Project Report: Funding Strategies and Financial Analysis of BAT

VerifiedAdded on 2023/01/10

|12

|3222

|83

Project

AI Summary

This project report analyzes the financial information of British American Tobacco (BAT), a FTSE-listed company. It delves into BAT's funding sources, including retained earnings, additional paid-up capital, accumulated other comprehensive income, and common stock. The report provides a detailed calculation of the weighted average cost of capital (WACC) for BAT, considering the cost of debt and equity. It explores various funding sources, such as angel investors, venture capital, bank financing, and retained earnings, outlining their respective pros and cons. The project also examines the role of risk, tax, and gearing in influencing funding choices. Overall, the report offers a comprehensive financial analysis of BAT's funding strategies and their implications.

PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Explanation of long term funding of chosen company............................................................................3

Calculation of weighted average cost of capital.......................................................................................4

Different funding sources with their pros and cons.................................................................................6

Role of risk, tax and gearing for funding choice....................................................................................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................12

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Explanation of long term funding of chosen company............................................................................3

Calculation of weighted average cost of capital.......................................................................................4

Different funding sources with their pros and cons.................................................................................6

Role of risk, tax and gearing for funding choice....................................................................................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................12

INTRODUCTION

The project report is based on analysis of financial information of a FTSE listed company

which is British American Tobacco. This company is involved in production of various kinds of

tobacco products and sales all around the United Kingdom. The project report covers detailed

information about calculation of weighted average cost of capital, different sources of funds and

role of tax, risk in choosing funding alternatives.

MAIN BODY

Explanation of long term funding of chosen company.

On the basis of given financial statement of above British American tobacco plc, this can

be assessed that they are based on various kinds of sources for funding that are mentioned below

in such manner:

Retained earnings- The retained profits of the company are the total net profit of the

business that is held by the company at a given date, such as at the close of the tax period.

At the completion of the time, the net gain (or net loss) at that stage shall be shifted from

the benefit and expense account to the remaining earnings report. When the value of the

remaining earnings report is negative, cumulative gains, residual losses or accrued

deficits or related terms can be used. In the aspect of above company, it can be find out

that their retained earnings are increasing effectively. Such as in year 2018, it was of

GBP 38557 that raised and became of GBP 40234.

Additional paid up capital- Additional paid-up capital (APUC) is the valuation of the

ordinary shares above its stated fair market value and is a financial reporting item on the

balance sheet under the stockholders ’ equity (Visser, 2019). APIC can be formed if a

firm reports new shares and can be decreased if the business organization focuses its

shareholdings. In the context of above company, it can be find out that their value of

additional paid up capital was of GBP 192 that raised and became of GBP 195 for year

The project report is based on analysis of financial information of a FTSE listed company

which is British American Tobacco. This company is involved in production of various kinds of

tobacco products and sales all around the United Kingdom. The project report covers detailed

information about calculation of weighted average cost of capital, different sources of funds and

role of tax, risk in choosing funding alternatives.

MAIN BODY

Explanation of long term funding of chosen company.

On the basis of given financial statement of above British American tobacco plc, this can

be assessed that they are based on various kinds of sources for funding that are mentioned below

in such manner:

Retained earnings- The retained profits of the company are the total net profit of the

business that is held by the company at a given date, such as at the close of the tax period.

At the completion of the time, the net gain (or net loss) at that stage shall be shifted from

the benefit and expense account to the remaining earnings report. When the value of the

remaining earnings report is negative, cumulative gains, residual losses or accrued

deficits or related terms can be used. In the aspect of above company, it can be find out

that their retained earnings are increasing effectively. Such as in year 2018, it was of

GBP 38557 that raised and became of GBP 40234.

Additional paid up capital- Additional paid-up capital (APUC) is the valuation of the

ordinary shares above its stated fair market value and is a financial reporting item on the

balance sheet under the stockholders ’ equity (Visser, 2019). APIC can be formed if a

firm reports new shares and can be decreased if the business organization focuses its

shareholdings. In the context of above company, it can be find out that their value of

additional paid up capital was of GBP 192 that raised and became of GBP 195 for year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018 and 2019 respectively. It is indicating that their owners are investing funds in

company.

