

accounting information for facilitating process of decision-making, this is serving as platform for

framing guidelines for ensuring uniformity, accuracy and relevance of accounting informations

& procedures over different organisations (Schroeder, Clark and Cathey, 2019).

Owners

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

They are investors in business and are titleholders to organisations. Owners include sole

proprietor, partners and shareholders of companies. Accounting information provides all the

essential information to its owners related to business. Main requirement of having accounting

information of organisation is of keeping track over the financial performance of businesses,

changes in financial position and economic conditions of organisation. These information

facilitates assessment of manager's performance of organisation for evaluating their effectiveness

and efficiency. Information helps owners in determining the performance whether business are

growing and maximising profits.

Customers

They are the people who purchase goods and services of businesses and also known as

economic drivers of organisations. Customers rely on organisation for their products and services

for resale or for their self consumption, they use accounting information for evaluating the

capability of organisations that they will continue their supplies and meet their future needs.

Information is derived from financial statements of company that indicates profit or loss and

financial position of organisations

Suppliers

These parties provide organisations with products and services that are essential for

sustenance and business of organisations. Supplies range over raw materials used in

manufacturing, outsourced services & transportation services (Schroeder, Clark and Cathey,

2019). Suppliers of businesses are compensated in cash or credit basis. Their need is of

determining the capability of firm to meet the obligations related to payment of supplies.

Lenders

Providers of alternate sources of capital to organisation. Lenders provide business with

debts and receive interest in return. Lenders include banks, financial institutions and debenture

holders. They require this information for knowing the economic performance & financial

standing of organisations for assessing the profitability of entities and their capacity of paying

interest on the borrowed amounts. They should have enough resources for paying principal as

well interest on loan.