Accumulated other comprehensive income- Other accumulated Detailed Revenue (OCI)

includes unfulfilled profits and losses listed in the balance sheet equity segment that are

offset elsewhere here-retained earnings. Other thorough revenue may consist of losses

and gains on certain forms of investors, public pensions, and deposit trying to hedge. In

the context of above company, this can be assessed that their accumulated other

comprehensive income was of GBP 26081 which reduced and became of GBP 22859 for

year 2018 and 2019 respectively.

Common stock- Common stock is a kind of control of corporate equities, a kind of

security. Often commonly used in other regions of the world are the words participating

share and normal share; "common shares" is mainly used in the USA. In the UK as well

as other overlay network they are classified as share capital or common stock. In regards

with British American Tobacco plc, it can be find out the value of common stock for year

2018 and 2019 was similar that was of GBP 614.

Calculation of weighted average cost of capital.

Weighted average cost of capital- The weighted average cost of capital is the rate a

business is required to pay to all its current shareholders on ordinary in capital to afford its

resources (Booth, Cleary, and Rakita, 2020). The WACC is typically referred to as the value of

capital for the company. Crucially, the external demand decides this and not the administration.

The WACC formula is as follows:

WACC = [(E/V) * Re] + [(D/V) * Rd * (1-Tc)]

Re = cost of equity (expected rate of return on equity)

Rd = cost of debt (expected rate of return on debt)

E = market value of company equity

D = market value of company debt

V = total capital invested, which equals E + D

company.

Accumulated other comprehensive income- Other accumulated Detailed Revenue (OCI)

includes unfulfilled profits and losses listed in the balance sheet equity segment that are

offset elsewhere here-retained earnings. Other thorough revenue may consist of losses

and gains on certain forms of investors, public pensions, and deposit trying to hedge. In

the context of above company, this can be assessed that their accumulated other

comprehensive income was of GBP 26081 which reduced and became of GBP 22859 for

year 2018 and 2019 respectively.

Common stock- Common stock is a kind of control of corporate equities, a kind of

security. Often commonly used in other regions of the world are the words participating

share and normal share; "common shares" is mainly used in the USA. In the UK as well

as other overlay network they are classified as share capital or common stock. In regards

with British American Tobacco plc, it can be find out the value of common stock for year

2018 and 2019 was similar that was of GBP 614.

Calculation of weighted average cost of capital.

Weighted average cost of capital- The weighted average cost of capital is the rate a

business is required to pay to all its current shareholders on ordinary in capital to afford its

resources (Booth, Cleary, and Rakita, 2020). The WACC is typically referred to as the value of

capital for the company. Crucially, the external demand decides this and not the administration.

The WACC formula is as follows:

WACC = [(E/V) * Re] + [(D/V) * Rd * (1-Tc)]

Re = cost of equity (expected rate of return on equity)

Rd = cost of debt (expected rate of return on debt)

E = market value of company equity

D = market value of company debt

V = total capital invested, which equals E + D

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

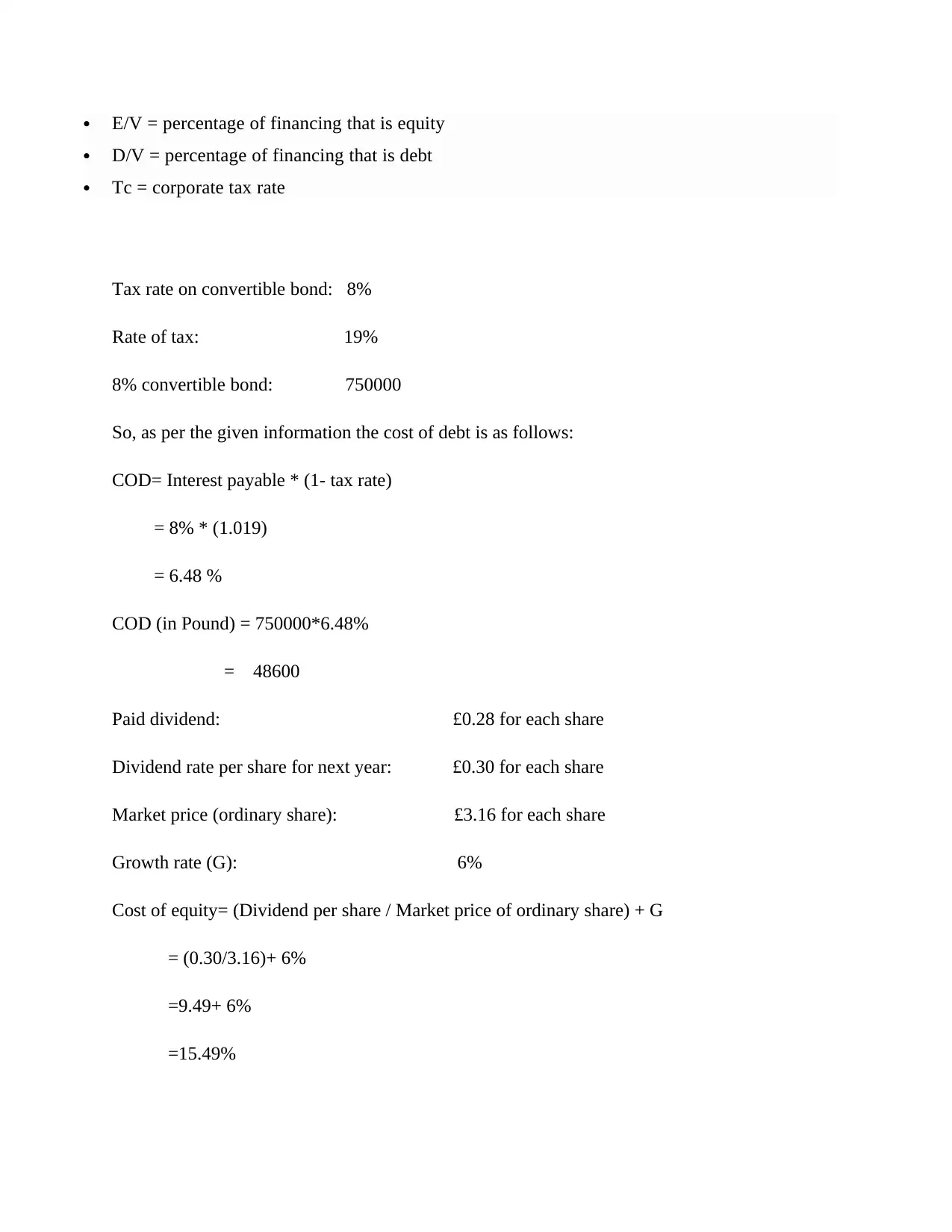

E/V = percentage of financing that is equity

D/V = percentage of financing that is debt

Tc = corporate tax rate

Tax rate on convertible bond: 8%

Rate of tax: 19%

8% convertible bond: 750000

So, as per the given information the cost of debt is as follows:

COD= Interest payable * (1- tax rate)

= 8% * (1.019)

= 6.48 %

COD (in Pound) = 750000*6.48%

= 48600

Paid dividend: £0.28 for each share

Dividend rate per share for next year: £0.30 for each share

Market price (ordinary share): £3.16 for each share

Growth rate (G): 6%

Cost of equity= (Dividend per share / Market price of ordinary share) + G

= (0.30/3.16)+ 6%

=9.49+ 6%

=15.49%

D/V = percentage of financing that is debt

Tc = corporate tax rate

Tax rate on convertible bond: 8%

Rate of tax: 19%

8% convertible bond: 750000

So, as per the given information the cost of debt is as follows:

COD= Interest payable * (1- tax rate)

= 8% * (1.019)

= 6.48 %

COD (in Pound) = 750000*6.48%

= 48600

Paid dividend: £0.28 for each share

Dividend rate per share for next year: £0.30 for each share

Market price (ordinary share): £3.16 for each share

Growth rate (G): 6%

Cost of equity= (Dividend per share / Market price of ordinary share) + G

= (0.30/3.16)+ 6%

=9.49+ 6%

=15.49%

Different funding sources with their pros and cons.