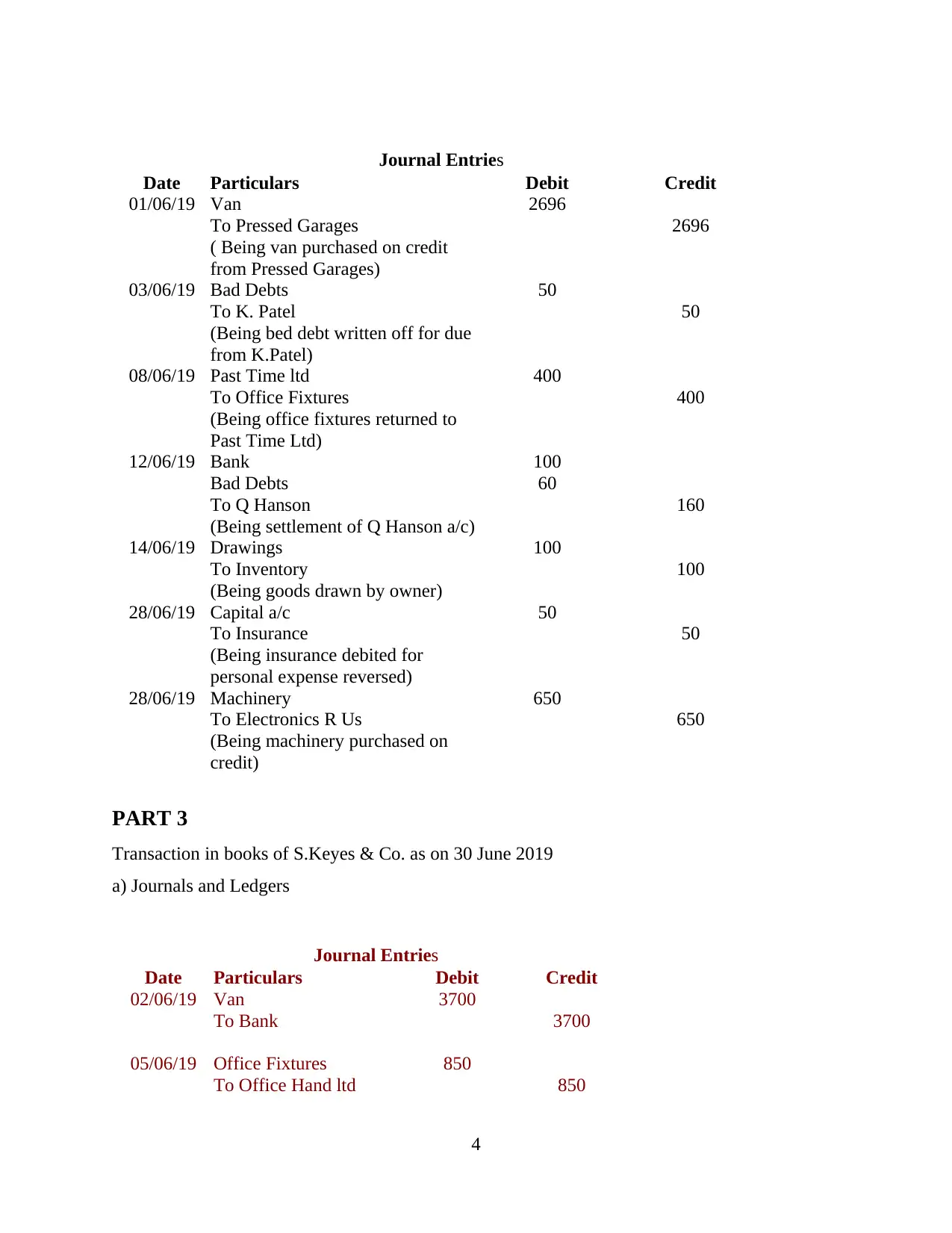

PART 2

Journal Entries for recording the transactions in books of S. Keyes & Co.

3

proprietor, partners and shareholders of companies. Accounting information provides all the

essential information to its owners related to business. Main requirement of having accounting

information of organisation is of keeping track over the financial performance of businesses,

changes in financial position and economic conditions of organisation. These information

facilitates assessment of manager's performance of organisation for evaluating their effectiveness

and efficiency. Information helps owners in determining the performance whether business are

growing and maximising profits.

Customers

They are the people who purchase goods and services of businesses and also known as

economic drivers of organisations. Customers rely on organisation for their products and services

for resale or for their self consumption, they use accounting information for evaluating the

capability of organisations that they will continue their supplies and meet their future needs.

Information is derived from financial statements of company that indicates profit or loss and

financial position of organisations

Suppliers

These parties provide organisations with products and services that are essential for

sustenance and business of organisations. Supplies range over raw materials used in

manufacturing, outsourced services & transportation services (Schroeder, Clark and Cathey,

2019). Suppliers of businesses are compensated in cash or credit basis. Their need is of

determining the capability of firm to meet the obligations related to payment of supplies.

Lenders

Providers of alternate sources of capital to organisation. Lenders provide business with

debts and receive interest in return. Lenders include banks, financial institutions and debenture

holders. They require this information for knowing the economic performance & financial

standing of organisations for assessing the profitability of entities and their capacity of paying

interest on the borrowed amounts. They should have enough resources for paying principal as

well interest on loan.

PART 2

Journal Entries for recording the transactions in books of S. Keyes & Co.

3

Journal Entries

Date Particulars Debit Credit

01/06/19 Van 2696

To Pressed Garages 2696

( Being van purchased on credit

from Pressed Garages)

03/06/19 Bad Debts 50

To K. Patel 50

(Being bed debt written off for due

from K.Patel)

08/06/19 Past Time ltd 400

To Office Fixtures 400

(Being office fixtures returned to

Past Time Ltd)

12/06/19 Bank 100

Bad Debts 60

To Q Hanson 160

(Being settlement of Q Hanson a/c)

14/06/19 Drawings 100

To Inventory 100

(Being goods drawn by owner)

28/06/19 Capital a/c 50

To Insurance 50

(Being insurance debited for

personal expense reversed)

28/06/19 Machinery 650

To Electronics R Us 650

(Being machinery purchased on

credit)

PART 3

Transaction in books of S.Keyes & Co. as on 30 June 2019

a) Journals and Ledgers

Journal Entries

Date Particulars Debit Credit

02/06/19 Van 3700

To Bank 3700

05/06/19 Office Fixtures 850

To Office Hand ltd 850

4

Date Particulars Debit Credit

01/06/19 Van 2696

To Pressed Garages 2696

( Being van purchased on credit

from Pressed Garages)