Funding is the act of supplying money to fund a mission, desire or plan. Although this is

normally in the form of cash, an organization can also take the form of endeavor or time. This

term is usually used when a company uses its internal reserves to fulfill its cash needs, whereas

the using above is used with the firm buys capital from investors. There are a range of methods

of funding and some of them are mentioned in such manner:

Angel investors- Angel investors are affluent individuals who would give funding to an investor

in return for a portion of the company’s equity (Cesa-Bianchi and Saleheen, 2019). Sizes of

investment spectrum but are generally less than $1 million. Angels also operate in structured

communities reviewing offers and investing alongside each other, while others invest by

themselves. Venture capitalists are more aggressive than the sort of shareholder they will

Funding is the act of supplying money to fund a mission, desire or plan. Although this is

normally in the form of cash, an organization can also take the form of endeavor or time. This

term is usually used when a company uses its internal reserves to fulfill its cash needs, whereas

the using above is used with the firm buys capital from investors. There are a range of methods

of funding and some of them are mentioned in such manner:

Angel investors- Angel investors are affluent individuals who would give funding to an investor

in return for a portion of the company’s equity (Cesa-Bianchi and Saleheen, 2019). Sizes of

investment spectrum but are generally less than $1 million. Angels also operate in structured

communities reviewing offers and investing alongside each other, while others invest by

themselves. Venture capitalists are more aggressive than the sort of shareholder they will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

encounter in a friends / community Ring, but are typically less intense than a Private equity

Company. In the context of above British American Tobacco plc this source of fund can be used

in order to fulfill need of funds. This has below mentioned pros and cons that are as follows:

Pros-

Angels usually have business expertise, and will provide invaluable advice and access to

their system.

Flexible partnership arrangements are popular as angels are less restrictive than VC

Firms.

Cons-

Not ideal for around £ 5,000 investment or greater than £150,000 investment

Take much longer to find an appropriate angel investor

Abandoning a share of the company

Less systemic aid accessible from either a BA than in an investment firm

Venture capital funding- Most businesspeople claim VC Funding is the secret to their growth.

Venture capitalists are creditors who are able to bring in a substantial amount of money in return

for the preferred equity, but they only get their cash back if another business either acquires it or

takes action (Bals, 2019). VCs are institutional traders with a whole lot of money. Usually

they’re looking for investment funds that can deliver a 6X return on that investment, so

companies’ better prepared to go big. Such as in the aspect of above company, they can use

these sources of finance in order to fulfill need of funds.

Pros-

If the startup fails or closes down, there is no needed to give the venture capitalist

shareholders. For start-ups, thus, venture capital funding is crucial. This will not put the

responsibility on the start-up on start repaying as is the situation for loans.

Company. In the context of above British American Tobacco plc this source of fund can be used

in order to fulfill need of funds. This has below mentioned pros and cons that are as follows:

Pros-

Angels usually have business expertise, and will provide invaluable advice and access to

their system.

Flexible partnership arrangements are popular as angels are less restrictive than VC

Firms.

Cons-

Not ideal for around £ 5,000 investment or greater than £150,000 investment

Take much longer to find an appropriate angel investor

Abandoning a share of the company

Less systemic aid accessible from either a BA than in an investment firm

Venture capital funding- Most businesspeople claim VC Funding is the secret to their growth.

Venture capitalists are creditors who are able to bring in a substantial amount of money in return

for the preferred equity, but they only get their cash back if another business either acquires it or

takes action (Bals, 2019). VCs are institutional traders with a whole lot of money. Usually

they’re looking for investment funds that can deliver a 6X return on that investment, so

companies’ better prepared to go big. Such as in the aspect of above company, they can use

these sources of finance in order to fulfill need of funds.

Pros-

If the startup fails or closes down, there is no needed to give the venture capitalist

shareholders. For start-ups, thus, venture capital funding is crucial. This will not put the

responsibility on the start-up on start repaying as is the situation for loans.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finding and locating VC within minutes, shareholders, is very easy since they are

recorded in various directories. This decreases the energy, commitment and cost invested

in seeking financing for the company.

Cons-

Venture capitalist supplies the start-ups with massive funding in exchange for a share in

the firm's equity. If the company works, it can help them gain massive sums of income.

Typically VC is a member of the commission. They are actively involved in decision-

making at the business. VC's will want their investment decisions protected. When there

is a conflict in view between the VC and the creator of the company, so things will get

messy. Any large judgment needs investor approval.

Paying for venture capital entails a huge deal of risk. So, it generally takes a long time for

VC's to make a decision if they really want to spend or not. Venture funding may be a

tremendous source of financing open to start-ups. Yet a huge downside is the lengthy

delay prior to actually having received the funds.

Bank financing- Bank loans are the most searched after funding vehicle and can be accessed at

the closest loan company (Cornée, 2019). Bank lending can be difficult considering that there are

several various forms of funding choices and interest levels to go along with. Before starting it is

essential to educate oneself on the procedure and the alternatives. Such as above British

American Tobacco plc can get financial assistance by help of banks. This source of fund has

below mentioned advantages and disadvantages such as:

Pros-

Companies should just think about getting the daily mortgage payments on time for bank

loans. This is an additional benefit over overdraft charges, where companies have to pay

the remaining price when the bank requests that. However, banks typically don't track

whether the spend the loan so long as make the payments on time, and they can use in

however company find fit.

recorded in various directories. This decreases the energy, commitment and cost invested

in seeking financing for the company.

Cons-

Venture capitalist supplies the start-ups with massive funding in exchange for a share in

the firm's equity. If the company works, it can help them gain massive sums of income.

Typically VC is a member of the commission. They are actively involved in decision-

making at the business. VC's will want their investment decisions protected. When there

is a conflict in view between the VC and the creator of the company, so things will get

messy. Any large judgment needs investor approval.

Paying for venture capital entails a huge deal of risk. So, it generally takes a long time for

VC's to make a decision if they really want to spend or not. Venture funding may be a

tremendous source of financing open to start-ups. Yet a huge downside is the lengthy

delay prior to actually having received the funds.

Bank financing- Bank loans are the most searched after funding vehicle and can be accessed at

the closest loan company (Cornée, 2019). Bank lending can be difficult considering that there are

several various forms of funding choices and interest levels to go along with. Before starting it is

essential to educate oneself on the procedure and the alternatives. Such as above British

American Tobacco plc can get financial assistance by help of banks. This source of fund has

below mentioned advantages and disadvantages such as:

Pros-

Companies should just think about getting the daily mortgage payments on time for bank

loans. This is an additional benefit over overdraft charges, where companies have to pay

the remaining price when the bank requests that. However, banks typically don't track

whether the spend the loan so long as make the payments on time, and they can use in

however company find fit.

Although firms that issue bonds to collect money frequently offer creditors a portion of

their earnings, banks allow lenders to pay just the amount of principal and interest on a

loan (Zhang, Aerts and Pan, 2019).

Cons-

Loan lenders have to make deposits to their banks annually. Those that fall well behind

payouts face the possibility of their investments being seized. Even if the company

manages to make missed fees, the bank can still document to the credit reporting agencies

– a move that has an adverse effect on the credit score of firms. With a lower rating, it

gets harder to obtain loans. The debt pressure is a drawback relative to investors

increasing capital as creditors do not need daily repayments. They are usually only paid

off handsomely on earnings, instead.