03/06/19 Bad Debts 50

To K. Patel 50

(Being bed debt written off for due

from K.Patel)

08/06/19 Past Time ltd 400

To Office Fixtures 400

(Being office fixtures returned to

Past Time Ltd)

12/06/19 Bank 100

Bad Debts 60

To Q Hanson 160

(Being settlement of Q Hanson a/c)

14/06/19 Drawings 100

To Inventory 100

(Being goods drawn by owner)

28/06/19 Capital a/c 50

To Insurance 50

(Being insurance debited for

personal expense reversed)

28/06/19 Machinery 650

To Electronics R Us 650

(Being machinery purchased on

credit)

PART 3

Transaction in books of S.Keyes & Co. as on 30 June 2019

a) Journals and Ledgers

Journal Entries

Date Particulars Debit Credit

02/06/19 Van 3700

To Bank 3700

05/06/19 Office Fixtures 850

To Office Hand ltd 850

4

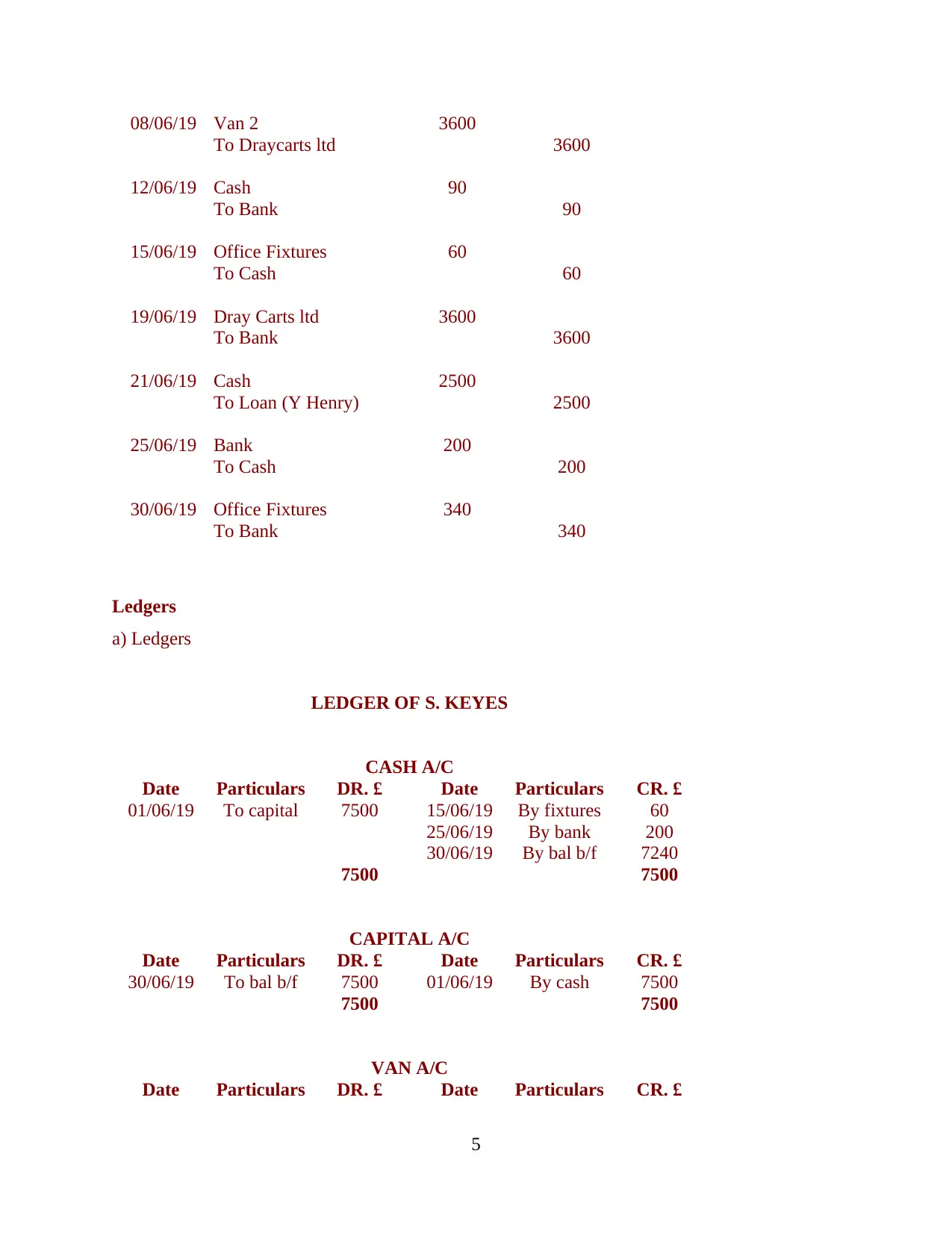

08/06/19 Van 2 3600

To Draycarts ltd 3600

12/06/19 Cash 90

To Bank 90

15/06/19 Office Fixtures 60

To Cash 60

19/06/19 Dray Carts ltd 3600

To Bank 3600

21/06/19 Cash 2500

To Loan (Y Henry) 2500

25/06/19 Bank 200

To Cash 200

30/06/19 Office Fixtures 340

To Bank 340

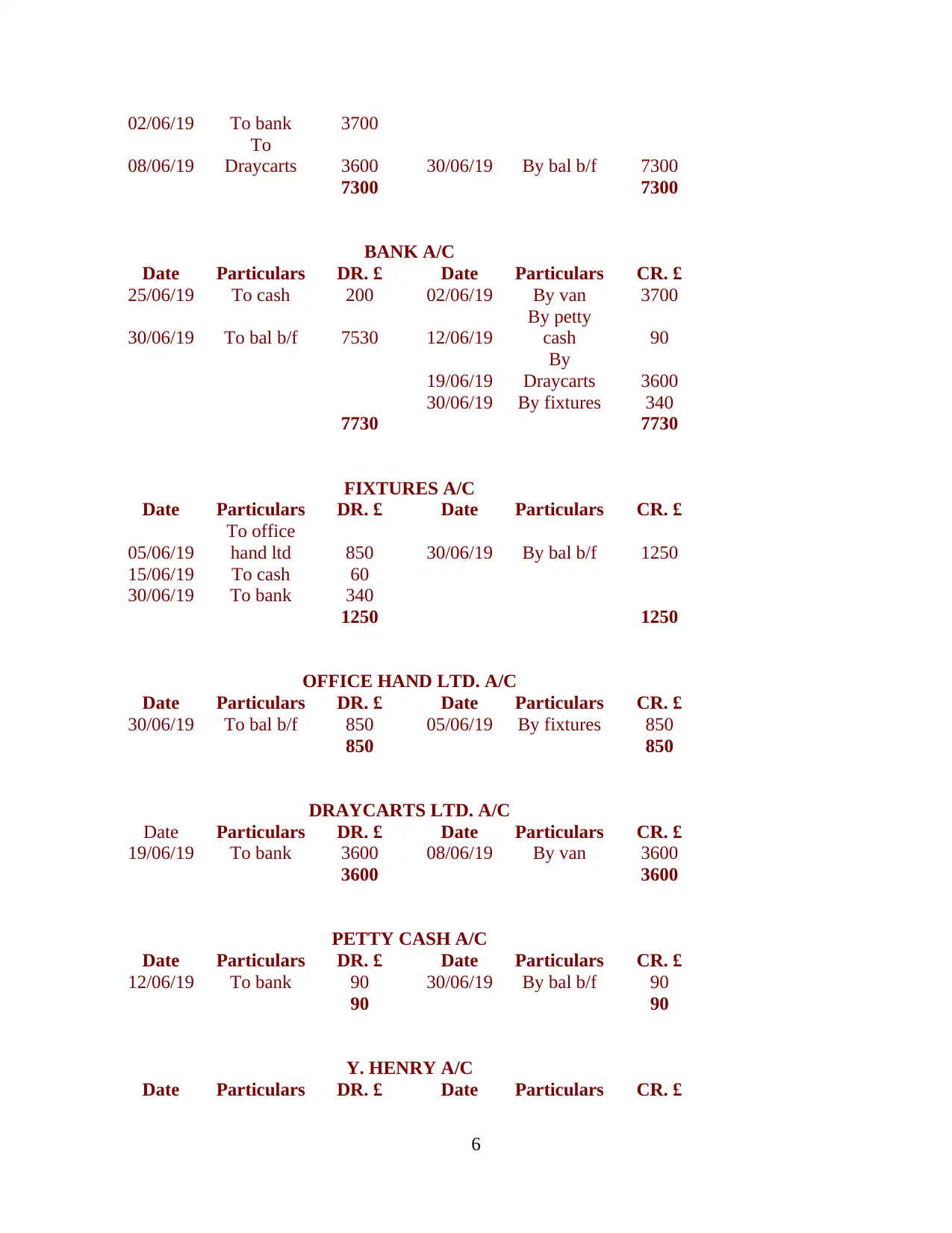

Ledgers

a) Ledgers

LEDGER OF S. KEYES

CASH A/C

Date Particulars DR. £ Date Particulars CR. £

01/06/19 To capital 7500 15/06/19 By fixtures 60

25/06/19 By bank 200

30/06/19 By bal b/f 7240

7500 7500