Since many loans necessitate some method of leverage, entrepreneurs and individual

firms can find it very difficult to get ones mortgage applications authorized with no

assets. If these lenders decide for personal debt, they would be struck by rising interest

rates.

Retained earnings- With the basic explanation that they are the end result of operating a firm,

remaining profits/earnings are considered the inner source of financing with a corporation. Also

known as the 'plow Back of Profits' concept (Pakdel and Ashrafi, 2019). Retained profits can be

treated as income left after the stockholders have paid a rate of return or the investment-owners

drawings. This source of funding is being used by above company which has below mentioned

advantages and disadvantages:

Pros-

First, they are lengthy-term finance, and no one can ask for payouts from them.

Secondly, because there is no new stock to be given, leverage and participation of the

company is not diminished.

Thirdly, there really are no fixed interest or incarnation payment obligations.

their earnings, banks allow lenders to pay just the amount of principal and interest on a

loan (Zhang, Aerts and Pan, 2019).

Cons-

Loan lenders have to make deposits to their banks annually. Those that fall well behind

payouts face the possibility of their investments being seized. Even if the company

manages to make missed fees, the bank can still document to the credit reporting agencies

– a move that has an adverse effect on the credit score of firms. With a lower rating, it

gets harder to obtain loans. The debt pressure is a drawback relative to investors

increasing capital as creditors do not need daily repayments. They are usually only paid

off handsomely on earnings, instead.

Since many loans necessitate some method of leverage, entrepreneurs and individual

firms can find it very difficult to get ones mortgage applications authorized with no

assets. If these lenders decide for personal debt, they would be struck by rising interest

rates.

Retained earnings- With the basic explanation that they are the end result of operating a firm,

remaining profits/earnings are considered the inner source of financing with a corporation. Also

known as the 'plow Back of Profits' concept (Pakdel and Ashrafi, 2019). Retained profits can be

treated as income left after the stockholders have paid a rate of return or the investment-owners

drawings. This source of funding is being used by above company which has below mentioned

advantages and disadvantages:

Pros-

First, they are lengthy-term finance, and no one can ask for payouts from them.

Secondly, because there is no new stock to be given, leverage and participation of the

company is not diminished.

Thirdly, there really are no fixed interest or incarnation payment obligations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fourthly, retained earnings as an internal stream of funding are cost-effective in spite of

the fact that no problem expenses are correlated with them varying from 2 to 3 per cent.

Cons-

There is almost no downside of producing or using remaining profits to fund the business'

expenditures. Considering that the funds internally developed are not free because the funds

belonging to the owners are, and the expense of such funds is equivalent to the equity level

(Gilli, Maringer and Schumann, 2019). There will be only one option that can be discussed, i.e.

forms of debt funding. The intent of researching the alternative relates to different-point

thinking.

Role of risk, tax and gearing for funding choice.

Risk- Financial risk is one of several categories of financing-related risks, including

financial transactions which include risk of default business loans. It is often assumed that this

concerns only downside risk, which implies the opportunities for capital loss and confusion as to

its degree. A business is exposed to different types of risks (Owen, Deakins and Savic, 2019).

Such uncertainties would be taken into account before determining the source of funding. For

example, if a business depends heavily on debt funding, they are considered to be highly

leveraged because it brings the considerable capital risk. This means, because mortgage

repayments are not done in schedule that will result in court proceedings and there is a possibility

of failure as a consequence. High capital structure also impacts per-share earnings. So a company

must analyze the level of leverage it can accept for choosing on a capital structure. In the aspect

of above British American Tobacco plc, this is essential for them to consider it before choosing

any source of finance for funding.

Tax- This is also an aspect before choosing any source of finance. Companies should choose

only those source of finance on tax rate is lower. It is so because if tax rate will higher then this

can be difficult for companies to repay the loan in an effective manner. Such as in the context of

the fact that no problem expenses are correlated with them varying from 2 to 3 per cent.

Cons-

There is almost no downside of producing or using remaining profits to fund the business'

expenditures. Considering that the funds internally developed are not free because the funds

belonging to the owners are, and the expense of such funds is equivalent to the equity level

(Gilli, Maringer and Schumann, 2019). There will be only one option that can be discussed, i.e.

forms of debt funding. The intent of researching the alternative relates to different-point

thinking.

Role of risk, tax and gearing for funding choice.

Risk- Financial risk is one of several categories of financing-related risks, including

financial transactions which include risk of default business loans. It is often assumed that this

concerns only downside risk, which implies the opportunities for capital loss and confusion as to

its degree. A business is exposed to different types of risks (Owen, Deakins and Savic, 2019).

Such uncertainties would be taken into account before determining the source of funding. For

example, if a business depends heavily on debt funding, they are considered to be highly

leveraged because it brings the considerable capital risk. This means, because mortgage

repayments are not done in schedule that will result in court proceedings and there is a possibility

of failure as a consequence. High capital structure also impacts per-share earnings. So a company

must analyze the level of leverage it can accept for choosing on a capital structure. In the aspect

of above British American Tobacco plc, this is essential for them to consider it before choosing

any source of finance for funding.

Tax- This is also an aspect before choosing any source of finance. Companies should choose

only those source of finance on tax rate is lower. It is so because if tax rate will higher then this

can be difficult for companies to repay the loan in an effective manner. Such as in the context of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

above company, it is necessary for them to select only those source of finance on which rate of

taxation is lower as compared to other source of finance.

Gearing- Gearing describes the relation, or proportion, of the loans to capital of a company.

Leverage ratio shows the depth with which borrowers vs. the stockholders finance the company

profitability — in many other words, it measures the leverage of a firm (Haggard, Maxfield and

Lee, 2019). When the debt-to - equity risk is increased, then a company can be considered highly

geared, or heavily leveraged.

As a small example, British American tobacco plc cannot advertise extra money from investors

at a decent cost in money to finance its growth; but instead, it acquires a short-term loan of

$10,000,000. British American tobacco plc currently holds $2,000,000 of equity; thus the debt-

to-equity (D/E) ratio is 5x—[$10,000,000 (total liabilities) divided by $2,000,000 (shareholders'

equity) is 5x]. British American tobacco plc would certainly be treated as highly geared.

Recommendation-

On the basis of analysis of all factors, it can be suggested to above company that they

should choose only those source of finance which are lower risky and with minimum tax rate.

From analysis of range of financial sources, it can be recommended to above company that they

should choose option of getting fund from banks. It is so because of lower risk and tax rate. If

they will do so then this will be easier for them to repay the loan in less time and with lower cost.

CONCLUSION

On the basis of above project report this can be concluded that companies have range of

funding option and each of them has own importance. By assessing financial statement of above

chosen company, calculation of weighted average capital has been done in the report. The further

part of report concludes about various kinds of funding sources such as angel investors, banks

and many more. As well as different kinds of factors are also mentioned such as tax, risk and

many more. From end part of report this can be concluded that British American Tobacco plc

should choose bank for taking financial assistance.

taxation is lower as compared to other source of finance.

Gearing- Gearing describes the relation, or proportion, of the loans to capital of a company.

Leverage ratio shows the depth with which borrowers vs. the stockholders finance the company

profitability — in many other words, it measures the leverage of a firm (Haggard, Maxfield and

Lee, 2019). When the debt-to - equity risk is increased, then a company can be considered highly

geared, or heavily leveraged.

As a small example, British American tobacco plc cannot advertise extra money from investors

at a decent cost in money to finance its growth; but instead, it acquires a short-term loan of

$10,000,000. British American tobacco plc currently holds $2,000,000 of equity; thus the debt-

to-equity (D/E) ratio is 5x—[$10,000,000 (total liabilities) divided by $2,000,000 (shareholders'

equity) is 5x]. British American tobacco plc would certainly be treated as highly geared.

Recommendation-

On the basis of analysis of all factors, it can be suggested to above company that they

should choose only those source of finance which are lower risky and with minimum tax rate.