CAPITAL A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 7500 01/06/19 By cash 7500

7500 7500

VAN A/C

Date Particulars DR. £ Date Particulars CR. £

5

To Draycarts ltd 3600

12/06/19 Cash 90

To Bank 90

15/06/19 Office Fixtures 60

To Cash 60

19/06/19 Dray Carts ltd 3600

To Bank 3600

21/06/19 Cash 2500

To Loan (Y Henry) 2500

25/06/19 Bank 200

To Cash 200

30/06/19 Office Fixtures 340

To Bank 340

Ledgers

a) Ledgers

LEDGER OF S. KEYES

CASH A/C

Date Particulars DR. £ Date Particulars CR. £

01/06/19 To capital 7500 15/06/19 By fixtures 60

25/06/19 By bank 200

30/06/19 By bal b/f 7240

7500 7500

CAPITAL A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 7500 01/06/19 By cash 7500

7500 7500

VAN A/C

Date Particulars DR. £ Date Particulars CR. £

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

02/06/19 To bank 3700

08/06/19

To

Draycarts 3600 30/06/19 By bal b/f 7300

7300 7300

BANK A/C

Date Particulars DR. £ Date Particulars CR. £

25/06/19 To cash 200 02/06/19 By van 3700

30/06/19 To bal b/f 7530 12/06/19

By petty

cash 90

19/06/19

By

Draycarts 3600

30/06/19 By fixtures 340

7730 7730

FIXTURES A/C

Date Particulars DR. £ Date Particulars CR. £

05/06/19

To office

hand ltd 850 30/06/19 By bal b/f 1250

15/06/19 To cash 60

30/06/19 To bank 340

1250 1250

OFFICE HAND LTD. A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 850 05/06/19 By fixtures 850