From analysis of range of financial sources, it can be recommended to above company that they

should choose option of getting fund from banks. It is so because of lower risk and tax rate. If

they will do so then this will be easier for them to repay the loan in less time and with lower cost.

CONCLUSION

On the basis of above project report this can be concluded that companies have range of

funding option and each of them has own importance. By assessing financial statement of above

chosen company, calculation of weighted average capital has been done in the report. The further

part of report concludes about various kinds of funding sources such as angel investors, banks

and many more. As well as different kinds of factors are also mentioned such as tax, risk and

many more. From end part of report this can be concluded that British American Tobacco plc

should choose bank for taking financial assistance.

REFERENCES

Books and journal:

Visser, H., 2019. Islamic finance: Principles and practice. Edward Elgar Publishing.

Booth, L., Cleary, W.S. and Rakita, I., 2020. Introduction to corporate finance. John Wiley &

Sons.

Cesa-Bianchi, A., Imbs, J. and Saleheen, J., 2019. Finance and synchronization. Journal of

International Economics, 116, pp.74-87.

Cornée, S., 2019. The relevance of soft information for predicting small business credit default:

Evidence from a social bank. Journal of Small Business Management, 57(3), pp.699-719.

Pakdel, M. and Ashrafi, M., 2019. Relationship between Working Capital Management and the

Performance of Firm in Different Business Cycles. Dutch Journal of Finance and

Management, 3(1), p.em0057.

Owen, R., Deakins, D. and Savic, M., 2019. Finance pathways for young innovative small‐and

medium‐size enterprises: a demand‐side examination of finance gaps and policy implications for

the post‐global financial crisis finance escalator. Strategic Change, 28(1), pp.19-36.

Haggard, S., Maxfield, S. and Lee, C.H. eds., 2019. The politics of finance in developing

countries. Cornell University Press.

Gilli, M., Maringer, D. and Schumann, E., 2019. Numerical methods and optimization in finance.

Academic Press.

Zhang, S., Aerts, W. and Pan, H., 2019. Causal language intensity in performance commentary

and financial analyst behaviour. Journal of Business Finance & Accounting, 46(1-2), pp.3-31.

Bals, C., 2019. Toward a supply chain finance (SCF) ecosystem–Proposing a framework and

agenda for future research. Journal of purchasing and supply Management, 25(2), pp.105-117.

Books and journal:

Visser, H., 2019. Islamic finance: Principles and practice. Edward Elgar Publishing.

Booth, L., Cleary, W.S. and Rakita, I., 2020. Introduction to corporate finance. John Wiley &

Sons.

Cesa-Bianchi, A., Imbs, J. and Saleheen, J., 2019. Finance and synchronization. Journal of

International Economics, 116, pp.74-87.

Cornée, S., 2019. The relevance of soft information for predicting small business credit default:

Evidence from a social bank. Journal of Small Business Management, 57(3), pp.699-719.

Pakdel, M. and Ashrafi, M., 2019. Relationship between Working Capital Management and the

Performance of Firm in Different Business Cycles. Dutch Journal of Finance and

Management, 3(1), p.em0057.

Owen, R., Deakins, D. and Savic, M., 2019. Finance pathways for young innovative small‐and

medium‐size enterprises: a demand‐side examination of finance gaps and policy implications for

the post‐global financial crisis finance escalator. Strategic Change, 28(1), pp.19-36.

Haggard, S., Maxfield, S. and Lee, C.H. eds., 2019. The politics of finance in developing

countries. Cornell University Press.

Gilli, M., Maringer, D. and Schumann, E., 2019. Numerical methods and optimization in finance.

Academic Press.

Zhang, S., Aerts, W. and Pan, H., 2019. Causal language intensity in performance commentary

and financial analyst behaviour. Journal of Business Finance & Accounting, 46(1-2), pp.3-31.

Bals, C., 2019. Toward a supply chain finance (SCF) ecosystem–Proposing a framework and

agenda for future research. Journal of purchasing and supply Management, 25(2), pp.105-117.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.