850 850

DRAYCARTS LTD. A/C

Date Particulars DR. £ Date Particulars CR. £

19/06/19 To bank 3600 08/06/19 By van 3600

3600 3600

PETTY CASH A/C

Date Particulars DR. £ Date Particulars CR. £

12/06/19 To bank 90 30/06/19 By bal b/f 90

90 90

Y. HENRY A/C

Date Particulars DR. £ Date Particulars CR. £

6

08/06/19

To

Draycarts 3600 30/06/19 By bal b/f 7300

7300 7300

BANK A/C

Date Particulars DR. £ Date Particulars CR. £

25/06/19 To cash 200 02/06/19 By van 3700

30/06/19 To bal b/f 7530 12/06/19

By petty

cash 90

19/06/19

By

Draycarts 3600

30/06/19 By fixtures 340

7730 7730

FIXTURES A/C

Date Particulars DR. £ Date Particulars CR. £

05/06/19

To office

hand ltd 850 30/06/19 By bal b/f 1250

15/06/19 To cash 60

30/06/19 To bank 340

1250 1250

OFFICE HAND LTD. A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 850 05/06/19 By fixtures 850

850 850

DRAYCARTS LTD. A/C

Date Particulars DR. £ Date Particulars CR. £

19/06/19 To bank 3600 08/06/19 By van 3600

3600 3600

PETTY CASH A/C

Date Particulars DR. £ Date Particulars CR. £

12/06/19 To bank 90 30/06/19 By bal b/f 90

90 90

Y. HENRY A/C

Date Particulars DR. £ Date Particulars CR. £

6

21/06/19 To loan 2500 30/06/19 By bal b/f 2500

2500 2500

LOAN A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 2500 21/06/19

By Y.

Henry 2500

2500 2500

b) Trial Balance

TRIAL BALANCE AS AT 30 JUNE 2019

PARTICULARS DR. £ CR. £

Capital 7500

Cash 7240

Van 7300

Bank 7530

Fixtures 1250

Office Hand ltd 850

Petty cash 90

Y. Henry 2500

Loan 2500

TOTAL 18380 18380

PART 4

a) Income Statement of S Keyes for year ending 30th September 2019.

Income statement as at 31 September

Revenues

Sales 400000

less returns 2000 398000

Total Revenues 398000

Expenses

Cost of goods sold 245400

Carriage inwards 810

Motor expenses 1500

Carriage outward 2400

Rent 4000

Telephone charges 540

Wages and salaries 21000

Insurance 750

7

2500 2500

LOAN A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 2500 21/06/19

By Y.

Henry 2500

2500 2500

b) Trial Balance

TRIAL BALANCE AS AT 30 JUNE 2019

PARTICULARS DR. £ CR. £

Capital 7500

Cash 7240

Van 7300

Bank 7530

Fixtures 1250

Office Hand ltd 850

Petty cash 90

Y. Henry 2500

Loan 2500

TOTAL 18380 18380

PART 4

a) Income Statement of S Keyes for year ending 30th September 2019.

Income statement as at 31 September

Revenues

Sales 400000

less returns 2000 398000

Total Revenues 398000

Expenses

Cost of goods sold 245400

Carriage inwards 810

Motor expenses 1500

Carriage outward 2400

Rent 4000

Telephone charges 540

Wages and salaries 21000

Insurance 750

7

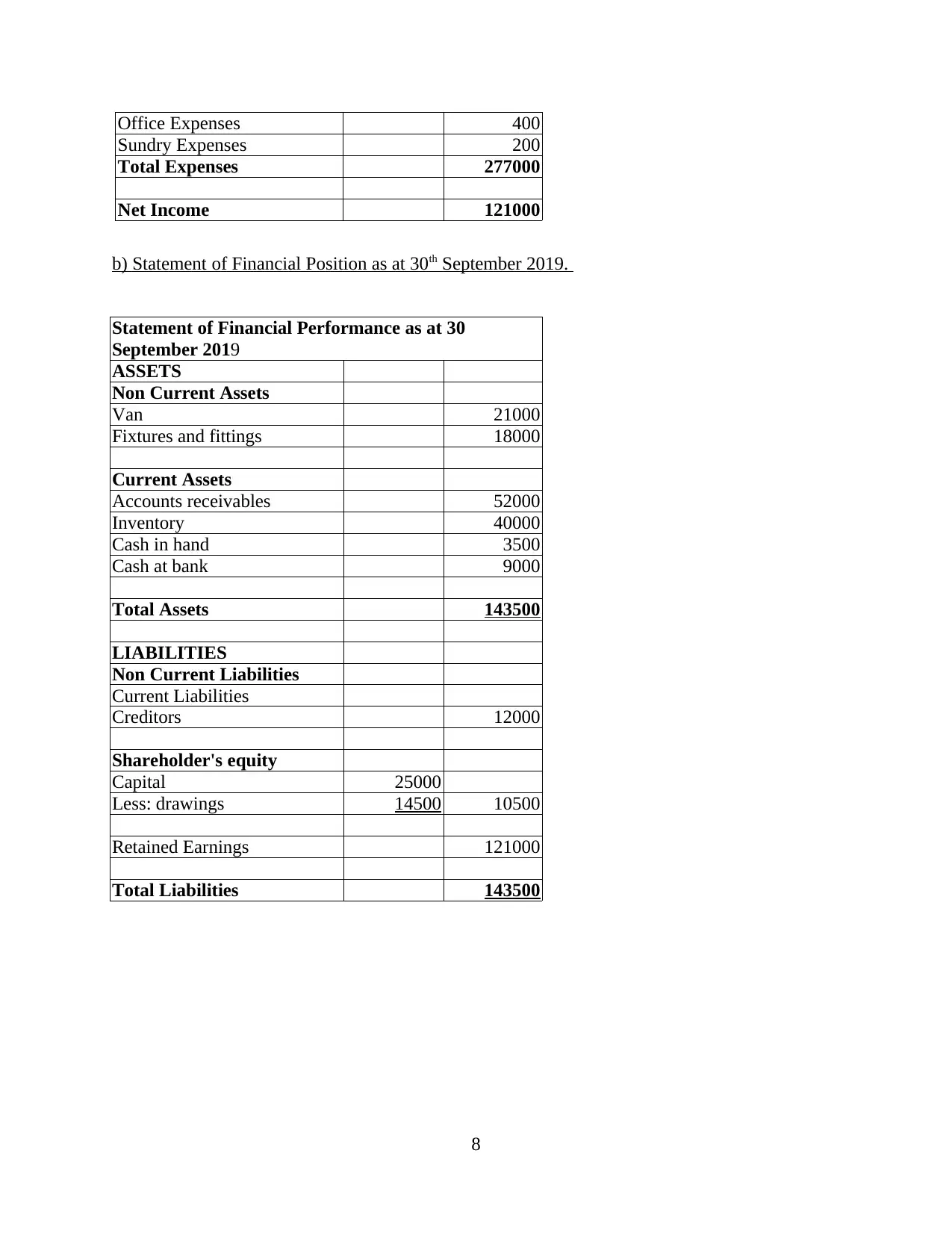

Office Expenses 400

Sundry Expenses 200

Total Expenses 277000

Net Income 121000

b) Statement of Financial Position as at 30th September 2019.

Statement of Financial Performance as at 30

September 2019

ASSETS

Non Current Assets

Van 21000

Fixtures and fittings 18000

Current Assets

Accounts receivables 52000

Inventory 40000

Cash in hand 3500

Cash at bank 9000

Total Assets 143500

LIABILITIES

Non Current Liabilities

Current Liabilities

Creditors 12000

Shareholder's equity

Capital 25000

Less: drawings 14500 10500

Retained Earnings 121000

Total Liabilities 143500

8

Sundry Expenses 200

Total Expenses 277000

Net Income 121000

b) Statement of Financial Position as at 30th September 2019.

Statement of Financial Performance as at 30

September 2019

ASSETS

Non Current Assets

Van 21000

Fixtures and fittings 18000

Current Assets

Accounts receivables 52000

Inventory 40000

Cash in hand 3500

Cash at bank 9000

Total Assets 143500

LIABILITIES

Non Current Liabilities

Current Liabilities

Creditors 12000

Shareholder's equity

Capital 25000

Less: drawings 14500 10500

Retained Earnings 121000

Total Liabilities 143500

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Petty, R.D. and Mandel, R.P., 2015. Business Entities. Wiley Encyclopedia of Management.

pp.1-8.

Spence, S. and Hyams-Ssekasi, D., 2015. Developing business students’ employability skills

through working in partnership with a local business to deliver an undergraduate

mentoring programme. Higher Education, Skills and Work-Based Learning. 5(3). pp.299-

314.

Steingard, D. and Gilbert, J.C., 2016. The Benefit Corporation: A Legal Tool to Align the

Interests of Business with Those of Society; An Interview with Jay Coen Gilbert, Co-

Founder, B Lab. Business and Professional Ethics Journal. 35(1). pp.5-15.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

9

Books and Journals

Petty, R.D. and Mandel, R.P., 2015. Business Entities. Wiley Encyclopedia of Management.

pp.1-8.

Spence, S. and Hyams-Ssekasi, D., 2015. Developing business students’ employability skills

through working in partnership with a local business to deliver an undergraduate

mentoring programme. Higher Education, Skills and Work-Based Learning. 5(3). pp.299-

314.

Steingard, D. and Gilbert, J.C., 2016. The Benefit Corporation: A Legal Tool to Align the

Interests of Business with Those of Society; An Interview with Jay Coen Gilbert, Co-

Founder, B Lab. Business and Professional Ethics Journal. 35(1). pp.5-15.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.